skipbreakfast

Forum Replies Created

-

AuthorPosts

-

skipbreakfast

ParticipantYes! You’re right, Ilargi. Something does NOT add up here. I was about to come on here and make a comment to the exact same effect, but you’ve written a whole article on the question.

Something is completely awry. I am simply gobsmacked by the EU decision on Cyprus, and it so clearly threatens the rest of the Euro enterprise, I can’t believe they ventured along this path.

They could have simply continued their ridiculous bailouts a little longer. Why not? They know more are coming for Greece, Italy, Spain, et al.

But something is different for Cyprus for some reason. Is it an experiment? As you suggest, it simply too loaded with contagion risk. Are they trying to force an exit? As you suggest, that would create just as much contagion risk as the “stability levy/theft”.

I’m really watching this in total amazement. I do not know what game they’re playing. We’re on some point of the collapse continuum, I just can’t figure out where–certainly I did not see the hand of the EU being forced, not to this degree. Not yet. That will surely come in the future. But this? I’m just utterly perplexed…and unnerved.

After all, even proposing this notion risks contagion.

Perhaps they know that the jig is up and they want to make an example of Cyprus–which will default and dissolve into chaos, and it will be so awful that no other country dares follow?

ParticipantIlargi, can you elaborate a little for me how high (or low) deposit-to-GDP ratios affect a country’s prospects going forward?

Participantauto-Daniel,

The dude is a pastor. I guess for me that seriously undermines his credibility in terms of any insight as to who is really being controlled by whom (given his religion’s shocking history of collusion, conspiracy and exploitation). He cites senior Exxon executives…and then doesn’t name them. One single solitary on-the-record name would help his case. Instead it’s all these shadowy cloak-and-dagger figures that border on the supernatural, especially in their powers to divine and control a future. A future which physics describes as infinitely variable and chaotic. But then as a pastor, he would have certain leanings to believing in the supernatural, and some individuals having magic powers beyond the rest of us.

I simply don’t see the point of these diatribes. If the powers are so magical, what are you going to do about them. Without any concrete evidence, what difference does it make. Your world is fucked either way (whether it is being controlled by wizards or simply following a very inevitable cycle of exploitative expansion and greed, ending in the equally inevitable cycle of contraction and fear). The more powerful will always seek to expand their power. And the weak will always succumb to greater or lesser degrees…until the tipping point, and the castle falls.

There is so much for us to do. Seeking out supernatural phantoms, beyond our reach whether they exist or not, doesn’t change our immediate circumstances. We have very real, concrete, tangible preparations to make. We should be educating ourselves about the dynamics of market cycles, and cutting through the obfuscation presented by very real mainstream media, which does have very ordinary, though grandly diabolical, intentions to pull the wool over our eyes.

I advocate truth-seeking where it leads us to answers that can change our lives and our chances for survival in an inevitably difficult future. I reject wasting time looking for scapegoats, demons, ghosts, witches, phantoms, illuminati, magic bankers and all other imaginary gremlins. The system is sick. We have to start by making our immediate communities healthier, and our families more resilient. Resisting and revolution on the larger scale will also follow naturally, but only if we’re alive long enough to be part of that movement.

ParticipantI trust most of you have just seen this haunting ’60-Minutes’ story on the China housing bubble, depicting entire cities full of shining but unoccupied skyscrapers and thousands more unfinished towers. It underlines something that I have noticed in my home country of New Zealand, where real estate speculation has been long elevated to its own truly twisted state of manic speculative fervour: some houses are worth $0. That’s not a typo. That is zero dollars.

Yes, when speculation reaches a certain point of mania, I can assure you people pay a lot of money for properties that are simply unfit for occupation or development. In the mania, folks are convinced that anything, as long as its some land they can call their own, will guarantee them future profits in a world where “god ain’t making any more land”. The truth, however, is that god made a lot of lands that, in more rational times, are simply forsaken for very good reason–they are worth $0 because they offer nothing a rational businessman or homeowner wants or needs. There is nothing unique about them (in the case of towering apartment buildings). Or you can’t sensibly build on them, grow on them, or even practically LIVE on them.

Where I currently reside, in New Zealand, speculative investors have talked themselves into buying south-facing cliff-faces at the height of a mania (remember south-facing, when your Antipodean is NOT a good thing–it’s bloody cold). There are A LOT of such properties, purchased with dreamy intentions of development, only to be abandoned after the first attempt to put in a frightening ski-slope driveway. Now that the mania is beginning to subside (though that is a relative term for this completely insane housing devotion here in Aotearoa), people are trying to unload these cliff properties. But to everyone’s surprise, there are no takers. Yup, some properties are worth $0. A rational man wouldn’t want to pay the property tax on the thing even if it was given to him for free.

And when you see the Chinese property video above, you realize this is a feature of every property mania. There are such great distortions in such markets that a sizeable percentage of the market is actually going to be unwanted and utterly rejected by any prospective buyer in the future, no matter what the price. Just think of the phenomenon of the “ghost town”, something we will begin see a lot more of over the next decade.

So, in a saner market, almost all property has SOME real value. But in these extremely distorted times, that is simply no longer the case. Good property will continue to be good property, but will still drop precipitously due to the pressures of a credit implosion. Meanwhile bad or useless property will be recognized as just that. This will absolutely, without a doubt push “average” property prices BELOW the long-term mean for some period of time. At least until the value-less properties are recognised as such and expunged from the marketplace in the big write-offs that are yet to come.

ParticipantHappy birthday TAE. I’ve only known the blog for 3 blinding fast years. I can only say how much I appreciate the wisdom and insights the site offers. Hope to catch Stoneleigh in New Zealand on her next Down Under tour. Sorry to hear Ilargi won’t be making it…but good to hear he’ll be bionic at least.

ParticipantYour comments about insurance companies failing to pay really strikes a chord with me here in New Zealand. Two years after the Christchurch earthquake, people I know personally are still struggling to get the compensation they’re owed from insurers. At this point I’d say every dollar unpaid so far has rapidly diminishing chances of ever being paid. Christchurch was the largest “insured disaster” ever—there have been bigger quakes but apparently not with so much coverage at stake. Now I have to wonder if Sandy now takes that prize. And given insurance companies may be suffering diminished returns on their own investments the past couple years, it really makes you wonder if they have anywhere near enough money to cover Sandy.

ParticipantGotta say, Alan is quibbling with the definition for no good reason, in my mind. The end result of TAE’s forecast is the same: prices collapse. The road we travel to get there is what is at issue, and as I have also argued in the TAE comments (because I find TAE’s forecast the most persuasive on the gawd-forsaken Interweb), this road does not follow a straight line and has many distracting curves that blind us to the final destination. One of these curves is the absurd notion of “biflation”, or as another economics blogger has called it “quasi-deflation”. Neither term is helpful. They don’t tell us where we are within Kondratieff’s theory of major cycles, which lead inexorably from inflation to deflation, without being bi or quasi anything.

Kondratieff’s six phases of a business cycle can be summarized as follows:

Phase 1: Credit Expansion and Liquidity

Phase 2: Commodity Prices Rise

Phase 3: Economic Activity Grows

Phase 4: Early Inflation

Phase 5: Wages and Spend Slowing Down with Inflation

Phase 6: Recession / Depression / Asset DeflationNote that after Phase 4 you are now headed into deflation, even while some prices “inflate” in value. The value in TAE’s view of deflation is that by only looking at prices, we completely miss the fact that we are on the deflationary, declining side of the mountain, which leads to one very unavoidable bottom way, way, way down.

There has ALWAYS been debates over how to define inflation and deflation, Alan. Economists can’t agree, and never will. Clearly, however, the dominant economic group-think about the forces of money and credit have failed us. Many smart, progressive economists are demanding that mainstream economics change their definitions too, such as Steve Keen. Please feel free to argue with Professor Keen as well about the definition of inflation or deflation and maybe he’ll choose to call it something else entirely to satisfy your inflexibility, like, maybe call it Pluto, I don’t know. I don’t see the point of that at all, though.

We are in deflation because the FORCES are pressuring prices DOWN, even while there can be periods of rising prices in SOME goods or services. That is deflation, and and all that is left is convincing people that is the case and waiting to see how and when the worst of it comes to pass. Coming up with new terms for such an age-old phenomenon will serve no one well and distracts us from the challenge at hand.

Let’s please keep in mind that NEVER, in any inflationary or deflationary cycle, will you find that all prices for all things rise or fall in lockstep with the overarching trend at the same time. If you were to adopt such a rigid outlook in YOUR definition of inflation or deflation, we would never, ever be in either one. That isn’t useful at all either. So maybe you’re the one who needs to come up with a new word for what you’re trying to describe. How about “life”? Fact: we are either heading to one or the other macro-direction, even while there is fractal noise on the journey, making the call murky UNTIL AFTER THE FACT. I have no interest in sitting passively until after the fact when so much is at stake, leaving myself ill-prepared for the worst of either trend.

So even while some prices may be falling, we can still be in an inflationary cycle, and should take certain precautions. On the other hand, we can see prices rising and still be at the edge of a deflationary collapse. Just because TAE has had the good sense to go deep into the failure of modern economics and find the real roots that presage infaltion/deflation doesn’t mean they are now required to call it something different for the sake of simplistic mainstream journalism, or to cater to Bernanke’s hopes that people will read an inflationary trend and start shopping, or to appease a cadre of failed Post-Keynesian economists.

Deflation means the forces in play are pressuring prices DOWN, even while the prices might be momentarily buoyed up. If you think that the pressures are the opposite, and will send prices sky high, well then, you are actually calling for inflation. A whole other kettle fish. And entirely different argument. Go ahead and write about that on your blog. I’d be curious to read your reasoning.

September 29, 2012 at 2:43 am in reply to: There's Only One Way Forward For Europe, And This Isn’t It #5830ParticipantProfessorlocknload post=5526 wrote: …Are central banks really all to blame here? Is a scorpion to blame for stinging the tortoise who transports him across the river, upon reaching the other side? Isn’t that what scorpions do?

I remember the story goes a bit more like, “The frog offers to take the scorpion to the other side of the river after the scorpion promises not to sting. Half way across, the frog feels the burning poison in his back and exclaims, “Scorpion! Why did you sting me? Now we will both drown.” And the scorpion replies, “It is my nature.”

I only like that version because it underlines how ultimately neither the frog nor the scorpion win in this game. 🙂

ParticipantA few quick quotes from audio interview with Danielle Park on TalkDigitalNetwork:

“A lot of key risk assets are below the [QE Infinity] announcement a few weeks ago…”

“Commmodity prices have probably peaked in the late 2007 cycle with the credit bubble…Here we are 6 years later and it seems that was the case…You keep making lower lows….You’ve got tons of money chasing after what is slowing demand globally. This QE has not been a friend to the producers…”

“The reality is with the second quarter with all the QEs…[the US] was barely able to grow 1%…We must be in a recession already.”

MY COMMENT: Park is a down-to-earth, plain speaker, but smart as a whip and brave enough to speak her mind. Nevertheless, it’s interesting to note how–just like the rest of the financial analysts and economists on the planet–we’ve all been drawn into discussions on QE’s performance vis-a-vis economic numbers. Instead, we should simply recognize there is no honest intention on behalf of the Fed to issue QE for the sake of jobs or the economy. That’s a ruse we have all fallen for (save, perhaps, Ilargi) as evidenced by constant comparisons of economic data to QE announcements. The reality is QE has one purpose only: it’s a wealth transfer to the banks to prepare for the ongoing deflation. The Fed’s primary concern is backstopping the banks against their deflating balance sheets which threaten to implode globally. We’re all missing this key element in the debates. But Park’s analysis is still interesting to track because she’s one of the few who called and continues to call for our current deflation.

ParticipantQuote from article,Why QE Won’t Create Inflation Quite as Expected – 27 September 2012 – Charles Hugh Smith

Add all this up and here’s what we get: money is not just being created by the Fed, it’s being destroyed by declines in asset valuations and writedowns of impaired debt. Credit may be expanding but the top rung of households is paying down debt, not borrowing more, and the bottom 95% are unable to add much to their already staggering debt load.

Incomes are declining, providing a smaller base for both spending and borrowing. The top 5% may be experiencing a “wealth effect” as stocks soar but 7 million people cannot levitate the entire $15 trillion U.S. economy much while the incomes of the 137 million other workers are stagnant or down.

Money velocity is plummeting and banks are hoarding Treasuries as much-needed collateral.

It’s difficult to see how these forces could generate inflation. There may be new money and credit being created, but very little of it is flowing to households whose spending in the real economy drives inflation.

MY COMMENT: I don’t have much to add. Charles sums up the reality of our current deflation perfectly in his article. I can only conclude, as I have argued in the TAE comments, inflationists are misjudging the implications of price rises in toothpaste and tomatoes. Some isolated cost of living increases do not offset the implications of vast deflation as described by Charles Hugh Smith.

___________________________________________________September 27, 2012 at 1:49 am in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5807Participantilargi post=5502 wrote: Skip et al

I think we need to consider much, nay MUCH, more seriously that Bernanke is not trying to fix the economy. That that’s nothing but a very persuasive fairy tale. The QEs and other bailouts are ways to minimize losses for banks and their shareholders, at the expense of the man in the street. They are mass wealth transfers.

You are 100% absolutely correct.

It’s a fact I’ve come to realize but the QE propaganda machine is so effective, I atually find myself slipping into discussions about how QE “won’t fix the economy”. Of course it won’t! It’s not even designed to!

I agree: Bernanke can’t publicly tell us he is delivering more QE because of the specter of deflation–even though that is the real reason for it! Instead, he has to give us a smoke-and-mirrors excuse for QE3 implying that it has something to do with creating more jobs.

Quite a subtle and devious tactic. You say you’ll buy mortgage backed securities through QE3 until job numbers reach some magic level. It implies that there is some obvious, causal connection between mortgage backed security purchases and job creation. He could just as easily have said, “We will buy mortgage backed securities until the polar ice cap increases 15%.” Not related. And probably not going to happen in any event.

Buying MBS is designed to backstop the banks because Bernanke sees an imminent deflation. He knows something the public doesn’t realize, and he will not say it for fear of making it worse (and he’s undoubtedly afraid it makes the Fed look like a fool, since the Fed has been so cavalier about its omnipotent powers to stop deflation).

The bull about job creation is just obfuscation. Its a way to sell more bank bailouts to the people. It’s very effective propaganda. Terribly ineffective job creation.

September 26, 2012 at 5:59 am in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5798ParticipantYou have a point Synchro. I think a fact to keep in mind, which actually agrees with your point, is that the governments of the world have been using growing credit to backstop a lack of real productive growth in the western world for longer than 25 years. We’ve used up our time and all the credit dollars already, if you believe, as I do, that eventually markets and politics reject unfounded credit creation by a government.

So the call right now is not so much about which month or even year such a credit expansion inevitably unwinds, but that there are terribly ominous signs that the expansion is on its last legs. This isn’t a vacuous timing call. This is an analysis of the facts as they currently stand. Things are unstable. Things have been unstable for a while now. Bernanke and others said such calls, like TAE’s, were unfounded…BEFORE 2008.

The fact that a “deflationary crisis” happened in 2008 was our wake up call. It was deflationary because money froze and became illiquid in the system. Something was and is now broken. It’s not been fixed. Quantitative easing does not FIX an economy that hasn’t been truthfully productive (i.e., earning its keep in terms of real wealth creation) for decades. QE is a desperate attempt to prepare the banks for a worsening deflation. But as far as fixing the economy goes, it won’t work. More and more QE has less and less impact on the economy. Because the markets HAVE woken up already and they’re telling us we’re living beyond our means. That’s what has given us the crisis. And it’s getting worse. This is deflationary.

The call is that credit creation will actually break down further long before it gets better.

Given how much credit has already been created to date, and yet we’re in even more trouble anyway, it is less than likely–more like impossible–for wanton credit creation by the Fed to last ANOTHER 22 years. They’re struggling to convince us that the past four years have been worth it. How much longer will we, the voters, not to mention the stock and bond markets, believe it? I don’t believe any economy can create unfounded credit for 100 years. We have pretty much used up our allotted 22 though (I’m using that number because you use it in your comment).

Philosophically speaking, nothing is certain. But risk is terribly pervasive right now, and it’s bigger than we’ve seen it in our lifetimes. Do with that what you will. Usually when you’re in mid-air over a 200 meter drop, you hit the ground and die.

The latest evidence that risk is pervasive? QE3. That wouldn’t have happened if Bernanke didn’t have a terrible feeling in his stomach about DEFLATION. By the way his terrible feeling is based on oodles of data you and I aren’t even privy to. He’s told us what he sees in the data. That’s why he gave us QE Infinity. That should be a sign to run and hide, not play the markets right now.

September 26, 2012 at 2:44 am in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5795Participantbluebird post=5484 wrote: Yeh, maybe it’s time to stop accessing banks/credit unions before Internet banking is denied. When the tipping point is reached that throws the world into a financial crisis, does anyone else think access to banks will suddenly stop the auto-deposits and auto-payments? Or will banking gradually be eliminated?

Thanks bluebird. I find these conversations more interesting than gold (buy into the gold bubble if you feel like gambling or hedging and take your chances–what’s more to be said?).

I think you’re saying we shouldn’t rely on digital money and I think you’re right. Cash–the fold-able kind, not the digital kind–is important.

As for banking, there’s a good chance that electronic banking lasts longer than any sort of cash banking. Which is NOT to say that digital banking lasts longer than fold-able cash in the economy–just that the banks will stop giving out fold-able cash at the tills and ATMs, while they continue to encourage the digital kind. (I’m not predicting as far as a day WITHOUT computers–that’s probably coming, but it’s much further off than our financial collapse).

I foresee a terrible shortage of actual hard printed currency (the fold-able kind as it has been called). The digital kind, such as the Fed is creating right now, will be more plentiful than the fold-able kind for a long while yet, even as the digital kind is erased faster and faster over time.

There is a reasonable argument to be made that fold-able currency may offer a premium over digital money. So a real paper dollar is worth say twice as much as a digital dollar. In some ways it always has been, which is why trades-people will offer to do the job for a lower price if you pay cash. Those hard dollars are worth more to him than the digital dollars.

Definitely, there will be capital controls coming which try to impede our use of fold-able currency. As tax revenues drop off a cliff, and more of the economy is driven underground, fold-able cash will be something everyone will want. Digital cash will serve the system for as long as the system can make it last.

So I think you’ll still be able to buy things with digital currency. There may be a few zeroes taken off your bank balance of digital currency in the meantime, though. That $100,000 balance could easily become $1000. You’ll still be able to shop with that $1000, in my opinion. You’ll just be much poorer than the person who somehow turned that $100,000 into dollar bills you can hold in your hand.

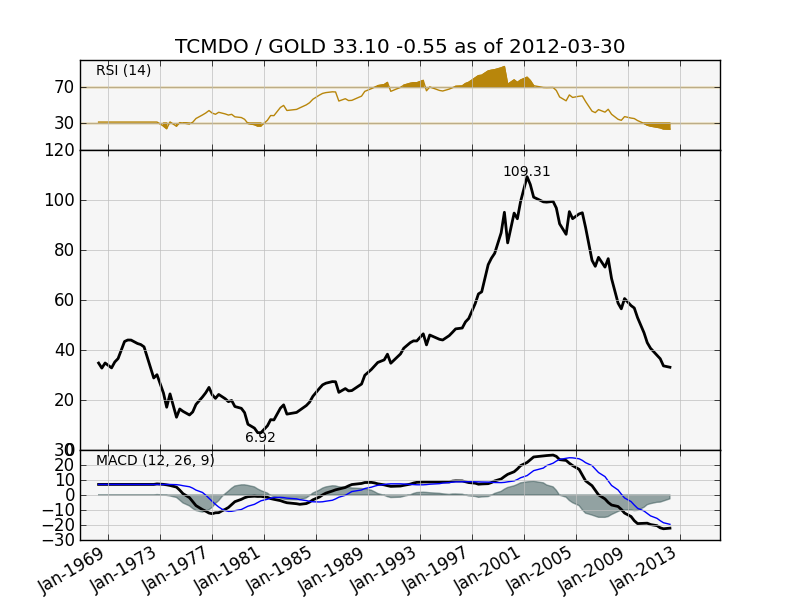

September 26, 2012 at 2:11 am in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5794Participantdavefairtex post=5471 wrote: Skip –

Gold is most definitely looking expensive from the standpoint of your chart right now. But check out this chart:

This odd chart is the US total credit market debt owed divided by the price of gold. With a bit of (hopefully forgivable) hand-waving, we could approximate this to be the following:

TCMDO – claims on real wealth (Billions of $ US; as of apr-2012=$55T)

GOLD – real wealth ($ US per ounce, on apr-2012=$1660)We can see this bottomed out at a ratio of 6.92 back in 1981. Its got a ways to go before it hits that point again. But it certainly has made a brisk move already.

I think this chart is interesting because it pretty neatly shows the interrelationship between gold and credit from the standpoint of the major moves in recent times – and it also puts the current move in the perspective of history.

Then again it could be total bollocks. Let me know what you think!

Thanks for this chart Dave. Am I reading it right–gold’s value increases with credit? If so, the deflationary position has always been a colossal vaporization of credit once the deflationary juggernaut gets rolling. As Ilargi points out it’s the zombie money keeping gold and Apple stock afloat. When Fed printing no longer keeps up with credit destruction, look out below (by the way it isn’t even keeping up with it now when you factor in the evaporation of credit in the ginormous shadow banking world).

So while Fed balance sheet and government debt expands, gold may be going up. But deflationists do see a reversal of the expansion of both those forces. Either the Fed is dismantled entirely or politically curtailed. How about a new Fed chairman, and one less inclined to print? Or a bond market pressure that resurfaces–something Synchro seems to think is no longer a threat, mainly because they left Japan alone for 20 years.

Synchro:

I don’t think Japan’s reprieve is indicative of our ultimate future. Many have said it before, and I will say it again too–Japan’s reprieve came during 20 years of zombie money expansion in the rest of the world–the same zombie money expansion that gave us a Euro crisis, the Chinese “miracle”, and the US subprime mortgage collapse.

Bond markets are manipulated only so long as they make money going along with it. It’s free gravy–they’ll take it. But if they sense that there’s some money to be made on the other side of the equation (or the opportunity to mitigate loss), there will be a frantic rush.

Deflationists see a limit on the ability of a government to manipulate a market. Historically, manipulation has NEVER worked indefinitely.

September 25, 2012 at 12:00 pm in reply to: You're Dreaming If You Think The Euro Crisis Is Resolved #5769ParticipantYup, gold is up. So is Apple stock and actually even the Euro. Lots of things are up. That’s what has me particularly worried.

Dalio and others DO need to deliver a RETURN ON THEIR MONEY. They have lots of their own already, and they’re playing with other people’s who demand some kind of return. Credit-money is chasing returns out of desperation, whether it’s mutual funds, hedge funs funds or ordinary small investors who thought they could retire by buying and selling stock. If you’re not rich, you should be more concerned about the return OF your money.

In the dying days of this economy, there are profits to be made for the lucky ones. Like every ponzi though, most will get burned.

Just look at the “you-can’t-lose” real estate bubble (which is still going up in a few ridiculous places). All of those people who thought they were so rich because they had money on paper. Anyone who didn’t buy in was thought to be a fool. Ultimately, only a small percentage can and will sell up early and walk away with the profit. The rest of them will be underwater. Why can’t gold be any different. Like the real estate market, some markets will go up longer than anyone expects, but the end result is the same in a deflation.

There could easily be some upside yet in precious metals. I won’t be at all surprised to see a final incredible rush on this investment class before the house of cards comes down. You might be able to benefit from it. But this is credit playing the casino. As such, only play with what you can afford to lose (and given how hard it is going to be to make money in the upcoming years, you better have a lot of money).

I agree some gold as insurance isn’t so crazy, but the fact that gold is rising is not a sure sign that it is going to save you. Apple stock won’t save you either. These are all functioning as “risk on” trades. The day gold rises when the markets tumble will be much more evidence that something fundamental has changed. Right now, gold goes up with the casino. Someone’s gotta blow a bubble up or all the hedge funds and mutual funds will go broke very very soon! We aren’t going to buy real estate. We’re rather skeptical of internet stocks. Tulips went out of fashion a long time ago. Gold is wonderful, but beware–it has all the hallmarks of another bubble investment. Doesn’t that parabolic rise remind you of anything else?

September 21, 2012 at 1:44 pm in reply to: Bernanke And Draghi Are Not Trying To Save Our Economies #5727Participant

September 21, 2012 at 1:44 pm in reply to: Bernanke And Draghi Are Not Trying To Save Our Economies #5727Participantdavefairtex post=5420 wrote: Of course until a good chunk of that debt is defaulted upon or nominal incomes rise to make it sustainable, these forces remain in place. How long can this go on? As you have pointed out, a good deal longer than TAE expected.

It brings to mind Keyne’s quote: “Markets can remain irrational a lot longer than you and I can remain solvent.”

Now Dave…you’re talking like a true trader here. It’s a bold prediction Stoneleigh made, but was never about a timing certainty, rather a timing probability at the moment. This is very early days. Seriously, if finance all falls apart in a year or two, will we look back in 10 years and say Stoneleigh was so wrong because she was off by 24 months? This is a major, life-changing, SOCIETY-changing, history-changing economic turning point here (if financial collapse can ever even be reduced to a single “point” in time at all).

The prediction that financial trouble is imminent is important for people to take it seriously. It could have happened at any time. It still could. Eventually, the heat might be off. Eventually maybe we can relax and say we dodged a bullet and TAE was “wrong”…but almost everything is WORSE since those calls were made, don’t you think? More QE means things were not fixed with QE1 and QE2. In fact, if QE3 turns out to be bigger, I would say that things are much worse. How long can they print? Longer than we expect? Sure. How long is too long. Depends on the individual. I’m comfortable standing on the sidelines for a couple of years. I’m not a trader. But I do not believe any government can print to the degree that is necessary to suddenly fix half a century of credit addiction.

All I’m saying is, even if the big credit event happens in 2 years, in the scheme of a 50 year credit bubble, Stoneleigh won’t have been off by much.

Unfortunately, we’re in a truly complacent lull at the moment. According to market reactions, QE has apparently worked. But we’re not out of the woods.

People shouldn’t mistake the lack of obvious collapse for the lack of CATASTROPHIC RISK. We’re still in unprecedented times here. I’m still inclined to be very careful. And as Stoneleigh has argued, being very careful and staying on the sidelines is really only about losing some opportunity costs. That’s fairly priced insurance, in my opinion.

Not saying there isn’t money to be made in the dying days of this economy. Who knows how long the disease will last. Doctors give patients 2 months and they last 2 years. It doesn’t mean they’re not gonna die. Who you gonna bet on?

September 21, 2012 at 2:09 am in reply to: Bernanke And Draghi Are Not Trying To Save Our Economies #5720Participantdavefairtex post=5413 wrote: Synchro –

Personally, I would be quite interested in further extrapolation of the timeline possibilities.

I’m playing around with that right now. I’ve laid out my personal favorite four scenarios in more detail, and I’m working on the triggers that have to occur to move us from one state towards another.

Perhaps I need to make my own site! After all Ash went spiritual on us and made his own place…I guess I could go all analytical and make mine!

I’m very interested in your conclusions, dave! Thanks for the Armstrong link. I’d not read his stuff yet. Insightful, I think. Though murky in places too.

September 18, 2012 at 10:47 am in reply to: Bernanke And Draghi Are Not Trying To Save Our Economies #5647ParticipantThrowing my hat in this ring, I have to agree with Ilargi–no jubilee. Not within a timeframe that matters to us anyhow. I don’t consider the following a jubilee, which I envision as the 4 Stages of Debt Slavery:

1. The First Stage (Hunt and Peck) – In these early years of this Greater Depression, an increasing number of people can’t afford their house payments. The system is still standing, though, and “most” people are making payments, even if it’s really, really hard and they eat potato chips for breakfast lunch and dinner. As such, it is in the banks’ interest to take your house…selectively. They only need to sell it for a price equal to the outstanding mortgage.

Banks pick off the houses with the best sale-over-mortgage value. It will be a scatter-gun approach. Banks don’t want a deluge, as this undermines the sale-values they’re trying to realize. No jubilee here for you. Do you want to be at risk of being in the line of fire? I don’t. So get out of debt.

2. The Second Stage (Avalanche) – The selective approach to foreclosure–which was supposed to keep house prices reasonably bouyed–is abandoned in a panic to sell the whole damn lot before your competitor does. In Stage One, banks are protecting each other’s books, in a coordinated mutual interest. But a herd of banks can stampede too, and when one of them “rushes for the exit” and tries to sell every possible foreclosed house for anything it can get, we have an avalanche. Do you want to be swept up in this chaos? Get out of debt.

3. The Third Stage (Détente) – Once Stage Two has been taken as far as it can go, most house values are below the outstanding mortgage. You can’t chase everyone out of their homes and have an entire nation of homeless people. So the government pretends to care and passes some legislation (in coordination with the banks) to prevent any more foreclosure evictions. It’s a ruse, however. Those who remain might get to live in the house without paying anything, but the banks are just lying in wait. Your “living-for-free” arrangement is a trap. Anything of value will be taken from you, whether it’s a car, your gold, nice furniture. Any dollar you make will be garnisheed to pay for the outstanding mortgage. Any opportunity that puts you back into the money also puts you back on the bank’s radar–they will have the government backed authority to come after you. You may still have a roof over your head, but you’re poor with no prospect of changing that. How will you ever pay off the outstanding debt now? So get out of debt.

4. The Fourth Stage (The Not-So-Jubilant Jubilee) – We’re now years into a depression. People have long been immobilized by their housing debts in Stage One and Two. Some form of debt-forgiveness is enacted…AFTER the bank takes the house. In theory, you can go live in a communal living housing project, because you’re “freed” from the shackles of your debt. Oh, and your landlord? Well, it’s the bank who owns the housing project (through aforementioned foreclosure proceedings).

There’s still another catch. We discover that, other than for a small percentage of the most fargone lost-causes (the aged, the infirm), this debt-forgiveness is not absolute. Yes, a percentage of your earnings are freely yours to keep. You can buy groceries and even a car (…or horse?). But don’t ever count on becoming a millionaire without that mortgage coming back to haunt you. It’s clear now to anyone lucky enough to make it in the New Depressionary Economy (because some surely will) that ye ol’ mortgage debt from 2005 really was for life. You just thought they forgot about it while you were making $10,000 a year. Now that you’ve broken through to $100,000+ they’re all over you again. So this Stage Four is a lot like Stage One, Two and Three in disguise. You can see how there is now a cap on the population’s ability to ever break out of the 99.9% Only those who didn’t have debt to start with have a chance. So get out of debt.

Conclusion: I can’t really see the upside of debt–no matter whether it’s credit card or mortgage or student loan debt. A hyperinflation is simply too much like a gift to the people at the expense of the very rich and the banks. So your mortgage is now the same nominal price as a loaf of bread? Unlikely! our debts will never go away, even while there may be opportunities to temporarily avoid them. Your freedom of action will be reduced. And you take risks at every turn that it will be used against you. Of course there’s risk everywhere. The idea is to reduce your risk!

If you can get out of debt, do so. If you can’t, then reduce it or plan accordingly to survive. I am sure many people will have to hide away money rather than make mortgage payments just to survive. It will be the only thing a sane person can do in the circumstances. If you can’t get out of debt, start thinking about these risks and the ways you can reduce them.

(Edit: I added an additional stage (“Avalanche”)… Couldn’t resist.)

ParticipantIt does seem desperate, I agree.

It’s scaring the living pants off of people too. Which is exactly what Bernanke wants. He wants to smoke us out of our caves and into “the markets”. So we’re scared… I wonder if you’re right, and he’s actually scared too. I think he might very well be.

Participantskipbreakfast post=5228 wrote: 10) Should I be suspicious that you introduced this massive plan for easing within the same four-week window as both China’s and Europe’s big quantitative easing? I mean, seriously–what bad thing do you know about that we don’t? Greece is about to exit isn’t it?

Quoting myself and responding to myself…yikes, I swear I’m not all that narcissistic. But I did get a kick out of the fact my question beat Tyler Durden at Zero Hedge to the punch:

why did Bernanke go full retard yesterday? Data didn’t exactly scream ‘panic’ mode. Perhaps he knows something about this weekend in Europe and wanted to get out in front of it?

https://www.zerohedge.com/news/bernanke-koolaid-steals-draghi-punch-spanish-bonds-slide

I still swear he (they) read the comments on TAE…and everywhere else, I’m sure. Then again, that’s probably the narcissism talking.

I actually would imagine that the Fed’s panic button pushing yesterday is more likely anticipating something a couple months away rather than this weekend. Oh, like January 1st maybe? After the US election anyhow. Just guessin’.

Participantpipefit post=5207 wrote: Here’s where I think you are making your mistake, if, in fact I’m right, lol. (see, I’m not one of those chest pounding morons, lol). You deflationists seem to think that once you have established a linear or even exponential equation, you can extrapolate it far into the future or far along the ‘x’ or ‘y’ axis.

I’m afraid it is clear to me that hyper-inflationists are in fact the ones who take an equation and extrapolate far into the future. That is, inflationists are seeing consumer price inflation, and more significantly they’re seeing quantitative easing, and extrapolating that to infinity.

We’ve had four QE’s so far now (including today and Twist). They haven’t been big enough to get inflation going in a meaningful way (certainly not as measured by major assets and the velocity of money–if you’ll allow me to disregard “tomatoes and toothpaste” for a minute please, for all the reasons already discussed at length). Rather we still teeter on the precipice of deflation (which is why QE is announced again and again by the way!).

So the inflationist extrapolates QE forever (ie., printing) and disregards both its diminishing returns to generate inflation and the INCREASING resistance to it in the public and political spheres. To print to infinity has to have the public and political licence to do it. Even Draghi’s “print to infinity” is already limited by the German constitutional courts only weeks after it was announced.

Any announcement of QE to infinity is just a really amazing and quite desperate public relations stunt. There is no such thing as QE to infinity when at any time the political tides can turn (Ron Paul or a similar icon can be voted into office…or given that it’s too late for him, a turn in sentiment in Congress, etc.). So infinity is suddenly curtailed quite abruptly. That’s not infinity.

Some of the smartest deflationist analysis from Robert Prechter (who you guys refuse to read, I know) long ago predicted that QE would have increasingly diminishing returns. That the Fed would increasingly become vilified by the press and the people. That the Greenspans who were celebrated on the cover of Time Magazine as person of the year would be later seen to be inept, incompetent and even evil. And that is exactly what we are seeing. That is the current which the hyperinflationist equation is swimming against. Charles Hugh Smith makes some great points in this regard: https://www.zerohedge.com/news/guest-post-psychoanalyzing-fed

At some point, the desperation of the Fed will be recognized as just that by the people, and they will turn the political tides against anymore QE with a vengeance. We’re already that much closer–just look at how much the press and economic analysis of Fed policy has evolved over the past 10 years. The Fed is nearly universally hated (by all except Apple stock and gold buyers–and they’re the minority by the way–most people just want to earn a wage and get by). When the average person turns against the Fed, it will get ugly.

Not to mention the awesome power of the bond market to turn against the US and demand less easing. Probably an even more likely backstop than political machinations. As Ilargi points out in his succinct comment above, the US depends on the bond market. Bernanke appears to act unfettered–but the bond market is his master, and it has him on an invisible leash. When the bond market changes its mind–or even hints at it–there may be a very different landscape for Bernanke to operate within.

If this latest QE to infinity doesn’t soon deliver the goods in terms of job creation and salary increases (i.e., the “real inflation” we need to be thinking about–not tomatoes and toothpaste), then it doesn’t matter what Bernanke or his successor says to us. It will fail. And the Fed and its policies will become increasingly isolated. And I must mention (again) that QE would have to be significantly bigger than previous injections to get us any real traction in terms of inflation–this QE money is just disappearing into bank reserves (a bottomless pit) never to reach the people or the economy. There’s no inflation in that! That is the crux of the deflationist point of view, from my perspective. Not that QE wasn’t going to happen. Not that QE wasn’t going to blow some bubbles in gold or the markets. But that QE would happen and eventually fail to the point that the people and the bond market force politicians to turn against it. How long until QE fails to that point? That is the tipping point I look for as a deflationist. I am not yet convinced QE will do much more than plug the holes of vanishing credit, simply keeping us in this horrible purgatory of job losses, houses price crashes, and rising grocery store costs. Hardly hyper-inflation. Still a precarious thin sheet of ice between the world and devastating deflation.

So deflationists are doing the opposite of extrapolating current policies and trends into the future. Deflationists instead realize that this current direction is slowing and will reach a logical limit and reverse. The reverse could come incredibly quickly. Time will have run out to prepare. I think it has a limit though.

Ultimately, remember that the point of Bernanke’s QE is to get you to abandon your cash and put into into houses and stocks and anything else. He’s desperate to get you spending. And you’re falling for it hook line and sinker. Maker your money while you can. I don’t know how much longer this run up will last. Nobody does.

Thanks Ilargi for pointing out how gold isn’t doing nearly so well against the Euro and in fact this is as much about a dip in the US dollar than anything else.

Participantpipefit post=5193 wrote: skip said, “I am a commenter here because there are relatively few places to speak intelligibly about deflation.”

Gold only needs a 10% advance from here to take out the all time high dollar price for the yellow metal. The only intelligent comment to make at that point (in a few months) will be ‘I was hopelessly wrong, and pipefit and G. Oxen were right’, lol.

Of course there is free speech in this land, for now, so you will have the option to say something not so intelligent, regurgitated from the broken clocks around here. Why not think for yourself? Are you going to follow them off the dollar collapse cliff, come what may?

Hm, as for thinking for myself, honestly hyperinflations, or at least serious inflationists, definitely are the majority opinion in the collapse blogosphere–or at least they WERE the majority, because I’m seeing a lot of capitulation from the hyperinflationists lately. A lot more talk of imminent deflation.

I’m not saying there isn’t anything valuable in the conversation about what a hyperinflation is, how it would unfold, and what conditions are currently in place to allow for it. But I don’t see how you aren’t just regurgitating the same thing.

There are special merits to gold. Every deflationist worth her/his salt recognizes them. Prechter calls gold the “only real money”. But the fact that gold is climbing in price again does not signal the same thing as hyperinflation. Just because a speculative asset overtakes a high does not change anything. It is one speculative asset. In a true hyperinflation, any asset is worth more than the rejected currency. From that point of view, a hyperinflationist would be wise to diversify and buy everything including gold. So houses, stocks, cars, stamp collections, bicycles. They’d all be worth more than the debauched currency.

So, no, gold hitting another high, if it does so, has no bearing on my belief we’re heading into deflation. Interest rates and money supply, liquidity and credit creation, salaries rocketing up–those would have a bearing on my decision. Gold going up, Apple stock going up, fine art going up–these are assets that taken in isolation do not persuade me one way or the other that we are not in a deflation.

ADDENDUM: by the way, I’ve called for a possible $2500 gold price months ago here in TAE comments. That’s on record. It doesn’t change my point of view about deflation. It’s simply a call about credit-money chasing desperately-needed returns. Returns are needed from somewhere, and as Soros (a recent gold-buyer) has said, money is made from bubbles. He also recognizes that bubbles pop.

ParticipantGO, the tone is totally deteriorating into the toxic. I really value that TAE tends to be one of the few places for intelligent, vitriol free places of online discussion about finance and economics and life! I am happy to accept sharp criticism of ideas with sound arguments. A sharp argument is as good a lesson as a good spanking. No need to get all personal.

My completely unemotional response to your points is that we had massive bank failures in the Great Depression. I don’t see that you’ve offered a reason that the current Greater Depression will be any different.

Participantpipefit post=5189 wrote: skip–You guys should not lean too heavily on Pretcher. Yeah, he’s a deflationist, a perma deflationist at that, so you all love him. But he’s mainly a technical analysis kind of guy, while TAE is mainly fundamental analysis. Pick your poison and stick to, or you’ll get hopelessly muddled.

To clarify, you should really just say “you” rather than “you guys should not lean too heavily on Prechter.” I’m not TAE. I have no official affiliation with TAE, while I do support TAE, because I simply find the insights and writing here to be amongst the most sound in the gawd-forsaken land of the Internet (or the printed press for that matter). A couple of my comments have struck a chord with Ilargi, and he made them bigger topics of conversation. But truthfully, so far, I am a commenter here because there are relatively few places to speak intelligibly about deflation. There are many places to speak unintelligibly about hyper-inflation. And so my “reliance” on Prechter is my own, and I think I’ve only ever seen him referenced by Stoneleigh once within all of her myriad articles with thousands of references.

I personally maintain that Prechter has many incredible insights. I don’t rely on him for the entirety of my life. I don’t rely on anyone to that degree. I suggest reading him and taking the best of his incredible insights. I’ve even disagreed with points on TAE in the past, though my convictions seem to remain very much in alignment with much that I’ve read on here.

I’m not a trader these days, so I don’t rely on technical analysis either. I am persuaded that business is cyclical though. That is just as influenced by Minsky as Prechter. And as such, we’re headed for a doozy of a dip in the next cycle.

ParticipantGolden Oxen post=5187 wrote: Hi Steve, It is a very complex question with many possible outcomes.

My answer as to the deflation scenario you speak of is probably going to startle you, but I have thought about it for quite some time and have to disagree with you

In a deflation, I picture crashing stock markets and corporate bond markets, with everyone selling and placing the proceeds in government bonds and FDIC insured bank deposits for their implicit government guarantee of safety. I realize it is a minority view but it is my opinion nonetheless. Your conclusion of many bank failures in a deflation is in error in my view.

There will of course be many who choose to hold cash, as they will trust no one, but I think they will be a minority, and fear of robbery and such will place a natural limit on hoarding too much cash.

Yikes, that’s a minority view for a reason. It’s just plain impossible.

In a deflationary depression, bank losses become gargantuan, as people can’t pay their loans. The amount of loans that the banks would have to write off would easily dwarf the deposits the citizens could possibly cobble together to put into a savings account. It really begs the question–in this current “early depression” moment of history, people don’t have any money to put on deposit at the bank–why on earth would they have the money once the depression gets going in full swing? Whether the government would print enough to bail out all the bank failures is another question–but that is one addressed quite thoroughly in the writings in the TAE primers regarding the limits of money printing in a deflationary crash.

Alas, SteveB, you fell for Golden Oxen’s hyper-inflationary hyperbole bait. And the discussion of bank deposit insurance is really worthy of a conversation on its own. You’re being a great and generous diplomat today, Steve. All I can say, is there’s a time for diplomacy…and your generosity might not be warranted. He’s just looking for trouble and refuses to address any of the true arguments that underpin TAE’s positions on deflation. A healthy debate is one thing. Repeating the same argument over and over on a deflation blog without ever referencing the deflation blog’s own writing, sources and position is another. I guess that’s what internet trolling is all about.

ParticipantSteveB post=5183 wrote: Also, in arguing for the abolishment of the FDIC he writes the following on p. 85: “Consumers in other countries manage to bank without deposit insurance. Are New Zealanders that much smarter than Americans?” You apparently haven’t caught up with your new compatriots yet, Skip. 🙂

I presume Schiff is suggesting that New Zealanders are doing something especially better than Americans with regard to having no equivalent to the FDIC–since apparently we have a great economy and banking system without it and the Americans should learn from our example.

You know, one thing that is becoming increasingly clear to me: sometimes one’s own, thoughtful, investigative experience on the ground is worth infinitely more than the wisdom of the “greats”. Because the greats can’t be everywhere, and so they have to rely on platitudes and accepted tropes like the rest of us. What I’m getting at is….

New Zealand is headed for a bigger economic collapse than anywhere I’ve lived yet. More so than Canada and the U.S. Schiff isn’t the only one who has lauded the NZ economy or its currency. But nearly three years into my life here, I’m deeply troubled. The life on the ground here is revealing vulnerabilities that the rest of the world seems to be unaware of or ignore. I think NZ is too small to really care about (its population is only 4 million). And yet the similarities with Ireland are quite shocking (also a country with a similar population and similar private debt).

Personally, I’m not looking for New Zealand to be an example of how we do anything right…except that farmers here really do know how to farm, and a lot of people seem closer to that way of life than the U.S. or Canada. Many of my Auckland compatriots grew up butchering a lamb themselves. I can’t say the same for my fellow Torontonians or Los Angelinos!

Anyhow, I disagree with Schiff in this respect. Our lack of FDIC insurance equivalent is NOT an indication we hold our banks to a higher standard–not today anyhow. It is truly because we are more naive and complacent, so the banks don’t even have to bother with the expense of it (because it DOES cost the banks something eh). Kiwi complacency will be our undoing.

ParticipantSteveB post=5178 wrote:

I’m finishing Peter D. Schiff’s The Real Crash, wherein he makes that case. It’s also full of interesting court decision citations regarding Social Security and other arguably unconstitutional US economic/monetary/tax policies and programs. Interesting stuff. (He does have some blind spots–energy being the main one.)

Clearly, the modern insurance policy is a symptom of the greater malaise: we have handed over the personal responsibility for our lives to someone else. Whether it’s our money or the integrity of our house construction or what happens to our garbage or where our water comes from.

Ultimately, I think Schiff is right–deposit insurance has lulled us to sleep and we have let banks get away with murder. Now, we are so comatose NZ banks don’t even need deposit insurance to keep us apathetic. We are complacent enough all on our own now. How perfect for them!

The psychology penetrates deeply in the Kiwi psyche (just as it does in Canada and the U.S. where I’ve also lived). Here in New Zealand, there is a pervasive “culture” of permits for everything. And these permits are EXPENSIVE. In terms of “building permits”, they are sucking the life out of the people and the economy. But shockingly, Kiwis continue to defend the permit system. Because they’ve been convinced that the permits protect us–that without permits your builder will make your house fall down.

It is a complete relinquishing of personal responsibility. We have absolved ourselves of knowing how a house should be built, while we go to work every day and type on a computer. We think we can pay someone else to worry about this for us.

Instead, we must return to a time when we are responsible for our own house. We should know how it’s built, know how it should be built for the particular climate we live in, know the builder we hire because he is our neighbour and part of our community. We have mainly become dependent on insurance policies like this because we have given up responsibility for our own lives.

Similarly, we should understand and take responsibility for what banks do with our money. Insurance cannot replace that responsibility.

Insurance is nothing more than a bet. It’s not a guarantee, and we have to wake up and realize this. In terms of banks, FDIC insurance is currently a bad bet.

ParticipantSteveB post=5178 wrote: What I’m thinking at this point wrt the FDIC fund is that it might get tapped out even before the next crash and never be replenished. (Which raises another question: how is it replenished?) So even fewer deposits might ultimately be insured than the limited amount that Nicole has suggested.

I think you’re right–it seems completely inevitable if the financial system continues to unravel–that leads to too many bank failures for the FDIC to possibly keep up with.

Insurance only seems to work when the claims are spotty. It doesn’t work where the claims are the result of a systemic failure.

An analogy for me is the Christchurch earthquake of 2011–people have insurance on their houses, but it becomes questionable whether insurance can pay out when EVERY house falls down. Many insurance companies have gone bust already, and I expect that there are more to come. I can’t help wondering if they’re already bust, and that’s why so many folks in Christchurch still haven’t received their insurance payouts! Every day that payout doesn’t come is another day closer to the point where no one is paid out.

ParticipantThis is a great topic–I’m glad you raised it.

I think a lot of Canadians are unaware of the fact that the deposit insurance won’t cover many types of Canadian bank accounts, like foreign currency accounts. So if you’re Canadian with US dollars in a US dollar account, you’re probably not covered.

And here in New Zealand, there is NO deposit insurance. In fact, bank employees here in NZ are pretty much unaware of what it is. I had to go through about four bank employees at my bank to find out what sort of government deposit insurance was on their accounts. Turned out finally, when I reached someone who knew what deposit insurance was, that the NZ government only provided temporary deposit insurance during the worst of the post-2008 credit crisis. That insurance has since expired, and the banker told me that “the banks are confident with their AA credit rating” so they don’t need it. Funny, I thought that deposit insurance was supposed to make ME feel confident, not you the banker. And tell me why AA is so great? Canadian banks with deposit insurance are triple-A. (The NZ bank has since been downgraded to AA-).

There have been some great arguments made that deposit insurance lulls us into a false sense of security about our banks’ risk-taking, and therefore deposit insurance should be abolished. It’s a persuasive argument. Except I see the total and utter complacency here in NZ when it comes to banks, and we have not had deposit insurance except for that short window I mentioned.

ParticipantI just mentioned two major market calls Prechter has made. I couldn’t count the hundreds of other calls that may have been right in the intervening years. Anyone making that many calls won’t be right 100% of the time, especially about timing. No one here at TAE is that interested in timing, but rather in the macro view which will have the most impact on anyone who is not a trader. Those two calls made by Prechter are just the most extreme in their degree that they were correct, because the markets themselves were so huge. I’m happy to speak for myself, GO–thanks for allowing me that. As for you: what great insight do you have in published form I can benefit from? Other than your buy gold bitchez posts?

ParticipantNow you’re just being disingenuous, GO. 30 years too early about what? 30 years ago, Prechter became famous for predicting the biggest bull run in stock markets of all time…when everyone said they were finished. He was right. He got rich. And he has more life yet in his insights into how markets work. More insight than you and I have. Certainly more insight than the “buy gold bitchez” crowd.

Prechter was early in predicting a credit crisis. Anyone who lost everything in 2008 would have done well to heed his “early” call.

He also predicted the post-2008 stock market rally. He believes the stock market rally has topped again.

His best advice? “Panic early!” He’s said that, and I agree.

ParticipantGolden Oxen post=5169 wrote: Robert Prechter, You must be joking skipbreakfast. Gold was supposed to be under 200 now, according to that mystic, and we entered a deflationary bust about 1980 according to him and his silly waves. Please come up with someone that has given the correct time of day sometime in the last few decades. Thanks

No one I know yet has a perfect batting average…especially about timing. Prechter admits his timing is bad. Everyone’s timing has been bad, to be honest (except those who continue to follow the status quo and assume everything is fine and will soon be better and bought Apple stock–in fact, by the numbers, their timing has been flawless the past twelve months…but I am not listening to them!).

I don’t think you should discount the brilliant insights of Prechter. At least you do so at your peril.

The fact gold is up is just one of infinite investments one might make. Many other investments are down. Gold can go up or down too. One investment call does not discount the life’s work of a brilliant man. And I expect he will be proven right about gold, even if gold doubles again before it crashes. I’m only interested in playing gold to the extent I can afford to lose a good chunk of the money I’m playing with.

As for Prechter having the “right time of day”–have you read his early predictions of how Fed monetization will play out? In this respect, his writing from circa-2000 sounds like he time-traveled ahead 12 years. If you’re looking for amazing predictions, I find them there in his writing.

Participantpipefit post=5162 wrote: Hi Steve. He addressed my point in a very incomplete way. The ANNUAL federal budget deficit, using GAAP accounting in $5 or $6 TRILLION. Sure, some of that is to create jobs and stimulate the economy. Some for the military industrial complex.

But the vast majority is accounting entries that exist because the government is defaulting on its legal obligations toward the huge entitlement programs. Got that, ‘entitlement’, lol. That means that the American people are ENTITLED to their social security and medicare benefits, and the government is short many trillions, and adding to the shortfall by several more trillion every year.

There is no way in heck that this deflationary. There are two possible outcomes. The obvious one is that the money to pay these REQUIRED benefits is created out of thin air, which is hyper inflationary.

The truth is that there is no more complete way one can answer your critiques in the comments of someone else’s blog. A deflationist blog, I might add. In fact, the strongest arguments against your points are all thoroughly covered in Stoneleigh’s and Ilargi’s lengthy, rock-solid essays now archived in the Primers. The reason I like to participate vocally in TAE’s comments is that these writings influenced my thinking a lot, and led me to research the thoughts of other deflationists (as well as hyper-inflationists).

It has been a “long road” since the 2008 credit crisis. The irony, however, is that I see the deflationists’ predictions playing out extremely faithfully, while the calls for hyper-inflation have simply not materialized in any respect. One to 3% consumer price inflation is NOT hyper-inflation. An expanded government debt is not hyper-inflation (even if it’s a bad thing)–especially given that safe-haven interest rates are at all-time historical bottoms. That is the OPPOSITE of a hyper-inflation.

I’m looking at the best arguments and the best evidence. I don’t discount a hyper-inflation in the future. But our deflation hasn’t even gotten fully rolling yet, so that is my primary concern. When most peoples’ wealth is still tied up with houses and stocks, it is the most critical message I personally want to get out there. Not to mention the fact that people will have a lot of trouble making ends meet when jobs vanish increasingly fast, and investments vanish too. I’d want to have cash. Hyper-inflation is a dangerous all-in bet that could result in more than financial disaster for the average person who tries to protect herself with speculative assets, all of which do go down in the worst of a deflation.

So, again. I can’t convince you pipefit. I’m not trying to actually–if Stoneleigh hasn’t convinced you to open your mind to the possibility of deflation, after you have read and posted on TAE the past months (years?), what hope do I have. I’m trying to provide some alternative perspective to anyone ELSE reading your comments, so they maybe stop to think to explore the possibility there will probably be a different kind of financial disaster awaiting us. Too much of what the deflationist perspective has warned us of is coming to pass. just look at the increasing difficulty that the Fed has in coming up with their QE-Anything, something many deflationists predicted would happen long before they managed to print us into oblivion.

Here are just a few of the primers from Stoneleigh and Ilargi. I also encourage you to read Robert Prechter’s work. If they can’t convince you, then I certainly cannot, and I shouldn’t really bother trying when i can just refer you to their superior writings and work.

https://theautomaticearth.com/Finance/dollar-denominated-debt-deflation.html

https://theautomaticearth.com/Finance/debunking-gonzalo-lira-and-hyperinflation.html

https://theautomaticearth.com/Finance/the-rise-and-fall-of-trade.html

https://theautomaticearth.com/Finance/the-infinite-elasticity-of-credit.html

https://theautomaticearth.com/Finance/a-future-discounted.html

https://theautomaticearth.com/Lifeboat/our-daily-bread-or-not-as-the-case-may-be.html

Cheers!

Skip

Participantpipefit post=5142 wrote: Hi Skip,

I have quite a few problems with your post. Let’s start with this line from you: “Hyper-inflations are triggered by collapsed economies that throw in the towel on the people in an effort to repay debts in a currency which the world has rejected.”

A big part of your argument is that we’re close to deflation because the economy is collapsing. But in the quoted line above, you admit that the exact same thing can lead to hyper inflation. This is why the deflation argument is so weak.

Not exactly. You’re taking only one part of the quoted sentence, and leaving out the key part which is “in a currency which the world has rejected.” You don’t have a hyper-inflation unless world rejects the currency in question. No matter what the economy is doing. A slowing economy is by its nature deflationary. So, no I don’t see how I admit that an economy collapsing is the same thing as hyper-inflation. I believe the opposite: a deflation is the result of a collapsing economy. A hyper-inflation is the result of a political decision of a government to throw in the towel on the currency, leading to worldwide rejection. Our governments are not throwing in the towel on the currency, as is evidenced by treasury rates and flights to safety. You can argue they’re playing with fire, and the bond market could lose faith in the system’s ability to play this game. But so far, we do not see an indication of that. And as all the sources I quote above emphasize, we are actually seeing indications of deflation (a hoarding of currency, etc.) not hyperinflation.

The key part to a deflation is falling money supply and declining velocity of money. There are too many indications that both money supply in the real economy is falling and slowing.

pipefit post=5142 wrote: As long as the economy is doing fair, and we keep buying junk from our creditors, there is no reason for them to reject the dollar. Its a rickety situation whenever vendor financing is in play, be it at the corporate or national level, but it works until it doesn’t. When it quits working, we’re gonna pay our debts in a devalued currency, or default and lose reserve currency status, which will have the same effect as hyper inflation.

Yes, possibly we will eventually have to print to pay our debts one day. There is no indication yet that we are about to do that. In today’s case, Deflation (due to overwhelming economic reality) precedes a hyper-inflation (due to a last-gasp political decision to throw in the towel on the government, the country, the people, the economy and the world). Given that deflation is the imminent threat, you have to survive a devastating deflation before you can survive the possible hyper-inflation in the future.

pipefit post=5142 wrote: You go on to say “Again, “the prices of things” don’t even tell us anything definitive about whether we’re in a deflation or inflation,…”.

They tell us absolutely nothing? That’s absurd, to use your favorite word, ha ha. If we were in deflation, EVENTUALLY this would manifest itself in the form of lower consumer prices. But, low and behold, five and half years into this credit bust, consumer prices are still rising.I didn’t say they tell us nothing. I said “they don’t tell us anything DEFINITIVE.” That’s a big distinction, pipefit! Too many people do what you’re doing and use basic cost of living prices as a DEFINITIVE indication (ie., air-tight PROOF) of an imminent hyper-inflation. That is absurd. I don’t expect you actually read my long arguments in this regard. Here’s the gist:

I think it’s still important to continually reflect upon the TAE perspective on inflation/deflation. Because the rise in basic costs of living can be a distraction from the much bigger problems we’re about to face. Yes, the problems heading our way are bigger (for most of us in the developed world) than whether tomatoes or toothpaste went up in price this year.

I don’t want to dismiss the impact of rising grocery prices on people’s lives, which especially impacts the poor. When you’re starving, no other issue is more pressing. Nevertheless, a lot of people cite rising grocery costs as proof of monetary inflation (i.e., expanding money supply) with the implication that we are heading towards an inflationary collapse. This is a red-herring. And it’s a dangerous one. Because it tricks us into making the WRONG preparations for what is coming–and what is coming is a deflationary collapse.

For the poor, rising food prices (triggered by many things, like drought, and not necessarily money supply) devastate their lives. It’s unsustainable and leads to riots and malnutrition and worse. However, for anyone who earns or has amassed enough money to pay for food with any money left over, the rising grocery costs factor less and less into your financial equation. For example, tomatoes may rise in price costing you another $100 per year. But if you’re also shopping for a house, the cost of that house is dropping in most places much more than $100 per year. Similarly, prices of things like cars, travel, computers, clothing and services like plumbers and dentists are dropping faster. And these price drops are like dominoes falling throughout our society, as they trigger job losses, business failures, abandonment of infrastructural improvements–basically society breaks down if it goes broke, and when business fails and there are no tax revenues to collect from the people, we’re broke.

pipefit post=5142 wrote: “Despite the repeated calls for hyper-inflation, it has not happened.”

O.k., I’ll admit I should have chosen my words a little more carefully. We’re not in hyper inflation YET, of course, but well on the way.Look at it this way. Using GAAP accounting, the federal govt. is running a deficit of $6 trillion per YEAR. That’s almost 40% of GDP. It is only going to go higher. How high does it have to go before you’ll admit defeat for your ‘deflation’ prayers? 100% of GDP. 300%? There must be some line where you will admit you are wrong, lol.

Read the sources above. The quantitative easing and debt accumulation is a fraction of what it would need to be to make up for the trillions in vanishing credit-money. Debt write-offs is an indication of vanishing money. I don’t think any government can come up with enough quantitative easing to stem the tide of trillions of defaulted debts. This doesn’t serve the government or the richest interests in our society.

I’ll admit that I’m wrong if it turns out I’m wrong. But I don’t take the increase of some prices as the reason to do so, since no TAE deflationist has ever said SOME prices rising/falling is the definition or the true implication of an inflation versus deflation. The implications of money supply have to be accounted for in a much more complete way, and not just by examining YOUR prices in your daily life shopping for mac and cheese. Ironically, given where we are at in 2012, it is the hyper-inflationists who should concede they might be wrong. Time will tell. At least hedge your bets given the evidence is mounting against the hyper-inflationists all the time.

Participantpipefit post=5139 wrote: For one thing, he seems to be stuck in the same box as everyone else in terms of dollar devaluation. None of the major currencies can devalue against each other, for the reasons given by Duncan, but they can all be devalued simultaneously against gold/silver.

In fact, this devaluation is well under way. This is why gasoline, food, health care, and just about everything else is up, in dollar terms, so much. As with most other bubbles, this one will be unwound in a hyper inflationary orgy of money printing.

Appreciate you chiming in on the Duncan interview.

Of course, I seriously disagree with your hyper-inflation call. There is simply so much evidence to the contrary.

Grocery prices increasing even 10% do NOT indicate a hyper-inflation. That’s absurd. Not when major assets around the world are droppping in price by double and triple that amount. For more on why such a hyper-inflationary call is absurd, check out Mike Shedlock’s cogent analysis:

“Every time the US dollar ticks lower, commodity prices tick higher, or the CPI rises two tenths of a percent, hyperinflationists come out of the woodwork with nonsensical predictions and silly comparisons to Zimbabwe or Weimar Germany.”

Again, “the prices of things” don’t even tell us anything definitive about whether we’re in a deflation or inflation, and can be dangerous red-herrings that keep us from making the necessary preparations. I made a lengthy argument in this regard in the TAE comments recently.

It’s important to keep in mind that hyper-inflations are not triggered by efforts to stimulate economic recovery and create jobs, the way Bernanke is attempting to do. Hyper-inflations are triggered by collapsed economies that throw in the towel on the people in an effort to repay debts in a currency which the world has rejected. We are not in that scenario. Not yet–not even close–in at least this respect: the world is clearly NOT rejecting US dollars or Swiss francs or even “German euros” when you look at interest rates and currency buying activity. The big players are finding security WITHIN currencies, not outside of them.

Despite the repeated calls for hyper-inflation, it has not happened. Rather we just get increasing evidence that the money supply is illiquid and DEFLATING. Despite being lone voices in the wilderness, pretty much everything that TAE has called for is happening before our eyes (if on a painfully protracted timeframe). By all measures, we’re in a deflation or teetering precariously close.

When you’re hungry, you want dollars so you can eat. When you’re broke, you want dollars so you can pay your rent. When you see an opportunity, you want dollars so you can buy into that opportunity. Gold is just a means to try to get more dollars. The day when you buy groceries with your gold is a long way off yet.

At least look at current indications as a guide. In what respect has gold begun to replace our confidence in currency besides the price going up. The price of Apple stock has gone up too. I do not take that as any indication that we have lost faith in currency and will soon be buying our groceries with Apple stock. Gold is unique in its ability to always retain some value no matter how low it goes. Gold can still go up in price, as a speculative bet. But it is not yet indicating a hyper-inflation at all, because when I see dollars flashed in front of a person, they want those dollars badly. Try spending your gold at Tesco. They would think you were a loon. You need a specialized gold broker to trade your gold for dollars, and it costs you money every time you do that. What’s it going to cost you to trade your gold for dollars if those brokers go out of business and vanish? Who will trade you dollars for gold to pay for your groceries then?

Despite the money printing over the past few years, all we see is that it has failed to stimulate the economy in a meaningful way. As Ponzi World writeswith regard to (possibly) imminent QE3:

“…if the Federal Government is going to continue running $1.3 trillion dollar deficits (aka. new bond issuance), then Fed monetization programs equal to that amount are not stimulative, they simply prevent new bonds being issued into the private market. Any amount of monetization less than the deficit would in fact be contractionary, as new bonds will enter the private market and “crowd out” other investments.”

And also from Zero Hedge’s article The Fed Is Not Printing Enough Money:

“…the amounts needed for the Fed to be able to create inflation are much, much higher than what we have seen so far. And it is not guaranteed to work.”

Indeed, our jobs are vanishing as is made clear by the recent jobs report. And remember this, from John Rubino:

“The real driver of inflation is labor costs, how much people are making,” LPL Financial’s Valeri said. “Salaries aren’t increasing much at all.” Valeri said he favors intermediate-maturity corporate bonds because “interest rates are going to stay low for a while.”

There is a distinction between “inflation” and “hyper-inflation”. They’re not even necessarily related phenomena, and it’s unfortunate they both contain the same root-word. One is primarily an economic force (dictated by the velocity of money). One is a political force (i.e., a final socio-political collapse).