William Henry Jackson Eureka, Colorado 1899

Remember how at the start of the current crisis, 2007/8, “leaders” and policy makers would state on a regular basis that they were forced to move into “uncharted territory”? Guys like Ben Bernanke were fond of it, presumably to cover their bee hinds if things would turn out wrong. I was thinking today, you never see that term anymore, not for quite a while. Well, when the US breaks through debt ceiling number 826, yes, but not from central bankers when they talk about stimulating the economy. Which is a little peculiar, because if they were in uncharted territory back then, boy, look at where they’re now. The right term for that probably must still be invented.

But they never even hint at being in uncharted territory anymore. They act as if they have it under control, as if they know exactly what they’re doing, and they can see way ahead into the future to boot. Looking back to 2007/8, and their demeanor back then, that doesn’t seem very likely, though. If they had no clue – which is what uncharted territory means – back then, when they pumped a few hundred billion into primary dealers, why would we presume they do now, while they do that on a weekly or monthly basis?

Central bankers have two tools they use all the time, whether they’re in Washington, Brussels or Beijing. 1) They force down interest rates and 2) They buy up – mostly bad – debt (this is most often labeled easing, or money printing, terms that don’t really cover the actual process). And then they look around and tell themselves that their actions have worked. Sure, they know GDP and jobless numbers are being polished up artificially, but with stock markets at record highs, what’s not to like?

That’s perhaps why they stopped talking about uncharted territory: what they did seems to have worked, so they tell themselves in retrospect they must have known what they were doing, and it wasn’t all a big gamble. When Bernanke waved goodbye last week, he certainly no longer felt he needed a cop-out to hide behind. He left feeling like a victor.

But then we look at the year so far, and we see emerging markets acting like damsels in dire distress, and western stock markets nervous and falling. The ECB just announced they’ll leave their interest rate target at 0.25%, despite the fact that large parts of Europe are in deflation, and people wanted another rate cut.

Draghi will probably say later today that he’ll stop sterilizing his bond purchases, something like that, provided Germany does a 180 and accepts a bigger ECB balance sheet. That’ll make a bunch of credit available to banks, sure, but it won’t do a thing to fight deflation. Deflation means people stop spending, and wages stop rising. Draghi may claim deflation is not a worry, and has perhaps resigned himself to waiting for good news from EU nations. Like Greece. And France. Yeah. Sure. Mario will make some general remark about “signs of recovery”, and hope doing nothing is seen as a sign of strength.

In fact, Mario Draghi may have come upon a stretch of uncharted territory he doesn’t like one bit, the looks of which scare him too much to move forward. And that may be the best news Europeans have had in a long time. It will cause chaos and mayhem, no doubt, but the way things have been going, everyone is only being set up for far more severe mayhem down the road. Why would we want to postpone it all the time, just to see it grow worse? We screwed up, big time, and as we say around here, you got to own your crap, right? Let’s clean up the mess and move forward, instead of letting the “career fear” of politicians and regulators drag us down ever further into what, guaranteed, will really be uncharted territory, unless you want to mention 1294 or 1873.

The pile of debt we’ve collected is as uncharted as the dark side of the surface of Jupiter’s moons. And we’re not going to make it go away by piling more debt on top of it. In a best case scenario for us, it’ll annihilate our kids’ futures. But is that what we want?

As for the stock markets, that shining beacon of recovery and optimism, SocGen’s uber cuddly uberbear Albert Edwards predicts they’ll be “locked in a ‘Freddy Kruger-Like’ nightmare”, while Marc Faber says the US markets will come down 20-30%, but should really fall 40% to become attractive again.

And you might say: those guys are always pessimistic, look at how great we’re doing, and many people say exactly that, but if that were the real story, then how does one explain away the notion that the entire global QE family has lifted those markets to where they stand today, knowing QE can’t go on forever? At the end of the day, it’s still simply shoveling more debt upon a mountain of debt already easily unprecedented in history (and history’s seen a few).

The British government has grown fond of using the term “escape velocity”, which supposedly means that if they just frack the entire nation to bits, squeeze the poor till they’re all so dry no clean unfracked drinking water is needed, and sell every single home in London to Asian dieselgarchs who’ve gotten rich off of China shadow banking virtual fantasy yuan printing, the UK economy will set off for the stratosphere selling its exports to all the countries who were neither so smart nor so lucky, and don’t have a penny left to buy those exports with. Escape velocity is empty political rhetoric. And there’s plenty of that. Spin doctors must be busier and more in demand than ever before. There’s such a load of nonsense being sold on a daily basis.

You can of course wait for the markets to fall. And whether it’s 20% or 40% is immaterial. It’ll lead to absolute panic. And when the smoke clears your wealth, your pensions, everything you don’t have hidden away, will be used to once again prop up the financial system that can’t be allowed to fail “or else”. Well, you’ll already be squarely inside the “else”. How to prevent the worst of this? Open the banks, their books, their vaults. Burn everything that smells too much like it’s died. Secure people’s deposits up to a maximum. Go through the hundreds of trillions in derivatives, and clear them. At the same time, set up new banks, real small, get rid of the glass monstrosities and design some nice parks where they stood in lower Manhattan. Preferably with edible crops and lowers.

But as I said, you can also wait for things to happen, markets to plunge, and see how uncharted the territory can become.

• The Countdown To The Nationalization Of Retirement Savings Has Begun (Casey’s)

Simply put, the new myRA program put forward by Obama is at best a sucker’s deal… or worse, it’s a first step toward the nationalization of private retirement savings. Even before the new myRA program was announced, there had been whispers about the need for the US government to assume some risk for US retirement accounts. That’s code for forced conversion of private retirement assets into government bonds.

With foreigners not buying as many Treasuries and the Fed tapering, the US government has been searching for new buyers of its unwanted debt. And this is where the new myRA program comes in. In short, it’s ostensibly a new way for people to save for retirement. Of course, you can only invest in government-approved investments—like Treasuries—which probably won’t even come close to keeping up with the real rate of inflation. It’s like Jim Grant says: “return-free risk.”

In reality, a myRA doesn’t really provide any significant new benefits over existing options. To me it just looks like a way for the US government to pass the hot potato on to unsuspecting Americans in exchange for their retirement savings. The net effect is the funneling of more capital to Treasury securities and thus helping the US government finance itself. [..]

As bad as it is to deceive naïve Americans into trading their hard-earned retirement savings for garbage (i.e., Treasury securities), the myRA program potentially represents something far worse… the first step toward the nationalization of existing private retirement accounts. I believe myRA is a way to nudge the American people into gradually becoming more accustomed to government involvement in their private retirement savings.

It’s incorrect to assume nationalization couldn’t happen in the US or your home country. History shows us that it’s standard operating procedure for a government in dire financial straits. In just the past six years, it’s happened in some form in Argentina, Poland, Portugal, Hungary, and numerous other countries.

To me it’s self-evident that most Western governments (including the US) have current debt loads and future spending commitments that all but guarantee that eventually—and likely someday soon—they will try to unscrupulously grab as much wealth as they can. And retirement savings are a juicy target—low-hanging fruit for a desperate government.

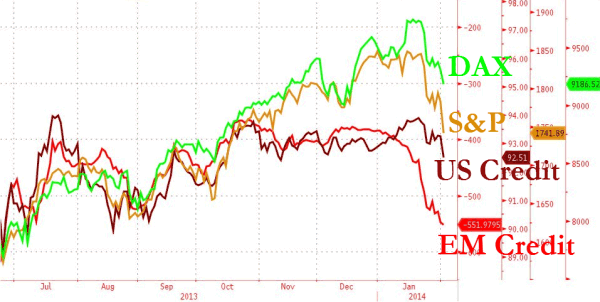

Great. Graph. Any more questions?

• What Happens Next? (Zero Hedge)

What goes up (via free money and practically infinite leverage and rehypothecation) must come down (when the flow slows)… the dominoes are falling… First Emerging Markets, then US High-yield credit, then US Stocks, and now European stocks…

… and remember – this “selling” overseas does not mean “buying” domestically as the majority of these hot money flow trades are credit-funded and merely extinguish the debt at the margin…

Albert with nice metaphors.

• Albert Edwards: Markets Will Be Locked In A ‘Freddy Kruger-Like’ Nightmare (BI)

“Our warnings throughout last year that an unravelling of emerging markets (EM) was the final tweet of the canary in the coal mine have still not been taken on board”

“The ongoing EM debacle will be less contained than sub-prime ultimately proved to be. The simple fact is that US and global profits growth has now reached a tipping point and the unfolding EM crisis will push global profits and thereafter the global economy back into deep recession.”

“One thing [SocGen’s Andrew Lapthorne] has been highlighting for some months is just how incredibly anaemic profits growth has been in both the developed and emerging markets, the latter being particularly poor having contracted for the past two years,”

“The dire profits situation will only get worse as EM implodes and waves of deflation flow from Asia to overwhelm the fragile situation in the US and Europe.”

“And even if the Fed resumes massive QE at some point as the world melts down, and markets desperately attempt their return to the dream trance, they will instead find themselves locked into a Freddie Kruger-like nightmare in which phase 3 of this secular bear market takes equity valuations down to levels not seen for a generation.”

Marc Faber states the obvious: stimulus bubbles have – among others – turned into equities bubbles, and stocks are way overvalued. Wait till they revert to reality.

• Marc Faber: US Stocks Need To Drop 40% To Become Attractive (CNBC)

“The market is way overdue for a 20% to 30% drop,” Marc Faber warns, “you won’t “hear this view from someone who is fully invested,” but “I hope the market drops 40% so stocks will become – from a value point of view – attractive.” “… the experience with quantitative easing is a complete failure. It has lifted asset prices and created asset inflation, but it hasn’t lifted the standard of living of most people in the U.S. nor worldwide.”

Could it be we finally have someone who does pull and push through? Lawsky’s already threatened to revoke one banking licence, let’s see if he has the guts to do it again, and make good on the threat. But let’s not get out hopes up just yet, shall we?

• NY Regulator Lawsky to Open Currency Probe of Over Dozen Banks (Bloomberg)

Benjamin Lawsky, New York’s top financial regulator, has asked more than a dozen banks including Goldman Sachs and Deutsche Bank, for documents related to their currency trading practices, a person familiar with the matter said. Lawsky also requested information from Lloyds, RBS, Credit Suisse and Standard Chartered, according to the person, who asked not to be identified because the investigation isn’t public. Lawsky has asked for traders’ e-mails and instant messages to review whether they manipulated currency rates, the person said.

At least 20 people have been fired, suspended or put on leave by banks since Bloomberg News reported in June that employees at some firms shared information about their currency positions with counterparts at other lenders. At least a dozen regulators and agencies on three continents are investigating the rigging allegations.

Lawsky, the superintendent of New York’s Department of Financial Services, has authority over financial institutions chartered in his state, including several non-U.S. banks that do business in the country. While Lawsky isn’t authorized to bring criminal charges, he can make referrals to prosecutors, according to Bartlett Naylor, a lobbyist for Public Citizen, a Washington-based consumer group. “You have a law enforcer with zeal who no doubt has numerous weapons, and he’s prepared to deploy them on behalf of the law and on behalf of consumers,” Naylor said in an interview. “The record shows that’s missing in so many other places including the federal level.”

In August 2012, Lawsky garnered attention when he made public statements about possibly revoking Standard Chartered’s banking license over the bank’s violations of U.S. sanctions involving dollar transfers to Iranian clients. Standard Chartered’s stock dropped 16% the day of Lawsky’s comments. A week later, the bank agreed to pay $340 million to resolve the matter. Other regulators followed, and the bank agreed to pay an additional $327 million for the conduct in December 2012.

At least Lawsky’s touched a nerve or two. But that’s not nearly enough.

• Currency Market Unsettled by Trader Exits on Lawsky Probe (Bloomberg)

The foreign-exchange trading business was in upheaval across Wall Street as senior executives resigned and others were fired amid an expanding probe of possible currency manipulation.

Benjamin Lawsky, superintendent of New York’s Department of Financial Services, asked more than a dozen firms including Deutsche Bank, Goldman Sachs and Citigroup for documents on their currency-trading practices. Deutsche Bank, the top foreign-exchange trader, fired four dealers after an internal probe. Goldman Sachs lost two partners while Citigroup said its foreign-exchange chief will leave in March.

Lawsky’s investigation is at least the 12th opened by authorities in Europe, the U.S. and Asia since Bloomberg News reported that traders at the world’s largest banks colluded to manipulate the benchmark WM/Reuters rates. Even staff who aren’t being probed are reassessing career plans as the scandal forces firms to change fundamental practices as revenue falls.

“Currency traders are now sitting in an unprecedented and unwelcome spotlight,” said John Purcell, chief executive officer of Purcell & Co., a London-based executive-search firm. “Regulatory pressures, scandals and attendant reputational issues are making it a much more challenging environment.”

At least 16 traders have been suspended or put on leave amid the global probe. Citigroup last month fired European spot trading chief Rohan Ramchandani.

Ambrose is always good for some juicy numbers. He’s the first one I’ve ever seen mention, apart from myself, that to get a somewhat realistic inflation number, you must subtract rising taxes. Or any government could always escape deflation by taxing more, and inflation by taxing less. How obvious does it have to get?

• ECB plays game of chicken with deflationary forces (AEP)

The US and China are withdrawing stimulus on purpose. The eurozone is doing so by accident, letting market forces drain liquidity from the financial system for month after month. The balance sheet of the European Central Bank has fallen by €553bn over the past year as banks repay money that they no longer want, either because ECB funds are too costly in a near-deflationary world or because lenders are being compelled by regulators to shrink their books.

This is “passive tightening” or “endogenous tapering”. The ECB balance sheet has plummeted to 23% of eurozone GDP from a peak of 32% in July 2012. Hardliners will be delighted to learn that we now have synchronized G3 global tightening at last, further compounded by enforced tightening in Brazil, India, Turkey, South Africa and a string of emerging market states trying to defend their currencies. At least two-thirds of the global economy is turning down the liquidity spigot.

The eurozone has been growing just enough on export growth and a burst of restocking to create the illusion of recovery, though business investment continues to fall each month, dropping to modern-era low of 18.9%. (It was 21% even during the depths of the dotcom bust in 2003.) Retail sales fell 1.6% in December, the biggest drop for two-and-a-half years. The unemployment rate has stabilised at 12%, but only because so many people have dropped off the rolls or fled abroad. Italy has lost a further 425,000 jobs over the past year.

Euroland is sliding further into Japanese deflation trap every month, whatever they claim in Frankfurt. Passive tightening has caused private sector loans to fall by €155bn over the past quarter. “The ECB’s insistence on waiting for more evidence of deflation is a dangerous gamble. Delays are costly, and risk allowing pathologies to fester,” said Ashoka Mody, formerly at the IMF.

Core inflation has fallen to 0.6% when you strip out taxes. The ECB has failed to meet its own 2% inflation by a shocking margin, and missed its 4.5% M3 money supply target (If it remembers that it had one) by an even bigger margin, and is therefore in breach of its EU treaty obligations. It has ignored pleas for action from the IMF and the OECD.

• Draghi as ECB Master of Suspense Keeps Investors on Edge (Bloomberg)

Mario Draghi’s habit of springing surprises means that few can say what he’ll do when European Central Bank officials decide on monetary policy today.

Inflation at a four-year low and volatile market rates speak for further action by the Governing Council, even after it cut official rates to record lows in November. At the same time, signs of economic improvement and the central bank’s prediction that price gains will gradually return to target suggest the ECB president may prefer to hold fire.

Expectations aren’t always a guide to the actions of Draghi, who has confounded investors with two rate cuts they didn’t see coming and unconventional efforts to keep the euro intact. With the currency bloc’s fragile recovery also threatened by turbulent global markets and the fallout from the U.S. Federal Reserve’s tapering, the chances are rising that he’ll announce another unprecedented measure. “There is a powerful case for the central bank to do more, and there’s a high chance they will ease policy somehow,” said Nick Kounis, head of macro research at ABN Amro Bank NV in Amsterdam. “That may not be through a rate cut.”

Kounis joins economists from Goldman Sachs Group Inc. to Nomura International Plc who say Draghi may sidestep a rate cut by ending the sterilization of crisis-era bond purchases. Halting those operations, which soak up money created by the ECB’s now-terminated Securities Markets Program, would add about 175 billion euros ($237 billion) to the financial system. The option has become more likely since Germany’s Bundesbank, a critic of the SMP, expressed support for ending the weekly absorption in the absence of inflation risks. Sterilization was put in place to assuage concern that the bond purchases would fuel price rises.

A halt would double the amount of excess liquidity, “have a strong impact on smoothing market volatility and put downward pressure on rates,” said Nick Matthews, senior economist at Nomura in London. “It would be a powerful signal that the ECB can do unsterilized bond purchases.”

Mr. WiIders has another report to present, and it says what he wants it to say. More fodder for his May EU election campaign. He’s already by far the biggest Dutch party for that. Don’t count out the euro-skeptics, they can’t be brushed aside anymore.

• Geert Wilders outlines case for a Dutch ‘Nexit’ from the EU (FT)

Geert Wilders, leader of the far-right Freedom Party (PVV) that is leading in Dutch polls for May’s European parliament elections, presented a study on Thursday that claims the Netherlands would be better off if it left the EU and urged voters to support his call for “Nexit”. The study, by the consultancy Capital Economics, claims the Dutch economy would quickly emerge from its current sluggishness to brisk growth, generating billions of euros – or new Dutch guilders – in fresh revenues for debt-laden Dutch households.

“Leaving the EU or Nexit will not only restore our national sovereignty but it will also boost the Dutch economy now and in the future”, Mr Wilders said in The Hague. “It also offers the Netherlands a way out of the crisis . . . Nexit will create jobs; the income of our citizens and companies will grow”.

Mr Wilders is one of a handful of populist leaders in the EU – including Marine Le Pen in France; Nigel Farage in Britain and Alexis Tsipras in Greece – whose sharp anti-Brussels rhetoric has helped push them into either first or second place in public opinion polls ahead of May s Europe-wide vote. The Netherlands is one of the founding members of the EU, and has long been seen as a core supporter of a more integrated Europe. Yet public opinion polls reveal growing support across the country for a renegotiation of powers with Brussels over a number of policy areas, including access to domestic welfare for other EU citizens.

“Nexit means that we no longer have to pay billions to Brussels and weak southern European countries”, added Mr Wilders. “We can save billions by liberating ourselves from EU regulations. We can end the mass immigration and stop paying welfare checks to, for instance, Romanians and Bulgarians”. According to a recent poll by the Dutch daily De Telegraaf, the PVV would win the most European parliament seats in May’s elections.

Mark Pragnell, one of the authors of Capital Economics report, said that the Netherlands would be significantly richer if it left the EU and the single currency, despite a short period of volatility.

“The economic and policy freedoms that an exit from the EU will give Dutch policy makers, especially in the long term, provide an opportunity for the Netherlands to see rates of growth in prosperity that have looked otherwise consigned to distant history”, Mr Pragnell said. “There are, of course, risks to leaving the union, but they are modest and manageable”.

If the Dutch opted for “Nexit” the country’s economy would be 10% bigger by 2024, adding €9,800 in the pockets of each household, according to the report. The report said that most of the gains would come from a reduction in the costs of doing business in the Netherlands, growing exports to emerging markets, greater control of its fiscal and monetary policy as well as ending financial contributions to the EU’s budget.

Capital Economics, a London-based economic research firm, has become a leading voice for eurozone break-up, last year winning a £250,000 prize from a British think tank for its proposal on how to end the single currency.

If Berlin and Brussels so much as try to force new austerity measures on Greece, they have another thing coming. Good news from Greece? Who believes that?

• Greece Plans to Impress Creditors With Good News (Spiegel)

New loans are welcome, but don’t ask us for any new austerity measures. This pretty much sums up Athens’ reaction to Germany’s reported willingness to approve further loans to Greece to cover the country’s multi-billion euro projected financing gap in 2015-2016. Government sources say that Berlin’s intentions were known to Prime Minister Antonis Samaras, adding that Germany will not pull the rug from under Greece’s feet, especially with the European election due in May.

But the Greek government has also made clear that it will not accept a new round of measures or a continuation of what are perceived by many in Greece as the asphyxiating and humiliating controls by the troika of European Commission, European Central Bank and International Monetary Fund.

Finance Minister Yannis Stournaras is preparing Greece’s position ahead of the troika’s arrival. With a fresh round of bargaining looming on the new loans, he promised an avalanche of “impressively good news” in the coming days to show that Greece doesn’t need any further belt-tightening. It only needs to press on with its structural reforms, he said.

According to a Greek Finance Ministry official, the good news will include the first increase of retail sales in 43 months, and the first rise in the purchasing managers’ index in 54 months. The “super-weapon” in Stournaras’ arsenal, however, is the hefty 2013 primary budget surplus, now estimated at €1.5 billion, well above the official budget forecast of €812 million.

Another warning signal for and from Japan. Abe has less than two months left before his April 1 sales tax raise takes effect and purchases will fall off a ladder. But wages are not rising, they’re even falling. How could this ever be remedied in 7 weeks? It’s too late.

• Japan Real Wages Fall to Global Recession Low in Abe Risk (Bloomberg)

Japan’s base wages adjusted for inflation last year matched a 16-year low in 2009 when the world was gripped by recession, posing a risk to consumer spending as the nation girds for a higher consumption tax. Pay excluding bonuses and overtime payments dropped to 98.9 in 2013 on a labor ministry index released today that takes price changes into account, equaling the level four years earlier. The gauge is based at 100 in 2010 in data back to 1990.

Prime Minister Shinzo Abe is calling on firms to boost wages to sustain a reflationary effort so far driven by stimulus and the yen’s 18% drop against the dollar last year. Amid a backdrop of market turbulence, business and union leaders met today to start annual pay talks – due to end in March, a month before a 3% increase in the sales levy.

Puerto Rico is America’s version if Portugal, like Detroit is its Cyprus. But who in Washington will stand up to protect it?

• Puerto Rico needs to prepare for its default (Reuters)

What you’re seeing here is a vicious cycle: as debt problems pile up, economic activity decreases, which causes even bigger debt problems, even lower economic activity, and so on. Puerto Rico is now shrinking at a 6% annual pace, and that number is probably going to get worse before it gets better. The chances of the island’s economy actually growing at any point in the foreseeable future seem remote: indeed, the country has essentially been in one long and nasty continuous recession since 2006.

Puerto Rico has $70 billion in debt outstanding, all of it needing to be repaid with interest — and the simple fact is that there’s no way it’s going to be able to do that, if its economy continues to shrink and its most talented nationals continue to decamp for the mainland, where their prospects are much brighter. Labor mobility from Puerto Rico to the rest of the US, and particularly to Florida, has never been higher, while most of the migration in the other direction comes in the form of retirees, who are not exactly going to kick-start the economy. In fact, in terms of the labor force participation rate, they’re just going to make matters worse, on an island where only 1.2 million of the 3.4 million inhabitants are employed.

In many ways, Puerto Rico is similar to those other tourist destinations, Portugal and Greece — it’s highly indebted; it’s not particularly well educated (only half of Puerto Ricans over 25 have graduated from high school, and only a quarter of high-school graduates go on to get a bachelor’s degree); and it is hobbled by being unable to devalue its currency.

All of this is a clear recipe for default: if Puerto Rico can’t repay that $70 billion in debt, then it won’t. The only alternative is a bailout — but as Martin Sullivan explains, the US government has already extended a back-door tax-code bailout worth some $2 billion per year, and even that is both insufficient and constitutionally dubious. A more explicit bailout is not going to happen — not when Detroit is being left to deal with the ravages of bankruptcy on its own.

Oh great! Oblige bankers to swear to God to be good and responsible people. This way, when caught cheating, they can always say “I don’t believe in God”. One staunch supporter of the pledge is the CFO (since 2004) at Rabobank, where he oversaw the actions that have led to a $1 billion fine and a whole slew of as yet unfinished legal investigations. Change you can believe in.

• Dutch Bankers Swear to God as Trust in Lenders Slumps (Bloomberg)

“I swear that I will do my utmost to preserve and enhance confidence in the financial-services industry. So help me God.” The oath, the first of its kind in Europe, became binding on board members of Dutch banks last month as the government sought to rein in an industry with assets more than four times the size of the country’s economy. All 90,000 Dutch bank employees must take the pledge, or a non-religious affirmation, starting the second half of this year.

They’ll be punished should they break new ethical rules, Banking Association Chairman Chris Buijink said in an interview in Amsterdam. Dutch bankers who fail to abide by the new rules may be blacklisted, face fines or suspensions, Buijink said. The revised code will be completed within months and disciplinary sanctions will be applied at the start of next year.

Bert Bruggink, chief financial officer at Rabobank Groep, the Dutch bank fined $1 billion in October for its part in a global interest rate-rigging scandal, took the oath last year in a ceremony with Lense Koopmans, the supervisory board chairman who has since left the company. He said the words were a confirmation of the ethics he already sticks to. “It’s a good signal to your employees and brings back awareness of the importance of these values,” said Bruggink, 50, who’s been CFO of the biggest Dutch mortgage lender since 2004. “It fits in with these times, where banks have to work hard to restore trust.”

Many aspects of the new disciplinary system remain unclear. Dutch banks have almost a year to set it up. There would be a disciplinary commission or tribunal similar to those policing the country’s brokers, investment advisers and medical profession. The system would apply to all bank employees taking the oath.

While Dutch bankers need to take the new ethical rules seriously, implementation may present challenges, Jonathan Soeharno, a lawyer at De Brauw Blackstone Westbroek in Amsterdam, said by telephone. “Other professions, such as lawyers and doctors, have a long-standing tradition of ethics,” he said. “With bankers, however, we don’t really know what the professional standards entail. More so, we don’t really know what ‘‘the banker” is. There is a large variation of roles within the industry.”

“An oath can be effective only if it is part of a broad reform program,” John Boatright, a professor of business ethics at Loyola University Chicago, said in an e-mailed response to questions. “It could be highly effective when combined with more stringent regulation and a more detailed code of conduct.”

The cost of bank rescues in the Netherlands contributed to an increase in national debt to an estimated 75 percent of gross domestic product in 2013 from 46 percent in 2007. The budget deficit grew to as much as 5.6 percent of GDP since the crisis, the widest since 1995.

The financial services industry is the least trusted of all industries globally, according to a survey of 31,000 people in 26 countries published by public-relations firm Edelman two weeks ago. 13% of Dutch citizens see banks’ performance as good or excellent compared with an average of 33% globally, the survey showed. 34% of Dutch citizens expressed trust in the finance industry last year compared with 90% in 2008 [..]

What to think of this? A Boston based company that stores information for 150,000 companies in 36 countries just had its third big fire, at a time when Argentina’s economy is under severe pressure, the government is under fire for fudging statistics and the central bank was about to limit its banks’ foreign exchange positions. Is that worth 9 human lives?

• Argentina Banking System Archives Burned in Deadly Fire (AP)

Nine first-responders were killed and seven others injured as they battled a fire of unknown origin that destroyed an archive of corporate and banking industry documents in Argentina’s capital on Wednesday. The fire at the Iron Mountain warehouse took hours to control and at least half of the sprawling building was ruined despite the efforts of at least 10 squads of firefighters. The destroyed archives included documents stored for Argentine corporations and banks, said Buenos Aires security minister Guillermo Montenegro.

If the cause is found to be arson, it wouldn’t be the first time for Boston-based Iron Mountain Inc., which manages, stores and protects information for more than 156,000 companies and organizations in 36 countries. Fire investigators blamed arson for blazes that destroyed its warehouses in New Jersey in 1997 and London in 2006, prompting rounds of legal claims over lost records.

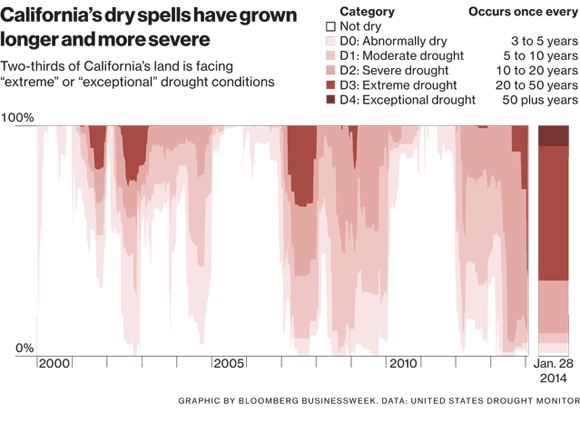

It seems safe to say that California will never be the same anymore. It doesn’t get much stronger than this: More than 98% of California land is now considered at least abnormally dry.

• California’s Drought in Two Terrifying Charts (BusinessWeek)

The Golden State is parched. California’s water reserves typically replenish over the winter, but the current drought is worsening in what’s supposed to be the wettest time of the year.

Almost 9% of the state is in “exceptional” drought, the most severe designation from the U.S. Drought Monitor, an interagency report whose classifications are based on measures of precipitation, soil moisture, and other factors. The “exceptional” rating, also known as “D4,” is reserved for dry spells so intense they occur fewer than once in 50 years. It’s the first time California has had any D4 areas since the Drought Monitor was launched in 2000. More than 98% of California land is now considered at least abnormally dry.

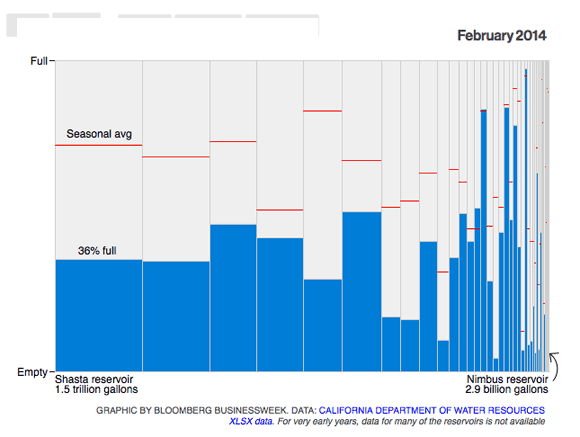

California’s reservoirs are holding just 39% of their combined capacity, when typically they should be 64% full by this time in winter. That has prompted the state to do something it’s never done before: At the end of January, officials cut to zero the amount of water that local authorities could draw from the series of reservoirs that supply 25 million Californians and 750,000 acres of farmland. Snowpack is at just 12% of levels typical this time of year, leaving little hope that the reserves will be replenished soon.

Without deliveries from the state reservoirs, cities are asking residents and businesses to conserve water, Bloomberg News reports. People are prohibited from washing cars, filling swimming pools, and watering lawns during the daytime, and farmers are letting thousands of acres lie fallow. All that, and it’s not even summer.

This article addresses just one of the many issues discussed in Nicole Foss’ new video presentation, Facing the Future, co-presented with Laurence Boomert and available from the Automatic Earth Store. Get your copy now, be much better prepared for 2014, and support The Automatic Earth in the process!

Home › Forums › Debt Rattle Feb 6 2014: Remember “Uncharted Territory”?