DPC Unloading cotton, Mississippi sternwheeler City St. Joseph,Memphis TN 1910

Janet Yellen is a religious nutcase. She may not appear like one at first glance, but take a look at her picture again and you may find that instead that’s exactly what she looks like. She may have that nice little grandma façade, but then those are often the worst cases. I realize this is not a nice thing to say, but there are limits to what even nice little grandmas can say and do, especially when they run a central bank where an embroidery class would seem like a much better fit.

The New Yorker has a portrait of Yellen that is behind a paywall, but CNBC has enough to get to the gist of it, which saves us from having to read about her hairdo too. They first refer to an older speech of hers, which nicely sets the tone:

“Although we work through financial markets, our goal is to help Main Street, not Wall Street.”

No, she really said that. CNBC, however, states the obvious:

“More than five years after the financial crisis, historically high numbers of Americans are still out of the labor force.”

AP, on the other hand, doesn’t seem to think this is a problem:

While unemployment stood at 6.7% in February, it has now fallen to 6.1%, the lowest point since September 2008, reflecting strong job growth in recent months. The economy has created an average of more than 200,000 jobs a month over the past five months, the strongest stretch since the late 1990s.

That looks more like the official party line. But we do remember, don’t we, that in the last BLS survey full-time jobs actually went down quite a bit, only to be replaced with a larger number of part-time jobs?! And we haven’t forgotten either that US Q1 GDP was down -2.96%? Sorry to repeat those things all the time, but they’re important when it comes to what Yellen has to say.

Still, while that first statement of hers was just a simple lie, this nest one is the clincher for me, this is where religion comes in and reason is washed away with the bathwater, and this is why I don’t hesitate to call her a nutcase, even though I don’t find that easy:

The Keynesian tradition, Yellen told the magazine, and the line of research known as “behavioral finance” have “come out of this crisis with greatly enhanced prestige in academia, and in institutions like [the Federal Reserve].”

I tell you, I can take a lot, but that truly pisses me off. That sort of blind arrogance makes Mrs. Nice Little Grandma an enormous danger to America. Bernanke and Yellen have blown up the Fed balance sheet to the tune of $4 trillion, and that’s just one of many tricks in their books. While unemployment rates only appear to have fallen because millions of Americans are no longer counted as participants in the labor force. And the number of people on foodstamps has shot through the ceiling and never came back down. And, and, and.

Meanwhile, Wall Street profits have shot up and stock markets set new records all the time. That last bit is what I guess gives Yellen the guts to state that the “Keynesian tradition” has been vindicated. She can do so only by conveniently forgetting that we’re in the sixth year of the alleged recovery, and we’re nowhere near past the end of the crisis – which must be setting records -, even if she would like to differ on that.

Well, if she feels that the Keynesian approach has been such a ravishing success, why doesn’t Yellen:

1) cut QE asset purchases to zero immediately,

2) sell off all assets presently on the Fed’s balance sheet, and

3) raise interest rates?

Because, and this is painfully obvious – I wish I could make this a multiple choice question for you, but there is only one possible answer – it hasn’t been successful at all. That’s why AP writes:

Yellen has stressed that while jobs are now being produced at a faster clip, the economy still needs the Fed’s help in the form of low interest rates because a variety of indicators, from measures of long-term unemployed to wage growth, still remain weak.

And that’s why Yellen tells the New Yorker:

… even when the headwinds have diminished to the point where the economy is finally back on track and it’s where we want it to be,” she told the New Yorker, “it’s still going to require an unusually accommodative monetary policy.”

What she says there is that the economy is where she wants it to be, but at the same time it’s not. Your average run of the mill mortal soul might think that the Keynesian measures have either been successful or they’ve not. But no, Yellen sees a third way: it’s both. The deity is always right, and when he’s not, you just pray harder. She believes in Keynesianism, so much so that if “accommodative monetary policy” doesn’t work, she pours on more, and “unusually” accommodative monetary policy. Little grandma’s deity is never wrong. I’m sure that reminds many of you of little old ladies you knew at one point or another in your lives.

If we were to summarize Bernanke and Yellen’s policies over the past 6-7 years, it would come down to something like this:

The Federal Reserve’s view is that it’s quite alright to not restructure debt in the banking system, no matter how large that debt is, and that you can – easily – avoid having to execute such restructuring by simply pumping seemingly unlimited amounts of additional debt into both that same banking system and – to a much lesser extent – into the economy at large.

It is useful to note here that not long after Ben Bernanke took over as Fed head, he talked in one of his speeches about the ‘uncharted territory’ the Fed was entering: he meant that nobody before in history had faced a crisis like the one we had in 2008, and nobody had ever attempted the response he was spearheading.

And it’s even more useful to note that since then, the Fed hasn’t come back out of that uncharted territory, it has wandered ever deeper in (and is now hopelessly lost, if you ask me).

But you wouldn’t know that from listening to Yellen speak today, or Bernanke in his last Fed head years, for that matter; it was never mentioned again. They have both been seeking to come across as if they did and do know what they were and are doing, and people mostly swallowed the message whole.

This week, she’ll talk to Congress trying to convey that same notion, that she’s in control. They’ll buy most of it, because they too have long forgotten that ‘uncharted territory’ idea Bernanke mentioned, and no-one there thinks of asking Yellen about it. But she will get asked why, now that she seems certain she’s got it down, she doesn’t raise rates and/or sell assets. And she’ll answer something to the extent – though not in those words – that her deity is always right, just occasionally slow.

Meanwhile, elsewhere, it’s all Keynes all the time too. 2 Bloomberg pieces:

China’s New Loans, Financing Top Estimates

China’s broadest measure of new credit topped analysts’ estimates in June, signaling policy makers’ shift toward supporting economic growth over reining in shadow banking. Aggregate financing was 1.97 trillion yuan ($317 billion) in June, the People’s Bank of China said on its website today, compared with the median estimate of analysts for 1.425 trillion yuan. New local-currency loans were 1.08 trillion yuan and M2 money supply grew 14.7% from a year earlier.

Eh, excuse me: “M2 money supply grew 14.7% from a year earlier”?! China doesn’t have a money supply problem, it has a velocity of money problem. Like the rest of the world. People are not spending.

China’s Local Governments Pile On Stimulus

China’s regional governments are starting to pull out their own stimulus cards to shore up growth as central authorities limit aid for the economy. Northern Hebei province, whose 4.2% first-quarter expansion pace was less than half that of a year earlier, will invest 1.2 trillion yuan ($193 billion) in areas including railways, energy and housing. Heilongjiang province in the northeast, with 2.9% growth that was China’s lowest in the first quarter, will spend more than 300 billion yuan over two years in areas including infrastructure and mining. Any borrowing to fund the investment risks exacerbating financial dangers from local-government debt that swelled to about $3 trillion as of June 2013.

China’s local governments to a large extent work through shadow banks. Any questions?

2 Wall Street Journal articles attest to Lord Keynes’ adventures in Europe:

IMF Touts Quantitative Easing Benefits for ECB

Large-scale purchases of government bonds by the European Central Bank would boost euro zone inflation and stimulate demand for bank credit, the International Monetary Fund said Monday in its latest effort to tout the potential benefits of quantitative easing in Europe. The IMF stopped short of calling on the ECB to immediately embark on the policy, which stirs deep skepticism in the euro zone’s largest member, Germany. [..] Quantitative easing “can push up inflation by raising consumption and investment across the euro area, and support that trend by reviving the supply and demand for bank credit,” wrote Reza Moghadam, head of the IMF’s European department, and the department’s deputy director Ranjit Teja.

They don’t really want inflation, they want to force people to spend. But people don’t have enough, either money or confidence, to spend. Still, they have a solution for that too: coax them into borrowing more. The Lord Keynes would have wanted it that way. Or so they say.

Debt Purchases Are Within ECB’s Mandate: Draghi

European Central Bank President Mario Draghi said Monday that large-scale purchases of public and private debt fall “squarely” within the ECB’s mandate to keep inflation low and stable. Draghi’s remarks, at a hearing at a newly formed European parliament that met in Strasbourg, France, are the latest indication that the ECB is open to additional aggressive stimulus measure if they are needed to keep inflation from staying too low for too long. He said the ECB’s ultralow interest rates – the ECB cut them to record lows last month and installed a negative rate on bank deposits at the central bank, the largest institution to do so – haven’t fueled asset bubbles but warned of “frothy” conditions in the housing markets of some euro-area countries. Regulatory policies are the primary defense against such risks, Draghi said, adding that monetary policy isn’t the right instrument to use at a time of low inflation.

Let’s hope the Germans have gained some extra strength from winning the World Cup, and continue to refuse to succumb to the Yellen, Bernanke, Lagarde and Krugman-led destruction of their children’s futures. And remember that there is no historic proof that what all these people are doing has even the potential to work. No proof whatsoever. It’s just faith based economics.

Throughout history, many bloody battles have been fought, and many societies destroyed, over religious conflicts or through sheer religious zealotry. Are we really sure we are ready to let that kind of thing knock on our doors? I’m asking because that is what’s happening.

• Yellen To Maintain Keynesian Slant (CNBC)

Janet Yellen’s strong support of Keynesian economics will likely determine future Federal Reserve policy, the New Yorker reported in an interview with the Fed chair on Monday. The Keynesian tradition, Yellen told the magazine, and the line of research known as “behavioral finance” have “come out of this crisis with greatly enhanced prestige in academia, and in institutions like [the Federal Reserve].” Both Yellen and her husband, George Akerlof, were strongly affected by their parents’ experiences with unemployment, the New Yorker said, citing papers the couple has published stating that people’s economic behavior is not mechanically rational and that the Fed can manage the economy better than the markets.

Yellen enjoys a ground-level approach, the article said, from interviewing security guards to hearing what every member of the Federal Open Market Committee has to say before an official meeting. But the article said she must move towards economic and political policy in managing the Fed since her ability to depend on personal discussions is disappearing as investors closely follow every conversation she has. “And so even when the headwinds have diminished to the point where the economy is finally back on track and it’s where we want it to be,” she told the New Yorker, “it’s still going to require an unusually accommodative monetary policy.”

• Federal Reserve’s Yellen Giving Congress Good News (AP)

Federal Reserve Chairwoman Janet Yellen will have some good news to tell Congress this week about the health of the labor market. But lawmakers will likely press her to provide more information on just how the central bank intends to react to the good news. Yellen is scheduled to deliver the Fed’s twice-a-year report to Congress on interest-rate policy and the economy. She testifies before the Senate Banking Committee on Tuesday and will follow that with testimony Wednesday before the House Financial Services Committee. She delivered her first monetary report to Congress in February, just a week after being sworn in to succeed Ben Bernanke as the first woman to head the central bank. While unemployment stood at 6.7% in February, it has now fallen to 6.1%, the lowest point since September 2008, reflecting strong job growth in recent months. The economy has created an average of more than 200,000 jobs a month over the past five months, the strongest stretch since the late 1990s.

That will be the good news that Yellen will relate. But lawmakers are certain to quiz her about what the performance of the labor market will mean for the Fed’s handling of interest rates in coming months. In recent comments, Yellen has stressed that while jobs are now being produced at a faster clip, the economy still needs the Fed’s help in the form of low interest rates because a variety of indicators, from measures of long-term unemployed to wage growth, still remain weak. Yellen’s comments will be followed closely to see whether there are any shifts in her view that inflation, while rising at a slightly faster pace than back in February, remains low with no danger that it is about to get out of hand. The Fed’s twin goals are to promote maximum employment while keeping inflation under control.

Lawmakers will want to hear Yellen’s views on both goals and on related subjects such as whether she has any concerns that the Fed’s prolonged period of low interest rates could be setting the stage for financial instability once the central bank starts raising rates. And lawmakers will also be looking for insights on how the Fed plans to unwind its massive holdings of Treasury bonds and mortgage-backed securities, which are approaching $4.5 trillion, more than four times the amount on the balance sheet when the financial crisis struck in the fall of 2008. The Fed’s bond purchases were aimed at keeping long-term interest rates low to give the economy a boost.

• When Do We Get Off The Fed Treadmill? (CNBC)

When do we get off this treadmill whereby central banks believe it’s their responsibility to not only maintain price stability and maximize employment, but also to boost asset prices (thereby creating new systemic risks)? The Federal Reserve’s assessment of “inflation” is flawed. Not only does the Fed essentially disregard the prices of food and energy (which disproportionately affects low- and moderate-income consumers), but the central bank also fails to consider asset-price inflation. Virtually everyone agrees that the Fed’s easy-money policies have directly contributed to a huge rebound in stocks and housing prices. In fact, aggregate household net worth has increased by $26 trillion to $82 trillion (an all-time high) since the first quarter of 2009. But the Fed’s goal was not simply to make rich people more rich (which they did). Rather, they are operating under the misguided assumption that higher asset prices will, by some miracle of trickle-down economics, lead to plentiful jobs and higher incomes for the masses.

The Fed’s current policy mistakes are eerily reminiscent of the ones made by Chairman Greenspan in the early 2000s. Following the implosion of technology stocks in 2000-2001, Greenspan kept the fed-funds rate at 2% or lower for the following three years. Low interest rates, along with deterioration in mortgage underwriting standards, led to huge increases in housing prices. We all know how that turned out. The only thing that makes it worse this time is that Chairman Bernanke (and now Chair Yellen) are making no attempt to veil this strategy. They have come right out and told us (fairly regularly) that they are targeting stock prices as a way to generate better economic growth. We found those comments troublesome then, and we still find them troublesome today. In our view, the Fed has no business influencing stock prices. So now we find ourselves in the familiar position of advocating for an end to quantitative easing while still believing that the Fed may not follow through with its plan to end QE by the end of the year. Why?

• IMF Touts Quantitative Easing Benefits for ECB (WSJ)

Large-scale purchases of government bonds by the European Central Bank would boost euro zone inflation and stimulate demand for bank credit, the International Monetary Fund said Monday in its latest effort to tout the potential benefits of quantitative easing in Europe. The IMF stopped short of calling on the ECB to immediately embark on the policy, which stirs deep skepticism in the euro zone’s largest member, Germany. But the comments from the Washington-based international lender—contained in a blog post addressing the question: “would the juice be worth the squeeze”—largely come down in favor of quantitative easing as a means to lift inflation rates across the 18-member euro bloc. Quantitative easing “can push up inflation by raising consumption and investment across the euro area, and support that trend by reviving the supply and demand for bank credit,” wrote Reza Moghadam, head of the IMF’s European department, and the department’s deputy director Ranjit Teja.

Annual inflation in the euro zone was just 0.5% in June, far below the ECB’s target of a little under 2%. Last month, the ECB took a number of steps to raise inflation, including a negative rate on bank deposits parked at the ECB and a long-term loan program that would give banks cheap credit provided they boost lending to businesses. The ECB didn’t announce a broad-based asset purchase program, though officials have said it remains an option if the outlook for inflation erodes further. If the ECB decides to go this route, it should focus on government bonds as the “only viable option,” the IMF officials wrote, noting that the market for bundled loans and corporate bonds is small in Europe. “ECB purchases should be across the board, not just core or periphery, because the problem of low inflation is across the board,” they wrote.

• Debt Purchases Are Within ECB’s Mandate: Draghi (WSJ)

European Central Bank President Mario Draghi said Monday that large-scale purchases of public and private debt fall “squarely” within the ECB’s mandate to keep inflation low and stable. Draghi’s remarks, at a hearing at a newly formed European parliament that met in Strasbourg, France, are the latest indication that the ECB is open to additional aggressive stimulus measure if they are needed to keep inflation from staying too low for too long. He said the ECB’s ultralow interest rates — the ECB cut them to record lows last month and installed a negative rate on bank deposits at the central bank, the largest institution to do so – haven’t fueled asset bubbles but warned of “frothy” conditions in the housing markets of some euro-area countries. Regulatory policies are the primary defense against such risks, Draghi said, adding that monetary policy isn’t the right instrument to use at a time of low inflation.

His remarks came hours after the International Monetary Fund renewed its calls for the ECB to consider big asset purchases, known as quantitative easing, to revive lending in the euro zone and keep ultralow inflation from damaging the bloc’s recovery. “QE falls squarely in our mandate,” Draghi told parliamentarians. Earlier Monday, the International Monetary Fund outlined a number of benefits of large-scale government purchases by the ECB. Such a policy, which has been used extensively by central banks in the U.S., U.K. and Japan, “can push up inflation by raising consumption and investment across the euro area, and support that trend by reviving the supply and demand for bank credit,” wrote Reza Moghadam, head of the IMF’s European department, and the department’s deputy director Ranjit Teja.

Still, Mr. Draghi said that the ECB’s recent easing steps, which in addition to record-low interest rates included new cheap loans to banks, have already had an effect on financial markets and should help boost annual inflation, currently at 0.5%, closer to the ECB’s target of just under 2%. [..] “The ECB is the only central bank of the world where the balance sheet has been going down,” he said, rebutting complaints from one lawmaker that he has been too generous to banks and that the ECB’s new targeted lending program is the “credit default swap of the future,” a reference to securities at the heart of the 2008-2009 global financial crisis. “As soon as recovery takes momentum, interest rates will go back up again,” Mr. Draghi said.

He should be fired for this: he’s admitting he gave money to banks with the explicit goal of using it to profit in carry trades.

• Draghi Says Banks Shouldn’t Count on Another Carry Trade (Bloomberg)

Banks shouldn’t count on a fresh round of European Central Bank cash to trade sovereign debt and reap big profits, Mario Draghi said. “The convenience to use the ECB cheap money to buy government bonds is much less” than in a previous funding round which started in 2011, the ECB president said in testimony to the European Parliament in Strasbourg, France yesterday. “The general situation is such that these carry trades are going to be much less profitable.” As spreads on government debt from Spain to Italy over similar German securities have fallen to record lows, a carry trade that was lucrative two years ago may now yield less, Draghi said.

In a liquidity drive that pins cash to banks’ performance in extending loans to the economy, the Frankfurt-based ECB could extend as much as €1 trillion ($1.36 trillion) in its so-called TLTRO program starting in September. A condition of that program is that banks have to meet a benchmark on lending to businesses and households, excluding mortgages, or else hand back the money in 2016. “If banks don’t lend to the non-financial private sector, they’ll have to repay,” Draghi said. Financial institutions will take up more than €700 billion and will increase credit to the real economy over the four-year span of the program, according to economists polled in a monthly Bloomberg News survey.

“M2 money supply grew 14.7% from a year earlier”. And that, we now know, goes towards buying US real estate. China doesn’t have a money supply problem, it has a velocity of money problem. Like the rest of the world. People are not spending.

• China’s New Loans, Financing Top Estimates (Bloomberg)

China’s broadest measure of new credit topped analysts’ estimates in June, signaling policy makers’ shift toward supporting economic growth over reining in shadow banking. Aggregate financing was 1.97 trillion yuan ($317 billion) in June, the People’s Bank of China said on its website today, compared with the median estimate of analysts for 1.425 trillion yuan. New local-currency loans were 1.08 trillion yuan and M2 money supply grew 14.7% from a year earlier. China’s foreign-exchange reserves, the world’s biggest, rose to $3.99 trillion from $3.95 trillion at the end of March. The financing measure was the highest for June since the lending spree of 2009, as PBOC Governor Zhou Xiaochuan tries to ensure enough credit without resorting to broad-based loosening that may stoke debt risks.

Data tomorrow on gross domestic product, industrial output and investment will indicate the impact of pro-growth efforts such as expedited spending on infrastructure projects after expansion in the first quarter slid to the weakest in 18 months. “Those projects need to be financed,” said Chang Jian, chief China economist at Barclays Plc in Hong Kong. The effects of credit easing will probably show up in tomorrow’s industrial production data, she said.

If they don’t, it’s the Titanic.

• China’s Local Governments Pile On Stimulus (Bloomberg)

China’s regional governments are starting to pull out their own stimulus cards to shore up growth as central authorities limit aid for the economy. Northern Hebei province, whose 4.2% first-quarter expansion pace was less than half that of a year earlier, will invest 1.2 trillion yuan ($193 billion) in areas including railways, energy and housing. Heilongjiang province in the northeast, with 2.9% growth that was China’s lowest in the first quarter, will spend more than 300 billion yuan over two years in areas including infrastructure and mining. Any borrowing to fund the investment risks exacerbating financial dangers from local-government debt that swelled to about $3 trillion as of June 2013.

While Premier Li Keqiang is trying to expedite spending from existing budgets and avoid broad stimulus, provinces such as Hebei are facing bigger shortfalls on their own growth goals than the national government, which has a target of about 7.5%. “The motivation is there – currently GDP is still the key performance indicator for local officials,” said Shen Jianguang, chief Asia economist at Mizuho Securities Asia Ltd. in Hong Kong, who previously worked at the European Central Bank. Figures today from the People’s Bank of China showed that the broadest measure of financing, new yuan loans and money supply all topped estimates in June, signaling policy makers’ shift toward supporting economic growth over reining in shadow banking.

Absolute must read from Pettis. As I wrote yesterday: “China has undertaken its $25+ trillion stimulus not just for its – state-owned – banks, but for its entire economic system. Catching the fall of an economy that grows, or used to grow, at double digit annual rates is not the same as propping up one that used to grow at 2-3%. The difference lies in the expansion.”

• Bad Debt Cannot Simply Be “Socialized” (Michael Pettis)

[..] … for several years I have been arguing that the main reason analysts have managed to get China so wrong is because of their failure to understand the basic distortions driving the economy and one of the major consequences of these distortions is the creation of debt, which itself further impacts the evolution of these distortions. All rapid growth, Albert Hirshman argued in the 1960s and 1970s, is unbalanced growth, and in many if not most cases the kinds of imbalances that result from rapid growth may be acceptable and even necessary in a growing economy. But as the economy changes, the nature and extent of the imbalances change too, and it is inevitable that eventually the system forces a reversal of the imbalances. This is especially true in countries, like China, with highly centralized decision-making. In these countries the imbalances can be taken to extremes impossible in other countries, thus creating all the more pressure for a reversal of the imbalances.

This means that in China, if you can figure out how the growth model works and how the model generates imbalances and debt, you can pretty much figure out logically, albeit fairly broadly, the various paths that the country must follow in order the reverse the imbalances. I tried to this in my most recent book, Avoiding the Fall, in which I listed the six different ways that China can rebalance, ranging from the catastrophic to the orderly. These were not predictions. They were simply a list of the various ways in which China could rebalance, and none of these various rebalancing paths included, for example, the possibility that China could maintain average GDP growth rates of 7-8%, or even of 5-6%, during President Xi’s administration except under very specific, and unlikely, conditions.

According to the logic of the model, it would require a massive transfer of wealth from the state sector to the household sector, on the order perhaps of 4-5% of GDP annually or more, for China to rebalance at growth rates significantly higher than 4-5%. Without this transfer, however, it simply cannot happen. [..] Burgeoning debt was not an unlucky accident. It is fundamental to the way the growth model works, and we have arrived at the stage, probably described most imaginatively by Hyman Minsky in his work on balance sheets, in which the system requires an acceleration in credit growth simply to maintain existing levels of economic activity.

China’s debt problems, in other words, cannot be resolved administratively, by fixing the shadow banking system, by imposing discipline on borrowers, or indeed by eliminating financial repression (much of which, by the way, has already been squeezed out of the system by lower nominal GDP growth). Without a massive transfer of wealth from the state sector to the household sector it will be impossible, I would argue, for GDP growth rates of anything above 3-4% – and perhaps even less – to occur without a further unsustainable increase in debt, whether that increase occurs inside or outside the formal banking system and whether or not discipline has been imposed on borrowers.

They’ll find another way to drive capital out.

• Chinese Banks Halt Controversial Yuan-Remittance Program (WSJ)

China’s major banks have halted an experimental program, sanctioned by the country’s central bank, that helped citizens transfer large sums overseas despite government capital controls, according to people with knowledge of the matter. The halt, which the people said was likely to be temporary, comes after the program was criticized by China’s powerful state television broadcaster, underscoring the political sensitivity of the issue of wealthy Chinese moving money abroad. Experts said the criticism could set back China’s efforts to ease its grip on the country’s financial system. Big commercial banks including Bank of China, Industrial & Commercial Bank of China and China Citic Bank have halted the program, which allowed Chinese to remit their yuan across borders, the people said.

The halt came after the People’s Bank of China, the central bank, started to look into allegations that Bank of China had used the program to help clients launder money, they said. Last week, China Central Television accused the lender of improperly helping clients skirt China’s controls on cross-border fund transfers. In some cases, CCTV said, the bank worked with immigration agents to help customers disguise the origins of their funds. Bank of China has denied the accusations. It said in a statement last week that it adhered to regulatory requirements in conducting the business, including those prohibiting money laundering. The controversy comes at a politically sensitive time. China’s top leadership is deepening a nationwide effort to fight corruption, with a focus on officials suspected of trying to move abroad assets they might have gotten through bribes or other illegal means.

Ouch!

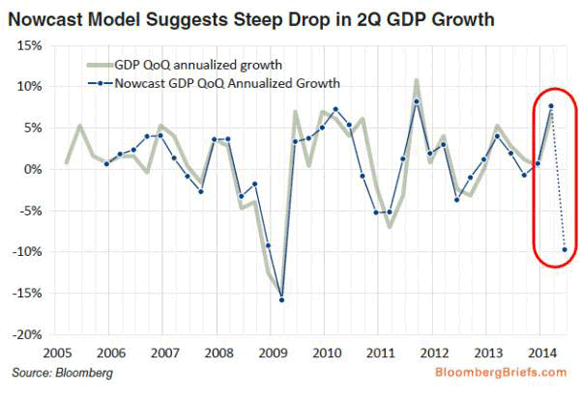

• Japanese Q2 GDP Could Be As Low As -10% (Zero Hedge)

Japan’s GDP may have declined in April and May, implying an overall collapse for Q2 not seen since 2009. Bloomberg’s Nowcast estimate suggests that the hope-strewn pre-tax-hike pile up of a +6.7% annualized GDP growth in Q1 will come crashing back to earth as consensus GDP for Q2 is -4.85% and even bigger based on Bloomberg’s models. As Bloomberg’s Tom Orlik warns, this could take markets by surprise. The good news is that Abe’s 3rd arrow has yet to reach escape velocity (any day now); below we highlight the entire package and how it will save the world… This is not what Abe wants to see…

Bloomberg’s Tom Orlik notes that their Econometric model indicates it could be significantly worse…

• The Implosion Is Near : Signs Of The Bubble’s Last Days (David Stockman)

The central banks of the world are massively and insouciantly pursuing financial instability. That’s the inherent result of the 68 straight months of zero money market rates that have been forced into the global financial system by the Fed and its confederates at the BOJ, ECB and BOE. ZIRP fuels endless carry trades and the harvesting of every manner of profit spread between negligible “funding” costs and positive yields and returns on a wide spectrum of risk assets. Moreover, this central bank sponsored regime of ZIRP and money market pegging contains a built-in accelerator. As carry trade speculators drive asset prices steadily higher and fixed income spreads steadily thinner – fear and short interest is driven out of the casino, making buying on the dips ever more profitable and less risky.

Indeed, the explicit promise by central banks that the money market rate will remain frozen for the duration and that ample warning of any change in rate policy will be “transparently” announced is the single worst policy imaginable from the point of view of financial stability. It means that the speculator’s worst nightmare—–suddenly going “upside down” due to a sharp spike in funding costs—-is eliminated by central bank writ. Stated differently, ZIRP systematically dismantles the market’s natural stability mechanisms. One natural deterrent to excessive financial gambling, for example, is the cost of hedging a speculator’s portfolio of “risk assets” against a broad market plunge. In an honest market environment, hedging costs consume a high share of profits, thereby sharply limiting risk appetites and the amount of capital attracted to speculative trading.

By contrast, an extended regime of ZIRP, coupled with the central banks’ perceived “put” under risk assets, drives the cost of “downside insurance” to negligible levels because S&P 500 put writers are emboldened and subsidized to pick up nickels (i.e. options premium) in front of a benign central bank steamroller. This ultra-cheap downside insurance, in turn, attracts ever larger inflows of speculative capital to the casino. This corrosive game has been underway ever since the Greenspan Fed panicked on Black Monday in October 1987 and flooded the stock market with liquidity. It is now such an endemic feature of Wall Street that it is falsely assumed to be the normal order of things. But, then, would anyone have been picking up nickels in front of the Volcker steamroller?

Ain’t that the truth…

• Homeowners: A New Class Of Fools (CNBC)

Owning a home isn’t just for suckers, as I stated in my CNBC column in November of last year; it’s creating a class of fools for those who do buy, because so many Americans continue to think home ownership is the passport to the so-called American dream. Headline news stories about rising interest rates and lack of supply are pushing people to make irrational decisions and, inevitably, finding themselves in the unenviable land of buyer’s remorse. And with a clear demographic shift, such as the millennial generation Kimberly and her peers find themselves in, the short-term and long-term prospects for the real estate sector are horrifically scary. 2014 was expected to be real estate’s Gatsby year. After promising sales numbers in 2012 and 2013, this was going to be the year we were going to hear how homeownership wasn’t just a stable investment, but also the gateway to American prosperity.

Sales and contracts jumped, including home values as reported from Case-Shiller. The former, however, is top-heavy as the most expensive properties are mostly selling; thus manipulating the data, as seen in the following chart from the National Association of Realtors: And with rates creeping higher this year, the feeling was those who were on the fence about buying were ready to make a commitment they most likely wouldn’t end until death. Hardly surprising, however, we haven’t seen that significant bump in real estate sales metrics, and the details behind the data suggest we’re on the cusp of another dramatic real-estate bust. Case in point is the data detailing housing starts — a key metric for new residential construction. Historically speaking, housing starts’ figures reach a yearly high in April and May because springtime in the country is typically its peak home buying period.

Yet, this year, despite a record-setting stock market and what some will argue is a significantly improved labor picture, we’ve seen a downward shift in housing. According to the U.S. Department of Housing and Urban Development, privately-owned housing starts in May dropped an unnerving 6.5% from a downwardly revised April reading. And single-family housing didn’t fare much better either, as starts fell by 5.9% against a lowered April print. This signals what is likely to be a brutal third and fourth quarter for the sector. As economist Karl “Chip” Case, the co-creator of the highly regarded S&P/Case-Shiller home price index, recently pointed out: “Every time [housing starts] have gotten below a million in the past, it’s come right back. Every time except the Great Recession.”

TEXT

• In Bizarro Market, Stocks Rise Along With Pessimism (MarketWatch)

Welcome to the Bizarro Market. This stock market reminds me of the great Seinfeld episode called “The Bizarro Jerry” when Jerry describes to Elaine the concept of the “Bizarro World,” an old Superman comic-book reference. The Bizarro World is the mirror opposite of the real world. “Up is down; down is up,” says Jerry. “[Superman] says ‘hello’ when he leaves, ‘goodbye’ when he arrives.” In the Bizarro Market, investors are actually leaving the stock market, even as stock prices keep recording new highs. In Bizarro Market, the post-financial-crisis economic recovery is so fragile after half a decade that the Fed is keeping its short-term interest rate target at a record low of near-zero to keep things afloat, even while the stock market roars like it’s 1999.

And in Bizarro Market, the bubble has few cheerleaders. Whatever bullish commentators exist are being drowned out by a constant barrage of media commentating and reportage making the case that stocks are way overvalued. The notion that the stock market is largely disconnected from the real economy is almost ubiquitous — self-evident even to people who know next to nothing about investing. And it’s hardly contrarian to be out making the case that stocks are in a bubble. A real contrarian in today’s environment would be arguing that the stock market is undervalued and has plenty of room to run. Even stock brokers and financial advisers desperate to lure new clients into stocks can only bring themselves to say that equities are probably fairly valued at best. And, still, the bull market charges on without even your token 10% correction.

Reminder.

• The Real Purpose Of The IMF (Eastwood)

To much trumpeting the IMF have kindly agreed to help out desperate and war torn Ukraine. How wonderful they are we are all meant to think, but the truth couldn’t be more opposite. The International Monetary Fund was set up in 1945, describing itself as an “organization of 188 countries, working to foster global monetary cooperation, secure financial stability, facilitate international trade, promote high employment and sustainable economic growth, and reduce poverty around the world.” This all sounds very laudable, but in reality the IMF has a very different purpose from that which is stated. If you look at the history of the IMF’s intervention in countries around the world you will see a trail of disaster and looting that repeats time and time again wherever they go. The many countries that are involved are supposed to have some influence but this is proportional to their financial clout, which in truth means that the USA has most of the control of what happens and many countries have effectively no say at all.

My opinion of the IMF, concurs with that of John Perkins, author of ‘Confessions Of An Economic Hitman’, his views being that of an insider in the system and mine merely as an observer. He succinctly points out that major western nations use financial warfare to get what they want and gain influence over other countries – the IMF being one of the tools with which they do this. Caribbean countries such as Jamaica have been destroyed by trade agreements and much the same thing has happened throughout Africa, South America and Asia at various times since world war II. What the IMF does is somewhat similar to a thug loan shark. The loan shark lends money to people who can’t afford to borrow so that the borrower ends up having to not eat to make the payments or face having broken legs.

“Customers are urged to pay off their home loans within 50 years … ” Translation: the problem has already gotten so out of hand the only “solution” is a crash. Therefore, it will come.

• Swedish Bankers in Talks on Joint Plan to Cut Mortgage Debt (Bloomberg)

Annika Falkengren, the chairman of the Swedish Bankers’ Association, is in talks with her members to target reducing mortgage debt. Falkengren, who is also chief executive officer of SEB AB (SEBA), is working on an industry-wide amortization plan to address growing indebtedness, she said yesterday in an interview. The goal is to set a standard that requires borrowers to cut mortgage debt to less than the 70% threshold of home values Swedish banks currently target, she said. “What we’re discussing at the bankers’ association is that we probably should have some kind of joint guidelines,” she said at SEB’s headquarters in Stockholm. “What we’re discussing now is very much amortization further down than 70%.” A joint approach will help ensure that banks don’t lose clients to competitors when taking a tougher stance on lending, Falkengren said.

Her warning follows the experiences of Sweden’s 2009 banking crisis in the Baltics, where a housing crash led to Europe’s steepest economic collapse. Back then, the lack of industry coordination aggravated the situation, Falkengren said. SEB’s decision years earlier to scale back in Latvia, Lithuania and Estonia initially resulted in lost market share as other banks continued to grow. Though SEB ultimately suffered smaller losses than Swedbank AB (SWEDA), the biggest Baltic lender, both firms incurred a surge in impairments. “We just lost a lot of market share – all clients went to other banks,” Falkengren said. “What we learned from the Baltic experience is that there’s no point in one bank starting to do something because this market is highly competitive and it’s easy to move your loan.”

At stake now is Sweden’s financial health. Household borrowing is at a record high with homeowners weighed down by debt equivalent to 370% of disposable incomes, the central bank estimates. Policy makers this month cut the benchmark repo rate by half a%age point to 0.25% to fight back the threat of deflation, making credit even cheaper. The latest borrowing data show credit growth accelerated to an annual pace of 5.3% in May. The industry needs to synchronize its moves because that’s how “you implement a new culture,” Falkengren said. “One participant doesn’t really change the way customers act.” SEB has already taken steps to limit client debt burdens. Customers are urged to pay off their home loans within 50 years and total borrowing is capped at five times household income. Only 4% of SEB’s client mortgages exceed 70% of home values, Falkengren said. The Swedish Financial Supervisory Authority estimates that 32% of homeowners nationwide had loans worth more than 75% of their properties at the end of last year.

• Japan Leads Global Volatility Decline to Seven-Year Low (Bloomberg)

Across global stock markets, nowhere is calm descending faster than in Japan. The Nikkei Stock Average Volatility Index, which tracks the cost of options on the Nikkei 225 Stock Average, tumbled 33% this year to 15.3 yesterday, the steepest decline among similar gauges tracked by Bloomberg worldwide. The measure touched 15.1 on July 8, the lowest in seven years. It climbed 4.5% last week, compared with surges of 17% on the benchmark U.S. volatility index and 25% in Europe. Japanese stocks have been aided by public institutions for more than a year. Unprecedented central-bank easing drove a 57% jump for the Nikkei 225 in 2013, and expectations for inflows from the nation’s biggest pension fund helped spur a 9.2% rebound from a May low. The gauge will climb another 7.9% by year-end, according to the average of 13 forecasts in a survey by Bloomberg News this month.

“There’s been an enormous rally in the Japanese market,” said Tim Schroeders, a portfolio manager who helps oversee $1 billion in equities at Pengana Capital Ltd. in Melbourne. “Risks over the direction of the yen, which could negatively affect the exporters, haven’t been priced in. Japan is on the right track but a lot of the stocks are probably priced to perfection.” The calm in Japan’s stock market is mirrored in sovereign-bond trading. Historical price volatility on Japanese government bonds slid to a record low of 0.647% on June 30, according to data compiled by Bloomberg going back to December 1994.

I feel for them.

• Empty Trading Floors Fray Traders’ Nerves (WSJ)

UBS’s trading floor in Stamford, Conn., once teemed with traders occupying a space equal to two football fields. The Guinness World Records recognized it as the biggest such facility on the planet. And the Swiss bank used it to showcase its Wall Street credentials. Stu Taylor, a former UBS managing director in trading who now runs trading-technology company Algomi Ltd., remembers when guests were brought around the gallery regularly. “It was very much a showpiece,” he said. Today, there are virtually no traders shouting into their phones or staring at terminals. UBS’s cavernous floor is taken up mostly by back-office, legal and technology staffers, according to people familiar with the bank. A spokeswoman for UBS said the trading floor was built for 1,400 traders, but wouldn’t disclose the number of employees at the facility.

A deep slump in trading activity in everything from stocks and bonds to currencies is changing the face of Wall Street. Businesses that once contributed disproportionately to the revenues of the world’s largest banks are now bleeding jobs and sparking fears of a permanent decline. Today’s markets are “boring,” said Thomas Thees, a former head of North American credit trading at Morgan Stanley and a former co-head of fixed income at Jefferies Group. “This is affecting the opportunity to make money, and ultimately the earnings these [trading] businesses can provide.” Global revenue from trading in fixed income, currencies and commodities, or FICC, dropped to $112 billion last year, down 16% from a year earlier and 23% from 2010, according to Boston Consulting Group. As big banks with large trading operations such as J.P. Morgan Chase, Goldman Sachs and Citigroup, report second-quarter earnings results this week, investors and analysts will be trying to find out whether the slowdown is a temporary funk or a lasting shift.

The forces arrayed against banks’ trading businesses are powerful. Since the financial crisis, regulators have limited their ability to take risks with their own money, and have made the process costlier, prompting many to dial back or push in different directions. At the same time, global markets have fallen into an unusually placid pattern that has damped clients’ desire to make trades. “It’s been absolutely dead,” said Jarrod Dean, a municipal-bond trader at Sierra Pacific Securities in Las Vegas. Municipal-bond trading volumes are down about 30% since last August, he said, while profits are down more than 70%.

Ha!

• Top 1% Is Even Richer Than Surveys Say (Bloomberg)

The oft-cited line that the top 1% of U.S. households lay claim to 30% of all wealth is probably an understatement, according to a European Central Bank working paper. Incorporating “missed” data on rich households pushes the share of wealth held by top earners up to between 35% and 37%, wrote Philip Vermeulen, a senior economist at the ECB. That’s higher than the 34% suggested by the 2010 U.S. Survey of Consumer Finances data from the Federal Reserve. “Our knowledge of the wealth distribution is less than perfect,” Vermeulen wrote. “The results clearly indicate that survey wealth estimates are very likely to underestimate wealth at the top.”

Richer households have a lower response rate to surveys measuring their assets, so holdings are undervalued, Vermeulen wrote. He uses data from Forbes billionaires lists in his analysis to provide new wealth distribution estimates for the U.S. and nine European nations. Though the U.S. change is “marginal,” the author writes, the effect in the Netherlands is much larger. Incorporating billionaires list pushes its concentration at the top to between 12% and 17% – close to nations such as Spain and Belgium – compared to the 9% concentration survey data would suggest.

Ha again!

• UK Execs Earn ‘180 Times’ Average Worker Pay (CNBC)

Executive pay has grown to almost 180 times that of the average worker, from 60 times, since the 1990s, according to a report by British think tank the High Pay Centre. The U.K. government needs to take more radical action to tackle the inequality gap by forcing firms to cap executive pay at a fixed multiple of their lowest paid employee, the High Pay Centre said in a report published Monday titled ‘Reform Agenda: How to make top pay fairer’. “It’s time to get serious about tackling the executive pay racket. The government’s tinkering won’t bring about a proper change in the U.K.’s pay culture,” said High Pay Centre director Deborah Hargreaves. “We need to build an economy where people are paid fair and sensible amounts of money for the work that they do and the incomes of the super-rich aren’t racing away from everybody else,” she added.

The report comes after 52% of shareholders in British fashion house Burberry last week voted not to support its remuneration report – a rare stand against excessively high salaries. The firm’s chief executive Christopher Bailey has a package worth up to £10 million a year. In October, regulations were introduced in the U.K. to force listed firms to give shareholders a binding vote on directors’ pay. Now over 50% of shareholders must approve a policy before it is passed. However, since rule changes were enforced, every vote at a FTSE 100 company has seen the majority of shareholders support the company policy on top pay, with the recent case of Burberry proving the exception.

Home › Forums › Debt Rattle Jul 15 2014: Janet Yellen Is A Religious Nutcase