How Central Banks Buy Growth

Home › Forums › The Automatic Earth Forum › How Central Banks Buy Growth

- This topic is empty.

-

AuthorPosts

-

July 26, 2013 at 2:43 pm #8368

Raúl Ilargi Meijer

KeymasterDorothea Lange Good Coffee May 1937 "Post office Finlay, Texas" The best of the lot must be the Daily Telegraph's headline: Economy firi

[See the full post at: How Central Banks Buy Growth]July 26, 2013 at 9:18 pm #8038jal

ParticipantThose who have been advocating a “jubilee” … “debt-deflation spiral” can rest assured that it will not happen for 90% of the people.

This would mean that the lenders would have to take a loss.

They are doing everything to avoid a “jubilee”.“Jubilee” means contraction, and a deflation of the wealth of the 10%.

Central bankers cannot continue to “buy growth” in this fashion forever. And when they stop, there will be contraction, and deflation. There is no real source of growth. It’s one big costly fake. Just look at the graphs.

IMF and others are fighting “jubilee” … “debt-deflation spiral”

The Fund said the European Central Bank must take countervailing action to prevent “a vicious circle setting in,” ideally by cutting interests, introducing a negative deposit rate, and purchasing a targeted range of private assets.

“Five years before John Maynard Keynes published his General Theory, Takahashi succeeded in extricating Japan from deep deflation ahead of the rest of the world. His example has emboldened me.” Takahashi’s triumph was to smash expectations. “It is impossible to get rid of ingrained deflationary psychology unless you clear it out all at once. I myself have attempted to do exactly that,” said Mr Abe.

There will be no “jubilee” … buying opportunities for 90% of us.

Time to go back to my gardening.

July 27, 2013 at 5:11 am #8042p01

ParticipantThe comment below is made by the top dog karma commenter, Wit Moar Karma than the adminz!!!!111.

How far the mighty have fallen.

July 27, 2013 at 9:45 am #8043ParticipantLook!!!

The 90% is not getting any breaks. No restitution.

The 10% are laughing all the way to the bank with freshly printed money and a “get out of jail card.”UBS AG (UBSN), Switzerland’s largest bank, agreed to pay $885 million to Fannie Mae and Freddie Mac to settle claims that it improperly sold them mortgage-backed securities during the housing bubble, a U.S. regulator said.

UBS disclosed earlier this week that it had reached an agreement in principle to settle the suit. The FHFA sued UBS in 2011 over $4.5 billion in residential mortgage-backed securities that UBS sponsored and $1.8 billion of third-party RMBS sold to Fannie Mae and Freddie Mac. The suits alleged losses of at least $1.2 billion plus interest. Fifteen other banks still need to resolve such lawsuits.

What’s your interpretation of this message?

July 27, 2013 at 6:27 pm #8046Golden Oxen

ParticipantThe hopelessness of the situation is certainly made clear by this article.

My only questions are, since a stopping of the current situation would no doubt cause an instant calamity; what’s next?

Legislation forcing banks to lend, they are after all scoundrels?

Negative interest rates?

Taxes on excess savings?

Cheap government loans for the middle and lower classes available at our now defunct post offices?

Perhaps a law that a percentage of all retirement accounts must be withdrawn and spent every year by everyone on social security or forfeited?

They all sound preposterous, I know, but what could be more insane than our current situation?

July 27, 2013 at 7:46 pm #8047Ken Barrows

ParticipantI have thought that a too high price of oil might end QE. But maybe that’s not it.

So, if QE keeps going and going (until the collateral runs out) and the price of oil specifically and rising prices generally don’t stop it, what will stop it? Would love to see a piece about that.

July 28, 2013 at 11:29 am #8050davefairtex

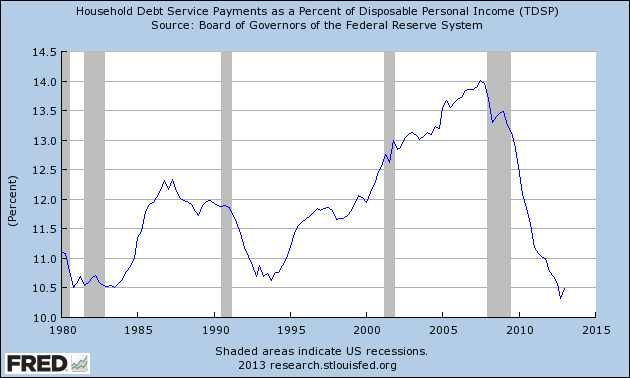

ParticipantQE causes bubbles in the bond market, and the money doesn’t make it out to the economy, but the lowered rates do help reduce the effective payment burden for those in debt – at least it did until rates went up two months ago.

Here’s a chart of that: this is the TDSP timeseries from FRED, which shows the percentage of disposable personal income devoted to mortgage payments. It has dropped to levels last seen back in the mid 90s. Timeseries is only updated quarterly though, so its a bit out of date.

The debt remains (no Jubilee, certainly) but the payment burden is far lower. Basically, you’re still a debt-slave, just the chains you are wearing aren’t quite as heavy.

July 28, 2013 at 8:16 pm #8052Participant

July 28, 2013 at 8:16 pm #8052ParticipantThere is no real source of growth. It’s one big costly fake. Just look at the graphs.

We have told you for years to get out before that steamroller comes. Many of you today are thinking and saying: but it looks so good! Now you know, if you didn’t already, and from yet another angle, what makes it look good.Count your blessings.

The economy is far stronger now than it was four and a half years ago.

The collapse of the financial system has been repaired.

(As long as one ignores the reality)

There is deepening alarm in the West over the course taken by Egypt, a country of 84 million people.

Meanwhile, the head of Egypt’s Central Statistics Bureau General Abu Bahar Jundi spoke with Egypt’s Al Ahram website and said that around 35 million people took to the streets Friday. Egyptian army officials put the number at around 30 million.

Can you imagine …

… your town, your city, your state/district/province, your country, …

Having 50% of the population out in the street demanding the rulers/gov. to make CHANGE

In the USA, There are 50 million people on food stamps and living in poverty.

In other countries the number of people living in poverty are higher and rising.

Why are the poor of the world not demonstrating and demanding change?

We have shitty economic and social systems and they are going to get worst.July 29, 2013 at 8:45 am #8056steve from virginia

ParticipantGood grief!

Anything by ‘Tyler Durden’ is simple garbage, why his/its nonsense is repeated over and over is hard to understand. I guess a lie repeated enough becomes the truth.

Central banks cannot create ‘new money’, they do not ‘print money’ they cannot do so. Central banks can only offer secured loans. Any loan (bond buying) by the central bank must be collateralized. The collateral offered are IOUs for loans already made. When the central banks lend they are simply changing custody of pledges.

Instead of repaying the issuing lender, the borrower pays the central bank instead.

Money is entirely created by the private sector, which can and do offer unsecured loans; against repledged collateral or against no collateral at all. (See Schumpeter, Keen)

+95% of private sector dollar debt is unsecured. US currency is secured 100%; the difference between currency in circulation and total booked debts is unsecured loans: in the US it is + $50 trillion.

Central banks cannot offer unsecured loans or they immediately fail. This is not a rule but a condition, like gravity. If the commercial banks are insolvent it is because they are overleveraged, that is, they have made unsecured loans that cannot be retired. When the central bank does the same thing as the commercial banks — or takes on the commercial banks’ loans as collateral — there is no discernible difference between the central bank and commercial banks. The entire system from top to bottom is perceived to be insolvent: there is no guarantor of bank liabilities, no real lender of last resort, only a bankrupt banking system and runs out of it … as are seen in Europe, Japan and China.

Capital flight is a run, BTW.

QE is an asset swap, BTW, there is no way the asset side of a bank’s balance sheet can migrate to the liability side where the bank’s depositors reside.

Durden should stick his head in a toilet and flush a few times.

July 30, 2013 at 8:07 am #8057Viscount St. Albans

ParticipantA basic and probably stupid question, but here goes:

If, as Steve Keen and others have noted, the vast majority of money in circulation is derived from unsecured private bank lending, then what constrains the magnitude of private bank lending? Is there any relationship or linkage between deposits and the magnitude of lending?

If bank lending is entirely de-linked from deposits, then what prevents the local Mom-and-Pop bank with a single Main Street Branch and $1 million in total deposits from lending $50 billion to a start-up solar energy farm in Wales? Who or what sets the limits on private lending?

August 12, 2013 at 10:10 pm #8137Participanthttps://www.zerohedge.com/news/2013-08-12/plain-fools-and-wall-street-fools

So what is the Fed doing? As of July 31, 2013 they have parked $1,157 billion in foreign banks as compared with $1,112 billion in U.S. banks. To us this is a telling sign. The European banks are in trouble and the Fed is propping them up.

What are the EU banks putting up for collateral?

Could I get that kind of money on “a promise to pay back”? -

AuthorPosts

- You must be logged in to reply to this topic.

Sorry, the comment form is closed at this time.