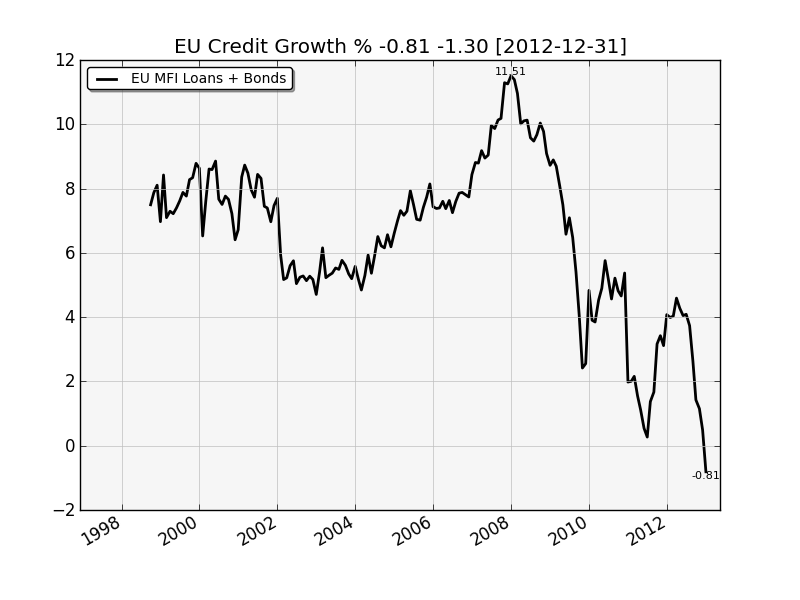

So I’ve recently been exploring the statistical data warehouse provided by the ECB, and I was able to assemble the following chart, comprising MFI Loans (MFI = monetary financial institution) + Bonds (sovereign & corporate). It was good timing, because it shows for the first time during this whole crisis, the eurozone has dropped into deflation.

Now don’t get me wrong, if the Spanish banks (among others) had been marking their loans to market, deflation would have arrived long ago, but according to the data series provided by the ECB, Official Europe has now recognized that they are in deflation.

However you slice it, deflation is NOT a good sign for the equity markets. Fewer bank loans means less money to buy stuff. I’m…perhaps not calling a top (that was back in 2007) but I am leaning short here, at least in the eurozone and especially Spain.

Fun exercise: the Spanish credit growth during the bubble years was a good 20% per year growth for 4 years. That’s twice what the US did during that same period. If you look at Ireland, its even worse.

Anyway, here are the charts. A vastly more detailed set of charts (per-nation) are available at my site, mdbriefing.com/eurozone-credit.shtml.

First – the growth (year/over/year) in credit in the eurozone. When the line goes below zero, that says credit is contracting year-over-year.

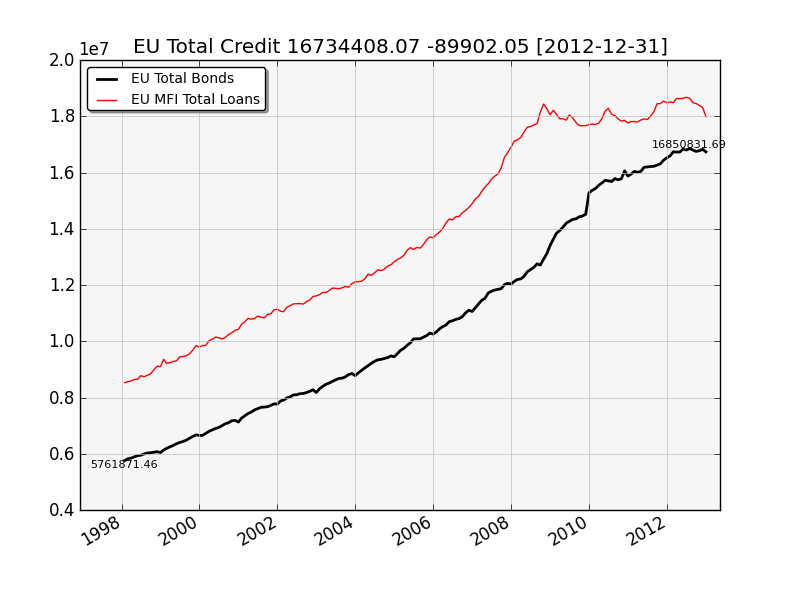

Next, the overall credit – bank loans and bonds. You can see bank loans have taken a bit of a spill recently.

Sorry, the comment form is closed at this time.