Arthur Rothstein Homesteader raising baby chicks, Bankhead Farms, Alabama February 1939

The Future Of Our Children Is Taking Shape Today. Ask any parent and they will say they care about this more than about anything else. These same parents, though, are leaving the shaping of that future to the global financial industry, which has gotten so powerful it can buy anything and anyone that can be bought, and decide who will be destitute and who will live lavishly. And that doesn’t cease to bother me.

This power takeover didn’t happen overnight, but it does seem to have reached a critical point lately, and left unchecked it will keep growing. The very moment a government declares one or more of its domestic banks too big to fail or “systemic”, and many have, political power in effect changes hands. There’s no ceremony, no gold ribbons and no crowns are being placed on heads, but that still is what it means. From the point onwards that power changes hands, only one set of interests will be addressed, and all others ignored. So when I read something like this …

“They are missing the point: Greece does not need a third bailout, it needs debt restructuring,” said the shadow development minister and economics professor, Giorgos Stathakis. “Even in the IMF, logical people agree there is no way we can have any more fiscal adjustment when the whole thing has reached its limits,” he said. “There is simply no room for further cuts and further taxes and that is what they are going to ask for.”

… several things come to mind. The first thing is the pattern of on the one hand the ubiquitous economic recovery claims by media and politicians, and on the other the fast growing numbers of reports about increasing poverty, kids going hungry and all-out misery, all across the west world.

The extent to which the claims of recovery contradict the misery of reality may be starkest in Greece, Detroit, Italy and West Virginia, but the underlying process is active all over: an ongoing gutting of western economies and societies through austerity measures, rising taxes and cuts to services and benefits, all delivered with the message that they must be complied with, or else. Just like 5-6 years ago governments said they had to rescue their banks, or else. We never get an explanation of what that “else” consists of, but the fear it instills obviously works like a charm, not in the least because it always comes with promise of better times ahead. Suffer now, party later.

The second thing is so obvious it has taken a long and strong denial to get people to stop talking, even thinking, about it, but it’s nevertheless still the only thing that makes sense. That is, it’s not just Greece that needs restructuring, the entire western world, and especially the banks, need restructuring of their debt. And there’s only one reason that hasn’t happened, see above: the financial industry has taken over political control, and hence now shapes our children’s futures.

And I’m naive enough that I don’t understand why people let that happen. From where I’m sitting, that future is simply too important to leave up to a bunch of people in glass highrises everybody knows care not one iota when happens to your children. If giving them a well-off future means more profits, they’ll have it, but if misery means more industry gains, they’ll have that to look forward to. Still, people, parents, seem to be so preoccupied with getting their share of the ever-shrinking pie that they forget, and are blinded to, what’s going on around them.

But it’s what’s around them that will shape their kids’ futures, who at some point will have to go out into the world out there. And if things keep on developing the way they have off late, that world will look a whole lot different from what it is today. So you can send them to what you think are the best schools, but schools educate according to what society looks like today, not 20 years from now, so there’s no guarantee that if and when societies change at a rapid clip, a particular education will keep its value. We could all push our kids to work in the financial industry, of course, but not many will have the skills, the will, the drive or the mindset to succeed in there. And if they’re among the 99.9% who don’t, their futures look very uncertain as long as the financial industry rules our societies.

As for the world at this moment, markets keep on losing. Don’t forget that substantial amounts of “capital” have been positioned to short the whole shebang. Japan down another 2%, European markets off 1% or more, Wall Street ditto. And please don’t forget that if we don’t restructure our banks and their debts, insane amounts of credit, virtual capital that should have been written down years ago as gambling debts, will keep circulating and blowing bubbles, helped along by central bank stimulus programs, public funds that are aimed exclusively at those same too big to fail banks, until it bankrupts entire societies that have seen their wealth be used to prop up lost wagers and never did anything to counter that because its members were too busy making money to send their kids to school. This is not going to turn out alright, not for you and not for your kids, unless you get up and do something about it, raise your voice, talk to your neighbors, bare your knuckles. It is not.

How would you like your kids to think about you, or remember you, 10-20 years from now? Mom and dad worked hard but were too stupid to see what was going on and in the end they just made things worse? Or would you like them to recognize your courage to stand up for what you felt was right for them?

Restructure bank debt, bankrupt those who are broke (that’s most of them), split up the banks into really small pieces, and make sure deposits are kept apart from investments and never the twain shall meet. A government can guarantee customer deposits (up to a point), no banks needed, it can be done through post offices, even grocery stores, no problem. There’s a way out of this, but it’ll mean reverting back 100 years or so. Don’t take that road and let the present process continue, however, and even a 100 year throwback becomes a pipedream for your children. We built our societies on borrowed money, and they still run on it. But the whole borrowing notion, the entire credit based society that’s the only thing we’ve ever known, is coming to an end, because as a society, and as individuals, we can no longer pay it back plus interest.

No more calm, and there won’t be any for a while. The Fed has no power over the economies of 20 or so different economies that have come into trouble. Janet Yellen can perhaps quell 1 or 2 storms, but not 10. It’s not just like western investors are withdrawing their money, there’s a whole bunch of them actively betting against nations and their currencies. They’re out for blood.

• Calm broken in markets amid concerns (Bloomberg)

Declines that erased $1.7 trillion from global stocks as currencies from Turkey to Argentina slid are proving a Wall Street maxim, according to Brian Barish of Cambiar Investors: selling can start anywhere.

“You’re never fully prepared for something like this,” Barish, the president of Denver-based Cambiar, which manages $9 billion, said. “You say to yourself, ‘I know the froth is picking up; I know this is starting to get a little out of hand; this is going to get ugly when the hammer comes down.’ You know all of that, but you just don’t know what is going to get sold and why and by who.”

From Thailand and Russia in the late 1990s to Portugal and Greece three years ago and Turkey and Argentina today, crises in emerging markets are as hard to predict as they are to contain. Now they’re threatening a run of gains that has gone virtually uninterrupted in the developed countries for more than a year as investors adjust to a world where neither China nor the US are likely to ride to the rescue.

The MSCI all country world index, which came within 5 percent of a record high on New Year’s Eve, has dropped 4% since January 22, the worst losses for worldwide equity markets in six months. Turkey’s attempt to stem declines in the lira backfired as a doubling of official interest rates led to even more selling. Stocks tumbled anew during the week as the Federal Reserve (Fed) said it would curtail its bond-buying programme in the second month of reduced stimulus.

“The reasons are always a little bit unexpected,” said Khiem Do, the head of Asian multi-asset strategy with Baring Asset Management in Hong Kong. Though the causes were obscure, the outcome was predictable, he said. “The correction is long overdue.”

“If you look at the things that have kicked off over the last two weeks in terms of currency, they are kind of long overdue,” said Gary Dugan, who helps oversee about $53 billion as the Singapore-based chief investment officer for Asia and the Middle East at Royal Bank of Scotland Group’s wealth management unit. “All of these things are well known, but it reached a crescendo that broke the back of the market.”

Good graphs to illustrate what we’ve been saying for a long time: there is no recovery, there’s only a transfer of virtual funds from the public sector to a group of individuals.

• “The ‘Recovery’ Is A Mirage, With As Much Monetary Distortion As In 1929” (Zero Hedge)

“Today there is a tremendous amount of monetary distortion, on par with the 1929 stock market and certainly the peak of 2007, and many others,” warns Universa’s Mark Spitznagel.

At these levels, he suggests (as The Dao of Capital author previously told Maria B, “subsequent large stock market losses and even crashes become perfectly expected events.”

Post-Bernanke it will be more of the same, he adds, and investors need to know how to navigate such a world full of “monetary distortions in the economy and the creation of malinvestments.” The reality is, Spitznagel concludes that the ‘recovery is a Fed distortion-driven mirage’ and the only way out is to let the natural homeostasis take over – “the purge that occurs after massive distortion is painful, but ultimately, it’s far better and healthier for the system.”

When Harvard economics professors start taking their money out of Bank of America, what do you do?

• Is your money safe at the bank? An economist says ‘no’ and withdraws his (PBS)

Last week I had over $1,000,000 in a checking account at Bank of America. Next week, I will have $10,000. Why am I getting in line to take my money out of Bank of America? Because of Ben Bernanke and Janet Yellen, who officially begins her term as chairwoman on Feb. 1.

Before I explain, let me disclose that I have been a stopped clock of criticism of the Federal Reserve for half a decade. That’s because I believe that when the Fed intervenes in markets, it has two effects — both negative. First, it decreases overall wealth by distorting markets and causing bad investment decisions. Second, the members of the Fed become reverse Robin Hoods as they take from the poor (and unsophisticated) investors and give to the rich (and politically connected). These effects have been noticed; a Gallup poll taken in the last few days reports that only the richest Americans support the Fed.

Why do I risk starting a run on Bank of America by withdrawing my money and presuming that many fellow depositors will read this and rush to withdraw too? Because they pay me zero interest. Thus, even an infinitesimal chance Bank of America will not repay me in full, whenever I ask, switches the cost-benefit conclusion from stay to flee.

Let me explain: Currently, I receive zero dollars in interest on my $1,000,000. The reason I had the money in Bank of America was to keep it safe. However, the potential cost to keeping my money in Bank of America is that the bank may be unwilling or unable to return my money. They will not be able to return my money if:

• Many other depositors like you get in line before me. Banks today promise everyone that they can have their money back instantaneously, but the bank does not actually have enough money to pay everyone at once because they have lent most of it out to other people — 90 percent or more. Thus, banks are always at risk for runs where the depositors at the front of the line get their money back, but the depositors at the back of the line do not.

• Some of the investments of Bank of America go bust. Because Bank of America has loaned out the vast majority of depositors’ money, if even a small percentage of its loans go bust, the firm is at risk for bankruptcy. Leverage, combined with some bad investments, caused the failure of Lehman Brothers in 2008 and would have caused the failure of Bank of America, AIG, Goldman Sachs, Morgan Stanley, Merrill Lynch, Bear Stearns, and many more institutions in 2008 had the government not bailed them out.

Recovery on the one end, poverty on the other. It’s what we always wanted, right? And if it’s not, what does that mean?

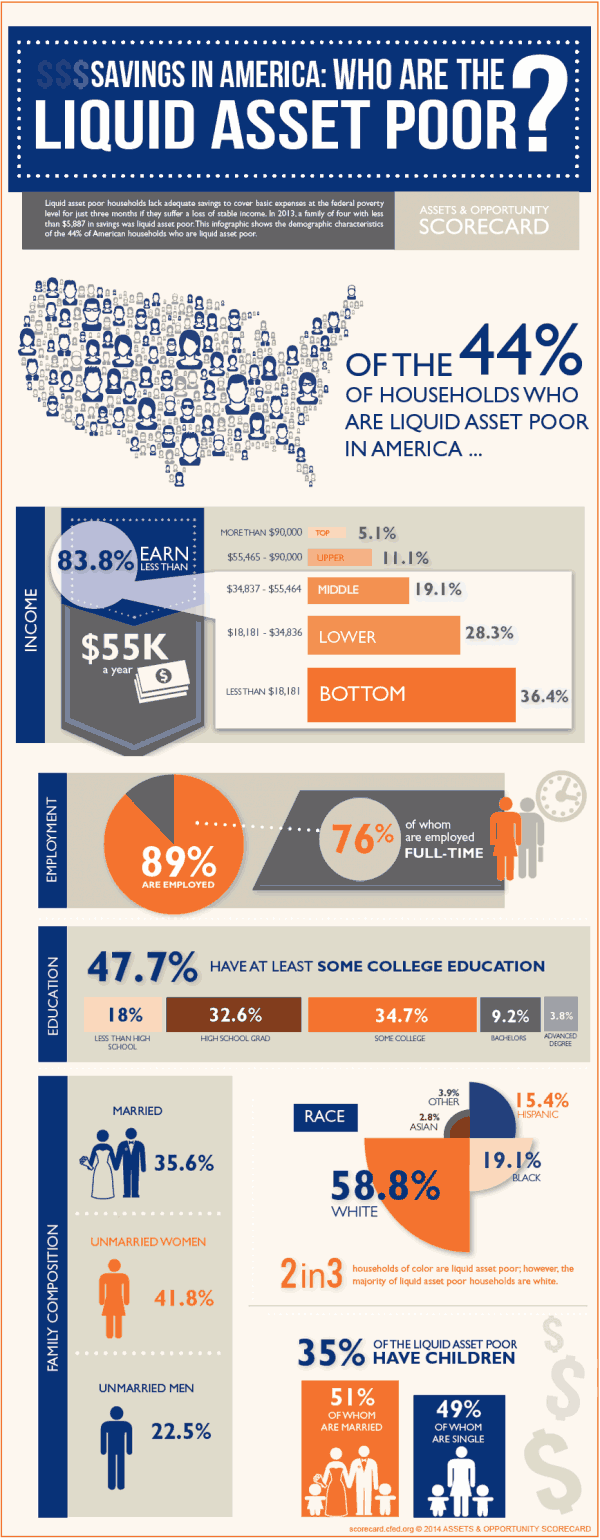

• Nearly Half of America Lives Paycheck-to-Paycheck (TIME)

The economic picture is looking brighter these days. The federal government announced Thursday that economic growth had picked up to its fastest pace in two years, while employment growth over the past five months has averaged a healthy 185,000 new jobs. But as evidenced by a report out Thursday from the Corporation for Enterprise Development, nearly half of Americans are living in a state of “persistent economic insecurity,” that makes it “difficult to look beyond immediate needs and plan for a more secure future.”

In other words, too many of us are living paycheck to paycheck. The CFED calls these folks “liquid asset poor,” and its report finds that 44% of Americans are living with less than $5,887 in savings for a family of four. The plight of these folks is compounded by the fact that the recession ravaged many Americans’ credit scores to the point that now 56% percent of us have subprime credit. That means that if emergencies arise, many Americans are forced to resort to high-interest debt from credit cards or payday loans.

And this financial insecurity isn’t just affected the lower classes. According to the CFED, one-quarter of middle-class households also fall into the category of “liquid asset poor.” Geographically, most of the economically insecure are clustered in the South and West, with Georgia, Mississippi, Alabama, Nevada, and Arkansas being the states with the highest percentage of financially insecure.

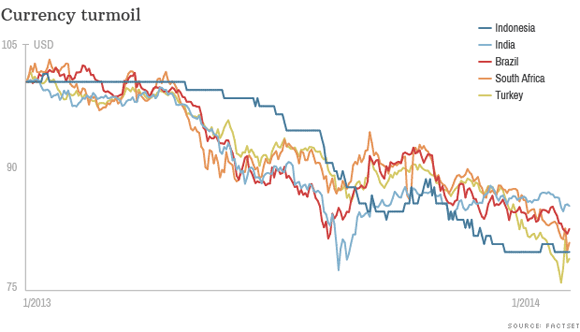

Emerging economies will continue to tremble for a while longer: there’s too much money to be made in shorting them to stop the process.

• Worst is yet to come for Fragile Five (CNN)

Last year was painful for emerging markets and 2014 is shaping up to be even worse. Among the hardest hit are Brazil, India, Indonesia, Turkey, and South Africa — dubbed the ‘Fragile Five’ by Morgan Stanley last August. Those countries have seen their currencies tumble 15% to 20% over the past year. And that plunge has continued this month, despite a series of aggressive and, in some cases, unexpected interest rate rises aimed at stopping the rot.

So after years of rapid expansion, and relative calm, what’s going wrong? For one, economic growth has slowed. As a group, emerging and developing economies grew on average by 6.4% over the past decade. Last year, that number was 4.5% and it’s forecast to rise only modestly in 2014. And signs of instability in China’s huge shadow banking system have raised fears of a credit crunch that would make it hard for Beijing to deliver its 7.5% growth target. The first decline in factory activity in six months has only made matters worse.

Cheap money is also drying up. The Federal Reserve said Wednesday that it would continue pulling back on its stimulus, to the tune of $10 billion. That means the U.S. central bank will pump $65 billion a month into the U.S. economy, down $20 billion from December. And the flow of cash is likely to cease completely by the end of this year.

But that doesn’t entirely explain the dramatic moves seen in some markets. Take India, for example. “The (Fed) decision was expected and should not in any way surprise or affect the Indian markets,” the Indian finance ministry said Thursday. That country’s central bank surprised investors with an interest rate hike this week, in an effort to calm the turmoil.

Still, the gradual normalization of monetary policy and rising U.S. interest rates make it less attractive to invest in emerging markets, particularly those which have failed to tackle deep-rooted problems during the years of plenty, or where other risks abound. And that’s where the Fragile Five come in. Over the past year or two, all have experienced slower growth, along with a heavy dependence on foreign capital, and stubbornly high inflation of between 6% and 11%.

“Several of the most vulnerable emerging markets in terms of external balances — Turkey, South Africa and Brazil — have not yet seen their currencies fall to fair value,” UBS noted this week. HSBC Chief Economist Stephen King said some of the weakest were experiencing a loss of competitiveness similar to that seen in countries of the eurozone periphery before the euro crisis.

Political upheaval is another thing they have in common, and may be the single factor that determines whether they can bounce back or not. The Fragile Five all face elections at some point in 2014, making painful reforms even less likely.

Any (prospective) profits from emerging markets are now in danger: you can make a 20% profit on your money, but if a government devalues its currency by 25%, you’re still a loser. Why take the risk?

• Carry Trade Doesn’t Shine in Emerging Currencies (WSJ)

With central banks hiking interest rates from Turkey to South Africa, some analysts and investors are predicting a new golden age for the carry trade. Others aren’t so sure. How the trade works: investors borrow in a currency from a country where interest rates are low, such as dollars or yen. They then exchange it for a currency where rates are higher. The wider the gap between borrowing costs and yields, the bigger the profits.

In theory, Turkey hiking its main policy rate from 4.5% to 10% should be a carry trade bonanza. A bet on the lira using dollars as a funding currency now offers investors three percentage points in annual returns once Turkey’s inflation rate is factored into the equation.

Actually securing those returns is another matter entirely. Since last year, the unfettered slide in emerging-market currencies has taken the zing out of carry trades. Just this year, the lira has dropped by 3.06% against the dollar, more than the potential gains from a carry trade involving the two currencies. “The volatility in emerging currencies has been so high that one-month’s carry can be wiped out in an hour’s move in the spot market,” said Nima Tayebi, portfolio manager at J.P. Morgan Asset Management. [..]

Societe Generale put a stop to its long Turkish lira vs the rand trade recommendation Wednesday morning, a mere 16 hours after it had suggested the trade on the back of sharp rise in Turkey’s policy rates. [..] “At some point, systemic worries can overwhelm the attractiveness of the carry trade,” said Vijai Mohan, founder of Hyphen Fund Management.

One thing we haven’t discussed in depth about China – though I did mention it – is the amount of foreign capital invested in the Chinese economy, and more interestingly, its shadow banking system. Where is Goldman in China?

• The $15 trillion shadow over Chinese banks (Telegraph)

Drawing attention to the problems at an individual bank is never likely to make you popular, but calling time on an entire financial system is another thing entirely. For eight years, until her resignation last month, Fitch banks analyst Charlene Chu has done just that, warning of the impending collapse of China’s debt-fuelled bubble.[..]

In a country where the banks, even the largest, are not known for openness, Chu has warned since 2009 about a rapid expansion in lending that has seen something close to $15 trillion (£9.1 trillion) of credit created, fuelling a property and infrastructure boom that has no equal in history.

Chu has explained the creation – from a standing start just five years ago – of a shadow banking industry in China that today is responsible for as many loans in terms of volume as the country’s entire mainstream financial system.[..] “The banking sector has extended $14 trillion to $15 trillion in the span of five years. There’s no way that we are not going to have massive problems in China,” she says.

And yeah, take that one step further and China starts to weigh on the global economy.

• Currency crisis at Chinese banks ‘could trigger global meltdown’ (Telegraph)

The growing problems in the Chinese banking system could spill over into a wider financial crisis, one of the most respected analysts of China’s lenders has warned. Charlene Chu, a former senior analyst at Fitch in Beijing and now the head of Asian research at Autonomous Research, said the rapid expansion of foreign-currency borrowing meant a crisis in China’s financial system was becoming a bigger risk for international banks.

“One of the reasons why the situation in China has been so stable up to this point is that, unlike many emerging markets, there is very, very little reliance on foreign funding. As that changes, it obviously increases their vulnerability to swings in foreign investor appetite,” said Ms Chu.

Ms Chu has been warning since 2009 about the growth of a shadow banking system in China that has helped fuel the credit expansion seen in the country in the wake of the Western financial crisis. However, fears are growing that the build-up of foreign borrowing by the Chinese, particularly in US dollars, is creating an even greater build-up of risk than that seen before the crisis of 2008.

The EU should be abolished and its buildings razed. Instead, they leak reports to press about losses caused by other people; not them. Let’s look at what Brussels costs instead. And what it returns.

• Corruption across EU ‘breathtaking’ (BBC)

The extent of corruption in Europe is “breathtaking” and it costs the EU economy about 120bn euros (£99bn) annually, the European Commission says. EU Home Affairs Commissioner Cecilia Malmstroem will present a full report. Writing in Sweden’s Goeteborgs-Posten daily, she said corruption was eroding trust in democracy and draining resources from the legal economy.

For the report the Commission studied corruption in all 28 EU member states. “The extent of the problem in Europe is breathtaking, although Sweden is among the countries with the least problems,” Ms Malmstroem wrote.

The Commission says it is the first time it has produced such a report. It also makes recommendations on how to tackle corruption. National governments, rather than EU institutions, are chiefly responsible for fighting corruption in the EU. The EU has an anti-fraud agency, Olaf, which focuses on fraud and corruption affecting the EU budget, but it has limited resources. In 2011 its budget was just 23.5m euros.

Ms Malmstroem said that in some countries public procurement procedures were vulnerable to fraud, while in others party financing was the main problem, or municipal bodies were badly affected. And in some countries patients have to pay bribes in order to get adequate medical care, she wrote.

Well, that’s a surprise ….

• Banks use new loophole to defy EU bonus ban (Sunday Times)

Banks could still pay top staff bonuses worth eight or nine times their basic salary after finding a way to sidestep European limits on annual payouts. The loophole hinges on the payment of monthly “allowances” that will boost banker’s take-home pay and multiply bonus payments. Widespread use of the loophole — the “overwhelming majority” of big banks are expected to use it this year, according to the accountancy firm PwC — will stoke further anger over City pay.

Even Royal Bank of Scotland, which remains 81%-owned by taxpayers, is considering using the trick, according to City sources. Barclays and Goldman Sachs are already known to be deploying the scheme. City pay remains high despite repeated calls for it to fall in the light of the 2008 financial crisis, which triggered the recession.

The EU and IMF are squeezing the Greek people just slow enough that they don’t raise a fully armed protest. Yet.

• Germany preparing third financial rescue for Greece (Guardian)

Germany has signalled it is preparing a third rescue package for Greece – provided the debt-stricken country implements “rigorous”austerity measures blamed for record levels of unemployment and a dramatic drop in GDP. The new loan, outlined in a five-page position paper by Berlin’s finance ministry, would be worth between €10bn to €20bn (£8bn-16bn), according to the German weekly Der Spiegel, which was leaked the document. [..]

Greece faces a financing gap of up to €15 billion over the next two years, according to foreign creditors, which have kept its economy afloat since May 2010. As the EU’s powerhouse, Berlin has bankrolled most of the emergency loans to date. But a German finance ministry spokesman, echoing similar statements by Schäuble, denied that a further restructuring of Greece’s staggering debt – this time by public creditors – was also on the cards. [..]

“They are missing the point: Greece does not need a third bailout, it needs debt restructuring,” said the shadow development minister and economics professor, Giorgos Stathakis. “Even in the IMF, logical people agree there is no way we can have any more fiscal adjustment when the whole thing has reached its limits,” he said. “There is simply no room for further cuts and further taxes and that is what they are going to ask for.” He said the assistance was “the wrong thing at the wrong time”. Unemployment is nudging 28% – and youth unemployment rate tops 60%.

Ditto for Italy.

• Italy is wasting away month by month (AEP)

Today’s headline from Italy is that unemployment has at last begun to fall, dropping from 12.8% to 12.7% in December. Drill deeper and the recovery story turns to dust. The number employed in Italy has fallen by 424,000 over the last year. Piangi Italia mia. As you can see from the chart below (only available on ISTAT’s Italian site), the slide has been relentless. There is no sign of stabilisation. A further 25,000 dropped out of the work force in December alone.

The overall employment rate has fallen to 55.3, a staggeringly low level. The rate for men has fallen by 1.6 percentage points over the last year. Youth unemployment was 41.6% despite a tide of emigration to Britain, Germany, and beyond. It is at Greek and Spanish levels above 50% in Naples and across much of the Mezzogiorno.

Oh wait, a “banks vs people” story. Can you guess the outcome?

• Detroit files lawsuit seeking to void pension debt (Reuters)

Detroit on Friday filed a lawsuit in U.S. bankruptcy court seeking to invalidate $1.44 billion of debt sold to fund public worker pensions – a move that also could void the ill-fated interest-rate swaps contracts that were a factor leading Detroit into bankruptcy. The lawsuit contends the city and its retirement systems violated Michigan law when they set up “sham” service corporations and funding trusts to facilitate the debt sales in 2005 and 2006. All other contracts or obligations connected to the debt are also void, the lawsuit claims.

Detroit in its lawsuit said the pension debt was “nothing more” than a borrowing by the city, and it violated borrowing limits imposed on Detroit by the state of Michigan. In the suit, Detroit asked bankruptcy judge Steven Rhodes to issue a judgment declaring the city is not obligated to continue making payments on the so-called pension certificates of participation (COPs). The COPs were issued during the term of former Mayor Kwame Kilpatrick, now in prison on federal corruption charges.

“This deal was bad for the city from its onset despite reassurances it would adequately resolve the city’s pension issues,” Kevyn Orr, Detroit’s state-appointed emergency manager, said in a statement. “We have tried without success, to negotiate a resolution to this dispute and to allow the city and its taxpayers to move forward and unwind these illegal transactions.”

A ruling in the city’s favor could invalidate the interest-rate swap contracts Detroit reached with investment banks UBS AG and Merrill Lynch Capital Services, a unit of Bank of America Corp. The swaps were meant to hedge interest-rate risk arising on variable-rate COPs, and Detroit in the lawsuit claims any contract arising from the COPs would be invalid from the start since “all other obligations incurred by the city in connection with the COPs transactions are unenforceable and void.”

No, it’s not just around the corner, Phoenix Capital, it’s here.

• Is the Next Great Bear Market Collapse Just Around the Corner? (Phoenix Capital)

The financial markets hit yet another series of bumps a week ago. Those bumps are:

1) Turkey’s financial meltdown.

2) China’s shadow banking issues.

3) Argentina veering towards default.While these economies are all markedly different, the common theme behind their current financial woes pertains to one dreaded word: DEFAULT.

The biggest problem with the epic Central Bank rig of the last five years is that propping up a bankrupt financial system by printing money only works for so long. The reason for this is that no one, whether it be a country, company, or person, can defy mathematics. A loan can be extended, it can be restructured, or it can be finagled in countless financial ways. But at the end of the day, if your creditors lost faith in your ability to repay it… it’s GAME OVER.

This issue is now beginning to ripple throughout the emerging market space.Moreover, the US equity market has entered a kind of mania a may in fact be topping. Take note of the following:

1) Investors piling into stock-based mutual funds at a pace not seen since the Tech Bubble.

2) Margin debt (debt investors take on to buy stocks) at a record high.

3) Market leaders (Tesla, Netflix, Amazon, etc.) showing clear signals of investor rotation.

4) Corporate profit margins at record highs and primed to fall.

5) Market breadth shrinking (meaning fewer stocks participating in the rally).

6) The VIX (a measure of investor sentiment) dropping to levels of complacency not seen since 2007.

7) Investor bullishness hitting record highs and investor bearishness hitting record lows.

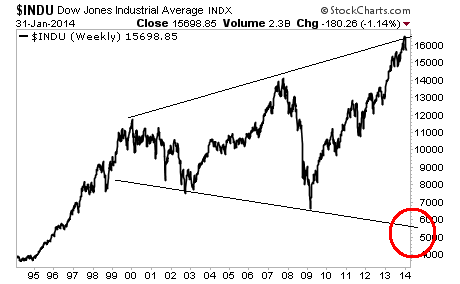

8) Investment legends either returning capital to investors (Icahn, Klarman) or sitting on mountains of cash (Buffett).In simple terms, the bull market of the last five years finally went into mania mode as retail investors stopped worrying about income (investing in bonds) and drank the Fed’s Kool-Aid: bought stocks. The blow off/ mania component of the rally occurred when retail investors began to pile into stocks (as is always the case with tops) around the end of 2012/ early 2013. Whenever this period ends, the chart of the DOW shows where we’re likely going:

Be smart… prepare in advance.

This article addresses just one of the many issues discussed in Nicole Foss’ new video presentation, Facing the Future, co-presented with Laurence Boomert and available from the Automatic Earth Store. Get your copy now, be much better prepared for 2014, and support The Automatic Earth in the process!

Home › Forums › Debt Rattle Feb 3 2014: The Future Of Our Children Is Taking Shape Today