Salvador Dali� City of drawers – The Anthropomorphic Cabinet �1936

2/3(?!) of it is in the US.

• OECD Countries’ Retirement Assets Surpass $43 Trillion In 2017 (PiO)

Retirement assets in OECD countries hit a record $43.4 trillion at the end of 2017, well above the pre-crisis level. The OECD said in its annual Pension Markets in Focus report that assets invested in all funded and private pension systems across 87 jurisdictions grew 12.1% over the year, and increased 53.9% compared with figures at the end of 2007. The report said assets are unevenly distributed worldwide, with less than $200 billion across 78% of the reporting countries, while 8% held more than $1 trillion each: the U.S. with about $28.2 trillion; the U.K. with $2.9 trillion; Canada at $2.6 trillion; Australia with $1.8 trillion; the Netherlands with $1.6 trillion; Japan at $1.4 trillion; and Switzerland with $1 trillion. The remaining 9% of assets, or about $3.9 trillion, are split among the other 29 OECD countries.

The largest amounts of assets are located in some of the biggest economies in the world and with a long history of retirement savings. High investment returns from equity markets partially explain the growth of these assets, said the report, with the real net investment rate of return on retirement assets exceeding 4% on average in 2017. U.S. retirement plans achieved a 7.5% real net investment rate of return in 2017, added the OECD. Funding levels for DB funds improved in the U.S., to 59.6% at end-2017 from 56% a year earlier; but worsened from 2007 figures of 68.6%. The funding ratio was calculated as the ratio of total investment and net technical provisions for occupational defined benefit plans using values reported by national authorities in the OECD template.

U.K. funding levels improved to 90.5% as of the end of 2017, up from 85.8% a year earlier, but down from 108.8% as of the end of 2007. Denmark had the highest funding level of OECD countries in the report, at 135.1%. However, that level was down from 146.1% a year earlier, but improved over the 127.4% funding level as of the end of 2007.

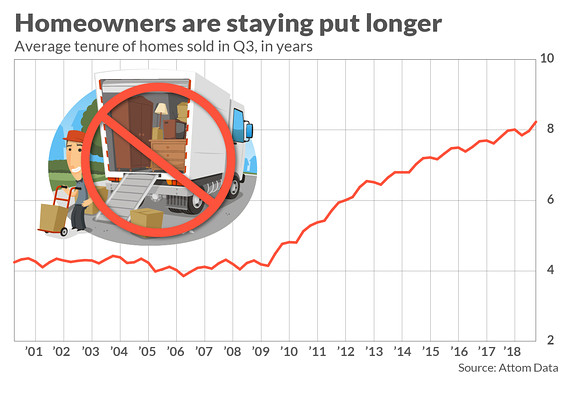

Bad time to become a real estate agent.

• As The Housing Market Stagnates, American Homeowners Are Staying Put (MW)

Housing-market headwinds are keeping American homeowners in their properties for the longest stretches on record, in a sharp distortion of the mobility Americans have for decades prized. Across the country, homes that sold in the third quarter of this year had been owned an average of 8.23 years, according to an analysis from Attom Data Solutions. That’s almost double the length of time a home sold in 2000, when Attom’s data begin, had been owned. It’s partly the long tail of the housing crisis that’s created stagnant conditions and a less dynamic housing market, Attom spokesman Daren Blomquist told MarketWatch.

As of the second quarter, 2.2 million homeowners were still underwater on their mortgages, meaning they owe more to their lending institution than the home is worth, according to data from CoreLogic. Another 550,000 have 5% equity or less, meaning that if that property were to be sold the transaction costs, such as a real-estate agent’s commission, would likely leave the homeowner with nothing. The hypercompetitive market that’s emerged from the wreckage of the crisis is also keeping people in place. Many homeowners have ample equity in their homes, but hesitate to list those homes because they’re worried about finding a property to buy if they do sell. A few others may be trapped by “rate lock” — enjoying the benefits of their ultralow mortgage rates, and unwilling to spend more on financing costs.

Interesting that he gets to say it.

• Economist Slams ‘China Model’ That ‘Inevitably Leads To Confrontation’ (SCMP)

Using the “China model” to explain the country’s economic success over the past four decades is wrong and dangerous, according to an influential Chinese economist, who says this misconception has inevitably led to antagonism between China and the West. Zhang Weiying, one of the most prominent liberal economists in the country and a professor at prestigious Peking University, made the comments in a lecture on October 14. An edited version of his speech was published on the university’s website on Wednesday. The speech is a wholesale negation of the “China model” theory that has gained traction in recent years, as the country becomes more confident in promoting its own development path under President Xi Jinping.

Zhang lashes out at those who attribute China’s economic growth to an exceptional “China model”, which includes a powerful one-party state, a colossal state sector and “wise” industrial policy, saying it is not only factually wrong, but also detrimental to the country’s future. “The theory of the ‘China model’ sets China as a frightening anomaly from the Western perspective, and inevitably leads to confrontation between China and the West,” he said. “The hostile international environment we face today is not irrelevant to the wrong interpretation of China’s achievement in the past 40 years by some economists.”

The economist’s rejection of the “China model” comes as debates about the country’s economic future are heating up. The world’s second largest economy is losing steam – growth is at its slowest pace since 2009 – as it marks 40 years since its market reforms. At home, it is grappling with a mountain of debt, plunging stocks and an ailing private sector. Abroad, tensions over the prolonged trade war with the United States appear to be spilling over into defence, diplomacy and politics. Zhang said the trade war not only reflected conflict between China and the US, but between China and the larger Western world. It also went beyond trade to reflect the clash over value systems, he said.

Like his dad, strongly anti-war.

• Rand Paul Seeks To Punish Saudi Arabia For Khashoggi Killing (Pol.)

Sen. Rand Paul says he’s not going to let Saudi Arabia off the hook after journalist Jamal Khashoggi was killed in Turkey by agents linked to the Saudi government. The Kentucky Republican said Saturday he’s intent on forcing another vote to block billions in arm sales to the autocratic Middle Eastern kingdom and won’t settle for targeted sanctions, seeking to capitalize on negative public sentiment surrounding the Oct. 2 killing. “Are we going to do fake sanctions? Are we going to pretend to do something by putting sanctions on 15 thugs. Or are we going to do something that hurts them?” Paul said in an interview here, explaining that he thinks Saudi Arabia is trying to wait him out until Khashoggi fades from the headlines before announcing the arms sale, which would allow him to try and stop it.

“They know if they have the vote they might lose. So they’re probably not going to make any announcement until this dies down,” Paul said. Rather than focusing simply on Khashoggi, Paul has made a broader critique of Saudi Arabia as supporting “violent Jihad” and a brutal civil war in Yemen. But he’s noticed a substantive shift in the way his colleagues are now talking about the country. [..] Paul, a longtime Saudi critic, has previously forced votes to block the arms sales, but they have failed given a strong hawkish wing in the Senate that wants to keep a key ally against Iranian influence in the Middle East. Paul says that has changed. “We would win the vote right now. It would be a very bad vote if 60, 65, or even 70 people voted to cut the arms sales for now and the president were to veto that, that would be bad,” he said.

President Donald Trump has been more circumspect when discussing arms sales, questioning the wisdom of canceling sales that he believes creates hundreds of thousands of jobs. Paul said he’s tried to convince the president to come to his position, but he’s not there yet. “He says he doesn’t want to disrupt the arm sales. And it’s something we have an honest disagreement on. I don’t think arms are jobs programs,” Paul said. He said their “discussions aren’t really that much that back and forth.” [..] Paul also broke further with the president on foreign policy. He called it a “terrible idea” for the United States to back away from nuclear and weapons agreements with Russia and said he’s asked Trump to appoint nuclear negotiators in a bid to preserve the NEW START treaty and the INF agreement.

Not sure how this would help their case at this point.

• Saudi Arabia Says It Is A Beacon Of Light Fighting ‘Dark’ Iran (G.)

Saudi Arabia’s foreign minister has described the kingdom as a “vision of light” in the region as it tries to control the fallout from Jamal Khashoggi’s killing – its biggest diplomatic crisis since the 9/11 attacks. After more than two weeks of international outrage over the journalist and dissident’s death, Adel al-Jubeir sought to portray the country as the moral beacon of the Middle East, in stark opposition to Iran, Saudi Arabia’s arch-rival. “We are now dealing with two visions in the Middle East,” Jubeir told a security summit in Bahrain on Saturday. “One is a [Saudi] vision of light … One is [an Iranian] vision of darkness which seeks to spread sectarianism throughout the region. History tells us that light always wins out against the dark.”

Condemning the media coverage of Khashoggi’s killing as “hysterical”, Jubeir rejected a call from Recep Tayyip Erdogan, the Turkish president, to try the 18 suspects in Turkey, stressing that they would be “held accountable” on Saudi soil. [..] Erdogan reiterated during an address to parliament on Friday that Riyadh must disclose the location of Khashoggi’s body and identify who ordered his killing – a sign that Ankara is willing to keep up the pressure on the beleaguered kingdom and its de facto ruler, the crown prince Mohammed bin Salman. [..] Jim Mattis, the US defence secretary, who also spoke at the summit in Manama, said that Khashoggi’s killing had “undermined regional stability”. Washington was considering additional punitive measures against those responsible after issuing visa bans for the suspects in the case, Mattis added.

5 months left. Nothing decided on.

• EU To Make Contingency Plans For A Second Brexit Referendum (Ind.)

The EU’s chief negotiator has been warned to make contingency plans for a second Brexit referendum, as pressure builds to give the public a final say on leaving. Prominent Remain politicians met with Michel Barnier in Brussels this week and said it was time to start “serious contingency planning”, as The Independent’s petition neared one million signatures and the future of Brexit looks increasingly uncertain. In a visit on Friday, Sadiq Khan, the mayor of London, told Mr Barnier that the negotiating period should be extended so Britain could have “time to have a referendum”. The warning comes after 700,000 people took to the streets of London last weekend to make the case for a vote on the final deal.

For there to be time to hold a referendum, the EU would likely have to extend the Article 50 negotiating period, which will automatically expire on 29 March 2019, leaving Britain to slide out with a no-deal Brexit. The calls for an extension came from across a number of parties. Liberal Democrat leader Vince Cable said following a meeting with Mr Barnier on Thursday: “My message to Michel Barnier was clear: it’s time to start serious contingency planning for a People’s Vote. We know the UK government has started making such plans as a result of the growing demand for such a vote, demonstrated by last weekend’s march. “The EU should do the same, because MPs who back the People’s Vote are fast forming the biggest and most cohesive bloc in Westminster.”

This will have an increasing effect on Europe as a whole. Who’s going to listen to Merkel as she’s fading at home?

• Germany’s Fragile Coalition Braced For More Upsets (G.)

[..] voters in the central state of Hesse have the power to deliver a second electoral upset within a fortnight to Germany’s embattled ruling parties, potentially plunging both into fresh crises. The regional election is seen as decisive for the future of Merkel’s rickety coalition government. Last-minute polling showed support plummeting for both her Christian Democrat Union (CDU) and coalition partner the Social Democrats (SPD) in a swing state traditionally seen as a bellwether for national politics. Both parties were predicted to drop 10 points each since the state’s last regional election in 2013. Such a trouncing would come on the heels of a disastrous result in Bavaria that was widely seen as a protest against the failings of the Berlin government.

“None of the parties are there for us,” said Müller, who has voted for both CDU and SPD in the past, but was still undecided. “What should I do? I have to vote, it’s my duty to stop the far right getting into power. But I also know I won’t be heard. I can vote for whoever I like; the politicians will still do whatever they want.” Hesse, home to Germany’s financial centre, Frankfurt, has been governed by CDU-led coalitions for the past two decades. But polls have the party nosediving to 28%, a result that would end the state’s CDU-Green coalition and leave a question mark over the future of CDU state premier and close Merkel ally Volker Bouffier.

With tensions running high in the CDU, mutinous members have implied that if Bouffier falls, it may cost the chancellor vital votes when she stands for re-election as party leader at its conference in early December. But Merkel, who joined Bouffier on the campaign trail last week, was at pains to play down the significance of the regional vote for her party, government and chancellorship. “Hesse, and what happens here, is being watched and considered from far beyond Germany’s borders,” Merkel told supporters on Thursday in Fulda. “I want to point out once again that on Sunday the vote is about Hesse. Afterwards we’ll talk again about Berlin.”

The fighting in Idlib must cease. It’s the only outcome.

• Russia-Turkey-Germany-France Talks On Syria Kick Off (RT)

Leaders of Russia, Turkey, Germany and France have gathered in Istanbul to discuss the Syrian peace process. While the outcome of such tricky talks is hard to predict, the new format appears to be, at least, quite refreshing. Russia’s President Vladimir Putin, his French counterpart Emmanuel Macron and German Chancellor Angela Merkel arrived in Istanbul on Saturday to talk Syrian reconciliation. The host, Turkey’s leader Recep Tayyip Erdogan, has put high expectations on the gathering. “The whole world is watching this meeting. I hope, that the hopes will be met,” Erdogan said, while opening the summit. The four leaders are also expected to be joined by UN Special Envoy to Syria Staffan de Mistura.

The four-way summit is an entirely new format of talks on the war-torn country, which has endured years-long conflict. The meeting is all about testing the waters and trying to bring about different formats of talks on Syria, as if the leaders were to “synchronize watches” rather than reach a breakthrough, Kremlin spokesman Dmitry Peskov said. Similar opinion was expressed by Germany, with Foreign Minister Heiko Maas stating that the summit effectively brings different sides together for the very first time. “There are Russians and Turks, who have been at the same format of talks with Iran. And on the other side, there are French and us, who partake in the so-called ‘Friends of Syria’ group,” Maas said ahead of the event, adding that having a “joint conversation” was a viable idea.

Turns out, the story was a bit different than many reported.

• “My” Suspended Twitter Account (Paul Craig Roberts)

Dear Readers:

It is all over the internet and international media that Twitter has suspended my account. This is not the case. I do not use social media. I discovered that a Twitter account was operating in my name. I requested that the account be taken down. I have no recollection of giving anyone permission to operate a Twitter account in my name. I am still extremely busy trying to help family relatives impacted by Hurricane Michael and could only quickly look at the Twitter postings. It seemed to be mainly innocuous, consisting of links or quotes from my posted columns.

However, there were other things, such as appeals that money be sent to Alex Jones InfoWars and other things. I have no objection to Alex Jones. However, my webmaster and I were concerned that things could be posted that would be dangerous for me, such as libel, death threats to others, and so forth. To repeat, the account was closed at my request. To repeat, I do not use social media.

Paul Craig Roberts

There’s something cynical about this, but also beautiful.

• Mexico Honors Migrants At Day Of The Dead As Caravan Treks North (R.)

Mexico City dedicated its Day of the Dead parade on Saturday to migrants, just as thousands of Central Americans were trekking from the country’s southern border toward the United States under pressure from U.S. President Donald Trump to disband. In an a twist on the traditional dancing skeletons and marigold-adorned altars making their way down the capital’s main thoroughfare, the parade also referenced Mexicans who emigrated as well as foreigners who settled in the capital. “The parade… is dedicated to migrants, who in their transit to other countries have lost their lives, and who in their passing through the country have contributed to a true ‘Refuge City,’” the Mexico City government said on Twitter.

In one segment, gray metallic panels representing the Mexico side of the U.S. border wall were stenciled with the phrase, “There are also dreams on this side.” Other presentations honored exiled Spaniards, Argentineans and Jews, Mexico City’s culture ministry said. The event ahead of Nov. 1 and 2, when Mexicans observe Day of the Dead in town squares, homes and cemeteries, coincided by chance with the journey of a migrant caravan traveling into Mexico, many fleeing violence and poverty in Honduras and Guatemala.