Debt Rattle Sep 30 2014: Why The Fed WILL Raise Rates

Home › Forums › The Automatic Earth Forum › Debt Rattle Sep 30 2014: Why The Fed WILL Raise Rates

- This topic has 17 replies, 11 voices, and was last updated 11 years, 8 months ago by

V. Arnold.

-

AuthorPosts

-

September 30, 2014 at 9:49 pm #15446

Raúl Ilargi Meijer

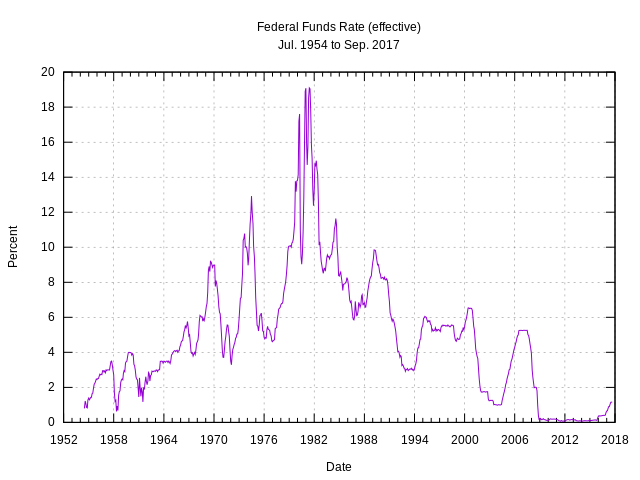

KeymasterHerbert Mayer Honi soit qui mal y pense: Aug 1939 This is not the first time I’ve written on this topic, but I want to do it again, because rate hikes

[See the full post at: Debt Rattle Sep 30 2014: Why The Fed WILL Raise Rates]September 30, 2014 at 10:37 pm #15447John Day

ParticipantEbola Shot JR in Dallas today.

The traveler from West Africa, visiting family, was sick out-of-hospital from 9/26 to 9/28, it seems.

I expect that a lot of emergency measures will be put in place by the end of the year.

(Hopefully less severe than in sierra Leone, but the framework is in place)

This may be worse for the economic status quo than Lehman, eh?

The power structure won’t let this crisis go to waste.

Certainly worse than a cold winter…September 30, 2014 at 11:09 pm #15448Ken Barrows

ParticipantI wonder what TPTB think about the effects of rising rates. I see it burying the American debtor and ending the fracking boom quickly, but who knows?

October 1, 2014 at 12:23 am #15449rapier

ParticipantI have to disagree about rising rates, for the benchmark Treasuries anyway. Except for the overnight bank lending rates, Fed Funds in the US, in the end all other bond rates are set at auction where direct action by central banks is not possible. Only indirect action is. That being things which heighten liquidity in the financial sphere. QE did that in spades, the BOJ is still on the case and the ECB is trying too.

With a lot of money surely flowing into the US, liquidity in the Treasury and bond markets will remain strong. The ROW not so much on a case by case basis.

‘The Fed Funds rate , the rate that they ‘set’ , can rise and fall and not effect overall liquidity. To wit from 2000 till now the rate rose sharply, plunged, rose sharply, plunged again, all the while liquidity was strong except for the crisis period say 8/08 to 3/09.

The amounts of money, liquidity, sloshing around the global financial system are stupendous and defy analysis. I don’t doubt for a moment interest rates are set to rise in various places and various sectors all over the globe. Nor do I doubt the Fed fully expects this and furthermore expects rates to rise most everywhere more than here.

However not just so the banks can make money. The Fed has another master and that is what is now popularly called the permanent government and others call the empire. For the empire the biggest weapon is currencies and we have now launched an economic war. Look no further than Russia. If the EU goes down, so be it. As Victoria Nuland famously said, “fuck the EU’.

Better than money is power. How much money is enough? I think they have enough. The power to keep it is more important and the best way to do that is to bring others down. If they would happen to lose 50% of marked to market value of their assets while others in other nations are losing 70% then you can guess who wins. The JPM’s and GS’s don’t need more money, they need the power to keep it.

October 1, 2014 at 12:55 am #15451Raleigh

ParticipantJohn Day – was just reading about that. Apparently the guy left Liberia on September 19th, arrived in the U.S. on September 20th. Four days later (September 24th) he started to get sick. On the 26th he went to the hospital; they sent him home without checking for Ebola (even though he’s just come from Liberia). On the 28th he’s back in the hospital, via ambulance. Those two days are going to be crucial.

Even though they say he was feeling fine when he boarded the plane from Liberia, perhaps there should be a quarantine put in place (at the Africa end) before anyone can get on a plane. That just makes sense to me.

October 1, 2014 at 2:39 am #15452V. Arnold

ParticipantWhat disturbs me most is this; it was reported there was Zero/0 chance of transmition on the flight. Hmm, me thinks there is already damage control, aka, manipulation of news.

October 1, 2014 at 4:44 am #15453Professorlocknload

ParticipantInverted yield curve going into a deflation?

.001% interest rate is negative in a 0% inflation.

0% interest is negative in any rate of deflation.

Hard to figure here.

Shorten duration to a couple years,,,in short term TIPS?

Unless of course, this is political.

Can’t stand any of ’em, they lie but, let’s say;

Red “juggernaut” wins both houses of Con-gress.

Blue Janet raises rates. Result hits the street 12 months out, in middle of 16 campaign.

Boobus Electorate believed everything was fine before the election.

To the rescue,,,,ta, da! https://www.realclearpolitics.com/2013/11/05/hillary_from_benghazi_to_goldman_sachs_319270.html

Does absolute power corrupt, or what?

October 1, 2014 at 6:30 am #15455TheTrivium4TW

ParticipantHi Ilargi,

There is no dual mandate. The mandate is singular and, if followed there are three listed expectations (not even two!).

Search Section 2A of the Federal Reserve Act and you will read this…Section 2A. Monetary policy objectives

The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.

[12 USC 225a. As added by act of November 16, 1977 (91 Stat. 1387) and amended by acts of October 27, 1978 (92 Stat. 1897); Aug. 23, 1988 (102 Stat. 1375); and Dec. 27, 2000 (114 Stat. 3028).]The mandate, contrary to the Big Lie Psy-Op that people can’t seem to shake… is…

“The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production…”

That’s the mandate…

Now, why is that their mandate?

“…so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

The dual mandate psy-op is to confuse the masses so that they don’t understand the mandate is to avoid exponential debt growth relative to GDP growth.

Guess what the Fed did why dazzling everyone with “dual mandate” BS for 30+ years. They took monetary and and credit aggregates EXPONENTIAL TO the economy’s long run potential to increase production – THEY BROKE THEIR SINGULAR MANDATE AND USED THE DUAL MANDATE HOAX TO COVER UP THEIR PREMEDITATED CRIMINAL BEHAVIOR.

</img>

</img> You aren’t doing anyone any favors by effectively running interference for the Fed’s criminal activity spreading the dual mandate false narrative.

Everyone would be much better served if you highlighted the singular mandate, the Fed’s lies about a phony dual mandate, and expose the purposeful and criminal exponential debt growth relative to GDP growth.

October 1, 2014 at 6:41 am #15457ParticipantHi Jal,

Re: yesterday… sorry for posting to the wrong person and mistyping “too” as “two.” I’ll try to pay better attention to detail.

Money pervades nearly everything humans do – both locally and across the globe. A fraudulent debt money system and the bombs being dropped on one’s country if one’s country doesn’t have a debt money system are going to impact people locally, regionally and globally. There is no escape hatch or truly safe zone.

The evil of debt money pervades the entire planet… locally, regionally, and nationally.

You can look anywhere you want and you will see the effects all around you as long as you comprehend the system. However, it does so without an obvious direct cause to the observed effects. Once one becomes aware of the mechanism, though, improved clarity follows.

Did you know that the guy down the street with lots of net cash savings is a debt slave master who enslaved someone else to inextinguishable debt that was used to create the net money s/he has saved up? Wow. And they told us we abolished slavery, didn’t they?

They lied.

Inequality: Why are the rich getting richer?

How To Be A Crook

October 1, 2014 at 8:42 am #15458Nassim

ParticipantI think this Ebola thing might shut down air travel before too long. It seems that there are some strains that can be transmitted from person to person without touching.

Here is a very scary article which explains that the death rate is far higher than the published figures. Essentially, because of its rapid spread (doubling every 4 weeks or so), counting the dead and dividing it by the infected gives a figure much lower than it should. The real death rate is more like 80%. Of course, no one has any idea of the effect on life expectancy of the “lucky” survivors.

Estimating the fatality of the 2014 West African Ebola Outbreak

And here is a more realistic model of its propogation

October 1, 2014 at 11:21 am #15459ParticipantWell, this thread by Raul was well above my pay grade, so-to-speak.

Being an expat, the strengthening dollar has meant a raise in my monthly income due to increasingly favorable exchange rates (for me).

Unfortunately the rest (above) is somewhat lost on me. Maybe it’s just as well. I do not see how it affects everyday life for the average American. I couldn’t care less how the wealthy fare…October 1, 2014 at 2:34 pm #15460Jef Jelten

ParticipantAbout the slave thingy.

As soon as finance enters the equation everything becomes more expensive and it becomes more expensive exponentially irregardless of actual costs.

As an example lets take an average house. With all cost covered including labor and pay for everyone involved the house should list for $75,000. People would save up for many years and buy it outright or make a deal with the builder to pay a large chunk and the rest over time.

Enter finance. Now because price doesn’t matter as anyone with a pulse can borrow, the price is $150,000. Add onto that interest, fees, and mandatory insurance, and by the time the house is paid off it has cost between $300,000. and $400,000……..for a $75,000 house.

Extrapolate this out to ….well just about everything humanity is involved in, consumption, government, education…everything. The average person, over a lifetime, gives at least half and more likely two thirds of what they make to finance. Some will say that there is no other way to buy big ticket items but that is propaganda BS!

Now even though the Merry-go-Round has virtually stopped finance still demands that that two thirds still gets paid volentarily or otherwise.

What makes this even more insidious is that those who manipulated us into this situation have linked nearly every aspect of our economy to this scam so that to end it means the collapse of life as we know it. And I don’t mean back to gardening and made by hand localization BS. I mean dirty, nasty, ugly, collapse.

October 1, 2014 at 4:42 pm #15461ParticipantRight on the mark, Jef.

It’s just that collapse can take several generations. 60 or 70 years is a long wait.

October 1, 2014 at 4:54 pm #15462Diogenes Shrugged

ParticipantV. Arnold,

> > “I do not see how it affects everyday life for the average American. I couldn’t care less how the wealthy fare…”

Please , I implore you, watch the two videos posted above by TheTrivium4TW. It’s pretty clear you must have missed them.TheTrivium4TW,

Your arguments against the worldwide bankster’s paradise are superb. I tend to focus too much on the pernicious nature of “government” (per se), or to contemplate my navel with salvos against “climate change” rather than address the real problem. Your posting of those two videos, in my opinion, constitutes a great public service. If only we could somehow get the bulk of this species to attentively watch them – – preferably more than once.

That said, money supplies issued out of thin air in the form of loans-at-interest isn’t the only fraud banks perpetrate on mankind. They also perpetrate a more readily recognizable fraud with an even more horrific toll: wars. The video I’m posting below is a longer video than most have time for, but if you’ve never seen it, I hope you can make room in your schedule sometime.

October 1, 2014 at 7:30 pm #15464ParticipantIlargi: This will show my shameful ignorance of finance, but I’m curious whether a very recent statement by Karl Denninger has the potential to contradict arguments you’ve put forth recently. Can the Fed rate diverge from treasury rates over long periods of time, or do they rise and fall in tandem?

Karl Denninger @17:00 – – “But I’m actually on the contrarian side when it comes to government bond rates. Everyone says they’re going up a lot. You have to realize there’s another side to this, which is if the economy sucks severely enough, they will go down instead. We could see a 2% 10-year treasury rate for the next 10-15 years, and of course the problem with that is you don’t get a 2% treasury rate for the next 10-15 years with a robust economy and good hiring. What you get it with is a 1930’s-style depression.”

October 1, 2014 at 8:42 pm #15465ParticipantDiogenes – “All Wars Are Bankers’ Wars” is a great video. I’ve posted it numerous times around the Internet. If you can’t watch it all in one go, watch a quarter or half now, then the rest later. It really explains a lot about how our world works.

Trivium – in the video “Inequality: Why Are the Rich Getting Richer,” at 1:10 minutes it says: “The shocking fact is, if nobody went into debt, there would be almost no money in the economy.” Why is that so bad? That would just mean house prices (essentially all assets) would come way, way, way down in price, a dollar would actually be worth something again. “But, but, but,” you might argue, “I paid a whole lot more for my car or house and now they’ve come way down in price, but I’ve still got to pay on them.” Well, as it turns out, you were only “renting” your house from the banks, anyway. Renting!

It’s all relative. When there are fewer dollars in existence, they are worth more (they buy more), and prices have to come down to reflect this. As we’ve seen, when people paid way too much for their houses (and their houses dropped in price), they simply walked away and bought another house that was much cheaper (and, to boot, they got the cheapest mortgage rates in history), or they rented. Of course, I didn’t see people complaining too much when the worth of their houses was doubling, but that’s another story. And you get a tax credit for the interest you pay on your mortgages.

Banking needs to go back to what it used to be: bank managers in crumpled suits, earning a decent living, and lending only to the most qualified borrowers who have a really good down payment that they’ve saved up. No securitization; in other words, getting rid of the ability of banks to unload inferior mortgages onto some sucker investor (passing the hot potato) who thinks he’s getting premium AAA beef. Make them keep the loans they hand out on THEIR books. That way they won’t be lending to people who can barely fog a mirror.

As far as I can see, Positive Money (and I may be wrong) appears to want the game to continue, but wants “more” money spent into the economy. Are we not already floating in the stuff? I mean, the government is guaranteeing inferior loans, supplying Section 8 housing, welfare, food stamps, free cell phones; banks are choosing not to foreclose on millions of mortgages because they don’t want to book the loss. All that creates free “positive money” floating around and being spent at Walmart and the 7-11. There’s no shortage of money floating around. QE has kept asset prices from crumbling (more positive money). We are awash in the stuff.

People want something for nothing (mainly the financial industry). They want their house debt inflated away, and they don’t mind if savers’ money is worth less because of it. Savers would have less money if not for all of the previous inflation, you say? Yes, they would have less, but what they’d have would be worth more, would buy more (because prices would be down). It’s all relative.

Adding more and more money to the situation just creates more and more inflation, which pushes prices up, which just maintains the status quo. Put a wall between investment banking and commercial banking (as was done before). If the investment bankers (and their investors) want to blow their brains out, go at it.

October 2, 2014 at 12:55 am #15483ParticipantRaleigh:

> > “As we’ve seen, when people paid way too much for their houses (and their houses dropped in price), they simply walked away and bought another house that was much cheaper (and, to boot, they got the cheapest mortgage rates in history), or they rented.”

This is news to me, but it is something I’ve wondered about. If people have walked away from the mortgages they’ve purchased (you don’t purchase a house, you purchase a mortgage), but have been granted new mortgages soon afterward, that would indicate that the banks have ignored credit risk altogether. This is a delicate question to ask, but do you know of any evidence that that has actually happened, or were you, for the sake of making a point, using hyperbole? Since the banks have been backstopped by the taxpayer, it wouldn’t surprise me if it were true.

Also:

> > “Trivium – in the video, ‘Inequality: Why Are the Rich Getting Richer,’ at 1:10 minutes it says: ‘The shocking fact is, if nobody went into debt, there would be almost no money in the economy.’ Why is that so bad? That would just mean house prices (essentially all assets) would come way, way, way down in price, a dollar would actually be worth something again.”One problem with gold and silver coinage (not the chief problem, by the way) is that there isn’t enough of it. How do I rush out and buy a can of beans with a silver coin worth $1,000 (ignoring that it might be the entirety of my wealth)? One might suggest copper coins with a smidgen of silver, but as a former fire assayer with over a-hundred-thousand meticulous fire assays to my credit, I have to ask how you’d know the silver was actually present in the correct concentration in the alloy? Anyway, my point is that Trivium appeared to be talking about a resulting hard money supply so small that it would present the same problems as gold and silver (i.e. no liquidity, and NOT an efficient means of exchange).

Wouldn’t it be more efficient to just revert to clamshells and beads? (Just being funny there. If I was serious, I’d have said Bitcoin.)

Your comments here are much appreciated.

October 2, 2014 at 1:10 am #15484Participant@ Jef & Diogenes + TheTrivium4TW

Thanks all, great responses.

Jef: This particularly hit me between the eyes;

“What makes this even more insidious is that those who manipulated us into this situation have linked nearly every aspect of our economy to this scam so that to end it means the collapse of life as we know it. And I don’t mean back to gardening and made by hand localization BS. I mean dirty, nasty, ugly, collapse.”World Made by Hand; romantic bullshit, IMO.

As an old guy, I hope I have a few more years before shit-hits-fan.

Cheers(?) 😉 -

AuthorPosts

{kind=link}

- You must be logged in to reply to this topic.

Sorry, the comment form is closed at this time.