G. G. Bain Traveling bridge, Marseilles, France June 30 1910

There’s never just one side to any story. The eastern – largely ethnic Russian – past of Ukraine has been saying for a while that it feared being overrun by “hordes” of their western compatriots, who ousted Yanukovych and want to move closer to Europe. This morning the Russian Foreign Ministry stated that “Armed men dispatched from Kiev to the southern Ukrainian region of Crimea attempted an overnight storm of the local Interior Ministry”. Whether such a move, assuming there’s some truth to the statement, would be as much a reaction to Russia’s own recent military movements as it might have ulterior motives, is impossible to say.

Also, as the Guardian reports, the Ukrainian army is quite “formidable”. Its weakest point seems to be that it has a light presence in the Crimean region, ostensibly to not provoke the local people. Who have been told many stories of how ‘those from Kiev’ would come and take their land away, and their culture, force them to speak another language, and perhaps go after their wives and daughters too (as is the age-old way this story has been told). So they might be happy now that Russia sends troops and prevents that from happening.

But while it may seem to make sense that the Ukrainian soldiers of Russian descent, if they were to face the task of halting a Russian invasion, would hesitate, they may well feel they are Ukrainian first. Not so much those in the Crimea, but then, it wasn’t part of Ukraine until Khrushchev gave it away to Kiev as a present. People tend not to react favorably to being given away.

And don’t think the entire Crimea loves the Russians either: the sizeable population of Tartar lineage despises the long term occupier, which cast them from their lands for 40 years and only allowed them to return 30 years ago. It’s all just a matter of putting your pieces on the board as best you can before the game starts, and then hope you will see a move or two more ahead than the other players.

It’s not a US theater, the American army has failed in such circumstances time and again, but it’s not ideally suited for Russia either. Both rely on big armies with big guns, planes, trains and automo-armed vehicles, and that’s not guerrilla gear. Russia can’t win on the ground, but they have a much bigger chance behind the negotiating tables. Especially if it’s with the bungling EU side. Separate from each other, Germany has great contacts in the region, and France and Britain have unequalled secret service departments, but out them together under one command and they don’t function.

It may be more useful at this point to review Ukraine’s financial situation, since that may trump everything else, and prove to be the more crucial chessboard. Der Spiegel – really, the Germans have great inroads in the region – reports on the topic:

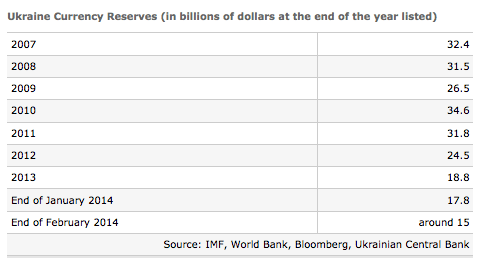

On Wednesday, Stepan Kubiv [governor of Ukraine’s national bank since Monday], noted that his country’s foreign currency reserves had dropped from $17.8 billion (€13 billion) to $15 billion just since the beginning of February, as the national bank attempted to prop up the exchange rate of the country’s currency, the hryvnia. Those efforts met with little success, and the hryvnia has fallen to a record low against the dollar.

And that’s not Kubiv’s only woe. Despite Ukrainian banks limiting cash withdrawals from ATMs, the central bank president says customers withdrew around $3 billion just during the three days of street battles last week, an amount equivalent to 7% of all deposits. On Friday, Kubiv announced that foreign currency withdrawals were being further limited to 15,000 hryvnia ($1,500) per day in order to calm the current volatility.

If we move back to Yanukovych for a moment, here’s a strong number: according to the new government, he made – or helped – $107 billion disappear. That could help build a few nice palaces:

Some $70 billion were taken out of the country in the last three years under Yanukovych, the new government revealed on Thursday, and $37 billion worth of state loans simply disappeared.

And that’s just the past. If more money is taken out of the country, everything could deteriorate very quickly:

So far, the government had pegged its financial requirements for the next two years at $35 billion. But that won’t be nearly enough if investors start pulling out of the country on a large scale.

So who’s going to volunteer to take the losses? Putin might, if he’s given free reign, but he won’t be, so why take losses?

The national bank projects that the loss of Russian credit in Ukraine wouldn’t amount to a dramatic change for Russia. According to the central bank’s calculations, Russian banks have less than 1% of their total assets invested in Ukraine. According to an estimate by ratings agency Moody’s, the four largest Russian financial institutions together have about $20 billion to $30 billion in Ukraine; Russian President Vladimir Putin put that number at $28 billion. From the Ukrainian perspective, though, that’s a considerable amount, with Russian banks’ market share in the country at 12%.

How about Euope then? $23 billion in outstanding loans in Ukraine, of which Italy alone has $6 billion, and Italy’s banks will have a hard time passing even highly compromised stress tests.

European banks, too, stand to lose in Ukraine. According to the most recent figures available from the BIS, European banks have more than $23 billion in outstanding loans in Ukraine. According to the statistics, German banks have lent only around $1 billion to Ukraine, but for Italy that figure is nearly $6 billion. “Italian financial institutions are already in the spotlight after the stress test for European banks,” says Bielmeier at DZ Bank. “Their involvement in Ukraine could increase that stress.”

But maybe it could have been worse. Still, Ukrainians will be subject to the IMF and its policies. Which have never helped one little man.

A long-lasting economic crisis in Ukraine … would not be in Russia’s best interest. “That naturally also has repercussions for joint companies we have with Ukraine,” Russian Economic Minister Alexei Ulyukayev told German business daily Handelsblatt. DZ Bank economist Bielmeier believes as well that these close ties may well be what will save Ukraine in the end. “The risk of national bankruptcy is not very high,” he says. “But only because none of the major blocs has an interest in that happening.”

It would seem Ukraine could use a few savvy negotiators. They could end up both safer and richer if they play their cards well. But with guys like Putin at the table, they will need to be proud as peacocks and have hardened poker faces. But it can be done.

• Amid Escalation Fears, Russia Says Kiev Sent Fighters to Crimea (RIA Novosti)

Armed men dispatched from Kiev to the southern Ukrainian region of Crimea attempted an overnight storm of the local Interior Ministry, the Russian Foreign Ministry said Saturday. “As a result of this perfidious provocation several people were injured,” the Foreign Ministry said in a statement. “This confirms that certain well-known political circles in Kiev are striving for the destabilization of the situation… we call on all those giving such orders from Kiev to show restraint.”

The allegation comes as international media report large scale Russian military movements in Crimea that have included tanks, helicopters and troops. In recent days heavily armed soldiers in unmarked uniforms have occupied the region’s parliament, airports and other strategic points across the peninsula. Reports from the regional capital of Simferopol on Saturday suggested that the military presence had been strengthened with the appearance of several manned machine gun positions around the parliament, which is flying the Russian flag after it was seized by unidentified gunmen earlier this week.

Ukrainian authorities have accused Russia of seeking to provoke a conflict. World leaders, including US President Barack Obama, have expressed their deep concern about the apparent Russian incursion into Crimea. Interim Ukrainian Prime Minister Arseny Yatsenyuk said Saturday that Russia should immediately recall all its troops to the bases where they are normally located. “If not, the responsibility for any armed confrontation provoked by the radicals being de facto supported by the Russian military will lie with the Russian leadership,” Yatsenyuk said.

Russia maintains that any military movements in Crimea are within the framework of a 1997 agreement regulating its use of Black Sea naval bases on the peninsula that it leases from Ukraine. Self-defense squads, which maintain that they will resist orders from Kiev, have been forming in the southern and eastern regions of Ukraine since the opposition swept to power in Kiev last weekend The Foreign Ministry said that the alleged assault on the Interior Ministry in Crimea on Saturday was fought off by some of these pro-Russian self defense squads. It did not specify which side suffered the casualties.

• Ukraine military still a formidable force despite being dwarfed by neighbour (Guardian)

Although Ukraine has a military force capable of making Russia think twice about invasion, it has a relatively light presence in the Crimea. Russia, by contrast, has for historical reasons a huge presence on the peninsula, with its Black Sea fleet based in Sevastopol. “It is a nightmare for everyone,” said Igor Sutyagin, a Russian military expert. “The entry of Russian troops would be a deep humiliation for Ukraine … It would be a second Chechnya.”

Russia has an overall military force of about 845,000 troops against Ukraine’s 130,000. Russia’s military spending is also vastly greater than Ukraine’s, $40.7bn last year compared with $1.4bn. But the Ukrainian forces are still formidable, better-trained, engaged over the last decade in international peacekeeping missions and established close contacts with western counterparts. Brigadier Ben Barry, a specialist on land warfare at the International Institute for Strategic Studies, said: “If there was ever military confrontation, the question is how much the morale and fighting-power of the Ukrainian forces would be boosted by fighting for their country.”

The small armed forces surrounding the two Crimea airports had no markings on their uniforms to identify them. Moscow denied responsibility but Kiev claimed the armed group at the Belbek airport, which is used by the Ukrainian air force and is close to Sevastopol, was made up of Russian marines. Barry said that what was striking about the forces at the airport is they do not look like a newly formed militia. “This is not a ragtag force. When you see a new militia, they will have a jumble-sale look. This lot are uniformly dressed and equipped and seem competent and efficient, ” he said.

Russia has put its combat planes on alert and has begun new training exercises, moves that prompted speculation of an impending invasion similar to the one into Georgia in 2008. But all-out invasion of Ukraine appears unlikely at present given that even if Russia was to win, it would face years of costly and bloody insurrection. Taking over just Crimea appears, at least initially, to be less risky given that more than half the population is ethnic Russian. As a peninsula, Crimea would be theoretically easy to defend.

Ukraine has only a single coastal defence unit in the Crimea, about 3,500-strong, with artillery but no tanks. But a Russian takeover of the Crimea could turn out to be disastrous in the long run. The Kremlin would be underestimating the impact of the sizeable population of Tartars who were forcibly deported from the Crimea by Stalin in 1944 and not allowed to return until the beginning of Perestroika in the 1980s.

Sutyagin, who is at the London-based Royal United Services Institute, said: “The Tartars are very anti-Russian. They will do anything not to be under the Russians. They will be determined to fight for Ukraine. It would be a second Chechnya. There are a lot of mountains in Crimea, just as in Chechnya.”

Many of the soldiers fighting in the Ukrainian army are ethnic Russians but it would be a mistake to assume they might desert or turn on their officers rather than take on Russian forces. Sutyagin said loyalty to the idea of an independent Ukrainian state would top their ethnicity. “The entry of Russian troops would be a deep humiliation for Ukraine. Ukrainians do not want to be occupied. It is a mistake by Russian politicians who think ethnic Russians are Russian,” Sutyagin said.

• The Uncertain Future of Ukraine’s Finances (Spiegel)

Stepan Kubiv, 51, looks as earnest as one would expect for the president of a central bank. Yet in Kubiv’s case, he has only held his office as the governor of Ukraine’s national bank since Monday. Prior to that, he was a “commandant” of Ukraine’s Euromaidan opposition movement, which managed to topple President Viktor Yanukovych. Now Kubiv must take up a different battle — keeping his country from financial collapse.

On Wednesday, Kubiv noted that his country’s foreign currency reserves had dropped from $17.8 billion (€13 billion) to $15 billion just since the beginning of February, as the national bank attempted to prop up the exchange rate of the country’s currency, the hryvnia. Those efforts met with little success, and the hryvnia has fallen to a record low against the dollar.

And that’s not Kubiv’s only woe. Despite Ukrainian banks limiting cash withdrawals from ATMs, the central bank president says customers withdrew around $3 billion just during the three days of street battles last week, an amount equivalent to 7% of all deposits. On Friday, Kubiv announced that foreign currency withdrawals were being further limited to 15,000 hryvnia ($1,500) per day in order to calm the current volatility.

Ongoing instability on the Crimea Peninsula has also not helped, with global stock exchanges hit hard on Thursday. Furthermore, the VTB on Thursday became the second major Russian bank to announce it was reducing its lending in Ukraine, which could cause businesses in the already economically stricken country to soon run out of cash. “Ukraine’s banking sector appears to be destabilizing considerably,” says Stefan Bielmeier, head economist at Germany’s DZ Bank.

These current developments are particularly worrying because Ukraine is already in danger of insolvency. Some $70 billion were taken out of the country in the last three years under Yanukovych, the new government revealed on Thursday, and $37 billion worth of state loans simply disappeared. So far, the government had pegged its financial requirements for the next two years at $35 billion. But that won’t be nearly enough if investors start pulling out of the country on a large scale.

But how likely is such a scenario? And who would be most seriously affected if it occurs? The national bank projects that the loss of Russian credit in Ukraine wouldn’t amount to a dramatic change for Russia. According to the central bank’s calculations, Russian banks have less than 1% of their total assets invested in Ukraine. According to an estimate by ratings agency Moody’s, the four largest Russian financial institutions together have about $20 billion to $30 billion in Ukraine; Russian President Vladimir Putin put that number at $28 billion. From the Ukrainian perspective, though, that’s a considerable amount, with Russian banks’ market share in the country at 12%.

European banks, too, stand to lose in Ukraine. According to the most recent figures available from the Bank for International Settlements (BIS), European banks have more than $23 billion in outstanding loans in Ukraine. According to the statistics, German banks have lent only around $1 billion to Ukraine, but for Italy that figure is nearly $6 billion. “Italian financial institutions are already in the spotlight after the stress test for European banks,” says Bielmeier at DZ Bank. “Their involvement in Ukraine could increase that stress.”

But of course the situation is most ominous for Ukraine itself. New Finance Minister Oleksandr Shlapak declared on Thursday that the situation was already stabilizing. At the same time, though, he announced that the country had asked the International Monetary Fund (IMF) for a financial injection of $15 billion. “We need to reach an agreement with the IMF immediately,” said new Prime Minister Arseniy Yatsenyuk. “As soon as we have an agreement with the IMF on a course of action, we will have funds for our reserves, and we will be able to stabilize the exchange rate.”

The IMF is certainly the obvious choice of partner for financial assistance, and an aid package would help to stem the risk of capital flight as well. But there’s another problem. “Normally, the IMF only extends loans to countries with a stable political system,” says DZ Bank head economist Bielmeier. “That’s the greatest stumbling block with Ukraine.” [..]

Russia’s government has made clear that it rejects the current political changes in Ukraine. If the IMF and EU step in with aid, it remains to be seen the degree to which Russia might economically sabotage the country. Ukraine is dependent on its eastern neighbor not only for financial loans, but for its supply of natural gas as well. In early February, the foreign trade and investment agency Germany Trade and Invest concluded that this conflict was “also being conducted using economic means,” for example with Russia apparently considerably increasing customs inspections for goods from Ukraine.

A long-lasting economic crisis in Ukraine, though, would not be in Russia’s best interest. “That naturally also has repercussions for joint companies we have with Ukraine,” Russian Economic Minister Alexei Ulyukayev told German business daily Handelsblatt. DZ Bank economist Bielmeier believes as well that these close ties may well be what will save Ukraine in the end. “The risk of national bankruptcy is not very high,” he says. “But only because none of the major blocs has an interest in that happening.”

• The New Great Game: Why Ukraine Matters to So Many Other Nations (BusinessWeeek)

Ukraine doesn’t seem like the kind of place that world powers would want to tussle over. It’s as poor as Paraguay and as corrupt as Iran. During the 20th century it was home to a deadly famine under Stalin (the Holomodor, 1933), a historic massacre of Jews (Babi Yar, 1941), and one of the world’s worst nuclear disasters (Chernobyl, 1986). Now, with former President Viktor Yanukovych in hiding, it’s struggling to form a government, its credit rating is down to CCC, a recession looms, and foreign reserves are running low. Arseniy Yatsenyuk, head of the opposition party affiliated with former Prime Minister Yulia Tymoshenko, said on Feb. 24 in Parliament, “Ukraine has never faced such a terrible financial catastrophe in all its years of independence.”

But Ukraine is also a breadbasket, a natural gas chokepoint, and a nation of 45 million people in a pivotal spot north of the Black Sea. Ukraine matters—to Russia, Europe, the U.S., and even China. President Obama denied on Feb. 19 that it’s a piece on “some Cold War chessboard.” But the best hope for Ukraine is that it will get special treatment precisely because it is a valued pawn in a new version of the Great Game, the 19th century struggle for influence between Russia and Britain.

Russia, which straddles Europe and Asia, has sought a role in the rest of Europe since the reign of Peter the Great in the early 18th century. An alliance with Ukraine preserves that. “Without Ukraine, Russia ceases to be a Eurasian empire,” the American political scientist Zbigniew Brzezinski wrote in 1998. Russian President Vladimir Putin wants Ukraine to join his Eurasian Union trade bloc, not the European Union. Russia’s Black Sea naval fleet is headquartered in Sevastopol, a formerly Russian city that now belongs to Ukraine.

Last year Russia’s state-controlled Gazprom sold about 160 billion cubic meters of natural gas to Europe—a quarter of European demand—and half of that traveled through a maze of Ukrainian pipelines. Those pipelines also supply Ukrainian factories that produce steel, petrochemicals, and other industrial goods for sale to Mother Russia. “Ukraine is probably more integrated than any other former Soviet republic with the Russian economy,” says Edward Chow, a senior fellow at the Center for Strategic and International Studies in Washington.

China looks to Ukraine as a secure source to satisfy its ravenous appetite for food and energy. It’s lending the country billions of dollars to upgrade farm irrigation and develop coal gasification. In December, Yanukovych and Chinese President Xi Jinping gripped and grinned while signing a “treaty of friendly cooperation.” According to the official China Daily, in addition to agriculture and energy, they agreed to collaborate on infrastructure, finance, high-tech, aviation, and aerospace.

Western nations want to keep Ukraine from becoming a failed state and to discourage Putin from retaking the nation by force. The U.S., busy with conflicts from Syria to Afghanistan, regards Ukraine as mainly the EU’s problem. The EU hopes eventually to welcome a stable Ukraine as a member, but not yet. On Feb. 25, EU policy chief Catherine Ashton stressed to reporters “the importance of the strong links between Ukraine and Russia.” Even Poland, which identifies with Ukraine because it too was once under the Soviet thumb, isn’t prepared to rescue its eastern neighbor unconditionally. “Poland will not sweat its guts out” providing foreign aid that just props up oligarchs, Prime Minister Donald Tusk said on Feb. 24, according to the New York Times.

The geopolitical struggle comes down to money. Russia pledged $15 billion in loans to pull Ukraine into its nascent Eurasian Union, but after paying out $3 billion it has put further funds on hold. On Feb. 26, Secretary of State John Kerry said the U.S. was organizing a stopgap $1 billion loan guarantee—far short of the $35 billion in aid Ukraine is seeking. The Institute of International Finance, which represents big banks, estimates that with no change in policy Ukraine would need $30 billion in foreign assistance this year alone. The IIF predicts that the International Monetary Fund will insist as a condition for aid that Ukraine cut natural gas subsidies to consumers and industry, and allow its currency, the hryvnia, to fall further, shrinking the trade deficit. The problem: Those measures will be so unpopular that they will jeopardize any new government.

The risk is that Ukraine will disintegrate. Opposition parties united only in their hatred of Yanukovych range from Europhile democrats to rightist nationalists. If the West doesn’t manage to stabilize Ukraine, Putin could plausibly present himself as the nation’s savior a year or two from now.

Ukraine stumbled after the Orange Revolution of 2004-05; the oligarchs kept power. The rebellion that brought down Yanukovych is a second chance. “The awakening of the people is much stronger this time,” says Oleh Shamshur, a former ambassador to the U.S. For those who want a free and democratic Ukraine, says Timothy Ash, chief emerging-market economist at Standard Bank in London, “it’s now or never.”

• China’s Central Bank Gets Its Yuan On (Bloomberg)

The 1.3% decline in the Chinese yuan against the dollar during the past week says little about China’s long-term growth outlook and a lot about the central bank’s willingness to flex its muscles. To understand why, remember that the People’s Bank of China has firmly managed the exchange rate ever since the mid-1990s. As with everything else, the price of a currency is determined by the interactions of buyers and sellers, whether they are businesses looking to build factories or households trying to find the best places to allocate their savings.

To fix prices, the PBOC announces a target rate and then buys (or sells) enough assets denominated in other currencies, such as U.S. Treasury bonds, to offset the flows of capital from domestic and foreign investors. This job is made easier by regulations that limit these capital flows. Reformers in China know that this hurts households and encourages excessive investment, which is why they have pushed for the “internationalization” of the currency as a way to break down the existing capital controls.

In a separate vein, China’s super-rich have proven quite adept at sneaking their assets into other countries, especially those such as Canada and Australia that make it easy to obtain citizenship if you buy a lot of property — a smart strategy for those worried about unrest over rising inequality, or ending up on the losing side of a factional dispute.

From the middle of 1995 through the middle of 2005, the yuan traded at 8.3 to the U.S. dollar, with almost no variation. This wouldn’t have happened if the PBOC’s foreign assets hadn’t grown from about $73 billion to about $725 billion during that period. Private investors were clamoring to move money into China to take advantage of its rapid productivity growth. This should have translated into rising household incomes, an appreciating currency and the emergence of a trade deficit. That’s what happened in the U.S. in the second half of the 19th century, as the country imported capital from the U.K. and the Netherlands to support investments in infrastructure and manufacturing.

Yet the yuan remained cheap because the Chinese central bank sold trillions of yuan propping up the value of the U.S. dollar. Partly in response to pressure from the U.S. and partly to offset rising commodity prices, the Chinese government let the currency appreciate 35% since mid-2005. The yuan would have appreciated far more, if the Chinese central bank hadn’t intervened by buying $3.1 trillion worth of foreign assets.

Investors have been trying to get around the capital controls this whole time. Foreigners who expect that China will eventually stop suppressing its exchange rate find creative ways to get money inside to profit from what they see as the inevitable appreciation of the yuan. The danger is that this hot money can leave as quickly as it arrived, which would destabilize the Chinese economy. China could get out ahead of the speculators with a surprise revaluation of the yuan that raised the currency 30% to 40% higher, after which the currency would float freely.

This line of thinking could also explain the sudden depreciation. There is no better way for the PBOC to discourage people from betting on the yuan’s appreciation than suddenly shoving the currency in the other direction.

• UK-Spain police swoop on boiler room shares fraud leads to 110 arrests (Guardian)

Criminal gangs blamed for fake-share scams that robbed British victims of millions of pounds in savings have been rounded up in an international crackdown involving UK police. Officers from City of London Police joined Spanish counterparts from the Policia Nacional in a series of raids in Barcelona, Madrid, Marbella and London in one of the biggest anti-fraud operations ever staged. There were further arrests in the US and Serbia. Details are being reported for the first time after a ban on publication was lifted by a Spanish judge.

A total of 110 people were held by police on accusations of participating in boiler room fraud, where investors are duped into buying worthless or non-existent shares. Investigators targeted a number of organised crime gangs. One of the suspects was believed to be paying £40,000 per month to rent an apartment. An Aston Martin and Ferrari were among the cars seized by police, along with various watches and £500,000 in cash.

Speaking near the site of one of the searches in Barcelona on Tuesday, City of London police Commander Steve Head, said: “What we’ve seen today is the culmination of a two-year investigation that has been worldwide in its nature. What we’ve seen is an unprecedented level of co-operation.

“We expect this network alone to have upwards of 1,000 victims. We’ve seen millions of pounds taken from people. “You see real victims in real communities whose lives have been devastated. Savings that they thought they could rely on in their old age have gone in a heartbeat.” The international team executed 35 warrants on offices used to run the fraud, as well as the homes of the accused. So far 850 UK victims of the gangs had been identified, mainly pensioners, who had lost a total of around £15m, police said, adding that thousands more might have been affected.

• Rome spared bankruptcy as Italy approves €500m rescue (Guardian)

Decadent and in decline, its beauty imperilled by physical and moral decay, the Rome portrayed in Paolo Sorrentino’s film La Grande Bellezza could end up giving Italy a yearned-for win at the Oscars on Sunday night. But off-screen and far from the glitz of Hollywood, the financial troubles of the eternal city – and the daily trials of its long-suffering residents – are no cause for celebration.

On Friday, at the end of a week which saw the spectre of bankruptcy loom large over the ancient capital, the Italian government said it had approved a last-minute decree that would give an urgently-needed injection of funds to the city, thus staving off imminent disaster. While not detailing the new plans, cabinet undersecretary Graziano Delrio said the sum to be transferred to the municipality “remains the same” – around €500m – as had been envisaged under a previous decree ditched earlier in the week by the government.

Nicknamed “Save Rome”, that decree had become so bogged down in a verbose and venomous parliamentary process that Matteo Renzi’s new administration withdrew it and said it would find a new way of helping the Rome authorities plug an €816m hole in their budget.

The decision prompted thinly-veiled hilarity among some in the opposition, with one MP for the rightwing, regionalist Northern League suggesting the best thing for the city would be a takeover by a special commissioner in the mould of hated emperor Nero, who fiddled while Rome burned. But on the Capitoline hill, where mayor Ignazio Marino is based, the decision sparked rage. In a furious outburst, the transplant surgeon-turned-centre-left politician said the capital risked a shutdown of public services as soon as next week if a replacement decree was not passed immediately.

Making it clear he would resign rather than implement swingeing cuts and mass lay-offs, he even said that plans for the canonisations of popes John Paul II and John XXIII in April would be put at risk if a transfer of funds was not guaranteed. “I promised Pope Francis, in a personal meeting with him, that I would take care to prepare everything,” Marino was quoted as saying. “If there aren’t the conditions in which to do so, I will tell the government that there aren’t the conditions in which I can be mayor.”

His comments set him on a collision course with Renzi, Italy’s new prime minister. On the front of Friday’s Corriere della Sera, the two Democratic Party politicians were depicted as Romulus and Remus suckling on the she-wolf of Rome’s founding myth. “There is no more latte [milk]!” says the unhappy mayor of Rome. “There is no more Letta!” replies Renzi – a reference to his recently-ousted predecessor. “And I am from Florence!”

The new decree appeared enough to ease tensions between the two men, but it will take a lot more to soothe the many dissatisfied citizens of the Italian capital who are indignant following years of parlous finances and bad government. “You want to bring the city to a standstill and have not realised that the city is already at a standstill,” wrote one commentator, Rome-born Marco Sarti, in an open letter to the mayor published on news site Linkiesta in which he cited the capital’s potholed roads, its “embarrassing” underground rail network and its general air of “degradation and filth”.

• Home ownership in Greece ‘a sick joke’ as property market collapses (Guardian)

There is constant motion on the second floor of 24 Kanari Street. At the Athens office of Remax, Greece’s largest property company, clients come and go, agents slip in and out and brokers pace the corridors barking into mobile phones. For Christos Vergos, it means a frenetic work schedule of 12-hour days and a client base that is ever growing. “At all hours, people call in wanting to sell or wanting to rent or wanting to expand because places now are so much cheaper,” says the estate agent in a conference room overlooking Kolonaki Square.

In a market that has hit rock bottom in the maelstrom of Greece’s financial meltdown, basement flats are selling for as little as €5,000 (£4,150) in the less salubrious parts of Athens. On the isle of Mykonos, cash-strapped Greek celebrities have been selling luxury villas for a song. But Vergos prefers to focus on another figure. “Last year, there were just 3,600 sales in all of Athens – I repeat, all of Athens.”

Greece’s social and economic crash is reflected in its property slump. Data released by Eurostat, the EU’s statistics agency, earlier this month showed that the country had suffered the second steepest decline in house prices after Croatia, the bloc’s newest member.

Since the outbreak of the Greek debt crisis four years ago, property values nationwide have dropped by around 32%, according to the Bank of Greece; estate agents contacted by the Guardian estimated the decline at nearer 50%. “At their peak, in 2005, in the euphoria of the Olympic Games, there were 250,000 sales in Athens,” said the property analyst Christos Bletas. “The lack of interest displayed last year, partly because of the incredible rise in property taxes, hasn’t been experienced since the second world war.”

Owners may be desperate to offload, but in a climate of pervasive uncertainty there are few who want to buy. With over a third of households unable to meet tax obligations, four out of 10 Greeks recently told a Kapa Research poll they would willingly hand over properties to the state to fulfil future payments; one in three, unable to keep up mortgage repayments, feared their homes would be confiscated in 2014.

The situation, says Bletas, is so dire that home ownership – at nearly 87% the highest in the EU – has become cause for black humour. “The joke now doing the rounds is: if you want to punish your child, you threaten to pass on property to them,” he said. “Greeks traditionally have always regarded property as a secure investment. But now it has become a huge millstone, given that the tax burden has increased sevenfold in the past two years alone.”

At no time has there been such a glut of property on the market, according to the Hellenic Property Federation (Pomida), which reckons more than 500,000 property owners want to sell. Across Greece, about 300,000 residences are believed to be empty. “For northern Europeans who want to buy a holiday home or a plot to develop for business, it’s a golden opportunity,” says Stratos Paravias, Pomida’s president. “The tax burden is not so big when you have one property; it is when [like most Greeks] you have two or more.”

With about 500 properties on his books, Manolis Akalestos, who runs the Scopas estate agency on the island of Paros, confirms that view. In the past year he has been deluged with requests for holiday homes from foreigners, many encouraged by the drop in prices and a new law granting non-EU citizens residence permits.

“In 2013, I had my best year yet, with 90% of all sales being made to people overseas,” he said. “Before, property prices were incredibly inflated because every Greek was able to get a cheap loan after our entry into the eurozone,” he explained. “And foreigners took a step back. Now that prices have calmed down and returned to natural levels, they are coming back with a vengeance.” With the market’s stagnation also being blamed for the lack of liquidity in Greece, politicians across the board are quietly hoping that non-Greeks will help save the day.

“In Crete, where I am from, a lot of investment went into housing for foreigners, and it was the first to collapse,” said Giorgos Stathakis, the shadow development minister for the radical left main opposition Syriza party. “Foreigners stopped buying, or started selling off their houses, when the crisis began in 2010. “We are in a very peculiar situation where prices are falling but the market isn’t moving. If the recession eases in Europe, and foreigners start to return, it would be part of the solution to one of Greece’s biggest problems.”

• Iceland Seen Threatened by Capital Flight From Its Own Citizens (Bloomberg)

U.S. hedge funds aren’t the only ones trying to exit Iceland. Its own citizens may follow if the government doesn’t show it can lift capital controls in place since 2008 without triggering a currency sell-off, according to Iceland’s biggest insurance firm. “If people lack confidence, they will take their money elsewhere as soon as the controls are lifted,” Sigrun Ragna Olafsdottir, chief executive officer of Vatryggingafelag Islands hf, said in an interview in Reykjavik. “And here I’m referring to Icelanders, not just foreigners. This presents a much greater threat to the Icelandic economy than if foreigners decide to leave.”

Iceland has yet to test the staying power of its economic recovery. Capital controls, imposed at the end of 2008 after the island’s three biggest banks defaulted on $85 billion, have so far stopped offshore investors selling $7.2 billion in assets, equivalent to half the nation’s gross domestic product.

Hedge funds, including Davidson Kempner Capital Management LLC and Taconic Capital Advisors LP, bought claims on the banks’ assets at prices well below face value. Five years later they’re still waiting to cash in. Efforts to speak with the government, communicated by the winding up committees of the failed banks, have fallen on deaf ears.

Prime Minister Sigmundur D. Gunnlaugsson said last month he won’t negotiate with speculators and underlined his commitment to removing capital controls in a way that underscores financial stability. “It’s in everyone’s interest to create a situation which would allow for the lifting of controls,” Gunnlaugsson said in January. There are signs investors are growing wary. Since hitting a low in June, the cost of insuring against losses on Iceland’s debt using credit-default swaps has risen about 50% to 190 basis points, according to data compiled by Bloomberg.

Though Iceland has managed to reduce its public debt to 82% of gross domestic product, the island still has net external debt equivalent to 436% of GDP, central bank statistics show. Iceland may need help from the other Nordic governments to help it through a transition out of capital controls, according to Lars Christensen, chief emerging markets analyst at Danske Bank A/S in Copenhagen. “The best way would be to try to negotiate some kind of a standby agreement with the other Nordic central banks to try to provide some support for the krona in a period,” he said by phone. “But that can be quite challenging.”

Iceland said back in 2008 the capital controls would be a temporary measure to protect its markets during the darkest hours of the crisis. The International Monetary Fund, which has praised the island’s crisis management program, says removing currency restrictions is key to restoring economic health.

The main concern for Icelanders now is whether they’ll be lifted without jolting markets and disrupting a recovery. The economy will expand 2.7% this year, according to the Organization for Economic Cooperation and Development. That’s better than the average for the OECD-area as a whole, which will grow 2.3%, the Paris-based group estimates.

Shielded by capital controls, companies like Vatryggingafelag have grown without needing to fend off the vagaries of market swings. Since the insurer went public last April, its stock has gained 15%. Yet the flipside is that companies can’t draw on foreign investors, limiting growth. “We’ve been waiting for the investment environment to improve with more investment opportunities,” said Olafsdottir. “That seems to be picking up although the capital controls have a severe impact on that.”

• UK spies on millions of Yahoo! webcams, ogles sex vids (Register)

British spies allegedly intercepted and stored nude pics and other stills from millions of Yahoo! Messenger webcams – and mulled capturing snaps from the XBox’s Kinect camera, too. The UK intelligence agency GCHQ started slurping photos from innocent netizens’ camera feeds in 2008, The Guardian reported today. In just one six-month period alone, pics from 1.8 million Yahoo! users were pulled into government servers. Blighty’s hush-hush nerve-center was also said to have explored the possibility of intercepting footage from the Kinect camera for Microsoft’s Xbox 360 games console as it generated “fairly normal webcam traffic.”

We’re told the British g-men made an unfortunate discovery while allegedly harvesting the snaps: between three and 11 per cent of the obtained Yahoo! webcam pics contained “undesirable nudity.” Although Yahoo!’s instant messaging service uses SSL to encrypt passwords when logging in, it does not prevent network eavesdroppers from intercepting, decoding and storing text messages and live webcam feeds between contacts. It’s alleged GCHQ grabbed stills from active cam chat sessions every five minutes – regardless of whether the users were suspected of any wrongdoing.

“Unfortunately … it would appear that a surprising number of people use webcam conversations to show intimate parts of their body to the other person,” GCHQ wrote in a document leaked by ex-NSA whistleblower Edward Snowden to the newspaper. “Also, the fact that the Yahoo software allows more than one person to view a webcam stream without necessarily sending a reciprocal stream means that it appears sometimes to be used for broadcasting pornography.” The spy agency did try to protect the delicate sensibilities of its staff, with a handbook note stating: “There is no perfect ability to censor material which may be offensive. Users who may feel uncomfortable about such material are advised not to open them.”

Yahoo! was incensed by The Guardian’s report. “We were not aware of nor would we condone this reported activity. This report, if true, represents a whole new level of violation of our users’ privacy that is completely unacceptable, and we strongly call on the world’s governments to reform surveillance law consistent with the principles we outlined in December,” Yahoo! told The Register. “We are committed to preserving our users’ trust and security and continue our efforts to expand encryption across all of our services.”

• Citi Paid $400 Million in Fake Mexico Oil Services Invoices (Bloomberg)

As far as I can understand it from Citigroup’s press release, which is not very far, here’s how Oceanografia S.A. de C.V. took Citi’s Mexican subsidiary, Banamex, for $400 million:

- Oceanografia is an oil services company that, until recently, performed oil services for Pemex, the Mexican state oil company.

- Oceanografia would perform some services and send Pemex a bill.

- Pemex would be like, “thanks, we’ll get right on this,” and then put the bill in its files somewhere.

- Meanwhile, Oceanografia would send another copy of the bill to Banamex.

- Banamex would pay Oceanografia the amount of the bill (less some discount obviously), and then wait to be paid back whenever Pemex got around to paying it.

- Oceanografia eventually realized that there was a more efficient system.

- In the more efficient system, Oceanografia wouldn’t perform oil services, or send Pemex a bill.

- They’d just make up a bill, write some numbers on it, and send it to Banamex.

- Banamex would pay it and wait, in vain, to be paid back by Pemex.

This went on for years? That to me is the oddest part. Oceanografia is — somewhat obviously — not a public company, but a random assortment of pseudo-comps suggest that typical accounts receivable turnover in the oil-services industry averages around three months.1 One imagines that Pemex gets more breathing room than the average customer, but still, at some point, wouldn’t Banamex call Oceanografia after not getting paid for a year or two? Did Oceanografia just say “yeah, I know, what jerks, they’re really slow, keep trying”?2 And Banamex kept extending more credit on more fake receivables, to a total amount of $585 million? And never called Pemex?

Eventually they called Pemex, after “Oceanografia was banned on Feb. 11 by Mexico’s anti-corruption agency from bidding on government contracts for 21 months because it violated agreements with Petroleos Mexicanos,” at which point:

Citi, together with Pemex, commenced detailed reviews of their credit exposure to OSA and of the accounts receivable financing program over the past several years. As a consequence of these reviews, on February 20, 2014, Pemex asserted that a significant portion of the accounts receivables recorded by Banamex in connection with the Pemex accounts receivable financing program were fraudulent and that the valid receivables were substantially less than the $585 million referenced above. Based on Citi’s review, which included documentation provided by Pemex, Citi estimates that it is able to support the validity of approximately $185 million of the $585 million of accounts receivables owed to Banamex by Pemex as of December 31, 2013.

So Citi charged off $400 million, though that only reduced profits by $360 million pre-tax ($235 million after-tax) because of “an offset to compensation expense of approximately $40 million associated with the Banamex variable compensation plan.” So Banamex executives are chipping in about 10% of the money they lost, which seems generous until you remember that Citi’s compensation ratio is around 38%. You get paid 38% of what you make, give back 10% of what you lose, and you’ve got a good business going.

• Why the Periphery Is Crumbling (OfTwoMinds)

While it is clear that the instability in periphery nations is arising from dynamics unique to each nation, there is one unifying causal factor: the spoils system in each nation is breaking down. Every nation-state, from brutal dictatorships to nominal democracies, ultimately depends on a spoils system that provides the various factions, classes, etc., with sufficient material and status benefits to accept the Status Quo arrangement.

The more a regime relies on oppression for its legitimacy (for example, North Korea or Saddam’s Iraq), the greater its vulnerability to erosion in the spoils system, which naturally favor the military and the regime’s Elites. In broad brush, the spoils available for distribution are the surplus generated by the national economy. In the case of North Korea, this surplus stems from extortion (of donations from other nations), satrapy (free oil from China) and illicit activities (arms sales and counterfeiting). A common source of surplus is oil (Venezuela, Iraq, Iran) or some other desirable commodity.

The vast majority of surpluses outside oil exporting nations have been generated by three factors: cheap energy, rising productivity and the expansion of credit. If we examine periods of rapid expansion and generalized prosperity, we find these three factors were active: cheap energy, rising productivity and ample credit. Just look at Europe and the U.S. in the 1950s and 60s, Japan in the 1960s and 70s, and China in the 1980s and 90s for examples.

Any reversal in these factors reduces surplus and the spoils being distributed. Sharply higher energy costs crimp profits and cause recessions, stagnating productivity leads to near-zero growth and institutional/state sclerosis and credit contraction leads to recession and the destruction of malinvestments.

Since ruling Elites are by definition constantly picking winners and losers, any Status Quo operated by Elites is systematically malinvesting on a gargantuan scale. This is the ontological imperative of any Elite: skim as much of the national surplus as possible and funnel it to cronies and loyal toadies. The prudent Elites (and imprudent Elites don’t last long–the spoils system is quite Darwinian) set aside enough surplus to distribute as spoils, effectively buying the complicity of key sectors, classes, factions, etc.

Thus the default policy of any ruling Elite is bread and circuses: supply the potentially disruptive masses with food and entertainment, and they’ll continue their grudging support of whatever arrangement is supplying the bread and circuses. Any mob that appears threatening can be dissipated with a “whiff of grapeshot.”

In the U.S., the spoils system is almost unlimited: corporate welfare for capital, food stamps and SSI disability for the lumpenproletariat, big-bucks jobs as water-carriers for the Elites for technocrats in the State, finance, think tanks, elite universities and Corporate America sectors, a variety of quasi-secure lower-level positions as enforcers, lackeys, apparatchiks and factotums and a smattering of tax subsidies (mortgage interest deduction, etc.) to placate what’s left of the non-state-dependent middle class.

The spoils system is not only the foundation of every Elites’ political legitimacy, it is the thin layer of plaster that covers all the longstanding ethnic, regional, linguistic, religious and political fault lines that run beneath current nation-state arrangements. Numerous national borders were drawn after World War II (1945) with little regard for historical divisions between various groups or preceding borders. Entire nations were penciled into existence by Imperial diktat in complete disregard for existing historical groups–Iraq and Syria being just two examples of many. As long as the stick of repression and the carrot of the spoils system were sufficiently persuasive, the tectonic plates beneath the regime were masked. But once the spoils system and the machinery of suppression crack, the old rivalries arise anew.

The spoils system can crack for two reasons: either the national surplus declines so there simply isn’t enough spoils left to keep everyone placated, or the spoils diversion to the Elites and their cronies exceeds the tipping point of legitimacy. Greece and Venezuela are examples of the first dynamic, and Ukraine is an example of the second dynamic. Greece essentially funded its vast spoils distribution system with borrowed money. When the regime’s free-money machine finally broke, the spoils system crashed along with the legitimacy of the Status Quo. Venezuela is suffering a similar crash, based not on a withdrawal of credit but on the current Elites’ destruction of the nation’s oil industry and what was left of its productive private economy.

In Ukraine, the plundering of the national surplus by oligarchic Elites finally exceeded the populace’s threshold of legitimacy, and once the armed forces and police refused to murder their cousins, brothers, nieces and nephews in the streets, the Status Quo arrangement collapsed. Now that the spoils system has crumbled, all the historical tectonics and fault lines are emerging in full force. the same can be said of Iraq and many other inherently unstable nation-states/regimes.

Why is the periphery crumbling? It’s simple: the conditions that enabled rising national surpluses and the distribution of spoils is breaking down for three reasons:

1. Energy is no longer cheap (compared to past prices)

2. The low-hanging fruit of higher productivity has all been plucked

3. The free-money flood of cheap, limitless credit is drying up

As regimes find surplus and credit are both contracting, their ability to placate every key group with spoils is also declining, and the conflicts between them can no longer be patched over with bribery or brutality.

This article addresses just one of the many issues discussed in Nicole Foss’ new video presentation, Facing the Future, co-presented with Laurence Boomert and available from the Automatic Earth Store. Get your copy now, be much better prepared for 2014, and support The Automatic Earth in the process!

Home › Forums › Debt Mar 1 2014: Peacocks and Poker Faces