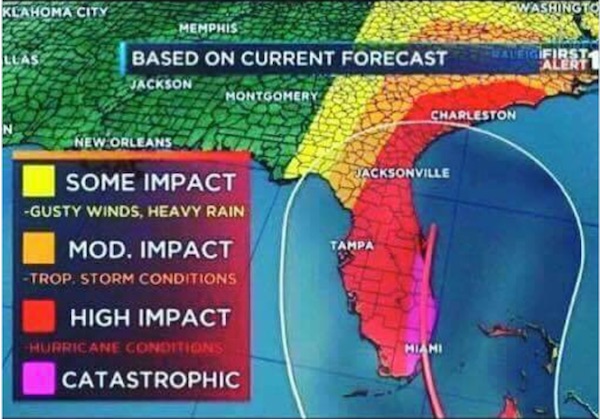

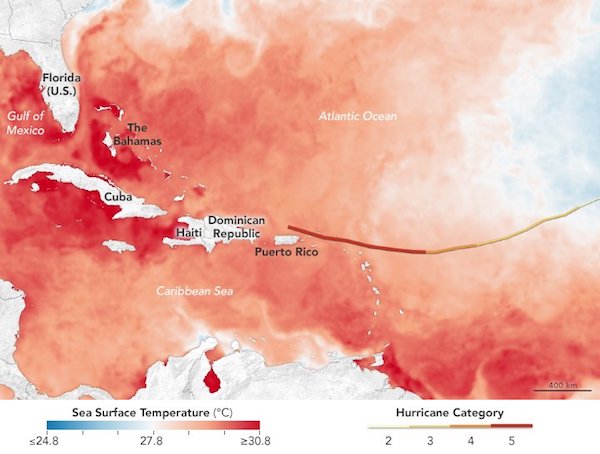

The eye of Hurricane Irma grazed the Turks and Caicos Islands on Thursday, rattling buildings after it smashed a string of Caribbean islands as one of the most powerful Atlantic storms in a century, killing 14 people on its way to Florida. With winds of around 185 miles per hour (290 km per hour), the storm the size of France has ravaged small islands in the northeast Caribbean in recent days, including Barbuda, Saint Martin and the British and U.S. Virgin Islands, ripping down trees and flattening homes and hospitals. Winds dipped on Thursday to 165 mph as Irma soaked the northern coasts of the Dominican Republic and Haiti and brought hurricane-force winds to the Turks and Caicos Islands. It remained an extremely dangerous Category 5 storm, the highest designation by the National Hurricane Center (NHC).

Irma was about 55 miles (85 km) south of Great Inagua Island and is expected to bring 20-foot (6-m) storm surges to the Bahamas, before moving to Cuba and ploughing into southern Florida as a very powerful Category 4 on Sunday, with storm surges and flooding due to begin within the next 48 hours. Across the Caribbean authorities rushed to evacuate tens of thousands of residents and tourists. On islands in its wake, shocked locals tried to comprehend the extent of the devastation while simultaneously preparing for another major hurricane, Jose, now a Category 3 and due to hit the northeastern Caribbean on Saturday.

The quake struck late on Thursday, and was recorded as a magnitude 8.4 on the Richter scale according to Mexico’s National Seismological Service. Government officials said that at least five people died in the country’s south. The US Tsunami Warning Center has cautioned that widespread, devastating tidal waves were possible on Mexico’s coast, as well as in Guatemala, El Salvador, Costa Rica, Nicaragua, Panama, Honduras and Ecuador. Shortly thereafter, authorities reported a tsunami was indeed headed towards the coast, fortunately only 0.7 meters (2.3 feet) tall. While there were no immediate reports of major damage, Mexico’s civil protection agency reported that it was the strongest tremor to hit the country since a 1985 earthquake that killed thousands and destroyed entire buildings.

Its epicenter was about 123 km (76 miles) south of the town of Pijijiapan in Chiapas state, but the shock was felt as far away as Mexico City, sending residents fleeing swaying buildings and knocking out electricity in parts of the city. The quake was also felt in much of Guatemala, which borders Chiapas. Civil Defense officials wrote on Twitter that their personnel were patrolling the streets in Chiapas aiding residents and looking for damage. They also issued a warning for aftershocks, several of which themselves registered a 5.0 magnitude according to the US Geological Survey (USGS). Chiapas Governor Manuel Velasco told broadcaster Televisa some homes had been damaged and a shopping center had collapsed in the town of San Cristobal. “Homes, schools and hospitals have been affected,” Velasco said.

Equifax, as a consumer credit bureau, collects financial, credit, and other data on every US consumer. It has names, birth dates, social security numbers, driver’s license numbers, bank account numbers, credit card numbers, mortgage data, and payment history data, including to utilities, wireless service providers, and the like. It collects data on bank balances, loan balances, credit card balances, credit card purchases, and myriad personal details. It has massive digital dossiers on every consumer in the US and in some other countries. And it sells this data to other companies, such as banks, credit card companies, car dealerships, retailers, and others, as a routine part of its business model. That’s how it makes money. But when someone breaks in and steals this data without paying Equifax for it, well, that’s a huge deal. And it is.

Turns out, Equifax got hacked – um, no, not today. Today it disclosed that it had discovered on July 29 – six weeks ago – that it had been hacked sometime between “mid-May through July,” and that key data on 143 million US consumers was stolen. There was no need to notify consumers right away. They’re screwed anyway. But it gave executives enough time to sell 2 million shares between the discovery of the hack and today, when they crashed 13% in late trading. Given the quantity and sensitivity of the stolen data, it may well be the biggest and worst breach in US history. That stolen data “primarily includes”:• Names • Social Security numbers • Birth dates • Addresses • “In some instances,” driver’s license numbers.

In addition, the stolen data includes: • Credit card numbers of around 209,000 US consumers • “Certain dispute documents with personal identifying information” of around 182,000 US consumers. • “Limited personal information for certain UK and Canadian residents.” This is the kind of information with which identities can be stolen and money can be borrowed in your name. Those data points are the crown jewels for hackers.

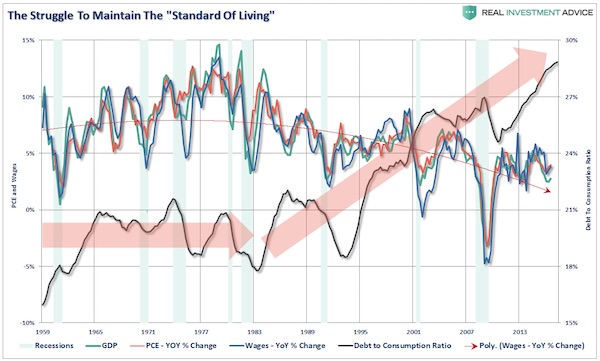

Under more normal circumstances rising consumer credit would mean more consumption. The rise in consumption should, in theory, led to stronger rates of economic growth. I say, in theory, only because the data doesn’t support the claim. Prior to 1980, when the amount of debt used to support consumption was fairly stagnant, the economy, wages, and personal consumption expanded. However, as I noted previously, that all changed with financial deregulation in the early 80’s which fostered three generations of debt driven excesses. In the past, if they wanted to expand their consumption beyond the constraint of incomes they turned to credit in order to leverage their consumptive purchasing power. Steadily declining interest rates and lax lending standards put excess credit in the hands of every American. (Seriously, my dog Jake got a Visa in 1999 with a $5000 credit limit) .

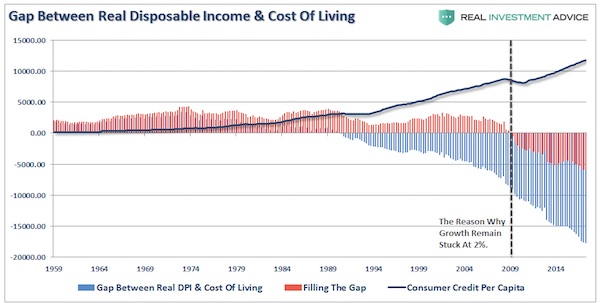

This is why during the 80’s and 90’s, as the ease of credit permeated its way through the system, the standard of living seemingly rose in America even while economic growth rate slowed in America along with incomes. Therefore, as the gap between the “desired” living standard and disposable income expanded it led to a decrease in the personal savings rates and increase in leverage. It is a simple function of math. But the following chart shows why this has likely come to the inevitable conclusion, and why tax cuts and reforms are unlikely to spur higher rates of economic growth.

The continued low interest environment in key markets such as Europe, the U.S. and the U.K. is a “major source of concern”, according to Felix Hufeld, the president of the German financial regulatory authority. Alluding to the results of a recent survey, the authority over which he presides carried out alongside staff at Germany’s central bank, the Bundesbank, Hufeld described the effect on domestic banks. “The impact is massive and is creeping into the balance sheets more and more. The longer it continues, the higher the risk for a change of interest rates is increasing as well,” he warned, speaking from the Handelsblatt annual banking summit in Frankfurt on Thursday. His wariness comes despite his acknowledgment that the banking system has become much more solid than it was 10 years ago when the financial crisis broke out.

“Both the amount as well as the quality of capital has been massively increased. Risk management procedures have been improved, governance procedures have been improved. Remuneration has been curbed – so all sorts of things – a very wide range of things have been done,” he explained before sounding a note of caution. “But one thing should be clear – no regulatory system and no financial market in the world is invulnerable. There can be and there will be new crises coming up somewhere in the future,” Hufeld declared, pointing to real estate as the most notable cause for concern. The BaFin president’s comments echoed those of fellow Handelsblatt summit participants such as Deutsche Bank CEO John Cryan and Goldman Sachs’s CEO Lloyd Blankfein. Cryan joined Hufeld in warning of the possibility of bubbles forming in certain asset classes, adding, “If you look at the higher risk end of the market, I don’t think you get the right reward for the risk you’re taking right now.”

Japan’s economic growth in the second quarter was much slower than seen in a stellar preliminary reading, government data showed on Friday, confounding hopes for a long awaited pick-up in domestic demand. The downgrade was widely expected after data used to revise gross domestic product figures showed capital spending in April-June rose at a slower annual pace than the previous quarter. While the disappointing data may weaken confidence in the government’s economic policies and the business outlook, analysts still expect the economy to sustain a steady recovery as robust global demand underpins exports and a tightening job market improves the prospects for higher wages.

Japan’s economy, the world’s third largest, expanded at an annualized rate of 2.5% in the April-June quarter, less than the initial estimate of annualized 4.0% growth, Cabinet Office data showed. That was also lower than a median market forecast for a revision to a 2.9%. On the quarter, the economy grew a revised 0.6% in real, price-adjusted terms, against a preliminary reading of a 1.0% increase and the median estimate of a 0.7% expansion. Capital expenditure, a key component of GDP, rose 0.5% for the quarter, marked down from the preliminary estimate of a 2.4% increase.

“North Korea has already beaten the world to the punch. They’ve been building up their strategic oil reserves. What that means is they have an estimated year’s worth of held in reserve and China has played a role in these things in the past.” “The area that would be effective for a reactionary measure would be for the United States to exclude the People’s Bank of China, the Industrial and Commercial Bank of China and some of the other major Chinese banks from within the U.S dollar payment systems. The U.S could completely shut down the U.S operations.” “Ultimately, the Chinese are facilitating the North Korean finance. The move would be a kind of sanction with bite behind it. My expectation would be that China wouldn’t necessarily put pressure on North Korea. In reaction we could see escalation of further sanctions from the Chinese against the United States leaving for a trade and financial war without solving the North Korean situation.”

“Currently, North Korea is in what is classified as a ‘break out.’ Under typical nuclear development phases, we’ve normally seen countries that are cheating on nuclear development programs complete their operations in baby steps. In the process they proceed gradually and when they do draw attention will stall programs until beginning again at a later date. North Korea has put that pattern aside and is in complete breakout.” “To give a U.S football comparison, they’re in the red zone and the quarterback is simply about to throw a pass into the end zone. The leader of North Korea is going for it and not hiding anything. The leadership in North Korea is hoping that the United States is bluffing and that they will be able to get a serviceable intercontinental ballistic missile (ICBM) with a hydrogen bomb that could threaten or destroy Los Angeles before the U.S could do anything. The United States is facing a six month window to act and I believe they will.”

Theresa May is poised to make an unprecedented attempt to fix the parliamentary system, allowing her to grab sweeping powers ahead of Brexit, The Independent can reveal. A late-night Commons vote to secure the Conservatives the muscle to use so-called “Henry VIII powers” to make new laws – behind the backs of MPs – will be staged next week. The move has been disguised on the Commons order paper under the innocuous description of “motions relating to House business”, but will be a decisive act in the Brexit process. It will allow the Tories to pack a crucial Commons committee with their own MPs, in defiance of Parliament’s rules, in order to carry out the power grab. To win the vote, the Conservatives will need the backing of the Democratic Unionist Party (DUP), under the much-criticised “cash-for-votes” deal that props up Ms May in power.

Opposition parties immediately accused the Prime Minister of a bid to “sideline Parliament and grant ministers unprecedented powers” – despite promises to restore sovereignty to MPs. “This is an unprecedented power grab by a minority government that lost its moral authority as well as its majority at the general election,” Valerie Vaz, Labour’s Shadow Commons Leader, told The Independent. And Alistair Carmichael, the Liberal Democrat chief whip, said: “The Tories seem determined to ram through their destructive hard Brexit even though they have no mandate for it.” The bid to seize control of the Committee of Selection comes despite unequivocal advice from parliamentary officials that the Tories must not do so, after losing their Commons majority at the election. Without the fix, it would be impossible to force through up to 1,000 “corrections” to EU law as intended through the EU (Withdrawal) Bill – the reason for the accusations of a power grab.

Standing at a Greek site where democracy was conceived, French President Emmanuel Macron called on members of the European Union to reboot the 60-year-old bloc with sweeping political reforms or risk a “slow disintegration.” Macron, on a visit on Thursday to Athens, urged EU nations to carry out six-month national reviews on EU reforms before imposing them — signaling his distance with the German-backed approach based on fiscal discipline within the eurozone. “It would be a mistake to abandon the European ideal,” Macron said. “We must rediscover the enthusiasm that the union was founded upon and change, not with technocrats and not with bureaucracy.” Elected by a landslide in May, the 39-year-old Macron has vowed to back efforts for closer integration in the EU, which has been rattled by a financial crisis, migration issues, a populist backlash and Britain’s decision to leave.

His proposal found enthusiastic support in bailout-stricken Greece, which considers France a vital ally and counterweight to fiscally hawkish Germany in its efforts to ease the stringent terms of its international rescue loans. Reinforcing his message, Macron urged the IMF to step back from its role in European bailouts — breaking with a widely accepted policy adopted when Greece sought international help seven years ago. “I don’t think it was the right method for the IMF to supervise European programs and intervene in the way it did,” he said. “Let’s work within Europe and not turn to outside agencies.” The eurozone rescue fund, the European Stability Mechanism, should play the lead role in financial rescue within the euro currency zone, he said. France, Europe’s No. 2 economy, had previously backed Germany’s insistence in involving the IMF to enforce austerity measures that came with bailout programs in Greece and other rescued economies including Ireland, Portugal and Cyprus.

Asian shares stumbled and the US dollar was on the defensive on Wednesday amid signs investors were becoming spooked by polls narrowing the gap between US presidential nominees Donald Trump and Hillary Clinton. Market anxiety has deepened over a possible Trump victory given uncertainty on the Republican candidate’s stance on issues including foreign policy, trade relations and immigration, while Clinton is viewed as a candidate of the status quo. Stocks across Asia Pacific saw a broad selloff on Wednesday with the Nikkei in Japan down by 1.8% at 4am GMT. There were also steep falls in Australia where the ASX/S&P 200 benchmark index was down almost 1.5%, with falls of 1.3% in South Korea and Hong Kong as markets took a lead from a sharp drop on Wall Street overnight.

The main European markets were also expected to begin the day in the red when they open later, according to futures trading. The tumultuous presidential race appeared to tighten after news that the FBI was reviewing more emails as part of a probe into Clinton’s use of a private email server. While Clinton held a five-percentage-point lead over Trump, according to a Reuters/Ipsos opinion poll released on Monday, other polls showed Trump ahead by 1-2 %age points. That pushed the US S&P500 Index down to a four-month closing low on Tuesday. The CBOE volatility index, often seen as an investors’ fear gauge, briefly rose to a two-month high, above 20%.

In the currency market, traders sold the dollar partly as they suspect Trump would prefer a weaker dollar given his protectionist stance on international trade. The euro rose to a three-week high of $1.1069, up about 2% from its seven-and-a-half-month low of $1.0851 hit just over a week ago. Against the yen, the dollar slipped to 104.03 yen from three-month high of 105.54 yen set on Friday. Koichi Yoshikawa at Standard Chartered Bank said: “If you had a long dollar position on the view that the dollar would gain because Clinton would win, you would surely close that position because her victory is less certain.”

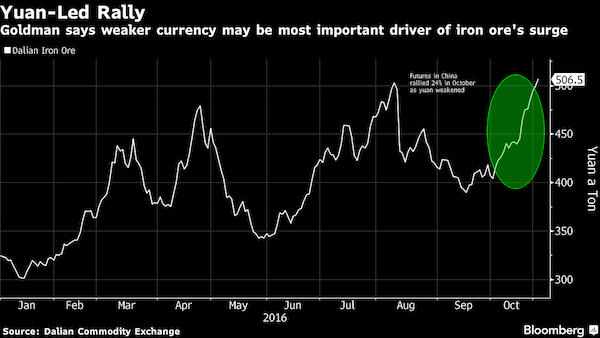

Iron ore’s eye-catching rally to the highest since April is probably due to the weakening of the yuan, according to Goldman Sachs, which said that China’s currency may decline further against the dollar and help to sustain prices of the raw material. Prices surged last month as losses in the yuan prompted some local investors to move into dollar-linked assets, including iron ore, analysts Hui Shan, Amber Cai and Christian Lelong said in a report received Wednesday. Should the Federal Reserve raise interest rates by the end of the year, there’s scope for further yuan weakness, they wrote in the Nov. 1 note. Iron ore has rallied even as signs of robust supply multiply, including a buildup in stockpiles at ports in China.

While some analysts have sought to explain the jump by pointing to higher coal prices as a driver, Goldman said that didn’t stack up as a reason, targeting the yuan’s drop instead. The Chinese currency has sagged as local policy makers signaled they are willing to allow greater currency flexibility amid a slump in exports and rise in the dollar. “By our estimates, about 60% of the iron ore price rally in October can be explained by the yuan depreciation,” the analysts said. Iron ore may be the first in line to benefit from onshore investment flows into commodities as the “futures curve is almost always backwardated, making long iron ore a positive-carry trade,” they said, referring to bets on gains.

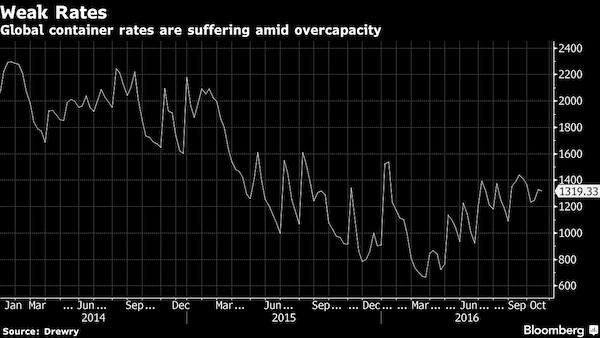

A.P. Moller-Maersk, owner of the world’s largest container line, reported a 43% decline in third-quarter profit as the shipping industry suffers from overcapacity. Net income fell to $429 million in the third quarter compared with $755 million in the same period a year earlier, the Copenhagen-based company said in a statement Wednesday. That missed the average estimate of $501 million in a Bloomberg survey of 15 analysts. “The result is unsatisfactory, but driven by low prices,” Chief Executive Officer Soren Skou said in the statement. “We generally perform strongly on cost and volume across businesses.” Maersk said its underlying profit for 2016 will be “below” $1 billion. Previously, the company had said the full-year result would be “significantly” below 2015’s $3.1 billion.

An excess of vessels and weak trade growth have driven container lines to try to under-bid each other on the rates they offer clients. The climate has proven lethal for some industry members, with South Korea’s biggest line Hanjin Shipping Co. filing for bankruptcy protection in August. Earlier this week, Japan’s three biggest container lines said they plan to merge their operations in an efforts to return to profit. Maersk’s response has been to cut costs. On Wednesday it said costs at Maersk Line declined 14% in the quarter, but that was outpaced by a 16% decline in freight rates. The shipping line reported a net operating loss after tax of $116 million compared with a profit by the same measure of $264 million a year earlier as freight rates fell 16%.

At law courts throughout Greece, people are lining up to file papers renouncing their inheritance. Not necessarily because some feckless uncle left them with a pile of debt at the end of his revels; they are turning their backs on what used to be a pillar of Greece’s economy and society: real estate. Growing personal debt, declining incomes and ever higher taxes as Greece’s depression grinds on have turned property and the dream of easy money into dread of a catastrophic burden. The figures are clear. In 2013, two years after a property tax was introduced (previously, real estate tax revenue came mainly from transfers or conveyance taxes), 29,200 people declined to accept their inheritance, according to the Justice Ministry. In 2015, the number had climbed to 45,627, an increase of 56% in two years.

Reports from across the country suggest that this year, too, large numbers of people are refusing to inherit. “This can be very painful,” said Giorgos Voukelatos, a lawyer. “People may lose their family home. Because if the father or mother had debts, the child might be unemployed and unable to carry this weight as well.” The growing aversion to property is evident in the drop in business at notaries public. The national statistics service, Elstat, reported in July that in 2014 there were 23,221 deeds in which living parents transferred property to their children, down from 90,718 in 2008. The number of wills drawn up or notarized has been steady through the crisis, at around 30,000 annually, suggesting that many inheritances being rejected were not part of formal wills. (More than 120,000 people die each year.)

The desire to inherit used to be so great that some took it upon themselves to give fortune a hand. Greeks were stunned in 1987 when the police uncovered a gang that had killed at least eight rich elderly people after forging their wills. The plot’s leader was a lawyer and former mayor of an Athens suburb; accomplices included a notary public and a gravedigger. Murder Inc., as the news media called it, was seared into popular consciousness as an instance in which criminals acted out a common desire. Today, people are more likely to run away from real estate than be tempted to kill for it.

The collapse of the real estate market shows why. The total number of transactions dropped by 74% from 2004 to 2014. People once hoped that if they came into property they could sell it and live easier; now they fear that they will be unable to sell it and the taxes will drag them down. If they did find a buyer, they would be unlikely to gain much, as prices of apartments have fallen by 41% since 2008, according to the Bank of Greece. Construction of homes has collapsed, dropping by 95% from 2007 to 2016. With no end to the crisis in sight, people will continue to dread coming into property.

We don’t know whether the reopening of the FBI probe of Hillary Clinton’s emails will cost her the election. It may be that she will still emerge the winner after next Tuesday’s vote, or that Donald Trump’s momentum from the Wikileaks emails, Obamacare’s failures, and Clinton’s flawed candidacy were going to carry him to victory in any case. What we do know is that whoever wins, we are in for a fiasco in politics that will make even this fiasco of a campaign pale by comparison. There is hardly any scenario that is too far-fetched. Even if the polls are right and Clinton’s lead translates into an electoral victory, she will be so damaged going into office that her chances of getting anything done will be virtually nil. In this sense alone, Trump’s claim that this scandal is “worse than Watergate” could prove to be true.

As an incumbent, Richard Nixon at least had an administration in place when he won re-election in 1972, though it took nearly another two years before he was forced to resign under threat of impeachment. Clinton is likely to be stymied from the start, especially if the ongoing investigations into her email practices and the Clinton Foundation lead to further damaging disclosures. For one thing, we now have the precedence of Watergate, and Republicans, who are sure to retain the House and now probably the Senate, will not let go. There is hardly a chance that it will all end well for Clinton and that she will be exonerated because what is already known has many Republicans convinced that she is guilty at the very least of mishandling classified documents and perhaps obstruction of justice.

While the immediate attention in the wake of last week’s disclosure about reopening the email investigation has focused on FBI Director James Comey, the real conundrum in all this concerns his boss, Attorney General Loretta Lynch. Lynch fatally compromised her position by meeting with former President Bill Clinton just days before the original investigation was closed without a grand jury ever considering the evidence. And now her failure to block Comey’s disclosure — while leaking that she wanted to — is another ethical lapse. Other reports indicate that she attempted to quash the investigation into the Clinton Foundation. It is hard to see how she can remain in office even if Clinton wins and wants to keep her. Her resignation — or even impeachment — seems inevitable with Republicans out for blood.

The damage done to the whole Clinton entourage through the machinations exposed in the Wikileaks emails means that many of them – Huma Abedin, Cheryl Mills, John Podesta, Neera Tanden – will be virtually untenable in any position of responsibility in a new Clinton administration. And this is the best-case scenario for Clinton. We all know what the worst-case scenario is.

Hilarious. 370 economists making Trump’s case for him: “The economists object to Mr. Trump for questioning the legitimacy of economic data produced by institutions such as the Bureau of Labor Statistics.” Everybody questions the BLS. Except for 370 economists?!

A group of 370 economists, including eight Nobel laureates in economics, have signed a letter warning against the election of Republican nominee Donald Trump, calling him a “dangerous, destructive choice” for the country. Signatories include economists Angus Deaton of Princeton University, who won the economics Nobel last year, and Oliver Hart of Harvard University, who was one of the two Nobel winners this year. The letter is notable because it is less partisan or ideological than such quadrennial exercises, and instead takes issue with Mr. Trump’s history of promoting debunked falsehoods.

“He misinforms the electorate, degrades trust in public institutions with conspiracy theories and promotes willful delusion over engagement with reality,” said the signatories, which also include Paul Romer, the new chief economist at the World Bank, and Kenneth Arrow, the 1972 Nobel winner. The economists object to Mr. Trump for questioning the legitimacy of economic data produced by institutions such as the Bureau of Labor Statistics. They say he hasn’t proposed credible solutions to reduce budget deficits and that he has promoted misleading claims about trade and tax policy. They also chide Mr. Trump for failing to “listen to credible experts” and for promoting “magical thinking and conspiracy theories over sober assessments of feasible economic policy options.”

[..] Peter Navarro, a Trump adviser and professor at the University of California, Irvine, said the economics profession has been so wrong about the impact of trade deals, including both the North American Free Trade Agreement in 1994 and the accession of China to the World Trade Organization in 2001, that it has little standing to criticize Mr. Trump’s position on those pacts. Tuesday’s letter “is a headline, whatever, and then they wind up being just so horribly wrong,” Mr. Navarro said. “You shouldn’t believe economists or Nobel Prize winners on trade.”

“You don’t need a Ph.D. in economics to know Trump’s plan to cut taxes, reduce regulation, increase oil, gas, and clean coal production, and eliminate our trade deficit by increasing exports and reducing imports will significantly increase growth, boost wages and generate trillions in new tax revenues,” he said. “This new letter is an embarrassment to an economics profession which continues to insist bad trade deals are good for America—a classic case of reality running roughshod over textbook trade theory.”

“Not only was Bill Clinton’s wife under an FBI investigation at the time [..] but his own charitable foundation was also under investigation, a fact that was unknown at the time to the public and the media.

Current and former FBI officials have launched a media counter-offensive to engage head to head with the Clinton media machine and to throw off the shackles the Loretta Lynch Justice Department has used to stymie their multiple investigations into the Clinton pay-to-play network. Over the past weekend, former FBI Assistant Director and current CNN Senior Law Enforcement Analyst Tom Fuentes told viewers that “the FBI has an intensive investigation ongoing into the Clinton Foundation.” He said he had received this information from “senior officials” at the FBI, “several of them, in and out of the Bureau.” That information was further supported by an in-depth article in the Wall Street Journal by Devlin Barrett. According to Barrett, the “probe of the foundation began more than a year ago to determine whether financial crimes or influence peddling occurred related to the charity.”

Barrett’s article suggests that the Justice Department, which oversees the FBI, has attempted to circumvent the investigation. The new revelations lead to the appearance of wrongdoing on the part of U.S. Attorney General Loretta Lynch for secretly meeting with Bill Clinton on her plane on the tarmac of Phoenix Sky Harbor International Airport on the evening of June 28 of this year. Not only was Bill Clinton’s wife under an FBI investigation at the time over her use of a private email server in the basement of her New York home over which Top Secret material was transmitted while she was Secretary of State but his own charitable foundation was also under investigation, a fact that was unknown at the time to the public and the media.

The reports leaking out of the FBI over the weekend came on the heels of FBI Director James Comey sending a letter to members of Congress on Friday acknowledging that the investigation into the Hillary Clinton email server was not closed as he had previously testified to Congress, but had been reopened as a result of “pertinent” emails turning up.

The Daily Mail reoprts on ‘persons of interest’: Huma Abedin, Terry McAuliffe, Cheryl Mills, Phillipe Reines, John Podesta, Tony Podesta, Doug Band, Justin Cooper, Anthony Weiner

The extent to which Hillary Clinton’s key advisers are now the focus of major FBI investigations is becoming clear. The Clintons’ long-term inner-circle – some of whom stretch back in service to the very first days of Bill’s White House – are being examined in at least five separate investigations. The scale of the FBI’s interest in some of America’s most powerful political fixers – one of them a sitting governor – underlines just how difficult it will be for Clinton to shake off the taint of scandal if she enters the White House. There are, in fact, not one but five separate FBI investigations which involve members of Clinton’s inner circle or their closest relatives – the people at the center of what has come to be known as Clintonworld.

The five known investigations are into: Anthony Weiner, Huma Abedin’s estranged husband sexting a 15-year-old; the handling of classified material by Clinton and her staff on her private email server; questions over whether the Clinton Foundation was used as a front for influence-peddling; whether the Virginia governor broke laws about foreign donations; and whether Hillary’s campaign chairman’s brother did the same. The progress of the Clinton Foundation investigation and that into McAuliffe was first reported by the Wall Street Journal. The FBI does not generally comment on investigations, so it is entirely possible there are more under way. Here are the advisers and consiglieri – and how the FBI is looking at them:

The Justice Department official in charge of informing Congress about the newly reactivated Hillary Clinton email probe is a political appointee and former private-practice lawyer who kept Clinton Campaign Chairman John Podesta “out of jail,” lobbied for a tax cheat later pardoned by President Bill Clinton and led the effort to confirm Attorney General Loretta Lynch. Peter Kadzik, who was confirmed as assistant attorney general for legislative affairs in June 2014, represented Podesta in 1998 when independent counsel Kenneth Starr was investigating Podesta for his possible role in helping ex-Bill Clinton intern and mistress Monica Lewinsky land a job at the United Nations.

“Fantastic lawyer. Kept me out of jail,” Podesta wrote on Sept. 8, 2008 to Obama aide Cassandra Butts, according to emails hacked from Podesta’s Gmail account and posted by WikiLeaks. Kadzik’s name has surfaced multiple times in regard to the FBI’s investigation of Democratic presidential nominee Hillary Clinton for using a private, homebrewed server. After FBI Director James Comey informed Congress on Thursday the FBI was reviving its inquiry when new evidence linked to a separate investigation was discovered, congressional leaders wrote to the Department of Justice seeking more information. Kadzik replied. “We assure you that the Department will continue to work closely with the FBI and together, dedicate all necessary resources and take appropriate steps as expeditiously as possible,” Kadzik wrote on Oct. 31.

Hillary Clinton began her presidential campaign by promising to do what it takes to rein in Wall Street. Boosted by Wall Street’s toughest critics, U.S. senators Bernie Sanders and Elizabeth Warren, the Democratic candidate has declared “the deck is still stacked in favor of those at the top” and said she would raise bank fees and tighten banking regulations. She has encouraged regulators to break up too-risky banks. And yet, Wall Street appears unperturbed by the prospect of a Clinton presidency. In fact, the banking industry has supported Clinton with buckets of cash and stocks have sold off on days when the Clinton campaign stumbles. Privately, bankers say that they trust her to remain a pragmatist who will keep the current regulatory regime laid down by the Dodd-Frank Wall Street reform legislation passed in 2010.

“I don’t think Clinton wakes up thinking about Wall Street,” one senior banking industry lobbyist said. There are hints in apparently leaked email discussions among Clinton’s campaign staff that bankers are not far off the mark when they count on her to tread lightly. Pressed during the campaign by progressive Democrats to call for a revival of the Glass-Steagall Act that would require separation of commercial and investment banking, Clinton ultimately refused. She also weighed another progressive favorite – a tax on financial transactions- but instead recommended a far narrower plan to tax only canceled orders by high speed traders. Ultimately, what bankers most like about Clinton is that she is not Donald Trump.

Many financiers fear her unorthodox Republican rival could disrupt global trade, damage geopolitical relationships and rattle markets, industry analysts and participants say. “Those are the kind of things that corner offices think about,” said Karen Shaw Petrou of Federal Financial Analytics, whose firm advises financial firms about U.S. regulatory policy. “The overriding concern about Trump has dominated people’s thinking.” [..] People who work for hedge funds and private equity firms have contributed more than $56 million to Clinton’s presidential campaign and the supporting groups that face no legal cap on donations. Trump’s campaign and related groups received just $243,000 from donors in the same sector, according to data from the Center for Responsive Politics.

Aren’t you surprised that Hillary and the presstitutes haven’t blamed Putin for FBI director Comey’s reopening of the Hillary email case? But the presstitutes have done the next best thing for Hillary. They have made Comey the issue, not Hillary. According to US Senator Harry Reid and the presstitutes, we don’t need to worry about Hillary’s crimes. After all, she is only a political woman feathering her nest, just as political men have done for ages. Why all this misogynist talk about Hillary? The presstitutes’ cry is that Comey’s alleged crime is far more important. This woman-hating Republican violated the Hatch Act by telling Congress that the investigation he said was closed is now reopened. A very strange interpretation of the Hatch Act. During an election it is OK to announce that a candidate for president is cleared but it is not OK to say that a candidate is under investigation.

In July 2016 Comey violated the Hatch Act when he, on orders from the corrupt Obama Attorney General, announced Hillary clean. In so doing, Comey used the prestige of federal clearance of Hillary’s violation of national security protocols to boost her standing in the election polls. Actually, Hillary’s standing in the polls is based on the pollsters over-weighting Hillary supporters in the polls. It is easy to produce a favorite if you overweight their supporters in the poll questions. If you look at the crowds attending the two candidate’s public appearances, it is clear that the American people prefer Donald Trump, who is opposed to war with Russia and China. War with nuclear powers is the big issue of the election.

Hillary’s problem has the ruling American Oligarcy, for which Hillary is the total servant, concerned. What are they going to do about Trump if he wins? Will his fate be the same as John F. Kennedy, Robert Kennedy, Martin Luther King, George Wallace? Time will tell. Or will a hotel maid appear at the last minute in the way that the Oligarchy got rid of Dominique Strauss-Kahn? All of the American and Western feminists, progressives, and left-wing remnant fell for the obvious frame-up of Strauss-Kahn. After Strauss-Kahn was blocked from the presidency of France and resigned as Director of the IMF, the New York authorities had to drop all charges against Strauss-Kahn. But Washington succeeded in removing Strauss-Kahn as a challenge to its French vassal, Sarkozy.

If I had cornflakes for breakfast (which I don’t), I would have choked on them, reading Andrew Parker’s view of the threat posed by Russia, not just to the world at large – that is a commonplace of the “new cold war” discourse – but to the stability of the UK. With the majority vote for Brexit against the strong preference of Scotland and Northern Ireland for remain, we have shown ourselves quite capable of inflicting potentially fatal harm to our national stability all by ourselves. Why would we need Russia to do it for us? That was a knee-jerk reaction to the main thrust of the MI5 chief’s first national newspaper interview in the agency’s history. But a second, more substantial, response chased behind it in the form of a rather basic, and recurrent, question.

Why is the UK establishment in general, and UK intelligence in particular, so fixated on a supposed threat from Russia? The cold war is a quarter-century behind us. The Warsaw Pact was dissolved; the Soviet Union collapsed. Today’s Russia has three quarters of the territory but only half the population of the old Soviet Union. Its GDP, whether overall or per capita, is far below that of the US, or ours. Its 2015 military budget took 5% of that – $70bn in actual money – less than an eighth of the nearly $600bn spent by the US. “Tsar” Vladimir Putin may have played a weak hand magnificently, as judged by admirers and detractors alike, but a weak hand is still a weak hand.

If Russia really harbours ambitions to reconstitute an empire, its only success to date is the expensive (in every respect) reacquisition of Crimea, a contested no-man’s land of ragtag rebels in the rust belt of eastern Ukraine, and two miniature enclaves inside independent Georgia. That recent “show of force”, when the might of the Russian navy made its stately progress through the English Channel, demonstrated only the obsolescence of the erstwhile superpower’s fleet. In the same interview, Parker disclosed that there were around 3,000 “violent Islamic extremists in the UK, mostly British”, and that cyber, not just in Russia’s hands, was the threat of the future. So let me repeat the question: why does Russia remain bogeyman-in-chief?

Here are a few ideas. The first is that blaming Russia carries little cost. Russia is not China. Investment is not a big consideration. For all sorts of reasons, political relations have long been dire. Applying the same virulent rhetoric to terrorism conducted in the name of Islam, on the other hand, risks fomenting social and cultural strife here at home. A second reason, now as in the past, is that blaming Russia aligns us comfortably with the US, where stalwarts in Congress and at the Pentagon have never emerged from their old thinking about the threat. The Russia card has been played to exhaustion during this presidential campaign, to the point where it could swing the election – and I don’t mean in Donald Trump’s favour. A third factor is the consensus about a strong and malevolent Russia that still rules the “expert” community, and will probably do so for a few years yet – helped along by the hatchet-faced Putin.

The reputation of central banks has always had its ups and downs. For years, central banks’ prestige has been almost unprecedentedly high. But a correction now seems inevitable, with central-bank independence becoming a key casualty. Central banks’ reputation reached a peak before and at the turn of the century, thanks to the so-called Great Moderation. Low and stable inflation, sustained growth, and high employment led many to view central banks as a kind of master of the universe, able – and expected – to manage the economy for the benefit of all. The depiction of US Federal Reserve Chair Alan Greenspan as “Maestro” exemplified this perception. The 2008 global financial crisis initially bolstered central banks’ reputation further.

With resolute action, monetary authorities made a major contribution to preventing a repeat of the Great Depression. They were, yet again, lauded as saviors of the world economy. But central banks’ successes fueled excessively high expectations, which encouraged most policymakers to leave their monetary counterparts largely responsible for macroeconomic management. Such “expectational” and, in turn, “operational” overburdening has exposed monetary policy’s true limitations. In other words, central banks’ good reputation now seems to be backfiring. And “personality overburdening” – when trust in the success of monetary policy is concentrated on the person at the helm of the institution – means that individual leaders’ reputations are likely to suffer as well.

Yet central banks cannot simply abandon their new operational burdens, particularly with regard to financial stability, which, as the 2008 crisis starkly demonstrated, cannot be maintained by price stability alone. On the contrary, a period of low and stable interest rates may even foster financial fragility, leading to a “Minsky moment,” when asset values suddenly collapse, bringing down the whole system. The limits of inflation targeting are now clear, and the strategy should be discarded. Central banks now have to reconcile the need to maintain price stability with the responsibility – regardless of whether it is legally mandated – to reduce financial vulnerability. This will not be easy, not least because of another new operational burden that has been placed on many central banks: macro-prudential and micro-prudential supervision.

Managing Britain’s exit from the EU is such a formidable and complex challenge that it could overwhelm politicians and civil servants for years, senior academics have warned. Theresa May has announced she will trigger article 50 – the two-year process of negotiating a separation from the EU – by the end of March next year. The government will also publish a great repeal bill, which will transfer all EU-originated laws into British law, so that MPs can decide how much they want to discard. A report from The UK in a Changing Europe, an independent group of academics led by Prof Anand Menon of King’s College London, warns that this will only be the start of the process of extricating Britain from the EU and establishing new relationships with other member states.

“Brexit has the potential to test the UK’s constitutional settlement, legal framework, political process and bureaucratic capacities to their limits – and possibly beyond,” Menon said. The group of experts, commissioned by the Political Studies Association, found that identifying and transposing the legislation to be included in the great repeal bill – and then deciding what to keep and what to ditch – will be a daunting task for civil servants. They also warn that while article 50, as set out in the Lisbon treaty, concerns the terms of a divorce with the rest of the EU – including what share of EU liabilities the UK should take on, for example – it is unclear whether the process can allow for parallel negotiations on Britain’s future status. And they suggest the repatriation of decision-making in key policy areas including agriculture, the environment and higher education to Britain from Brussels could affect the balance of power between Westminster and the devolved parliaments – another major constitutional headache for politicians.

Several damaging Los Angeles-area earthquakes of the 1920s and 1930s, including the deadliest ever in southern California, may have been brought on by oil production during the region’s drilling boom of that era, US government scientists have reported. The findings of a possible link between oil extraction and seismic events in the LA basin do not apply to modern industry practices but suggest the natural rate of quake occurrences in the region may be lower than previously calculated, the scientists said. The study’s authors, Susan Hough and Morgan Page of the US Geological Survey, stressed a distinction between their results and separate research attributing a growing frequency of quakes in Oklahoma and elsewhere to underground wastewater injection associated with fossil fuel production.

The new study, published in the Bulletin of the Seismological Society of America, also noted that early 20th-century industry techniques differed greatly from today, so the findings “do not necessarily imply a high likelihood of induced earthquakes at the present time”. The report suggested four major Los Angeles-area quakes in 1920, 1929, 1930 and 1933 were triggered by early drilling methods in which oil was extracted without water being pumped into the ground to replace it, causing the ground to subside. This could have artificially placed more pressure on seismic faults near oilfields. The most devastating event was the so-called Long Beach earthquake of 10 March 1933, a 6.4-magnitude quake that ruptured the Newport-Inglewood fault along the coast, toppling scores of buildings and killing 115 to 120 people – the highest death toll on record from a southern California earthquake.

Turkey’s prime minister said he had no regard for Europe’s “red line” on press freedom on Tuesday and warned Ankara would not be brought to heel with threats, rejecting criticism of the detention of senior journalists at an opposition newspaper. Police detained the editor and top staff of Cumhuriyet, a pillar of the country’s secularist establishment, on Monday, on accusations that the newspaper’s coverage had helped precipitate a failed military coup in July. The United States and European Union both voiced concern about the move in Turkey, a NATO ally which aspires to EU membership. European Parliament President Martin Schulz wrote on Twitter that the detentions marked the crossing of ‘yet another red-line’ against freedom of expression in the country.

“Brother, we don’t care about your red line. It’s the people who draw the red line. What importance does your line have,” Prime Minister Binali Yildirim told members of his ruling AK Party in a speech in parliament. “Turkey is not a country to be brought in line with salvoes and threats. Turkey gets its power from the people and would be held accountable by the people.” Prosecutors accuse staff at Cumhuriyet, one of few media outlets still critical of President Tayyip Erdogan, of committing crimes on behalf of Kurdish militants and the network of Fethullah Gulen, a U.S.-based cleric blamed for orchestrating the July coup attempt. Journalists at the paper were suspected of seeking to precipitate the coup through “subliminal messages” in their columns before it happened, the state-run Anadolu agency said.

You may own your car, but you don’t own the software that makes it work— that still belongs to your car’s manufacturer. You’re allowed to use the software, but in the past, trying to alter it in any way (including fixing it by yourself when it breaks or patching security holes) was a form of copyright infringement. iFixit, Repair.org, the Electronic Frontier Foundation (EFF), and many others think this is ridiculous, and they’ve been lobbying the government to try to change things. A year ago, the U.S. Copyright Office agreed that people should be able to modify the software that runs cars that they own, and as of last Friday, that ruling came into effect. It’s good for only two years, though, so get hacking. The legal and technical distinction between physical ownership and digital ownership is perhaps most familiar in the context of DVD movies.

You can go to the store and buy a DVD, and when you do, you own that DVD. You don’t, however, own the movie that comes on it: Instead, it’s more like you own limited rights to watch the movie, which is a very different thing. If the DVD is protected by Digital Rights Management (DRM) software, the Digital Millennium Copyright Act (DMCA) says that you are not allowed to circumvent that software, even if you’re just trying to watch the movie on a different device, change the region restriction so that you can watch it in a different country, or do any number of other things that it really seems like you should be able to do with a piece of media that you paid 20 bucks for.

Cars work in a similar way. You own the car as a physical object, but you only have limited rights to the software that controls it, because the car’s manufacturer holds the copyright on that software. This prevents you from making changes to the software, even if those changes are to fix problems or counter obsolescence, as well as preventing you from investigating the security of the software, which can have very serious and direct consequences for you as the owner and driver. It’s also worth pointing out that (especially in older vehicles like the 1995 Volvo 940 Turbo belonging to a certain anonymous journalist) relatively simple computerized parts can cost a ridiculous amount of money to replace because there is no legal alternative besides buying a new one from the manufacturer, who hasn’t made them in 20 years and would much rather you just bought an entirely new car anyway.

Oil prices plunged on Monday after the world’s top producers failed to reach an agreement on capping output aimed at easing a global supply glut during a meeting in Doha. Hopes the world’s main producer cartel, OPEC, and other major exporters like Russia would agree to freeze output has helped scrape oil prices off the 13-year lows they touched in February. But crude tanked after top producer Saudi Arabia walked away from the talks, which many hoped would ease a huge surplus in world supplies, because of a boycott by its rival Iran. Oil tumbled in early Asian trade after the collapse of Sunday’s talks, with prices dropping as much as seven% in opening deals.

At around 0100 GMT, US benchmark West Texas Intermediate for May delivery was down $2.11, or 5.23%, from Friday’s close at $38.25 a barrel. Global benchmark Brent crude for June lost 4.71%, or $2.03, to $41.07. “Despite many of the 18 oil producers believing the meeting in Doha was merely a rubber stamp affair for an oil production freeze, Saudi Arabia managed to throw a spanner in the works,” said Angus Nicholson at IG Markets. “With Saudi Arabia fighting proxy wars with Iran in Yemen and Syria/Iraq, it is understandable that they had little inclination to freeze their own production and make way for newly sanctions-free Iran to increase their market share.”

It was the worst possible outcome for oil producers at their weekend meeting in Doha, with their failure to reach even a weak agreement showing very publicly their divisions and inability to act in their own interests. Expectations for the meeting had been modest at best, with sources in the producer group predicting an agreement to freeze output. But even this meagre hope was dashed by Saudi Arabia’s insistence Iran join any deal, something the newly sanctions-free Islamic republic wouldn’t countenance. From a producer point of view, an agreement including Iran that shifted market perceptions on the amount of oil supply available would have been the best outcome.

The acceptable result would have been an agreement that froze production at already near record levels, with an accord that Iran would join in once it had reached its pre-sanctions level of exports. What was delivered instead was confirmation that the Saudis are prepared to take more pain in order not to deliver their regional rivals Iran any windfall gains from higher prices and exports. The meeting in Qatar on Sunday effectively pushed a reset button on the crude markets, putting the situation back to where the market was before hopes of producer discipline were first raised. What happens now is that the market will have to continue along its previous path of re-balancing, without any assistance from the OPEC or erstwhile ally Russia. Brent crude fell nearly 7% in early trade in Asia on Monday, before partly recovering to be down around 4%.

The potential is for crude to fall further in coming sessions as long positions built up in the expectation of some sort of producer agreement are liquidated in the face of the reality of no deal. It’s likely that recriminations will follow for some time among the oil producers, with the Russians and Venezuelans said to be annoyed at what they see as the Saudi scuppering of a deal that had almost been locked in. This will make it harder for any future agreement, with the OPEC meeting on June 2 the next chance for the grouping to reach some sort of agreement. For the time being, OPEC’s credibility is shot, and won’t be restored by even a future agreement as it will take actual, verifiable action to convince a now sceptical market. However, as the events in Doha showed, the Saudis are unlikely to agree to anything in the absence of Iranian participation, and that is also equally unlikely.

The failure by the world’s biggest oil producers to agree on an output freeze spurred a selloff across emerging markets, with stocks halting a seven-day rally as Brent crude plunged as much as 7%. The ringgit led declines in developing-nation currencies as the disappointment stemming from the weekend meeting in Doha disrupted a recovery in commodity prices, putting pressure on Malaysian finances as a net oil exporter. Hopes an agreement would be reached had pushed Brent above $44 a barrel for the first time since December and spurred gains across asset classes in recent days. It’s now headed back toward $41 as the discussions to address a global oil glut stalled after Saudi Arabia and other Gulf nations wouldn’t commit to any deal unless all OPEC members joined, including Iran.

“We have seen a high correlation between oil, commodity prices and emerging assets this year and we have seen a strong run up, so the latest development on the failure to agree on an oil output freeze should spark profit-taking among investors,” said Miles Remington, head of equities at BNP Paribas Securities Indonesia. Energy-related companies fell the most among the 10 industry groups of the MSCI Emerging Markets Index, which dropped 0.7% and retreated from last week’s highest level since November. While that was the biggest decline since April 5, the energy component slid 1.4% and industrial stocks 1%.

The Canadian and Australian dollars dropped as crude tumbled after oil-producing nations failed to reach an accord to freeze output. The yen, used by investors as a haven, rose toward a 17-month high. The currencies of Australia, Canada, Malaysia and Norway all retreated at least 0.7% after negotiations in Doha ended without an agreement from OPEC and other oil producers to freeze supplies. Foreign-exchange traders sought the safety of Japan’s currency as the diplomatic failure threatens to send crude back toward the more than 13-year lows reached in February. World leaders at the end of last week signaled opposition to any efforts from Japan to directly halt the yen’s 11% climb this year.

“Lack of agreement from Doha has hit commodity currencies lower,” said Robert Rennie at Westpac Banking in Sydney. “The prospects of another near-term round of talks appear limited ahead of the June OPEC meeting.” The Aussie dropped 0.8% to 76.65 U.S. cents as of 7:01 a.m. London time, set for the largest decline since April 7. Canada’s loonie tumbled 1.1% to C$1.2962 against the greenback. Crude is the nation’s second-largest export. Malaysia’s ringgit slid 0.8% to 3.9348 per dollar. Oil futures fell as much as 6.8%, the biggest intraday drop since Feb. 1. “The oil price will reset lower and could even retest $30 over the next three months,”said James Purcell at UBS’s wealth-management business in Hong Kong.

“Short term, that will dampen enthusiasm for risk assets. However, markets are being slightly myopic. Economic data have improved in both China and the U.S. of late.” The lack of agreement at Doha highlights the deep divisions between OPEC members, and importantly, within Saudi Arabia, Westpac’s Rennie said. The Aussie should hold support from about 75.75 cents to 76 cents at least through the next day or so, he said. The yen jumped 0.7% to 107.96 per dollar, and touched 107.77. It reached 107.63 on April 11, the strongest since October 2014. Hedge funds and other large speculators pushed wagers on yen strength to a record last week as Japanese authorities appeared reluctant to intervene to reverse the strengthening currency.

All is calm. All is still. Share prices are going up. Oil prices are rising. China has stabilised. The eurozone is over the worst. After a panicky start to 2016, investors have decided that things aren’t so bad after all. Put your ear to the ground though, and it is possible to hear the blades whirring. Far away, preparations are being made for helicopter drops of money onto the global economy. With due honour to one of Humphrey Bogart’s many great lines from Casablanca: “Maybe not today, maybe not tomorrow but soon.” But isn’t it true that action by Beijing has boosted activity in China, helping to push oil prices back above $40 a barrel? Has Mario Draghi not announced a fresh stimulus package from the European Central Bank designed to remove the threat of deflation? Are hundreds of thousands of jobs not being created in the US each month?

In each case, the answer is yes. China’s economy appears to have bottomed out. Fears of a $20 oil price have receded. Prices have stopped falling in the eurozone. Employment growth has continued in the US. The International Monetary Fund is forecasting growth in the global economy of just over 3% this year – nothing spectacular, but not a disaster either. Don’t be fooled. China’s growth is the result of a surge in investment and the strongest credit growth in almost two years. There has been a return to a model that burdened the country with excess manufacturing capacity, a property bubble and a rising number of non-performing loans. The economy has been stabilised, but at a cost. The upward trend in oil prices also looks brittle. The fundamentals of the market – supply continues to exceed demand – have not changed.

Then there’s the US. Here there are two problems – one glaringly apparent, the other lurking in the shadows. The overt weakness is that real incomes continue to be squeezed, despite the fall in unemployment. Americans are finding that wages are barely keeping pace with prices, and that the amount left over for discretionary spending is being eaten into by higher rents and medical bills. For a while, consumer spending was kept going because rock-bottom interest rates allowed auto dealers to offer tempting terms to those of limited means wanting to buy a new car or truck. In an echo of the subprime real estate crisis, vehicle sales are now falling. The hidden problem has been highlighted by Andrew Lapthorne of the French bank Société Générale. Companies have exploited the Federal Reserve’s low interest-rate regime to load up on debt they don’t actually need.

“The proceeds of this debt raising are then largely reinvested back into the equity market via M&A or share buybacks in an attempt to boost share prices in the absence of actual demand,” Lapthorne says. “The effect on US non-financial balance sheets is now starting to look devastating.” He adds that the trigger for a US corporate debt crisis would be falling share prices, something that might easily be caused by the Fed increasing interest rates.

BBG senior editor David Shipley displays the general fallacy: all that’s there are desperate attempts to go back to something that once was, only in a more centralized fashion. But there’s no going back.

The deeper the slump, economists used to say, the stronger the recovery. They don’t say that anymore. The effects of the crash of 2008 still reverberate, with the latest forecasts for global growth even more dismal than the last. The persistently stagnant world economy is more than just a rebuke to economic theory, of course; it exacts a human toll. And while politicians and central bankers – or economists, for that matter – can’t be faulted for their creativity, their remedies might have more impact if they were bolder and better-coordinated. By ordinary standards, to be sure, governments haven’t been timid. Without fiscal stimulus and aggressive monetary easing in the U.S. and other countries, things would look even worse. And yet, worldwide output is predicted to rise only 3.2% this year, falling still further below the pre-crash trend.

Simply doubling down on current strategies is unlikely to work. Large-scale bond-buying, or so-called quantitative easing, has run into diminishing returns. Negative interest rates, where they’ve been tried, haven’t revived lending, and central banks are unable or unwilling to cut further. What about new fiscal stimulus? Where possible, that would be good – but it’s hardest to do in the very countries that need it most, because that’s where public debt is already dangerously high. True, as the IMF’s new fiscal report says, almost all countries could become more growth-friendly by combining measures to curb public spending in the longer term (for instance, raising the retirement age) with steps to increase demand in the short term (cutting payroll taxes, raising employment subsidies and building infrastructure).

Getting fiscal policy right country by country would surely help – yet probably wouldn’t be enough: No single country can adequately deal with a global shortfall of demand. A finance ministry for the world isn’t happening any time soon. Still, it’s a pity that governments aren’t trying harder to coordinate their fiscal policies more intelligently, or indeed at all. The global slump persists partly because of international spillovers. Better coordination would take these into account: Countries that could safely deploy fiscal stimulus would give some weight to global as well as national conditions, and fiscal policy would be formed interactively. Even within the EU, where you’d expect economic coordination to be the norm, and where the single currency makes it essential, there’s no sign of it.

At the global level, in forums such as the IMF, you might expect the U.S. to take the lead in any such effort. So it should – but it will need to mend its shattered policy-making machinery first. If Washington can’t come to a decision on its own on taxes or spending, the question of coordination doesn’t arise. The last resort, if the slump goes on and governments can’t coordinate better, might be to combine monetary and fiscal policy in a hybrid known (unfortunately) as helicopter money. Governments would cut taxes and/or spend more, but meet the cost by printing money rather than by borrowing. In one variant, central banks might simply send out checks to taxpayers. That’s a startling idea, no doubt – but so was quantitative easing not long ago.

China’s growth rates for quarter-on-quarter and year-on-year GDP for the past year don’t match. That, combined with confirmation that 1Q output was underpinned by an unsustainable resurgence in real estate, tarnishes the newly acquired shine on the country’s economic prospects. The initial reaction to the 1Q GDP data, published Friday, was a sigh of relief. Growth at 6.7% year on year was in line with expectations and comfortably inside the government’s 6.5-7% target range. If anyone noticed that the normal quarter-on- quarter data was missing from the National Bureau of Statistics release, few thought anything of it. Then, on Saturday, the quarter-on-quarter data was published, and some of the relief turned to consternation.

Quarter-on-quarter growth in 1Q was just 1.1% – an annualized growth rate of 4.5%, and the lowest print since the data series became available in 2011. Worse, based on the accumulated quarter-on-quarter data over the last year, annual growth in 1Q was just 6.3% – substantially below the NBS’s 6.7% reading for year-on-year growth. Explaining the inconsistency between the two data points is tough to do. Accumulated quarter-on-quarter growth over four quarters should add up to year-on-year growth. In the past, it has. The divergence in the 1Q readings might reflect something as simple as difficulties with seasonal adjustment. Even so, against a backdrop of concerns about data reliability, it can only add to skepticism about China’s true growth rate.

China’s state-owned enterprises are likely to suffer more defaults over the next year as the government shows its readiness to shut companies in industries struggling with overcapacity, according to Standard & Poor’s. “In a major policy shift, the central government appears willing to close and liquidate struggling enterprises in the steel, mining, building materials, and shipbuilding industries,” S&P analyst Christopher Lee wrote in a report Monday. “We believe this stance will exacerbate the problems of companies in these cyclical and capital-intensive sectors, which are facing sluggish demand amid slowing investment growth.”

The warning follows S&P’s decision earlier this month to cut China’s sovereign rating outlook to negative from stable because economic rebalancing is likely to proceed more slowly than it had expected. Moody’s Investors Service also downgraded the outlook to negative in March, highlighting surging debt and the government’s ability to enact reforms. The revisions were biased, Finance Minister Lou Jiwei said in Washington on Friday. Premier Li Keqiang has pledged to withdraw support from so-called zombie firms that have wasted financial resources and dragged on economic growth, which is at the slowest in a quarter century. China’s central bank has lowered benchmark interest rates six times since 2014, underpinning a jump in debt to 247% of GDP.

China Railway Materials, a state-backed commodities trader, is seeking to reorganize debt and halted trading on 16.8 billion yuan ($2.6 billion) of bonds this month. Baoding Tianwei last year became the first government-backed company to renege on onshore bonds. Sinosteel defaulted on onshore debt in October. Leverage among the largest state-owned enterprises has reached a “critical” level, according to Lee. It is likely to worsen in 2016 as a weak top line is not fully offset by cost cuts and capital expenditure reductions, he wrote in the report.

China etched in details of plans to help workers laid off from the bloated coal and steel industries, saying assistance would include career counseling, early retirement and help in starting businesses, among other measures. New guidelines released by seven Chinese ministries over the weekend build on previously announced commitments to restructure the coal and steel industries, whose excess production is dragging on the economy, and to take care of an estimated 1.8 million workers who will be displaced. The new measures place priority on finding jobs and cushioning the transition to reduce the unemployment that the authoritarian government sees as a threat to social stability.

“Proper placement of workers is the key to working to resolve excess capacity,” said the document issued by the labor ministry, the top economic planning agency and others. It urged local governments to “take timely measures to resolve conflicts” and to “avoid ignoring the issue.” Unlike a far-reaching restructuring of state industries two decades ago, Beijing is taking a cautious approach this time around, prompting some economists to caution that the protracted pace may make the situation worse. Government data released Friday showed economic growth slowing slightly in the first quarter, buoyed by new loans, debt and investment in real estate and factories—methods that are likely to lengthen the transition to a more consumer-driven society from one driven by investment and manufacturing.

Western-style “restructuring is not on the horizon here,” said ING economist Tim Condon. “Rebalancing, forget that. That’s for another day.” Government plans call for reducing some 10% to 15% of the excess capacity in the steel and coal sectors over the next several years. That is less than half the portion analysts say is needed to bring supply closer in line with demand. And steel and coal are only two of numerous other industries plagued by overcapacity that haven’t been addressed. The large number of ministries that have signed off on the plan dated April 7 but released more than a week later underscore the sensitivity, importance and breadth of resources China is devoting to the unemployment problem.

[..] Germany, Austria, France and Sweden, among others, have reintroduced border checkpoints in some places. They are pressured by Europe’s biggest refugee crisis since World War II – about 1 million migrants arrived in Greece and Italy in 2015 – terrorist attacks, and the growth of anti-immigration movements. But the economic cost of dumping Schengen, at a time when growth across the continent is still weak, would be massive. A permanent return to border controls could lop €470 billion of GDP growth from the European economy over the next 10 years, based on a relatively conservative assumption of costs, according to research published by Germany’s Bertelsmann Foundation. That’s like losing a company almost the size of BMW AG every year for a decade.

The open borders power an economy of more than 400 million people, with 24 million business trips and 57 million cross-border freight transfers happening every year, the European Parliament says. Firms in Germany’s industrial heartland rely on elaborate, just-in-time supply chains that take advantage of lower costs in Hungary and Poland. French supermarket chains are supplied with fresh produce that speeds north from Spain and Portugal. And trans-national commutes have become commonplace since Europeans can easily choose to, say, live in Belgium and work in France. For many Europeans, passport-free travel is part of being, simply, European. For the company hiring driver Unczorg, the security checks increase costs in terms of delays, storage and inventory.

Permanent controls would destroy the business model of German industry, says Rainer Hundsdoerfer, chairman of EBM-Papst. “You get the products you need for assembly here in Germany just in time,” he said by phone. “That’s why the trucks go nonstop. They come here, they unload, they load, and off they go. The cost isn’t the only prime issue” in reinstating border checks. “It’s that we couldn’t even do it.” Nor could anyone else, he adds: “Nothing in German industry, regardless of whether it’s automotives or appliances or ventilators, could exist without the extended workbenches in eastern Europe.”

This sort of over the top comment could be the biggest gift to the Leave side. Then again, they have Boris Johnson and Nigel Farage as their figureheads. Not going to work.

Britain would be “permanently poorer” if voters choose to leave the EU, George Osborne has warned, as a Treasury study claimed the economy would shrink by 6% by 2030, costing every household the equivalent of £4,300 a year. In the starkest warning so far by the government in the referendum campaign, the chancellor describes Brexit as the “most extraordinary self-inflicted wound”. Osborne will embark on one of the government’s most significant moves in the referendum campaign on Monday when he publishes a 200-page Treasury report which sets out the costs and benefits of EU membership. In a Times article the chancellor wrote: “The conclusion is clear for Britain’s economy and for families – leaving the EU would be the most extraordinary self-inflicted wound.”

Osborne warned that the option favoured by Boris Johnson – a deal along the lines of the EU-Canada arrangement – would lead to an economic contraction of 6% by 2030. Supporters of Britain’s EU membership say the EU-Canadian deal would be a disaster for the UK because it excludes financial services, a crucial part of the British economy. The chancellor asked whether this was a “price worth paying” as he said there was no other model for the UK that gave it access to the single market without quotas and tariffs while retaining a say over the rules. Osborne continued: “Put simply : over many years, are you better off or worse off if we leave the EU? The answer is: Britain would be worse off, permanently so, and to the tune of £4,300 a year for every household.”

“It is a well-established doctrine of economic thought that greater openness and interconnectedness boosts the productive potential of our economy. That’s because being an open economy increases competition between our companies, making them more efficient in the face of consumer choice, and creates incentives for business to innovate and to adopt new technologies.”

Brazilian president Dilma Rousseff suffered a crushing defeat on Sunday as a hostile and corruption-tainted congress voted to impeach her. In a rowdy session of the lower house presided over by the president’s nemesis, house speaker Eduardo Cunha, voting ended late on Sunday evening with 367 of the 513 deputies backing impeachment – comfortably beyond the two-thirds majority of 342 needed to advance the case to the upper house. As the outcome became clear, Jose Guimarães, the leader of the Workers party in the lower house, conceded defeat with more than 80 votes still to be counted. “The fight is now in the courts, the street and the senate,” he said. As the crucial 342nd vote was cast for impeachment, the chamber erupted into cheers and Eu sou Brasileiro, the football chant that has become the anthem of the anti-government protest.

Opposition cries of “coup, coup,coup” were drowned out. In the midst of the raucous scenes the most impassive figure in the chamber was the architect of the political demolition, Cunha. Watched by tens of millions at home and in the streets, the vote – which was announced deputy by deputy – saw the conservative opposition comfortably secure its motion to remove the elected head of state less than halfway through her mandate. There were seven abstentions and two absences, and 137 deputies voted against the move. Once the senate agrees to consider the motion, which is likely within weeks, Rousseff will have to step aside for 180 days and the Workers party government, which has ruled Brazil since 2002, will be at least temporarily replaced by a centre-right administration led by vice-president Michel Temer.

On a dark night, arguably the lowest point was when Jair Bolsonaro, the far-right deputy from Rio de Janeiro, dedicated his yes vote to Carlos Brilhante Ustra, the colonel who headed the Doi-Codi torture unit during the dictatorship era. Rousseff, a former guerrilla, was among those tortured. Bolsonaro’s move prompted left-wing deputy Jean Wyllys to spit towards him. Eduardo Bolsonaro, his son and also a deputy, used his time at the microphone to honour the general responsible for the military coup in 1964. Deputies were called one by one to the microphone by the instigator of the impeachment process, Cunha – an evangelical conservative who is himself accused of perjury and corruption – and one by one they condemned the president. Yes, voted Paulo Maluf, who is on Interpol’s red list for conspiracy. Yes, voted Nilton Capixiba, who is accused of money laundering. “For the love of God, yes!” declared Silas Camara, who is under investigation for forging documents and misappropriating public funds.

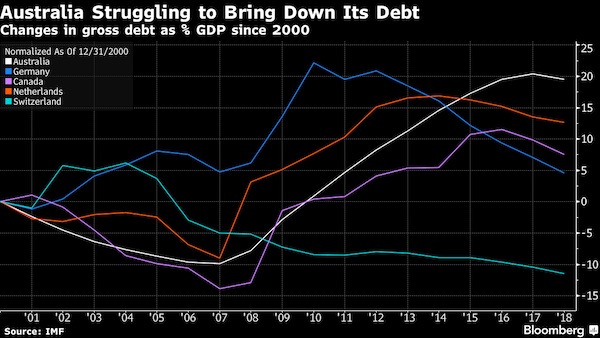

Australia played all on red. Which can you take to mean either China, for exports, or debt, for housing. Realizing that in the ned the house always wins, it’s a suicide strategy.

1986 may seem like a long time ago, but for Australian Treasurer Scott Morrison some of the parallels with his current budget balancing act are getting too close for comfort. Back then, Moody’s and Standard & Poor’s pulled their AAA ratings as weak commodity prices wrecked government income and external finances. With resources again in a funk and a widening funding gap, National Australia Bank and JPMorgan said last week Morrison needs to undertake repairs in his May 3 budget to safeguard the country’s top rankings. Moody’s warned Thursday that debt will grow without revenue-boosting measures. “Moody’s are understandably getting impatient,” said Shane Oliver at Sydney-based AMP Capital Investors.