Marjory Collins Super Suds in cooperative store, Greenbelt, Maryland May 1942

Sifting through the debris after the initial wave of the year’s first major storm has subsided, there’s no escaping the realization that the damage is structural, this was no incident, and the next wave may well topple the whole structure. Its foundations have been impaired so thoroughly by many years of intentional neglect that the only sensible thing to do is to raze it, lay down new foundations, and erect a whole new edifice.

Ironically, it’s the utter contempt for the free market system as exhibited by the major players in what still poses as a capitalist society, that has done us in. Recklessly flooding the entire premises with ultra cheap liquidity is the one thing the building proved to have no resistance against. Turns out, if you don’t replace weak pieces with new and stronger ones, if you don’t throw out what has started rotting, you end up compromising the entire foundations.

Tyler Durden quotes Deutsche Bank strategist Jim Reid as saying his bullish on the markets, but only because the Fed and other central banks have walked into a trap, which makes it impossible for them to leave their positions, and they must continue to inject the liquidity that now holds the whole system upright in a Wile E. sort of suspension, or the system must collapse.

” … it means that central banks have little option but to keep high levels of support for markets for as far as the eye can see and defaults will stay artificially low. As such we remain bullish for 2014. However it’s largely because we think the authorities are trapped for now rather than because the global financial system is healing rapidly”.

But liquidity is no replacement for solid foundations, and what’s more, it will run out at some point. And that’s not all: the Fed can no longer try to only keep its own house from crumbling, the poorer neighbors are begging for their share as well: Fed liquidity is now propping up the castles in their air too. And if it would refuse to provide for the whole neighborhood, the ensuing damage would severely risk what’s left of the home of America. The entire town could become one giant sinkhole. Which it will anyway, with all that liquidity slushing around underground, but that doesn’t seem to worry the somewhat-less-than-Federal Reserve.

What Janet Yellen inherited, and it’s quite possible she hasn’t realized it yet, is the supposedly most powerful institution on the entire planet, that has painted itself into a very tight corner, from which no obvious escape route is in sight. If she opts to continue doling out Bernanke’s liquidity overdoses, she will hollow out America’s economic strength in a fatal way. And if she decides to get up and turn around, she’ll do the same, only more rapidly.

There is one other problem, and there’s no way Janet is not aware of this. The Fed may be the supposedly most powerful institution on the planet, but it’s that of course only in name. In reality, the Fed is the tool constructed – through the years – to give the real most powerful institutions, the Wall Street banks, access to the full faith and credit of the American people.

The people behind those banks don’t care that the building is shaking: they don’t live there. And besides, they know this situation can’t last forever. They’ll simply pump out what they can and leave for the greener pastures they’ve purchased before they started to blow the behemoth bubble. Many of those left behind will simply drown, and whoever manages to save themselves will be thrown back to days of yore, tasked with building a whole new country from the ground up.

So what is Yellen going to do? Large numbers of Americans seem to believe there is an actual recovery happening, so there will be many who clamor for more tapering. But that’s going to sink the poorer neighbors. And with emerging economies now providing about 50% of world trade, that might be too risky to try. The US can appeal to China and Europe to do more, but they have their own sets of problems, so that’s not a very likely source of aid.

What could set off a wide chain of negative events in one fell swoop is a fast rising US dollar. But to the extent that Yellen has control over that – and don’t overestimate that -, there’s a point to be made for a stronger dollar being good for America in this world and this market. The US will have a few years in which much less oil and gas must be imported, so less goes out there, and emerging market products could become much cheaper at home. At the present time, it’s hard to see how the dollar can be kept much longer from rising against for instance the euro and the yuan, two currencies events will place under increasing pressure. Another Yellen trap, or part of the same one perhaps.

How severe the crisis is in some parts of the world becomes clear through data provided by Ambrose E-P. There have been such enormous amounts of fresh debt raised in emerging markets, they’re risking imminent collapses already today. Take away QE from Washington, and it’ll get much worse. A Braziliacn hedge funder says “Brazil needs a 60% to 70% devaluation to restore industrial competitiveness”. But industrial competitiveness does not a country make, or an economy. Such a move would do huge damage to Rio and Sao Paulo, and well over 100 million people. And that’s just one country in a long row nations suffering from the same post bubble hangovers. That same hedge funder says “This will end badly,” and who’s going to claim he’s wrong?

• Emerging markets more vulnerable than ever to Fed tightening, warns BIS (AEP)

Emerging markets may be even more vulnerable to an interest rate shock today than they were during the East Asia crisis in 1998, the Bank for International Settlements (BIS) has warned. The Swiss-based watchdog said there has been a “massive expansion” in borrowing on global bond markets by banks and companies in developing countries, leaving them exposed to “powerful feedback” risks as borrowing costs rise in the West.

“The deeper integration of emerging market economies into global debt markets has made emerging market bond markets much more sensitive to bond market developments in the advanced economies,” the BIS said in a working paper. “The global long-term interest rate now matters much more for the monetary policy choice facing emerging market economies than a decade ago,” it said.

Brazil’s industrial output slumped 3.5% in December as the delayed effects of monetary tightening bite deeper, a foretaste of what lies in store for a string of countries that have raised rates to defend their currencies. “This was the biggest monthly contraction since December 2008 ,” said George Lei, from Nomura.

Brazil is facing pressure on every front. Its budget deficit surged to $65 billion in 2013 . The current account deficit widened to 3.7% of GDP, hit by sliding iron ore prices. Edmar Bacha, from the Casa das Garças Institute, said Brazil is living beyond its means and will have to accept a “contraction of internal demand” to right the ship. Marcelo Ribeiro from the hedge fund Pentagono said Brazil needs a 60% to 70% devaluation to restore industrial competitiveness . “This will end badly,” he said. [..]

The BIS report said debt issuance in emerging markets has been so great that a “sudden stop” could overwhelm central banks and pose a risk to financial stability. The twin effects of falling currencies and rising bond yields may feed on each other in a vicious circle. Unprecedented access to global capital markets has allowed emerging market companies to borrow vast sums at real interests rates near 1%, almost doubling their local currency debts to $9.1 trillion since 2008 . This is a Faustian Pact, leaving them more leveraged than ever before to the global cost of money.

The BIS said quantitative easing by the US, UK and Japan – combined with surging foreign reserve accumulation by China and other emerging powers – held borrowing costs by around 250 basis points below historic levels, until the Fed lost control last year and long-term rates began to spike.

This so-called “term premium compression” led to a surge in offshore dollar lending through the bond markets. Companies and banks raised almost $2 trillion from 2010 to mid-2013, creating a liability mismatch that could go badly awry if the dollar surges – as it already has against the real, the Turkish lira, the Indian rupee and South Africa’s rand.

The BIS hinted at a nasty possibility in which emerging market companies rush to pay off foreign debts and try to raise debt in their own currencies instead from local banks. This would cause a “sharp drop” in the exchange rate even for states with an ostensibly healthy current account surplus, an effect seen in Russia in 2008-2009.

I’m starting to like the Phoenix Capital notes Durden provides. They’re clear and concise and they say the same things I do. It’s all so obvious you wonder why it’s not more obvious.

• Is Anyone Really Surprised That the System is On the Brink Again? (Phoenix Capital)

We find it truly extraordinary that anyone is surprised the financial system is under duress again. After all, what have the Central Banks accomplished in the last five years?

1) Did they clear out the bad debts that caused the 2008 collapse? NOPE

2) Did they implement structural reforms to insure another 2008 didn’t happen? NOPE

3) Did they punish fraud or corruption in any way to insure that the system was clean? NOPE

So what did they do? They cut interest rates over 500 times and funneled over $10 trillion into the financial system, over 98% of which went to the very players (key banks) who nearly blew up the world in 2008. And people are actually surprised that the system is back in trouble again? Would you be surprised if giving another shot of heroin to a drug addict who was in a coma didn’t bring him to health?

Honestly, did anyone think this would really work? I know that the connected elites loved it because the whole process allowed them to hand off their garbage investments to the public while leveraging up to acquire more assets via the Fed’s cheap money… but what about those who DON’T work for a top 20 global financial institutions? Did anyone actually believe this would work?

So here we are today, Europe’s already insolvent banks are now potentially on the hook for $3 trillion in Emerging Market investments. When your entire banking system is leveraged at 26-to-1 it really doesn’t matter who you lend to… you’re bust. But in this case, the bad emerging market investments are just the icing on the rotten cake that is Europe’s banking balance sheets.

Hopefully Mario Draghi can “promise” something again and the whole system will hold together. After all, THAT and Bernanke’s decision to engage in more and more QE (despite NO evidence that QE benefits the economy) are what brought us back from the brink in June 2012… maybe Janet Yellen and Mario Draghi can repeat this.

Then of course there’s China… which has created the single biggest credit bubble relative to GDP in history. Never mind, that they literally blow up buildings to build new ones to pad their GDP numbers… China is a miracle and its economy is on the verge of becoming another US. The world believes China can become more driven by consumers… though the data shows consumer spending has grown by 9% a year for 30 years there… so hoping that things are going to erupt higher there is a little misguided.

And of course there’s the US, which is STILL printing $65 billion per month despite two QE tapers… which folks claim were terrible for the world (how exactly is printing $65 billion per month five years into an alleged recovery, a good thing? Doesn’t that NEGATE the entire claim of a recovery at all?).

You can build a house on a rotten foundation (bad debt, fraud, corruption) and it will stand for a while. But eventually it will collapse. This will again happen with the markets. The only difference is that this time around, the Central banks have already spent most if not ALL of their ammo propping up the system.

“We’ve created a global debt monster that’s now so big and so crucial to the workings of the financial system and economy that defaults have been increasingly minimised by uber aggressive policy responses.”.

And that comes from a Wall Street primary dealer analyst. It’s almost funny. Bullish because the system is doomed. And thinking you’ll be smart enough to get out in time. Maybe it’s time to reconsider that option. Why take the risk? For a few extra bob? Don’t have enough yet?

• Deutsche Bank: “We’ve Created A Global Debt Monster” (Zero Hedge)

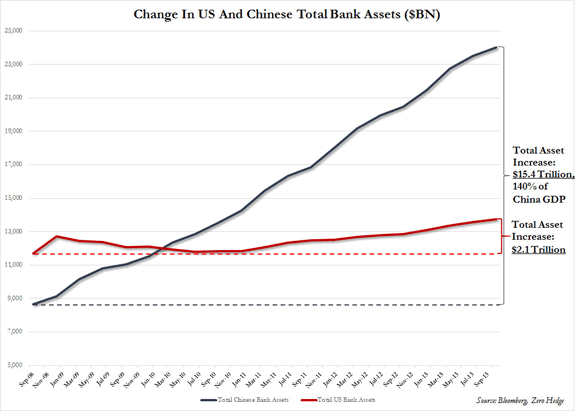

Two observations on the latest thoughts by Jim Reid (DB’s best strategist by orders of magnitude): He is far more concerned by what is going on in China than any of the other noise around the world. And rightfully so. As we first showed a few months ago, the money creation in China puts what all the other global central banks do to shame. Any slowdown in this credit creation and the wheels have no choice but to fall off, which also explains why even the tiniest default in this $9 trillion economy will be bailed out as it would risk an outright “flow” collapse.

Note from Reid: “For me it’s a microcosm of the fragility still present in global financial markets that a $9.0 trillion dollar economy – that will be the biggest in the world within the time frame of most of our careers – struggles to allow a $500 million investment product to default without there being market fears of it igniting panic in financial markets. [..]

We’ve created a global debt monster that’s now so big and so crucial to the workings of the financial system and economy that defaults have been increasingly minimised by uber aggressive policy responses. It’s arguably too late to change course now without huge consequences. This cycle perhaps started with very easy policy after the 97/98 EM crises thus kick starting the exponential rise in leverage across the globe. Since then we saw big corporates saved in the early 00s, financials towards the end of the decade and most recently Sovereigns bailed out. It’s been many, many years since free markets decided the fate of debt markets and bail-outs have generally had to get bigger and bigger.

This sounds negative but the reality is that for us it means that central banks have little option but to keep high levels of support for markets for as far as the eye can see and defaults will stay artificially low. As such we remain bullish for 2014. However it’s largely because we think the authorities are trapped for now rather than because the global financial system is healing rapidly .”

In other words: bullish… because the system will continue to collapse and need more bailouts. The Bizarro world Bernanke created truly is an exciting place.

Mish has a translated interview with Greek economist Costas Lapavitsas who has a few more specifics on the Greek case. And on France. While it’s not entirely impossible that Europe sails through another year relatively smoothly, its chances are not good. The $3 trillion EU banks have invested in shoddy EM assets could backfire and necessitate more bank bailouts. But the appetite for more of that same old is now so low, any such attempt could easily result in violent blowback. And if France is as bad as more and more voices claim, Europe’s problems to date will feel like a barefoot walk in the park on a sunny day with your favorite person the world.

• “Situation Impossible” (Mish)

Greek economist Costas Lapavitsas says “The Euro has Already Failed” and it’s “Situation Impossible” for France. Via translation from La Vanguardia:

LV: Are we far from a stable eurozone crisis solution?

CL: The ECB stabilized the fiscal deficit and the trade deficit and hence financial markets. But the crisis has become a crisis in the real economy. There is foul growth and impoverishment.

LV: Has the crisis moved from the periphery crisis to other countries?

CL: Yes. The euro crisis has moved to the heart of the eurozone. France and Italy are now facing the same problems as the periphery in 2010 and 2011. The crisis is now in France and Italy.

LV: Is there more inequality now than at the beginning of the crisis?

CL: Of course. Here’s how the situation has stabilized: recession, austerity without growth, more impoverishment and huge social problems for most of the working class.

LV: Can we forget the idea introduced a couple of years ago regarding a two-speed euro?

CL: I do not think it’s going to be a two-speed euro. I think the policy that comes from Berlin and Brussels is the austerity of all European countries. France is now in a situation impossible . The real problem in the eurozone is now France. It has a great competitiveness gap with Germany.

LV: Why?

CL: The competitiveness gap that the periphery had in 2010-11 is now in France. Wages in Germany have gone up a bit or frozen, wages in France have grown in line with inflation. This gap makes it difficult for the French economy to grow significantly. If France is moving towards austerity, as the periphery, Europe faces serious problems. Depression. And France is facing huge social and political problems. The eurozone crisis has moved to the heart of the euro.

LV: Do you think that the euro will fail?

CL: The euro has already failed. It was a project that was supposed to create convergence, growth and solidarity between the peoples of Europe, it was supposed to create a commonality among Europeans. The euro has created divergences, recession, poverty, it is like a straitjacket for Europe, increases the national and the social tensions in Europe. It succeeds now only because it instills fear. I do not think this is sustainable for long.

LV: How is the situation in Greece?

CL: Greece is a mess. In 2010 Greece should have left the euro and put its economy in another direction. The economic and social catastrophe in Greece is worse than what happened in Argentina in the late 90s and early 2000 . This is what happens when you’re within this monetary structure that is the euro.

Stunning numbers from Elizabeth Warrren. America’s poor spend an entire one month’s paycheck per year just for simple financial services. Unbelievable.

• Coming to a Post Office Near You: Loans You Can Trust? (Elizabeth Warren)

The poor pay more. According to a report put out this week by the Office of the Inspector General (OIG) of the U.S. Postal Service, about 68 million Americans — more than a quarter of all households — have no checking or savings account and are underserved by the banking system. Collectively, these households spent about $89 billion in 2012 on interest and fees for non-bank financial services like payday loans and check cashing, which works out to an average of $2,412 per household. That means the average underserved household spends roughly 10% of its annual income on interest and fees – about the same amount they spend on food.

Think about that: about 10% of a family’s income just to manage getting checks cashed, bills paid, and, sometimes, a short-term loan to tide them over . That’s more than a full month’s income just to try to navigate the basics. The poor pay more, and that’s one of the reasons people get trapped at the bottom of the economic ladder.

But it doesn’t have to be this way. In the same remarkable report this week, the OIG explored the possibility of the USPS offering basic banking services — bill paying, check cashing, small loans — to its customers. With post offices and postal workers already on the ground, USPS could partner with banks to make a critical difference for millions of Americans who don’t have basic banking services because there are almost no banks or bank branches in their neighborhoods. [..]

If the Postal Service offered basic banking services — nothing fancy, just basic bill paying, check cashing and small dollar loans — then it could provide affordable financial services for underserved families, and, at the same time, shore up its own financial footing. (The postal services in many other countries, it turns out, have taken steps in this direction and seen their earnings increase dramatically.)

Detroit remains a test case to follow. Many municipalities after this will need to implement whatever comes out of the Detroit case, in their own bankruptcy or salvation procedures. Will a judge force huge losses on pensioners, so more will be available for bondholders, or will he decide to try and make pensioners as whole as he can? This could take along time, as in years, to wrap up.

• Detroit Turns Bankruptcy Into Challenge of Banks (NY Times)

Detroit’s bankruptcy is rapidly shaping up as a battle of Wall Street vs. Main Street, at least as far as the city’s creditors are concerned. Amy Laskey,a managing director at Fitch Ratings, said in a recent report that she sensed an “us versus them” orientation toward debt repayment. And in the view of bondholders, bond insurers and other financial institutions, it only grew worse last week after the city circulated its plan to emerge from bankruptcy and filed a lawsuit on Friday.

The suit, brought by the city’s emergency manager, Kevyn D. Orr, seeks to invalidate complex transactions that helped finance Detroit’s pension system in 2005. In a not-so-veiled criticism, the city said the deal was done “at the prompting of investment banks that would profit handsomely from the transaction.”

The banks that led the deal were Bank of America and UBS. They helped Detroit borrow $1.4 billion for its shaky pension system and also signed long-term financial contracts with the city, known as interest-rate swaps, to hedge the debt. Detroit has already stopped paying back the $1.4 billion, but for the first six months of its bankruptcy it kept honoring the swaps contracts and at one point offered to pay the two banks hundreds of millions of dollars — money it would have had to borrow — to end them. But the lawsuit now seeks to cancel the swaps, arguing they were illegal from the outset along with the related debt transactions.

“The savings of an average Briton would cover less than two weeks living expenses”. What else do I need to say here? That there’s more austerity on the way? Bet you already knew that.

• ‘Deadline to Breadline’ weighs on Britons, third have nothing to save (RT)

A third of Britons don’t have any money to save, with North East families having cash reserves for just 11 days, warns a Legal & General report. Cutting spending on energy and clothes are the most popular personal “austerity measures” another report adds.

The savings of an average Briton would cover less than two weeks living expenses, according to the “Deadline to Breadline” report from the financial services firm Legal & General. The report says that afterwards they’ll have to turn to the governmental for help or ask friends or family for support. “It serves as a stark reality check to see that most of us are still in a precarious financial situation – the average working-age family is just 11 days away from the breadline,” John Pollock, Legal & General chief executive, said.

However, the 11-day period is the minimum that affects some people in the North East of England, in Greater London the figure stands at 78 days. Another market research firm Nielsen found that the rising energy bills are making 60 percent of Britons save on energy, with another 58% being forced to cut on clothes spending and 57% enjoying fewer takeaway meals.

Consumer confidence also dropped, as the corresponding index fell to three points to 84 from its six-year high of 87. This put the country in between the global reading of 94 and the European index of 73. The disheartening view from both financial surveys shows that average working families have yet to feel the benefits of economic recovery. In a consumer confidence index 100 points serve as a baseline, with any readings below and above it reflecting levels of optimism and pessimism.

Funny how the Guardian proves that a deflation story can easily become totally convoluted and go off track if you us the empty populist definitions of inflation and deflation. But prices are falling, and they have been for nine months now. And what other possibility is there when “The savings of an average Briton would cover less than two weeks living expenses”? Got to lower your prices or you’re not going to sell anything.

• UK shop prices fall for ninth consecutive month (Guardian)

Shop price deflation accelerated to 1% last month from 0.8% in December according to the British Retail Consortium/Nielsen shop price index, as January sales were deeper than usual. It was the ninth consecutive month of falling prices and the sharpest deflation rate on record since the series began in December 2006. The report reflected the recent trend in the consumer prices index – Britain’s official inflation measure – which fell back to the Bank of England’s 2% target for the first time in four years in December from 2.1% in November.

Shop price deflation in the non-food sector overall accelerated to 2.7% in January from 2.3% in December, with clothing and footwear deflation the biggest contributor at 9.9%. Food inflation meanwhile slowed by 0.2 percentage points to 1.5% – the lowest level in almost four years.

Fox loves this story, got to be careful. Here’s the core: “In its latest U.S. fiscal outlook, the nonpartisan CBO said the health law would lead some workers, particularly those with lower incomes, to limit their hours to avoid losing federal subsidies that Obamacare provides to help pay for health insurance and other healthcare costs.“. So a truckload of work hours will be lost because people wold rather stay home than lose benefits. These are low income people, who’ve figured out that working those extra hours could cost them a huge amount of money. See, my first reaction was: so give those extra hours to the unemployed! You got this great recovered economy, so you’re going to have to get those hours filled, right? This is low income, these are burger flippers, so hire another burger flipper, what’s the problem? It might be better to adapt the law a little, but it sure doesn’t all look so bad.

• Obamacare to cut equivalent of 2 million jobs (Reuters)

President Barack Obama’s healthcare law will reduce American workforce participation by the equivalent of 2 million full-time jobs in 2017, the Congressional Budget Office said on Tuesday, prompting Republicans to paint the law as bad medicine for the U.S. economy.

In its latest U.S. fiscal outlook, the nonpartisan CBO said the health law would lead some workers, particularly those with lower incomes, to limit their hours to avoid losing federal subsidies that Obamacare provides to help pay for health insurance and other healthcare costs. The biggest impact would begin in 2017, CBO said, because major provisions of the law will be well under way by then. The CBO said there would be smaller declines in work hours that would occur before then.

Work hours would be reduced by the equivalent of 2.5 million jobs in 2024, said the agency, which earlier predicted 800,000 fewer fulltime jobs by 2021. The bottom line would be a slower rate of growth for employment and compensation in the coming decade, according to the report.

The link that the CBO drew between the health law and slower employment growth is likely to become fodder for partisan attacks in this year’s congressional election battle, which will determine who controls Congress in the final years of the Obama presidency. Obamacare is unpopular with many voters and its botched October rollout was accompanied by a public outcry by millions of people who saw their health plans cancelled as a result of its implementation.

Smile! You’re on the Art Channel.

• Italy threatens to sue Standard & Poor’s for failing to value its history and art

Italy is threatening to sue the credit ratings agency Standard & Poor’s for failing to value its historical and cultural treasures. The country that bequeathed the world Dante, da Vinci and an enviable vision of La Dolce Vita, thinks financial analysts would not have issued a damaging credit downgrade against Italy if they had paid more attention to its cultural wealth than its spiralling budget deficit.

According to the Financial Times, Italy’s auditor general, the corte dei conti, believes that S&P may have acted illegally and could be sued for £234m. The paper cites a letter from the corte dei conti notifying S&P that it is considering legal action: “S&P never in its ratings pointed out Italy’s history, art or landscape which, as universally recognised, are the basis of its economic strength.” S&P has described the claims as “frivolous and without merit”.

The investigation extends to S&P’s rivals Moody’s and Fitch, with further details expected to be revealed by the corte dei conti on 18 February. Moody’s dismissed the allegations, while a spokesman for Fitch said: “As we understand the prosecutor’s concerns, we believe Fitch at all times acted appropriately and in full compliance with the law.”

I haven’t written about the tar sands in a long time. At some point, it seems you’ve said it all, and besides, in Canada today, who can be bothered to get off the couch? But this PhysOrg article holds no surprises for me. Bunch of fools and wankers. But then, that’s what man has become. Be it credit bubbles, or pollution, or any other self-inflicted issue, nobody gives a sh*t if there’s money to be made. And they’ll just continue to label themselves “smart” anyway. Can’t lose.

• Oil sands pollution 2-3 times higher than thought (Phys.org)

The amount of harmful pollutants released in the process of recovering oil from tar sands in western Canada is likely far higher than corporate interests say, university researchers said Monday. Actual levels of polycyclic aromatic hydrocarbon (PAH) emissions into the air may be two to three times higher than estimated, said the findings in the Proceedings of the National Academy of Sciences, a peer-reviewed US journal.

The study raises new questions about the accuracy of environmental impact assessments on the tar sands, just days after a US State Department report said the controversial Keystone pipeline project to bring oil from Canada to Texas would have little impact on climate change or the environment.

Current, government-accepted estimates do not account for the evaporation of PAHs from wastewater pools known as tailings ponds, which are believed to be a major source of pollution, said researchers at the University of Toronto.

According to corporate interests which are responsible for projecting their environmental impact, the Athabasca oil sands beneath Alberta, Canada—which hold the third largest reserve of crude oil known in the world—are only spewing as much pollution into the air as sparsely populated Greenland, where no big industry exists.

Lead study author Frank Wania, a professor in the department of physical and environmental sciences, described the corporate estimates as “inadequate and incomplete.” “If you use these officially reported emissions for the oil sands area you get an emissions density that is lower than just about anywhere else in the world,” he told AFP. “Only with a complete and accurate account of the emissions is it actually possible to make a meaningful assessment of the environmental impact and of the risk to human health,” he added.

The US launches ‘climate hubs’. Translation: we’re not going to change a thing, we’re going to burn it all as fast as we can, and we now have a place where you can come talk about it. What, you’re a farmer? Then why don’t I give you $10 million in subsidies and insurances and you sign this piece of paper that tells you to shut up about it? Next!

My main man VK sent this slide from Kevin Anderson’s 2012 presentation on climate change (available at EcoShock), and says:“For a 50% chance of not exceeding a 2ºC rise in global temperatures (so land temps go up 3-4ºC) fossil fuel use must drop by 90% in 16 years! And that’s for a 50% chance! If we want to limit the risk than the drop is even faster over a shorter time frame. It just seems like a ridiculous task because even a mega financial crisis will not see fossil fuel use drop by 10pc+ per annum for 16 years.”

Time to wake up to the fact that we’re not going to stop this, we’re not going to cut emissions by anything near even the minimal requirements. It’s not who we are. Not saying anything about individual people, but as a group, as a species, that’s simply who we are. And the sooner we acknowledge that, the sooner the individuals can get together and talk about what to do next. Trying to stop the species from being what it is, is not going to work.

• U.S. to launch ‘climate hubs’ to help farmers face climate change

President Barack Obama’s administration will announce on Wednesday the formation of seven “climate hubs” to help farmers and rural communities adapt to extreme weather conditions and other effects of climate change, a White House official said. The hubs will act as information centers and aim to help farmers and ranchers handle risks, including fires, pests, floods and droughts, that are exacerbated by global warming.

The hubs will be located in Ames, Iowa; Durham, New Hampshire; Raleigh, North Carolina; Fort Collins, Colorado; El Reno, Oklahoma; Corvallis, Oregon; and Las Cruces, New Mexico, the official said. Additional “sub hubs” will be set up in Rio Piedras, Puerto Rico; Davis, California; and Houghton, Michigan.

The hubs are an example of executive actions Obama has promised to take to fight climate change. The president has made the issue a top priority for 2014 and has the authority to take many measures that address it without congressional approval.

This article addresses just one of the many issues discussed in Nicole Foss’ new video presentation, Facing the Future, co-presented with Laurence Boomert and available from the Automatic Earth Store. Get your copy now, be much better prepared for 2014, and support The Automatic Earth in the process!

Home › Forums › Debt Rattle Feb 5 2014: From the Bernanke Put to the Yellen Trap