The Cyprus Solution – Coming To a Town Near You

Home › Forums › The Automatic Earth Forum › TAE Blog › Finance › The Cyprus Solution – Coming To a Town Near You

- This topic has 22 replies, 1 voice, and was last updated 13 years, 2 months ago by

skipbreakfast.

-

AuthorPosts

-

March 22, 2013 at 5:27 am #7196

skipbreakfast

ParticipantI’ve been thinking a lot about Cyprus. Haven’t we all? And I’ve tossed around the various theories about why the Troika has taken this precarious path, risking contagion but perhaps having no other choice. Only time will tell us what is really behind their machinations. But it led me to another, rather unpalatable conclusion. The reasons don’t matter. Stoneleigh and Ilargi have predicted the Cyprus Solution all along, so I’m hardly surprised that it has appeared. The brazen-ness of the solution seems confounding if only because the Troika masters have been so coy about most of their manoeuvers. However, this is simply an example of Stoneleigh’s “multiple claims to real underlying wealth”. There are more claims to Euros than there are Euros to go around. Eventually it MUST come to this.

Which then leads me to the question of how to receive such turns of events, because readers of TAE have known all along this is what is coming to Cyprus and Greece and EVERYWHERE else in the world, in varying shapes and forms. And I have concluded that demanding that “innocent savers” be spared in favour of “dastardly bondholders” is a wasted exercise. It may be fatalistic, but it is also be realistic.

In fact, I dispute the notion that poor savers are “innocent” at all. In a world where we have all lived far beyond our means, where multiple claims to the dollars we believe that we hold vastly outstrip any possible “fair” solution, where we’re all bankrupt, then who should be made to pay out first? Who is first to give up their cash in a world that is uniformly broke. Let’s not forget all the “innocent savers” have been players in this game of “Me First” wherein capitalism promises that it is just and fair to “win” more than your neighbour if you just play the game better. How many savers have not been willing participants in the spectacle of capitalism, even while so many have lost so woefully throughout the match.

I point you to the depressing studies that reveal how under-privileged African Americans can be the most staunch defenders of capitalism in its extreme, because the promise of rising above one’s sorry state of poverty to attain riches is just so appealing, even if the game is clearly rigged so that you have the most dismal chance of winning.

Every one of us has a distorted sense of entitlement. We believe that it is a right that food should magically appear on our supermarket shelves, no matter what we have done as individuals to contribute to food production. We believe we have a right to a car and a telephone and a job. But when there is not enough to go around for everyone, who has the first right which trumps yours or mine or his? Should naiveté bestow some right to charity over the savvy player who knows how to game the system? I think that distinction is partly behind the notion that savers are more deserving of protection, because they have some innocence about capitalism’s evil machinations, while the bondholders know exactly what evil they work. I’m not sure I buy that distinction. I especially don’t buy it when we’re all equally culpable in our wilful blindness about the effects of global capitalism.

It all becomes an exercise from a first-year university philosophy course in Ethics. I took that course. There was seldom a truly clear answer–the answers wavered depending on one’s self-interests and point of view. We’re down to the fatalistic question of three people at sea in a lifeboat, and there’s only enough food for two. How do you go about choosing who eats?

And so, I ask how innocent are the savers? Because if we’re all living beyond our means, blindly consuming without properly understanding and questioning the state of things, it seems we all have to pay something back and downsize our standard of living. We can fight for fairness, but the inevitable write-down of each one of our bank accounts MUST occur, as we are indeed broke. Asking bondholders to take the haircut first simply postpones this reality, and probably not by very long.

Indeed, in a world where there is simply not enough real money (in terms of real wealth) to go around, can anyone be blamed for trying to ensure they don’t take a hit before the next guy. If I’m a bondholder, do I really have less right to fight to keep what I thought I “earned and deserved” more than the saver? I’d argue very few of us have earned and deserved what we’ve got. And I have no idea how we’d really tease apart those most deserving from those who aren’t.

And so it becomes a scramble to preserve as much as you can for yourself, and do it now. Before someone else comes and takes it. Because they will, whether you are an “innocent” bondholder or an “innocent” saver. The entire system is broke. The chance of some holy messiah rising above the deflationary collapse to fairly dole out what remains is a pipe dream.

So we can rise up and protest the rich exploiting the poor. And we may make some headway in our own neighbourhood. But this changes nothing in terms of the fact we will all give up something. And the measure of how much you give up, or I give up, in terms of what we thought was our right to our “wealth”, is not going to be fairly determined because this is an impossible thing to measure.

I return again to something I’ve mentioned in TAE comments before. What I want to happen is not relevant to what will happen. I’d like us all to have the future I was promised–one where we can all aspire to shinier cars and bigger houses and more spectacular careers where we don’t get our hands dirty. I really wish that fantasy were true. It’s not. And the fantasy that we can fairly determine who loses the most or least in a game that is bankrupt worldwide, is equally just a dream.

The reality is they’re coming for you, we just don’t know who THEY are yet. They might be you coming for me, and you might think you’re a very good person. You probably are. So it is only my responsibility to understand that this is now a question of preserving what we can before they come and take it. That is your only responsibility to yourself and your family and your community. Tough choices are at hand. It’s up to you to protect your wealth so that you have a chance to survive and do some good. Demanding that bondholders take the hit before savers won’t change the fact that your wealth is going to be attacked sooner than later. TAE has excellent ideas around preparing for this inevitability. You owe it to yourself and your loved ones to do it before you are a victim of the Cyprus Solution.

March 22, 2013 at 7:16 am #7197Nassim

ParticipantI ask how innocent are the savers?

It’s funny how the savers always get it in the butt. First, we have ZIRP (Zero Rate Interest Policy] combined with false price inflation statistics – i.e. negative real interest rates over a period of many years. Now, their deposits are being raided.

I do so wish that the big borrowers were subject to the following:

1- A real rate of interest

2- No tax concessions for borrowingThe sad truth is that many savers are old and cannot work. It is money that they put aside after paying their taxes. Borrowers tend to be a lot younger and smarter. It used to be advised to “save for your retirement”

The ageing widowed mother of a Greek-Cypriot friend of mine has already had her pension reduced, and now this.

Frankly, your attitude and ethics quite disgust me. They are a reflection of the times, I guess

March 22, 2013 at 7:45 am #7198Golden Oxen

ParticipantNassim, Thank you for all your superb postings. GO

March 22, 2013 at 8:50 am #7199davefairtex

ParticipantIn the US, in a bank bankruptcy, depositors have seniority over all other liabilities as the result of a law passed in 1993 called “depositor preference.” This law was put in place to help reduce losses to FDIC during a bank resolution process. It also reduces losses to depositors above the insured limit.

This is relatively unique to the US – not many other nations have such a law in place.

When a bank goes down in the US, the FDIC rolls in, sells all the assets, writes checks to insured depositors, and with whatever cash remains, pays off creditors in order of precedence. With depositor preference, that means all those remaining UNINSURED depositors are paid fully, before any other creditor – including junior and senior bondholders – sees a dime. The amount paid to the rest of the creditors depends on how bad those assets are.

What *should* happen in Cyprus depends on how they legally treat depositors in a bankruptcy. If a depositor is an unsecured creditor, wow, tough luck for them, they stand in line along with the junior bondholders. If they have depositor preference laws in place, then the bondholders should be completely wiped out before those depositors – even the uninsured depositors – lose a nickel.

Of course once the government steps in and circumvents the usual processes, then they get to pick winners and losers, just like we did when TARP parachuted billions in equity buys across the US banking system in 2008-2009.

If depositors are unsecured creditors, and they do end up getting thrown under the bus in this process, then I suspect a price will be paid eurozone-wide as small depositors remove their money at the first sign of trouble in their nation’s banking system. If you can avoid a 6% “wealth tax” on your insured deposits by simply withdrawing your money, heck, why not?

Is this the effect they were looking for?

Deposit guarantee programs were put in place to instill confidence and stop bank runs. With that confidence “impaired” by this new wealth tax – a service fee for the privilege of having your money in that fine banking institution – all I can think of is “unintended consequences.”

I’ll take cash, thanks. No wealth tax yet on cash.

As for the moral argument – I’m quite comfortable picking small depositors (especially the ones given a guarantee of protection by the government) over bondholders who were “the smartest guys in the room” who signed up for risk when they made their investment.

This ethical discussion reminds me of the argument that the majority of the blame for the housing bubble should be placed on home buyers. Bankers have been in the business of making loans for 400 years. Its not rocket science – there are well-established principles of doing business. Basically: don’t make a loan that can’t or won’t be paid back. So in that transaction, who was the smartest guy in the room? The guy who takes out a home loan 5 times in his life, or the company that has processed thousands if not millions of loans before?

Sure, without a greedy mark there is no con. But I’m quite comfortable placing the vast majority of the responsibility on the con men. Especially when “the con” is their entire business model.

But that’s just me.

March 22, 2013 at 10:13 am #7200ParticipantTo give you a further idea of how f***ed up the Cyprus economy has become since joining the EU, the elderly lady I mentioned above cannot find tomatoes for less than 3 Euros per kilo. I hardly need mention that Cyprus offers an ideal climate for growing tomatoes and there are plenty of people with time on their hands.

IMHO, they would be better off leaving the EZ. Obviously, it would accelerate the departure of the Spanish, Portuguese, Italians, Irish, French and so on. The Germans would find it really hard selling their BMW’s to Southern Europe and real competition would ensue.

March 22, 2013 at 4:19 pm #7202ParticipantNassim –

Not knowing what tomato prices were prior to the eurozone admission, I can’t comment other than – perhaps your elderly lady could grow a few tomato plants? They’re so easy, and nothing beats a home-grown tomato. I think food engineers have GMOed all the taste out of tomatos these days.

But I digress. 🙂 And I really don’t mean to trivialize the struggles of someone on a fixed income. I just happen to like home grown tomatos.

My mom is retired, and CALSTRS (the manager of her pension) is looking more and more tenuous since the crash. They’re expecting a 7.5% ROI each and every year and even with that expectation, they’re going to go broke in about 30 years. If they were to assume no growth, I wonder how long they’d last.

March 22, 2013 at 10:10 pm #7203jal

ParticipantIts a troika experiment.

Now we get to see what happens when the central banks do the right thing and don’t start up the printing press.The objective is to get a default and gather the data from the resulting chaos.

All doomers should pay attention.The main benefit will be Greece who will not need to pay back the money lent to them by the Cyprus banks who have gone bankrupt.

Lets wait and see how financially dumb everyone is.

March 22, 2013 at 11:46 pm #7204gurusid

ParticipantHi Skip,

Good post that highlights the real issues. Also,

The reality is they’re coming for you, we just don’t know who THEY are yet.

In the case of Ireland, this guy has had a shot at finding out who some of the banks ‘bond holders’ are:

I suspect similar people to be involved in Cyprus, possibly residing in Russia:

Roman Abramovich, owner of the Chelsea soccer team in England. His fortune is estimated at $14.6 billion. He runs the investment company Evraz through the Cyprus brand Lanebrook

Michael Prochorof, former presidential candidate. His property worth is $13 billion. In 2008 he stated Cyprus as the head office of the company Intergeo Management

Vladimir Lisin is a steel tycoon with a fortune of $15.9 billion, and who has the largest amount of his business in Novolipetsk through the Cypriot company Fletcher Holding

Alexei also Morntasof, also a steel baron, $15.3 billion

Vladimir Potanin, $14.5 billion

Vagkit Alekperof, an oil company owner, $13.5 billion

Suleiman Kerimof, a mining tycoon with a fortune estimated at $6.5 billion

Aliser Ousmanof, an internet businessman and Prime Minister Dimitri Medvedev’s friend with an $18.1 billion

Batourina Elena, wife of the former Moscow Mayor Yury Louskof, whose property worth is $1 billion

Dmitry Rimpolovlef, the biggest shareholder of Cyprus Bank, also the owner of the Monaco football team. His property is more than $9 billionLast year, more than 3,000 Learjets landed and took off from Cyprus, 375 of which were going in Russia and 245 to Great Britain, while 108 went to Ukraine.

Golem also has a similar take on Cyprus’ ‘Nuclear’ option as regards the current crisis:

Cyprus – The ‘nuclear’ option By Golem XIV on March 22, 2013

Either Cypriot members of parliament ignore the will of the Cypriot people or the ECB stops supporting Cypriot banks and they implode. Which would mean either Cyprus leaves the Euro and re-introduces its own currency (which it could do) or it tells its people that ALL their money is now gone.

The problem is the private Cypriot banks spent a great deal of the money deposited in them on buying high yielding Greek bonds/debt which were partially defaulted by Greece with the say-so of the ECB et al. So bear in mind that whatever else Cyprus is guilty of (and there is plenty of guilt to go around) it is NOT a case of a government spending profligately. Cyprus debt to GDP at 87% was lower that the Europe area average of 93%.

…

So does Cyprus have an option? I think they do. A nuclear one.It is true they have no fiscal bullets left. They never really had any. All they ever really had was a little plastic tomahawk they got from Woolies. Even that’s bent now. Even if they decide to let the ECB pull the life support on their banks the EU has said it feels confident no contagion will spread to the rest of Europe. What they mean is financial contagion. The contagion of one defaulted debt, causing another to default causing another. That danger, the EU thinks it has contained. And it may well have.

But Cyprus has one other option – not fiscal but legal.

The nuclear option of Cyprus is to not seize the money in peoples’ accounts but the information about that money. Such as where it came from, if it was criminal or laundered, and if so which banks, businesses and professionals knew about it and helped it on its way. The information which their regulators should have been collecting but never bothered to for the last 15 years. But even so, it is still there. Could still be used.

Cyprus has been laundering money. Its banks and businesses have helped. But so too have the banks and businesses of other countries. To my knowledge there is documentary evidence which implicates at least two huge European banks. A third, a German bank, would, I think, find itself dragged in also. As would dozens if not hundreds of British registered shell companies and the British authorities who do nothing to regulate them, and yet are implicated in four major fraud cases I know of personally.

…The plot thickens.

As regards the problem of:

How do you go about choosing who eats?

More specifically as regards going hungry:

How can you be so cold-blooded as to oppose sending food to the starving peoples of Africa?

…and the response:

To understand my answer, you have to understand the origins of starvation in Africa. For millennia (indeed for hundreds of millennia) starvation was UNKNOWN in Africa. There were no starving people there for the same reason that there were no starving lions, no starving zebras, no starving giraffes. Why? Because all these creatures (including humans) were living in balance with the resources of their environment.Here’s how this balance comes about. As the population of every animate species grows, its food supply begins to diminish (as it must, since it’s being consumed). As its food supply diminishes, the species’ population diminishes as well (as it must, since less food is available to it). As the species’ population diminishes, its food supply begins to recover. As its food supply recovers, its population again begins to grow. As its population grows, its food supply again begins to diminish. As its food supply diminishes, its population diminishes – and so on and on and on, for every animate species on this planet. Populations and food supply constantly balance each other in this way, and this explains why lions have neither overrun Africa nor disappeared from Africa, why kangaroos have neither overrun Australia nor disappeared from Australia. Each of these species lives in balance with the resources available to them in their environment. And so did the peoples of Africa for hundreds of millennia.

And what happened to change this? We did. We moved into Africa in a big way in the nineteenth century and in an even bigger way in the twentieth. We were driven to this by one of the prime directives of our cultural mythology: “There is one right way for people to live — our way — and everyone in the world must be made to live our way.” We told the people of Africa, “The way you’re living is not the way humans were meant to live, like lions and giraffes. We’ll show you how humans should live.”

The youngsters of the Peace Corps felt great about what they were doing, showing people how to take control of their resources, how to increase food production, how to defeat that feedback relationship that had kept African populations in balance with their resources for millennia. They no longer had to put up with a population cycle of growth and decline. Through improved agricultural techniques, decline was eliminated from the cycle. With the wisdom of these polite young visitors from another world, they were now free to just grow and grow and grow and grow, until for some strange, unimaginable reason . . . they were starving.

For centuries there had been a constant, never broken working relationship between them and their resources. Now that relationship was gone. Their populations had grown to a point where their resources could not support them.

And what did the great-hearted people of our culture say about this? Did they say, “We have foolishly helped these people destroy a way of living that worked well for them for millennia. We must let them return to living in balance with their resources, so that they will no longer be starving”? No, we said: “We must not let that happen. If we let that happen, it would cast doubt on the fact that ours is the one right way for people to live. If their own resources aren’t enough to keep them alive, we’ll graciously send them some of ours.”

The food we send doesn’t stop them from starving. It just keeps them alive — starving — dependant on us for their lives — year after year after year. And we congratulate ourselves for doing this. Having brought starvation to the people of Africa, we bless ourselves for keeping them alive, starving. And anyone who doesn’t endorse keeping them alive and starving forever, is denounced as cold and heartless.

Most people will not be able to comprehend what lies ahead for the bulk of humanity. While the kings and queens play with the pawns on the human chess board, non realise that the board itself is built upon fundamental natural laws that while seeming to have been stretched, cannot be broken. Over the next few decades we are all going to run into these laws, bailout or no bailout we all rich and poor will find out that you cannot eat or drink money.

L,

Sid.March 23, 2013 at 12:16 am #7206ParticipantHI Dave,

perhaps your elderly lady could grow a few tomato plants? They’re so easy, and nothing beats a home-grown tomato. I think food engineers have GMOed all the taste out of tomatos these days.

But I digress. And I really don’t mean to trivialize the struggles of someone on a fixed income. I just happen to like home grown tomatoes.

You haven’t digressed at all, you’ve hit the nail on the head. Learn about tomato growing, learn about heirloom varieties, then grow them save the seed, and learn how to preserve the tomatoes via a myriad different techniques from drying to making chutney.

But maybe I digress…

L,

Sid.March 23, 2013 at 1:05 am #7208Participant[quote=Nassim post=6909]

The ageing widowed mother of a Greek-Cypriot friend of mine has already had her pension reduced, and now this.

Frankly, your attitude and ethics quite disgust me. They are a reflection of the times, I guess

I’m glad my ethics disgust you, because they’re not really my ethics so much as all of our reality. And reality is vomit-inducing these days.

Personally, if I could just find my magic wand, I would much rather enact an equitable distribution of wealth around the world. We don’t have that and I would probably have to admit we have never had that. Hardly. World poverty statistics put such lofty ideals to shame (and the aging widow lives much better than most, probably, just not in her hometown).

Yes, I’m throwing in the towel on fighting for such equity at this stage. Because I don’t believe it is going to have any impact. Not immediately at least. Not until we have survived the worst of the write-downs. As such, I would prefer that every aging widow protects herself by employing some of the wise strategies suggested by Ilargi and Stoneleigh. A broke system means even the widow has been living above her means in some respects (e.g., living in cities and countries that provide for their people by enjoying the largest credit bubble in world history–our standards of living have not been bought and paid for).

The write-down of your standard of living will take many forms. Even if you protect ALL of your wealth through various strategies and some very good luck, your standard of living will still drop as the services we take for granted disappear (paved roads, garbage pick-up, policing, etc.).

Ultimately, once the worst of this blows over (which is probably going to take decades), a society might arise with more humanity that insists on wealth equity. We’re not anywhere close to that yet.

So we’re left with the fact that we are ALL broke, and will ALL have our wealth reduced. And I find it very difficult to make a blanket statement that one saver is more deserving of preserving all/some of her wealth over another performer in this theatre in which we all play a part.

March 23, 2013 at 5:40 am #7209ParticipantMarch 23, 2013 at 6:42 am #7210ParticipantThe main benefit will be Greece who will not need to pay back the money lent to them by the Cyprus banks who have gone bankrupt.

jal,

When a concern goes bankrupt, the debt of others to this concern do not disappear!

The debts now belong to the creditors of that bankrupt concern – its depositors in the case of a bank. It does not mean that they will eventually get it (except in the best-case scenario), only that the debt is still there and has not disappeared.

March 23, 2013 at 7:02 am #7212ParticipantI just happen to like home grown tomatos.

The tomatoes – as you well know – were just an example of the dislocation of that society. A dislocation not unconnected to having joined the EU and the EZ.

When I was studying civil-engineering in London in ’68-’71, I had a friend from Cyprus – it was one country at that time. He used to tell us about how “backward” the “peasants” on his island were. For example, he mentioned that in the villages the women washed the reusable condoms and hung them on their wash-lines to dry in the sun. I bet that trick does not have a place in the TAE’s Primers. 🙂

By the way, he vanished shortly after the Turkish army invaded Cyprus. His home town was Famagusta and it is now in the Turkish zone. I made enquiries recently and I guess he was one of the many victims.

In 2009, I went to the South of France on holiday with my family. I wanted the kids to see the place before we moved to Australia. I found they were selling grapes in the supermarkets at 5 Euros/kilo – during the month of September. Amazing. Nearby, there were vineyards and the as yet unharvested grapes were rotting and falling in bunches on the ground.

This is what I mean by dislocation. There are tax and administrative reasons why this is happening. It is a direct consequence of governmental meddling in the marketplace. The EU has a battery of laws which prevent people from carrying on activities that they were doing from Roman times. Cyprus suffers from the same malaise.

March 23, 2013 at 7:29 am #7213ParticipantGood day Nassim

I can think of various mechanisms from the pre-bank failures.

ie. Loans sold to hedge fund for pennies and settled by Greece for pennies.But since the meltdown, those rules no longer apply and new rule are being invented every day.

( As of the end of January Greek banks used €122bn of collateral to borrow €31bn via ELA, i.e. an implied haircut of 75%.)

https://www.zerohedge.com/news/2013-03-22/jpmorgan-inevitability-europe-wide-capital-controls

JPMorgan On The Inevitability Of Europe-Wide Capital Controls

ELA is limited by the availability of collateral and the haircuts that the central bank applies to this collateral. The Greek case is the most characteristic example of how punitive haircuts on ELA collateral can be. As of the end of January Greek banks used €122bn of collateral to borrow €31bn via ELA, i.e. an implied haircut of 75%. In contrast, they borrowed €76bn via normal ECB operations posting collateral of €97bn, i.e. the implied haircut on their normal ECB borrowing was 22%. The higher haircut on ELA collateral i.e. is mostly the result of the lower quality of this collateral, typically credit claims, vs. that accepted in normal ECB operations, typically securities. But it perhaps also reflects the higher riskiness the ECB sees with its counterparty, i.e. the national central bank and eventually the sovereign, when a country’s banking system has to resort to ELA.

What is the maximum ELA borrowing for Cypriot banks? Looking at their assets, Cypriot banks had €72bn of loans to non MFIs as of the end of January, roughly equal to total non-MFI deposits of €68bn. Assuming that all these loans are acceptable as ELA collateral with the same average haircut as in the case of Greek ELA, i.e. 75%, results to only €18bn of total ELA. Given that Cypriot banks have already €9bn via ELA, this leaves them with another €9bn of potential additional ELA. Of course the ECB could be more lenient with its ELA haircuts with Cypriot banks relative to Greek banks, and indeed even in the case of Greek banks, ELA haircuts appear to have been as low as 50% at certain points of time during 2012. But we doubt that total ELA could exceed €30bn, which represents more than 40% of the loan assets of Cypriot banks. In the case of Greek banks ECB reliance never exceeded 40% of total loan and security assets. So further liquidity support from the ECB seems limited, and not enough to offset the €21bn of non-euro area deposits with Cypriot banks, largely Russian (80%) and British (20%) and the €5bn of deposits with other euro area residents outside Cyprus.

March 23, 2013 at 8:28 am #7214Participantdavefairtex post=6911 wrote: What *should* happen in Cyprus depends on how they legally treat depositors in a bankruptcy. If a depositor is an unsecured creditor, wow, tough luck for them, they stand in line along with the junior bondholders. If they have depositor preference laws in place, then the bondholders should be completely wiped out before those depositors – even the uninsured depositors – lose a nickel.

Of course once the government steps in and circumvents the usual processes, then they get to pick winners and losers, just like we did when TARP parachuted billions in equity buys across the US banking system in 2008-2009.

…

As for the moral argument – I’m quite comfortable picking small depositors (especially the ones given a guarantee of protection by the government) over bondholders who were “the smartest guys in the room” who signed up for risk when they made their investment.

This ethical discussion reminds me of the argument that the majority of the blame for the housing bubble should be placed on home buyers. Bankers have been in the business of making loans for 400 years. Its not rocket science – there are well-established principles of doing business. … I’m quite comfortable placing the vast majority of the responsibility on the con men. Especially when “the con” is their entire business model.

Hey Dave, don’t get me wrong. I fully agree with the notion that corruption is rampant and corruption will squash the little guy, and I wish it weren’t so. Nevertheless, I do not agree that drawing a clear line between savers and bondholders gets us very far in preventing this.

1) While many bondholders are gargantuan financial enterprises with huge financial power, bonds are also held by ordinary investors trying to protect their wealth. Indeed, the aging widow may own bonds and have no savings. Her pension may also be made up largely of bond investments.

2) Many gargantuan financial enterprises are “savers”. Indeed, part of the insinuated moral argument behind the Cyprus Solution is predicated on the fact that huge savings in Cypriot banks belong to rich and nefarious Russian mobsters. So savers cannot uniformly be lumped together as innocents.

3) I am a saver. And so I know that I am a prime target. I must take responsibility for my future, or I fear someday I won’t eat. I have some “safe haven” bonds towards this same effort.

4) A bank deposit is another promise to re-pay with little distinction for me from the promise to re-pay on a bond. Both promises can and, going forward, certainly WILL be broken. There are more promises to pay than there is money to pay all the promises.

5) The fact that there is a sequence of entitlements in a default that is supposed to flow down from bondholders being hit first before depositors, well that is simply a rule invented by the very system that is now rewriting the rule. The rule was only in place so long as it suited the system. It provided a certain base of “trust” upon which the status quo accomplished all its dastardly, credit-driven deeds. The status quo must re-write these rules to survive. And being a depositor means being part of that game. I have long advocated NOT being a depositor, but rather a saver who relies much less on the banking system.

6) When we are broke, globally, because there are far more promises to pay than money to pay them with, then I maintain that trying to choose who gets a haircut first is tantamount to rearranging the deck chairs on a sinking ship. All the players will take haircuts, and the weakest will first. I would like that to be different, but in the interim it will not be.

7) An alternative, more palatable solution would be for haircuts to be means-tested. That is impossible for so many reasons. And so what cannot happen , will not happen. Just as what cannot be repaid, will not be repaid.

8 ) Finally, I’d argue that if we overly emphasize the moral high-ground of depositors over other players in our capitalist charade, then we risk increasing depositors’ complacency. Why did ordinary Cypriots not withdraw their money when they could have? Because they believed deposits were sacrosanct. How can anything be sacrosanct when the whole system is debauched and desperate? And so, I’ll argue for the sake of argument that deposits are one more facet of the same global Ponzi that includes bonds and stocks and we’d be fools to try to distinguish any of them on moral grounds.

9 ) I certainly advocate helping aging widows in your community. If you can survive all of this with some wealth intact, you have an opportunity to help those who do not. Because the social safety net that we also assume is a right will vanish along with the bonds and the deposits too. Just as your own wealth preservation is your personal responsibility, it will increasingly become our personal responsibility to help our neighbours in need.

March 23, 2013 at 11:57 am #7215Participantskip –

As always you make me think. However!

I’m going to paraphrase one of my favorite quotes from Dr. Strangelove: at this moment, Cyprus is choosing between two admittedly regrettable, but nevertheless distinguishable outcomes: one, where they live up to their promises to little depositors, and the other, where they swipe money from everyone regardless of the guarantees that came before.

In this article: https://www.reuters.com//article/2013/03/23/us-cyprus-parliament-idUSBRE92G03I20130323

there is discussion about the reasons why Cyprus originally wanted to include everyone in the losses: protecting their offshore banking establishment. Now it appears that is off the table. And I think that’s a good thing.

Even though there will be losses going forward, we can still choose societally better and worse ways of apportioning them. I think this process is happening now in Cyprus.

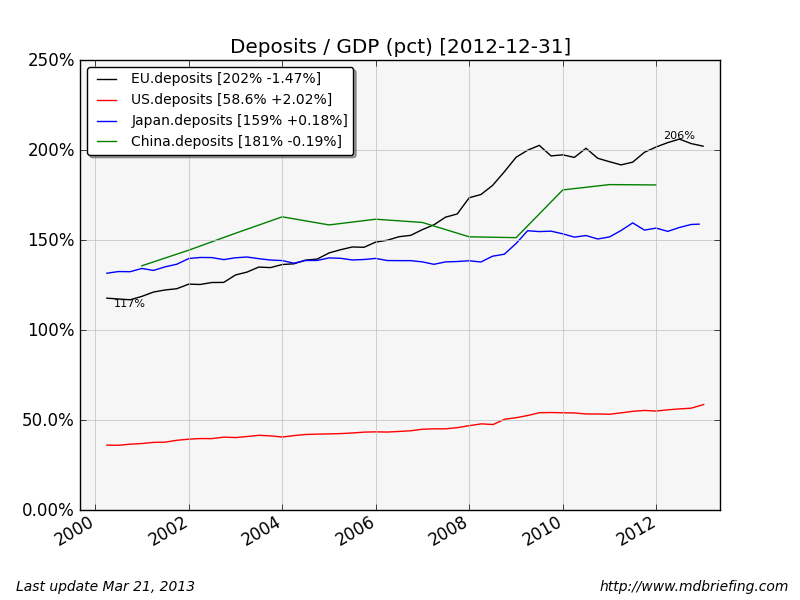

Just as a matter of interest, I wanted to see what the overall liabilities looked like in each area’s banking system. Here is a chart (of course) of what I found. The eurozone has deposits equal to 203% of their annual GDP, while the US has deposits equal to 59% of GDP. Europe’s banking system is massive, which means practically speaking when all of our property bubble chickens come home to roost, their uninsured depositors are going to take proportionally larger losses.

Because Cyprus was heavily exposed to Greek debt which has already defaulted (you cannot pretend-away a sovereign default) and its banking system was really huge relative to its GDP, it is operating as the canary in the coalmine – the earliest losses, in a place least able to cope.

Regarding bondholders. I am familiar with who owns bonds. Largely, it’s not grandma – if it is, its Rich Grandma who can generally deal. It might be grandma’s pension fund, but the professionals managing the diversified portfolio of bonds in her pension fund have a much higher level of experience about these things than grandma herself has in managing her own deposits. And mostly it is top-10% types, like you and me, who can more easily absorb the losses.

Again, two regrettable but distinguishable outcomes: one where you soak grandma herself, and another where you hurt a percentage of grandma’s diversified pension fund – the better to educate those pension fund managers about where to invest grandma’s pension money.

Of course the lesson that really bad losses have the potential to hurt everyone is there for all to learn. If and when losses get more severe, everyone is going to be invited into the problem-solving circle. So to speak.

March 23, 2013 at 2:28 pm #7216Participantskip –

One last note. Götterdämmerung has not yet arrived. It may – or may not – ever arrive. So I am not going to act as if it is a present reality unless and until such a thing comes to pass. We still have trash collection, police (more or less), and paved roads. I will therefore continue to advocate that losses be apportioned largely along lines I consider to be reasonable.

In the case of Cyprus, I advocate that their banking system that has been acting as a safe-harbor for offshore money gets thrown under the bus and the small depositors on Cyprus get saved – given that explicit promises on that exact point were made to small depositors. Perhaps after the end of times actually hits I’ll feel differently, but until that catastrophe strikes, I’m cool with how things are proceeding today.

March 23, 2013 at 3:02 pm #7217Participantdavefairtex post=6928 wrote: skip –

One last note. Götterdämmerung has not yet arrived. It may – or may not – ever arrive. So I am not going to act as if it is a present reality unless and until such a thing comes to pass. We still have trash collection, police (more or less), and paved roads. I will therefore continue to advocate that losses be apportioned largely along lines I consider to be reasonable.

In the case of Cyprus, I advocate that their banking system that has been acting as a safe-harbor for offshore money gets thrown under the bus and the small depositors on Cyprus get saved – given that explicit promises on that exact point were made to small depositors. Perhaps after the end of times actually hits I’ll feel differently, but until that catastrophe strikes, I’m cool with how things are proceeding today.

That is a pretty good argument. Safe, but persuasive. Nevertheless, we probably diverge in the respect that I do think this is part and parcel of the End Game. It is here. This is it. I don’t think the curtain opens and the music swells to cue the real commencement of the big event. Various cascading calamities have been with us since 2008. Just as TAE has predicted, it is now resulting in deposit confiscation and capital controls, and in a westernized Euro country no less. They will only increase in scale–eventually giving us a couple of events you might agree is the real “biggie”, but there will be lots of biggies that take us to the worst of it. It’s not a single night, in my opinion. Your roads will paved for quite a while, but the pot-holes will increase too (as they probably already have). And in this respect, that is the decline in the standard of living I was referring to, except it will come on multiple fronts, not just pot-holes in the road.

I think part of what doesn’t sit right for me, in making this “innocent depositor” distinction, is that it presupposes a solution. The notion is completely dependent on the idea that choosing some other option (i.e., bondholder haircuts, for example, and no deposit levy) will take us to a place where Cyprus or the Eurozone will be made whole. It is my deeply held conviction that it will not solve anything. And in not solving anything, deposits will ultimately vanish anyhow, just at some later date–maybe only days or weeks later, too.

Essentially, I do not think that any version of the Troika’s or even the Cypriot people’s preferred solutions makes an insolvent country solvent. Only declaring the insolvency can do this (which entails write downs everywhere in this case, including deposits, since there is not enough money to pay everyone out on their deposit, ever, once the Ponzi sham is fully understood). Bankrupt is bankrupt, and we’re not talking about a person, or a company or even a government, but an entire system. All the bets made in that casino are going to get raked in by the house, no matter who is making them. And that includes every Cypriot who made the bet of trusting their bank. And it means us too.

The dilemma reminds me somewhat of the protests in Spain. I sympathize with the plight, but most of the Spaniards hope their rioting will somehow convince the Troika to be nicer, with a view to returning things back to the way they were, when everyone had money for $8 coffees every day and great government jobs with pensions at age 55. However, the reality is that while Spain should be fighting for its freedom and independence from bankers control, winning this fight will not make them whole in the way they hope. They will still be broke. Standards of living must collapse and will collapse, because they don’t have the real wealth to continue living the way they have been living. None of us have the real wealth to live how we have been living. And our deposits, along with our bonds, must eventually reflect that. The question only remains whether you can try to preserve something more, as a weaker participant, given the stronger players are going to outgun us most of the time. This is where I think Ilargi and Stoneleigh have provided some great insights so the ordinary person has a fighting chance of staying afloat in the coming years.

March 23, 2013 at 8:24 pm #7218ParticipantBankrupt is bankrupt, and we’re not talking about a person, or a company or even a government, but an entire system.

None of us have the real wealth to live how we have been living.

I can only repeat.

What is happening has been planned.Its a troika experiment.

Now we get to see what happens when the central banks do the right thing and don’t start up the printing press.

The objective is to get a default and gather the data from the resulting chaos.

All doomers should pay attention.

Coming To a Town Near You

March 24, 2013 at 11:46 am #7220Participantskip –

I think where we differ is one of viewpoint and expectation.

As I’ve said before, I see the future as a continuum of possibilities, one of which includes your EOW (in fits and starts) scenario. But that’s not the same thing as being certain that EOW is the only possibility. I will take what comes, and adapt as things become more clear.

Great example. Some people were dead certain The Final Crash was going to occur in 2008-2009. That didn’t happen. These people (and I include myself in here) were unable to correctly interpret events in real time. The takeaway for me from that event is, I believe it is best to remain mentally flexible and avoid confirmation bias. That way, I can clearly see what is actually happening rather than misinterpreting current events because I’m viewing everything through the lens of false certainty.

People who are certain of a future outcome tend to fall into confirmation bias. Its a very rational response – why on earth would you spend time considering evidence that something ISN’T happening when you are 100% certain that it will? Of course that’s a only a dangerous mental place to be if your job is to successfully interpret events and see what is really happening.

Its good to be out of debt. Its also good to have cash lying around, be in good physical shape, have a stash of food just in case, own as much of the critical bits of your life as reasonably possible, and be mentally and emotionally flexible enough to adapt to whatever change comes along.

Now for particulars.

Depositors (of course) under 100k aren’t innocent. But they WERE promised immunity, the bondholders knew they were taking a risk position, had no such promise, and these bondholders were compensated for the risk they were taking through years of interest payments. It just makes sense the ones NOT promised immunity take losses and the ones promised immunity do not. It conforms with my sense of justice.

Will this fix everything, everywhere, suddenly making everything all better? Of course not. But its the right thing to do in this situation. My opinion, of course. And the future can be left to take care of itself.

March 25, 2013 at 9:31 am #7227ParticipantLooks like after all that was said and done, they’ve decided to resolve the two ill banks in Cyprus the standard way, with insured depositors being protected, bondholders and uninsured depositors taking losses together. Amazing! It’s a first!

What’s more, normal savers in OTHER Cyprus banks aren’t having to pay for the stupid lending decisions made by the two large bad banks. This of course concentrates losses at the two banks that bought way too many Greek sovereign bonds, but I personally think that’s just fine.

https://www.reuters.com//article/2013/03/25/us-eurozone-cyprus-text-idUSBRE92O02920130325

1. Laiki will be resolved immediately – with full contribution of equity shareholders, bond holders and uninsured depositors – based on a decision by the Central Bank of Cyprus, using the newly adopted Bank Resolution Framework.

2. Laiki will be split into a good bank and a bad bank. The bad bank will be run down over time.

3. The good bank will be folded into Bank of Cyprus (BoC), using the Bank Resolution Framework, after having heard the Boards of Directors of BoC and Laiki. It will take 9 billion Euros of ELA with it. Only uninsured deposits in BoC will remain frozen until recapitalization has been effected, and may subsequently be subject to appropriate conditions.

4. The Governing Council of the ECB will provide liquidity to the BoC in line with applicable rules.

5. BoC will be recapitalized through a deposit/equity conversion of uninsured deposits with full contribution of equity shareholders and bond holders.

6. The conversion will be such that a capital ratio of 9 % is secured by the end of the program.

7. All insured depositors in all banks will be fully protected in accordance with the relevant EU legislation.

8. The program money (up to 10 billion Euros) will not be used to recapitalize Laiki and Bank of Cyprus.

April 12, 2013 at 2:17 am #7386Evan

Member“It’s up to you to protect your wealth so that you have a chance to survive and do some good….your wealth is going to be attacked sooner than later. TAE has excellent ideas around preparing for this inevitability.”

Hi Skipbreakfast,

Could you provide a link to the page about these “excellent ideas”?

Thank you.

April 12, 2013 at 7:30 am #7387ParticipantI think Stoneleigh provides some good advice here:

https://theautomaticearth.com/Lifeboat/how-to-build-a-lifeboat.html

Personally, I’d read all the Primers (see the links at the top of the TAE main page).

But a lot of the insights from Ilargi and Stoneleigh are best gleaned by reading as much of the Primers, articles and even the comments, going back as far as you have the patience and tenacity to read.

-

AuthorPosts

- You must be logged in to reply to this topic.

Sorry, the comment form is closed at this time.