Esther Bubley for OWI “Sign on the bus route through Indiana to Chicago” September 1943

Saxo’s Steen Jakobsen looks at his data and comes up with a number of predictions, in particular about China: “China is not happy these days”. Then again, who is? Russia is not, that’s for sure. Or Ukraine. Or Japan. Neither are America or Europe. They’re all not happy for different reasons, and even inside their borders there are different reasons people are not happy. When you see how the EU talks about Ukraine, how it will save the country by offering it membership, but not now, how it will offer capital to stave of bankruptcy, but not now and not enough, you get the impression Brussels is simply to blind not to be happy, and you get to feel sorry for the Greeks for having to talk to them.

Washington is not happy because is sees its influence vanish before its eyes in the (too) early eastern European spring sunlight. Armed men occupy parliament building in the Crimea. Doesn’t look like the kind of target the US army has been training for. Ukraine is the core of a larger region that through history has been the playing field of “bigger” powers from both east and west. The region is home to more different peoples and interests than anyone seems to comprehend, and they’ve all got an axe or two or three to grind. Much more Putin’s strong point than it is of any possible US president. The sentiments that blew up the Balkan, by a magnitude of steroids. Unless you play it well and keep everybody happy.

But the Ukraine is dead broke. Its hryvnia currency plunged 19% so far this week, saw some 10% of deposits withdrawn, and had its dollar peg removed, so it’ll fall further. The ruble keeps falling too, and the yuan, so Jakobsen is right, and so is The Automatic Earth by the way: the US dollar is set to rise. It does make one wonder: where has all the muscular language about currency manipulators gone? How long ago is it again that Washington last chided Beijing for keeping the yuan artificially low? Is it a while two years yet? Strange you don’t hear anything about that anymore now that the yuan is tumbling. That’s perhaps the kind of thing that easily gets lost in translation when one has bigger fish to fry.

Like how will Obama play the Ukraine and Crimea theaters. It’s not about Putin sending in his army. It’s a chessboard filled with guerrilla pawns. Over the past century, Ukraine, or rather, what today is the territory of Ukraine, was first ravaged by Stalin in the 1932-33 starvation genocide called Holodomor. In his “Extermination by hunger” campaign, Stalin attempted to obliterate the people living in the most fertile lands in his empire by starving them. The Holodomor may have killed more people than the Holocaust.

Which, less than ten years later, didn’t pass by Ukraine either. And then when the Germans left, it was back to Russian rule again. Hossanah heysannah. Only, Ukraine was never one people. It was just a matter of waiting for the next bad spell for differences to rear their heads again. And here we are. And who are the Ukrainians supposed to trust with their fate this time? The invaders from the east or the west? Who’s going to protect them from the next devil, and then turn out to be that devil…

It would seem that Putin is much better at this kind of chess than Washington. Playing one group out against the other, with all the bad memories collected over time, who needs a Russian army? One difference of course with days gone by is that today everybody, or at least the militant ones, are so much “better” armed than ever. Whole bags full of Kalashnikovs and grenade launchers were apparently dragged into Crimea parliament buildings early this morning by a 120 man strong militia. How do you protect yourself from that? It’ll a jungle out there, but who wants to live in one?

Jakobsen writes that the soon also not too happy Chinese will see their GDP growth slow to 5%, from the double digit numbers they’ve seen for years. Beijing will then manipulate the yuan down, if only because Japan doesn’t leave it any choice. I think you call that currency wars. Which will lead to lower growth in Germany and the rest of Europe, even turning it into negative territory, and squeeze world growth down to 3% or less.

And that will inevitably mean deflation in Europe and the US. And a 30% fall in “developed world” equity markets. Mind you, most of that is not money that will be invested elsewhere, but funny money that will vanish. And lead to a lot more not happy people. 30% looks very reasonable, benign almost. The grand mirage of western economics risks being popped and exposed by armed to the teeth rag tag local militias. Well, something had to do it.

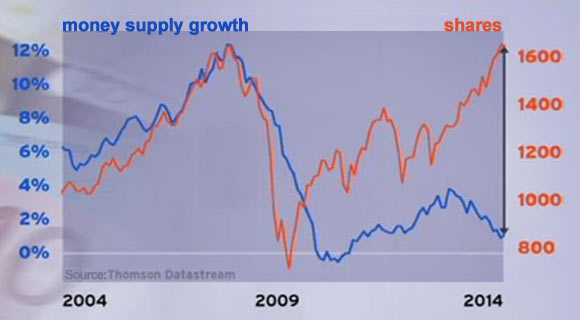

Oh wait, I made this little graph today from something I picked up at RTLZ, EU money supply (growth came in at 1.2% today) vs stock markets. Isn’t that just great? Tell me, where would you see that go? -30%? You think? I’m not sure I know why it would stop there.

• Implications of China’s currency move poorly understood (Saxo)

The market seems to be very sluggish in picking up on the implications of China’s recent move to weaken its currency, with the yuan now suddenly trading at its lowest level in months versus the US dollar.

My conclusion is this:

- China will slow down to 5% growth over the next two to three years;

- China will start devaluing its currency in response to Abenomics and China’s weaker terms of trade;

- China will no longer be the world’s biggest investor and importer of investment goods.

This will have huge implications outside of China and in 2014, these developments will likely mean the following:

- Germany growth will turn negative (quarter-on-quarter) in the fourth quarter relative to the third quarter;

- World growth will come down from its recent 3.7 percent to less than 3%;

- The recovery projections will once again be postponed and the out-of-synch monetary policies of the major central banks will be questioned, leading to all-time new lows in interest rates;

- Deflation will take hold in Europe and become a major risk in the US;

- Equity markets need to be sold off. This comes after commodities sold off after the US banking and housing crisis, followed by fixed income during the late stage European debt crisis. Now I see a 30% correction in the second half of 2014 after a high is registered between current levels of 1,850 and 1,890 in the S&P 500.

China leads the world economy. It took the burden of supporting world growth in its hands during the peak of the crisis in 2008/09, with the largest fiscal expansion ever seen (nearly USD 600 billion). China also increased its investment-to-GDP ratios, which brought export orders for major European and US exporters until late 2013. But since the Third Plenary Session of the 18th CPC Central Committee in November 2013, the main objectives for the political elite in China have changed from growth for its own sake to rebalancing, fighting graft, reducing pollution and hoping that they can engineer a transition of their economic growth model with a smaller crisis now rather than a bigger one later.

I have already spent some effort explaining why China is proactively seeking a small crisis rather than a big one and how China can no longer afford to keep its investment-to-GDP levels at excessive levels.

Now, China seems to have embarked on a fundamental change to its currency policy with its move to weaken the renminbi. It’s worth noting that China has been a strong critic of Abenomics and the resulting JPY devaluation as Japan and Korea remains its key export competitor. But until last week, China allowed its currency to continue higher in recent months — a side effect of a relatively tight monetary policy that was aimed at reining in bubbly credit markets. But now the focus has shifted back to the risks from a strong yuan and China’s shift to weaken the currency is a pivotal new development:

Source: Bloomberg and Saxo Bank

With the present tensions between China and Japan, this chart is cause for concern for all of us: it now appears that China will no longer “play nice” and we have to wonder what this will mean for the US-China relationship. President Barack Obama’s provocative decision to receive, once again, the Dalai Lama in the White House is not helping the situation. That the rally in USDCNY kicked off almost to the day Obama hosted the Dalai Lama is, of course, a pure coincidence (they met on Friday, February 20)!

China is not happy these days: the domestic economy needs rebalancing, with the risk that doing so upsets the population and those in the public sector who have benefited so handsomely from the status quo of the past several years. Overseas, Japan’s Abe is insisting on a stronger Japan, the US is “misbehaving” by talking to the Dalai Lama and the recent G20 meeting had the developed world blaming the recent slowdown on emerging markets.

It’s certainly not been a good month for monetary policy coordination or friendly summits. The growing potential for a political crisis comes ironically at a time when stock markets across the world are reaching 7-, 14- or even all-time highs, as was the recent case of the US S&P 500 Index. My old economic theory: The Bermuda Triangle of Economics remains in place. We’ve still got slow growth, high unemployment and high stock market valuations — all driven by a policy that only benefits the 20% of the economy that comprises large, listed companies and banks, who get 95% of all credit and access to policy subsidies. Meanwhile, the 80% of the economy that is the SMEs, who historically create 100% of all jobs, get less than 5% of credit and less than 1% of the political capital.

Markets and monetary policy

It’s the weather! The reason for the disappointing start to 2014 in the US is now all about the weather — well partly. I think most investors/pundits forget that the data for December and January was actually “born” three, six and nine months before due to impulses in interest rates and the overall cycle. As I have covered in the past, the slowdown in housing was “expected” in our models owing to the spike in mortgage rates between May and August 2013.

Elsewhere, the US consumer must have known the weather would be bad as far back as last summer judging by this retail sales (Mom) chart:

FRED Graph — retail sales US monthly change

US consumers remain two thirds of the economy, but they are still conservative: spending rose 2% in 2013 after 2.2% in 2012 and 3.4% in 2011. This is mainly due to low wage growth. Since 2010, the average after-tax income growth, adjusted for inflation, has only been +1.6% — to reach the magic 3% growth level, we will need wages to grow at least 3% on their own! This is not likely to happen in world of excess capacity, but nevertheless the pundits started the year with a 2.9% average expected growth for 2014. Now, one month into the year, the revisions are pouring in: the first quarter has already been reduced from 2.3% to 2% and the blockbuster Q4 growth of +3.2% is now expected to be revised lower to only +2.4%! Again, one has to laugh at how imprecise these measures are — we watch them, take decisions on them but ultimately their reliability is really only valid six months past the first announcement. Talk about looking in the rear-view mirror!

Strategy

Fixed income: still see new low yields in 2014 — mainly in Q4 — and into Q1 2015. ETF flows into fixed income are at USD 16bn year-to-date, which could be the largest inflow since 2002! Mainly prefer US and core Europe, although Italy’s BTPs have done well with the political transition from Enrico Letta to Matteo Renzi as prime minister. My view on falling yields goes back all the way to last year.

Dividend yield is at 1.89% versus 2.72% and still attracts my money.

Equity: We have had a call for a peak in Q1 — admittedly I did not expect 1,850 to be broken, but my partner in Economo-physics still sees the chance of 1,870/90 before a top is in place. I submit our updated November 2013 forecast, which, slightly corrected, still stands. The risk reward looks compelling: the upside is perhaps 50 S&P 500 points versus 500 points of down-side potential. Remember that a 20% to 30% correction happens every four to five years — and a 10% correction occurs twice a year, on average.

Source: Bloomberg

My most recent update called for a correction higher of the equity market, which is now almost complete from tactical point of view:

Source: Bloomberg

FX:Overall, the USD should soon find support. The best long-term gauge of the USD is world growth minus US growth. Why? Because the USD is the reserve currency and often the currency of choice in trade. When world growth is slowing (now …) then the US and the USD need to pull ahead to fill the gap. We need to monitor the US Dollar Index over the next week or two as it’s sitting on a major trend support line:

Conclusion:

China has now joined the currency devaluation game as it jostles with others for some wind for its sails. But there is only so much wind to go around.

• Yuan Turns Worst Emerging Carry Trade as PBOC Stokes Volatility (Bloomberg)

The yuan has gone from being the most attractive carry trade bet in emerging markets to the worst in the space of two months as central bank efforts to weaken the currency cause volatility to surge. The yuan’s Sharpe ratio, which measures returns adjusted for price swings, turned negative this year as three-month implied volatility in the currency rose in February by the most since September 2011.

The exchange rate tumbled the most since 2010 on Feb. 25, losing money for investors who borrowed dollars to buy yuan, amid speculation the People’s Bank of China was intervening to deter one-way bets on currency gains. “A lot of investors globally were invested in the yuan because of the interest-rate differential and the low volatility,” Rajeev De Mello, who manages $10 billion as Singapore-based head of Asian fixed income at Schroder Investment Management Ltd., said in a Feb. 25 phone interview. “All of a sudden, the low volatility part of the argument is no longer there.”

An unwinding of the carry trade may spur a slide in the yuan, which is set for the biggest monthly decline since the government unified official and market exchange rates at the end of 1993. Deutsche Bank AG, the world’s largest foreign-exchange trader, estimated this week that bullish bets on China’s currency amount to about $500 billion. Dollar-funded carry trades in the yuan lost 1.1% this year, compared with a gain of 5.6% in the Indonesian rupiah and a return of 2.1% in the Brazilian real, according to data compiled by Bloomberg. The trades involve borrowing funds in a nation with low interest rates to purchase higher-yielding assets elsewhere.

Is the EU’s endless meeting culture going to let Ukraine sink?

• West Deliberates as Ukraine Economy Sinks (WSJ)

Ukraine’s prospective Western benefactors suggested Wednesday that it could take months before a major aid package arrives, even as a sinking currency highlighted fast-eroding confidence in the economy following the ouster of the country’s president. As Russia announced military exercises of 150,000 troops, some less than 200 miles from Ukraine, banks in Ukraine said they were being deluged with inquiries about switching savings into safer dollars and euros.

Alfa Bank, a major Russian lender, said its Ukrainian arm stayed open late to help deal with demand. “People in Ukraine do really prefer foreign-currency deposits these days,” Sberbank, another Russian lender with operations in Ukraine, said in an email. Arseniy Yatsenyuk, who was designated to become Ukraine’s prime minister on Wednesday, painted a stark picture: “The treasury is empty, it faces debts of $75 billion and Ukraine’s overall debt is $130 billion. Pensions haven’t been paid in full for more than a month and the foreign-exchange reserves have been looted.”

Western officials said they moving quickly on a rescue, but there was little sign of quick cash. U.S. officials said they were reluctant to take any big steps until Ukraine’s new government is established – presidential elections are due May 25 – and begins to tighten budget controls. A senior French official also said Western countries should wait until after the May elections before pledging large-scale assistance, and European Union officials said privately it could be days or weeks before the bloc announces an aid package.

Amid the uncertainty, the Ukrainian hryvnia slumped to more than 10 to the dollar for the first time, dragging the Russian ruble down with it. The plunge accelerated after Moscow announced the military drills. Ukraine’s central bank said it had abandoned support of the hryvnia, and the country’s foreign-exchange reserves had fallen to $15 billion. While that total suggests some breathing room for any new government, Ukrainian officials have said they would put together a program of economic measures to secure a loan program from the International Monetary Fund as quickly as possible.

The EU’s head of enlargement policy Stefan Füle said the bloc had raised expectations in Ukraine and must now keep its promises. Such loan guarantees could help Ukraine pay for the $1 billion in bonds coming due in June—a move that would ostensibly keep borrowing costs down for the time being. That cash could be seen by Kiev as an act of good faith to help lubricate tough talks ahead on a large-scale, multilateral bailout package that Ukraine needs over the next several years to repair its badly maimed economy. Some analysts estimate the country’s full financing need at around $35 billion for two years, with the IMF contribution at approximately $15 billion.

EU officials also renewed their appeal for Russia to come on board an international support package. Mr. Füle said Russia “risks losing heavily if Ukraine fails.” Baroness Ashton will meet Russian Foreign Minister Sergei Lavrov to discuss Ukraine next week. Moscow can undercut any Western aid package, the senior French official said, by raising natural-gas prices on Kiev. Russia could also counter with a separate aid package lacking conditions for economic reforms, undercutting Western efforts to overhaul Ukraine’s economy. “The best way to decide on an assistance program and conditions is with the Russians, because otherwise it’s very complicated,” the official said.

[..] EU policy makers have talked about providing upward of €20 billion of financial assistance to Ukraine by 2020, and Brussels is exploring ways of front-loading some of that aid. Allowing a substantial depreciation in the exchange rate is likely to ease the way to a deal with the IMF. Also, the IMF says that the government needs to raise natural-gas prices to market levels, but that could come in stages. Raising fuel prices would take a major burden off government finances and stem a source of state corruption, economists say.

Meanwhile, the Russian ruble also hit record lows. As a more easily tradable currency, analysts said it was bearing some strain as a proxy for the hryvnia. The ruble slid to a weakest-ever level of 42.10 against the basket of euros and dollars that the central bank uses as key gauge, echoing heavy selling pressure in the ruble that accompanied Russia’s conflict with Georgia in August 2008.

• Ukraine Currency Extends Plunge as Bonds Slump on Crimea Tension (Bloomberg)

The hryvnia tumbled to a record low for a fourth day and Ukraine’s Eurobonds slumped after the central bank abandoned its dollar peg and Russia put fighter jets on alert amid tension in the Crimea region.

The currency weakened 7.7% to 11 per dollar, according to data compiled by Bloomberg at 11:22 a.m. in Kiev. That extended the slide in the past four days to 19% and 25% this year. Ukraine’s U.S. currency-denominated bonds due in June dropped to 93.78 cents on the dollar from 93.94 yesterday, lifting the yield to 34.3%.

Ukraine’s interim leaders have started a search for a bailout of as much as $35 billion after last week’s ouster of Viktor Yanukovych left reserves at an eight-year low and tension flared in the Russian-speaking east and south of the country. As opposition leader Arseniy Yatsenyuk sought confirmation as premier in Kiev, gunmen raised the Russian flag over parliament and the government building in Ukraine’s Crimea region, while Russia’s defense ministry said it’s conducting a check on the combat-readiness of armed forces.

“Russian reaction to a pro-Western government is providing increasing cause for concern,” Thu Lan Nguyen, a Frankfurt-based analyst at Commerzbank AG, wrote in an e-mailed report today. The hryvnia may benefit if the formation of a new government brings a Western bailout closer, she said. With the central bank giving up interventions to protect currency reserves, there is “nothing to prevent” further weakening of the hryvnia against the dollar, Nguyen wrote.

Losses and bonuses. What better way is there to summarize our present set of values?

• RBS pays out £588 million in bonuses despite £8.24 billion loss (Guardian)

Royal Bank of Scotland has defended plans to pay £588m in staff bonuses despite suffering an £8.24bn loss in 2013 as it slumped into the red for the sixth successive year. The size of the bank’s bonus pool fell 18% from last year but the RBS chief executive, Ross McEwan, acknowledged that the issue was “highly emotional” as he explained the multimillion pound windfall at the taxpayer-owned institution. “I need to pay these people fairly in the marketplace to do the job. I do need to make sure we are there or thereabouts and that is all I’m asking for,” he said.

The latest annual loss was caused by £3.8bn of costs for settling litigation and regulatory problems – including £1.5bn extra to compensate customers mis-sold payment protection insurance and interest rate swaps in the UK – and £4.5bn of losses on bad assets. The company’s shares fell 6.7% to 330.2p in early trading, wiping more than £2.5bn off the market value of a business that is 81%-owned by the taxpayer. McEwan, who took over from Stephen Hester in October, said RBS needed to regain the trust of its customers and the public. “We happen to be the least trusted bank in the least trusted sector in the marketplace,” he said.

McEwan also announced plans to revitalise the business, including:

• Refocusing on UK retail and business customers to increase the share of total assets from Britain to 80% from 60%.

• Shrinking RBS from seven businesses into three: personal and business banking, commercial and private banking, and corporate and institutional banking.

• Simplifying products for retail and small business customers, including scrapping “teaser rates” and 0% credit card transfers.

• Cutting costs because the bank is “too expensive and too bureaucratic”.

RBS had warned last month that its pretax loss for the year would be about £8bn but investors were shocked by an operating loss of £2.3bn – far worse than the £1.7bn analysts expected. Ian Gordon, banks analyst at Investec, said: “We currently see no relative or absolute support for RBS’ ‘frothy’ valuation; a correction is due. Sell.”

RBS was bailed out by taxpayers during the financial crisis of 2008 and 2009 with a £45bn investment, following a disastrous expansion into risky investment banking and trading. The bank has since slashed those businesses but McEwan said the cuts would go further still so that its markets business served the basic requirements UK and European companies. He declined to put a figure on potential job cuts but he said RBS – which employs 120,000 people – could get out of more businesses that customers did not need after quitting equity capital markets, mergers and acquisitions and structured finance.

Bankers’ bonuses continue to plague the industry amid public uproar over past misconduct. Barclays increased bonuses by 10% last week to £2.4bn. HSBC said on Monday it would increase salaries for its bosses to get around a European union cap on bonuses. McEwan, who has turned down his bonus for 2013 along with his executive team, declined to say whether RBS would ask shareholders, including the government, for permission to circumvent the EU bonus cap this year. “The board has not opined,” he said.

Yanukovych got the money to build his palaces thanks to British banks. Pecunia never non olet. Unless someone’s looking.

• Where are the guardians of the City? (Independent)

London laundry: Companies House: International authorities are considering freezing the assets of Ukrainian millionaires associated with the regime of Viktor Yanukovych. If it happens, a fresh light could soon be shone on London, where much of Kiev’s wealth is said to have either ended up, or travelled through “brass plate” companies during complex laundering process.

We pride ourselves on being one of the easiest places in the world to do business. The current Government, as with all UK governments in recent memory, is committed to encouraging enterprise, reducing unnecessary business regulation, and helping people to set up in business. This is excellent encouragement for legitimate businesses but a heaven-sent stimulus to crooks from all over the world.

Under current laws, to set up a limited company in the UK can cost as little as £15 online from Companies House, and requires no minimum capital. Anyone can be a company director, unless he or she is disqualified. A convicted fraudster can become a company director and companies can be formed from prison.

There are no checks on the identity or address of company directors, or on their past history. Phoenix companies can be formed in the wake of the collapse of a failed enterprise, which may have gone bust owing thousands of pounds to creditors. Such a firm can be made with no debt, with the same directors, the very same day.

Companies House is a repository of corporate information and no more. It neither regulates companies nor even guarantees the accuracy of the information it holds about companies and publishes on its website. It carries out some very basic checks to make sure that documents have been fully completed and signed and to make sure that the company’s name is not similar to another existing company. But it has no statutory power or capability to verify the accuracy of the information that corporate entities send to it.

As the disclaimer on its website states: “We accept all information that such entities deliver to us in good faith and place it on the public record. The fact that the information has been placed on the public record should not be taken to indicate that Companies House has verified or validated it in any way.”

Filings can still be lodged in paper form, rather than online. This means that, unless its staff trawl by hand through the details of the 30,000-40,000 new companies incorporated each month and the nine million annual filings, there is no way they can verify, cross-check or analyse the information submitted. In some cases, accounts of a company on the Companies House website have been cut and pasted by fraudsters from those of another (perfectly respectable) company, with no connection at all to the first one. Nominee directors cannot be identified as such and the real beneficial owners of companies can legitimately hide behind them.

As if that weren’t bad enough, you can’t even have total faith in the address provided. A new breed of “company service providers” has sprung up, offering serviced offices rented on a daily or hourly basis with telephone answering services. While usually used for legitimate purposes, they are also wide open to abuse by criminals wishing to give the impression of a permanent place of business for the entity clients are dealing with.

Yet another piece of creative accounting. The broker the bank, the more creative it gets.

• Banks Averting Bond Losses With Accounting Twist (Bloomberg)

JPMorgan Chase and Wells Fargo are leading a shift in how banks account for their bond investments after a $44 billion plunge in value exposed a potential drain on capital under new rules.

The largest U.S. lenders are moving assets into the “held-to-maturity” column of their books instead of designating them as “available for sale,” an accounting method that under post-crisis banking regulations allows paper losses to erode measures of their health. The change pushed the share of securities that the five biggest banks keep in the held-to-maturity category to 8.4%, the highest in almost two decades, according to Credit Suisse Group AG analysts.

Banks are seeking to protect themselves from a weakening of their capital as economists predict bond yields will continue to climb from record lows after their biggest investments, government-backed mortgage securities, posted their first annual losses since 1994. While the strategy may bolster banks’ financial standing, overuse of the accounting method may limit their ability to raise cash to make loans as the economy strengthens and mask risks.

“You don’t want somebody loading the boat and taking on tremendous” interest-rate risk by exploiting the distinction, said William Weber, a former Federal Deposit Insurance Corp. official and bank treasurer who now advises lenders on their balance sheets as head of Drexel Hamilton LLC’s institutional depository group. At the same time, “they have the right” to switch their accounting methods, he said.

U.S. deposit-takers invest more in the $5.4 trillion of Fannie Mae, Freddie Mac and Ginnie Mae mortgage bonds than in other securities because they carry little default risk, offer higher yields than Treasuries and are easy to trade. The top 50 banks owned $1.2 trillion at year-end, increasing those designated as held-to-maturity, or HTM, by $38.4 billion in the three months ended Dec. 31 and reducing available-for-sale, or AFS, investments by $23.3 billion, according to data compiled by Morgan Stanley analysts.

JPMorgan experienced the “most dramatic shift,” the analysts led by Vipul Jain wrote in a Feb. 19 report. The New York-based bank boosted the holdings in the first category by $18.6 billion, while cutting them in the AFS grouping by $16.8 billion. Wells Fargo, based in San Francisco, increased HTM holdings by $6.3 billion, while reducing those in AFS by about $200 million. The two banks used the HTM designation for less than $10 million of the investments a year earlier, according to regulatory data available through the National Information Center website.

• Banks Prefer Losses They Don’t Have to Talk About (Bloomberg)

If you own a bond and interest rates go up, your bond will lose value. That’s just a fact. But the consequences of that fact, if you’re a bank, are all over the place. If you own that bond in your trading portfolio, you have what is colloquially called a trading loss: You owned a thing, it went down in price, you have lost money. Not in a strict literal sense — you have not turned the bond back into money, so your losses are “on paper” — but in every relevant accounting and capital and so forth sense. So your net income goes down (or becomes a net loss), and your regulatory capital goes down, by the amount of value that your bond has lost.

If you own that bond for investment purposes, and you don’t have any “intent of selling it within hours or days,” you have an investment loss on paper, but you get to treat it a bit more gently. (This is called “available for sale,” or AFS.) The loss doesn’t flow through your net income; instead it flows through a different place called “other comprehensive income,” and everyone agrees to treat that as somewhat less important than net income. Everyone except Basel III bank capital regulation: Last year, regulators ungallantly decided to require you to treat those unrealized investment losses as reducing your capital.

If you have the “positive intent and ability” to hold the bond until it matures, then you can just ignore the economic loss until maturity. (This is called “held to maturity,” or HTM.) You just keep the bond on your books at the price you paid for it,4 and at maturity you get back par and your loss vanishes. You ignore the loss in net income, other comprehensive income, your balance sheet, your capital, whatever.

The point is: The economic loss is the economic loss, but the accounting treatment varies from “recognize the economic loss immediately” through “recognize it for some purposes but not for others” all the way to “ignore it in all ways forever.” And you get some choice about what accounting treatment you’ll use.Generically speaking, ignoring losses is more attractive than recognizing losses. So you’d expect that, when losses seem likely — say when you have a giant portfolio of bonds in a low interest rate environment in which everyone expects long-term interest rates to increase in the next few years — held-to-maturity treatment would be more attractive than available-for-sale. And, lo:

The largest U.S. lenders are moving assets into the “held-to-maturity” column of their books instead of designating them as “available for sale,” an accounting method that under post-crisis banking regulations allows paper losses to erode measures of their health. The change pushed the share of securities that the five biggest banks keep in the held-to-maturity category to 8.4%, the highest in almost two decades, according to Credit Suisse Group AG analysts. …

U.S. deposit-takers invest more in the $5.4 trillion of Fannie Mae, Freddie Mac and Ginnie Mae mortgage bonds than in other securities because they carry little default risk, offer higher yields than Treasuries and are easy to trade. The top 50 banks owned $1.2 trillion at year-end, increasing those designated as held-to-maturity, or HTM, by $38.4 billion in the three months ended Dec. 31 and reducing available-for-sale, or AFS, investments by $23.3 billion, according to data compiled by Morgan Stanley analysts.

There are many delights in the story. But let’s quickly pick two. First, one reaction to a rising interest rate environment might be to reduce one’s holdings of long-dated fixed-income securities. One might say “hmm, I should maybe sell my trillions of dollars of very liquid Fannie Mae bonds that I expect to lose value in the next few years.” Or not, I mean, I’m not advising anyone to predict the timing of interest rate rises. The point is though that banks seem to be reacting to their expectations of rising interest rates with the opposite of the economically rational strategy: Not “sell bonds to avoid losses later,” but rather “reclassify bonds as hold-forever to avoid recognizing losses later.” The accounting provides opposite incentives from the economics.

Second is this very deep passage at the end of the article:

At the same time that regulators are putting bank capital at greater risk from bond slumps, they’re also working on separate rules stemming from Basel III that will make lenders increase holdings of easy-to-trade assets such as agency mortgage securities so they can survive a financial crisis.

The use of HTM accounting, which so far appears to be getting done in a “thoughtful” and limited way that shouldn’t increase banks’ risks, is a logical response to the pair of new regulations, said Greg Hertrich, the head of U.S. depository strategies at Nomura Holdings Inc.’s securities arm. “If you tell banks they have to hold” a certain amount of easy-to-liquidate assets, “it behooves them to find a way to do it in which there isn’t a significant amount of capital volatility from quarter to quarter,” he said.

Did you get that? New Basel III related regulations require banks to have a “liquidity buffer” of assets they can use to raise cash in an emergency. Banks are willing to do this, but they don’t want their liquidity buffer to create “a significant amount of capital volatility.” That is, they don’t want mark-to-market losses on their liquidity buffers to reduce their regulatory capital. This is part of their broader desire not to have any mark-to-market losses on anything reduce their regulatory capital, but the liquidity buffer is part of that, sure.

So why not classify (some of) your liquidity buffer as held-to-maturity, that is, as bonds that you plan to hold on to forever? You tell your accountants “we never plan to sell these bonds,” and you tell your regulators “well we can always sell these bonds in an emergency.” It’s its own little miniature regulatory arbitrage: You treat the same thing in opposite ways under different regulatory regimes. Normally that takes some significant effort, but here, just pronouncing a few magic words seems to do the trick. It’s somewhat less of a fact if it’s a floating-rate bond, but it’s probably not. Also I don’t want to hear about credit spreads being inversely correlated to rates or whatever, you know what I mean.

Yup. That’s what I said. Kill the middle class, kill the nation.

• IMF study finds inequality is damaging to economic growth (Guardian)

The International Monetary Fund has backed economists who argue that inequality is a drag on growth in a discussion paper that has also dismissed rightwing theories that efforts to redistribute incomes are self-defeating. The Washington-based organisation, which advises governments on sustainable growth, said countries with high levels of inequality suffered lower growth than nations that distributed incomes more evenly. Backing analysis by the Keynesian economist and Nobel prizewinner Joseph Stiglitz, it warned that inequality can also make growth more volatile and create the unstable conditions for a sudden slowdown in GDP growth.

And in what is likely to be viewed as its most controversial conclusion, the IMF said analysis of various efforts to redistribute incomes showed they had a neutral effect on GDP growth. This last point is expected to dismay rightwing politicians who argue that overcoming inequality robs the rich of incentives to invest and the poor of incentives to work and is counter-productive. The paper, written by Jonathan Ostry, the deputy head of the IMF’s research department, and the economists Andrew Berg and Charalambos Tsangarides, comes after several years of heated debate over the path that developed and developing countries’ economies have taken since the financial crash and whether their recoveries are sustainable.

Anti-poverty charity Oxfam welcomed the report, saying it shows “extreme inequality is damaging not only because it is morally unacceptable, but it’s bad economics”. It added: “The IMF has debunked the old myth that redistribution is bad for growth and demolished the case for austerity. That redistribution efforts -essential to fight inequality- are good for growth is a welcome finding. Low tax and low public spending are clearly not the route to prosperity.”

It is 18 months since the IMF published its controversial view that government cuts to public-sector spending were having a larger detrimental effect than previously thought. The paper, written by its chief economist, Olivier Blanchard, was incendiary and sparked denials in London and Brussels where calls for austerity were strongest. Heated debate over Blanchard’s analysis has continued ever since, with many economists claiming that assumptions used in the critique were flawed.

The authors of this latest report can expect the same backlash, especially in the US where the Tea Party has defended tax cuts for wealthy individuals and studies show most of the country’s income growth since the crash has gone to the richest 1%. Last year the UK’s coalition government cut tax on incomes over £150,000 from 50p to 45p after a debate over the negative effects on growth of high taxes on wealthy individuals. The French president, François Hollande, has come under severe criticism for raising the tax on incomes above €1m to 75% from business groups that claim it will hit GDP and discourage wealthy investors from staying in France.

The report’s authors said the study, which excluded so-called market interference such as banker bonus caps and increases in welfare spending, showed the largest redistributions of income had negative effects on growth, but were offset by the benefits of lower inequality. “We find that higher inequality seems to lower growth. Redistribution, in contrast, has a tiny and statistically insignificant (slightly negative) effect.”

Get out of Dodge!

• Troika, governor of European colonies : Lawmakers fed up with debt crisis tactics (RT)

European lawmakers are calling into question the ability of the Troika to effectively deal with the crisis, and many are attacking its methods. An investigation report due in April will look at the handling of the Greek sovereign debt debacle. The probe by the European Parliament on how the International Monetary Fund (IMF), the European Central Bank (ECB), and the European Commission (EC) monitored and helped to solve the euro debt crisis, which started in 2008, triggered by the US financial collapse.

The Troika acts like a governor and visits it s colonies in the south of Europe and tells them what to do. The measures that they come up with though are not always very effective, Derk Jan Eppink, an MEP from Belgium who initiated the probe into the Troika, told RT. The IMF has admitted it made mistakes in the handling of Greece’s first international bailout, but some EU lawmakers want more answers.

Initially, the Troika was established to provide bailout loans to the eurozone s most indebted nations and get them back on track, but instead crippling austerity has left most economies worse off than they were before the crisis. In terms of public debt. In terms of potential growth. In terms of employment, the results are worse now than before troika intervention in a country like Greece, Dr. Yves Bertoncini, director of Notre Europe, a Paris-based EU policy think tank, told RT.

The eurozone s three big lenders, known as the Troika, yield a great amount of power, as they have lent over €396 billion to Greece, Cyprus, Ireland, Portugal, and Spain. Greece was the first in 2010, and most recently, Cyprus in 2013. Greece has already received over €240 billion in loans from the troika of lenders, almost the equivalent to the country’s entire economy.

Ireland was the first country to exit the IMF bailout program, which it did in December 2013. In order to do so, it had to slash the national budget by €30 billion and cut salaries by up to 20%. Mounting debt and high-unemployment have only worsened since the onset of the crisis in 2008. Greece’s economy hasn’t expanded since 2007, despite the IMF predicted 1 and 2% growth in 2011 and 2012. In 2011 it shrunk more than 7%, and in 2013 it contracted 4.21%.

The eurozone has over $11 trillion in debt- much of which Cyprus, Greece, Ireland, Portugal and Spain hold a significant portion. In southern Europe hopes of a light at the end of the tunnel aren’t high, especially for the generation growing up under the troika.

Isn’t it great? The broker the banks, the bigger and richer they get. And everyone just stands there looking at this.

• Fewer banks and higher profits, that’s post-crisis reality in the US (Quartz)

Looking at this key gauge of bank profitability, it’s hard to believe the US banking industry just suffered through the worst economic crisis in a generation.

In fact, American banks are faring better than they ever have, according to data released today by the Federal Deposit Insurance Corp.

America’s banks rang up profits of $154 billion last year, that’s nearly 10% more than the $141 billion in profits reported in 2012. It’s also 6% higher than the pre-crisis peak of $145 billion in profits, which banks posted in 2006.

In a prepared statement, FDIC chairman Martin Gruenberg noted that the robust profit recovery was partly driven by financial institutions releasing cash previously earmarked to protect against potentially problem loans. Such reserve releases were the “single largest component of the improvement in industry earnings,” he said.

Source: Federal Deposit Insurance Corp.

Source: Federal Deposit Insurance Corp.Of course, banks still face headwinds. For example, the boomlet in mortgage refinancing, which generated significant fees for US banks, has lost steam as mortgage rates moved higher in 2013. JP Morgan Chase CEO Jamie Dimon, the head of the largest US bank by assets, seems less than enthused about the the prospects (paywall) for economic growth this year.

Of course, even if the size of the financial pie isn’t growing exceptionally fast, there are fewer banks to share it. For example, the solid 2014 profit performance comes even as the number of the banks regulated by the FDIC has shrunk dramatically. In other words, despite all the blustering and outrage over too-big-to-fail institutions, fewer lenders control more assets and are ringing up more—even record—profits.

Not my kind of article normally, but interesting to see that Steve Cohen made $2.3 billion at the exact same time he pleaded guilty to criminal insider trading charges and agreed to pay $1.8 billion in fines and penalties. Surprised? Really?

• The 25 Highest-Earning Hedge Fund Managers And Traders

In 2013, hedge fund managers and traders bet on an economic revival in Japan, laid siege to corporate boards, invested in hospitals that could benefit from Obamacare and helped make General Motors a hot stock. They waged an epic battle over a seller of diet shakes, drew the ire of actor George Clooney and were blamed for the problems of a 111-year-old American department store chain. In the end, the vast majority of hedge fund managers were yet again unable to keep up with the U.S. stock market as equities boomed from New York to Tokyo.

But prominent hedge fund managers and traders did not have to match the 32% return of the Standard & Poor’s 500 index to make a lot of money in 2013—and many of them increasingly argued they should not even be measured against such a benchmark during a bull market. In fact, the legend of one of the most famous hedge fund managers of all time grew last year even though he did not beat the performance of the U.S. stock market.

George Soros tops Forbes’ list of the highest-earning hedge fund managers and traders, personally making an estimated $4 billion in 2013 as his Soros Fund Management generated returns of more than 22%. At 83, Soros is not involved in the day-to-day operations of Soros Fund Management, the family office that manages some $29 billion belonging to Soros and foundations to which he has given money. The firm is overseen by Scott Bessent, Soros Fund Management’s chief investment officer, but Soros remains involved and the firm’s big short bet on the yen at the start of 2013 was vintage Soros.

Perhaps the most remarkable performance of 2013, however, belongs to former Goldman Sachs trader David Tepper, who has been setting a new standard for hedge fund managers. His track record has long been phenomenal, but since the financial crisis his returns have reached a new level. In 2013, the 56-year-old founder of Appaloosa Management outperformed the U.S. stock market and the vast majority of hedge fund managers, with his biggest fund posting net returns of more than 42%. Over the last five years, Tepper’s main hedge fund has generated annualized net returns of nearly 40%—and gross returns of some 50%. In what has almost become an annual tradition, he gave back some cash to his investors at the end of the year. Tepper made $3.5 billion in 2013.

In total, the 25 highest-earning hedge fund managers and traders made $24.3 billion in 2013. The lowest earning hedge fund managers on our list made $280 million last year. While the amount of money made by the top hedge fund managers in a year like 2013 is generally notable, the earnings of one hedge fund manager in particular is bound to raise a few eyebrows.

Steve Cohen was the most highly scrutinized and watched hedge fund manager last year. His hedge fund firm, SAC Capital Advisors, pleaded guilty to criminal insider trading charges and agreed to pay $1.8 billion in fines and penalties to the federal government. That’s a big number, but it’s less than Cohen earned in 2013, when he made an estimated $2.3 billion. One of the most successful traders ever, Cohen is transforming his Stamford, Ct., hedge fund firm into a family office, returning billions of dollars to outside investors. Through all the legal headaches, Cohen, 58, continued to do what he does best—make profitable trades and earn plenty of money. SAC Capital knocked out net returns of about 19% in 2013. That was not as good as what the U.S. stock market returned, but it beat most other hedge fund managers.

Oh, great!

• Ryanair to offer US to Europe flights for $10 (Belfast Telegraph)

Never one to shy away from an eye-catching headline, Ryanair supremo Michael O’Leary says he plans to offer flights to the United States for under £10. The no-frills airline will sell €10 seats, £8.20 at today’s exchange rate, when it eventually manages to secure the long haul aircraft needed, O’Leary announced today. The airline has a business plan ready for launching transatlantic flights but admits it will be several years before it can get the planes needed.

Mr O’Leary told the Irish Hotels Federation conference in Meath that Ryanair would offer €10 flights to the United States and US$10 flights from the US to Europe, though passengers would pay extra for everything from meals to baggage. The flights would operate from 12-14 major European cities to 12-14 major US destinations and a full service would begin within six months of Ryanair getting the aircraft to do so. However it would be four to five years before this happened as currently the Gulf state airlines are buying up all available aircraft.

Mr O’Leary praised the Republic’s government for scrapping the travel tax to Ireland from April 1st as the single biggest step to boosting tourism to Ireland since it came into power. He said Ryanair would deliver an extra 1 m passengers to Ireland as a result creating an extra €300m in tax revenue to the government through increased tourism spending.

But he urged Transport Minister Leo Varadkar to sell off Irish airports to make them more efficient as had been done in most European countries. Mr Varadkar hinted that privatising airport terminals while maintaining government ownership of the runways and ground areas could be an option, noting this was an option favoured in the US.

Maybe when you allow this to happen to you, you deserve it.

• GCHQ: Inside Her Majesty’s Listening Service (Spiegel)

GCHQ’s spies, who see themselves as the country’s eyes and ears, don’t like being the center of attention. It was only through the actions of American whistleblower Edward Snowden that the world learned about many of their operations. The documents Snowden leaked, from the innermost circles of the US National Security Agency (NSA), revealed that the British agency has begun monitoring increasingly large portions of global data traffic in recent years — infiltrating computer networks around the world, launching attacks and extracting information from mobile telephones.

In 2008, GCHQ agents began testing the “Tempora” program, which they hoped would allow them to tap into global data links, especially fiber optic cables. In the four years that followed, the agency’s access to data grew by 7,000%, according to a PowerPoint presentation described in the British newspaper The Guardian. Today the agency — which cites “mastering the Internet” as one of its objectives and boasts about extracting more data from the web than the NSA — employs 6,100 women and men, almost as many as MI5 and MI6, Britain’s domestic and foreign intelligence agencies, combined.

While GCHQ refuses to answer questions about its objectives, its former employees paint a picture of an agency that, in decades of existence, has become a modern surveillance monster.

Catchy title!

• The end of the automobile is coming (MarketWatch)

To hear some tell it, we are witnessing the rebirth of the automobile. Tesla Motors has brought electric cars mainstream with its Model S sedan, auto sales are steadily on the rise and once-troubled U.S. automakers are soundly back in the black after painful restructurings. But before you fall for the hype about Detroit’s comeback and China’s never-ending appetite for automobiles, it’s worth considering the other side of the argument before you throw any money at auto stocks.

Because while the most recent numbers show big strength for the industry worldwide, there are increasing signs that automakers may have their best days behind them. To be fair, the auto business — particularly in Detroit — has come a long way from the pain of the Great Recession. And that’s certainly something to celebrate.

In the wake of the financial crisis, Ford reported a record loss of $14.6 billion and General Motors and Chrysler both declared bankruptcy. Now both GM and Ford are sharing profits with employees, to the tune of $7,500 and $8,800 per eligible worker, respectively. Furthermore, U.S. auto sales bottomed in 2009 at a mere 10.4 million vehicles sold that calendar year — the worst annual total since 1982 . Now, new U.S. vehicle sales are predicted to top 16 million in 2014. These are indeed noteworthy accomplishments, and part of the reason that Ford stock is up over 850% from its 2009 lows.

But looking ahead, things are going to get much harder for investors as year-over-year comparisons get less favorable. Case in point: Ford and GM are expecting revenue to be basically flat in 2014, with low single-digit growth. And their counterparts in Japan, Honda and Toyota TM are actually expecting single-digit declines in overall revenue. That’s because a lot of the pent-up demand created by tighter spending has been used up.

Don’t take my word for it — listen to Jim Lentz, Toyota’s North American chief executive, who said as much in an Associated Press interview last year. “The market then has to work off a much better economy, an improving economy,” Lentz said. “If we don’t have that, I think the market may flatten out.” His timeline for that flattening in U.S. auto sales without a significant boost from broader economic and spending trends? “Sometime in late 2014.”

They will still call it progress, don’t worry.

• China’s toxic air pollution resembles nuclear winter (Guardian)

Chinese scientists have warned that the country’s toxic air pollution is now so bad that it resembles a nuclear winter, slowing photosynthesis in plants – and potentially wreaking havoc on the country’s food supply. Beijing and broad swaths of six northern provinces have spent the past week blanketed in a dense pea-soup smog that is not expected to abate until Thursday.

Beijing’s concentration of PM 2.5 particles – those small enough to penetrate deep into the lungs and enter the bloodstream – hit 505 micrograms per cubic metre on Tuesday night. The World Health Organisation recommends a safe level of 25. The worsening air pollution has already exacted a significant economic toll, grounding flights, closing highways and keeping tourists at home. On Monday 11,200 people visited Beijing’s Forbidden City, about a quarter of the site’s average daily draw.

He Dongxian, an associate professor at China Agricultural University’s College of Water Resources and Civil Engineering, said new research suggested that if the smog persists, Chinese agriculture will suffer conditions “somewhat similar to a nuclear winter”. She has demonstrated that air pollutants adhere to greenhouse surfaces, cutting the amount of light inside by about 50% and severely impeding photosynthesis, the process by which plants convert light into life-sustaining chemical energy.

She tested the hypothesis by growing one group of chili and tomato seeds under artificial lab light, and another under a suburban Beijing greenhouse. In the lab, the seeds sprouted in 20 days; in the greenhouse, they took more than two months. “They will be lucky to live at all,” He told the South China Morning Post newspaper. She warned that if smoggy conditions persist, the country’s agricultural production could be seriously affected. “Now almost every farm is caught in a smog panic,” she said.

Early this month the Shanghai Academy of Social Sciences claimed in a report that Beijing’s pollution made the city almost “uninhabitable for human beings”. The Chinese government has repeatedly promised to address the problem, but enforcement remains patchy. In October, Beijing introduced a system of emergency measures if pollution levels remained hazardous for three days in a row, including closing schools, shutting some factories, and restricting the use of government cars.

This article addresses just one of the many issues discussed in Nicole Foss’ new video presentation, Facing the Future, co-presented with Laurence Boomert and available from the Automatic Earth Store. Get your copy now, be much better prepared for 2014, and support The Automatic Earth in the process!

Home › Forums › Debt Rattle Feb 27 2014: A Chessboard Filled With Guerrilla Pawns