Otto Dix The Triumph of Death 1934

https://twitter.com/real_EBS_/status/2083557271749959771?s=20

BREAKING: China’s Playbook for the Iran War.

— General Mike Flynn (@GenFlynn) August 2, 2026

China arms Iran while hollowing out America's supply chains. This is fifth-generation warfare (5GW) playing out in real time. Read this and understand what's at stake for our national sovereignty. https://t.co/Fi9hoLzFmP pic.twitter.com/8MPAKQPjmf

Thomas Sowell on the Clintons and Barack Obama:

— Thomas Sowell Daily (@DailySowell) August 2, 2026

“The Clintons had the saving grace of utter lack of principle—when they saw which way the political wind was blowing, that’s the way they’d go, regardless of what they’d been saying before.”

“[Obama] has been a far-left ideologue… pic.twitter.com/Tv3CLvxqDb

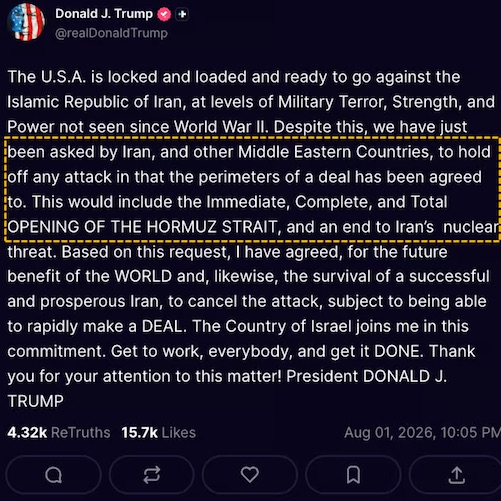

“When we talk we say ‘we’re talking’, if we’re not talking, when you ask me, ‘no we’re not talking’, I’ll say it. But we are talking right now, we’re talking, and we’re talking at the request of Iran..”

• Trump Says Iran Faces ‘Decapitation’ If It Doesn’t Sign A ‘Good’ Deal (ZH)

President Trump has told reporters in the Oval Office that the Iran conflict is “working out very well” and that this is Tehran’s “last chance to sign a good document”. On Hormuz, he said: “It has to be [free], I am not going to let them charge. If anybody is going to charge, we will charge, we are the ones … with a total control,” he said. “We have a thing called a blockade … No, no, there is not going to be charging. We are not talking about charging at all. There won’t be charging.”

*TRUMP: WANT TO GIVE IRAN LAST CHANCE BEFORE 'DECAPITATION'

— zerohedge (@zerohedge) August 3, 2026

… at 4:01pm on Friday

On engaging Iran in talks even while the Iranians themselves insist they will not participate in any new talks:“When we talk we say ‘we’re talking’, if we’re not talking, when you ask me, ‘no we’re not talking’, I’ll say it. But we are talking right now, we’re talking, and we’re talking at the request of Iran, backed by Saudi Arabia, backed by UAE, and backed by Qatar in particular, but others also, many countries called, many-the leaders of many, I’m friendly with a lot of them–This is a last chance, this is not something-if it doesn’t happen, this is a last chance for them to sign a… good document.”

BREAKING: Trump on Iran:

— Clash Report (@clashreport) August 3, 2026

This is their last chance to sign a good document. pic.twitter.com/sLD3HkQEV3Curiously, Trump is again insisting that when Iran says talks are off, they are lying…

Reporter: Talks with Iran are now off.

— Clash Report (@clashreport) August 3, 2026

Trump: They are going on right now. It's an amazing thing.

They are not denying it this time.

But for some reason, when they are talking, they don't like to say that they are talking. pic.twitter.com/m1slQoACy0Trump: Looking for Solution ‘Caused’ by Iran

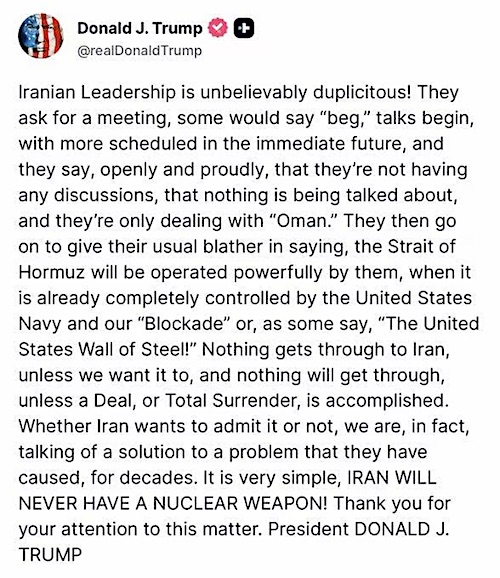

President Trump on Monday issued a new Truth Social, perhaps trying to explain his latest weekend TACO move, accusing Iran’s leadership of being “unbelievably duplicitous,” claiming Tehran privately sought and sheduled talks while publicly insisting it is only dealing with Oman. He asserted that the Strait of Hormuz is already “completely controlled by the United States Navy” through what he called the “United States Wall of Steel,” adding that “nothing gets through to Iran” unless Washington allows it. Trump also insisted discussions toward a resolution are underway despite Iranian denials, while reiterating his bottom line: “IRAN WILL NEVER HAVE A NUCLEAR WEAPON!”U.S. officials say that no novel negotiations are scheduled with Iran despite Trump’s statements, maintaining that ongoing talks are limited to indirect discussions via mediators involving envoy Steve Witkoff and Jared Kushner. – CBS. Trump is increasingly letting his frustration and ‘exasperation’ go public. This seems to only confirm that indeed there are no talks taking place at this point. The US president continues to insist that the whole crisis was “caused” by the Iranians “for decades” but that it is the US now looking for a “solution” – but Iran won’t play ball, after apparently ‘begging’ for talks…

Read more …

The US president said the sides are “talking of a solution to a problem” that Tehran have caused ..

• Trump Says US And Iran In Talks, Even If Tehran Denies It (TASS)

US President Donald Trump said that the United States and Iran are holding negotiations, even if Tehran does not publicly acknowledge it.”They ask for a meeting, some would say ‘beg’, talks begin, with more scheduled in the immediate future, and they say, openly and proudly, that they’re not having any discussions, that nothing is being talked about, and they’re only dealing with Oman,” he wrote on Truth Social. “Whether Iran wants to admit it or not, we are, in fact, talking of a solution to a problem that they have caused, for decades. It is very simple, IRAN WILL NEVER HAVE A NUCLEAR WEAPON!”Read more …

“Mine-clearing is Iran’s sole responsibility,” he claimed, meaning the mullahs want the mines to remain where they are and terrorize ships.”

• Iran’s Regime Demands Full Control of Strait of Hormuz (Catherine Salgado)

Just before the end of July, an official of the terrorist Iranian regime once again insisted that the current conflict cannot end until and unless the U.S. concedes the murderous mullahs full and uncontested control—and likely toll power—over the Strait of Hormuz.Read more …

It is very important to understand that no matter how many times the Iranian regime says it is willing to look at a proposal from the United States in order to put off major strikes, that doesn’t mean the regime ever changes its core demands. Nor will it ever do so, because the regime is run by fundamentalist Muslims who believe that by waging endless jihad against the United States, they are triggering the coming of their Islamic messiah, the Mahdi.Iranian Deputy Foreign Minister for Legal and International Affairs Kazem Gharibabadi gave an interview July 28 during which he laid out Iran’s demands. “We submitted a proposal to Oman regarding the Strait of Hormuz to establish a new lane that will be under Iranian control,” Gharibabadi said, according to a translation published on the Middle East Media Research Institute. “If this proposal is accepted, the strait will be opened; but if it is rejected, we are ready for a resumption of the fighting.”

U.S., of course, rejected the proposal. Despite what Gharibabadi said, Iranian forces have not succeeded in closing the strait to all commercial traffic, but they have made it impossible to get through the strait without the security that American troops are providing. And the Iranian strikes still occasionally hit or hinder ships.

Gharibabadi insisted, “The Strait of Hormuz will not revert to the pre-war arrangements, and this is the absolute policy of the [Iranian] regime.” He then griped about Americans trying to clear Iranian mines from the strait. “Mine-clearing is Iran’s sole responsibility,” he claimed, meaning the mullahs want the mines to remain where they are and terrorize ships.

Then Gharibabadi declared, “The Americans, in cooperation with Oman, created a southern transit lane within Omani territorial waters for ship traffic. Iran does not recognize this southern lane for even one hour, and the current round of fighting began precisely because of ships illegally passing through this lane.” Notice Gharibabadi fully admits the waters are Omani territory but still claims sovereignty over them. The Iranian regime is imperialist and lawless.

The ayatollahs aren’t interested in compromise. “The Omanis suggested planning a transit lane of which 50% would be under Iranian control and 50% under Omani control,” Gharibabadi noted. “We said that this does not dispel Iran’s apprehensions. Our demand is for complete Iranian control over the inbound lane and also over part of the outbound lane. If this proposal is rejected, no other proposal will be approved and the strait will remain closed.” That is, the terrorism will continue.

Stop debating the Islamist regime’s intentions. They’re clear: they want to kill all of us. Focus on capability. Its nuclear and war-making capabilities have been severely degraded. Now the Trump administration must finish the job and eliminate them.

— Mark Dubowitz (@mdubowitz) August 2, 2026For 47 years, Iranian terrorists have attacked Americans and spread jihad around the world. It’s time to finish the job.

The president sells access to his decisions. That won’t fly.

“The sudden strike call-off followed a week of threats that helped keep crude near $90 a barrel..”

• Truth Social Starts Selling Fast Access To Trump Posts (RT)

US President Donald Trump has teased new negotiations with Iran after abruptly calling off a major attack in a Truth Social post published on the same day that his media company began selling Wall Street firms millisecond-fast access to the platform’s market-moving content. Speaking to reporters aboard Air Force One on Sunday, Trump claimed that talks would begin on Monday and said several Middle Eastern governments had urged him to give diplomacy another chance.Read more …

“We’re just going to see whether or not we can make a deal,” Trump said, claiming that the canceled operation would have been the “biggest attack since World War II.”Last Monday, Trump claimed that “very friendly negotiations” with Tehran were already underway. Within days, however, the US had resumed bombing Iran, while Trump adopted increasingly aggressive rhetoric, promising to hit the country “very hard.”His administration declared US forces “locked and loaded” and prepared to unleash levels of military power not seen since World War II.US media reported on Friday that Washington and Israel were preparing an extensive campaign against Iranian power plants, refineries and other energy infrastructure.The threats, combined with continued disruption to shipping through the Strait of Hormuz, helped sustain fears of a wider energy shock and propelled crude prices toward $90 a barrel. On Saturday, Trump abruptly called off the strikes in a Truth Social post, claiming that Iran and several regional governments had agreed to the outlines of a deal that would reopen the Strait of Hormuz and address Tehran’s nuclear program.

The sudden reversal triggered another sharp market swing when Asian trading resumed on Monday morning. Brent crude fell by more than 7% at the open, while West Texas Intermediate dropped 6.7% to $78.98 a barrel. US stock-index futures rose as traders priced in a reduced risk of further escalation and disruption to Gulf energy supplies.

August 1 was also the launch date of Truth API, a paid service operated by Trump Media & Technology Group that provides institutional customers with a licensed, machine-readable feed of posts from influential Truth Social accounts. The service is aimed specifically at high-frequency and algorithmic trading firms and reportedly costs as much as $100,000 per month. Trump Media says paying customers receive posts within milliseconds of publication, while market specialists have argued that the direct feed allows well-equipped firms to process announcements and execute trades much faster than retail investors relying on the public website or app.

Trump’s posts are particularly valuable because he routinely uses Truth Social to announce abrupt changes involving wars, tariffs, individual companies and other policies capable of moving stocks, currencies and commodities. The AP noted that policy reversals can be especially lucrative for high-speed traders, who can profit from an initial threat that moves prices in one direction and then rapidly change their positions when Trump announces the opposite.

Iran has previously accused Trump of publicizing purported diplomatic breakthroughs to lower oil prices and buy time for further military action. The latest pause also follows an established pattern: Trump has repeatedly announced that strikes against Iran were being suspended to allow negotiations, only for military operations to resume after talks faltered or new attacks occurred. Tehran had not publicly confirmed that any new negotiations with the US were scheduled, and rejected Washington’s claim to a role in determining the future of the Strait of Hormuz.

Iranian Foreign Minister Abbas Araghchi said negotiations with Oman over the waterway’s management were “nearing completion,” while Foreign Ministry spokesman Esmaeil Baqaei described the discussions as a bilateral matter that “does not concern any other party.” Baqaei said Iran and Oman were negotiating a new shipping route that would replace the existing northern and southern routes. He stressed that any agreement “does not mean that the Strait of Hormuz will be opened or remain closed,” contradicting Trump’s claim that the proposed deal would provide for its “immediate, complete and total” reopening.

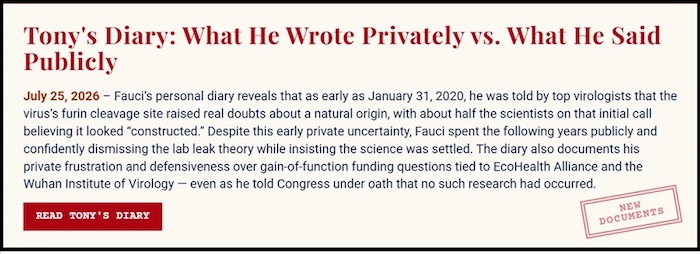

“We’ve been preparing all wrong for pandemics by imagining bureaucratic wizards will manage them best. ”

• Anthony Fauci, Our Own Wizard of Oz (Clarice Feldman)

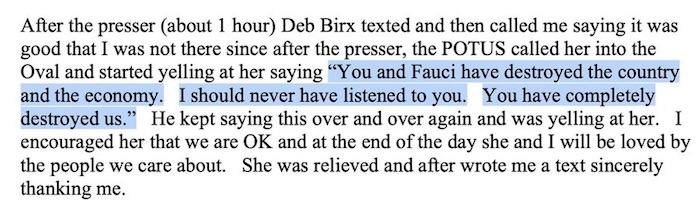

This week, the Senate Homeland Security Committee subpoenaed Dr. Anthony Fauci to testify. The committee secured extensive daily logs he had prepared while at NIH heading up the COVID-19 response. (The committee still lacks almost 700 pages of these logs, all of which had been secreted on 11 different government servers until retrieved by Secretary Robert F. Kennedy, Jr.)Read more …

The contrast between what he wrote in his hidden logs and his public statements was extreme. To take but one example, he admits in the log that the six-foot distancing rule was just something made up. Here’s a video compilation of him emphatically promoting that very rule as if there were some scientific basis for it. As a reminder of the failures of the Fauci response to the virus, here’s Toby Rogers in 2024 documenting them:

Every step was designed to inflict maximum harm:

— Toby Rogers (@uTobian) February 28, 2024

Splicing HIV into a coronavirus.

Blocking access to hcq and ivm.

Removing NAC from the shelves.

No early treatment.

Respirators that kill 90% of patients.

Seeding nursing homes with Covid+ patients.

Blanket DNR orders for the…By the end of the hearing, Fauci’s reputation, once burnished to a fine gleam by an adoring press, was vastly diminished:The Picture of Dorian Grey [sic] also comes to mind. Fauci guarded his reputation as a scientist just as Dorian guarded his seeming youth. To do so required a costly exchange. In both stories, the status of the soul (represented by the painting for Dorian) belies appearances. Nowhere could he have anticipated [snip] that he would be trapped in a chair in a Senate chamber, ashen and defeated, surrounded by silent lawyers, his accusers on all sides, pleading the 5th amendment 111 times. The wings completely melted. De profundis clamavi.

Classics professor Victor Davis Hanson sees the fall of Fauci as “a now all too familiar example of narcissistic and bureaucratic insiders who start with a classic rise only to fall into utter destruction.” He adds Fauci’s name to others like John Bolton, James Comey, and Jack Smith:Fueled by media flattery, and their over the top rhetoric, they posture as consummate “professionals.” These egomaniacs convince themselves they are our untouchable defenders of the established Washingtonian order, as supposedly sober and judicious custodians of the government. And when warned where they are ultimately headed, and to tread lightly, they instead interpret such sound advice as the jealousy of the envious.

In the current decade that arrogance is best manifested as crusading against public enemy number one, Donald J. Trump. So insidiously they up their Trump derangement rhetoric. They cite their titles and degrees as they vaingloriously skirt the law.

Finally drunk on leftwing media adulation, they delude themselves into believing that their megalomaniac behavior is exempt from any consequences. And then what? At the apex of their hubris, Nemesis strikes. And they fall hard by their own overweening arrogance. [snip] These unelected legends in their own minds confuse their enormous government granted powers at their disposal as bureaucrats with some sort of regal right that will exempt them from any consequences of their lawless arrogance.

And so soon they lie under oath to Congress, or call up Chinese generals to warn them about their own president, or sign patently false affidavits attesting that the Hunter Biden laptop was the work of the Ruskies, or tap senatorial phones—or almost anything that would ensure their inevitable fall from grace and utter humiliation. So too with the once celestial and now laughingstock Anthony Fauci (who once compared himself to Albert Einstein). The common denominator? The greater their arrogance, the harder they certainly fall.

You probably needn’t go back as far as Greek myth to explain what just happened. It’s as if Toto knocked over the screen and revealed that the Wizard of Oz was just a humbug. Dorothy could get back to Kansas only by tapping into her own potential. As Glinda the good witch said, “You had the power all along, dear.” And that’s the point Jeff Childers argues when he says we’ve been preparing all wrong for pandemics by imagining bureaucratic wizards will manage them best.

WHO, CDC and CMS, he argues, “framed pandemic response as a coordinated system with a ‘common operating picture.’ The whole world was enslaved to it. It all came from one delusional narcissist who was placed in charge.”Ours is a big and varied republic “fifty states, three thousand counties,” Childers reminds us.

Wherever some slight experimentation was allowed, individual states outperformed the baseline. Florida opened beaches and schools. Georgia reopened restaurants. Leftist fury ensued — “Georgia’s Experiment in Human Sacrifice” — but those states did better. We did not need them to be perfect. We needed them to be different. Difference is how science learns.

We’ve been preparing for pandemics all wrong. By anointing a single man to coordinate the world’s response, we instantly created a single point of failure. If that lone apex expert is conflicted, retarded, or worse, a malignant narcissist, then, well, we can all now see the result: The Fifth Amendment invoked for questions about tie colors.

In other words, what we needed most was room to conduct experiments. The CDC should have supported states and local governments trying different things, like ivermectin or hydroxychloroquine. There should have been no federal guidelines, no mandates, no vaccine incentives, no censorship, no indefinite shutdowns to flatten the curve.

Just give us the data. And maybe some money. Let us handle it.

“Do a lot of grown men keep diaries? Fauci’s own narcissism came back to haunt him.”

• Fauci’s Worst Nightmare Is Fauci! (James Zumwalt)

It was an interesting display of contempt for Senator Rand Paul exhibited by Anthony Fauci: having initially agreed to testify before the committee chaired by Paul only to change his mind, Fauci was hit with a subpoena. The main focus of the inquiry was Fauci’s public and private contrary views concerning the COVID-19 pandemic’s origin. Fauci refused to testify, claiming the Fifth Amendment—a plea which Paul reported to be invalid.Read more …

Paul opened the hearing with a list of reasons why a subpoena mandating Fauci’s testimony on the matter was warranted. He stated millions of American lives were lost due to COVID-19; that the American people had a right to know why dangerous research was funded by NIAID in a foreign country’s lab that lacked acceptable safety standards; and why Fauci steadfastly held to the public position the pandemic was not an accidental release from China’s Wuhan lab but a natural evolution. He did so while privately holding “a mountain of evidence” supporting the former—later even acknowledging it in his diary—over the latter.(Since Fauci’s pardon is inapplicable to state crimes, some states like Florida are exploring prosecution to get at the truth. While Fauci would obviously still take the Fifth, the pardon would not shield him from prosecution and accountability.)

In making his opening statement detailing his past testimonies, Fauci ended his comments with the following allegation: [G]iven Senator Paul’s obvious obsession with calling for my prosecution, his repeated slanderous comments about me, and recently his publicly releasing my unredacted personal diary aimed at embarrassing and intimidating me, the only conclusion I can reach is that the sole reason he is calling me before this Committee is to get me to say something, anything that could vindicate his repeated public pledges that I end up in his words, ‘Behind bars.’

[snip] [A]lthough it pains me to do so because of the respect I have for the legislative branch of government, and my decades-long record of cooperating with Congress, under the advice of my attorneys, I will invoke my right under the Fifth Amendment of the Constitution to refrain from answering your questions.

Fauci’s accusation was show rather than substance. He sought to hide the real reason for refusing to testify. But first, it is worth exploring the fate Fauci’s attorney, David Schertler, suffered during the hearing.

It had been made clear to Schertler he should not sit at the witness table with Fauci or in any way disrupt the hearing. However, he did sit with Fauci and later sought to speak. Paul’s repeated warnings to Schertler fell on deaf ears, and Paul finally ordered the attorney’s removal by security—an action many of those present applauded.

“Biden gave Hur a virtual confession, and Hur gave him a pass.”

• The Confession of Joe Biden (Turley)

For years, former President Joe Biden has fought to prevent the release of tapes acquired by former special counsel Robert Hur in his investigation. After those efforts collapsed this month, it became clear why Biden and his aides were so determined to keep the public from seeing the evidence. In addition to showing Biden’s mental diminution even before he was elected president, the tapes show that Biden effectively confessed to the crimes Hur would later excuse on the grounds of his mental infirmity.Read more …

Biden’s interviews with his biographer, Mark Zwonitzer, conducted four years before he would be elected president, show that Biden was already having trouble remembering names and dates. Hur was tasked with determining whether Biden had committed the same crimes that led later to charges against President Trump — retaining classified material, mishandling such material, and related crimes. It turns out that Biden had already admitted to these alleged crimes, years before the documents were found in various offices and the garage of his home.I wrote for years about Biden’s absurd denials after files were found in offices where he was working on his book. There was also evidence that the material had been divided, distributed, and transported between different locations. Despite all the evidence of knowledge and use of the classified materials, Biden and his aides suggested that no one had been aware of its removal and repeated transfer. In the meantime, after the raid on Mar-a-Lago to search for classified material removed by Trump, the Justice Department granted Biden and his team every possible accommodation.

Then came the searches of his home, with the pictures of files in his garage, office, and other locations. These included clearly marked classified material. Hur then issued his report, concluding that there was evidence of the crimes, but that he would still not charge Biden as Special Counsel Jack Smith had done with Trump. The report stated that “President Biden willfully retained and disclosed classified materials after his vice presidency when he was a private citizen.” It further stated that the clearly marked classified material was “stored in unsecure places” and posed a risk of “serious damage to America’s national security.”

For his part, Biden was defiant and, when confronted about the documents, insisted that “They’re mine,” and that other presidents had done what he did. This was the same president who condemned Trump for retaining classified information. Biden mocked Trump’s defense and asked CBS 60 Minutes how “anyone could be that irresponsible.”

We now know that Biden himself was that irresponsible, if not more so. Biden not only kept classified material longer and in even less secure locations, but he did nothing to protect the material as he attacked Trump over Mar-a-Lago. Nevertheless, Hur declared that he would not bring a single charge because Biden “would likely present himself to a jury, as he did in our interview of him, as a sympathetic, well-meaning elderly man with a poor memory.” The tapes show Biden struggling to give answers even before he announced his candidacy for the presidency, despite denials from key aides such as Jen Psaki and Karine Jean-Pierre.

However, Hur had actual tapes showing that Biden had clear memory and knowledge of his retention of classified material. Combined with Biden’s later public statements, the combination would have been deadly at trial. In the interview, Biden read “nearly verbatim” from notebooks containing sensitive national security and foreign policy information, according to Hur. On the tapes, Biden is heard saying, “So this was, I early on, um, in ’09 I just found all the classified stuff downstairs.” At another point, he states, “Some of this may be classified, so be careful with it.” He repeatedly mentions that some of the items in his office and home may be classified.

He even brags to his ghostwriter, in a report made on Oct. 10, 2016, that “I have extensive notes over this period of time … They didn’t know I have this.” Once again, the Justice Department had already declared and defended in court the idea that such removal and retention of classified material did constitute a federal crime by a president, let alone a vice president. Where Trump acknowledged his retention of classified material and agreed to security measures that the FBI requested, Biden did not inform anyone of his classified materials and kept them in his garage long after the Mar-a-Lago raids.

Meanwhile, in public, he expressed shock that any president would act as recklessly as Trump. It is hard to see how any of that would present “a sympathetic, well-meaning elderly man with a poor memory.” It sounds more like a cynical, shrewd politician with poor ethics. It also sounds like it would have been a strong foundation for a prosecution. For many, the tapes will reinforce the view of a two-tier legal system, long maintained by the Justice Department, whereby key Democratic figures including Hillary Clinton and Joe Biden were given favorable treatment while others were indicted for similar conduct.

What is truly galling for some of us is that Biden knew all of this when he went public to attack Hur for suggesting that he had knowingly retained classified material and showed diminished mental faculties— at one point forgetting when his son Beau died. Biden savaged Hur at the time for raising this issue, famously demanding, “How the hell dare he raise that?” Even that was a lie, because it was Biden who had raised Beau’s death in the interview.

After the report, Biden was still denying that he had retained classified material, even though he had discussed that classified material with his ghostwriter years earlier and had admitted as much to Hur. But before the public, Biden declared, “I’ve seen headlines since the report was released about my willful retention of documents. This assertion is not only misleading, it’s just plain wrong.”The record is now largely complete. So is the inescapable conclusion: Biden lacked clarity on most everything but his alleged crimes. His deception and culpability were established in both the Zwonitzer and Hur interviews. Biden gave Hur a virtual confession, and Hur gave him a pass.

“I underestimated how emotionally committed much of the press is to rallying around Anthony Fauci. His reputation is more important to them than anything. . .” —Matt Taibbi

No Matt, it’s about their own reputation..

• Everybody Knows (James Howard Kunstler)

The baleful afterburn of Dr. Fauci’s one-sentence testimony (“On the advice of counsel, I respectfully decline to answer. . . .”) seeps over the land like some ghastly pestilence now. You couldn’t have seen a more vivid demonstration of manifest evil than the master bureaucratic grifter formerly self-styled as “The Science” stonewall his way through that fateful reckoning in Sen. Rand Paul’s committee hearing last Wednesday.Read more …

The score so far: over a million dead in America from the Covid-19 virus that Dr. Fauci helped develop starting as far back as the 1990s, with Dr. Ralph Baric of the University of North Carolina. Tens of thousands left with serious, lasting injuries from the vaccines they promoted. The exact number of vaccine-connected deaths unknown because the public health agencies refused to report honestly on an operation that they caused to happen. There are whole legions of high officials and doctors behind Dr. Fauci now desperate to cover their asses.Along with the mendacious news media. HHS Sec’y Robert F. Kennedy, Jr. happened to be on Dana Bash’s CNN Sunday morning program. By the way, Dana Bash used to be married to one Jeremy Bash, Chief-of-Staff to CIA-Director Leon Panetta under Barack Obama. CNN lied consistently to the American people during the years of the Covid emergency. You have to wonder if CNN takes direction from the CIA, or maybe rogue elements in (or retired from) the agency. Sunday, Dana Bash went on offense against RFK,Jr.

Didn’t work. RFK, Jr. kept his cool. The harshest thing he said to Bash through all her hectoring was “you were part of the problem,” a startling understatement. Ms. Bash otherwise only wrecked herself, over-speaking her guest at every opportunity, pettifogging, and filibustering. Everybody could see what she was up to. Imagine how desperate CNN was to think that Dana Bash could bluster her way over Mr. Kennedy. He helped her expose herself as a tool.

The news media has been a very active co-conspirator in the Covid operation. You’d think Senator Paul might want to subpoena some network executives from CNN, CBS, NBC, MSNOW (especially), plus Executive Editor Joe Kahn of The New York Times (and his predecessor during Covid, Dean Baquet) to find out why they reported so much pure falsehood around the so-called pandemic. How did they happen to become the propaganda department for the Democratic Party, and what was the party’s interest in the Covid operation? D’unh. . . .

Everybody knows. Even the super-hyped-up cat ladies, nose-rings, NPR stars, and moiling transsters of the lefty-left know. They have kin and friends who either died on respirators with IV lines of remdesivir in their arms, or were gifted by the vaxx shots with turbo-cancer or myocarditis or neuromuscular disease or immune system failure or some mystery illness. They have been harmed even more than those of us who declined to get vaxxed. Sooner or later, that’s got to mean something.

As for Dr. Fauci’s motive in this huge fiasco. . . it’s got to be clear both from the record of his career — nicely reported in RFK,Jr’s 2021 book The Real Doctor Fauci — and from the 1000-plus-page personal diary he recorded on the HHS computers, that Fauci was doggedly in pursuit of glory. Glory! And that his personal holy grail was to find a “universal vaccine” that could defeat any virus, so as to be acclaimed by all mankind! Glory! Glory! Glory!

Given what is understood now about viruses and their interaction with vaccines — for instance, the flu vaccine which uniformly fails to adapt to annual virus mutations — that Dr. Fauci’s quest was quixotic, very basically foolish. All he ever produced, from the AZT wonder-drug for AIDS he developed back in 1986 (that probably killed as many people as died from the disease itself) to the Pfizer / Moderna mRNA shots for Covid in 2021 . . . all that frantic, questing “science” just ended up killing and harming the credulous in large numbers. The buttoned-up little fellow appears to be guilty of mass-murder on an epic scale.

Of course, he is presumed to be protected by the autopen-signed peremptory pardon he received from minions of “Joe Biden.” Perhaps Dr. Fauci’s invoking the Fifth Amendment under those circumstances will prompt an overdue look at just how this autopen thing really worked. In any case, Dr. Fauci is liable to be voted in contempt of Congress this week for not answering any questions put to him. The connected legal procedure will keep Dr. Fauci’s misdeeds under public scrutiny for at least months to come.

It’s also a fact that the autopen pardon does not shield him from charges brought in state courts. The AGs of Florida, Louisiana, Alabama have declared investigations. Louisiana and Missouri have already made Dr. Fauci sit for depositions, and now they can compare his answers with the entries from his diary. It is obvious that on countless occasions and on many vital issues, Dr. Fauci told the public one thing while he believed (and recorded) the opposite in his diary.

One question that the public badly wants Secretary RFK,jr. to answer: how come you haven’t pulled the mRNA Covid vaccines altogether? They don’t work and they harm people. Why are they even still available? Would such a move amount to an admission that the whole emergency was a fake and a failure? And that the government’s own public health agencies are culpable? Would the survivors of the 268-million Americans who got the shots be a little pissed-off? What, then?

The beginning of the end of open borders.

• Don’t Be Fooled, What’s Going On Is an Invasion of Spain (Rebecca Downs)

The consequences of “an ongoing invasion” from military-aged men into Spain played out in real time on Thursday, as Tony Kinnett covered on “The Tony Kinnett Cast.” Men were streaming past gates and into the Spanish territories of Ceuta and Melilla, which border Morocco. By Friday, blood was in the streets, while invaders were breaking off parts of gravesites to attack citizens and police. Cars were also on fire.Read more …

Kinnett spoke to how “thousands of military-aged men, not packs of desperate women and children, not the elderly, military-aged men… are streaming over the border into the country and… invading people’s homes in Spanish territory.” There was even footage of one man confirming he was under investigation for murder in Morocco, which contradicts claims that such individuals are seeking “economic opportunity” and “a better life.”“It’s not over,” Kinnett shared at the start of Friday’s broadcast, in light of claims many had returned to Morocco. “Now if there is an invasion that is over… usually you do not see people continuing to do the invading,” he added as men climbed over fences. Kinnett likened the invasion to the open borders under President Joe Biden. “Just one administration ago, you saw under Homeland Security Secretary Alejandro Mayorkas… the same kinds of mass migration into the country,” Kinnett reminded, about which Mayorkas couldn’t even be truthful.

President Donald Trump has called out the risks of unfettered immigration, while Democrats have been “insane,” Kinnett said.

The situation was so dire it necessitated leaders from Ceuta, on left and right, calling on Prime Minister Pedro Sánchez for assistance. When Sánchez “finally” addressed the situation on Thursday, he claimed that “the government of Spain is fully committed to providing an immediate response to the situation” and were “mobilizing all necessary resources, working with Moroccan and international authorities, and preparing the necessary measures to restore normalcy as soon as possible.”

Kinnett also noted Sánchez had previously defended open borders as “compassion” and “empathy.”As Kinnett pointed out on Friday, the prime minister “was heckled immediately” in Spain. On Friday, Sánchez “for the first time” acknowledged that “what has happened is an attack on Spain’s territorial integrity” and “deserves our most resounding and energetic condemnation.”

Kinnett noted it was “an interesting line” that Sánchez said “the government of Spain stands with the autonomous city,” with Ceuta being Spanish territory, given federal law still applies there. But he’s saying autonomous as though this is somehow some extra nicety that he’s laying around. Maybe, maybe the socialists have a point that really these territories should be ceded to Morocco.”

The situation in Spain has become so bad that European neighbors could ignore it no longer and have tightened borders. “As a result… it should be very clear here that other nations in Europe have responded by reinforcing their borders,” Kinnett said, despite how there is free travel between the European Union countries. This includes the leaders of Italy, Austria, and even France, “because of this migrant crisis.”

I find terrorism a strange complaint when you’re at war.

• Kiev’s ‘Terrorist Plague’ Spreading Across Europe – Russian Embassy (RT)

Ukraine’s “terrorist plague” is spreading across Europe, the Russian Embassy in Italy has claimed, accusing Kiev of orchestrating the deadly bombing of the Balzi Rossi restaurant in central Moscow. An improvised explosive device detonated outside the Italian restaurant on Kudrinskaya Square on Saturday evening after an unidentified woman allegedly attempted to carry it inside. The security guard who stopped her at the entrance was killed in the blast, along with the courier and at least three patrons attending a private event. Almost two dozen others were injured.Read more …

The National Antiterrorism Committee has not publicly identified any suspects or linked the attack to Ukraine, another state or any particular organization, while no group has claimed responsibility. In a statement on Sunday, the Russian Embassy in Italy claimed that the “bloody tentacles of Zelensky’s terrorist gang” had chosen Balzi Rossi partly to frighten foreigners working in Russia. It described the “Kiev regime” as “another emanation of Al-Qaeda and Islamic State” and accused Western officials who continue to fund and arm Ukraine of enabling terrorism.“It has now become completely clear that the explosion at the Balzi Rossi restaurant and other terrorist attacks in Russia, Monaco and elsewhere show that the Ukrainian terrorist plague is already spreading across Europe, and particularly Italy,” the embassy said.Moscow Mayor Sergey Sobyanin described the explosion as a “brutal terrorist act” and vowed that those responsible would be found and punished. Russian officials have not announced any arrests or disclosed a suspected motive, but the embassy’s allegations follow several previous bomb attacks for which Moscow explicitly blamed Ukrainian intelligence services.

Russian journalist Darya Dugina was killed in August 2022 after a bomb was planted in her vehicle. Russia’s Federal Security Service accused Ukrainian special services of organizing the assassination and identified Ukrainian national Natalya Vovk as the alleged perpetrator. According to the FSB, she fled to Estonia and has since vanished from public view. A bombing that killed military blogger Vladlen Tatarsky in St. Petersburg in April 2023 bore a more direct resemblance to the Balzi Rossi attack. Darya Trepova carried an explosive device disguised as a statuette into a café where Tatarsky was addressing an audience and presented it to him as a gift.

The device exploded shortly afterwards, killing Tatarsky and injuring dozens of people.= Russian investigators concluded that Trepova had acted on instructions from handlers in Ukraine. She maintained that she had been deceived and believed the statuette contained a listening device rather than a bomb, but a court convicted her of terrorism and sentenced her to 27 years in prison. Kiev never formally admitted involvement, but its former military intelligence chief, Kirill Budanov, later hinted that his agency was behind several high-profile killings inside Russia and promised to “keep killing Russians anywhere on the face of this world.”

Terrorism beyond Russia

The June 29 bombing in Monaco cited by the embassy also involved a woman allegedly recruited by a Ukrainian military intelligence network, according to Russian law enforcement sources. In that attack, a backpack containing an improvised explosive device packed with shrapnel was placed outside a residential building and detonated remotely, injuring Ukrainian businessman Vadim Ermolaev, his partner and her 13-year-old son.The suspected courier, Anastasia Berezovskaya, fled to Ukraine before Interpol issued a Red Notice for her arrest. She was later found shot dead and buried near Kiev. Ukrainian authorities detained two men in connection with her killing, including Vitaly Zhikovich, whom Russian law enforcement sources described as a serving colonel in Ukraine’s military intelligence agency. Recordings obtained by RT captured Zhikovich discussing plans to recruit unsuspecting civilians, including women and minors, to transport explosives, sometimes without knowing that they would be killed when the devices detonated.

A reminder that the US economy is not doing as bad as the likes of CNN want you to think.

• Manufacturing Index Reflects Continued Strong Growth – Highest in 4 Years (CTH)

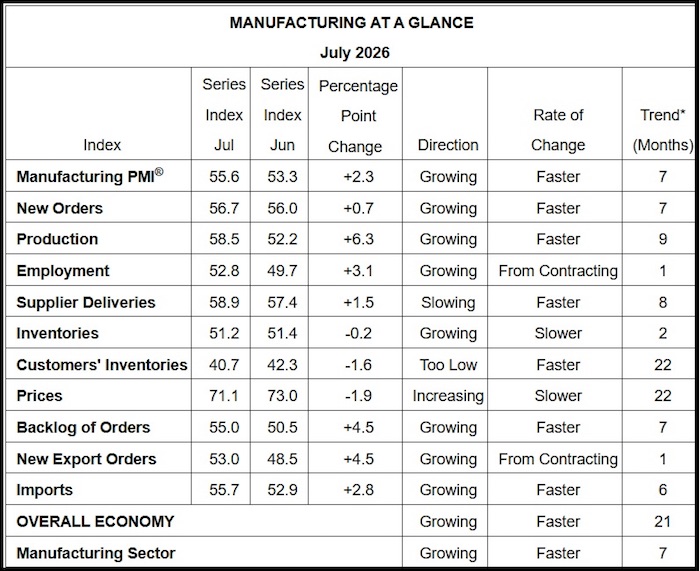

What we can take away from the Institute for Supply Management (ISM) index on manufacturing: overall, the U.S. manufacturing sector is continuing to expand significantly. The current index of 55.6 percent in July is 2.3 percentage points above the June figure and the highest reading since May 2022 (55.9 percent), when we were trying to recover from the COVID-19 shutdowns and supply chain problems.

PMI – The overall economy continued in expansion for the 21st month in a row. (A Manufacturing PMI® above 47.5 percent, over a period of time, generally indicates an expansion of the overall economy.) The New Orders Index expanded for the seventh consecutive month after four straight readings in contraction, registering 56.7 percent, up 0.7 percentage point compared to June’s figure of 56 percent.The July reading of the Production Index (58.5 percent) is 6.3 percentage points higher than the 52.2 percent recorded in June and the highest figure since November 2021 (60.5 percent). The Prices Index remained in expansion (or ‘increasing’ territory), registering 71.1 percent, a 1.9-percentage point decrease from June’s reading of 73 percent. The Backlog of Orders Index registered 55 percent, up 4.5 percentage points compared to the 50.5 percent recorded in June.

The Employment Index reading of 52.8 percent is up 3.1 percentage points from June’s figure of 49.7 percent, putting the index in expansion territory for the first time in 33 months.” (source)All that data and a couple of bucks will buy you a cup of coffee, but here’s what it means in common speak. Overall, companies wanting to make products in the United States are expanding the manufacturing sector. However, they are running into a problem when trying to source the component goods and/or raw materials. The resource goods they need are constantly in a status of flux and the prices are unstable.

For large companies their supply chain management can deal with the short inventory issue through various sourcing networks using multiple suppliers. However, for smaller companies this is frustrating. The manufacturing system is a network of complex suppliers who make component materials needed for the core product. In order to get really successful, the smaller manufacturing component goods need to start up inside the USA just like the larger companies who are producing a finished product.

This is why even during a manufacturing surge we end up importing a lot of goods on the front end of the transition. Absent a domestic supplier, industrial component products are heavily imported in order to manufacture the finished durable good.

It takes time, well, technically its never been tried – so, no one is sure, but it takes time for all of the component manufacturing to establish inside the USA in order to feed the component parts to the various manufacturers who depend on the sub-sourcing. This is the period we are in at the moment, and prices are fluctuating as people try to get their arms around costs here and abroad.

The 15 manufacturing industries reporting growth in July — listed in order — are: Printing & Related Support Activities; Apparel, Leather & Allied Products; Electrical Equipment, Appliances & Components; Primary Metals; Nonmetallic Mineral Products; Transportation Equipment; Miscellaneous Manufacturing; Textile Mills; Machinery; Computer & Electronic Products; Food, Beverage & Tobacco Products; Wood Products; Plastics & Rubber Products; Furniture & Related Products; and Fabricated Metal Products. The only industry in contraction was Chemical Products.

[…] Commodities Up in Price Acrylonitrile Butadiene Styrene (ABS); Aluminum* (32); Copper (13); Corn; Corrugated Products (4); Electrical Components (2); Electronic Components (7); Freight (5); Fuel* (5); Integrated Circuits; Memory Components (5); Metal Products (4); Ocean Freight (3); Oil Based Products (4); Paper Products (4); Plastic Based Products (4); Plastics (5); Printed Circuit Boards; Resin Based Products; Resins (6); Semiconductors (2); Soybean Meal; Steel (9); Steel — Cold Rolled; Steel — Hot Rolled (7); Steel — Stainless (6); Steel Products (8); and Sulfur Products (4).

Commodities Down in Price Aluminum*(2); Fuel* (2); and Polypropylene Resin (2).

Commodities in Short Supply Aluminum; Copper; Electrical Components (13); Electronic Components (17); Integrated Circuits; Memory (7); Oil Based Products; Printed Circuit Boards; Rare Earth Components; Semiconductors (5); Steel; Steel — Hot Rolled (2); and Tungsten Products.

The blue-collar jobs are expanding significantly. There is massive upward pressure on wages for blue collar workers as the manufacturing sector continues to expand.

It’s Warren Buffett’s idea, and he wasn’t the first either.

• Javier Milei Just Proposed a Great Idea (Anderson)

Javier Milei has done great things for Argentina — and honestly, the entire region — and will continue to do so, but I have to admit that his latest proposal left me weak in the knees. He’s calling it the grillete fiscal or the “fiscal shackle,” and it’s part of a larger reform of the Central Bank’s charter that he’s sending to the country’s Congress, possibly for a mid-to-late-August vote.Read more …

I said we would achieve a fiscal balance in our first year in office, and we achieved it in the first month. Today, we can say that we lifted fourteen million Argentines out of poverty.

— Milei in English – Official Account (@jmilei_english) August 1, 2026

LONG LIVE FREEDOM, DAMN IT…!!! pic.twitter.com/7CYUTZcezE

Essentially, if the Argentine national government runs a fiscal deficit for several months in a row, the Congress receives a warning that it has a matter of weeks to fix it. If it doesn’t hit the deadline, the “shackle” activates automatically, and the political class will be the ones impacted. Here’s what happens:

1. Non-essential government functions are suspended (hello, government shutdown).

2. All new spending is frozen and will not be authorized until the problem is resolved.

3. No new contracts can be awarded.

4. No new public-sector employees can be hired.

5. Discretionary transfers to the provinces are halted.

And last but not least, the best part:

6. The salaries of the top politicians stop completely. The vice president, ministers, secretaries, undersecretaries, national senators, national deputies, and even El presidente himself will not receive a dime of taxpayer money until they solve the problem.

Of course, essential services will remain protected. “For the first time in our history, if politics doesn’t do its homework, politics will pay the cost — not the people,” Milei said during a national broadcast last week, during which he introduced the proposal. My question is why the heck isn’t every national government in the world doing this? More specifically, my question is why doesn’t the United States do this? (I know the answer.)

We do have our fair share of government shutdowns when Congress can’t get its act together, but the everyday people who work for the federal government are the ones who suffer and are often furloughed without pay, while those same members of Congress continue to receive their salaries.

Now, I will point out that in May of this year, Sen. John Kennedy (R-La.) sponsored a resolution that would make it so that our senators are not paid in the case of a government shutdown. It had bipartisan support and was unanimously approved. It states that these senators’ salaries are withheld and released once a shutdown ends. That will take effect the day after the November 2026 elections and only applies to the Senate, not the House.

While that’s progress, it looks weak compared to what Milei has proposed. Now, his biggest hurdle is getting these legislators whom it impacts to actually vote for it. Milei’s La Libertad Avanza party has the largest bloc in the Chamber of Deputies after the 2025 midterms, but it doesn’t have an outright majority. It’s ambitious, but it’s not impossible, and if it does pass, I hope the U.S. will take note, though I’m not holding my breath.

https://twitter.com/EricLDaugh/status/2083927432017420393?s=20 https://twitter.com/EricLDaugh/status/2083984910260294133?s=20NVIDIA CEO Jensen Huang: Elon Musk is in a phenomenal position to lead the future of AI, autonomous vehicles, and humanoid robotics.

— DogeDesigner (@cb_doge) August 2, 2026

“Collecting world data is very expensive, and Elon has a great advantage because, number one, his AI factory for his cars is fantastic, has a lot… pic.twitter.com/yLOi6319YV

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.

Russian Foreign Ministry Ambassador-at-Large Rodion Miroshnik

Russian Foreign Ministry Ambassador-at-Large Rodion Miroshnik

Victoria Taft/AI

Victoria Taft/AI

Lodovico Carracci St. Sebastian Thrown into the Cloaca Maxima

Lodovico Carracci St. Sebastian Thrown into the Cloaca Maxima

President Donald Trump, pictured in the Oval Office on July 21, during a meeting with the President of Lebanon

President Donald Trump, pictured in the Oval Office on July 21, during a meeting with the President of Lebanon Construction on President Donald Trump’s White House ballroom is seen on July 14. Daniel Heuer/Bloomberg/Getty Images

Construction on President Donald Trump’s White House ballroom is seen on July 14. Daniel Heuer/Bloomberg/Getty Images

New British Defence Secretary Wes Streeting

New British Defence Secretary Wes Streeting