Harris & Ewing “Shirley Temple told President Roosevelt about losing a tooth last night” June 24, 1938

When I look at this Bloomberg quote:

The singling out of three debt types most at risk by the People’s Bank of China has prompted Nomura Holdings Inc. to warn that rising borrowing costs will make it even harder to avoid a default by these issuers. The PBOC will enhance monitoring of local government financing vehicles, industries with overcapacity and property developers to prevent default risks from spreading, according to its fourth-quarter policy report issued on Feb. 8.

Jinzhou Economic Technology Zone Development, an LGFV in Liaoning province, sold new seven-year bonds at 9.1% in January, while Guangxi Nonferrous Metal issued nine-month bills at 8.5%. That’s almost twice as high as the yield on 2021 government debt. “The three industries singled out by the PBOC are the most likely to have defaults this year,” Nomura economist Zhang Zhiwei said. “Individual LGFV defaults will happen this year, but are unlikely to lead to a systemic financial crisis as the central government is expected to intervene.”

And combine it with this one (also Bloomberg):

Shares of China’s biggest listed coal producers have dropped to their lowest valuations on record as falling fuel prices make it harder to repay debt. Slowing economic growth and efforts to boost use of alternative fuels have dragged down coal prices in China, the world’s biggest producer and consumer of the fuel. The nation’s banking regulator ordered its regional offices to increase scrutiny of credit risks in the coal-mining industry,[..] signaling government concern about possible defaults.

And include this graph:

Plus one more quote:

China’s coal industry is “dead,” said Laban Yu, a Jefferies Group analyst with an underperform rating on all three stocks. “There are 10,000 producers in China. A lot of them are taking on debt. It gets harder and harder to service debts when coal prices keep falling.”

I’m thinking: Uh-oh ….!

China’s coal industry is already in pretty extreme trouble, and that’s before borrowing costs are expected to rise. While prices are falling. And of course you may argue that it’s good if China moves away from coal, but that doesn’t mean an industry collapse is the way to go. And people may repeat ad nauseum that “the central government is expected to intervene”, but there are some serious issues with that idea.

Remember, the People’s Bank of China has announced it will focus on “1) local government financing vehicles, 2) industries with overcapacity and 3) property developers”. So what is Beijing expected to do? Bail out 10,000 coal producers? No, because there would seem to be overcapacity. So they would need to close down plants, lots of them, merge many others, and then grant subsidies to guarantee low borrowing costs for who’s left standing.

But it can’t do that without handing similar – or better – subsidies to cleaner energy producers, since cleaner is a major policy point. And it would need to organize transport facilities for the longer trek the coal would require to reach clients. Or perhaps Beijing can artificially raise coal prices. China’s economy needs coal desperately, after all, even as Beijing, the city, may well be the world’s smog capital. This is not as easy as it may seem at first glance.

And that’s all still presuming that the Communist Party leadership actually – still- has the power to intervene. Something I’ve questioned on numerous occasions recently. Because of the surging shadow banking system, which at $6 trillion, or 69% of GDP, has become a major economic and therefore political factor. Limiting that power is another one of the CCP’s goals going forward. That and “1) local government financing vehicles, 2) industries with overcapacity and 3) property developers”. Nice and lofty goals one and all. But.

The shadow banks are heavily involved in all three of those “sectors”. That means that whatever Beijing decides to do about its – overcapacity – “dead” coal industry, chances are it will reinforce the power of the shadow banks. Subsidies for coal and other forms of energy will mean subsidies for shadow banks.

As for local government financing vehicles (LGFVs), while some may say and think that they’re under strict central control, it’s exactly that sort of control that has driven local governments into the hands of the shadows. For the longest time, local leaders were judged on numbers of bridges and highways built, not on financial caution. They got credit from wherever they could get it. So if the CCP wants to bail out their debts, which could, to put it mildly, surprise to the upside, it will fork over money/credit to the shadow banks. And forking over money will mean, once you get to the bottom line, forking over power.

Number three in that list: property developers. We can all figure out, just intuitively, how much of the capital that allowed the X million empty apartments and bridges to nowhere to be built was provided by shadow banks, and their wealth management products and other investment vehicles. Beijing, in its ecstasy over seeing China become a global economic power, and its own standing being enhanced in the process, ignored what went on in its own backyard, and was even blind to it, since it didn’t recognize what went on.

The leadership greatly enjoyed the newfound wealth and glory, but never understood how it was built, what was needed to achieve it. That’s not so strange, since those who rose through the party ranks did so in times when China was still an economic backwater, and a – more or less – fully centralized, simple system. What they never knew, and how could they, was that, as someone pointed out recently, complex systems need a degree of individual freedom to function. And to get where it is today, China had to become such a complex system. And its ruling party was never, and still isn’t, ready for the transition from a simple to a complex system.

And there is no way to avoid it: this adds up to a scary situation. And I don’t think that’s necessarily because China might attack Japan or some other country. Not for the reasons you might think, however, but because Beijing would now need to cooperation, if not the permission, of the shadow banks to embark on any such adventure. And going to war would seem to be the proverbial step too far for the shadow banks, in the exact same way, and for the exact same reasons, that the new capitalist riches have proved to be for the Communist Party. All things must come to pass.

What’s scary is not China’s threat outside of its borders, but the one inside. Whatever it is Beijing would desire to do to curb financial risk, insane leverage levels and upcoming debt defaults, whether it’s in energy industries, like coal, or empty apartments and bridges, or bloated local governments, it would be making the shadow banking system stronger. If it would insist on trying to avoid doing that, it risks an overall economic plunge, because, when it wasn’t paying attention, an increasingly large part of the recent domestic growth was financed from the shadows.

Can they just simply merge the two, the Communist Party and the shadow banks? It seems very unlikely, since they move to entirely different beats. What makes one strong, weakens the other. You can’t control a global economic power along the same set of ideals and principles Mao used to build up the Communist Party. It’s one or the other.

Lawrence Vance evokes Jefferson and Smedley Butler in a good piece. Putting Ron Paul on the same level as those two will always make me wonder.

• How To Dismantle the American Empire (Mises.org)

Can U.S. foreign policy be fixed? Although I am not very optimistic that it will be, I am more than confident that it can be. I propose a four-pronged solution from the following perspectives: Founding Fathers, military, congressional, libertarian. In brief, to fix its foreign policy the United States should implement a Jeffersonian foreign policy, adopt Major General Smedley Butler’s Amendment for Peace, follow the advice of Congressman Ron Paul, and do it all within the libertarian framework of philosopher Murray Rothbard.

Thomas Jefferson, our first secretary of state and third president, favored a foreign policy of “peace, commerce, and honest friendship with all nations — entangling alliances with none.” This policy was basically followed until the Spanish-American War of 1898. Here is the simple but profound wisdom of Jefferson:

• “No one nation has a right to sit in judgment over another.”

• “We wish not to meddle with the internal affairs of any country, nor with the general affairs of Europe.”

• “I am for free commerce with all nations, political connection with none, and little or no diplomatic establishment.”

• “We have produced proofs, from the most enlightened and approved writers on the subject, that a neutral nation must, in all things relating to the war, observe an exact impartiality towards the parties.”

No judgment, no meddling, no political connection, and no partiality: this is a Jeffersonian foreign policy.

U.S. Marine Corps Major General Smedley Butler was the most decorated Marine in U.S. history. After leaving the military, he authored the classic work War Is a Racket. Butler proposed an Amendment for Peace to provide an “absolute guarantee to the women of America that their loved ones never would be sent overseas to be needlessly shot down in European or Asiatic or African wars that are no concern of our people.” Here are its three planks:

1. The removal of members of the land armed forces from within the continental limits of the United States and the Panama Canal Zone for any cause whatsoever is hereby prohibited.

2. The vessels of the United States Navy, or of the other branches of the armed services, are hereby prohibited from steaming, for any reason whatsoever except on an errand of mercy, more than five hundred miles from our coast.

3. Aircraft of the Army, Navy and Marine Corps is hereby prohibited from flying, for any reason whatsoever, more than seven hundred and fifty miles beyond the coast of the United States.

Butler also reasoned that because of “our geographical position, it is all but impossible for any foreign power to muster, transport and land sufficient troops on our shores for a successful invasion.” In this he was echoing Jefferson, who recognized that geography was one of the great advantages of the United States: “At such a distance from Europe and with such an ocean between us, we hope to meddle little in its quarrels or combinations. Its peace and its commerce are what we shall court.” [..]

The U.S. global empire with its 1,000 foreign military bases and half a million troops and mercenary contractors in three-fourths of the world’s countries must be dismantled. This along with the empire’s spies, covert operations, foreign aid, gargantuan military budgets, abuse and misuse of the military, prison camps, torture, extraordinary renditions, assassinations, nation building, spreading democracy at the point of a gun, jingoism, regime changes, military alliances, security guarantees, and meddling in the affairs of other countries.

U.S. foreign policy can be fixed. The United States would never tolerate another country building a string of bases around North America, stationing thousands of its troops on our soil, enforcing a no-fly zone over American territory, or sending their fleets to patrol off our coasts. How much longer will other countries tolerate these actions by the United States? We have already experienced blowback from the Muslim world for our foreign policy. And how much longer can the United States afford to maintain its empire?

It is time for the world’s policeman, fireman, security guard, social worker, and busybody to announce its retirement.

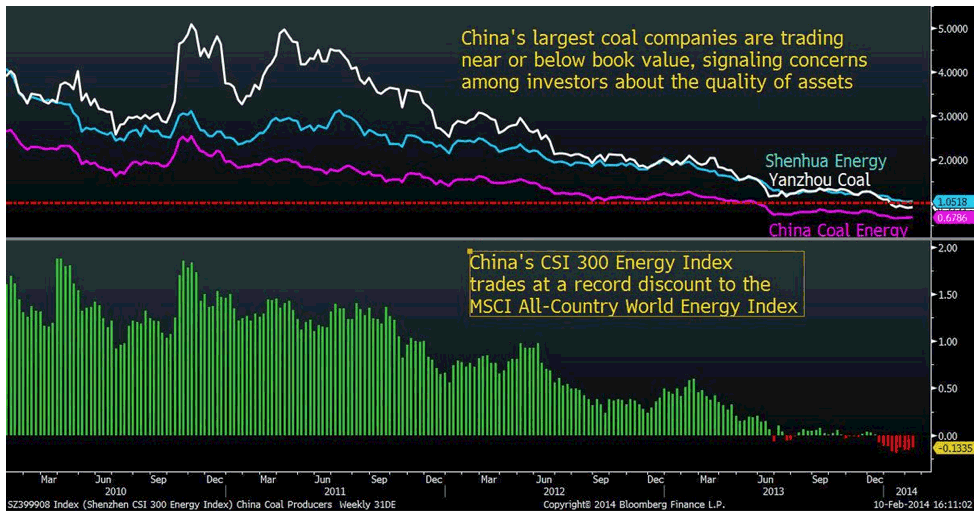

• China’s coal industry is “dead” (Bloomberg)

Shares of China’s biggest listed coal producers have dropped to their lowest valuations on record as falling fuel prices make it harder to repay debt.

The CHART OF THE DAY tracks the price-to-book ratio of China Shenhua Energy Co., China Coal Energy Co. and Yanzhou Coal Mining Co. Both China Coal and Yanzhou Coal trade below the value of their net assets, while Shenhua Energy has fallen to about 1 times book. The lower panel shows the CSI 300 Index’s energy gauge traded at a record discount to the MSCI All-Country World Energy Index last month.

Slowing economic growth and efforts to boost use of alternative fuels have dragged down coal prices in China, the world’s biggest producer and consumer of the fuel. The nation’s banking regulator ordered its regional offices to increase scrutiny of credit risks in the coal-mining industry, two people with knowledge of the matter said last month, signaling government concern about possible defaults.

China’s coal industry is “dead,” said Laban Yu, a Jefferies Group LLC analyst in Hong Kong with an underperform rating on all three stocks. “There are 10,000 producers in China. A lot of them are taking on debt. It gets harder and harder to service debts when coal prices keep falling.”

The world economy is going to undergo a major reboot. Emerging markets have used the boost provided by western stimulus to go way beyond their “natural” status, and must now come down. If you ask me, they should simply forget about the globalized rat race, and take care of their own people. But for many that would mean a change in both leadership and idea(l)s.

• Emerging-Market Sharks Circle Reserves in Rapid Dive (Bloomberg)

Foreign-exchange reserves are emerging as the latest battleground between traders and developing nations trying to stem the worst rout in their currencies since 2008. Nations with the least reserves to fend off currency speculators will continue to see their exchange rates under pressure, prices of options show. Of the 31 major currencies tracked by Bloomberg, the four traders are most bearish on are Argentina’s peso, Turkey’s lira, Indonesia’s rupiah and South Africa’s rand, while the forwards market signals that Ukraine’s hryvnia will fall 20% in a year.

“If you start to burn too quickly through your foreign reserves, it’s an ominous sign — and of course in the forex market, they smell blood,” Robbert Van Batenburg, the director of market strategy at broker Newedge Group SA in New York, said Feb. 5 by phone. “It creates this domino effect.”

From Argentina to Turkey, emerging markets are under siege as the U.S. Federal Reserve pares its record stimulus measures and reports showing a slowdown in Chinese manufacturing raise concerns about the strength of their economies. A Bloomberg index tracking 20 exchange rates has fallen 2.1% this year, building upon the 7% decline in 2013.

Turkey spent 27% of its foreign reserves trying and failing to defend its currency since June, leaving it with $34 billion as of Feb. 10, excluding commercial banks’ deposits. That’s only enough to cover 0.29% of short-term debt, the least among 14 developing nations tracked by Goldman Sachs Group Inc. South Africa’s $46 billion amounts to 13% of gross domestic product, less than the 18% it needs to finance its trade deficit and debt, according to the U.S. bank. The lira fell to a record 2.39 per dollar and the rand tumbled to a more than five-year low of 11.3909 last month.

“Burning through their reserves, that’s not sustainable,” Viktor Szabo, a money manager in London at Aberdeen Asset Management Ltd., which oversees $10 billion, said by phone on Feb. 6. “People will be more than happy to short your currencies,” he said, referring to a strategy of betting against an asset. “The pressure was there and there’ll be more pressure.”

Do you ever get the idea that finance has become far too big in our lives? If so, step out. But really, not halfway, that won’t work.

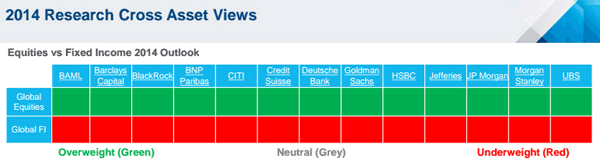

• Animal Spirits Deflating (Tim Price via Zero Hedge)

[The following table] shows the recommended positioning of Wall Street’s finest with regard to bond markets and equities. (This exercise may well show that when everyone is thinking the same, nobody is really thinking at all.)

As far as the sell side was concerned, brash individualism and bold contrarianism died some time during 2013. By the start of 2014, all that remained on Wall Street was the hive mind of the Borg – a rather bland consensus that bonds were bad and equities were good. Astonishing that stockbrokers might possibly nurse such bias. So January’s primary trends (bonds rallying, and equities tanking), if sustained, may serve to remind us all that unsolicited sell side research, being to all intents and purposes free, is worth precisely what folk pay for it.

If the last investor is already loaded up to the gills on stocks, where is the greater fool to whom those stocks can then be sold? January may have given us an answer. Pimco’s Bill Gross comes to a similar conclusion in his latest investment outlook, from which the following is taken:

..be “careful.” Bull markets are either caused by or accompanied by credit expansion. With credit growth slowing due in part to lower government deficits, and QE now tapering which will slow velocity, the U.S. and other similarly credit-based economies may find that future growth is not as robust as the IMF and other model-driven forecasters might assume. Perhaps the whisper word of “deflation” at Davos these past few weeks was a reflection of that. If so, high quality bonds will continue to be well bid and risk assets may lose some lustre.

Astonishing, too, that the world’s largest bond manager might possibly nurse such bias in favour of “high quality bonds”. Especially when they’re not (high quality, that is) – there just happen to be oodles of them. But the fact remains that investors seem to have been spooked by the final arrival of Fed tapering, and those in emerging markets doubly so. But since we’re all trapped in what James Grant calls that valuation ‘hall of mirrors’, courtesy of central banks endlessly tinkering with asset prices via the most aggressive monetary stimulus in world history, it’s not remotely easy trying to foresee the outlook for either bonds, or stocks, or anything else. Rather than just abandon the field and sit disgruntled on the sidelines in cash, our response is to seek solace in the most compelling examples of deep value we can find, both in the credit market and in stocks.

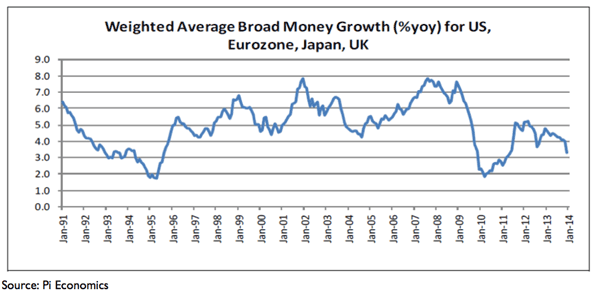

Tim Lee of Pi Economics also sees evidence of a growing deflation shock. His chart below shows that a proxy for global broad money growth (a simple weighted average of money growth rates for the US, the Eurozone, the UK and Japan) peaked in 2011 and now appears to be rolling over.

Tim Lee believes it is “quite obvious” what the Fed will ultimately do:

They will expand their balance sheet dramatically further by doing QE in outright risk assets – junk debt, equities, etc. They will swap money for risk assets, not money for safe assets.

The problem is that this would be a very big step; a further violation of the ‘rules’ of central banking. And we have a new Fed chairman, who has only just taken office. It is likely that things will have to get very bad before that very big step can be taken.

Six years into this crisis, and in the words of Lily Tomlin, things are going to get a lot worse before they get worse. From our perspective as asset managers, it comes down to a simple mantra: continually question precisely what you own, and why you own it.

I’ve said it before, Abenomics will be judged post April Fools day. That’s 7 weeks away, and it already looks plenty frightening. Deflation has been sort of mild on Japan over the past 20 years. But that may not last. So what will 2014 bring with both China and Japan threatening to be in big trouble?

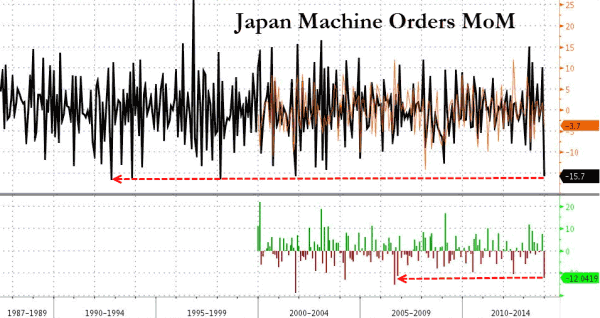

• Japan Machine Orders Crumble At Fastest Pace In 22 Years (Zero Hedge)

If you needed another reason to buy stocks, trust in the growth meme, and have your faith in Abenomics confirmed… look away. Japanese Machine orders for December just printed -15.7% in December – the biggest MoM plunge since 1992. This is the biggest miss to expectations since 2006 and what is considerably more problematic for Abe et al. is that YoY expectations of a core machine order rise of 17.4% was hopelessly missed with a small 6.7% gain (and this is data that excludes more volatile orders).

As Bloomberg notes, core machine orders are an indicator of future capital expenditure and it seems, just as in the US, that thanks to “stocks” now being considered central bank policy tools that capex no longer means productive capital use… it means buybacks, dividends, and shareholder recaps in any which way we can. How was the weather in Japan in December?

But while collapsing machine orders are “completely irrelevant”, even if a plunge of this magnitude usually portends a recession, what should be far more troubling to the Kool aid addicts is if the BOJ were to announce that just like the Fed, it too is tapering its Open-ended QE ambitions. Considering this is precisely what BOJ board member Kiuchi just did, that relentless USDJPY meltup overnight may not be such a slamdunk. From Market News…

Bank of Japan board member Takahide Kiuchi, who is against a rigid two-year timeframe for achieving 2% inflation, said side-effects of an additional easing would be bigger than its positive effects if the economy were deviating only slightly downward from the BOJ’s recovery scenario, the Nikkei reported. Kiuchi, a former Nomura Securities economist, told the daily in an interview that it is difficult to predict how much a further easing would push up consumer prices, and that wages should rise in line with price gains.

He also said the BOJ “should make a cautious decision as to whether to continue or scale back” the current aggressive easing at the end of the target period to hit stable 2% inflation in about two years from April 2013.

• PBOC Singling Out Industries Fuels Nomura Anxiety (Bloomberg)

The singling out of three debt types most at risk by the People’s Bank of China has prompted Nomura Holdings Inc. to warn that rising borrowing costs will make it even harder to avoid a default by these issuers.

The PBOC will enhance monitoring of local government financing vehicles, industries with overcapacity and property developers to prevent default risks from spreading, according to its fourth-quarter policy report issued on Feb. 8. Jinzhou Economic Technology Zone Development Group Co., an LGFV in Liaoning province, sold new seven-year bonds at 9.1% in January, while Guangxi Nonferrous Metal Group Co. issued nine-month bills at 8.5%. That’s almost twice as high as the yield on 2021 government debt.

“The three industries singled out by the PBOC are the most likely to have defaults this year,” Zhang Zhiwei, Nomura’s Hong Kong-based chief China economist, said in a Feb. 10 e-mail interview. “Individual LGFV defaults will happen this year, but are unlikely to lead to a systemic financial crisis as the central government is expected to intervene.”

The cost of potential bailouts is escalating, with an official audit estimating regional liabilities alone jumped 67 percent from the end of 2010 to 17.9 trillion yuan ($2.95 trillion) as of June 30 last year. The PBOC has allowed money-market rates to surge to deleverage debt in the world’s second-largest economy that the Chinese Academy of Social Sciences estimates accounts for 215% of gross domestic product.

The buildup has evoked comparisons to Japan’s debt surge before its lost decade and to that in Thailand ahead of Asia’s financial crisis. Japan’s credit-to-GDP ratio rose to 176 percent in 1990 from 127 percent in 1980, JPMorgan Chase & Co. said in a July report.

The first credit events in China will probably occur in industries with excess capacity because demand is weak and the government is seeking to curb expansion, said Zhang. China has ordered more than 1,400 companies in 19 industries such as steel, ferroalloys and cement to slim down as part of a drive to refocus the economy on domestic demand and cut air pollution.

Let’s see something tangible come from this investigation, and then we’ll talk again.

• Foreign exchange scandal widens with inquiry into official ‘collusion’ (Independent)

The Bank of England has launched a “full legal review” into claims that its officials gave tacit approval to collusion among foreign-exchange traders, now part of a major international investigation. Andrew Bailey, a deputy governor, told MPs on the Treasury Select Committee that the review was being carried out by in-house lawyers “supported by outside counsel”.

He said: “The governors have taken these claims extremely seriously. We have released a minute (of the meeting) but obviously there are now allegations of different versions.” He said that the governors had “immediately” acted in the wake of the publication of the claims, holding that a senior trader’s note of the meeting differed sharply from the Bank’s own minute. This said blandly that “there was a brief discussion on extra levels of compliance that many bank trading desks were subject to when managing client risks”.

Trust, right? While the predator devours the prey?!

• Trust in short supply between developed and emerging countries (Satyajit Das)

Recent economic growth and prosperity has been underpinned by greater international integration and cautious increase in mutual trust. This is now breaking down. Developed nations have chosen policies to devalue their currencies, through a combination of low interest rates and increasing the supply of money. These actions erode the value of sovereign bonds in which other nations, like China, Japan, Germany and others, have invested their savings.

Nations increasingly manipulate the value of currencies to allow them to capture a greater share of global trade, boosting growth. But a calculated policy of engineered currency devaluations to gain trading advantages invites destructive retaliation in the form of tit-for-tat currency wars. These beggar-thy-neighbour policies exacerbate international tensions, manifesting itself in trade protectionism and trade disputes.

Low interest rates and weak currencies have also encouraged investment into emerging nations, with higher rates and stronger growth prospects. These volatile money movements have the potential to destabilise these economies, derailing their development. This initially forced some nations to deploy financial repression of their own – controls on capital flows into the country. Now some countries are concerned about the flight of capital from emerging markets.

The devaluation of the US dollar has driven up the price of commodities, such as food and energy which are denominated in the American currency. In poorer countries where spending on food and energy, including everyday essentials like cooking oil, is a high proportion of income, this has caused hardship. These developments threaten to reverse progress in reducing poverty.

Under the guise of regulations needed to strengthen the financial system, the US has implemented measures whose extra-territorial application may give American banks a business advantage. Such measures do not foster international co-operation in regulating finance. [..]

In return for American support for their candidate for the IMF presidency (Christine Lagarde), the Europeans helped elect the American candidate (Jim Yong Kim) as the head of the World Bank. In both cases, the US and Europe used their disproportionate voting power to achieve the desired outcome.

Speaking at an IMF press conference, Brazil’s finance minister highlighted the inequality of the quotas that dictate voting power: “The calculated quota share of Luxembourg is larger than the one of Argentina or South Africa… The quota share of Belgium is larger than that of Indonesia and roughly three times that of Nigeria. And the quota of Spain, amazing as it may seem, is larger than the sum total of the quotas of all 44 sub-Saharan African countries.”

This is what happens at banks that were bailed out with your money. If you don’t like that, I suggest you say so.

• Barclays to cut 12,000 jobs, but raise bonuses 10% to $3.9 billion (RT)

Britain’s Barclays Bank plans to cut about 12,000 jobs worldwide, after profits dropped 32% in 2013. A shrinking bottom line is coupled with a 10% increase in the bonus pool, which grew to $3.9 billion. Barclays, one of the UK’s biggest lenders, with a staff of 140,000 said it is to cut between 10,000 and 12,000 jobs globally, including 7,000 in Britain.

The announcement follows the bank’s early release of its full year results on Monday that showed its pre-tax profit plummeting to £5.2 billion, well below the £7 billion of 2012. Meanwhile, the bonus pool rose by 10% to £2.38 billion, while the reward for investment bankers was up 13%.

“We employ people from Singapore to San Francisco. We compete in global markets for talent. If we are to act in the best interests of our shareholders, we have to make sure we have the best people in the firm,” as Barclays chief executive Antony Jenkins told reporters in a conference call. “At Barclays, we believe in paying for performance and paying competitively,” he added.

There are several degrees of blindness at the Fed. Not everyone is completely myopic. Yet.

• Plosser Says ‘I’m Worried’ Fed May Be Too Late in Raising Rates (Bloomberg)

Federal Reserve Bank of Philadelphia President Charles Plosser, who votes on policy this year, said central bank officials should focus on communicating the conditions under which interest rates will rise. “I’m worried that we’re going to be too late” to raise rates, Plosser told reporters after a speech at the University of Delaware in Newark. “I don’t want to chase the market, but we may have to end up having to do that” if investors act on anticipation of higher rates.

Long-term rates could start rising and the Fed would be “forced to chase them up” with its primary policy instrument, short-term rates, Plosser said, “and then we will really be behind.” Fed officials have said improvements in economic growth and the labor market are reasons to continue tapering monthly bond buying that has expanded its balance sheet to a record $4.1 trillion.

A jobless rate dropping toward the Fed’s stated threshold of 6.5% may prompt policy makers to elaborate on guidance for raising the target interest rate, which remains near zero. The Fed has said rates will hold “well past the time” unemployment reaches that level. “We have to figure out a better way to describe how we’re going to react to data,” Plosser said. Fed officials need to “let people know that we’re going to adjust our policy rates as certain variables change, and what variables are those?”

Krishna Guna, a former member of the management committee of the Federal Reserve Bank of New York, thinks Draghi should buy bank bonds, to prevent clashing with various EU laws. It will stretch until it won’t anymore. But imitating subprime securitization? You sure that’s a good thing?

• Can Mario Draghi Beat Deflation? (Bloomberg)

The European Central Bank may soon have to roll out the heavy artillery, in the form of an asset purchase program similar to those in the U.S., U.K. and Japan, to fight the specter of deflation. But in a currency union with 18 different sovereign bonds, the tough question will be what to buy. The best solution: Purchase loans from banks – what I call euro quantitative easing in bank loans. [..]

As ECB President Mario Draghi has hinted on at least two occasions, the central bank has an alternative: purchases of bank loans packaged into asset-backed securities. This would provide monetary stimulus while alleviating capital and leverage constraints, thereby enabling banks to make new loans. As such, it would be akin to the Federal Reserve’s purchases of mortgage-backed securities — what former Fed Chairman Ben Bernanke called “credit easing,” a form of quantitative easing that takes interest-rate risk out of private hands while also lowering other risk premiums and supporting credit supply.

The ECB could use the asset quality review it is now conducting to make sure the loans weren’t marked at inflated values by the banks. To be sure, the ECB would still require some protection from loan defaults. This could be achieved through the process of tranching, which splits securities into pieces with different levels of risk and return. The issuing banks would retain a piece designed to absorb the first losses to defaults. Pieces absorbing further losses could be sold to investors; national governments might be asked to add some partial guarantees.

There would be costs. Even with default protection, the ECB would be influencing credit allocation and might be exposed to losses in some extreme scenarios — something all central banks seek to avoid. But the uncomfortable reality is that central banks always take on some risk during crises, even when lending against collateral.

The ECB could use its muscle as the new banking regulator to push banks to package more loans for sale as securities, while encouraging investors with the prospect that it would buy the senior tranches if deflation risk escalated. However, it would probably take a number of months for banks to issue enough loan-backed securities for the ECB to make large-scale purchases. In the meantime, the ECB should have a back-up plan to buy the senior interest in loan portfolios directly from banks through simple structures created specifically for this purpose, in case it needs to scale up quickly to fight deflation.

Squeeze the olives!

• Europe Can’t Let Greece Drown in Debt (Bloomberg Ed.)

Greece and its creditors are wrestling with the country’s debts yet again. It probably won’t be the last time. As long as they keep making the same mistake, the next agreement is no more likely to succeed than the others.

Back in 2010, Greece was given one of the biggest bailout programs in history. It got new lending in return for fiscal austerity, but its debts weren’t reduced: Creditors were spared any write-offs. Experts objected that the program put too big a burden on Greek taxpayers, that this was neither politically nor economically sustainable, and that creditors should be made to take losses. They were right then, and they still are.

There’s been some limited bailing in of creditors since then, an extension of maturities and lowered interest rates, but the basic pattern hasn’t changed. As a result, Greece’s debt keeps rising. It now stands at roughly 180% of gross domestic product. This is plainly unsustainable.

The new fix under discussion, according to a recent Bloomberg News report, would extend Greek loan maturities further, to 50 years from 30, and lower the interest rate paid by 0.5%. Another bailout loan, adding €15 billion, also looks likely. All this might keep the show on the road and allow the so-called troika representing Greece’s creditors — the European Commission, the European Central Bank and the IMF — to say that the country can meet its debt target of 124% of GDP by 2020. Of course, after every previous negotiation, they also said that Greece was on track.

Great rundown from Australia.

• The ‘pause’ in global warming is not even a thing (Guardian)

The idea that global warming has “paused” or is currently chillaxing in a comfy chair with the words “hiatus” written on it has been getting a good run in the media of late. Much of this is down to a new study analysing why one single measure of climate change – the temperatures on the surface averaged out across the entire globe – might not have been rising quite so quickly as some thought they might.

But here’s the thing. There never was a “pause” in global warming or climate change. For practical purposes, the so-called “pause” in global warming is not even a thing.

The study in question was led by Professor Matt England at the University of New South Wales Climate Change Research Centre. England’s study found that climate models had not been geared to account for the current two decade-long period of strong trade winds in the Pacific. Once the researchers added this missing windy ingredient to the climate models, the surface temperatures predicted by the models more closely matched the observations – that is, the actual temperature measurements that have been taken around the globe. [..]

When the salty water of the oceans heats up, it expands, pushing sea level higher. If ice that’s attached to land – such as the two major ice sheets in Greenland and Antarctica – melt, they also add to the water in the ocean, further pushing up sea levels. Melting glaciers also add to sea level rise. So what’s been happening while global warming was apparently having a holiday?

Here’s a chart from Australia’s CSIRO science agency showing sea level rise in recent decades. The drop you can see around 2011 was actually down to water being temporarily stored on the Australian land mass following the major flooding and rainfall event that year.

And here’s the video.

• How Trade Winds Explain Earth’s Surface Warming Slowdown (YouTube)

Heat stored in the western Pacific Ocean caused by an unprecedented strengthening of the equatorial trade winds appears to be largely responsible for the hiatus in surface warming observed over the past 13 years.

New research published in the journal Nature Climate Change indicates that the dramatic acceleration in winds has invigorated the circulation of the Pacific Ocean, causing more heat to be taken out of the atmosphere and transferred into the subsurface ocean, while bringing cooler waters to the surface.“Scientists have long suspected that extra ocean heat uptake has slowed the rise of global average temperatures, but the mechanism behind the hiatus remained unclear” said Professor Matthew England, lead author of the study and a Chief Investigator at the ARC Centre of Excellence for Climate System Science.

“But the heat uptake is by no means permanent: when the trade wind strength returns to normal – as it inevitably will – our research suggests heat will quickly accumulate in the atmosphere. So global temperatures look set to rise rapidly out of the hiatus, returning to the levels projected within as little as a decade.”

This article addresses just one of the many issues discussed in Nicole Foss’ new video presentation, Facing the Future, co-presented with Laurence Boomert and available from the Automatic Earth Store. Get your copy now, be much better prepared for 2014, and support The Automatic Earth in the process!

Home › Forums › Debt Rattle Feb 12 2014: Central Control vs Complex Systems