Arthur Rothstein Family on relief living in shanty at city dump, Herrin, Illinois 1939

My buddy VK sent me a link yesterday to a limits to growth piece by Nafeez Ahmed, executive director of the Institute for Policy Research & Development, in the Guardian, The Global Transition Tipping Point Has Arrived – Vive La Révolution, in which the author says almost all of the right things, but unfortunately gets a lot wrong as well.

What Nafeez gets wrong, a lot of people do, in alternative energy circles and beyond, like for instance someone he quotes extensively, my old – former – pen-pal Chris Nelder, with whom he has in common that both come far too close for my comfort to replacing one wave of techno-happiness with another. And I don’t think that all that’s wrong with us is that we’ve picked the wrong flavor of techno-happy. Nafeez:

… what we are seeing are escalating, interconnected symptoms of the unsustainability of the global system in its current form. While the available evidence suggests that business-as-usual is likely to guarantee worst-case scenarios, simultaneously humanity faces an unprecedented opportunity to create a civilisational form that is in harmony with our environment, and ourselves. [..]

… our current trajectory is unsustainable because our demand for ecological resources and services is increasingly going beyond what the planet is able to provide. This ‘overshoot’ is already responsible for a range of overlapping crises – the financial crash, the food crisis, intensifying civil unrest to name just a few – and is likely to worsen without meaningful action.

Told you: almost all of the right things. There’s more of that.

… what we are facing is something far more complex than an ‘end-is-nigh’ scenario: not the end of the world, but the end of the old industrial paradigm of endless growth premised on practically endless oil, that is increasingly breaching its own biophysical limits; and the emergence of an emerging paradigm of civilisation based on a vision of a global commons for all.

Sounds good and uplifting, doesn’t it? Empowering even. But you have to remain vigilant, perhaps especially when things sound good. What my unbelieving brain comes up with right away is this:

The essential question that neither he nor anyone else answers is that you can of course say that, in his words:

“humanity faces an unprecedented opportunity to create a civilisational form that is in harmony with our environment, and ourselves”

… but saying it doesn’t make it true. If you assume that people want such a civilizational form, then first answer this question: why don’t they already have it? For one thing, certainly such a form, like everything else, is easier to set up in times of plenty then times of misery.

If you can’t answer the question why so far people have not opted for such a form, and instead chose the unsustainable one we have now, how are you going to know that we are capable of turning around on a dime and “creating” a form that is “in harmony with our environment, and ourselves”?

Or to put it differently: if you had to choose between the option that we’ll “create a civilisational form that is in harmony with our environment, and ourselves” versus the option that we’ll burn on through until we hit the wall at 1000 miles an hour, which one would you put your money on given human history as we know it?

When we had all the natural resources at our disposal that would have made it a – comparative – piece of cake to set up “a civilisational form that is in harmony with our environment, and ourselves”, we did no such thing, in fact we did the exact opposite. But now that those resources are dwindling, and building that civilizational form will be more difficult, we would, all of a sudden? Why? Only because we have no other choices left, we would choose to live “in harmony with our environment, and ourselves”?

Can we do it? Obviously, in theory. But that theory has been valid all along, and look where we are. So when you ask: will we do it, there is reasonable doubt based on past experience. Because the “unprecedented opportunity” isn’t really all that unprecedented, is it? In reality the opportunity has been available to us every single day for the past 100 years or so, and we opted against it, and the only thing that’s different is that at this point in time, it’s not so much an opportunity as it is a force majeure.

And you don’t get away from those questions by evoking extreme fatalism, as Nafeez does, and suggesting you’d have to pick either that or the “unprecedented opportunity” line:

Of course, there are those who go so far as to argue that humanity is heading for extinction by 2030, and that it’s too late to do anything about it. But as other scientists have pointed out, while the number of positive-feedbacks that could go into ‘runaway’ on a business-as-usual scenario appears overwhelming, whether they have yet is at best unclear from the numbers – and at worst, we find that proponents of fatalism are actually systematically misrepresenting and obfuscating the science to justify hopelessness.

I find that awfully weak as an argument, and it easily slides into what I can see only as religious overtones, something much better avoided when you want to focus on science:

Faced with the overwhelming scale of the multiplicity of global challenges we now face, a sense of disempowerment is understandable. However, as I’ve argued before, it is unnecessary and self-defeating.

Nafeez goes on to quote Chris (Nelder):

As Nelder writes in his latest column, we find ourselves at a potentially exciting crossroads: the literal death throes of the fossil fuel industry, amidst the inexorable, sporadic rise of a new renewable energy system. Renewable sceptics are simply wrong, obsessed with the slow, centralised economic dynamics of fossil fuels rather than understanding the unique, distributed dynamics of the new.

That’s quite a thing to say, “Renewable skeptics are simply wrong”. It would have been helpful if the author had explained who he means to include in that. But I’ll partly take the bait. I think it’s important to note that renewables are not fit to run a (centralized) grid on. And I know that Chris sees lots of opportunities in decentralized systems, but we’re very far away from building those in relevant quantities, and there are numerous obstacles strewn across the way.

Just to name two: there’s the – awfully tenacious – centralized political power a centralized grid provides for, and then there’s the plunging economic system that will prevent any meaningful investment into yet-to-be-built infrastructure. And even with all his well-meaning enthusiasm for technological progress in grid infrastructure, Nelder two years ago concluded this in Why Baseload Power is Doomed:

Renewables should be able to meet at least 20% of electricity demand without disrupting the grid just about anywhere in the world with good grid planning and management.

20% is nice, but it’s hardly a revolution. And if you read Chris’s work, you find that even that requires for instance a lot of technological input (which Chris sees as a good thing) in the form of constant – live – monitoring of grid systems, based on a lot of computer power etc. That’s where my trepidations about switching one tech happy wave for the other come in. I suggest that we need to seriously consider the option that it’s technology that has gotten us into this mess, and there’s either no guarantee or no way technology will lift us out of it. Nafeez continues:

In the new paradigm, neither money nor credit will be tied to the generation of debt. Banks will be community-owned institutions fully accountable to their depositors; and whirlwind speculation on financial fictions will be replaced by equitable investment schemes in which banks share risks with their customers, and divide returns fairly. The new currency will not be a form of debt-money, but, if anything, will be linked more closely to real-world assets.

All the right and lofty words, for sure, but how did we get there from here? What exactly is that new paradigm, and the new ethos? It sounds good, but what does it mean? Is it just me, or does this all sound like a nice dream, not unlike anything you and I could have just as easily have proposed – since we all have more or less the same dream anyway -, while there’s a huge missing gap, as in how do we shift from paradigm one to two?

It’s easy pickings: hardly anybody in their right mind these days wants centralized fossils, or industrial monoculture food, but everyone has it. And painting rosy pictures of how things could be is not going to change that. Nafeez’ and Chris’s idea that we are about to enter some new ear and things will be great is cute and all, but leaves too many questions. And even if we could make the move into some new paradigm, something I see little proof of, we would still have to get there, and neither explains what that process of moving would look like.

And I also think that what the techno happy 2.0 crowd wants for us to hang on to growth, but in a “new” way, and I think that’s fundamentally wrong.

Re-defining the meaning of economic growth to focus less on materially-focused GDP, and more on the capacity to deliver values such as health, education, well-being, longevity, political and cultural freedom.

Apparently growth is a hard one to distance oneself from, and it’s easier to conjure up ideas of one energy source replacing the other. Nowhere in what either Nafeez nor Chris write do I see anything that is not aimed at keeping up energy supply levels, and economic growth is there to stay as well. Whereas I think we need to limit our energy use by 90% or so, and growth is an idea that needs to die, be buried, and never spoken of again. When you start on about “re-defining the meaning of economic growth”, you’ve already lost me.

I think that maybe we need to stop thinking in global terms about everything we want to do for our own neck of the woods, and that even the anti-globalization movement should perhaps stop being global in its quest. Not everything scales up well, and much of it doesn’t scale up at all. If we manage to do something well, and make it happen, and it works where we are, we don’t need to strive to export it to all corners of the world. Think small, and keep thinking that way. It’s hard enough to make things work in your own backyard.

• Yellen Speaks For An Hour, Market Only Hears Three Words (MarketWatch)

Federal Reserve Chairwoman Janet Yellen spoke for an hour at her press conference Wednesday, but the market only heard three words: “around six months.”She was asked how long the Fed would wait after the tapering ends before it begins to raise interest rates. Her answer: “So the language that we used in the statement is ‘considerable period.’ So I, you know, this is the kind of term it’s hard to define. But, you know, probably means something on the order of around six months, that type of thing.”

She added lots of qualifiers to that, including the assessment of the labor market and the inflation outlook, but the markets only heard “around six months.” Markets sold off.The taper of the Fed’s bond purchases is on course to end in October or November. Six months after that would be April or May. So Yellen said the first rate hike could come in April or May, depending on how the economy is doing. Before this Fed meeting, the market had been expecting the first rate hike to come toward the end of 2015, perhaps in October or December. The updated forecasts provided by the Fed’s “dot plot” would point to a first rate hike in September or October of 2015, just a little faster than the market had been expecting.

Now we’ve heard from the Fed chair that the first hike could — emphasize could — come two or three meetings before that. Did Yellen mean to be that specific? No, the Fed has always loosely defined “considerable period” as about half a year. It’s supposed to be a little vague. She probably didn’t intend to give any hints about timing beyond what the “dot plot” said. No Fed chair is going to confidently tell markets that it’s going to raise rates in 14 months.

But now that she’s leading the Fed, the markets will react to what she said, not what she means. Now it’s up to Yellen and her colleagues to walk this back, if they don’t like what the market heard.

• Yellen and the Fed Go Dark (Bloomberg)

It’s hard to believe now, but the Federal Reserve used to keep its policy decisions a secret until weeks after the fact. Announcements at the end of each meeting, much less the detailed explanations and the news conferences, are all recent practices. The Fed’s latest policy statement, and subsequent comments by the central bank’s new chief, Janet Yellen, both suggest that some policy makers are having some second thoughts about the push for greater transparency. Opacity is back on the menu.

Compare the second-to-last full paragraph of today’s statement to the last paragraph of the statement from Jan. 29. Gone is the so-called Evans Rule, which gave guidance about when the Fed would begin raising short-term interest rates based on a numerical threshold for unemployment. The rule was never very helpful anyway, because the Fed never said it would raise interest rates once unemployment fell below 6.5%, only that it would become less tolerant of inflation at that point. Since inflation is much slower than the target rate of 2%, the Evans Rule served only to confuse. In this case, less information about the Fed’s intentions is clearly better.

What’s intriguing is that the Fed tried to compensate for dropping the Evans Rule by emphasizing “a wide range of information” that would weigh on policy decisions. My favorite is the delightfully vague “readings on financial developments,” which seems to give the Fed a pass to do whatever it wants for any reason it can invent.

Given the difficulty of interpreting the meaning of the statement, many analysts chose to rely on the individual predictions by Federal Open Market Committee members of the level of short-term interest rates at the end of 2015 and 2016. However, the range of estimates for 2016 is so wide as to be meaningless. That may explain, despite hints that the Fed has no plans to raise rates any time soon, why medium-term U.S. Treasury bond yields spiked and Eurodollar futures plunged. Just for good measure, Yellen said that the individual forecasts were worthless as a guide to future policy.

Yellen gave a clue about one thing she wanted to see before raising rates: faster wage growth. Wages now are growing a little faster than 2% annually, which is still far below the historical average. During the press conference, she said that she wouldn’t want to increase rates until wages were growing at a more normal pace of around 3% to 4% annually. Unless you have a crystal ball that tells you what will happen with wages, this possible new target tells you almost nothing about when rates will be raised.

These developments suggest a desire to turn the clock back to a time when traders had to make bets without Fed hand-holding — even if the Fed still does release its economic projections. A shift toward opacity might be wise. The economy is a complex system that no one fully understands, so it would be foolish to commit to any unbending numerical rule that limits policy makers’ flexibility to react to unforeseen events. That was why former Chairman Alan Greenspan was opposed to formal inflation targets.

An additional benefit of opacity is reduced predictability. Scholars have found that financiers take too much risk when they think they know what will happen in the future, so muddying the waters may be just what’s needed to promote a safer financial system.

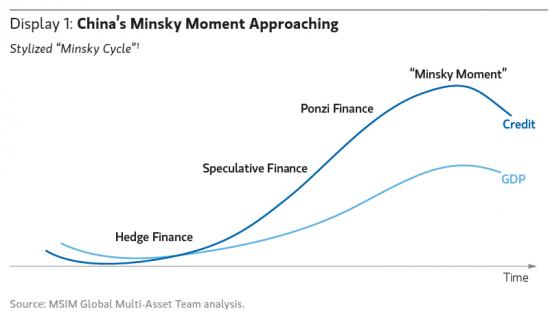

• China’s “Minsky Moment” Is Here (Morgan Stanley)

We have described in detail over the past two years how we believe China’s twin excesses (excessive investment funded by excessive debt) will inevitably unwind, causing a substantial slowdown in China’s economy, significantly below market expectations. In recent weeks, a trip to the region and further research into China’s shadow banking system have convinced us that China is approaching its “Minsky Moment,” (Display 1) which increases the chances of a disorderly unwind of China’s excesses. The efficiency with which credit generates economic activity is already deteriorating, as more investments are made in non-productive projects and more debt is being used to repay old debts.

Based on our analysis, our baseline case is that China may slow from the current level of 7.7% Gross Domestic Product (GDP) growth to 5.0% over the next two years. A disorderly unwind could take Chinese growth down to 4% in a shorter time frame with potentially disastrous consequences for levered Chinese assets (banks, property) and the entire commodity supply chain (commodity stocks, equipment stocks, commodity-sensitive countries and their currencies).

The consensus is more optimistic and expects China’s economy to grow by 7.4% in 2014 and 7.2% in 2015. Most market participants have concluded that the Chinese economy, despite its excesses, will slow only moderately as the government successfully manages to “soft-land” the credit and investment boom and that, as a result, the impact on global GDP growth could be moderate and is not likely to derail the global developed-market-led expansion. However, one of the more controversial conclusions of our analysis is that global economic growth could be impacted severely enough to cause a global earnings recession.

Hyman Minsky was a neo-Keynesian economist who developed a theory called the Financial Instability Hypothesis, similar to the Austrian school of thought, about the impact of credit cycles on the economy. In his 1993 paper entitled “The Financial Instability Hypothesis,” Minsky identified three financing regimes that economies can operate under: the first, which he called hedge finance, is a regime in which borrowers have sufficient cash flows to meet “their contractual obligations,” i.e. interest payments and principal repayment, usually by having a large equity component in their capital structure; the second, speculative finance, is a regime under which borrowers have cash flows that are sufficient to pay interest but not to repay principal, i.e. they must roll over their debts; the third, Ponzi finance, is a regime in which borrowers have insufficient cash flows to pay either principal or interest and therefore must either borrow or sell assets to make interest payments.

Minsky stated that “it can be shown that if hedge financing dominates, then the economy may well be an equilibrium-seeking and containing system. In contrast, the greater the weight of speculative and Ponzi finance, the greater the likelihood that the economy is a deviation amplifying system.” His paper draws the following two conclusions: 1) that “the economy has financing regimes under which it is stable, and financing regimes in which it is unstable” and 2) “that over periods of prolonged prosperity, the economy transits from financial relations that make for a stable system to financial relations that make for an unstable system.” In essence, the longer an economic expansion goes on, the greater the share of speculative and Ponzi finance, and the more unstable the economy becomes.

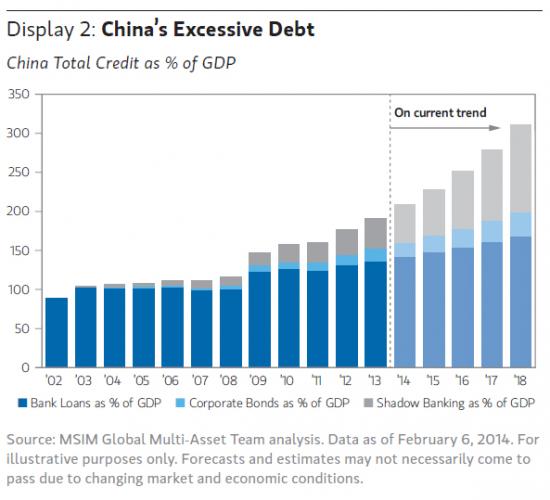

Our analysis indicates that China’s economy has arrived at that unstable state where speculative and Ponzi finance appear to dominate. From a macroeconomic perspective, very few economies have ever created as much debt as China has in the past five years. China’s private sector debt has increased from 115% of GDP in 2007 to 193% at the end of 2013.3 (Display 2) That 80% increase over five years compares to the U.S.’s 26% in 2000-2005. In recent years, only Spain and Ireland have achieved debt growth greater than China’s. Every year, China is now adding $2.5 trillion of private sector debt to a $9.7 trillion GDP.

There is evidence that this debt growth has become excessive and non-productive. It now takes 4 renminbi (RMB) of debt to create 1 renminbi of GDP growth from a nearly 1:1 ratio in the early and mid-2000s. After the massive stimulus and more than doubling of new bank loans in 2009, the government attempted to stabilize credit growth, but the growth of the shadow banking system exploded instead. Shadow banking now accounts for more than a fifth of total credit in China—or about 40% of GDP from a base of 12% just five years ago. The shadow banking system funnels credit to borrowers who can no longer get loans from the formal banking sector, such as Local Government Funding Vehicles, the property sector, and companies in sectors with massive overcapacity and low or negative profitability such as coal mining, steel, cement, shipbuilding, and solar. Work by Nomura’s Chief China Economist indicates that more than half of Local Government Funding Vehicles, which borrow money on behalf of local governments to invest in infrastructure, have insufficient cash flows to pay interest or principal; the exact manifestation of Minsky’s Ponzi finance regime.[..]

• The Chinese Yuan Is Collapsing (Zero Hedge)

The Yuan has weakened over 250 pips in early China trading. Trading at almost 6.22, we are now deeply into the significant-loss-realizing region of the world’s carry-traders and Chinese over-hedgers. Morgan Stanley estimates a minimum $4.8 billion loss for each 100 pip move. However, the bigger picture is considerably worse as the vicious circle of desperate liquidity needs are starting to gang up on Hong Kong real estate and commodity prices. For those who see the silver lining in this and construe all this as a reason to buy more developed world stocks on the premise that the money flooding out of China (et al.) will be parked in the S&P are overlooking the fact that the purchase price of these now-unwanted positions was most likely borrowed, meaning that their liquidation will also extinguish the associated credit, not re-allocate it.

While widening the trading bands keeps some semblance of rationality, this is anything but an orderly unwind of the world’s largest carry trades:

For some context, this is the biggest quarterly drop in CNY since Q4 1993…

• Dropping Like Flies: Largest Shanxi Steel Maker Defaults (Zero Hedge)

When we started discussing the upcoming onslaught of corporate defaults in “Minsky Moment” China, now that the bankruptcy seal has been broken, we warned that the worst is about to come. Well, it’s coming.

Overnight, Hong Kong’s The Standard reported that in addition to the solar, coal and real-estate developer companies that are on everyone’s radar as potential future bankruptcy candidates, one can also add steel makers to the list, with its report that Highsee Group, the largest private steel makers in Shanxi province has defaulted on CNY3 billion of debt, unable to repay its bonds on time.

According to The Standard, “Highsee Group’s 3 billion yuan debt was overdue last week,” the 21st Century Business Herald reported yesterday. “The company is running in red, and has failed to pay workers for months. Many of its furnaces have stopped operating.” The reason for this most recent collapse: the plunge of domestic steel prices , which have fallen to their lowest level in more than eight years in mid-March as a result of weak demand and a surge in output.

Earlier, Shanxi coal miner Liansheng Resources Group went bankrupt while its loans, which were packaged into a wealth management product distributed by China Construction Bank (0939), are likely to be bailed out. UBS Securities securities analyst Chen Li said it is the peak season for corporate debt dues. Up to 80 percent of the nation’s trusts have obligations to meet within the second quarter, he added.

IBT adds that “Highsee Iron and Steel Group … is just one of numerous steel mills facing issues in the country. Data from the National Bureau of Statistics revealed that China produced 2.22 million tonnes of crude steel a day over the first two months of 2014, Reuters reports. This record amount was manufactured even though demand wasn’t as strong.”

It remains to be seen if Highsee is bailed out, however now that pretty much any corporation with exposure to the commodity and real estate space that has maturing debt is on the rocks, the PBOC may be better suited just to let the system cleanse itself, even if that means the collapse in both the Chinese stock market, which unlike the US is largely irrelevant (especially since it once again dropped below 2000 while the Hang Seng entered a bear market), but the bigger issue is that the Chinese housing bubble is set to burst both domestically and abroad, as we reported yesterday.

And lest readers are left with the impression that merely operational companies with direct exposure to the deleveraging carnage that is taking place in China – at least until such time as China unleashes another multi-trillion stimulus – are exposed, also overnight financial firm Southchina Futures announced it is terminating it business on “major operation risks.”

• China to Accelerate Measures to Stabilize Growth (Bloomberg)

China will speed up construction projects and other measures to support economic growth after a slowdown in industrial output and investment boosted risks of missing an expansion target for the year. The nation will “seize the moment to roll out already-determined measures in expanding domestic demand and stabilizing growth,” the State Council, or cabinet, said in a statement last night after a meeting. China will “accelerate preliminary work and construction on key investment projects with timely assignment of budgeted funds,” the cabinet said.

The statement suggests the slowdown’s depth is testing Premier Li Keqiang’s tolerance for growth below what he says is a flexible target of “about” 7.5%. Li, who led the cabinet meeting, is also dealing with challenges including pollution, surging debt and increasing risks of defaults in financial products and companies. “Against the background of increasing downward pressure on growth, the pro-growth signals from the meeting are very timely and necessary,” Xu Gao, chief economist with Everbright Securities Co. in Beijing, said in a note. “Measures to stabilize growth will materialize gradually to cause a modest acceleration in growth,” wrote Xu, who formerly worked at the World Bank.

• ‘Ring of Death’ Throttles Atlanta as Small Banks Close (Bloomberg)

Georgia homebuilder Blankenship Homes lost its source of loans for new construction after four local community banks failed since 2009. “The economy just shut down,” said owner Johnny Blankenship, 54, a builder for more than 30 years in Douglasville, 20 miles west of Atlanta. “We are just starting back to do a few homes. The economy is still very, very slow.”

While the Federal Reserve and U.S. Treasury rescued major banks amid the 2008 financial crisis to avert a meltdown of the nation’s financial system, the bailouts didn’t prevent the collapse of about 500 small lenders. Their disappearance, part of a syndrome of economic weakness, still weighs on growth and employment in dozens of counties across the U.S.

“It will be difficult to fill the void left by failing small banks,” said Mark Zandi, chief economist at Moody’s Analytics Inc. in West Chester, Pennsylvania. “Small bank failures matter a lot to the communities in which they operate, especially in non-urban areas. Small banks are key to small businesses.”

Counties that experienced bank failures from 2008 to 2010 saw income growth reduced as much as 1.43%, job growth cut as much as 0.5%age point and poverty rise as much as 1.4% in the following year, Fed economist John Kandrac reported in research presented last October at a community banking conference at the Federal Reserve Bank of St. Louis. He concluded bank failures had “measurable effects” on economic performance. On average, that meant a drop of as much as $700 in per capita income and a loss of close to 600 jobs in the first year after a failure, Kandrac’s research found.

The demise of local lenders has inflicted a disproportionate blow on small enterprises, said Mark Gertler, an economist at New York University and co-author of research with former Fed Chairman Ben S. Bernanke on how bank failures contributed to the severity of the Great Depression. Community banks provide almost half of small loans, those under $1 million, to farms and businesses, according to a 2012 Federal Deposit Insurance Corp. report.

Bank failures have been more common in four states that experienced real estate booms and busts or had large concentrations of community lenders. Georgia has had the most failures with 88 since September 2007, followed by Florida’s 70, Illinois’s 56 and California’s 39, according to Trepp LLC, a real estate and financial data provider in New York.

Failures nationwide have slowed, with 24 in 2013, led by Florida, with four, and Georgia and Arizona, with three each. Even so, the adverse effects of bank failures, coupled with tighter lending standards, persist. In the counties surrounding Atlanta, that’s compounded by the lingering effects of the collapse of the real estate market.

“There’s a ring of death all around metro Atlanta,” said Brian Olasov, managing director of law firm McKenna Long & Aldridge LLP in Atlanta, using a phrase popularized in the real estate bust by Steve Palm, president of Smart Numbers, a Marietta, Georgia, provider of real estate data. Olasov, who has represented about a dozen boards of banks that failed or are operating under agreements with regulators, said the demise of small banks, coupled with losses that put others on life support, “has sidelined the important mission of allocating capital to borrowers with legitimate needs. It has had a very damaging impact on the state.”

• The Real Gist Of Osborne’s Speech Was That Britain Remains In Deep Trouble (Guardian)

A penny off a pint. Cheaper long-haul flights. Petrol duty frozen. A real corker of a package if you are a bingo-playing pensioner who likes a tot of the hard stuff and has a few quid in the bank. In some ways, George Osborne’s fifth budget was exactly the sort of affair you would imagine with a year to go before a general election.

The chancellor made sure that there was no repeat of the “omnishambles” of two years ago. There was house-building, support for regional theatre and a pledge that Britain will cash in on its discovery of graphene. Not a pasty tax or a granny tax anywhere in sight.

But all the headline-grabbing stuff was beside the point. The real gist of Osborne’s speech was that Britain remains a country in deep, deep trouble. He promised to level with voters, and duly did so. Although growth is now picking up, the deficit is too high and investment too low. Britain, he said, had 20 years of catching up to do and the budget marks the start of the long haul ahead.

It was, of course, a speech that glossed over any failings on the chancellor’s part. Osborne is the first to admit that the Treasury coffers remain empty and upfront about the need for austerity to continue deep into the next parliament. But he has real trouble accepting that he might be in any way responsible for the fact that borrowing in 2014-15 is expected to be £96bn against the £37bn predicted in the first coalition budget in June 2010.

Instead, his message to voters is that Labour left the country skint and it has taken far longer than he imagined to put things right. No mention of the increase in VAT that slowed the economy in 2010 and 2011; no regrets for the over-the-top comparisons between Britain and Greece; no hint of an acknowledgement that austerity might have held back recovery.

All that said, Osborne’s assessment of the fundamental state of the economy is right. For decades, weaknesses have been papered over by debt, North Sea oil and the willingness of other countries to allow us to live beyond our means. The challenge of raising investment, boosting production and increasing saving will face whichever party wins the 2015 election. [..]

• England’s lights ‘would go out without Scotland’s renewable energy’ (Guardian)

Scottish energy minister hits back after UK energy secretary claims independent Scotland would face higher energy bills England’s lights would go out without Scotland’s large and growing supply of renewable energy, according to Scotland’s energy minister. Fergus Ewing hit back after the UK energy secretary, Ed Davey, said independence for Scotland would force up energy bills for Scottish households. “England does require Scotland’s electricity to keep the lights on,” Ewing told the Guardian. He gave the go-ahead on Wednesday for the third largest offshore wind farm in the world, big enough to power 1m homes, as well as new financial support for floating wind turbines to exploit deep water sites.

Ewing, a Scottish National Party minister, contrasted the 20% spare electricity margin in Scotland with the 2-5% margin in the UK as a whole. “The reality is that the supplies of electricity in the UK, especially down south, are parlously tight. There have been successive warnings by Ofgem, the regulator, and it is difficult to see the response to those warnings as anything other than a serial failure to come up with any coherent strategic response,” he said. “On a security of supply basis, England will require to receive imports of Scotland’s electricity for most of the time.”

Davey said on Tuesday: “The size of the UK protects Scottish consumers from the full costs of Scottish power generation. In the UK, Scotland’s households pay less than they would in Scotland alone.”

Scotland has 10% of the UK population but a third of its renewable energy and Davey argued that citizens of an independent Scotland would therefore have to pay more towards the subsidies that support wind and marine energy. He also warned that he would look to Ireland, Iceland and continental Europe for power if Scotland became independent after the referendum on 18 September, as well as boosting renewable energy in the rest of the UK.

Ewing called the claims “political posturing” and said wind energy subsidies make up a “very small proportion” – currently 1.4% – of the costs on the average energy bill. “Over time bills would go down [in an independent Scotland] because we would have greater security of supply.” He also said an independent Scotland would not have to pay the large subsidies agreed by Davey for a new nuclear power station in Somerset, which he estimated at £35bn. Davey, an opponent of nuclear power before entering government, countered: “The Hinkley Point C price we agreed with EDF is at a much lower rate than the strike price for offshore wind.”

• Merkel: Russia faces more sanctions, G8 suspended (BusinessWeek)

German Chancellor Angela Merkel says the European Union will impose more sanctions on Russia following its decision to annex Ukraine’s Crimean Peninsula and will suspend all G-8 meetings until the political situation changes. Merkel told the country’s Parliament Thursday ahead of an EU summit in Brussels that the bloc would expand a freeze of bank accounts and travel bans of people that have been linked to the crisis.

Earlier this week, the EU and the United States slapped sanctions on certain individuals that were involved in what they say was the unlawful referendum in Crimea over joining Russia.She also said that the G-8 will not meet until the situation changes. Russian President Vladimir Putin was due to host leaders from the top industrial countries in Sochi in June.

• Swedish Banks Tighten Amortization Rules to Stem Debt Growth (Bloomberg)

Sweden’s main bank association recommended lenders force more borrowers to pay down their home loans as regulators and the government are working on a “road map” for stricter rules to halt a buildup in consumer debt. The Swedish Bankers’ Association will ask banks to force households to amortize on all mortgages that exceed 70% of their property’s value, from a previous level of 75%, the group said today in an op-ed in newspaper Dagens Nyheter. “Many households do not build a necessary buffer for their mortgage and a more healthy credit culture needs to be created,” Thomas Oestros, head of the association, wrote.

Low rates over the past years and a limited housing supply have fueled a surge in home prices and pushed debt levels to records in the $550 billion economy. Officials are working on a set of rules that will span several years of regulation to get debt growth under control and lower financial risks. They have signaled they will present a plan in the spring.

The government, Financial Supervisory Authority and central bank have joined forces to try to stem household borrowing. Mortgages were capped at 85% of a property’s value in 2010 while the risk-weights banks must apply to their mortgages were tripled last year. Sweden has also imposed some of the world’s strictest capital requirements on its banks.

Finance Minister Anders Borg said the group’s new rules won’t change the road map he plans to present. “The government, the FSA and the Riksbank and others must still act so that we gradually tighten rules, not least on capital requirements, in the coming years,” he said. “This is a good additional measure, but it is not a measure that will replace other measures.” Riksbank Governor Stefan Ingves said today in Stockholm that the new guidelines are “definitely a step in the right direction” even as the level of amortization in Sweden is still lower than in many other countries. “One can always question” whether 70% is enough, he said.

While credit growth slowed to a 20-year low of 4.5% last year, it has since accelerated to more than 5%. Swedish apartment prices rose an annual 11% last year while prices of single-family homes climbed 5%, according to data from Svensk Maeklarstatistik. A report released last year by the FSA showed that at the current pace of amortization it would take households on average 140 years to repay their loans. Only 40% of borrowers with mortgages smaller than 75% of their property’s value actually pay down their debt, the report showed.

• Austerity And Addiction In Greece (NeoKosmos)

At Iasonos street in downtown Athens, a popular hangout for drug addicts, Michalis, 27, is looking for his dealer to buy his ‘fix’. Like most of Athens’ drug users, he is constantly harassed by the police that, since 2013, has multiplied a series of controversial operations aiming to drive drug users and sex workers out of the city centre. “Police and authorities treat us worse than animals,” he says. “The police forcibly put people in their van,” adds Spiros, 48, a fellow drug user. “Once we are in the van, they drive us some 20 kilometres out of Athens and leave us there. Sometimes they will just open the doors and kick us out onto the highway. Just like a garbage bag.”

As Greece enters its sixth year of economic hardship, despair is fraying the country’s social fabric under the weight of austerity measures that have cut the income of ordinary Greeks by 40%. In a nation of 11 million, one third of the population is unemployed while some three million people live below the poverty line.

Greece has been forced to reduce its healthcare expenditures below 6% of its gross domestic product, which was worth 249.10 billion in 2012. Public health spending dropped by 25% between 2009 and 2012 and outlays on medicine were cut by one-third between 2010 and 2011 to 3.75 billion euros. While there was no explanation of where the 6% target came from (the average for the countries of the Organisation for Economic Cooperation and Development is 9%), Greek health system has cracked under the pressure, leaving thousands of people without access to basic medical care.

Across Greece, the by-products of the politics of poverty are visible: data from the Athens-based University Mental Health Research Institute (EPIPSI) indicate that major depression rates have increased by 50% since 2009, affecting more than 12% of the general population in 2013, while drug use and alcohol abuse has risen dramatically. In 2011-2012 Greece experienced an outbreak in HIV infections amongst injecting drug users with a total increase of 1,500% in new infections. Slashing all safety nets is causing the perfect storm of a public health disaster and young Greeks, marginalised by the highest youth unemployment rate in the European Union – six out of ten are jobless – lead the way. Data from the EPIPSI suggests that rates of drug use among teenagers have increased significantly in the last four years, with one out of seven youngsters reporting drug use.

Until recently, any crisis within the Greek welfare system was absorbed by the families, that were the main provider of care and protection to its members, but the brutal recession has deprived households from this ability. For Vasilis Gkitakos, director of the Therapy Centre for Dependent Individuals (KETHEA), one of Greece’s largest networks of drug outreach and rehab facilities, unemployment and drug use are the two major threats to the nation’s health.

“As the hope for a better life and the motivation for treatment decreases but poverty rises, drug addicts increasingly tend to refrain from taking measures to protect their health and become more self-destructive,” says Gkitakos. “But the state fails to acknowledge, let alone to respond, to what is a public health disaster.”

• The global Transition tipping point has arrived – Vive La Révolution (Guardian)

A new post-carbon era dawns as the old fossil fuel system dies. It’s time to step up. Last Friday, I posted an exclusive report about a new NASA-backed scientific research project at the US National Socio-Environmental Synthesis Center (Sesync) to model the risks of civilisational collapse, based on analysis of the key factors involved in the rise and fall of past civilisations.

The story went viral and was quickly picked up by other news outlets around the world which, however, often offered rather misleading headlines. ‘Nasa-backed study says humanity is pretty much screwed’, said Gizmodo. ‘Nasa-funded study says modern society doomed, like the dodo’, said the Washington Times.

Are we doomed? Doom is not the import of this study, nor of my own original research on these issues as encapsulated in my book, A User’s Guide to the Crisis of Civilisation: And How to Save It. Rather what we are seeing, as I’ve argued in detail before, are escalating, interconnected symptoms of the unsustainability of the global system in its current form. While the available evidence suggests that business-as-usual is likely to guarantee worst-case scenarios, simultaneously humanity faces an unprecedented opportunity to create a civilisational form that is in harmony with our environment, and ourselves.

Of course, there are those who go so far as to argue that humanity is heading for extinction by 2030, and that it’s too late to do anything about it. But as other scientists have pointed out, while the number of positive-feedbacks that could go into ‘runaway’ on a business-as-usual scenario appears overwhelming, whether they have yet is at best unclear from the numbers – and at worst, we find that proponents of fatalism are actually systematically misrepresenting and obfuscating the science to justify hopelessness.

Then there are those on the opposite end of the spectrum who have taken up the personal crusade of spreading joy and happiness by pretending that everything’s going to be just fine – all the while ignoring the fact that our leading lights of science such as the US National Academy of Sciences, Nature and the Royal Society are pointing to the convergence of environmental, agricultural and energy challenges in coming decades without some sort of major change.

What the cross-disciplinary study I wrote about last week suggests – like previous research – is that our current trajectory is unsustainable because our demand for ecological resources and services is increasingly going beyond what the planet is able to provide. This ‘overshoot’ is already responsible for a range of overlapping crises – the financial crash, the food crisis, intensifying civil unrest to name just a few – and is likely to worsen without meaningful action.

• US Grid Could Be Down for 18 Months if 9 of 55,000 Substations Destroyed (EconomicCollapse)

What would you do if the Internet or the power grid went down for over a year? Our key infrastructure, including the Internet and the power grid, is far more vulnerable than most people would dare to imagine. These days, most people simply take for granted that the lights will always be on and that the Internet will always function properly. But what if all that changed someday in the blink of an eye?

According to the Federal Energy Regulatory Commission’s latest report, all it would take to plunge the entire nation into darkness for more than a year would be to knock out a transformer manufacturer and just 9 of our 55,000 electrical substations on a really hot summer day. The reality of the matter is that our power grid is in desperate need of updating, and there is very little or no physical security at most of these substations. If terrorists, or saboteurs, or special operations forces wanted to take down our power grid, it would not be very difficult. And as you will read about later in this article, the Internet is extremely vulnerable as well.

If terrorists, or saboteurs, or special operations forces wanted to take down our power grid, it would not be very difficult. And as you will read about later in this article, the Internet is extremely vulnerable as well. When I read the following statement from the Federal Energy Regulatory Commission’s latest report, I was absolutely floored…

“Destroy nine interconnection substations and a transformer manufacturer and the entire United States grid would be down for at least 18 months, probably longer.”

Wow. What would you do without power for 18 months? FERC studied what it would take to collapse the entire electrical grid from coast to coast. What they found was quite unsettling…

In its modeling, FERC studied what would happen if various combinations of substations were crippled in the three electrical systems that serve the contiguous U.S. The agency concluded the systems could go dark if as few as nine locations were knocked out: four in the East, three in the West and two in Texas, people with knowledge of the analysis said. The actual number of locations that would have to be knocked out to spawn a massive blackout would vary depending on available generation resources, energy demand, which is highest on hot days, and other factors, experts said. Because it is difficult to build new transmission routes, existing big substations are becoming more crucial to handling electricity.

Home › Forums › Debt Rattle Mar 20 2014: An Unprecedented Opportunity