John Collier Grandfather Romero, 99 years old. Trampas, New Mexico 1943

Private debt: 207%.

• China’s Debt-to-GDP Ratio Just Climbed to a Record High (Bloomberg)

While China’s economic expansion beat analysts’ forecasts in the second quarter, the country’s debt levels increased at an even faster pace. Outstanding loans for companies and households stood at a record 207% of GDP at the end of June, up from 125% in 2008, data compiled by Bloomberg show. China’s stimulus, including interest rate and reserve-ratio cuts to shore up growth, threatens to delay the country’s efforts to reduce its debt, posing risks to the financial stability of the world’s second-largest economy. Nonperforming loans had already climbed by a record 140 billion yuan ($23 billion) in the first quarter as the expansion in gross domestic product slowed.

“It’s quite an alarming issue,” says Bo Zhuang, a China economist at London research firm Trusted Sources. “The government is trying very hard to slow down the pace of the leveraging up, but they are not deleveraging. The debt-to-GDP ratio will continue to go up.”

China’s economy expanded 7% in the three months through June from a year earlier, the National Bureau of Statistics said Wednesday, unchanged from the first quarter and beating economists’ estimates of 6.8%. Corporate and household borrowing rose 12% in June from a year earlier. China went on an unprecedented borrowing binge following the 2008 global financial crisis and has been struggling to clean it up ever since. Rising debt will keep slowing the country’s growth, according to Ruchir Sharma at Morgan Stanley

Do we even want to know?

• China Stock Suspensions Opens Can Of Derivatives Worms (Reuters)

The suspension of hundreds of mainland China stocks during a market plunge from mid-June could lead to disputes between banks and their clients over the valuation of billions of dollars of equity derivatives. Banks dealing in derivatives are concerned that valuation terms covering market disruptions in other Asian markets, such as trading halts when stocks move up or down by the exchange’s daily range limits, might not apply to the wave of stock suspensions in China. As China’s stocks tumbled by 30 percent in less than a month, around 1,500 listed companies, more than half the market, suspended their own stocks in a bid to sit out the rout.

“It’s not yet clear if the existing disruption event language for other Asian jurisdictions can be applied to China or how the existing disruption definitions for limit-up, limit-down would apply to suspended stocks,” said Keith Noyes, regional director, Asia Pacific, at the International Swaps and Derivatives Association (ISDA), which represents the world’s largest derivatives dealers. Noyes and an in-house lawyer at a major Asian dealer said banks were reviewing the issue. “There could be wrangling over issues such as whether the Shanghai composite index closing price, which would generally be the easiest to use to value contracts, is a good price or a disrupted price, given that so many stocks are now suspended,” said Noyes.

Dealers have written at least $150 billion of outstanding over-the-counter (OTC) equity derivatives on mainland-listed shares, according to estimates by Shanghai-based investment consultancy Z-Ben Advisors. When drawing-up such instruments, most dealers draw on ISDA standard definitions as a basis for valuing equity derivative positions when the underlying stock market is disrupted. The language was drawn up in 2008 following disruptions in the South Korean and Taiwan markets, when China’s markets were all but closed to outside investors, and applies to a number of Asian markets, including Taiwan, South Korea, Singapore, and Hong Kong, but not mainland China. Noyes said the dealer community may need to reach an agreement on whether it could be extended to China to help more easily resolve disputes.

Major shuffle coming?!

• Greek Lawmakers Pass Austerity Bill Despite Strong SYRIZA Dissent (Kathimerini)

Greek Parliament passed the prior actions demanded by lenders to pave the way for bridge financing and a third bailout in a vote during the early hours of Thursday morning. A total of 229 MPs voted for the measures, 64 voted against, six voted present and one was absent. Prime Minister Alexis Tsipras saw 32 of his MPs vote against the measures, while another six abstained. All of the deputies from coalition partner Independent Greeks backed the legislation. This means that the number of coalition lawmakers supporting the bill remained above the 120-mark, which is the level below which the government is considered not to have a mandate to continue.

Before the vote, Tsipras said the agreement with lenders was the only viable option open to him and challenged rebels within his party to propose a better one. In his speech before Parliament, Finance Minister Euclid Tsakalotos sought to defend Greece’s agreement with creditors as a necessary evil. “It’s a difficult agreement, a deal which only time will show if it is economically viable,” he said. “I don’t know if we did the right thing, but I know we felt we had no choice,” he said. “We never said this was a good agreement,” he added, noting that “a lot will depend on how politicians will handle the many changes included in the agreement.”

Economy Minister Giorgos Stathakis, for his part, declared that “these are moments for responsibility,” noting that everyone “must state clearly where they stand on Greece’s dilemma. The government received a half-finished second bailout which was frozen and was confronted by non-viable system,” he said. SYRIZA’s parliamentary spokesman Nikos Filis accused eurozone officials of executing a “coup” at a summit in Brussels on Monday when the agreement was reached. Their aim, he said, was “to topple the Greek government, to give the message that a leftist administration cannot survive in Europe.”

“The lesson that they will draw from this debacle is: negotiating with Germany is a waste of time; be willing to act unilaterally, be willing to default unilaterally, have a plan for achieving a primary surplus if you haven’t already achieved it, have a hard default and euro exit option in your back pocket, and be willing to use it at the first sign of hassle from the ECB,”

• EMU Brutality In Greece Has Destroyed The Trust Of Europe’s Left (AEP)

The EU establishment henceforth faces what it has always feared: a political war on two fronts at once. It is long been fighting an expanding coaltion of free marketeers, parliamentary “souverainistes”, anti-immigrant populists on the Right. Its has now lost its remaining emotional hold on the Left after the scorched-earth treatment of Greece over the past five months – culminating in the vindictive decision to impose yet harsher terms on this crushed nation just days after its cri de coeur in a landslide referendum.

This has been coming for a long time. We Conservatives have watched in disbelief as one Socialist party after another immolates itself on the altar of monetary union, defending a project that favours the elites – a “bankers’ ramp”, as the old Left used to call it.We have watched our friends on the Left apologise for 1930s policies. We have seen them defend a regime of pro-cyclical fiscal cuts imposed on the whole eurozone by a handful of “Ordoliberal” reactionaries in the German finance minstry. To the extent that these gentlemen know what they are doing – and most Nobel economists would dispute that – they have certainly not risen to the challenge of pan-EMU leadership. As ex-official Philippe Legrain writes in Foreign Policy, Germany is proving to be a “calamitous hegemon”. By a twist of fate, the Left has let itself become the enforcer of an economic structure that has led to levels of unemployment once unthinkable for a post-war social democratic government with its own currency and sovereign instruments.

It has somehow found ways to justify a youth jobless rate still running at 42pc in Italy, 49pc in Spain and 50pc in Greece, despite mass emigration. It has acquiesced in the Long Slump of the past six years, deeper in aggregate than the span from 1929 to 1935. It meekly endorsed the EU Fiscal Compact, knowing that it imposes a legal requirement on eurozone states to slash their public debt by 1.5pc of GDP in France, 2pc in Spain and 3.5pc in Italy and Portugal, every year for the next two decades – a formula for near permanent depression. It outlaws Keynesian economics, and indeed classical economics. It is a doomsday construct. This is what they agreed to, and what they have reluctantly defended, because until now they dared not question the sanctity of EMU.

And so the once mighty Dutch Labour Party has been reduced to a pitiful relic. Pasok has been obliterated in Greece. The Spanish Socialist Workers’ Party has lost its left-wing to the rebel Podemos movement, freshly victorious in Barcelona. France’s Socialist leader, Francois Hollande, has been languishing at 24pc in the polls as the French working class defects to the Front National. Yet events in Greece have finally broken the spell. “Progressives should be appalled by EU’s ruination of Greece. It’s time to reclaim the Eurosceptic cause,” writes Owen Jones in a remarkable piece in The Guardian. The new term “Lexit” is gaining currency. The voices of Left are uneasy. Their instincts are to oppose everything that UKIP stands for. “At first, only a few dipped their toes in the water; then others, hesitantly, followed their lead, all the time looking at each other for reassurance,” Mr Jones writes.

Perhaps “Leftit” is a better term. And not just in Britain.

• Lexit: The Left Must Now Campaign To Leave The EU (Guardian)

At first, only a few dipped their toes in the water; then others, hesitantly, followed their lead, all the time looking at each other for reassurance. As austerity-ravaged Greece was placed under what Yanis Varoufakis terms a “postmodern occupation”, its sovereignty overturned and compelled to implement more of the policies that have achieved nothing but economic ruin, Britain’s left is turning against the European Union, and fast. “Everything good about the EU is in retreat; everything bad is on the rampage,” writes George Monbiot, explaining his about-turn. “All my life I’ve been pro-Europe,” says Caitlin Moran, “but seeing how Germany is treating Greece, I am finding it increasingly distasteful.” Nick Cohen believes the EU is being portrayed “with some truth, as a cruel, fanatical and stupid institution”.

“How can the left support what is being done?” asks Suzanne Moore. “The European ‘Union’. Not in my name.” There are senior Labour figures in Westminster and Holyrood privately moving to an “out” position too. The list goes on, and it is growing. The more leftwing opponents of the EU come out, the more momentum will gather pace and gain critical mass. For those of us on the left who have always been critical of the EU, it has felt like a lonely crusade. But left support for withdrawal – “Lexit”, if you like – is not new. If anything, this new wave of left Euroscepticism represents a reawakening. Much of the left campaigned against entering the European Economic Community when Margaret Thatcher and the like campaigned for membership.

It would threaten the ability of leftwing governments to implement policies, people like my parents thought, and would forbid the sort of industrial activism needed to protect domestic industries. But then Thatcherism happened, and an increasingly battered and demoralised left began to believe that the only hope of progressive legislation was via Brussels. The misery of the left was, in the 1980s, matched by the triumphalism of the free marketeers, who had transformed Britain beyond many of their wildest ambitions, and began to balk at the restraints put on their dreams by the European project.

“The real disaster is if everything stays as it is..”

• There’s No End In Sight To The Greco-European Drama (Guardian)

The last act of the classical Greek tragedy ends with two outcomes: disaster and catharsis. In the current Greek debt drama, however, there has been no catharsis. The purification has failed to materialise. It would have meant that both sides had seen the error of their ways and come to their senses. Instead, the madness continues: Greece will take on €86bn of debt in addition to the existing €317bn (not including the emergency loans from the ECB). From Angela Merkel through François Hollande to Alexis Tsipras, all eurozone government leaders assert that Greece will emerge from over-indebtedness more quickly this way and will be economically healed in three years. Europe pretends that the bailout will help. And Greece acts as if everything is fine now.

The Brussels summit was not a disaster, though. Greece does not fall into chaos and the euro remains stable. Maybe Walter Benjamin, who once said: “The real disaster is if everything stays as it is,” was right. When it comes to classical drama, it seems we have not reached the final act after all. The fourth act, the “retardation”, continues. The action is slowing down, with suspensory moments: the troika returns to Athens and monitors the situation, while the Greek authorities delay and tinker about again. Until the action moves into a phase of extreme tension towards the finale. When will that be? Merkel hopes it will be after the next parliamentary elections.

For the Greeks, there is more at stake in this drama than there is for the Germans. The Germans will lose a lot of money at the most. The Greeks, however, have long since come under the tutelage of the donors. What Tsipras signed on Monday is the permanent abandonment of Greek sovereignty. Athens will be told what budget surplus it must achieve and what taxes it should raise. Fiscal sovereignty is broken. The constitution will be interfered with to impose pension cuts. The administration and judiciary must be rebuilt according to the standards of the northerners. It is not about a bailout loan, but it is avowedly about nation building, as if Greece were a failed state. Even the IMF has condemned the deal as unworkable and said the levels of debt are unsustainable.

Greek culture is being encroached upon in every way. The Sunday opening of shops is being enforced, whether the still strongly religious population likes it or not. Consumption is more important than orthodox religion – that is the credo of the north. In international law the internal affairs of a nation are largely taboo; in the euro protectorate there are no taboos.

And more than once.

• Shock Announcement From IMF Reveals Greece Was Duped by Europe (EI)

The IMF has fiercely criticised the bailout deal offered to Greece by the Eurozone, revealing that the Eurogroup of finance ministers had ignored its advice when negotiating with Greece over the weekend. In a communique released last night, the IMF said Greece’s public debt was now “highly unsustainable” before concluding: “Greece’s debt can now only be made sustainable through debt relief measures that go far beyond what Europe has been willing to consider so far.” It now appears that the deal, rather than seeking to help the Greek economy, was designed principally to teach Greece a lesson and remove Syriza from power. Today the Greek parliament votes on whether to accept the austerity deal that it was bullied into over the weekend during negotiations dominated by Germany.

Certainly, the IMF bombshell is likely to stiffen the resolve of the those Syriza MPs such as Papas Lapavitsas, an economics Professor from the School of African and Asian Studies (SOAS) in London, who have long argued that a Greek exit from the euro is the only realistic choice open to revive the Greek economy. He’s previously outlined these ideas in articles he has written for the Guardian and for ThePressProject. Regardless of the immediate outcome of the vote, the whole drama has weakened transparency and democracy in Europe. The euro project is now clearly seen as a failing project and its eventual break-up appears inevitable to many. The only questions remains when and how exactly it will occur.

“I don’t take hostages I’m not willing to shoot..”

• The EU Shot Its Greek Hostage, Now Spain Is Nervous (Fiscal Times)

In a battle over banking regulation at the end of the Clinton administration, former Republican Sen. Phil Gramm of Texas remarked on the importance of being willing to inflict pain when negotiations don t go your way. “I don’t take hostages I’m not willing to shoot”, Gramm explained. The point Gramm was making is that once you demonstrate that you don’t make idle threats, future negotiations are easier. The treatment of Greece by its European creditors may have had a similar effect. In Spain, which is even more indebted than Greece, the leftist Podemos Party has been gaining influence, in part by making promises in line with those made by Greece’s Syriza Party. In May, Pablo Iglesias, the leader of Podemos, demanded that Spain’s debt be restructured and that debt payments be tied to economic growth.

“For Spain to be able to meet its international obligations, we have to link debt payments to economic growth and expansive job creation policies”, he said. A similar argument had been made by former Greek finance minister Yanis Varoufakis, who so aggravated his European counterparts that he was eventually replaced. The reaction of Podemos to the punishing deal to enable another Greek bailout was telling. After battling to the bitter end, Syriza was forced to accept a humiliating offer from its creditors. In a deal primarily driven by Germany and other northern European countries, Greeks face pension cuts, huge tax increases, reduced services, and the forced sale of $50 billion worth of the country s physical assets.

In Madrid on Tuesday, it was as though the Eurogroup, fresh from dealing with Greece, had turned to Spain with smoking gun in hand and asked, “What were you saying”? The answer from Podemos top economic policy officer, Nacho Alvarez, was essentially, “Who, me? Nothing. Nothing at all.” Speaking to reporters, Alvarez said that debt restructuring wasn t really necessary after all. ‘Spain, he said, is not Greece’. Or so he must fervently hope. “Greece and Spain are different economies in very different situations which demand different economic strategies”, Alvarez said at a press conference. He added, “Podemos and Syriza have different economic approaches and said that he is confident the country’s current programs to stimulate economic growth will allow it to manage its debts.

Whether Podemos has detected a significant shift in the country s economic future over the last two months or has had a change of heart more related to the Eurogroup s treatment of Greece is up for debate. However, if part of the aim of Greece’s creditors was to punish Syriza pour encourager les autres, there seems to be little room for debate at all. It worked. In the near term, at least, it worked.

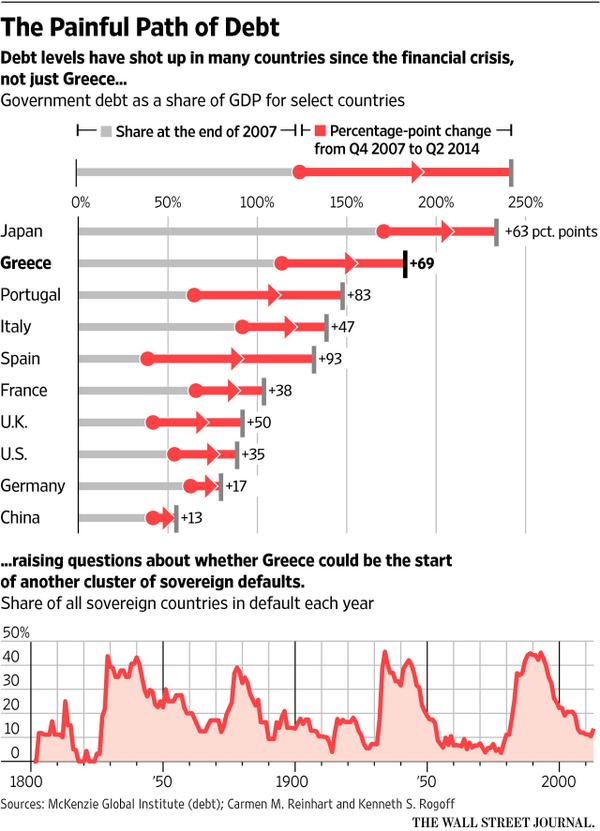

Defaults come in clusters.

• Greece’s Lessons for an Indebted World (WSJ)

Sovereign defaults are like cockroaches: There’s seldom just one. Greece’s debts are so high, its recession so deep and its economy so uncompetitive, it’s easy to play down the lessons it offers to the rest of the world. But while Greece is exceptional, the entire world is suffering from an overhang of debt. Since 2007, public debt in advanced economies (including national, state and local governments) has risen by 35 percentage points of total economic output, according to the McKinsey Global Institute. In many countries it has risen by far more: 47 points in Italy, 50 in Britain, 63 in Japan, 83 in Portugal. A country can shed such steep debt several ways: via austerity, economic growth and low real (that is, inflation-adjusted) interest rates.

More common than appreciated, though, is the more radical step of restructuring debt by reducing interest, lengthening the maturity or slashing the amount owed. “Will Greece be the last sovereign debt restructuring of this cycle? No,” says Susan Lund of McKinsey. “Look around the world and you can see other countries with very toxic combinations of high debt and low growth.” In their 2009 history of financial crises, Harvard University economists Carmen Reinhart and Kenneth Rogoff observe that “country defaults tend to come in clusters.” In the 1930s, the Great Depression triggered defaults throughout Europe and Latin America. In the 1980s, plunging commodity prices triggered a wave of defaults by emerging economies that had borrowed heavily from Western banks.

Noteworthy defaults this time around have been rare: they include Greece, Cyprus and Argentina (the latter linked to its prior-decade restructuring). The quietude is unlikely to last. Ukraine is now seeking to restructure its debts to private investors, as is Puerto Rico (which, to be sure, is not a sovereign country). Opposition politicians in Ireland, Spain and Italy have in the past pressed to restructure some of those countries’ debts, which according to McKinsey stood last year at 115%, 132% and 139% of gross domestic product, respectively.

“The euro system today is an instrument in the hands of European capital to roll back the gains of social democracy.”

• 13 Short Lessons From The Greek Crisis (J.W. Mason)

The deal, obviously it looks bad. No sense in spinning: It’s unconditional surrender. It is bad. There’s no shortage of writing about how we got here. I do think that we — in the US and elsewhere — should resist the urge to criticize the Syriza government, even for what may seem, to us, like obvious mistakes. The difficulty of taking a position in opposition to “Europe” should not be underestimated. It’s one of the ironies of history that the prestige of social democracy, earned through genuine victories by and for working people, is now one of the most powerful weapons in the hands of those who would destroy it. Personally I don’t think I can be a useful contributor to the debate about Syriza’s strategy. But we also need to understand the economic logic of the situation. So, 13 theses on the Greek crisis and the crisis next time. These points are meant as starting points for further discussion. I will try to write about each of them in more detail, as I have time.

1. The euro system today is an instrument in the hands of European capital to roll back the gains of social democracy. On twitter, Marshall Steinbaum says, “That is why everyone supports the euro: as a route around their domestic political difficulties, ie, voting.” I think that’s right, I think the overriding goal of the system today is to create a set of apparently objective constraints that allow elected governments to take unpopular measures while saying “we had no choice, the markets require it.” I’ve written about this here and here.

2. A great myth of the euro is that it’s been good for Germans. It’s a puzzle, the kind of story that calls for dialectics, that Germany has both Europe’s strongest working class and most advanced social democracy, and its most rigidly conservative elite. For a while those forces were roughly balanced, but over the past generation German workers have done the worst, absolutely and relatively, of any country in Europe. The north-south divide in Europe perhaps analogizes to the racial divide in the US, so perhaps the same slogans apply: Black and white, unite and fight!

3. The euro is not a new gold standard. This is a tricky one — I feel a clear vision here requires one to first see how the euro is a new gold standard, and only then seeing how it isn’t one after all. Despite the dreams of its supporters (and fears of its opponents) the euro system does not provide an automatic constraint on the choices of elected governments. In the abstract, it looks more like Keynes’ proposals at Bretton Woods. Its actual functioning as the enforcement mechanism of neoliberalism, requires the active intervention of the authorities.

4. The ECB is a political actor. You may think that the ECB has violated the norms of independent central banks, or you may think it has revealed their true content. But either way it is actively intervening in the political process to reshape society in fundamental ways, not just following a set of objective rules to fulfill a narrow technical function. It was already evident several years ago that the ECB was selectively withholding support from financial markets to put pressure on elected officials, and now it is undeniable.

Brutally honest. Yanis voted NO last night. Can he stay on as MP?

• The Euro-Summit ‘Agreement’ on Greece – Annotated (Yanis Varoufakis)

The Euro Summit statement (or Terms of Greece’s Surrender – as it will go down in history) follows, annotated by yours truly. The original text is untouched with my notes confined to square brackets (and in red). Read and weep…

Euro Summit Statement Brussels, 12 July 2015

The Euro Summit stresses the crucial need to rebuild trust with the Greek authorities [i.e. the Greek government must introduce new stringent austerity directed at the weakest Greeks that have already suffered grossly] as a pre- requisite for a possible future agreement on a new ESM programme [i.e. for a new extend-and-pretend loan].

In this context, the ownership by the Greek authorities is key [i.e. the Syriza government must sign a declaration of having defected to the troika’s ‘logic’], and successful implementation should follow policy commitments.

A euro area Member State requesting financial assistance from the ESM is expected to address, wherever possible, a similar request to the IMF This is a precondition for the Eurogroup to agree on a new ESM programme. Therefore Greece will request continued IMF support (monitoring and financing) from March 2016 [i.e. Berlin continues to believe that the Commission cannot be trusted to ‘police’ Europe’s own ‘bailout’ programs].

Given the need to rebuild trust with Greece, the Euro Summit welcomes the commitments of the Greek authorities to legislate without delay a first set of measures [i.e. Greece must subject itself to fiscal waterboarding, even before any financing is offered].

“Perhaps Hell is full of creditors who failed to fit through the eye of a needle..”

• I Love Germany. And Greece. And Especially Finland. (Waldman)

If you are sympathetic to Greece and therefore mad at Germany, you are a sucker. If you think the Greeks are lazier and more dishonest than is usual in the human species, you are also a sucker, and have let a political framing cajole you into bigotry. If you think Germans are unusually cruel, you have also let politics make a bigot of you. If you are taking sides in a conflict framed as nation versus nation, you have already taken the wrong side. You’ve made a basic error, like picking a day when a tricky prosecutor asks whether you committed the murder yesterday or last Thursday. (I presume your innocence.)

You can usually find evidence in support of lots of different narratives. Hypotheses of human affairs are not in general mutually exclusive. Many different stories can in some sense be true. Among those in-some-sense-true narratives, we should choose to emphasize those whose application will lead to better social outcomes over other potentially defensible narratives. That’s why I frequently argue that we should emphasize the role of creditors rather than debtors when lending arrangements go bad. I am not making a claim about God’s view of the subject. Perhaps Hell is a debtors’ prison, and there is truly no greater evil than failing to repay a loan. Perhaps Hell is full of creditors who failed to fit through the eye of a needle. These questions are, I think, beyond the sort of knowledge that should inform policy.

What is clear is that unserviceable debt arrangements, when they accumulate, are enormously costly in human and economic terms, and so we need norms and institutions to regulate credit extension. My view, which I think almost anyone with a passing familiarity with the human species would have to concede, is that people under financial stress make decisions with a view to a shorter-term time horizon and with less capacity to be fastidious than people who have already financed their own immediate term. That is why I argue that we should emphasize norms that hold creditors accountable more than norms that hold debtors accountable. Creditors as a class are capable of regulating the initiation of debt arrangements at lower cost and with greater effectiveness that debtors are.

If we want societies that yield good outcomes, then, we should impose a heavy regulatory burden on creditors, and we must choose moral narratives consistent with that. Perhaps the very worst moral narratives in all of human history are those that allocate blame on the basis of tribal, ethnic, or national groups. There is just never, ever, any sufficient reason to go there in my view. It is perfectly reasonable to hold leaders and governments accountable, as well as the institutional embodiments of interest groups. This is not because leaders individually are worse people than members of the public who may agree with their decisions. I carry no water for fairy tales about the inherent virtue of ordinary folk.

Shouldn’t be so hard, you know what to do.

• IMF Chief: Greek Bailout Talks a ‘Colossal’ Challenge Going Forward (WSJ)

IMF chief Christine Lagarde said she still had hope the eurozone would provide Greece with a substantial restructuring of the country’s debt, but warned of difficult negotiations as officials seek to complete a bailout deal in the weeks ahead. Ms. Lagarde’s comments come a day after the fund warned in a report that Greece needed much more debt relief than European officials have so far considered—an apparent effort to pressure Germany into concrete commitments on debt restructuring. Normally, the fund reserves its most honest assessments for secret, high-level meetings.

But by taking the highly unusual step of making public its bleak appraisals of Greece’s economy, Ms. Lagarde and her lieutenants are drawing a red line for the eurozone: Agree to substantial debt relief or lose the fund’s support and risk a Greek exit from the eurozone. “What I very much hope is that we can all keep to a very tight timetable and we can respond to a challenge that is colossal,” Ms. Lagarde said in an interview on CNN on Wednesday. The debt-restructuring commitments will be key as Athens tries to sell a bailout program that Greece’s voters have already rejected in a recent referendum.

The IMF and its largest shareholder, the U.S., worry that without such a commitment the government won’t be able to persuade the public or parliament to support the major budget cuts and economic overhauls creditors say are vital for the country’s financial salvation. “Up until a few months ago, our partners didn’t discuss the issue of debt restructuring,” said Finance Minister Euclid Tsakalotos. Still, he said it was “too early to judge this deal.” “We will be able to see when talks wind up in 30 to 40 days when we have the final agreement. Then we can all judge it with seriousness for the good of the country,” Mr. Tsakalotos said.

“The eventual implosion of the European Union, and the banking system hugging its face vampire squid style, will be the financial equivalent of the Black Death..”

• Greek Pudding (Jim Kunstler)

The proof of the pudding is in the eating, the old saw goes. This one, alas, is a mélange of several old shit sandwiches bound in a liaison of subterfuge and seasoned with political absurdities. Having been fooled in this bistro before, citizen-patrons leave the table resigned to yet another bout of food poisoning as the music of universal upchuck rings across the European Union from Helsinki to Lisbon What is on display more brightly and clearly than ever, though, is the utter fakery of international banking. The players have lost faith in their own shenanigans. They simply go through the motions now awaiting the political fallout, which is to say the revolt of the people who can still do arithmetic. So, now Greece can supposedly expect another $90Billion-equivalent in new loans on top of the $350Billion-equivalent already racked up.

That’s rich. The loan repayment schedule must look like a map of Middle Earth. Most perplexing — especially for those on summer hiatus in which time seems to be suspended — is the fact that the rescue package will take weeks, perhaps months, to gin up while Greece is right now so utterly paralyzed in bankruptcy that no goods can move, no bills can be paid, and the economy cannot deliver the necessities of daily life. The old refrain, “your check is in the mail” may not be so reassuring to folks who haven’t eaten for three days. Personally, I would expect the gasoline bombs to be flying around Syntagma Square before the middle of the week.

Has anyone noticed the eerie paucity of news emanating from the other hard-luck nations of the EU, namely Spain, Portugal, Italy, and Ireland? The money hole that these deadbeats are in makes Greece look like a dimple in the sand. What, I wonder, is the message to them from the Greek negotiation melodrama? (Lend more money to real estate developers to build more houses and condos that will never be sold? That’ll work!) No, the entire EU debt fiasco harks back to the original meaning of “ring around the rosie” — a theme song of the Black Death. The eventual implosion of the European Union, and the banking system hugging its face vampire squid style, will be the financial equivalent of the Black Death. Kingdoms will fall and social systems will be turned upside down.

“The idea of giving private banks a monopoly over money creation goes back to seventeenth century England.”

• What’s Wrong with Our Monetary System and How to Fix It (Kuzminski)

Something’s profoundly wrong with our global financial system. Pope Francis is only the latest to raise the alarm: “Human beings and nature must not be at the service of money. Let us say no to an economy of exclusion and inequality, where money rules, rather than service. That economy kills. That economy excludes. That economy destroys Mother Earth.” What the Pope calls “an economy of exclusion and inequality, where money rules” is widely evident. What is not so clear is how we got into this situation, and what to do about it. Most people take our monetary system for granted, and are shocked to learn that the government doesn’t issue our money. Almost all of it is created by loans made “out of thin air” as bookkeeping entries by private banks.

For this sleight-of-hand, they charge interest, making a tidy profit for doing essentially nothing. The currency printed by the government – coins and bills – is a negligible amount by comparison. The idea of giving private banks a monopoly over money creation goes back to seventeenth century England. The British government, in a Faustian bargain, agreed to allow a group of private bankers to assume the national debt as collateral for the issuance of loans, confident that the state would be able to service the debt on the backs of taxpayers. And so it has been ever since. Alexander Hamilton much admired this scheme, which he called “the English system,” and he and his successors were finally able to establish it in the United States, and subsequently most of the world.

But money is too important to be left to the bankers. There is no good reason to give any private group a lucrative monopoly over the creation of money; money creation should be the public service most people mistakenly believe it to be. Further, privatized money creation allows a few large banks and financial institutions not only to profit by simply making bookkeeping entries, but to direct overall investment in the economy to their corporate cronies, not the public at large. Ordinary people can get the financing they need only on burdensome if not ruinous terms, leaving them as debt peons weighed down by mortgages, student loans, auto loans, credit card balances, etc. The interest payments extracted from these loans feed the private investment machine of Wall Street finance, represented by the ultimate creditor class: the notorious “one percenters.”

Not looking good down under.

• Kiwi Dollar Falls As Dairy Prices Plunge At Latest Auction (NZ Herald)

The latest GlobalDairyTrade auction was another shocker, the GDT price index dropping by 10.7% from the last sale a fortnight ago and with wholemilk powder prices registering their biggest fall in 12 months Whole milk powder – which is responsible for about 75% of Fonterra’s farmgate milk price – fell in price by 13.1% to US$1,848 a tonne to its lowest level in six years. Fonterra’s current milk price forecast of $5.25 per kg of milksolids for 2015/16 is based on GDT prices reaching about US$3500 a tonne towards the end of this season. Dairy NZ estimates $5.70 a kg to be the breakeven point for most farmers. AgriHQ dairy analyst Susan Kilsby said the auction result was “disastrous”.

“Farmers now face two consecutive seasons of extremely low milk prices,” she said in a commentary. “The majority of farmers can’t breakeven at such a low milk price.” Economists estimate a $1/kg drop in the milk price equates to about $2 billion less income for dairy farmers. “Farm debt levels will rise. Rural communities will suffer as farmers reduce spending to the bare essentials,” Kilsby said. AgriHQ’s theoretical 2015-16 farmgate milk price has decreased to $4.22 per kg milksolids – down 83c on a fortnight ago and $1.27 lower than a month ago. The dairy auction result was responsible for taking around 40 pips off the Kiwi dollar, and the NZ/Australian dollar cross rate dropped to below A89.50c.

Home › Forums › Debt Rattle July 16 2015