Library of Congress Dallas motorcade minutes before shooting November 22, 1963

Well, if you thought you’d seen all the madness and absurdity that could possibly come out of the financial system by now, you are definitely being caught on the wrong flat foot as we speak. And there can be no doubt that much more of this will be revealed as we go along. Jamie Dimon renting Buckingham Palace to celebrate his $13 billion settlement with US regulators is just the beginning, though it’s a pretty clear statement of just how untouchable too big to fail policies have made Wall Street and the City feel. And they don’t feel that way for nothing, in every sense of the word, count on it.

A Labour spokesman said this about the party at the Palace, which included appearances by the Royal Philharmonic and the English National Ballet: ““There is also the fact that this should be a special place. This is the home of the Queen. Where is it all going to end?“ Well, sir, maybe it’s time to wake up, because the new kings and queens of the world have taken over. And they intend to be loud and proud about it, like any group of conquerors throughout history ever did.

Fine dining for Dimon at the Palace raises concerns of commercialisation

It must have been a welcome spot of light relief for Jamie Dimon. Only days after he finally agreed to a $13 billion settlement with US mortgage regulators, the boss of JPMorgan – and dozens of his corporate clients – were sitting back amid the splendour of Buckingham Palace, enjoying a fine dinner and performances by the Royal Philharmonic and the English National Ballet.

The event, hosted by Prince Andrew, Duke of York, reflects growing enthusiasm by the Royal Family to use its premises to promote business interests. But it also risks stoking criticism over its apparent commercialisation and its intimacy with business.

The JPMorgan event on October 30, had a guestlist that included up to 100 corporate and political heavyweights, ranging from Kofi Annan, the former UN secretary-general, to Indian industrialist Ratan Tata. Also present was Tony Blair, the former prime minister who chairs JPMorgan’s “international council” of senior advisers.

That’s one sign that there’s been a takeover and a change of guards. The story coming out over the weekend about Royal Bank of Scotland – RBS – is another. And the “Royal” label in its name starts to sound mighty cynical. RBS is now being accused of pushing healthy client businesses into bankruptcy, so it could take over their assets for pennies on the pound. There’s one little detail that should make this even more preposterous: RBS is 81% government owned.

RBS accused of pushing small businesses to the edge to boost profits

City regulators have been handed a dossier of evidence compiled by an adviser to Vince Cable which claims that Royal Bank of Scotland was deliberately wrecking viable small businesses to make profits for the bailed out bank.

The business secretary – a long-time critic of the banking industry’s lending practices – said some of the allegations were so serious that he had handed the report, compiled by businessman Lawrence Tomlinson, to the regulators and the bank. It has also been given to Sir Andrew Large, a former deputy governor of the Bank of England, whose report on lending failures by RBS will also be released on Monday.

Tomlinson, appointed by Cable as “entrepreneur in residence”, has compiled evidence from hundreds of businesses which have approached him after ending up in the bank’s global restructuring group (GRG), and subsequently had their properties sold to its specialist property arm, West Register.

“There are many devastating stories of how RBS has wrecked good businesses and the ruinous impact this has on the lives of the business owners,” said Tomlinson.

How do you like them apples, right? Still, if I were a betting man, I’d put my money on these stories sounding so hard to believe, and on people being so unwilling to believe them, that they’ll be filed under ‘too far out of left field’, and we all go about our days as if nothing ever happened.

This thing about the Fed paying interest on reserves that banks have with it, is another example of this. We’ve all seen to which extent those reserves originate as directly as possible from the Fed’s own QE policies. They hand that $85 billion a month to Wall Street, much of it in exchange for MBS, so the mortgage debt risk no longer rests with the banks, and then pay interest on what it’s just handed to the banks. And whatever explanations and excuses may emanate from the banks themselves and the financial press that serves them, in essence it’s just another piece of too big to fail folly. Once it’s become acceptable to complain about the interest the Fed pays you on the reserves it’s just handed you, it’s like that Labour guy said about Buckingham Palace: “What’s next”?

US banks warn Fed interest cut could force them to charge depositors

Leading US banks have warned that they could start charging companies and consumers for deposits if the US Federal Reserve cuts the interest it pays on bank reserves. Depositors already have to cope with near-zero interest rates, but paying just to leave money in the bank would be highly unusual and unwelcome for companies and households.

The warning by bank executives highlights the dangers of one strategy the Fed could use to offset an eventual “tapering” of the $85bn a month in asset purchases that have fuelled global financial markets for the last year. Minutes of the Fed’s October meeting published last week showed it was heading towards a taper in the coming months – perhaps as soon as December – but wants to find a different way to add stimulus at the same time. “Most” officials thought a cut in the interest on bank reserves was an option worth considering.

Executives at two of the top five US banks said a cut in the 0.25 per cent rate of interest on the $2.4tn in reserves they hold at the Fed would lead them to pass on the cost to depositors.

Banks say they may have to charge because taking in deposits is not free: they have to pay premiums of a few basis points to a US government insurance programme. “Right now you can at least break even from a revenue perspective,” said one executive, adding that a rate cut by the Fed “would turn it into negative revenue – banks would be disincentivised to take deposits and potentially charge for them”.

Other bankers said that a move to negative rates would not only trim margins but could backfire for banks and the system as a whole, as it would incentivise treasury managers to find higher-yielding, riskier assets.

“It’s not as if we are suddenly going to start lending to [small and medium-sized enterprises],” said one. “There really isn’t the level of demand, so the danger is that banks are pushed into riskier assets to find yield.”

I suggested the other day that since the $85 billion a month QE that Janet Yellen intends to keep going is such an unmitigated failure – that is, from the point of view of the real economy -, why not try and give it to the American people instead of the banks? There’s no doubt that would do a lot more to revive the economy. Come to think of it: there’d be another advantage: the people wouldn’t insist on being paid interest on it, and whine and threaten and throw tantrums when they didn’t get it.

Yves Smith posted a nice piece by economics professor Rajiv Sethi on Saturday, who also looks at alternatives to the QE disaster:

Why Should Banks be the Only Ones with Accounts at the Fed?

About forty minutes into the final session of a recent research conference at the IMF, Ken Rogoff made the following remarks:

We have regulation about the government having monopoly over currency, but we allow these very close substitutes, we think it’s good, but maybe… it’s not so good, maybe we want to have a future where we all have an ATM at the Fed instead of intermediated through a bank… and if you want a better deal, you want more interest on your money, then you can buy what is basically a bond fund that may be very liquid, but you are not guaranteed that you’re going to get paid back in full.

This is an idea that’s long overdue. Allowing individuals to hold accounts at the Fed would result in a payments system that is insulated from banking crises. It would make deposit insurance completely unnecessary, thus removing a key subsidy that makes debt financing of asset positions so appealing to banks. There would be no need to impose higher capital requirements, since a fragile capital structure would result in a deposit drain. And there would be no need to require banks to offer cash mutual funds, since the accounts at the Fed would serve precisely this purpose.

But the greatest benefit of such a policy would lie elsewhere, in providing the Fed with a vastly superior monetary transmission mechanism. In a brief comment on Macroeconomic Resilience a few months ago, I proposed that an account be created at the Fed for every individual with a social security number, including minors. Any profits accruing to the Fed as a result of its open market operations could then be used to credit these accounts instead of being transferred to the Treasury. But these credits should not be immediately available for withdrawal: they should be released in increments if and when monetary easing is called for. [..]

Banks can continue to accept deposits but they will not be insured. If they want to promise redemption at par they will have to have a capital structure that has a lot more equity relative to debt. Admati and Hellwig have been arguing for significantly higher capital requirements to counteract the subsidization of bank debt financing; this will no longer be necessary under once deposit insurance is removed.

Bank loans will be financed by bank equity, long term debt, commercial paper, and money market mutual funds. The only source of financing to be removed is insured deposits.

The important point is that banks can be allowed to fail without putting the payments system at risk.

Don’t worry, I know how hard it is to make people realize to what extent QE is so bad for the US economy. Because they are being told to look at the stock markets, and the records they set, and interpret those records as evidence that QE is a big success.

The problem with that interpretation is that it’s evidence of the exact opposite. Stock market records in a time of global high unemployment, austerity and budget cuts are a sign of how, and to what extent, the financial industry has taken over our societies. Just like Jamie Dimon in Buckingham Palace, like RBS intentionally bankrupting its own healthy clients, and like Wall Street complaining about interest paid on free hand-outs.

And for those who care to look, there are more sign of this finance coup d’état we’re in the middle of. You have to look no further than that same $13 billion JPMorgan settlement. I’ve seen all sorts of interpretations of this, but I get back to the same point all the time: only $2 billion of it looks to be certain to be non-deductible.

All of the remaining $11 billion is at the very least open to interpretation. And with US banks having paid $100 billion (!) already in legal costs, vs $77 billion for their European counterparts, who would dare doubt that deals such as this have been very carefully constructed to favor the banks?

I mean, once you note that these legal costs, $177 billion, are much higher than the actual penalties and fines and settlements, estimated at $125 billion and largely tax-deductible to boot, doesn’t that tell you the whole story?

JPMorgan can deduct big chunk of $13 billion deal

The majority of the $13 billion settlement JPMorgan struck with the government Tuesday is likely to be tax deductible, reducing the bank’s financial hit. Here’s why: Many of the costs associated with corporate legal cases are treated as deductible under the tax code, in much the same way that a company’s wages or equipment expenses are.

That means JPMorgan will be able to reduce its tax bill because of many of the settlement payments that it must make. “From 1913, our tax laws have permitted companies to deduct their ‘ordinary and necessary’ expenses, which include compensation and restitution payments,” said Steve Rosenthal, a lawyer specializing in financial institution taxation and a visiting fellow at the Tax Policy Center.

But not all types of settlement payments are deductible. For instance, companies are prohibited from deducting fines and penalties payable to the federal government. “In 1969, Congress decided that allowing companies to deduct fines and similar penalties frustrated public policy, so it disallowed deductions for these payments — and, separately, disallowed deductions for antitrust damages, illegal bribes, and kickbacks,” Rosenthal said.

The U.S. Department of Justice, which negotiated the deal with JPMorgan, said the bank will pay $2 billion as a “civil penalty” to settle certain legal claims. And it’s JPMorgan’s understanding that the $2 billion is not deductible, the bank’s chief financial officer said on an analyst call Tuesday.

It wasn’t immediately clear how much of the rest of the $13 billion settlement, if any, may be considered non-deductible as well. But here’s the general bottom line: The compensation or restitution portions of a settlement like the one struck by JPMorgan may be deducted, but the penalties can’t.

While that may seem like a bright line, settlements are often written in a way that can leave a lot open to interpretation. In some deals, for instance, a penalty may be characterized in such a way that the company could argue that it should be deductible.

And the guys and dolls on Capitol Hill of course put in a token appearance, but in (sad) reality they have no more power left than the Queen of England does.

Congressman Peter Welch (D-VT) sent a letter to Jamie Dimon:

It was the taxpayer who initially funded the bailout of Wall Street. It was the taxpayer who continues to endure the consequences of the worst recession since the Great Depression. The taxpayer should not, therefore, be required to contribute a nickel towards the fines imposed for conduct that got America into this mess in the first place.

What, that’s supposed to make Dimon see the errors of his ways? Bring him to tears? Report to the nearest police station? No, this is simply Welch illustrating the demise of the American democracy in two simple sentences.

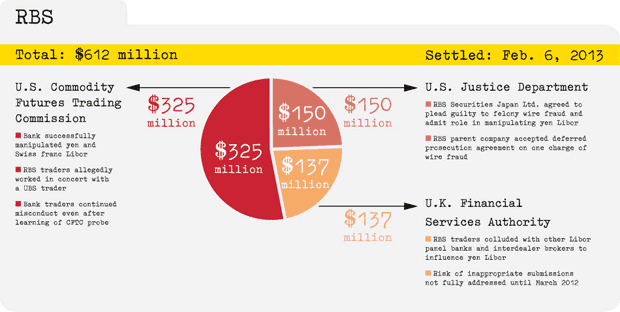

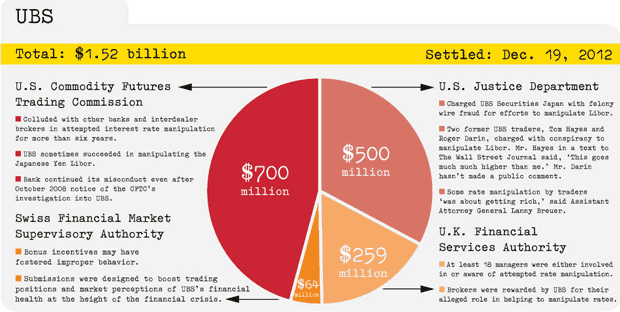

The JPMorgan settlement, and the shenanigans that surround it, is not an isolated case. It perfectly fits an established pattern. Remember Libor? Here’s the Wall Street Journal’s interpretation of events, with some great graphs. And before we go any further, why not ask yourself how it’s possible that this long term and at times hefty manipulation of an instrument to which according to the WSJ, $800 trillion in securities and loans are linked, results in total fines of just $5 billion or so. But that’s not even what I would like to point out here, that’s a story for another day.

Banks across the world face a hefty bill for alleged attempts to manipulate Libor, the London interbank offered rate benchmark, and other interest rate indexes. More than a dozen banks remain under investigation and civil lawsuits are under way. More than $800 trillion in securities and loans are linked to Libor. The charts below show regulators’ principal allegations and settlements agreed to by that particular company.

The WSJ added a number of graphs, which I’ll post in order, with the question if you can spot a common feature in all of them:

If you didn’t see that common feature, that’s alright, it wasn’t the first thing that I thought of either. But it’s there: all these banks pay far more in fines to foreign regulators than to their own. In particular, these European banks pay by far the biggest chunk of their fines to US regulators. But why?

Dutch newspaper NRC asked that same question a few weeks ago, and, focusing on domestic Rabobank, concluded that A) the Dutch central bank (the regulator), which got zero, doesn’t have the legal power to fine more than €60,000 no matter what, while the Dutch justice department, having never fined a bank anything near €96 million, was even sort of embarrassed to do so. A source at the justice department is quoted as saying the “fines culture” in the US is much more developed than in Holland. Also, that Holland doesn’t want to copy/paste the US: “you don’t want two cops”(?!). And finally, that the US simply started its investigation sooner.

Now, I’m not an expert in international banking law, but I do find it curious that a company pays far more in fines to foreign authorities than it does domestically, for having engaged in fraudulent behavior globally. For instance, does this mean Rabobank and RBS can expect fines from all 200-something countries on the planet? I doubt it.

The EU is preparing its own settlements with banks over various Libor and Euribor frauds, but it has already announced Rabobank won’t be fined over a yen Libor case it’s working on. I love the – partial – explanation for that: a large part of Rabobank’s involvement in yen Libor fraud consisted of internal communications between it own traders and benchmark submitters, and that means a charge of conspiracy to commit fraud is not applicable, because under antitrust law you can’t conspire with yourself.

So why do the Dutch let their own bank pay over $1 billion to foreign regulators, while they get less than 10% of that? I tell you, when I finally figured it out, I felt really stupid for not having thought of it before. It’s so simple: what Rabobank pays in fines abroad is tax deductible!! Of course! Now it all makes sense!

And I don’t know what exactly the situation is for RBS and Barclays and UBS, but I do have a hunch. You, the taxpayer, get to pay the fines. The EU will fine US banks a billion here and there in return, just for good measure, and use it to build a swanky office or two in Brussels, and bob’s your now poorer uncle.

There’s a lot more symbolism hidden in JPMorgan’s temporary takeover of Buckingham Palace that you might want to concede. But it getting ever harder to ignore, and you really shouldn’t.

Just to be clear on one thing: for people like Jamie Dimon, it’s all a big game. No matter what his bank is fined, he’s not paying it from his own pocket, the bank pays. It’s merely a matter of sport to try and lower the fine for the bank as much as possible, using billions in bank assets to pay lawyer’s fees.

But even more than that, it’s a way – while everybody else remains blissfully unaware, thinking this can’t possibly be true – to show kings and queens and regulators and justice departments and parliaments and presidents alike who’s really king of the world today.

Home › Forums › Who’s Really King Of The World Today