Jack Delano Myrtle Beach, S.C. Air Service Command Technical Sergeant Choken 1943

It’s all derivatives all the way down.

• The REAL Issue With a Grexit/Greek Default is Derivatives (Phoenix)

The situation in Greece boils down to the single most important issue for the financial system, namely collateral. Modern financial theory dictates that sovereign bonds are the most “risk free” assets in the financial system (equity, municipal bond, corporate bonds, and the like are all below sovereign bonds in terms of risk profile). The reason for this is because it is far more likely for a company to go belly up than a country. Because of this, the entire Western financial system has sovereign bonds (US Treasuries, German Bunds, Japanese sovereign bonds, etc.) as the senior most asset pledged as collateral for hundreds of trillions of Dollars worth of trades. Indeed, the global derivatives market is roughly $700 trillion in size. That’s over TEN TIMES the world’s GDP. And sovereign bonds… including even bonds from bankrupt countries such as Greece… are one of, if not the primary collateral underlying all of these trades.

Lost amidst the hub-bub about austerity measures and Debt to GDP ratios for Greece is the real issue that concerns the EU banks and the EU regulators: what happens to the trades that EU banks have made using Greek sovereign bonds as collateral? This story has been completely ignored in the media. But if you read between the lines, you will begin to understand what really happened during the previous Greek bailouts. Remember: 1) Before the second Greek bailout, the ECB swapped out all of its Greek sovereign bonds for new bonds that would not take a haircut. 2) Some 80% of the bailout money went to EU banks that were Greek bondholders, not the Greek economy. Regarding #1, going into the second Greek bailout, the ECB had been allowing European nations and banks to dump sovereign bonds onto its balance sheet in exchange for cash.

This occurred via two schemes called LTRO 1 and LTRO 2 which happened in December 2011 and February 2012 respectively. Collectively, these moves resulted in EU financial entities and nations dumping over €1 trillion in sovereign bonds onto the ECB’s balance sheet. Quite a bit of this was Greek debt as everyone in Europe knew that Greece was totally bankrupt. So, when the ECB swapped out its Greek bonds for new bonds that would not take a haircut during the second Greek bailout, the ECB was making sure that the Greek bonds on its balance sheet remained untouchable and as a result could still stand as high grade collateral for the banks that had lent them to the ECB. So the ECB effectively allowed those banks that had dumped Greek sovereign bonds onto its balance sheet to avoid taking a loss… and not have to put up new collateral on their trade portfolios.

Which brings us to the other issue surrounding the second Greek bailout: the fact that 80% of the money went to EU banks that were Greek bondholders instead of the Greek economy. Here again, the issue was about giving money to the banks that were using Greek bonds as collateral, to insure that they had enough capital on hand. Piecing this together, it’s clear that the Greek situation actually had nothing to do with helping Greece. Forget about Greece’s debt issues, or protests, or even the political decisions… the real story was that the bailouts were all about insuring that the EU banks that were using Greek bonds as collateral were kept whole by any means possible. This is why the current negotiations in Greece boil down to one argument: whether or not it will involve an actual restructuring of Greek debt that will affect bondholders across the board.

Greece wants this. The ECB and EU leaders don’t for the obvious reasons that any haircut of Greek debt that occurs across the board will: 1) Implode a small, but significant amount of EU bank derivatives trades. 2) Be immediately followed by Spain, Italy and ultimately France asking for similar deals… at which point you’re talking about over $3 trillion in high grade collateral being restructured (collateral that is likely backstopping well over $30 trillion in derivatives trades at the large EU banks). Remember, EU banks as a whole are leveraged at 26-to-1. At these leverage levels, even a 4% drop in asset prices wipes out ALL of your capital. And any haircut of Greek, Spanish, Italian and French debt would be a lot more than 4%. The next round of the great crisis is coming. The ECB bought two years of time with its pledge to do “whatever it takes,” but the global bond bubble is still going to burst. And when it does, it’s going to make 2008 look like a joke.

Read more …

“I would willingly, eagerly, accept any terms offered to us if they made sense.”

• Grexit Dangers Mount: Yanis Varoufakis Warns Of ‘Liquidity Asphyxiation’ (AEP)

Greek finance minister Yanis Varoufakis has acknowledged that his country is desperately short of funds, accusing Europe’s creditor powers of trying to force his country to its knees by “liquidity asphyxiation”. “Liquidity is drying up in Greece. It is true,” he told a gathering at the Brookings Institution in Washington. Mr Varoufakis said a conspiracy of forces was trying to “snuff out” Greece’s Syriza government but warned that this could have devastating effects. “Toying with Grexit, or amputating Greece, is profoundly anti-European. Anybody who says they know what will happen if Greece is pushed out of the euro is deluded,” he said.

The warnings were echoed by Eric Rosengren, head of the Boston Federal Reserve, who said Europe risks sitting off uncontrollable contagion if it mishandles the Greek crisis, even though Greece may look too small to matter. “I would say to some European analysts who assume that a Greek exit would not be a problem, people thought that Lehman wouldn’t be a problem. If you measured the size of Lehman relative to the size of the US economy it was quite small,” he told a group at Chatham House. “I wouldn’t be overly confident that just because the Greek economy is small relative to the size of the European economy that something like that wouldn’t be a major dislocation. I think everybody should be a little bit concerned,” he said.

Christine Lagarde said the IMF is worried about the “liquidity situation” in Greece but made it clear that the institution would not give the country any leeway on €1bn of debt repayments coming due in early May. “We have never had an advanced economy asking for payment delays. It is clearly not a course of action that would be fit or recommended,” she said. Mrs Lagarde insisted that the the Fund would defend the interests of its contributors, many of them much poorer countries than Greece. Mr Varoufakis said the ECB and the EMU authorities were deliberately tightening the tourniquet on Greece until the arm was “gangrenous” in order to pressure his Syriza government to give in.

“I would willingly, eagerly, accept any terms offered to us if they made sense. Insisting on a primary budget surplus of 4.5pc in a depressed economy with no functioning banking system is absurd. We have the right to challenge the logic of a programme that has failed,” he said. He was speaking before a reception to celebrate Greek independence at the White House. It is understood that he spoke privately with President Barack Obama, though not at the Oval Office.

Read more …

Greece’s almost nieghbor lives off the fat of the rest of Europe’s land.

• Germany: Has Any Country Ever Had It So Good? (Bloomberg)

How much good news can one country handle? If you work in the German Ministry of Finance—the Bundesfinanzministerium—you might be wondering that at the moment. This morning the average yield on German sovereign debt turned negative for the first time ever. This wasn’t the only good news today. The German economy is built on manufacturing, and it is by far the largest car builder in the euro area. So data released this morning showing that European car sales were up 11% in March, the fastest growth in 15 months, is certainly welcome. That is not to say the German export sector has been waiting on tenterhooks for an increase in European car sales for a boost; Germany has been running a positive trade balance for decades.

Unemployment is at an all-time low, and employment in the economy has never been higher. Which is great for the German economy. Even better, it has the added benefit of a falling currency. Importantly for Germany, it has managed all this without stoking inflation. With this background, it should come as no surprise that Germany is determined (and able) to balance its budget. So no shortage of customers, no shortage of jobs for its citizens, and no shortage of revenue. Has any country ever had it so good? In fact, as projections released by Eurostat this morning show that the only thing Germany is likely to have a shortage of soon is Germans. Germany currently has the lowest proportion of population under the age of 15 of any country in the European Union, and Eurostat’s projections indicate that will continue to be the case for the foreseeable future.

Read more …

“..labour relations, the social security system, the VAT increase and the rationale regarding the development of state property.”

• Greece To Raid Coffers As IMF Dashes Hopes Of Resolving Crisis (Telegraph)

Cash-strapped Greece is planning to resort to drastic measures to stay afloat, as the country’s bail-out drama moves to Washington today. Finance minister Yanis Varoufakis is due to drum up support for his debt-stricken nation when he meets with President Obama at the White House later today. The meeting with the world’s most powerful leader comes as a desperate Athens could raid the country’s pensions funds in order to continue paying out its social security bill. Greece’s deputy finance minister Dimitris Mardas hinted that state-owned enterprises may have to transfer their cash balances to the Bank of Greece if the state was to avoid going bankrupt. The government has long protested it will run out of funds to continue paying out a €1.7bn monthly wage and pension bill if a release of cash is not arranged in the next few days.

With their coffers running dry, Greek officials reportedly made an informal request to delay loan repayments to the IMF, but were rebuffed, according to reports in the Financial Times, However, the Fund’s managing director Christine Lagarde said a moratorium on repayments was “not a course of action that would be fit or recommended”. “We have never had an advanced economy asking for payment delays,” Ms Lagarde said today, adding that any period of clemency would constitute additional financial aid to a debtor economy. “This would mean additional contributions by the international community and some of these countries are in a dearer situation than those seeking the delays,” said Ms Lagarde, who will meet with Mr Varoufakis today. “We will do everything we can so lending to the Fund remains the safest lending route any debtor can adopt.”

Greece came to the brink of falling into an arrears process with its senior creditor last month, but avoided the ignominy of becoming the first developed country to ever fall into an IMF default. The debtor nation, which has received no emergency cash since August 2014, faces a €2.5bn IMF loan bill over May and June. Hinting at the gulf between Greece and its creditors, Greek Prime Minister Alexis Tsipras said “political disagreements” were continuing to block a bail-out extension. Mr Tsipras said there were four areas of disagreement over its reform programme. These were ” labour relations, the social security system, the VAT increase and the rationale regarding the development of state property.” However, the Leftist premier added he was confident Europe would not “choose the path of an unethical and brutal financial blackmail” and ensure Greece remained in the monetary union.

Read more …

They just throw everything out that Greece proposes.

• Greece Deal Appears Distant Amid Deadlock In Reform Talks (Kathimerini)

With negotiations between Greece and its creditors effectively deadlocked, a potential deal that could unlock crucially needed funding appeared more distant than ever on Thursday with doubts appearing about whether an agreement can be reached in time for a Eurogroup planned for May 11, well after the next scheduled eurozone finance ministers’ summit in Riga next Friday, which had been the original deadline. Even representatives of the European Commission, which has been Greece’s closest ally in the talks, appeared to be losing their patience. In comments on Thursday spokesman Margaritis Schinas said the EC was “not satisfied” with the level of progress in talks and called for work to “intensify” ahead of next week’s Eurogroup summit.

Sources indicated that the so-called Brussels Group, comprising officials from the government and Greece’s creditors, was to convene in the Belgian capital on Saturday. But a European official told Kathimerini he had no such information and that talks were likely to resume on Monday. The aim is for that meeting to yield a detailed list of reforms that could form the basis for a staff-level agreement and potentially lead to the disbursement of much-needed aid. But the two sides remain far apart. In a statement to Reuters on Thursday Tsipras highlighted several points of agreement – on areas such as tax collection, corruption and redistributing the tax burden – but also conceded that the two sides disagreed on four major issues: labor rules, pension reform, a hike in value-added taxes and privatizations, which he referred to as “development of state property” rather than asset sales.

Despite the differences and “the cacophony and erratic leaks and statements in recent days from the other side,” Tsipras said he was “firmly optimistic” his government would reach an agreement with its creditors by the end of April. “Because I know that Europe has learned to live through its disagreements, to combine its parts and move forward.” Finance Minister Wolfgang Schaeuble, who has leveled some of the harshest criticism against Greece in recent days, indicated that creditors remained ready to help but expected concessions. “If Greece wants support, we will give this support as in recent years, but of course within the framework of what we agreed,” he told Bloomberg. “Whatever happens, we know that Greece is part of the European Union and that we also have a responsibility for Greece and we will never disregard this solidarity.”

In a speech at the Brookings Institution in Washington on Thursday, Schaeuble said Greece was welcome to seek other sources of funding but might have difficulties. “If you find someone else, whether it’s in Beijing, in Moscow, in Washington DC, or in New York who will lend you money, OK, fine, we would be happy. But it’s difficult to find someone who is lending you in this situation amounts [of] 200 billion euros.” He added that Greece must seek to boost competitiveness and its primary surplus.

Read more …

“The public finances are completely screwed, it can’t go on like this..”

• Finland: ‘Not As Bad As Greece, Yet, But It’s Only Matter Of Time’ (Guardian)

A sudden flurry of spring snow has dusted the steps of an evangelical church in central Oulu, northern Finland, where about 100 people are crowded together for a Friday sermon. But perhaps the true object of their devotion is inside black binliners by the door. Once a week, food parcels and a free meal attract a mix of unemployed men, single mothers and pensioners to the church. The most highly prized items are packs of sausages just within their sell-by date. Shops used to donate meat, but now they too are feeling the pinch. “There is a group of people in Finland that has dropped out of the employment market,” says pastor Risto Wotschke, whose example has encouraged other churches to offer food handouts.

The weakest economy in the eurozone this year might not prove to be Greece or Portugal, but Finland. The Nordic country is entering its fourth year of recession, with output still well below its 2008 peak. The north of Finland, home to the “Oulu miracle” that was built on the twin pillars of plentiful timber and mobile phone technology, has been hit in particular. Although a paper mill still dominates Oulu’s skyline, jobs in pulp and cellulose have moved abroad, while the collapse of Nokia’s handset business knocked the guts out of the local economy. With unemployment officially at more than 17% – almost twice the Finnish average – this once-booming city of 200,000 people has gone from a poster child of prosperity to a symbol of deepening cracks in the Nordic model.

“It’s not yet as bad here as Greece, but that’s only a matter of time,” says Seppo, a 43-year-old software engineer who lost job along with 500 others last summer after Microsoft, the new owner of Nokia’s mobile devices and services division, abandoned Oulu. Seppo, who asked that his full name not be used, has since found work, but it is 375 miles (600km) away. Every Sunday night he leaves his family for a rented room. “The public finances are completely screwed, it can’t go on like this,” he says, as he stands outside a polling booth on the outskirts of Oulu, where people are already queuing to vote early in Finland’s general election on Sunday. “The politicians are promising everything to everybody, but they won’t take any hard decisions until we are in a really deep crisis.”

Read more …

Their markets have dried up.

• China’s Incredible Shrinking Factory (Reuters)

Eight years ago, Pascal Lighting employed about 2,000 workers on a leafy campus in southern China. Today, the Taiwanese light manufacturer has winnowed its workforce to just 200 and leased most of its space to other companies: lamp workshops, a mobile phone maker, a logistics group, a liquor brand. “It used to be as long as you had more orders, you could get everything you needed to expand your factory, and you could expand,” says Johnny Tsai, Pascal’s general manager. No longer. The Chinese factory – an institution that was once so large, it was measured in football fields – is shrinking. Rising labor costs, higher real estate prices, less favorable government policies and smaller order volumes are forcing Chinese plants to downsize just to survive.

Their contraction suggests a new model of light manufacturing emerging from China’s economic slowdown: smaller plants are replacing the vertically integrated behemoths that defined Chinese manufacturing in the early 2000s. Cankun, an appliances factory in southern China featured in the documentary Manufactured Landscapes, had more than 22,000 manufacturing employees in 2005, according to its annual report. Today, that number has shrunk to just 3,000. Some Hong Kong-owned factories in southern China have cut their staff numbers by 50-60%, according to Stanley Lau, chairman of the Federation of Hong Kong Industries. To be sure, the giant Chinese factory is hardly extinct. Taiwan’s Foxconn still employs about 1.3 million people during peak production times, many of them piecing together Apple iPhones.

And factories that can afford to, including Foxconn, are increasing automation. But for industries where the product design changes frequently, such as lighting, robots add little value. Chinese factories’ contraction illustrates how much the advantages they once enjoyed have eroded. In the 1990s and early 2000s, cities in Chinese coastal regions competed to offer investors discounted land. Today, the same land is scarce, and dear. New labor and environmental laws have been introduced, too, making life tougher for employers. And the workforce has changed. China’s working age population began to contract in 2012.

The number of strikes more than doubled last year compared to 2013. Jobs have shifted into the services sector. And labor costs have more than quadrupled in US dollar terms since 2005. Nor are orders what they used to be. On Monday, China announced that export volumes fell 15% in March compared to the same period the year before. China’s manufacturing PMI, which measures activity in the industrial sector, has been hovering around 50, the inflection point between expansion and contraction, for nearly two years.

Read more …

Beijing is playing with pitchforks. From housing bubble to stock bubble to..?

• ‘Beijing Put’ May Be Driving China’s Stock-Market Fever (MarketWatch)

China’s stock markets are climbing to feverish heights as a record number of ordinary Chinese, including teenagers, flood into equities. But in the eyes of many, the share-buying frenzy and wild bull market are all due to one thing: The Chinese government wants it that way. Like the “Greenspan put” of the dot-com era, in which U.S. investors believed then Federal Reserve chairman Alan Greenspan was backstopping the market, Shanghai now seems to be surging on the belief in a “Beijing put.” Although emerging markets have been doing quite well recently — the MSCI EM Index has risen by more than 10% so far this year – the surge in China markets is particularly prominent.

By the close of Thursday trade, the benchmark Shanghai Composite Index was up 30% year-to-date, and it has more than doubled in just the past 10 months. The boom has also spilled over to the nearby Hong Kong equity market, where the city’s benchmark Hang Seng Index has surged nearly 18% since the start of January, while the mainland-China-tracking Hang Seng China Enterprises Index has climbed by 22% over the same period. Emboldened by the astounding advance, an increasing number of ordinary Chinese have joined what the state-run China News Service has called the “great army of stock investors,” lining up outside of brokerage firms to open new trading accounts.

The sharp increase in new investors and market volume has even caused system breakdowns for China Securities Depository and Clearing Corp. (CSDC) — the national clearing house — as well as individual securities firms. Statistics from CSDC show that last week the number of new stock-trading accounts opened hit a fresh all-time high of 1.68 million, beating the previous 1.67 million recorded for the week of March 27. In only the past month, mainland Chinese investors opened more than 6 million such accounts, according to the data. The CSDC said that this “steep rise” in new stock-account applications left it unable for a while on Tuesday to handle the barrage of requests, while Haitong Securities, the second-largest securities firm in the country, also encountered “a system breakdown” the same day, according to a report in the Beijing Youth Daily.

Read more …

For professionals, it’s fish in a barrel. Clean out grandma.

• China’s Smart Money Is Riding the Stock Boom as Amateurs Rush In (Bloomberg)

Individual investors aren’t the only ones pouring cash into Chinese stocks after they surged faster than any other market worldwide. Five of the 11 professional money managers from mainland China, Hong Kong and Taiwan surveyed by Bloomberg from April 8 to 16 said they plan to boost holdings of yuan-denominated A shares this quarter, while four will maintain positions and just two will reduce their stakes. Technology, consumer, health-care and financial shares were preferred industries among the managers, who oversee a combined $41 billion. The responses show the Shanghai Composite Index’s 99% surge over the past year, driven by a record pace of new stock-account openings, still has support outside the Chinese individuals who comprise at least 80% of trading.

Institutional investors are betting that sustained inflows, interest rate cuts and prospects for an improving economy will keep the rally going. “New funds have been continuing to flow into the market and I need to follow the trend,” Dai Ming, a money manager at Hengsheng Asset Management said in Shanghai. “Furthermore, China’s economy will make headway going forward.” Mainland investors have opened a record 10.8 million new stock accounts this year, more than the total number for all of 2012 and 2013 combined, data from China Securities Depository and Clearing show.

The flood of money from these rookie stock pickers has helped feed market momentum after policy makers stepped up efforts to bolster an economy expanding at the slowest pace since the global financial crisis six years ago. The government won’t allow growth to fall below this year’s target of 7%, said Hao Hong, head of China research at Bocom International in Hong Kong, who forecasts at least three more interest-rate cuts in 2015 following reductions in November and March. Premier Li Keqiang said this week that China will accelerate targeted measures to support the economy after it expanded at the slowest pace since 2009 in the first quarter.

Read more …

Yeah, let the no. 1 developer default, see what happens then.

• China’s Kaisa Keeps Creditors Guessing as Dollar Default Looms (Bloomberg)

Kaisa has until Monday to find $52 million for missed payments on two of its dollar bonds as it seeks to avoid default. The troubled developer must pay the interest on its 2017 and 2018 notes that was due on March 18 and March 19 respectively after the expiry of a 30-day grace period. The delay is the latest twist in a saga that has seen Kaisa’s founder Kwok Ying Shing make an unexpected return to the company, projects in Shenzhen blocked, a near default on a loan in December and a takeover offer from Sunac. Standard & Poor’s doesn’t expect Kaisa to pay and downgraded it to default last month. “Kaisa in the last four months has been mysterious and unpredictable, and Kwok coming back is equally surprising,” said Ashley Perrott at UBS. “It wouldn’t be a good signal if they didn’t pay the coupon.”

The mishaps threaten to make Kaisa the first Chinese developer to default on its dollar-denominated bonds as it seeks ways to service interest-bearing debt to onshore and offshore lenders that totaled 65 billion yuan ($10.5 billion) as of Dec. 31. Kaisa has also been tied to a corruption probe amid President Xi Jinping’s crackdown on graft, called the harshest since the 1949 founding of the People’s Republic of China by official Chinese media. Kwok exited the company he founded more than 15 years ago on Dec. 31, citing health reasons. Kaisa said in a Hong Kong stock exchange filing April 13 that he’d been appointed chairman and executive director.

In the interim, Sunac agreed to buy a controlling 49.3% stake from the Kwok family on Jan. 30, subject to a debt restructuring that would require investors to accept lower coupons and defer repayment by up to five years. Kaisa has said offshore creditors would stand to recover just 2.4% in a liquidation. Independent research firm CreditSights said Kwok’s reappointment should boost confidence and may be good news for debt investors, while Citigroup Inc. said he’s likely to regain control of the builder. Sunac Chairman Sun Hongbin said on April 15 his company’s takeover of Kaisa is still proceeding. Kaisa was to pay $16.1 million of interest on its $250 million of 2017 notes on March 18 and $35.5 million on its $800 million of 2018 securities March 19. Given the end of the 30-day grace period falls over a weekend, Kaisa technically has until Monday.

Read more …

Steeled my ass.

• Australia Steeled For China Slowdown As Iron Ore Prices Fall (FT)

The last time Western Australia was engaged in a dispute with Canberra of this magnitude, it threatened to secede during a financial crisis sparked by the 1930s Depression. The current friction is linked to China’s slowdown — a sign of how closely Australia’s fortunes are tied to Beijing’s appetite for its commodity exports. “It’s not secession but it is tension and disengagement,” Colin Barnett, Western Australia’s premier, said this week when Canberra and other states rejected a request to help plug a widening hole in the state budget caused by plunging iron ore prices. Western Australia is a mining state that enjoyed a decade-long boom selling iron ore — a key ingredient in steel — to China. Known by some as “China’s quarry”, the state hosts BHP Billiton, Rio Tinto and Fortescue, which have spent billions of dollars building mines, railways and ports to almost double iron ore production to 717 million tons over the past five years.

But just as global supply hits record levels, China’s economy is slowing and its desire for the reddish-brown ore may have plateaued. Since peaking at US$190 in 2011, iron ore prices have slid more than 70% to about US$50 a ton. This is denting tax revenues, forcing smaller mining companies to close and lay off thousands of employees. “Western Australia was the big beneficiary of the China boom,” says Chris Richardson at Deloitte. “But it is suffering now as the mine construction phase ends and commodity prices fall amid a surge in iron ore supply and faltering demand.” In 2013 the state lost its triple-A credit rating. On Tuesday, Standard & Poor’s warned it may face a further downgrade because of its budget problems.

Western Australia says that if iron ore prices stay at US$50 per ton it would wipe out A$4 billion (US$3 billion) in projected royalty revenues in 2015-16, 12% of the state budget. Unemployment in the state, although still modest at 5.8%, has risen from 3.8% when iron ore prices peaked. House prices have started to fall in the state capital Perth, while they continue to grow in Sydney and Melbourne. Mr Barnett wants other states to give Western Australia a greater share of revenues from a nationwide goods and services tax. But so far Canberra and other states have rejected his pleas. On Friday, state premiers will discuss the dispute. Weak Chinese data are fueling concerns that Western Australia’s problems could spread across a country that has avoided recession for two decades by riding China’s commodities boom.

Read more …

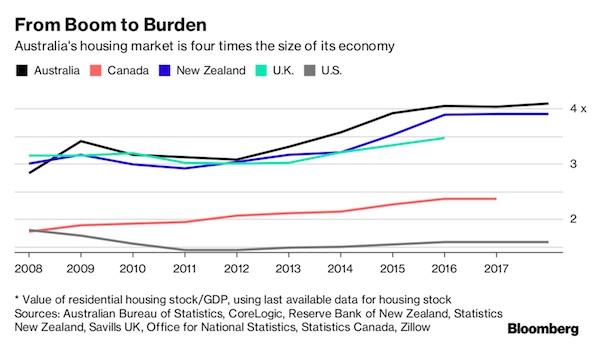

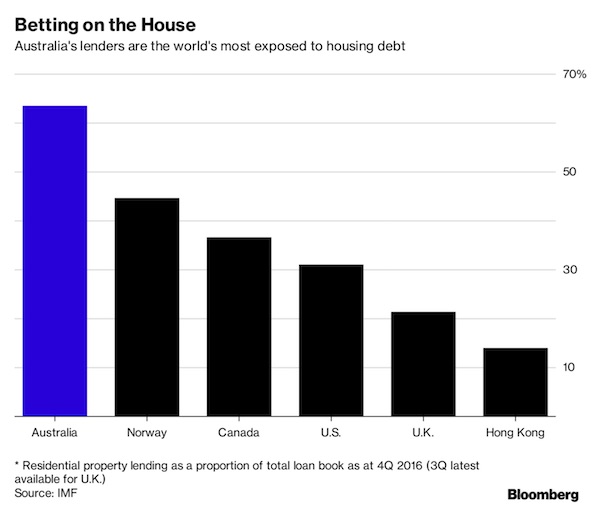

Smart guy. But why doesn’t he know it’s the – Australian-owned – banks that control the country, and they want to continue as is?

• New Zealand Housing: Human Rights Commisioner Calls For Drastic Action (NZH)

New Zealand’s human rights watchdog has added its voice to those calling for drastic action to tackle New Zealand’s housing problems. Chief human rights commissioner David Rutherford said today all political parties should make a cross-party accord to tackle the “very serious” issues of adequate housing in this country. His comments followed a warning by the Reserve Bank this week that Government needed to do more to dampen demand in the face of increasing housing pressures. Mr Rutherford said the housing issues in New Zealand were “many and varied” and there was no co-ordinated plan to address them.

“We’re seeing housing issues being talked about as separate issues when in fact they need to be addressed as a whole: housing affordability in Auckland and Canterbury, the provision of adequate housing in Northland, South Auckland and other places throughout the country, which would reduce the incidence of childhood illnesses due to cold, damp, overcrowded accommodation, and the call for more of our elderly to be cared for in homes which are in many cases likely to be unsuitable for elderly habitation to name just a few of the issues.” He said the human right to adequate housing was a binding legal obligation for the state, which meant the Government had a duty to protect this right and a responsibility to provide remedies.

Mr Rutherford said it would take decades to solve myriad problems but immediate action was needed, beginning with a cross-party accord. “We have had a talkfest about these issues for over 30 years, mainly centred on how many State-owned houses should or should not be built. “In that time, a state like Singapore has surpassed New Zealand in providing adequate housing and that in turn has led to higher levels of wealth and health in Singapore than New Zealand.” The Green Party hailed the Chief Commissioner’s message, saying a lack of action was denying New Zealanders the basic human right of adequate housing. “The Government’s do-nothing approach hasn’t worked,” housing spokesman Kevin Hague said. “It is time for all parties to put their political colours aside and work together to find enduring solutions to the housing crisis.”

Read more …

Politicians want bubbles to keep going.

• New Zealand Government, Central Bank Clash On Housing (CNBC)

Increasing supply is the only way to cool off New Zealand’s red-hot housing market, the country’s deputy prime minister told CNBC, ignoring the central bank’s call for a capital gains tax. Property markets across New Zealand’s major cities are steadily climbing, prompting fears of a sharp correction. Sales volume in March rose to an eight-year high, with median prices in the capital city of Auckland soaring 13% on year, nearly double the nation’s 8% gain, the Real Estate Institute of New Zealand (REINZ) said on Tuesday. New Zealand is one of the few advanced economies that hasn’t experienced a major price correction in the past 45 years. Those statistics prompted an unusually aggressive warning from the Reserve Bank of New Zealand (RBNZ).

In a speech on Wednesday, deputy governor Grant Spencer said he “would like to see fresh consideration of possible policy measures to address the tax-preferred status of housing, especially investor related housing.” That’s a clear reference to a capital gains tax on the sale of investment properties, economists widely agreed. However, Bill English, deputy prime minister & minister of finance of New Zealand, told CNBC on Thursday that he believes increased housing supply is the best way to fix the issue. “We just need more houses on the ground faster to deal with the inflows from migration and the positive attitudes of many New Zealand households in a world of lower interest rates,” adding that the government is going through a deliberate, long and complicated process to improve supply.

But the RBNZ believes supply-side solutions are unlikely to yield quick results, noting that increased supply will take a number of years to eliminate the housing shortage. Waiting that long has severe risks, the bank said: “Rising house price inflation, particularly in Auckland, represents a risk to financial and economic stability. The longer excess demand persists, the further prices will depart from their underlying fundamental determinants and the greater the potential for a disruptive correction.”

Read more …

More revolving doors. They want the Bernank for who he knows, not his brilliant insights.

• 5 Financial Crisis Regulators Cashing In On New Careers (Fortune)

The man who occupied one of the most important economic posts in the U.S. during the financial crisis will soon be collecting his paychecks from one of the largest hedge funds on Wall Street. Former Federal Reserve board chairman Ben Bernanke, who oversaw the country’s central bank from 2006 until last year, will be a senior adviser to Citadel, the hedge fund announced Thursday morning. Founded by billionaire Kenneth Griffin, Citadel manages $25 billion in assets. Bernanke, a former economics professor at Princeton University, left the Fed more than a year ago at which point he was succeeded by current chair Janet Yellen. Bernanke’s new role will find him advising Citadel on global economic and financial matters and monetary policy.

Speaking with The New York Times about his new career path, Bernanke said he had spent the past year scouting job opportunities, and that Citadel represented the prudent choice due to the fact that the asset manager is not regulated by the Fed. Bernanke also told the Times that he is well aware of the public’s poor reception to the so-called “revolving door” that escorts so many Washington regulators to cushy Wall Street positions. That is exactly why he chose Citadel over various banking and lobbying positions he was offered elsewhere in the industry, Bernanke said.

After all, Bernanke’s tenure at the Fed will primarily be remembered for his role helping to engineer the government bailout of the financial industry, as well as for implementing the Fed’s economic stimulus program. As the former Fed chair alluded to, though, Bernanke is far from the only high-profile government employee to have spent the late-2000’s fiscal crisis trying to right the Wall Street ship only to eventually land a lucrative gig in the financial industry. Here are five former regulators from the financial crisis who left the government to make millions.

Read more …

Fascinating read.

• Stephen F. Cohen: U.S./Russia/Ukraine History The Media Won’t Tell You (Salon)

Salon: What is your judgment of Russia’s involvement in Ukraine? In the current situation, the need is for good history and clear language. In a historical perspective, do you consider Russia justified?

Cohen: Well, I can’t think otherwise. I began warning of such a crisis more than 20 years ago, back in the ’90s. I’ve been saying since February of last year [when Viktor Yanukovich was ousted in Kiev] that the 1990s is when everything went wrong between Russia and the United States and Europe. So you need at least that much history, 25 years. But, of course, it begins even earlier. As I’ve said for more than a year, we’re in a new Cold War. We’ve been in one, indeed, for more than a decade. My view [for some time] was that the United States either had not ended the previous Cold War, though Moscow had, or had renewed it in Washington. The Russians simply hadn’t engaged it until recently because it wasn’t affecting them so directly. What’s happened in Ukraine clearly has plunged us not only into a new or renewed—let historians decide that—Cold War, but one that is probably going to be more dangerous than the preceding one for two or three reasons.

The epicenter is not in Berlin this time but in Ukraine, on Russia’s borders, within its own civilization: That’s dangerous. Over the 40-year history of the old Cold War, rules of behavior and recognition of red lines, in addition to the red hotline, were worked out. Now there are no rules. We see this every day—no rules on either side. What galls me the most, there’s no significant opposition in the United States to this new Cold War, whereas in the past there was always an opposition. Even in the White House you could find a presidential aide who had a different opinion, certainly in the State Department, certainly in the Congress. The media were open—the New York Times, the Washington Post—to debate. They no longer are. It’s one hand clapping in our major newspapers and in our broadcast networks. So that’s where we are.

Read more …

“The Hague ruled that the Greek party’s right for reparations remains intact but the capacity to execute that right against German property was rejected..”

• Why A Greek Call For German War Reparations Might Make Sense (MarketWatch)

German officials have dismissed the Greek war reparations claim for Nazi atrocities as a “dumb” attempt to distract from Greece’s looming debt crisis. However, the truth is that a group of Greek citizens, all relatives of people murdered by the Nazis in 1944, have been seeking war reparations from the German government for almost 20 years – and have won rulings in Greek and Italian courts. Germany fought the claims, bringing the case in 2012 all the way to the International Court of The Hague, where the Greek side scored a hollow victory.

The Hague ruled that the Greek party’s right for reparations remains intact but the capacity to execute that right against German property was rejected, due to a legal principle called “sovereign immunity,” which protects one sovereign country from being sued before the court of another country. It is important to note that Germany brought its case against Italy, not Greece, invoking “sovereign immunity.” Germany argued that Italy should not have allowed Greeks to foreclose against property of the German government on Italian soil. Ultimately, The Hague agreed. It ruled in favor of Germany, stating that Italy had in fact violated international law. But the international court never resolved the underlying issue of reparations – it merely issued a judgment on sovereign immunity.

Even as that case was pending in The Hague, Italian Prime Minister Silvio Berlusconi issued a decree that suspended all civil-enforcement procedures against foreign countries on Italian territory. Almost three years have elapsed since the case was closed in The Hague, and as the Greek bailout negotiations continue to drag on and tensions build, the war reparations issue is coming into focus again. Germany’s counterargument has more or less remained the same over the years. Berlin claims the issue was settled in 1960 when West Germany paid 115 million Deutschmarks to Athens in compensation and was finally closed in 1990 with a final settlement, when West and East Germany reunified.

Read more …

It’s about the bottom line. Companies are supposed to be in the way we set them up.

• BP Dropped Green Energy Projects Worth Billions, Prefers Fossil Fuels (Guardian)

BP pumped billions of pounds into low-carbon technology and green energy over a number of decades but gradually retired the programme to focus almost exclusively on its fossil fuel business, the Guardian has established. At one stage the company, whose annual general meeting is in London on Thursday, was spending in-house around $450m (£300m) a year on research alone – the equivalent of $830m today. The energy efficiency programme employed 4,400 research scientists and R&D support staff at bases in Sunbury, Berkshire, and Cleveland, Ohio, among other locations, while $8bn was directly invested over five years in zero- or low-carbon energy. But almost all of the technology was sold off and much of the research locked away in a private corporate archive.

Facing shareholders at its AGM, company executives will insist they are playing a responsible role in a world facing dangerous climate change, not least by supporting arguments for a global carbon price. But the company, which once promised to go “beyond petroleum” will come under fire both inside the meeting and outside from some shareholders and campaigners who argue BP is playing fast and loose with the environment by not making meaningful moves away from fossil fuels. In 2015, BP will spend $20bn on projects worldwide but only a fraction will go into activities other than fossil fuel extraction. An investigation by the Guardian has established that the British oil company is doing far less now on developing low-carbon technologies than it was in the 1980s and early 1990s. Back then it was engaged in a massive internal research and development (R&D) programme into energy efficiency and alternative energy.

Read more …

Jeffrey Brown’s Export Land Model in action.

• Saudi Arabia Adds Half a Bakken to Oil Market in a Month (Bloomberg)

Saudi Arabia boosted crude production to the highest in three decades in March, with a surge equal to half the daily output of the Bakken formation in North Dakota. The kingdom boosted daily crude output by 658,800 barrels in March to an average of 10.294 million, according to data the country communicated to OPEC’s secretariat in Vienna. The Bakken formation, among the fastest-growing shale oil regions in the U.S., pumped 1.1 million barrels a day in February, according to data from the North Dakota Industrial Commission. Oil prices have rallied about 16% in New York this month on stronger fuel demand and as a record decline in U.S. rigs fanned speculation that the nation’s production will slow from its highest pace in three decades.

Prices collapsed almost 50% last year as Saudi Arabia led OPEC in maintaining production in the face of a global glut rather than make way for booming U.S. output. “It confirms the new strategy of the Saudis,” Giovanni Staunovo at UBS said. “If OPEC isn’t balancing the market any more, why should the Saudis hold so much spare capacity when they can use it to make money? Production is still likely to increase in the near term as domestic demand will increase.” In the space of 31 days, Saudi Arabia managed a production boost that took drillers in North Dakota’s Bakken almost 3 years to achieve, according to data compiled by Bloomberg. Output from the Bakken shale increased by about 668,000 barrels a day from February 2012 to December 2014, according to data from the state’s industrial commission.

The increase reflects Saudi Arabia’s own growing requirements rather than an attempt to defend market share, according to Harry Tchilinguirian at BNP Paribas in London. “It’s a big jump in Saudi production but it is commensurate with the increase in their domestic needs,” Tchilinguirian said by e-mail. “Saudi Arabia has made large capacity additions in refining, and they’ll probably want to build up crude stocks before demand from local utilities peaks in the summer.” The output figure for Saudi Arabia is in line with a level of 10.3 million a day announced by Oil Minister Ali Al-Naimi in Riyadh on April 7.

Read more …

“..this year’s death toll has already reached 909, compared with about 50 deaths in the same period in 2014, when Italy’s Mare Nostrum rescue mission was still in effect. That programme has since been replaced by Europe’s Triton, a far less ambitious border patrol..”

• Italy Calls For Help Rescuing Migrants As 40 More Reportedly Drown (Guardian)

Italy has called on the rest of Europe to share the burden of the growing migration crisis in the Mediterranean as news of yet another tragedy emerged, with 41 migrants feared dead after their boat capsized just off the Sicilian coast. Four people survived the disaster, according to witnesses who interviewed them. The demand for Europe-wide action comes just days after 400 people were killed after a boat capsized on its way from Libya, and as the Italian coastguard brought two vessels with an estimated 1,100 rescued migrants on board to Sicily. There were also unconfirmed reports that Italian authorities had arrested 15 people following allegations that 12 migrants had intentionally been killed after a fight broke out on one of the ships.

According to interviews with the four survivors of the most recently capsized boat conducted by the Organisation for Migration (OIM), which follows the issue closely, the inflatable boat left Libya on Sunday with 45 people on board and was at sea for four days when the boat capsized. A spokesperson for OIM said it was likely that the vessel had trouble finding the correct route to Italy, given how long they were at sea. According to the men, who were picked up by the Italian navy vessel Foscari after they were spotted by an aircraft, the boat quickly began losing air forcing the migrants into the water.

Italy’s foreign minister, Paolo Gentiloni, appealed for help in coming to grips with the humanitarian crisis, saying that 90% of the rescue effort in recent weeks had fallen on the Italian navy, which responds to calls for help from migrant boats in international waters close to Libya. “The emergency is not just about Italy,” he said. “We have a duty to save lives and welcome people in a civilised manner, but we also have a duty to seek international engagement.” Another Italian ship, the Fiorillo, arrived in Sicily with about 301 people on board following the rescue of a vessel in distress, and the Dattilo had at least 592 following six separate rescue operations that took place over two days.

Survivors of the disaster earlier this week in which 400 people died said the vessel sank after passengers surged to one side to catch the attention of a passing commercial ship. About 8,500 migrants were rescued in the Mediterranean between Friday and Monday alone. The warm weather and good sea conditions have led to a sharp increase in attempted crossings. According to some estimates, this year’s death toll has already reached 909, compared with about 50 deaths in the same period in 2014, when Italy’s Mare Nostrum rescue mission was still in effect. That programme has since been replaced by Europe’s Triton, a far less ambitious border patrol that monitors incoming vessels within 30 miles of the Italian coast.

Read more …