Spain Has A Long Way To Go Down

Home › Forums › The Automatic Earth Forum › Spain Has A Long Way To Go Down

- This topic is empty.

-

AuthorPosts

-

March 4, 2013 at 11:59 am #8396

Raúl Ilargi Meijer

KeymasterIlargi: I received another entry from Dave Fairtex, who delves into Spanish housing data this time around. We had a nice discussion about it, since I

[See the full post at: Spain Has A Long Way To Go Down]March 4, 2013 at 7:43 pm #7025p01

ParticipantDebt forgiveness may allow big numbers on paper to return to pre-bubble levels, and that’s about all it can achieve. Return to “normal” is not possible, unless you consider Franco’s era or the Spanish inquisition as “normal”.

March 4, 2013 at 10:01 pm #7026davefairtex

ParticipantOne of the clear takeaways from the bubble pop in Spain, Ireland, and the US, is that most underwater homeowners continue to pay on their properties, if they can. The Central Bank of Ireland noted that 93% of their underwater homeowners were still making payments, even with the massive price drops. People have that emotional/irrational attachment to where they live. I believe that factor, more than anything else, will cushion the bottom with respect to residential real estate prices during this bubble pop.

You can see this in the deflation curves for the different sectors. Loans to homeowners are deflating slowly, while loans to corporations and banks are deflating rapidly. The latter dump their underwater mal-investments relatively quickly, while the former hold on for as long as they possibly can.

Ilargi said, “If Spain were to recognize the full 55% price drop, that would be the end of a large part of its banking system. And that in turn, for instance, would drive prices further down.”

That’s a possible outcome, but not a required outcome. By plowing in huge amounts of cash and taking the really bad assets off the hands of the bankers, Ireland appears to have effectively stopped that from happening, keeping its banking system afloat. Half of the rescue money in Ireland went to capital infusions directly into Ireland’s banks – their version of TARP. Their taxpayer saved their banking system (today it is mostly government-owned) and if current trends continue they will end up with a 55% drop in home prices.

If the US had done a TARP of a similar size, it would have been 6,352 billion dollars – ten times the size of the actual US TARP. And this is actual cash money dropped into the banks in Ireland. And there were no GM bailouts, no GE bailouts. Just the six banks. It was a very expensive operation.

Sweden executed a similar type of rescue (bad bank, capital infusions) in 1991, and they managed to avoid that outcome.

Perhaps most interestingly, during the 1929-1933 Depression, US home prices (when adjusted for in/deflation) actually were more or less flat. The only explanation for that is, the 20s weren’t caused by a housing bubble. But the point there is, even during a deflationary depression where cash was a scarce item and thousands of banks really did collapse, housing prices maintained their value in real terms. The last thing people want to lose is their home.

https://en.wikipedia.org/wiki/File:Case-Shiller_data_from_1890_to_2012.png

As Ilargi quoted me before, Houses are not Tulips. I should make a bumper sticker or something.

March 4, 2013 at 11:50 pm #7027jal

Participant“… the solutions that our leaders will present to us will involve even more debt and even more money printing. And each time, those “solutions” will only make our problems even worse. Right now, events are unfolding in Europe and in the United States that are pushing us toward the next major crisis moment. I sincerely hope that we have some more time before the next crisis overwhelms us, but as you will see, time is rapidly running out.

The following are 12 things that just happened that show the next wave of the economic collapse is almost here…Sadly, most people will continue to deny that anything is wrong until it is far too late.

Many areas of Europe are already experiencing economic depression, and it is only a matter of time before the U.S. follows suit.

Time is running out, and I hope that you are getting ready.

So what do you think?

How much time do you believe that we have left before the next wave of the economic collapse strikes?”The Canadian [strike]bank[/strike] band is still playing music as the ship is sinking.

There are not enough life jackets for everyone.Will putting on a life jacket really help to save your life?

https://www.ctvnews.ca/business/bmo-lowers-five-year-fixed-mortgage-rate-1.1179702

The Canadian Press

Published Sunday, Mar. 3, 2013 2:32PM ESTBMO lowers five-year fixed mortgage rate

TORONTO – The Bank of Montreal is lowering its rate for a five year fixed mortgage amid concerns about a cooling housing market.

Effective immediately the rate will drop to 2.99 per cent from the current 3.09 per cent.

The other big banks could follow suit.March 5, 2013 at 1:17 am #7028Participant@Ilargi

Of course it’s textbook tulips 😆

https://en.wikipedia.org/wiki/Spanish_property_bubbleThe housing burst can be clearly divided in three periods: 1985-1991, in which the price nearly tripled, 1992-1996, in which the price remained somewhat stable, and 1996-2008, in which prices grew astonishingly again

March 5, 2013 at 2:09 am #7029Anonymous

GuestAlthough some points in the article may be fair, there is one which is just ridiculous: you say that many of the houses built in Spain these last years were of too poor quality to last more than 20 years. I have lived in Spain many years but I live for the last few years in Amsterdam. Most of the houses built in Spain in this period were of good quality and at least as good as what I find in Amsterdam. I am not saying there is no exception, specially towards the top of the bubble when things may have been rushed a bit, but in general they are good quality. So please don´t make things up.

Secondly, since the beginning of the boom there has been around 30% inflation in Spain. So, we would not necessarily expect prices to fall to the nominal pre-boom year prices. They might due to the intensity of the crisis, but this would be overshooting the necessary correction.

Third, one explanation for the increase in housing prices during the last 2 decades has been the significant decrease in interest rates in Spain, as a result of joining the Euro.

As an example, I bought in 2003 an apartment in a new development in Madrid, which I currently rent out. The nominal price now in 2013 is below the 2003 price. So, market prices have already decreased significantly, more than what I think you suggest. I don´t think an additional 33% decrease is required to reach the bottom. However I do think prices will decrease further in the next or two, due to the severity of the crisis. But by then they will be undervalued, which is different than saying that they will have finished their market corrections.

Regarding the banking system, I believe the German banks are hiding more than the Spanish banks. I would suggest the author investigates the German Landesbanken, if he is able to find data, which the German government probably does its best to hide. Spain has been a lot more transparent with its banking balances than Germany has.

Finally, I would also suggest to the author to not rely too much on one single source in Spain. People in Spain tend to exaggerate things a lot: one day they think Spain is the best country in the world and the next they think it is the worst. Usually it is something in between, both in the good times and the bad. Because of the crisis they are now in their negative phase and they tend to make things look worse than they really are (some things are bad or very bad, but not everything). This applies also to corruption. While it does exist I don´t believe it is extended as the media would make us believe. In the many years I have lived in Spain I have never actually experienced any sort of corruption in my daily or business life. I´m sure it exits, but many people live their lives in Spain without corruption.

March 5, 2013 at 3:39 am #7030skipbreakfast

ParticipantI trust most of you have just seen this haunting ’60-Minutes’ story on the China housing bubble, depicting entire cities full of shining but unoccupied skyscrapers and thousands more unfinished towers. It underlines something that I have noticed in my home country of New Zealand, where real estate speculation has been long elevated to its own truly twisted state of manic speculative fervour: some houses are worth $0. That’s not a typo. That is zero dollars.

Yes, when speculation reaches a certain point of mania, I can assure you people pay a lot of money for properties that are simply unfit for occupation or development. In the mania, folks are convinced that anything, as long as its some land they can call their own, will guarantee them future profits in a world where “god ain’t making any more land”. The truth, however, is that god made a lot of lands that, in more rational times, are simply forsaken for very good reason–they are worth $0 because they offer nothing a rational businessman or homeowner wants or needs. There is nothing unique about them (in the case of towering apartment buildings). Or you can’t sensibly build on them, grow on them, or even practically LIVE on them.

Where I currently reside, in New Zealand, speculative investors have talked themselves into buying south-facing cliff-faces at the height of a mania (remember south-facing, when your Antipodean is NOT a good thing–it’s bloody cold). There are A LOT of such properties, purchased with dreamy intentions of development, only to be abandoned after the first attempt to put in a frightening ski-slope driveway. Now that the mania is beginning to subside (though that is a relative term for this completely insane housing devotion here in Aotearoa), people are trying to unload these cliff properties. But to everyone’s surprise, there are no takers. Yup, some properties are worth $0. A rational man wouldn’t want to pay the property tax on the thing even if it was given to him for free.

And when you see the Chinese property video above, you realize this is a feature of every property mania. There are such great distortions in such markets that a sizeable percentage of the market is actually going to be unwanted and utterly rejected by any prospective buyer in the future, no matter what the price. Just think of the phenomenon of the “ghost town”, something we will begin see a lot more of over the next decade.

So, in a saner market, almost all property has SOME real value. But in these extremely distorted times, that is simply no longer the case. Good property will continue to be good property, but will still drop precipitously due to the pressures of a credit implosion. Meanwhile bad or useless property will be recognized as just that. This will absolutely, without a doubt push “average” property prices BELOW the long-term mean for some period of time. At least until the value-less properties are recognised as such and expunged from the marketplace in the big write-offs that are yet to come.

March 5, 2013 at 6:19 am #7032Nassim

ParticipantMark,

I fully sympathise with you. You would have clearly done very well had you sold your Spanish property a while back.

I also agree that property quality in Spain – on modern properties – is no different from elsewhere. Older buildings in good parts of Madrid are very similar to Parisian properties from that age and are of a superior quality to London properties from a similar epoch. Furthermore, the benign climate keeps things together for much longer than in places like Ireland and the Netherlands.

My first encounter with Spanish property speculation was back in 1964. I had a schoolmate whose dad was building holiday homes in Spain. He must have become very wealthy as his timing was impeccable, or maybe too early. My parents lived in Spain 1965-70 and they considered property expensive at that time. They could have bought a villa in a place like Sitges for what was almost pocket money to them at that time. It just goes to show how difficult it is to tell what is really going on when one is actually in it. A little distance gives better perspective, IMHO.

I personally think that property prices pretty well everywhere are going to go down to what people can pay cash for. That is the way it was historically and it is obvious that the banks are all going to be put through the wringer and hung out to dry – eventually.

March 5, 2013 at 12:24 pm #7033Participant

March 5, 2013 at 12:24 pm #7033ParticipantMark –

Great to hear from someone on the ground who actually owns property in Spain! I read about it, and use data provided by the Spanish government, but you actually are living it.

Corruption in Spain: since I don’t live there, I can’t judge for myself; I refer you to the Corruption Perceptions Index. Spain’s rating: 65, Ireland’s rating: 69. I was making this relative comparison only to make the case that Spain may well continue to overpay for bad loans more egregiously than the Irish – who also overpaid for their bad loans. This will make the bailout more expensive than it needs to be.

My sense is that property prices will continue to decline in Spain. I’m looking at this using overall country numbers, but real estate is always local so situations can vary a great deal. As skipbreakfast pointed out, there are probably homes built in what turn out to be pretty undesirable locations that are only revealed once the madness has ebbed.

I base my sense on the amount of bad bank loans that still need to be marked down. Given the size of the bubble, there hasn’t been enough “pop” in the banking industry. That’s because the banks have held properties off the market deliberately, to avoid taking losses that would end up bringing down the bank. Once all the bank rescue money is available, the sale of these properties will likely lower prices further. The only question is, how much further will that be?

If you are telling me that prices have already dropped to 2002 levels, that (paradoxically) makes me think my case is too optimistic, much as Ilargi has said. My gut feeling based on just how much unacknowledged deflation (unresolved nonperforming loans) is waiting on bank balance sheets says there is a lot of work still left to be done. Ireland’s prices have dropped back to 2000-2001 levels and it has plateaued for a year now. To get that to happen, they basically gifted 143 billion euros to their banking system in 2009-2010. Spain has done basically nothing – Spain spent 2009-2011 largely in regulatory denial; only in the last year has any progress been made.

I realize this is not what anyone who owns property in Spain wants to hear, but given Spain’s limited progress, and where you say prices are, is entirely possible that my scenario of the bubble pop stopping at 2002 prices is too optimistic.

Instead of saying how much further as a percentage property prices will drop (given the lies in the government statistics) I should use years instead. If you say prices are at 2002 levels now, given how much workout remains ahead, I’d say there are 3 scenarios:

1) 2000 (60%) – assuming a real resolution occurs in 2013 that successfully arrests the GDP drop and cleans up the bad debt in the banking system.

2) 1997 (30%) – assuming Rajoy takes his time negotiating with the ECB, people in power tell the truth slowly about the costs, all the while GDP continues dropping, and unemployment rises; full cleanup takes 3 years.

3) ???? (10%) – Spain leaves the eurozone, goes back to the Peseta, and prints money to solve the problem; possibly civil war or authoritarian government results in property prices becoming true bargains based largely on the Peseta’s 3:1 (?) exchange rate to the euro.Where will property prices will eventually end up? I think that depends on the scenario. At some point, when things become stable again in Spain, all the Spanish deposit money hiding outside the country will rush back in and buy up properties that have become true bargains. But that will await stability. Without stability in expectation, money will remain hidden.

Likewise, GDP and unemployment will likely not recover until a higher degree of certainty returns to Spain. Who in their right minds would take their savings (that is likely hiding out in Germany anyway) and start a business until this mess gets sorted out?

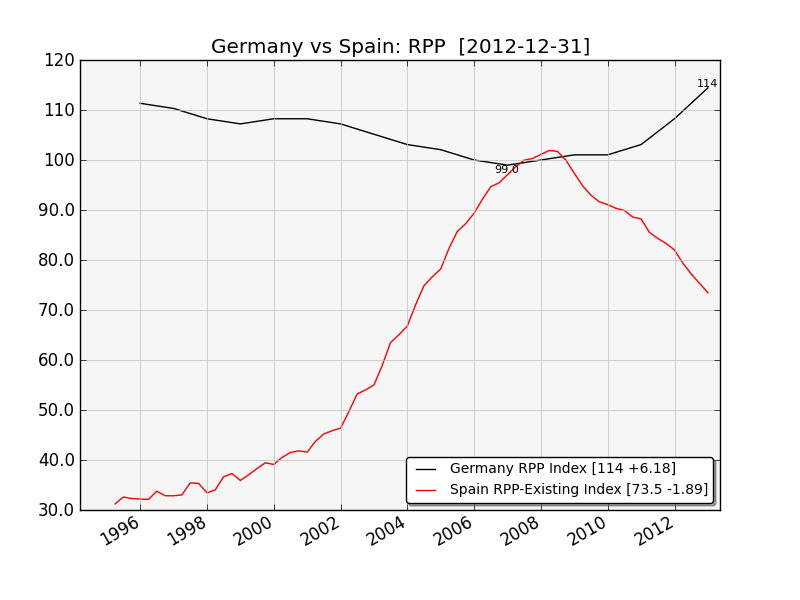

As for Germany, they didn’t have a property bubble. Perhaps their landesbanken are broke (I haven’t looked) but its not as a result of unsustainable property price growth. Here’s a comparison chart:

March 5, 2013 at 5:23 pm #7034

March 5, 2013 at 5:23 pm #7034gurusid

ParticipantHi Skip,

The same goes for the UK:

Where in some places you can’t sell property at all.Going forward there is likely to be an increase in this very ‘localised’ type of situation, especially as benefits are cut, and work remains non-existent.

The same for the US, Canada, and the UK, only here we turn it into a business…

L,

Sid.March 5, 2013 at 5:36 pm #7035ParticipantHi Dave,

Interesting point about the stage of pay down/bailout of Irish debt (posted here about it yesterday), especially in the commercial sector, that further explains why they have cancelled the ‘state guarantee’ for deposits over €100,000:

Ireland to remove bank deposit guarantee from end-March

DUBLIN (Reuters) – Ireland (OTC BB: IRLD – news) will remove a state guarantee on bank deposits next month to help ease pressure on loss-making lenders and move the country further towards exiting its EU/IMF bailout, finance minister Michael Noonan said.Ireland’s almost fully state-owned banks, whose rescue cost the equivalent of 40 percent of annual economic output, have had widening losses partly because of fees they had to pay for the guarantee, and they have been clamouring for its removal for months.

…

The removal of the guarantee will not impact the vast majority of bank customers because deposits over 100,000 euros are covered by a separate guarantee which has been in operation in Ireland since 1995.The Eligible Liabilities Guarantee (ELG) scheme guaranteed deposits over 100,000 euros in case banks got into trouble. Lenders had to pay a fee to the government for the guarantee, which cost the country’s three remaining domestic banks 1.1 billion euros last year.

And it also points to a ‘get it while you can’ attitude on mortgage repayments:

Trackers don’t track and fixes move: The truth about mortgage deals

The Bank of Ireland is about to increase the cost of its tracker mortgages, despite the base rate not increasing, but is your mortgage rate safe?

Thousands of Bank of Ireland mortgage customers are to be hit with higher repayment costs on their tracker mortgages, whether the Bank of England Base rate changes or not.The lender has announced rate hikes to take effect from May, seeing rates for 13,500 customers on base rate tracker deals double.

The changes mean that a buy-to-let mortgage customer on a typical interest rate of 2.25% will see their rate climb to 4.99% from May 1.

Residential customers will see increases introduced in two stages: 2.49% plus base rate will take effect from May 1, changing again to base rate plus 3.99% on October 1, jumping to an overall rate of 4.49% if the base rate stays at 0.5%.

That is they seek to reap as much flesh from the loans before they are paid off or defaulted upon, though the rate rise might prove very counter productive if many start to default earlier on those mortgages…

L,

Sid.March 5, 2013 at 7:51 pm #7036pipefit

ParticipantI enjoyed reading the article. In the preface, Ilargi notes that modern man, including Spaniards, occupy more sq.ft. per person than in prior decades, and therefore, were this to contract, you would have a lot farther to go down, in price per sq.ft.

Along the same line, if you compare the population of Spain to that of the rest of the world where Spanish is either the primary or secondary language, I think you will see that 10%, or even 50% of the population of Spain could easily be absorbed. Particularly the USA, where Spanish is practically an official language and no visa is required for entry, for EU inhabitants.

I don’t believe the exodus from Spain is as great as from Portugal or Ireland, yet. Unlike most of northern europe, southern europe residents, particularly Iberians, have a vast continent, actually two continents, that can absorb them should they decide to leave.

Once you get into this situation (mass exodus) you are really getting to be exactly like Japan, which is currently experiencing population loss, though due to low birth rate there. Regardless, a contracting population is deflationary, since you have less economic activity.

March 5, 2013 at 11:06 pm #7037Participanthttps://www.zerohedge.com/news/2013-03-05/last-time-dow-was-here

The Last Time The Dow Was Here…Dow Jones Industrial Average: Then 14164.5; Now 14164.5

Regular Gas Price: Then $2.75; Now $3.73

GDP Growth: Then +2.5%; Now +1.6%

Americans Unemployed (in Labor Force): Then 6.7 million; Now 13.2 million

Americans On Food Stamps: Then 26.9 million; Now 47.69 million

Size of Fed’s Balance Sheet: Then $0.89 trillion; Now $3.01 trillion

US Debt as a Percentage of GDP: Then ~38%; Now 74.2%

US Deficit (LTM): Then $97 billion; Now $975.6 billion

Total US Debt Oustanding: Then $9.008 trillion; Now $16.43 trillion

US Household Debt: Then $13.5 trillion; Now 12.87 trillion

Labor Force Particpation Rate: Then 65.8%; Now 63.6%

Consumer Confidence: Then 99.5; Now 69.6

S&P Rating of the US: Then AAA; Now AA+

VIX: Then 17.5%; Now 14%

10 Year Treasury Yield: Then 4.64%; Now 1.89%

EURUSD: Then 1.4145; Now 1.3050

Gold: Then $748; Now $1583

NYSE Average LTM Volume (per day): Then 1.3 billion shares; Now 545 million sharesMarch 6, 2013 at 10:46 am #7038Participantpipefit,

The fertility (babies per woman) in Japan is 1.27 while it is (drumbeat) 1.41 in Spain. Not a huge difference when 2.2 is the natural replacement rate.

https://en.wikipedia.org/wiki/List_of_sovereign_states_and_dependent_territories_by_fertility_rate

March 6, 2013 at 11:50 am #7039Golden Oxen

Participant@reply jal, Facts have no place in the financial world of today my friend. We deal in perceptions, Fed policy statements, and statistics massaged to fit the current fable. There is also technical analysis to consider, as well as the actions of the PPT, and the pool operations of the banksters and hedge funds.

There is always someone like you trying to ruin a speculative orgy with factual data, and it goes against the spirit and intoxicating mood of a grand bash. Lighten up, drink some punch, and join in the festivities; all your worries will just vanish. The Fed has promised to keep the booze flowing until all is well, so the fun is just beginning.

March 6, 2013 at 7:55 pm #7040ParticipantThanks for the link, Nassim. I see that the only countries with even lower fertility rates are other European States, with very few exceptions. This is a natural consequence of following deflationary policies. There’s no hope for the future, so why have kids.

So with such a low fertility rate, once emigration gets going, population is going to tank hard, and the remnants of the economy tank harder.

March 6, 2013 at 10:17 pm #7041ParticipantRe.: factual data

Central banks have never cared about anyhing except their well being. Meaning … the well being of those having and controlling the assets and wealth.

It has always been so.

Somehow, the rich still need ordinary people to make babies to serve the few.

All my worries have been for nothing.

March 7, 2013 at 2:31 am #7042ParticipantPipefit,

It has always been my contention that when women have few babies – let’s face it, they make the decision – it is a sign of declining expectations. The fact that this decline – in native European women – has been so great over the past few decades is highly significant, IMHO.

In the UK, the fertility of native-born women is significantly less than that of other women (1.89 versus 2.28)

Dramatic differences can be found between Polish women in Poland and those who have moved to the UK – 1.23 versus 2.48

https://www.dailymail.co.uk/news/article-1366063/Polish-population-growing-faster-UK-Poland.html

Personally, I think the rich should be encouraged to have more kids. The current system tries, inadvertently, to encourage the poor to have more. They should also be encouraged to marry the not-so-rich. I mean, the big landowners in the UK only hung onto these phenomenal properties by giving it all to their first-born son and by only marrying others in a similar situation. That very limited gene pool has resulted in some of them looking like equines.

https://au.answers.yahoo.com/question/index?qid=20120721090756AAdSjt0

March 7, 2013 at 3:41 am #7043ParticipantNassim,

Also, not having kids makes 20 somethings more mobile, as in my point about emmigration. I haven’t see that much about Spain, but neighboring Portugal is seeing a brain drain of their smartest, best educated youth.

About a year ago I read a Zero Hedge article about them going to Brazil. However, more recently I have seen articles about them going to former Portuguese colonies Angola and Mozambique. Also, a lot of them are low wage alternatives for Swiss corporations. If you have no job prospects at all, those backwater places might not seem that farfetched, especially if you have a good education you can use in an under educated 3rd world place where you speak the language of the elite class. And Switzerland must seem like Disneyland!!

So what class of people will be left behind in the PIIGS? The under educated, lazy, or otherwise unemployable, but hungary folk that need handouts to survive. Quite frankly, I don’t see the upside to ‘austerity’, but I’m not a banker, so what do I know, lol.

March 7, 2013 at 7:48 am #7045ParticipantHi folks,

Pipefit:

So with such a low fertility rate, once emigration gets going, population is going to tank hard, and the remnants of the economy tank harder.

In the UK net immigration is boosting population as this report by Rosamund McDougall, Co-chair of the Optimum Population Trust 2002-2005 and joint Policy Director 2006-2009:

Britons are marrying later in life, having children later in life, and dying later too – affecting the number of deaths each year. With expected increasing life expectancy, boys born in 2005-7 could expect to live to the age of 88.1 years and girls

to 91.5 years. Men aged 65 in 2004-6 could expect to live another 16.9 years and women 19.9 years, which contributes to the Ageing of the UK population. Births have exceeded deaths every year since 1901, except in 1976. But uncomfortable though it has been to say so, the main cause of UK population growth remains high net inward migration flows and the effects of this on the number of births. “Of the 5.6 million natural increase projected between 2008 and 2033,” reported the ONS in its 2008-based Population Projections, “only 3.3 million would occur if net migration were zero (at each and every age)…Thus just over two-thirds of the projected increase in the population over the period 2008 to 2033 is either directly or indirectly due to migration.” Of this, 45 per cent is directly attributable and 23 per cent indirectly.Annual population growth has quadrupled since the 1970s. Continued growth at the officially projected rate would involve adding a population of nearly 10 million – more than London’s – to the UK by 2033, with all its needs for additional housing,

energy and power supplies, reservoirs, schools, hospitals, transport, shops, waste disposal, prisons – and all its impacts in the form of waste and emissions. Those who argue for population growth will not answer the question of what they think is an environmentally sustainable level, nor at what level they believe growth should stop. Our numbers cannot grow for ever.Also Nassim:

It has always been my contention that when women have few babies – let’s face it, they make the decision – it is a sign of declining expectations. The fact that this decline – in native European women – has been so great over the past few decades is highly significant, IMHO.

In the UK, the fertility of native-born women is significantly less than that of other women (1.89 versus 2.28)

Women only have that choice when the culture allows it, and also where they are educated and have control over their lives. While the social support for having children has been blamed for the high level of teenage unmarried mothers for instance (recent data shows a decline), there are many other factors such as social deprivation/isolation, peer pressure, male sexual dominance in those communities and low levels of education (education that has excluded and dumbed them down). Also the religious/cultural is probably still the biggest influence; the secularity of ‘western women’ means they have access to contraception, which combined with education and sexual equality suggests that they have the most choice over having children. While Catholicism still preaches abstinence from contraception, their birth numbers are not as high as they used to be, and the scares over the birth rate of Islamic families in the UK are down to demographics: these imigrants tend to come from Pakistan and Bangladesh, which have traditions of large families (as seen in Nassim’s link above), and first generation immigrants tend to keep this tradition, so boosting migrant community numbers, though second and further generations tend to become more secularised and adopt the ways of the country they were born into. Coupled with shifting demographics of people living longer, and one can see that population dynamics is a complex thing.

Also, population growth has always been linked to the economic ideal of a never ending ‘growth economy’ which expresses itself in extreme exploitation of both the planet and its inhabitants of all species.

However if humans are to live sustainably upon the planet, then a smaller (much smaller) population needs to be aimed for over the coming centuries, other wise long-term depletion of soil, water and mineral resources will do it for us, and in the process probably kill off most of the other life on the planet too… Either that or we all learn to live on the same resources as the average Indian, and somehow I don’t see that happening in a hurry:

L,

Sid.March 7, 2013 at 7:57 am #7046ParticipantHi Illarghi,

On the depression and child poverty in America, for those that can get it, check out this film: This World – America’s Poor Kids

It supports your reduction of per capita square footage of living space (families crammed into one room having previously lived in a house), and accommodation based upon what people can afford, from low rent to no rent and the social consequences for all concerned, especially the children. Heart wrenching in places…

The Director Jezza Neuman’s blog is very insightful too.

Over half a million more kids in poverty since 2007 and its getting worse. Says a lot about the true ‘state of the Nation’…

L,

Sid.March 7, 2013 at 9:54 am #7047Nicole Foss

ModeratorPeople I know who live in Spain tell me that the official figures underestimate the size of property bubble significantly, because official property prices do not include the ‘brown envelope money’ that also changed hands on completion. That aspect is greatly reduced now, but that part of the price fall is invisible. The housing bubble in Spain was truly gargantuan. I think it has a very long way to go to the downside, and that prices will undershoot where the bubble began to the point where they would temporarily be worth less than the cost of their constituent materials. Skyhigh unemployment and a lack of access to credit mean purchasing power, and therefore price support, will be falling for a long time.

Dave, your scenario 3 best reflects my view:

“3) ???? (10%) – Spain leaves the eurozone, goes back to the Peseta, and prints money to solve the problem; possibly civil war or authoritarian government results in property prices becoming true bargains based largely on the Peseta’s 3:1 (?) exchange rate to the euro.”

I agree with Skipbreakfast that many properties will be completely worthless, and that this will drag down the average. As I have said before, a 90% fall from peak to trough is simply typical for a bursting bubble following an asset mania. It could easily be worse than that considering the scale of this particular bubble.

I would expect house price to bottom in nominal terms for a decade at least. Housing markets go illiquid and then ratchet down one step at a time. Most people need do nothing at all for their home to lose value. All it takes is a few bargains at the margins at a lower price to give price discovery, then the whole neighbourhood of comparable properties goes down in value. The virtual value built up in the boom years simply disappears, because it never had any basis in reality. This is profoundly deflationary as the knock-on effect on the real economy are huge.

Even when house prices merely stop rising, a large economic stimulus is removed because people can no longer borrow against their home and spend the money extracted. In the bubble years in the US some people were supplementing their income by perhaps tens of thousands per year by using the house as an ATM. Cutting off that flow of money was a primary cause of the 2008 recession.

Credit bubbles artificially stimulate demand through the creation of excess purchasing power. When that purchasing power goes away, the demand borrowed from the future must be repaid. Recession becomes depression as economic activity freezes over. Spain is only at the beginning of this process.

As for Germany, they didn’t have a housing bubble, but their banks funded everyone else’s. Germany may be able to bail out their own banks, but not other EU institutions. I think a German internal bank bailout would come on a German exit from the EU.

The Sewdish bank bailout of the 1990s cost some 4% of GDP, compared to 40% for the Irish version (to date). Other countries could be worse. This is unrepayable debt. It’s nowhere near having fully deflated.

March 7, 2013 at 10:56 am #7048TheTrivium4TW

ParticipantRemember, folks, the monetary system is a 5th grade level fraud upon society.

If I lend you $20 in Federal Trivium Notes @ 5% interest.

After one year, you owe me $21, but I only gave you $20.

The only way you can pay me back is if I allow you to pay me back – I’m in the control, the sovereign, if you will.

“When a government is dependent upon bankers for money, they and not the leaders of the government control the situation, since the hand that gives is above the hand that takes. Money has no motherland; financiers are without patriotism and without decency; their sole object is gain.”

– Napoleon BonaparteIf I allow you to work for me, you can earn that $1 in interest from me, in a timely manner, and then pay me the $1 in addition to the $20 I lent you originally – nobody has any money anymore.

I could do the same as above, except you would trade your assets for the $1 in a timely manner. Again, nobody has any money when the debts are paid.

Or, I can create another $20 in debt to make the first $21 easier to pay off, but I’ve then created an exponential debt growth machine that would produce something similar to this (second chart)…

https://market-ticker.org/akcs-www?post=218297

The point is the people who control and profit from the institutions that lend nation states money ar simply con artists that suck labor, suck assets and asset strip society based on the ebb and flow of the bubble / bust cycles they engineer.

It’s all fraud, people – criminals are running the show at the very top.

That’s why their puppet Presidential Puppet demands the right to murder anyone he wants, anytime he wants with no oversight.

“If all the bank loans were paid up, no one would have a bank deposit, and there would not be a dollar of currency or coin in circulation. This is a staggering thought. We are completely dependent on the commercial banks for our money. Someone has to borrow every dollar we have in circulation, cash or credit. If the banks create ample synthetic money, we are prosperous; if not, we starve. We are absolutely without a permanent monetary system. When one gets a complete grasp upon the picture, the tragic absurdity of our hopeless position is almost incredible – but there it is. It (the monetary system problem) is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse unless it is widely understood and the defects remedied very soon.”

Robert H. Hemphill, Credit Manager, Atlanta Federal Reserve Bank, in foreword to 100% Money by Irving Fisher 1936One mechanism used by this international criminal debt money fraud cartel to exert control is the Council on Foreign Relations.

This presentation by Jame Perloff is excellent on the whole…

March 7, 2013 at 11:45 am #7049ParticipantStoneleigh –

I think another (unspoken here) requirement that is key to your scenario is a complete collapse of credit availability. If however the credit system remains more or less intact, bank depositors are bailed out FDIC-style but the bondholders are thrown under the bus and/or the banking system gets a massive injection of capital, credit will remain available and deflation will be more limited than you anticipate.

I think that outcome – the one where credit remains largely intact – is quite possible. The deflation will be bad, but not world-ending. Then again, I also believe your outcome is quite possible as well.

The scenario I presented in the article was the one I think that is almost guaranteed to occur – there is a very low likelihood avoiding that outcome given the situation I see today. In some sense, I’m saying: “I am virtually certain it will be at least this bad” based on the evidence I’ve collected.

Unfortunately I didn’t go to the next step and ask the question: “under what conditions could the outcome be substantially worse.”

It would be interesting to me to have a discussion about a set of trigger events that if they occur, would cause things to become dramatically worse. in other words, what would take the outcome in Spain from Ireland’s case (where things are bad, but haven’t collapsed because of that 140 billion they dropped on their banks) and push it into something substantially worse.

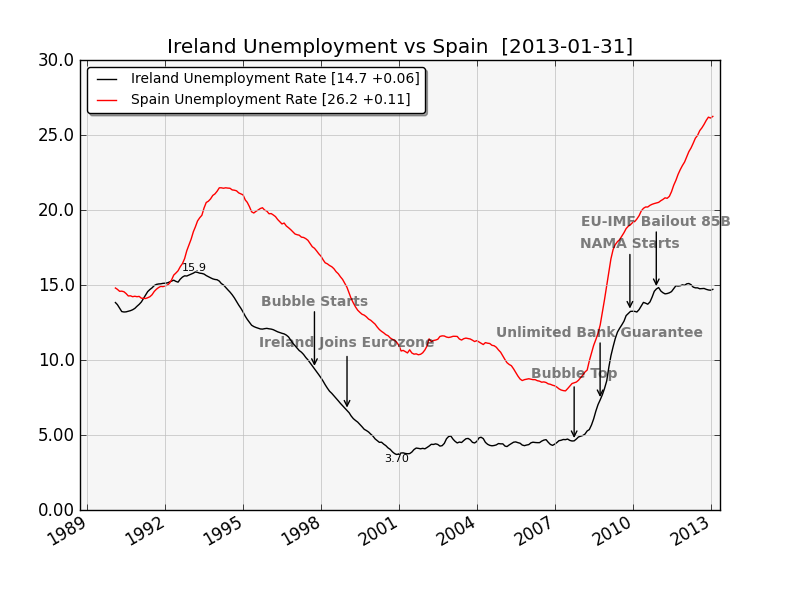

Ireland’s GDP stopped dropping as did their unemployment rate as soon as they resolved the uncertainty through the 143 billion euro money drop. This put a floor on the damage done. Spain didn’t do this, at least it hasn’t done this yet. If they do, will that arrest the economic collapse? Take a look at this unemployment chart:

Ireland’s property bubble was at least as bad as Spain’s – likely worse based simply on the fact that 25% of their economy that was employed in the construction industry at the bubble’s height. Spain had “only” 15%.

March 8, 2013 at 8:20 pm #7059ChartistFriendPgh

MemberWriters Love Charts Because Readers Can’t Read Charts https://chartistfriendfrompittsburgh.blogspot.com/2013/03/writers-love-charts-because-readers.html

March 9, 2013 at 12:14 am #7060ParticipantChartistFriend –

I’m a big fan of specific, focused, helpful criticism that shows me how to better present information. Since you are a chart expert, I’m quite open to hearing what specific and focused criticisms you have about the charts I’ve created.

March 9, 2013 at 3:13 pm #7061Viscount St. Albans

ParticipantWhy is the stock market making all-time highs?

My short positions are hemorrhaging. I’m going to bleed-out if this keeps up.

How can everything be so bad if the market is so good? Is Stoneleigh going to update things sometime? At some point, the disconnect is so blazing hot, your brain gets third degree burns just for thinking in the gutter.

I look around and I see cars accelerating, and I hear jets soaring overhead, and I smell burgers and steaks sizzling at the cafes. I pinch my skin and I learn two things: I’m getting fat and no, I’m not dreaming.

I’ve started watching Jim Cramer again.

March 9, 2013 at 4:23 pm #7062ParticipantViscount –

Now now, that position hemorrhaging is your own fault for not using stops. The couple of shorts I tried were stopped out basically even. Now its time to wait for the market to show its hand again.

High volume down days and low volume up days are an indication of a possible top. The words “indication” and “possible” are the key. If this stuff were a sure thing, we’d all be absurdly rich swapping stories on a beach.

The fat bit is your own fault as well. Try self control. 🙂

Last point; as much as I watch it, the world is not the market. The market reflects (ideally at least) profits – and expectation of profits – of the public companies. Welfare of people, on the other hand, isn’t included, such as the 26% unemployed in Spain, for instance. Nor is sustainability.

In the US, government borrow & spend of a trillion a year is making everything look better than it actually is. As long as that continues, that’ll put a floor supporting corporate profits. The moment we have to reduce spending back to the old more sustainable levels pre-2008, we’ll drop into recession faster than you can say “sequester.”

Hope that helps.

March 9, 2013 at 6:34 pm #7063ParticipantWhy is the stock market making all-time highs?

Viscount, That is merely the Fed creating the Wealth Effect.

It doesn’t seem to be working well for you, but Lloyd Blankfein bought a new 35 million dollar home last month.

You know what they say, Don’t Fight the Fed, Buy Gold, the punch is supposed to be flowing until 2016 last I heard from Uncle Ben.

March 10, 2013 at 4:38 am #7066alan2102

ParticipantWhat G.O. said. Don’t fight the Fed. Buy gold. Then: relax.

And read Walayat:

https://theautomaticearth.com/index.php?option=com_kunena&func=view&catid=15&id=5752&Itemid=96#6713Shorting the market could be a terrible mistake.

March 10, 2013 at 6:45 am #7067ParticipantViscount asked, “How can everything be so bad if the market is so good?”

Because we’re in a hyperinflationary depression. Bought any groceries lately, or anything else for that matter. Notice how the packages are smaller and the prices are higher? This is the logical outcome of unrestrained money creation by those in charge.

For the fiscal year ending 9/30/2012, the federal govt. ran a GAAP budget deficit of $6.9 trillion. That’s about 40% of GDP. Money creation in the extreme.

Why should China call us out now? We’re suppressing the price of gold, enabling them to get in cheap. When the time is right for them, they will dump the dollar, don’t ask me when.

March 10, 2013 at 7:22 am #7068Participant@pipefit –

GAAP budget deficits are not money creation. The GAAP deficit is just about promises. No actual money is created.

Thought experiment. If I promised you 10 trillion dollars to be delivered next tuesday, no actual money would be created until tuesday rolled around. Same thing here. The US government has promised to deliver social security & medicare payments, and that’s where the GAAP deficit comes from. GAAP is about accounting for promises. Presumably, we should be putting money aside every year so we can make good on those promises, but we aren’t.

But that’s not the same thing as creating money. Money creation comes from borrowing to fund a CASH deficit.

March 10, 2013 at 3:24 pm #7069Participantpipefit post=6779 wrote: Viscount asked, “How can everything be so bad if the market is so good?”

Because we’re in a hyperinflationary depression. Bought any groceries lately, or anything else for that matter. Notice how the packages are smaller and the prices are higher? This is the logical outcome of unrestrained money creation by those in charge.

Pipefit, please. It is obvious that we’re in an inflationary mega-trend in commodities and most of the things that people buy and use — i.e. with respect to real costs of living — and this goes back many years. But it is equally obvious that we are not in anything like HYPER-inflation, which would see prices rising at (say) 10% per month, or more. Be reasonable. Do not abuse the word “hyperinflaton”.

Why should China call us out now? We’re suppressing the price of gold, enabling them to get in cheap. When the time is right for them, they will dump the dollar, don’t ask me when.

Right! Either that or THEY are suppressing the (paper) price of gold, allowing them to get physical on the cheap. In any case, they are accumulating massive amounts of physical, far in excess of stated amounts, while the west is being bled. The big wealth and power shift is dead ahead.

Meanwhile, you can protect yourself by becoming your own central bank, even if it is to the extent of only buying one single ounce. In the coming years, you might be astonished at how very much that one ounce will buy, and how much trouble and grief it will save you. It might even save your life. It is easily the best single “prep” you can make.

March 10, 2013 at 10:41 pm #7072ParticipantDaveF. said, “GAAP is about accounting for promises. Presumably, we should be putting money aside every year so we can make good on those promises, but we aren’t.”

You are half way there. dave. The govt. isn’t setting aside money, like they promise. AND, as a result of the failure of the average rube to figure that out, the average rubes aren’t setting aside money either.

This is where the inflation comes in. What if the govt., in a rare bout of honesty said, “please, please, please start setting a lot more money aside for retirement, because using honest accounting the govt., including ss and medicare, is completely broke? You know the answer. Spending would decline by 30% or more from present levels. That means that 30% of retail employees would be fired, and the people that the newly unemployed buy stuff from would be fired, etc. i.e. a deflationary collapse.

It is a lot easier for the fed to just print $85 billion a month, and for Congress to deficit spend $7 trillion a year. Also note, by not setting more money for entitlement programs, the fed. govt. has more cash on hand for money that can be dumped into the economy, such as salaries of govt. workers.

March 10, 2013 at 10:54 pm #7073ParticipantAlan-IMHO, we are very close to entering the ‘hyper’ part of this inflationary trend. One indicator that I gave you already was that the 2012 fed. budget deficit, using GAAP accounting, was 40% of GDP.

Another indicator is the oil:ng ratio (stockcharts.com symbol $wtic:$natgas). This is fairly good proxy for inflation expectations. It has dropped a little recently, to 25:1, but oil is still selling at 250% premium to natural gas. Keep in mind that on a btu equivalent basis, the ratio should be 7:1, and during the 80’s and 90’s this ratio averaged 9:1 over a 20 year span.

Near the bottom of the deflation scare, in late 2008/early 2009, this ratio dropped all the way below par, to 6:1. If you see that again, you really don’t want to be anywhere near where there electricity, computers, any utilities, etc., since it means a deflationary collapse is at hand.

March 10, 2013 at 11:12 pm #7074ModeratorPipefit,

Natural gas is ahead of oil in its ponzi cycle, in that the unconventional natural gas hype came first, in response to the terrible prospect in conventional projects. Now that cycle is reversing, and natural gas prices are set to rise on a looming supply crunch (because natural gas companies were losing so much money at the low prices their hype, and the consequent perception of glut, had generated). The same phenomenon is about to unfold in relation to unconventional oil, now that the hype is shifting in that direction. The perception of glut will drop prices substantially, even in the face of actual (but masked) scarcity in relation to current demand. As demand falls on economic contraction, that trend to lower prices will accelerate.

I don’t regard the ratio of oil price to gas price as any kind of indicator of inflation expectations. Nor would I expect either price to reflect relative BTUs, since prices are set by perception of scarcity/glut, not by the fundamentals. For what it’s worth, I expect the ratio to fall substantially over the next few years as the gas squeeze begins while oil prices fall, at least in North America. Elsewhere the cycle for gas is in a different position, with fracking hype only beginning.

I regard our financial position as at or near the peak of a counter-trend rally (a ‘b’ wave in an expanded flat correction to be specific, as the 2007 peak was in relation to the 2000 peak at a higher degree of trend). The implication is that the downtrend should resume fairly soon (ie wave ‘c’ is dead ahead, and ‘c’ waves above a moderate degree of trend are devastating). The persistent unnaturally low volatility combined with a sentiment extreme and insider selling are clear indications of a top. As we go over the edge, I expect volatility to spike.

March 10, 2013 at 11:21 pm #7075ModeratorWe are not in, or anywhere near, any kind of hyperinflationary trend. Commodity prices are set to fall, and so-called money printing is not having any kind of stimulating effect on the real economy. Prices have been rising as a lagging indicator of desperate attempts to stave of financial collapse, but that trend has nearly run its course. What we need to be looking at, and preparing for, is the trend change at hand. It has been a long time in coming, but it is quite clear if you know what to look for. Betting on the recent uptrend continuing could not be more dangerous at this point. Look at the markets with a contrarian eye, and do the opposite of the what the herd is doing.

March 10, 2013 at 11:46 pm #7076Moderatordavefairtex,

I think another (unspoken here) requirement that is key to your scenario is a complete collapse of credit availability. If however the credit system remains more or less intact, bank depositors are bailed out FDIC-style but the bondholders are thrown under the bus and/or the banking system gets a massive injection of capital, credit will remain available and deflation will be more limited than you anticipate.

The disappearance of credit is exactly what I am expecting. Credit is already tightening substantially in many places, and I expect that trend to pick up momentum. Credit is normally only available to the relatively wealthy, except during bubble times. As this has been a very large bubble, credit availability has persisted for long enough for us to have come to see it as the natural state of affairs. I think we’ll be returning to the previous condition, with an undershoot, where credit becomes far less available than normal, as opposed to far more available than normal.

So many people are going to be maxed out across the board, with looming (or realized) unemployment, a major credit squeeze, rising interest rates (as a risk premium) and rising taxes (especially property taxes). In this kind of financial perfect storm, price support for almost everything is very likely to plummet, with the caveat that the essentials would receive relative price support and would therefore fall less far in nominal terms (even as they rise in real terms).

I think you’re charting work is really good, and we’re really happy to give it the exposure it deserves. I’m just more bearish than you are.

March 11, 2013 at 1:30 am #7081Participant@pipefit –

“as a result of the failure of the average rube to figure that out, the average rubes aren’t setting aside money either”

The average rube is both more and less clever than you give him credit for. They know what’s happening, and their widespread failure to set aside money is thus completely inexplicable.

When non-retired adults were asked in 2010, “Do you think the Social Security system will be able to pay you a benefit when you retire?” 36% said YES, and fully 60% said NO.

Of course the survey goes on to highlight the incredible wish-impulse for free lunches that American citizens have displayed for far too long. But they DO know there’s a problem.

https://www.gallup.com/poll/1693/social-security.aspx

“It is a lot easier for the fed to just print $85 billion a month, and for Congress to deficit spend $7 trillion a year.”

The Congress is deficit-spending about 900 billion a year these days, not 7 trillion. The missing 6 trillion is all just promises. Same as my promise to pay you a trillion dollars by next Tuesday. It only matters when Tuesday rolls around. At that point, I’ll likely default – what happens when an unsustainable promise comes due. But didn’t you feel happy over the weekend? Yet no money was created. The only thing created by my promise was your feeling of happiness.

Money – something that is used to buy goods & services in the real economy – is created in two ways:

1) it is borrowed into existence by a willing borrower

2) it is printed by the FedThat’s it. Promises don’t fall under either heading.

March 11, 2013 at 1:59 am #7082ParticipantThanks for your kind words about my charts!

Its my goal to remain as evidence-driven as possible given the limitations of the data we have available. That’s what my charts are all about. I have been continually surprised by the various crisis outcomes, and my data collection is an attempt to avoid as much as possible such surprises in the future.

I do agree that you are more bearish than I am. That said, I definitely assign a non-zero probability of your scenario occurring. If events unfold the way you describe, it will certainly lead to the outcome you predict. I see things unfolding along a continuum of possible outcomes, and I get more clarity as to likelihood as events unfold.

I have to say how much I enjoy these discussions. Often someone’s question or comment will cause me to think, or run off and search my data to see if its true or not.

I did a simple study of debt burden and payment burden in the US on this page at my site:

mdbriefing.com/us-rpp.shtmlIt shows that the Fed has successfully reduced the payment burden for homeowners in the US – back to pre-bubble levels, but the vast majority of the debt burden remains. In other words, they’re underwater, but at least they aren’t experiencing the pain.

The cost: interest income for savers, about 500B per year just wiped out. Sorry grandma.

What’s almost equally fascinating to me is that even with payments set so incredibly low, home mortgage total loan amounts outstanding are still deflating.

-

AuthorPosts

{kind=link}

- You must be logged in to reply to this topic.

Sorry, the comment form is closed at this time.