Harris&Ewing Woodward & Lothrop dept. store trucks, Washington DC 1912

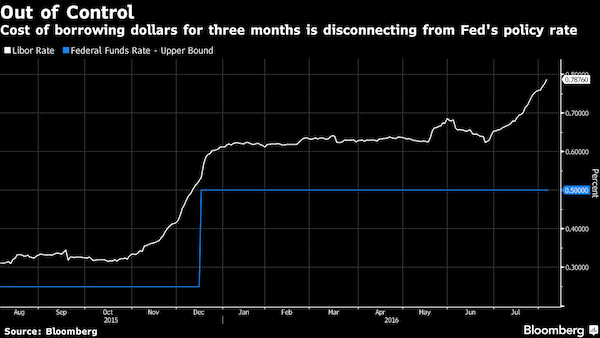

Libor. And by the way: The Fed never had control, just the illusion.

• The Fed Is Losing Control of Global Monetary Conditions (BBG)

Libor is coming unhinged from other borrowing costs and that has real implications for the cost of money in the real world. On this basis, the U.S. has already had an interest-rate increase, according to Bloomberg View’s Mark Gilbert. While there are plenty of market participants who favor the Austrian school of economics and would welcome the removal of central banks from the rate-setting mechanism, the change in money-market conditions is something the Fed should take into account as it ponders its next move.

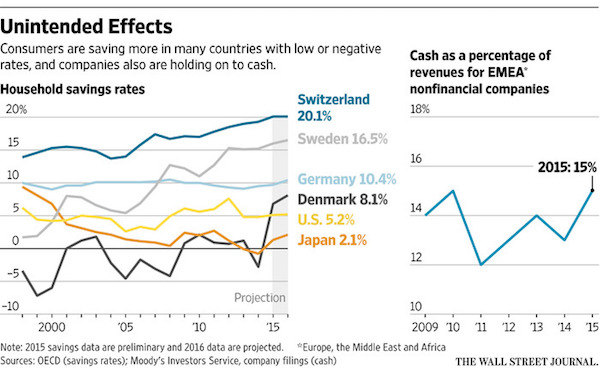

They do what they’re supposed to prevent: encourage saving. Get the central banks out of the economy!

• Are Negative Rates Backfiring? (WSJ)

Recent economic data show consumers are saving more in Germany and Japan, and in Denmark, Switzerland and Sweden, three non-eurozone countries with negative rates, savings are at their highest since 1995, the year the Organization for Economic Cooperation and Development started collecting data on those countries. Companies in Europe, the Middle East, Africa and Japan also are holding on to more cash. Economists point to a variety of other possible factors confounding central-bank policy: Low inflation has left consumers with more money to sock away; aging populations are naturally more inclined to save; central banks themselves may have failed to properly explain their actions.

But there is a growing suspicion that part of problem may be negative rates themselves. Some economists and bankers contend that negative rates communicate fear over the growth outlook and the central bank’s ability to manage it. “People only borrow and spend more when they are confident about the future,” says Andrew Sheets at Morgan Stanley. “But by going negative, into uncharted territory, the policy actually undermines confidence.” Going negative was a big bet by central banks faced with a sluggish recovery from the financial crisis. Whether negative rates succeed or flop has huge implications for the global economy. Japan and Europe are already doing large volumes of bond buying to spur their economies, and their central bankers have little left in their tool kits.

The U.S. Federal Reserve’s next move is likely to raise rates, but Chairwoman Janet Yellen has said negative rates could find a place in the Fed’s armory in any future crisis. The Bank of England, shaken by June’s surprise vote to leave the European Union, cut interest rates to their lowest in its 322-year history last week but said it was reluctant to go negative. BOE Gov. Mark Carney said he is “not a fan” of a policy that has negative consequences for savers and the financial system. European banks say their profitability has been hit hard by low rates. Some central bankers say it is too early to judge negative rates. “The effect won’t be seen all at once, but it will gradually become clear,” said Bank of Japan Gov. Haruhiko Kuroda in a June news conference.

Governments should stay out of housing markets. Their only interest is make banks make money.

• Fannie And Freddie Could Need $126 Billion To Get Through A Crisis (R.)

Fannie Mae and Freddie Mac, two government-controlled housing finance agencies, would need a big cash injection to weather another financial meltdown, a government regulator said on Monday. Fannie and Freddie would need as much as $126 billion in taxpayer funds to come through a serious downturn, according to a ‘stress test’ from the Federal Housing Finance Agency. The companies, which were once owned by shareholders, have drawn $187 billion from the U.S. Treasury since they were seized by the government in September 2008 as the global financial crisis tightened. Since then, as the housing market has strengthened, they have returned roughly $250 billion to the Treasury. Lawmakers have not settled on the future of two companies. The ‘stress test’ required by the Dodd Frank reform legislation of 2010 projected the companies would have to draw at least $49 billion to $126 billion in the case of a serious economic downturn.

People are forced to use Help to Buy: it acts as an insurance policy in case homes lose value. Then the taxpayer pays.

• UK Government Has Gambled Hundreds Of Millions On House Price Rises (TiM)

Taxpayers stand to lose hundreds of millions of pounds if house prices fall, thanks to a gamble the government has been making with our cash for the past three years. Some £3.59billion has been lent to first-time buyers through the Help to Buy loan scheme to help them purchase newly-built properties they may not otherwise have been able to afford, according to the latest government statistics. The scheme was launched by the former Chancellor George Osborne in 2013, in response to a stagnating housing market. It effectively lets borrowers with small deposits top them up with a government loan, worth up to 20% of the value of a new build property.

For the 81,014 buyers who have taken advantage of the scheme so far, it has been an invaluable lifeline, the difference between making that step on to the first hallowed rung of the property ladder and continuing to rent. However, the side effect of the scheme leaves taxpayer funds extremely vulnerable to losses if house prices start to fall. This is because the size of loans is not fixed, but rather is measured as a proportion of the value of the properties bought. Take, for example a first-time buyer who uses the scheme to buy a home costing £300,000. They could borrow up to 20% of the value of the property – £60,000 – using Help to Buy, and put down just a 5% deposit themselves.

However, the size of the loan remains 20% of the value of the property – regardless of how it fluctuates. So if the house increases in value by 10% to £330,000, the value of the loan will increase by 10% as well to £66,000. The taxpayer turns a profit. But if the value of the home declines by 10% to £270,000, the value of the loan will decrease to £54,000. Taxpayers will just have to suck up the £6,000 shortfall. A total of £3.59billion has been lent out so far. If the value of the homes they helped paid for drops by just 10%, the borrowers will be off the hook for as much as £359million – a cost that will be picked up by the taxpayer.

And this is what you get when a government blows a bubble.

• One In Three British Families Are A Month’s Pay From Losing Homes (G.)

More than one in three families in England are a monthly pay packet away from losing their homes, according to research by Shelter highlighting how many households have almost no savings. The housing charity found that 37% of working families would be unable to cover their housing costs for more than a month if one partner lost their job. The findings mirror government figures, which show that there are 16.5 million working age adults in the UK with no savings. Campbell Robb, the chief executive of Shelter, said: “These figures are a stark reminder that sky-high housing costs are leaving millions of working families stretched to breaking point and barely scraping by from one paycheque to the next.

“Any one of us could hit a bump along life’s road, and at Shelter, we speak to parents every day who, after losing their job or seeing their hours cut, are terrified of losing the roof over their children’s heads too.” The charity is calling for an improved welfare safety net to prevent families where someone loses a job from “hurtling towards homelessness”. The phenomenon of the working poor, those earning a regular salary, but living from one paycheque to the next with no savings to speak of, is a widespread feature in English-speaking western economies such as the UK, Canada, the US and Australia. An annual survey by US website Bankrate found that 63% of Americans have no emergency savings for necessities such as a $1,000 (£770) emergency room visit or a $500 car repair. Most turn to credit cards when financial disaster looms.

If they didn’t, where would their share prices be?

• Vulnerable UK Banks Still Pay Billions In Dividends To Shareholders (Ind.)

Three of the UK’s biggest banks have paid out billions of pounds in dividends to investors while turning a blind eye to huge capital holes in their balance sheets, researchers argue. The findings, which come in the wake of estimates the UK banking sector has an aggregate £155bn shortfall of capital, will reinforce calls for the Bank of England to take a tougher stance on the capital adequacy of the lenders it oversees and to restrict the payment of dividends. Between 2010 and 2015 HSBC paid out £37bn in dividends, Barclays paid out £6.3bn and Lloyds paid out £2.3bn according to the calculations of Sascha Steffen of the University of Mannheim, Viral Acharya of New York University and Diane Pierret of the University of Lausanne.

If this cash had been retained by the banks it could have boosted their capital buffers by an equivalent amount. The three researchers last month produced an estimate that suggested UK banks would be massively exposed and at high risk of going bust in another serious financial crisis. They found that the majority state-owned Royal Bank of Scotland, Lloyds, Barclays and HSBC could collectively need to raise another £155bn of capital to maintain a comfortable equity safety buffer in the wake of a fresh crisis based on the market value of their equity.

Can’t say it enough: ““There is no means of avoiding a final collapse of a boom brought about by credit expansion.”

• A Crisis Of Intervention (Price)

For those that already have, Mark Carney is the gift that keeps on giving. Borrowed imprudently and struggling to make those interest payments ? Worry not; the Bank of England has your back. For those that don’t have, the Bank of England is taking away your chance of ever realistically saving anything, now that interest rates have been driven down to new historic lows of 0.25%, and may go lower yet. For the asset-rich, for the 1%, for property speculators, and for zombie companies and banks, Carney is your man. For the asset poor, or for savers, or pensioners, or insurance companies, or pension funds, the Bank of England has morphed from being anti-inflationary fireman to monetary arsonist. The economist Ludwig von Mises foresaw all this, nearly a century ago.

He called it “the crisis of interventionism”. Actions have consequences everywhere (except in Keynesian and Marxist economic theory). Interfere with the free market process and inefficiency and complexity are certain to rise. More actions and interventions are required. Pretty soon the entire system becomes a Heath Robinson contraption requiring constant amendments and ad hoc fixes and bolt-on workarounds. Welcome to the modern monetary system – the last, doomed refuge of the central planner with messianic delusions of adequacy. “The essence of the interventionist policy is to take from one group to give to another. It is confiscation and distribution. Every measure is ultimately justified by declaring that it is fair to curb the rich for the benefit of the poor.”

But so warped has our monetary system become after almost a decade of furious interventionism that Mark Carney’s redistributive efforts don’t even attempt to deliver to that objective. With interest rates fast approaching the theoretical lower bound of zero, Mark Carney is curbing the prospects of the poor for the benefit of the rich. He is redistributing capital from the prudent saver and gifting it to the borrower and the speculator. A crisis of too much debt is being met with ever more urgent attempts to prime the credit pump. Mises had something to say about credit expansion, too. “There is no means of avoiding a final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as a result of a voluntary abandonment of further credit expansion or later as a final and total catastrophe of the currency system involved.”

Right. Spain. Hasn’t had a real government in a long time now. Unemployment is sky high. So everyone wants their bonds… Not. But Draghi buys all.

• Spanish 10-Year Bond Yield Falls Below 1% for First Time (BBG)

Spanish 10-year bond yields fell below 1% for the first time on record Monday, marking another milestone in the four-year rally in the nation’s securities. The drop highlights how local political risk is being offset by monetary easing by central banks across the developed world. The yield fell to as low as 0.99%, down from more than 7.75% during the euro region’s debt crisis in July 2012.

Strange headline for an article that translates as: BUBBLE!

• China Leaders Head to the Beach, With Calmer Seas Ahead (BBG)

China’s top leaders are gathering for their annual conclave at the Beidaihe beach resort having defied the doomsayers once more. Economic data in coming days are projected to confirm the stabilization in growth achieved in the first half of this year continued into July. The backdrop of calm has won China a sustained respite from the financial-market turmoil and capital outflows that accompanied the Communist leadership’s traditional beach-resort meeting last year. But the stability has come at a cost. Instead of delivering on what Premier Li Keqiang called reforms so tough they’d be like cutting “flesh,” authorities have relied on another dose of cheap credit to prop things up.

That’s added more leverage to a nation where debt is already 2.5 times the economy’s size. Behind the reluctance for a bigger economic shakeup is a desire for stability ahead of a potentially wide-ranging reshuffle of the Communist hierarchy next year, according to Credit Suisse. “Candidates will prefer to be playing it safe rather than executing substantial reforms – especially state-owned enterprise reforms,” the bank’s China analysts, led by Vincent Chan, wrote last month. State-owned enterprises offer the major lever for ramping up growth through infrastructure spending, making officials reluctant to implement wide-ranging changes.

Yet their dominance in access to capital has squeezed opportunities for the more efficient private sector, contributing to a build-up in non-performing loans. “The immediate consequences of course are a relatively becalmed economy, which seems to have some staying power,” said George Magnus, senior economic adviser to UBS. “But at what cost in the medium to longer term if there’s no change in the instability-causing policies?”

He needs to avoid the idea that the elites will profit most. This will be thrown at him no matter if it’s true or not.

• Trump Tax Cuts Would Be Costly (CNBC)

Call it a work in progress. GOP presidential candidate Donald Trump unveiled Monday the latest version of his plan to overhaul the American tax code, offering relief for everyone from parents paying for child care to the world’s largest corporations. But it remains to be seen where the money will come from to pay for those cuts. Details of the plan are still fairly sketchy, but in his speech at the Detroit Economic Club, Trump promised they would be forthcoming soon. “In the coming weeks we will be offering more detail on all of these policies,” Trump said Monday. The Trump campaign has promised that the tax plan would “benefit working families while ensuring the wealthy pay their fair share.”

But based on details of Trump’s plan released earlier in the campaign, some analysts think the biggest winners would be those at the top of the income ladder. “The proposal would cut taxes at every income level, but high-income taxpayers would receive the biggest cuts, both in dollar terms and as a percentage of income,” according to an analysis in December by the Tax Policy Center. Trump’s campaign said Monday the tax plan would “dramatically reduce taxes for everyone and streamline deductions, presenting the biggest tax reform since [the] Reagan [administration].” But based on the details released so far, the plan would also explode the federal budget deficit, add trillions of dollars to the national debt and substantially raise the government’s interest payments, according to several independent analysts.

Trump’s tax cuts would amount to some $12 trillion over the next decade, according to the Tax Foundation. Even after accounting for stronger economic growth, the plan would leave the government more than $10 trillion short over the next 10 years. That money would have to be made up for with more borrowing, dramatically expanding the nation’s debt. Trump also promised to ease the burden on American corporations by limiting taxes to 15 percent. The campaign has also promised to “make our corporate tax globally competitive and the United States the most attractive place to invest in the world.” Based on the latest available data, that promise should be fairly easy to keep.

Security experts? They’re neocons. Brilliant riposte: “We thank them for coming forward so everyone in the country knows who deserves the blame for making the world such a dangerous place..”

• Republican Security Experts Rail Against Trump In Open Letter (BBC)

An open letter signed by 50 Republican national security experts has warned that nominee Donald Trump “would be the most reckless president” in US history. The group, which includes the former CIA director Michael Hayden, said Mr Trump “lacks the character, values and experience” to be president. Many of the signatories had declined to sign a similar note in March. In response, Mr Trump said they were part of a “failed Washington elite” looking to hold on to power. The open letter comes after a number of high-profile Republicans stepped forward to disown the property tycoon. Mr Trump has broken with years of Republican foreign policy on a number of occasions.

The Republican candidate has questioned whether the US should honour its commitments to Nato, endorsed the use of torture and suggested that South Korea and Japan should arm themselves with nuclear weapons. “He weakens US moral authority as the leader of the free world,” the letter read. “He appears to lack basic knowledge about and belief in the US Constitution, US laws, and US institutions, including religious tolerance, freedom of the press, and an independent judiciary.” “None of us will vote for Donald Trump,” the letter states. In a statement, Mr Trump said the names on the letter were “the ones the American people should look to for answers on why the world is a mess”.

“We thank them for coming forward so everyone in the country knows who deserves the blame for making the world such a dangerous place,” he continued. “They are nothing more than the failed Washington elite looking to hold on to their power and it’s time they are held accountable for their actions.” Also among those who signed the letter were John Negroponte, the first director of national intelligence and later deputy secretary of state; Robert Zoellick, who was also a former deputy secretary of state and former president of the World Bank; and two former secretaries of homeland security, Tom Ridge and Michael Chertoff.

Surprised?

• US Taxes Well Spent: Pentagon Can’t Account for $6.5 Trillion (Sputnik)

While US lawmakers are applying pressure on the Pentagon to be more transparent about how it spends money, a new report shows that the Defense Department’s substandard bookkeeping practices make that virtually impossible. Despite a 1996 law requiring all federal agencies to conduct regular spending audits, the Pentagon has so far failed to conduct a single one. While US lawmakers have pressed the DoD to comply by September of 2017, a new inspector general’s report indicates that meeting this deadline is highly unlikely.

“Army and Defense Finance and Accounting Service Indianapolis personnel did not adequately support $2.8 trillion in third quarter adjustments and $6.5 trillion in year-end adjustments made to Army General Fund (AGF) data during FY 2015 financial statement compilation,” the report reads. In common language, the Pentagon has no idea how it spent nearly $7 trillion. This is largely due to the fact that the DoD fails to provide the “journal vouchers” for its transactions, intended to provide serial numbers and dates, for bookkeeping purposes. But the report also found that many of the Pentagon’s records were missing without explanation.

“DFAS Indianapolis did not document or support why the Defense Departmental Reporting System-Budgetary, a budgetary reporting system, removed at least 16,513 of 1.3 million records during third quarter FY 2015,” the report reads. While nothing suggests foul play, a lack of proper accounting makes it impossible to determine how much money the Pentagon spends, and on what.

There is a huge potential for this to backfire. Facebook better watch out.

• Facebook Removes Potential Evidence Of Police Brutality Too Readily (I’Cept)

As more details emerge about last week’s killing by Baltimore County police of 23-year-old Korryn Gaines, activists have directed growing anger not only at local law enforcement but also at Facebook, the social media platform where Gaines posted parts of her five-hour standoff with police. At the request of law enforcement, Facebook deleted Gaines’ account, as well her account on Instagram, which it also owns, during her confrontation with authorities. While many of her videos remain inaccessible, in one, which was re-uploaded to YouTube, an officer can be seen pointing a gun as he peers into a living room from behind a door, while a child’s voice is heard in the background. In another video, which remains on Instagram, Gaines can be heard speaking to her five-year-old son, who’s sitting on the floor wearing red pajamas.

“Who’s outside?” she asks him. “The police,” he replies timidly. “What are they trying to do?” “They trying to kill us.” Statements made by officials in the days after the incident revealed little-known details of a “law enforcement portal” through which agencies can ask for Facebook’s collaboration in emergencies, a feature of the site that remains mostly obscure to the general public and which has been criticized following Gaines’ death. It’s not the first time Facebook has become the stage on which violent encounters between law enforcement and residents play out – and it seems likely more and more such incidents will be documented on the social media hub, given that the company’s livestreaming app, Facebook Live, is only nine months old and spreading at a time when recording police has become an instinctive reflex in some communities.

We can see the earth disappear beneath our feet.

• More Than 60% Of Maldives’ Coral Reefs Hit By Bleaching (G.)

More than 60% of coral in reefs in the Maldives has been hit by “bleaching” as the world is gripped by record temperatures in 2016, a scientific survey suggests. Bleaching happens when algae that lives in the coral is expelled due to stress caused by extreme and sustained changes in temperatures, turning the coral white and putting it at risk of dying if conditions do not return to normal. Unusually warm ocean temperatures due to climate change and a strong “El Nino” phenomenon that pushes up temperatures further have led to coral reefs worldwide being affected in a global bleaching event over the past two years. Preliminary results of a survey in May this year found all the reefs looked at in the Maldives, in the Indian Ocean, were affected by high sea surface temperatures.

Around 60% of all assessed coral colonies, and up to 90% in some areas, were bleached. The study was conducted by the Maldives Marine Research Centre and the Environmental Protection Agency, in partnership with the International Union for Conservation of Nature (IUCN). It took place on Alifu Alifu Atholhu – North Ari Atoll – chosen as a representative atoll of the Maldives. Dr Ameer Abdulla, research team leader and senior adviser to the IUCN on marine biodiversity and conservation science, said: “Bleaching events are becoming more frequent and more severe due to global climate change. “Our survey was undertaken at the height of the 2016 event and preliminary findings of the extent of the bleaching are alarming, with initial coral mortality already observed. “We are expecting this mortality to increase if bleached corals are unable to recover.”

Home › Forums › Debt Rattle August 9 2016