Pablo Picasso Brick factory at Tortosa 1909

From an email sent to Mish.

• Emerging Markets and US Treasuries (Albert Edwards)

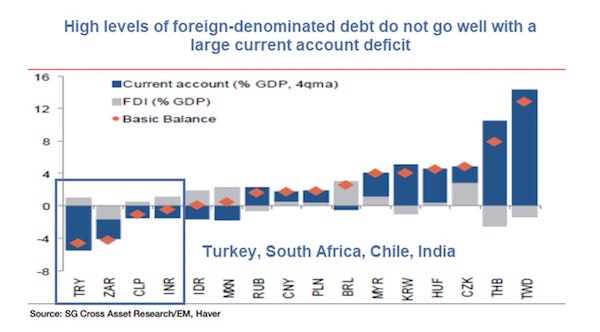

Turkey has discovered that high and rising foreign-denominated debt never sits well with a huge current account deficit and a reluctance to raise interest rates. The problem though is that this is not about Turkey or even EM. It is as always, about the Fed. When the most important person in the free world starts lobbing macro hand-grenades in an effort to drain the swamp, the financial markets will always eventually react badly. No, I am not talking about President Trump with his tweets about imposing tariffs on Turkey. I am actually talking about Fed Chair Jerome Powell draining the global liquidity swamp.

Make no mistake, whatever the macro-idiosyncrasies of Turkey, the key to the current turmoil that is spreading into EM generally, is Fed tightening and the strong dollar. As we have repeated ad infinitum, since 1950 there have been 13 Fed tightening cycles, 10 of them ended in recession and the others usually saw the EM blow up – such as the 1994 collapse in the Mexican peso. The Fed always tightens until something breaks. It is usually its own economy, but sometimes it is the EM’s. And when the liquidity tide goes out we always find out who is swimming naked. If it hadn’t been Turkey it would eventually have been someone else.

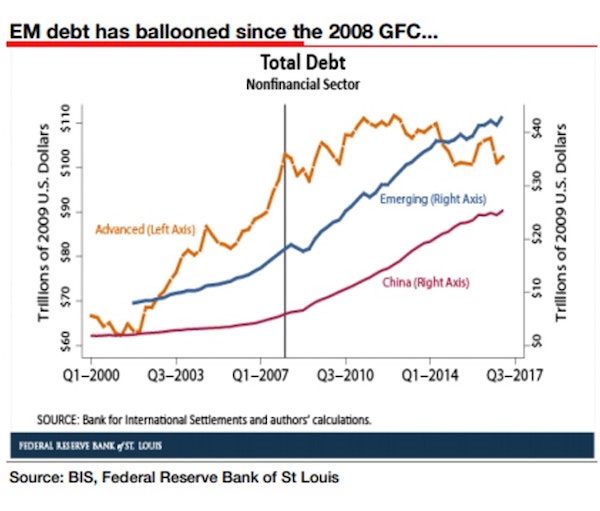

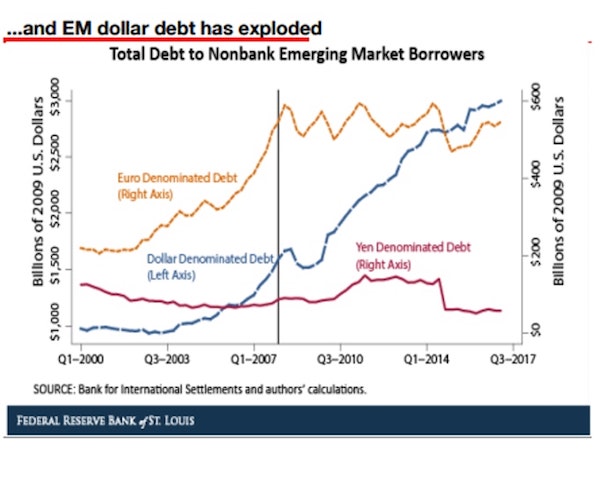

To be sure the unfolding EM crisis has been building for many years. And just as investors ignored the naysayers in the run-up to the Global Financial Crisis (GFC), they have ignored the IMF and BIS, who have been cautioning for some years about the explosive build-up in EM debt and especially dollar-denominated debt. According to the BIS, total dollar-denominated debt outside the U.S. reached $10.7 trillion in the first quarter of 2017, and about a third of this debt is owed by the EM nonfinancial sector. EM specialists, the Institute of International Finance (IIF), have also warned about this build-up in EM foreign-denominated debt. They too note that the EM corporate sector has been leading the explosion of debt, with Turkey standing out for the increase in its exposure since the GFC. Turkey has never managed to escape membership of ‘The Fragile Five’ EM country club.

Dollar shortages.

• Asia the Next Source of Downside Systemic Risk for Financial Markets (WS)

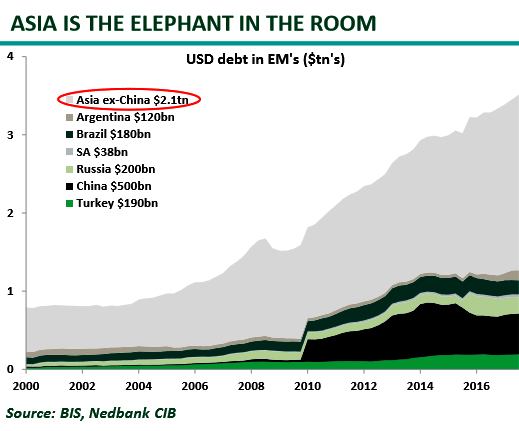

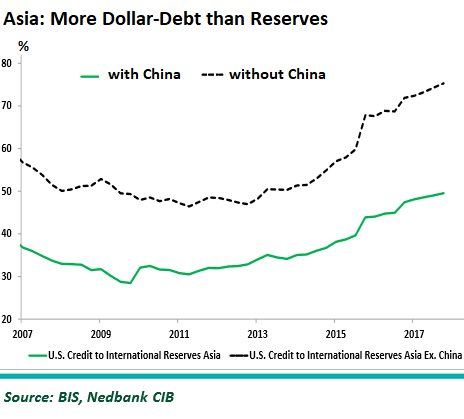

“Except for an expected short-term reprieve, we expect these tighter USD conditions to remain in place for the rest of the year,” the strategists write. “That is unless policy makers react soon to stimulate financial markets with liquidity.” “Southeast Asia stands out again as in 1997/8, with a large amount of USD denominated debt outstanding,” the write. “The only difference is then Asia had fixed exchange rates and now they are floating! We believe Asia will be the next source of downside systemic risk for financial markets.” The chart below shows dollar-denominated debt in the EMs, in trillion dollars. This does not include euro-denominated debt which plays a large role in Turkey. The fat gray area represents Asia without China:

Asia’s dollar-denominated debt, relative to its foreign exchange reserves and exports, has risen significantly since 2009, they note. The chart below shows the ratio between dollar-denominated debt and foreign exchange reserves in Asia, with China (green line) and without China (black dotted line). Values over 50% mean that there is more dollar-debt than foreign exchange reserves:

“This leaves these nations susceptible to a shortage in USDs,” they write: “Notably, the Asian nations that have amassed record amounts of USD debt are also home to the largest technology companies i.e. Tencent (China), Alibaba (China), TSNC (Taiwan), Samsung (South Korea). The tech sector is now 28% of the MSCI EM index. The rally in the US Dollar, dented global growth prospects, credit growth in China slowing down and escalating political tensions from the US leaves these nations very exposed to a shortage in USDs.”

More sanctions. Yesterday’s relief is gone.

• Trump Says US ‘Will Pay Nothing’ To Turkey For Release Of Detained Pastor (R.)

U.S. President Donald Trump said on Thursday the United States “will pay nothing” to Turkey for the release of detained American pastor Andrew Brunson, who he called “a great patriot hostage.” “We will pay nothing for the release of an innocent man, but we are cutting back on Turkey!” Trump said on Twitter. The U.S. warned Turkey on Thursday to expect more economic sanctions unless it hands over Brunson, as relations between the two countries took a further turn for the worse. U.S. Treasury Secretary Steven Mnuchin assured Trump at a Cabinet meeting that sanctions were ready to be put in place if Brunson was not freed. “We have more that we are planning to do if they don’t release him quickly,” Mnuchin said during the meeting.

The United States and Turkey have exchanged tit-for-tat tariffs in an escalating attempt by Trump to induce Turkish President Tayyip Erdogan into giving up Brunson, who denies charges that he was involved in a coup attempt against Erdogan two years ago. “They have not proven to be a good friend,” Trump said of Turkey during the Cabinet meeting. “They have a great Christian pastor there. He’s an innocent man.” Trump’s national security adviser, John Bolton, had issued a blunt warning to Turkish ambassador Serdar Kilic when he met him on Monday at the White House, an administration official said on Thursday. When Kilic sought to tie conditions to Brunson’s release, Bolton waved them aside and said there would be no negotiations.

But that was yesterday. Today, the lira’s lost 4% already.

• Lira Rallies As Turkey Pledges Spending Cuts To Avoid IMF Bailout (G.)

Turkey’s finance minister sparked a recovery in the lira after he addressed thousands of international investors, pledging to protect beleaguered local banks and cut public spending to prevent the country defaulting on its loans. Berat Albayrak, who has faced criticism for failing to tackle the country’s growing financial crisis, spoke to around 6,000 investors on a conference call to rebuff concerns that a funding squeeze on Turkey’s banks and a damaging trade war with the US would force him to seek a rescue bailout from the IMF. Albayrak, who was appointed as finance minister last month by his father-in-law, president Recep Tayyip Erdogan, said Turkey will not hesitate to provide support to the banking sector, which was capable of accessing funds itself during the current turmoil in financial markets.

He added that deposit withdrawals by panicked investors remained low and manageable. “We are experiencing unfavourable conditions but we will overcome,” he said. The Turkish lira was up 4% against the US dollar following the conference call and after reassuring words from the French president, Emmanuel Macron, and Germany’s chancellor, Angela Merkel, that Turkey’s stability was important. However, Albayrak’s attempt to shore up confidence in the lira was quickly undermined by the US Treasury secretary, Steve Mnuchin, who reportedly told president Donald Trump in a cabinet meeting that he was preparing further sanctions against Ankara. The lira slipped back to settle at just 1% up on the previous day.

It’s not Spain or Italy. It’s Britain.

• Turkish Tremors Will Cause Shocks In Britain (Times)

There are many strange things about Recep Tayyip Erdogan, but one of the oddest is his pet theory about interest rates. The Turkish president believes that high borrowing costs produce high inflation. “The interest rate is the cause and inflation is the result,” he said a few months ago. “The lower the interest rate is, the lower inflation will be.” No, you didn’t misread that. In defiance of economic orthodoxy (not to mention centuries of experience) which says that high interest rates tend to reduce inflation, President Erdogan believes the opposite. As one economist put it, this is a little like believing that umbrellas cause rain.

The Turkish president’s eccentric attitude towards monetary policy is not the only reason his country is now facing an economic crisis, but it is at least part of the explanation. Over the past decade or so, Turkey became one of the great bubbles of the modern era. Housing bubble? Check. Debt binge? Check. Yawning current account deficit? Check. Runaway inflation? Check. These traits alone qualified the Turkish economy for crisis candidacy some time ago. But as always, saying a country is due a crunch is far simpler than predicting when and how. And Turkey may well have muddled through a little longer were it not for four critical ingredients.

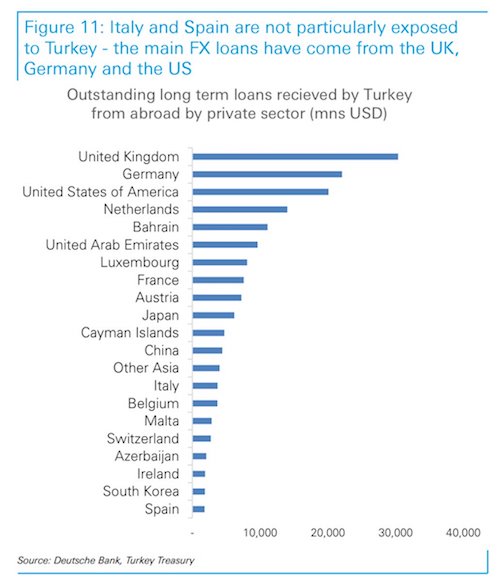

[..] Who is most exposed to this looming crisis? Conventional wisdom says Spain and Italy, whose banks have Turkish subsidiaries. However, this slightly misses the point, since much of that lending is in lira. Those banks should be able to survive even the loss of their stakes. The real question is: who has been lending Turkish companies all this foreign exchange debt? That brings us to the sting in the tail. For when you dig through Turkish treasury data, as the Deutsche Bank economist Oliver Harvey has, you discover that the country that lent most to Turkey, both short and long term, was the UK. That’s right: Britain, or more specifically the City of London, is by far the most exposed to a collapse in the Turkish economy.

Creative accounting 101.

• $125,000: The Pension Debt Each Chicago Household Is On The Hook For (WP)

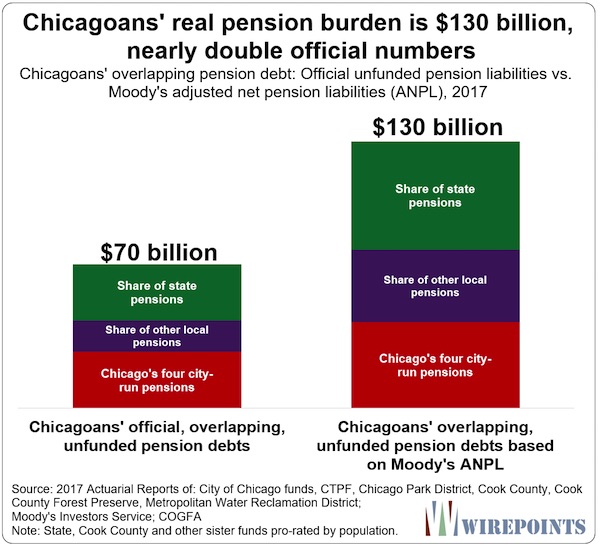

Chicagoans have no idea how much pension debt Illinois politicians have saddled them with. Officially, Windy City residents are on the hook for $70 billion in total pension shortfalls from the city and its sister governments plus a share of Cook County and state pensions. But listen to Moody’s Investors Service, the rating agency that’s been most critical of Chicago’s finances, and you’ll get a different picture. Moody’s pegs the total pension debt burden for Chicagoans at $130 billion, nearly double the official numbers. (Yes, by chance the number is eerily similar to the official shortfall of $129 billion facing the five state-run pension funds. But don’t confuse the two.)

That’s scary news for Windy City residents. Barring real reforms, concessions from the unions or bankruptcy, Chicagoans can expect to be hit with whatever series of tax hikes politicians will try to enact to reduce that debt. That $130 billion is the total Moody’s calculates when adding up the direct pension debt owed by the city government, Chicago Public Schools, the park district and Chicago’s share of various Cook County governments and the five state pension funds. Moody’s takes a more realistic approach to investment assumptions than the city and county governments take.

Russia’s had time to prepare.

• Russian Oil Industry Would Weather US ‘Bill From Hell’ (R.)

Stiff new U.S. sanctions against Russia would only have a limited impact on its oil industry because it has drastically reduced its reliance on Western funding and foreign partnerships and is lessening its dependence on imported technology. Western sanctions imposed in 2014 over Russia’s annexation of Crimea have already made it extremely hard for many state oil firms such as Rosneft to borrow abroad or use Western technology to develop shale, offshore and Arctic deposits. While those measures have slowed down a number of challenging oil projects, they have done little to halt the Russian industry’s growth with production near a record high of 11.2 million barrels per day in July – and set to climb further.

Since 2014, the Russian oil industry has effectively halted borrowing from Western institutions, instead relying on its own cash flow and lending from state-owned banks while developing technology to replace services once supplied by Western firms. Analysts say this is partly why Russian oil stocks have been relatively unscathed since U.S. senators introduced legislation to impose new sanctions on Russia over its interference in U.S. elections and its activities in Syria and Ukraine. The measures introduced on Aug. 2, dubbed by the senators as the “bill from hell”, include potential curbs on the operations of state-owned Russian banks, restrictions on holding Russian sovereign debt as well as measures against Western involvement in Russian oil and gas projects.

Too expensive.

• NATO Repeats the Great Mistake of the Warsaw Pact (SCF)

Through the 1990s, during the terms of US President Bill Clinton, NATO relentlessly and inexorably expanded through Central Europe. Today, the expansion of that alliance eastward – encircling Russia with fiercely Russo-phobic regimes in one tiny country after another and in Ukraine, which is not tiny at all – continues. This NATO expansion – which the legendary George Kennan presciently warned against in vain – continues to drive the world the closer towards the threat of thermonuclear war. Far from bringing the United States and the Western NATO allies increased security, it strips them of the certainty of the peace and security they would enjoy if they instead sought a sincere, constructive and above all stable relationship with Russia.

It is argued that the addition of the old Warsaw Pact member states of Central Europe to NATO has dramatically strengthened NATO and gravely weakened Russia. This has been a universally-accepted assumption in the United States and throughout the West for the past quarter century. Yet it simply is not true. In reality, the United States and its Western European allies are now discovering the hard way the same lesson that drained and exhausted the Soviet Union from the creation of the Warsaw Pact in 1955 to its dissolution 36 years later. The tier of Central European nations has always lacked the coherence, the industrial base and the combined economic infrastructure to generate significant industrial, financial or most of all strategic and military power.

[..] When nations such as France, Germany, the Soviet Union or the United States are seen as rising powers in the world, the small countries of Central Europe always hasten to ally themselves accordingly. They therefore adopt and discard Ottoman Islamic imperialism. Austrian Christian imperialism, democracy, Nazism, Communism and again democracy as easily as putting on or off different costumes at a fancy dress ball in Vienna or Budapest. As Russia rises once again in global standing and national power, supported by its genuinely powerful allies China, India and Pakistan in the Shanghai Cooperation Organization, the nations of Central Europe can be anticipated to reorient their own loyalties accordingly once again.

Case in point: the cost of NATO and Russiagate.

• Italy’s NATO Racket… A Bridge Too Far (SCF)

What should be a matter of urgent public demand is why Italy is increasing its national spending on military upgrades and procurements instead of civilian amenities. As with all European members of the NATO alliance, Italy is being pressured by the United States to ramp up its military expenditure. US President Donald Trump has made the NATO budget a priority, haranguing European states to increase their military spending to a level of 2 per cent of GDP. Trump has even since doubled that figure to 4 per cent. Washington’s demand on European allies predates Trump. At a NATO summit in 2015, when Barack Obama was president, all members of the military alliance then acceded to US pressure for greater allocation of budgets to hit the 2 per cent target.

The alleged threat of Russian aggression has been cited over and over as the main reason for boosting NATO. Figures show that Italy, as with other European countries, has sharply increased its annual military spending every year since the 2015 summit. The upward trend reverses a decade-long decline. Currently, Italy spends about $28 billion annually on military. That equates to only about 1.15 per cent of GDP, way below the US-demanded target of 2 per cent of GDP. But the disturbing thing is that Italy’s defense minister Elisabetta Trenta reportedly gave assurances to Trump’s national security advisor John Bolton that her government was committed to hitting its NATO target in the coming years. On current figures that translates roughly into a doubling of Italy’s annual military budget. Meanwhile, the Italian public have had to endure years of economic austerity from cutbacks in social spending and civilian infrastructure.

But the company’s become a secret service.

• Google Staff Tell Bosses China Censorship Is “Moral And Ethical” Crisis (IC)

Google employees are demanding answers from the company’s leadership amid growing internal protests over plans to launch a censored search engine in China. Staff inside the internet giant’s offices have agreed that the censorship project raises “urgent moral and ethical issues” and have circulated a letter saying so, calling on bosses to disclose more about the company’s work in China, which they say is shrouded in too much secrecy, according to three sources with knowledge of the matter. The internal furor began after The Intercept earlier this month revealed details about the censored search engine, which would remove content that China’s authoritarian government views as sensitive, such as information about political dissidents, free speech, democracy, human rights, and peaceful protest.

It would “blacklist sensitive queries” so that “no results will be shown” at all when people enter certain words or phrases, leaked Google documents disclosed. The search platform is to be launched via an Android app, pending approval from Chinese officials. The censorship plan – code-named Dragonfly – was not widely known within Google. Prior to its public exposure, only a few hundred of Google’s 88,000 employees had been briefed about the project – around 0.35 percent of the total workforce. When the news spread through the company’s offices across the world, many employees expressed anger and confusion. Now, a letter has been circulated among staff calling for Google’s leadership to recognize that there is a “code yellow” situation – a kind of internal alert that signifies a crisis is unfolding.

The letter suggests that the Dragonfly initiative violates an internal Google artificial intelligence ethical code, which says that the company will not build or deploy technologies “whose purpose contravenes widely accepted principles of international law and human rights.” The letter says: “Currently we do not have the information required to make ethically-informed decisions about our work, our projects, and our employment. That the decision to build Dragonfly was made in secret, and progressed with the [artificial intelligence] Principles in place, makes clear that the Principles alone are not enough. We urgently need more transparency, a seat at the table, and a commitment to clear and open processes: Google employees need to know what we’re building.”

Don’t be surprised if he’s aquitted.

• Jury in Paul Manafort’s Case Asks Judge to Redefine ‘Reasonable Doubt’ (BBG)

A Virginia jury deliberating the fraud charges against President Donald Trump’s former campaign manager Paul Manafort sent a note with four questions to the judge in the case. Near the end of the first day of deliberations on Thursday, the jury asked whether a report of foreign bank and financial accounts, known as an FBAR, needed to be filed by a person with less than a 50 percent ownership. Manafort is charged with four counts of failing to file FBARs for offshore companies. The jury also asked about the definition of a shelf company.

U.S. District Judge T.S. Ellis III replied that the jurors should rely on their collective memory. The jury also requested that the judge redefine “reasonable doubt.” Ellis replied that the government wasn’t required to prove its case beyond “all doubt,” just to the extent that a person would consider reasonable. Finally, the jury asked if the exhibit list could be amended to include the indictment. The jury was excused for the day and is to return Friday to continue deliberations.