Ben Shahn Ads for popular malaria cure. Natchez, Mississippi October 1935

I’m going to take a number of different sources to paint a portrait of China. I’ll take a great series of numbers from Ambrose Evans-Pritchard, whose analysis we can all do without, and leave the analysis up to David Stockman, who goes a long way but, in my proverbial humble view, seems to be stumbling a bit towards the end. That is to say, as I’ve written before, when I look at China these days, I see a bare and basic battle for raw power, economic as well as political power, between the Chinese government and the shadow banking system it has allowed, if not encouraged, to establish and flourish, and which now has grown into a threat to the central state control that is the only model Beijing has ever either understood or been willing to apply.

The Chinese shadow banking system, which you need to understand is exceedingly fluid and has more arms and branches than a cross between an octopus and a centipede, has become a state within the state. That this should happen, in my view, was baked into the cake from the start. Either the Communists could have maintained their strict hold on all facets of power and allow economic growth only in small increments, or it could, as it has chosen to do, push full steam ahead with dazzling growth numbers, but that would always have meant not just the risk, but the certainty, of relinquishing parts of their power and control.

As someone mentioned a while back, if you want to have an economic system based on what we call capitalist free market ideas (leaving aside all questions that surround them for a moment), the players in that system need to have a range of – individual – freedom that will of necessity be in a direct head-on collision with – full – central control. We bear witness to that very battle for power between Beijing and the ”shadows”, right now, as we see the most often highly leveraged shadow capital change shape and identity whenever the political leadership tries to get a handle on it through banning particular forms of borrowing, lending and financing.

There can’t be much doubt that the cheap credit tsunami unleashed in the Middle Kingdom has turned into an extremely damaging phenomenon, as characterized by massive overbuilding, pollution, but the government and central bank have far less power to rein it in than people seem to assume. The shadow system has made so much money financing empty highrises and bridges to nowhere that it will try to continue as long as there’s a last yuan that can be squeezed from doing just that. And when that aspect stops, it will retreat back to where it came from, the shadows, leaving the Xi’s and Li’s presently in charge with the people’s anger to deal with.

Increasingly over the past two decades, China has had two economies. That’s not an accident, it’s what has allowed it to expand at the rate it has. But that expansion is as doomed to failure as any credit boom, and given its sheer size, it’s bound to come crashing down much harder than anything we’ve seen so far in the “once rich” part of the world we ourselves live in. The odds of a soft landing are very slim, and one, but certainly not the only, reason for that is that Beijing has traded in control for faster growth. And that now the negative aspects of the growth process become obvious, it no longer has sufficient control to foster a soft landing.

On the way up, the interests of Beijing and the shadows were very much aligned for obvious reasons; going down, that is no longer true. Li and Xi will be held responsible for the downturn, the men behind the shadows won’t, because no-one will be able to find them. There’ll be middle men hanging from lampposts, but the big players will be retreating to London, New York, Monaco.

But I was going to let others do the talking today. Here are Ambrose’s numbers:

Chinese Anatomy Of A Property Boom On Its Last Legs (AEP)

So now we know what China’s biggest property developer really thinks about the Chinese housing boom. A leaked recording of a dinner speech by Vanke Group’s vice-chairman Mao Daqing more or less confirms what the bears have been saying for months.

It is a dangerous bubble, and already deflating. Prices in Beijing and Shanghai have reached the same extremes seen in Tokyo just before the Nikkei boom turned to bust, when the (quite small) Imperial Palace grounds were in theory worth more than California, and the British Embassy grounds (legacy of a good bet in the 19th Century) were worth as much as Wales.

“In 1990, Tokyo’s total land value accounts for 63.3% of US GDP, while Hong Kong reached 66.3% in 1997. Now, the total land value in Beijing is 61.6% of US GDP, a dangerous level,” said Mr Mao. “Overall, I believe that China has reached its capacity limit for new construction of residential projects”.

• China’s house production per 1,000 head of population reached 35 in 2011. The figure is below 12 in most developed economies “even when the housing market is hot; no country has a figure of greater than 14”.

• “By 2011, housing production per 1000 people reached 30 in Tier 2 cities, excluding the construction of affordable houses.

• “Many owners are trying to get rid of high-priced houses as soon as possible, even at the cost of deep discounts.

• “In China’s 27 key cities, transaction volume dropped 13%, 21%, 30% year-on-year in January, February, and March respectively.

• Among the 27 key cities surveyed, more than 21 have inventory exceeding 12 months, among which are 9 greater than 24 months.

• 42 new projects for elite homes in Beijing will be finished in 2015, hitting the market with an extra 50,000 units that “can’t possibly be digested”.

• China will have 400 million people over the age of 60 by 2033. Half the population will be on welfare by then.“

• Nomura: “We believe that a sharp property market correction could lead to a systemic crisis in China, and is the biggest risk China faces in 2014. The risk is particularly high in third and fourth- tier cities, which accounted for 67% of housing under construction in 2013 … ”

• Land sales and property taxes provided 39% of the Chinese government’s total tax revenue last year, higher than in Ireland when such “fair-weather” taxes during the boom masked the rot in public finances.

• The International Monetary Fund says China is running a budget deficit of 10% of GDP once the land sales are stripped out, and has “considerably less” fiscal leeway than assumed.

• Credit has already grown to $25 trillion. Fitch says China has added the equivalent of the entire US and Japanese banking systems combined in five years.

David Stockman points out what may be the biggest bull in the China shop: because of the massive debt expansion it’s undergone, its economy is inherently unstable. And it’s nonsense to presume that Beijing can, in Stockman’s nicely puts it, “walk the bubble back to stable ground”. This is in part due to the sense of entitlement government policies have instilled in the population, and in part to the rise of the shadow banking system that the Communist party not only has far less control over than it likes to make us believe, but that it fights an active economic war with over control of the economy. Unfortunately Stockman’s analysis, good as it is, glazes over that last point.

Beijings Tepid Efforts To Slow The Credit Boom Are Springing Giant Leaks

China is a case of bastardized socialism on credit steroids. At the turn of century it had $1 trillion of credit market debt outstanding – a figure which has now soared to $25 trillion. The plain fact is that no economic system can remain stable and sustainable after undergoing a 25X debt expansion in a mere 14 years. But that axiom is true in spades for a jerry-built command and control system where there is no free market discipline, meaningful contract law, honest economic information or even primitive understanding that asset values do not grow to the sky.

Nor is there any grasp of the fact that the pell-mell infrastructure building spree of recent years is a one-time event that will leave the economy drowning in excess capacity to produce concrete, steel, coal, copper, chemicals and all manner of fabrications and machinery, such as backhoes and cranes, which go into roads, rails and high rises.

At bottom the fatal error among China bulls is the failure to recognize that the colossal boom and bust cycle that China is undergoing is not symmetrical. The much admired alacrity by which the state guided the export boom after 1994 and the infrastructure boom after 2008 is not evidence of a superior model of governance; its only proof that when credit, favors, subsidies, franchises and speculative windfall opportunities are being passed out freely and to everyone, when there are all winners and no losers (e.g. China’s bankruptcy rate has been infinitesimal), a statist regime can appear to walk on water.

But what it can’t do is walk the bubble back to stable ground. The boom phase unleashes a buzzing, blooming crescendo of enterprising, investing, borrowing and speculating throughout the population that cannot be throttled back without resort to the mailed fist of state power. But the comrades in Beijing have been in the boom-time Santa Claus modality for so long that they are reluctant to unleash the economic gendarmerie.

That’s partly because their arrogance blinds them to the great house of cards which is China today, and partly because they undoubtedly understand that the party’s popularity, legitimacy and even viability would be severely jeopardized if they actually removed the punch bowl. [..]

In short, the Chinese population “can’t handle the truth” in Jack Nicholson’s memorable line. They by now believe they are entitled to a permanent feast and have every expectation that their party and state apparatus will continue to deliver it. As a result, Beijing has resorted to a strategy of tip-toeing around the tulips in a series of start and stop maneuvers to rein-in the credit and building mania. But these tepid initiatives have pushed the credit bubble deeper into the opaque underside of China’s red capitalist regime, meaning that its inherent instability and unsustainability is being massively compounded.

The credit bubble is now migrating into the land of zombie borrowers such as coal mine operators who have always been heavily leveraged but now face plummeting demand and sinking prices owing to Beijing’s unavoidable crackdown on pollution and the rapid slowing of the BTU-intensive industrial economy. Moreover, the $6 trillion in shadow banking loans are the opposite of long-term debt capital: they are ticking time bombs in the form of 12-24 month credits that are being accumulated in a vast snow-plow of maturities that will only intensify the eventual crisis.

There’s no-one debating that Beijing walks a very tight line between growing its economy and bringing that growth back to earth. That would have been a severe challenge no matter what. But its biggest problem now is that there are many buttons and switches and levers in the economy that it effectively no longer even has access to. The shadow state within the state will, as long as there’s a profit in it, behave like water in the sense that you can build a dam at one place but it will find another route to flow down through. This Wall Street Journal article provides a nice example of the how and why of that process:

Entrusted Lending Raises Risks In Chinese Finance

With credit tight in China, companies in industries beset by overcapacity are turning to an unconventional source for cash – other companies – in a new rising risk for the country’s financial system. These company-to-company loans, known as entrusted lending, have emerged as the fastest-growing part of China’s shadow-banking system, which provides credit outside of formal banking channels. Net outstanding entrusted loans increased by 715.3 billion yuan ($115.4 billion) in the first three months of 2014 from a year earlier, according to the most recent data from China’s central bank.

The increase in entrusted loans last year was equivalent to nearly 30% of local-currency loans issued by banks – almost double the portion in 2012. The jump is all the more pronounced since China’s total social financing, a broad measure of overall new credit, shrank 561.2 billion yuan over the same period, largely because other forms of shadow credit declined as Beijing sought to rein in runaway debt growth. [..]

Officials at the People’s Bank of China, the central bank, have warned that much of the intercompany lending is flowing to sectors where the regulators have urged banks to reduce lending: the property market, infrastructure and other areas burdened by excess capacity. In central Shanxi province, 56% of entrusted loans in the past few years have gone to power producers, coking companies and steelmakers, among others, according to a recent paper by Yan Jingwen, an economist at the PBOC. Access to entrusted loans allows struggling companies to hang on longer than they otherwise could, delaying the consolidation that the government and some economists say is needed in a swath of industries.

Big publicly traded companies with access to credit – such as the shipbuilder Sainty Marine and specialty-chemicals producer Zhejiang Longsheng – are among the most active providers of entrusted loans. These companies, instead of investing in their core businesses, lend funds at hand to cash-strapped businesses at several times the official interest rate.

In an analysis for The Wall Street Journal, ChinaScope Financial, a data provider partly owned by Moody’s Corp., found that 10 publicly traded Chinese banks disclosed that the value of entrusted loans facilitated by them reached 3.7 trillion yuan last year, up 46% from the previous year. Compared with 2011, the amount was more than two-thirds higher.

It’s only a matter of time before the Communist party tries to assert control over, and ban, theses entrusted loans. But the people who initiated them will simply move on to other forms of shadow lending, ones that they probably already have waiting in the wings. There are many thousands of party officials and heads of state enterprises who are many miles deep into leveraged debt and will grasp onto any opportunity to double down on their wages in order not to be exposed as gamblers, to hold on to their positions, and to avoid the tar and feathered noose. Beijing will let them, lest the Forbidden City itself fill up with tarred feathers, and try to deflate the balloon puff by puff. As the shadows simultaneously re-inflate it just as fast, if not more.

Still, once it’s clear that you’ve greatly overbuilt, overborrowed and overleveraged, the only way forward is down. The “water always seeks the least resistance” analogy holds up there as well. At some point, in economics like in physics, gravity takes over. And this time around the China avalanche as it moves down its slope has a good chance of burying the rest of the world in a layer of dirt and bricks and mud and mayhem too. So we might as well try to understand this for real, not quit halfway down.

• Entrusted Lending Raises Risks In Chinese Finance (WSJ)

With credit tight in China, companies in industries beset by overcapacity are turning to an unconventional source for cash—other companies—in a new rising risk for the country’s financial system. These company-to-company loans, known as entrusted lending, have emerged as the fastest-growing part of China’s shadow-banking system, which provides credit outside of formal banking channels. Net outstanding entrusted loans increased by 715.3 billion yuan ($115.4 billion) in the first three months of 2014 from a year earlier, according to the most recent data from China’s central bank.

The increase in entrusted loans last year was equivalent to nearly 30% of local-currency loans issued by banks – almost double the portion in 2012. The jump is all the more pronounced since China’s total social financing, a broad measure of overall new credit, shrank 561.2 billion yuan over the same period, largely because other forms of shadow credit declined as Beijing sought to rein in runaway debt growth. The growing popularity of such company-to-company lending offers a fresh – and to regulators, troubling – look at the rapid buildup of debt in China. In its latest report on the country’s financial stability, issued Tuesday, the central bank singled out entrusted lending as a problem, saying it is being used by banks to evade regulatory restrictions on lending. Banks, while generally not risking their own capital directly, act as middlemen in these transactions.

It’s time to crush the euro once and for all. But it’ll be a bitter fight against the zealots who depend on it for their ego’s.

• 3 Things You Have To Believe To Be A Euro Bull (Paul Singer)

The Euro reminds us of the weather in London: One minute you are basking in sparkling sunshine, and the next minute the sky opens in a deluge reminiscent of Noah’s flood. Could it really be that peripheral countries’ interest rates are plunging and borrowing costs have converged to pre-crisis levels, Greece is issuing debt, and the euro crisis is over forever, but Mario “Whatever-It-Takes” Draghi is musing about starting QE now? Have policymakers lost touch with reality to such a startling degree that they now reach for the QE bottle like it is some 1850s cure-all nostrum, regardless of what is wrong with the patient? All we can imagine is the good doctor, handle bar moustache and full regalia, sitting behind his desk: “You have the vapors? Take this QE, you’ll feel better. Ma’am, you have a little hysteria? QE is just the thing! Sir, this QE will cure that headache! Son, you need some inflation, so QE is just right for you.”

There is nothing – we repeat, nothing – that is being done at present to enable Europe to perform better economically, to encourage its unemployed to get off the dole, or to empower its peripheral countries to deal with their underperformance on a sustainable basis. In this context, the bloc’s primary focus on generating inflation is nothing short of astounding. Indeed, one could analogize this currency union at the present moment to a labor camp in the middle of a frozen waste: It is really bad to be locked in, but if you are obedient, you will at least get your next serving of bailout gruel, whereas if you are not obedient, you will be cast out into the howling cold of devaluation and collapse. Lure them in, load them up with debt and whip them into line … is this the plan that the Brussels crowd devised in the 1990s?

This is obviously preferable to constant and terrible continental warfare, but is it sustainable? How will it end? The spectacle is akin to a hair-raising (albeit slow-motion) TV series. Two years ago, it was about to collapse. Today it is working. What will happen on the next episode? All of this talk may seem flip and sardonic, but it is really amazing that this currency union sans sovereignty has lasted so long – long enough to make Rube Goldberg drool with jealousy. Nobody knows how it will ultimately turn out, but we must admire in a sense the gall of politicians who think they can stay the current course and therefore must believe that citizens will stand for no growth and high unemployment forever. Below are some specific outcomes that must be assumed to justify continued stability in the Eurozone, given current pricing of stocks and bonds:

- Italy’s current government will succeed in solving its problems in the promised 100 days, and there will be no talk of elections that might be won by the comedian (who wants out of the Euro).

- The Spanish and Italian unemployed will wait patiently for the good jobs they want without causing any social unrest or political turmoil.

- The higher trading value of the euro will not cause even more pain to the countries that would have already devalued their currencies more than 50% against the current euro price if they were not in the Eurozone. (Remember, if you cannot devalue, you have to increase productivity to be competitive with Germany and the rest of the world. Easy, right?)

The world’s most important industry over the past 100 years is in trouble, and it will never recover. That’ll take some getting used to.

• Chevron’s Profit Plunges 27% As Production Falls (AP)

Chevron Corp. reported a steep decline in its first-quarter profit because of lower global oil prices and bad weather that slowed oil production. Chevron said Friday that it earned $4.52 billion in the first three months of the year on revenue of $50.98 billion. Last year during the same period, Chevron earned $6.18 billion on revenue of $54.3 billion.

San Ramon, Calif.-based Chevron and other major oil companies are struggling to maintain production as they drain oil and gas from their fields around the world. At the same time, the cost of exploring new fields is rising as they have to venture into more extreme and remote conditions to access hydrocarbons. Profits are getting squeezed as these costs rise, because average oil prices have been roughly flat for about three years. Chevron is developing several enormous projects in Australia and the Gulf of Mexico that are expected to help the company expand its production in the coming years. But they aren’t producing anything yet, and analysts worry about Chevron’s ability to get the projects up and running on time and on budget.

In the first quarter of this year, Chevron’s oil and gas production fell 2% worldwide. In the U.S., production fell 4% as higher production of oil and natural gas in New Mexico and western Pennsylvania were more than offset by normal field declines elsewhere. Overseas, where Chevron produces the vast majority of its oil and gas, production fell 2%. Increased production from projects on Nigeria and Angola was offset by field declines and weather-related shutdowns in Kazakhstan.

The race to nowhere is on.

• Hundreds Of Multinational Giants Line Up For Tax Breaks In Britain (Telegraph)

Hundreds of multinational companies are lining up to establish operations in the UK, paving the way for thousands of new jobs and billions of pounds in extra tax revenues. Amid a renewed wave of mergers and acquisitions that has seen US drugs giant Pfizer’s renew its bid for rival AstraZeneca, KPMG, one of Britain’s biggest accountancy firms, said changes to the tax system aimed at improving the UK’s competitiveness were “paying dividends”. It said it was working with almost 100 multinational corporations that wanted to increase their footprint in this country.

PwC, Britain’s biggest accountancy firm, said it was in dialogue with “more than 100” multinational companies, while EY said last year that 60 firms were looking to complete global and regional headquarters relocations into the UK. EY estimated this would add £1bn to corporation tax revenues and create more than 5,000 jobs. Ministers said the revival would help to rebalance Britain’s economy and secure a self-sustaining recovery. “The UK is now very much top of the list for foreign companies looking to increase their activity in the UK,” said David Gauke, the exchequer secretary to the Treasury.

“A few years ago it wasn’t even making the shortlist. All sorts of industries are looking at the UK in a way that is very encouraging. “There is increasingly the sense that the UK is as competitive and as attractive as other jurisdictions, whereas previously multinationals might have looked at Ireland, the Netherlands and Switzerland.” The renewed appetite is in stark contrast to a few years ago, when almost two dozen firms, including advertising giant WPP moved their global headquarters abroad. Several, including WPP, have said they will move back to the UK following the tax overhaul.

Come on, America, buy a car! Make it two!

• Carmakers’ Summer Plans: Back to Bankruptcy? (Bloomberg)

With General Motors’ non-recall scandal raising fresh questions about the kind of company taxpayers rescued five years ago, and its lawyers back in front of a bankruptcy court this week to fend off class-action suits, Detroit is finding out just how difficult it can be to escape the stain of bailout. Another reminder was this week’s report from the Troubled Asset Relief Program special inspector general, indicating the losses on GM and Chryslers’ bailouts ($11.2 billion and $2.9 billion respectively) were higher than previous Treasury Department accountings. Be prepared, taxpayers, the worrying news on your two carmaker “investments” seems to be just getting started.

America’s auto market remains a precarious contradiction: loan terms are longer than ever and subprime penetration is approaching pre-recession levels, yet transaction prices are up. Gas prices, which usually spike in the summer, are heading toward 2008 levels again — yet trucks have been outselling cars for months. Even sales volume itself has to be questioned as inventory to sales ratios indicate that the automakers’ real customers, new car dealers, are choking on supply that factories count as sales. And you don’t have to guess which automakers have the most exposure on these issues.

Always good.

• Punk Economics: Lessons from the Banking Crisis (David McWilliams)

• Chinese Anatomy Of A Property Boom On Its Last Legs (AEP)

So now we know what China’s biggest property developer really thinks about the Chinese housing boom. A leaked recording of a dinner speech by Vanke Group’s vice-chairman Mao Daqing more or less confirms what the bears have been saying for months. It is a dangerous bubble, and already deflating. Prices in Beijing and Shanghai have reached the same extremes seen in Tokyo just before the Nikkei boom turned to bust, when the (quite small) Imperial Palace grounds were in theory worth more than California, and the British Embassy grounds (legacy of a good bet in the 19th Century) were worth as much as Wales. Li Junheng from JL Warren Capital has translated his comments, which I pass on for readers.

“In 1990, Tokyo’s total land value accounts for 63.3% of US GDP, while Hong Kong reached 66.3% in 1997. Now, the total land value in Beijing is 61.6% of US GDP, a dangerous level,” said Mr Mao. “Overall, I believe that China has reached its capacity limit for new construction of residential projects. Only those coastal Tier 3/Tier 4 cities have the potential for capacity expansion. “I don’t see any possibility for a rise in home prices, especially in cities with large housing inventory, unless the government pushes out another few trillion. Beijing and Shanghai have already been listed among the most expensive cities in the world in terms of the medium central city property prices.”

Mr Mao said China’s house production per 1,000 head of population reached 35 in 2011. The figure is below 12 in most developed economies “even when the housing market is hot; no country has a figure of greater than 14”.

“By 2011, housing production per 1000 people reached 30 in Tier 2 cities, excluding the construction of affordable houses. A persistently high figure such as this should cause alarm,” he said.

China’s anti-corruption campaign is spreading terror through the Party cadres. They are frantically trying to offload properties in the top-end range of 40,000 – 50,000 yuan per square metre in case their ill-gotten wealth is exposed by spot audits. The numbers of flats and houses for sale has suddenly doubled. “Many owners are trying to get rid of high-priced houses as soon as possible, even at the cost of deep discounts. As a result, ordinary people who want to sell homes in the secondary market must face deep price cuts,” he said.

“In China’s 27 key cities, transaction volume dropped 13%, 21%, 30% year-on-year in January, February, and March respectively. We expect the trend to continue in April. The drivers behind the fall in price are credit tightening from the banks.”

“Most cities have seen an increase in the ratio of inventory to sales. Among the 27 key cities we surveyed, more than 21 have inventory exceeding 12 months, among which are 9 greater than 24 months. The supply of residential buildings is rapidly increasing month-on-month.”

Mr Mao said 42 new projects for elite homes in Beijing will be finished in 2015, hitting the market with an extra 50,000 units that “can’t possibly be digested”.

As for the demographic time-bomb, he said China will have 400 million people over the age of 60 by 2033. Half the population will be on welfare by then. “If China fails to develop technology as a driving force for its economic growth, the country will be in trouble.”

So there we have it. Vanke Group say the comments do not reflect the view of the company or indeed Mr Mao – which is odd – but they do not dispute that the recording is authentic. His words compliment recent warnings by Nomura’s Zhiwei Zhang that the problem is even worse in the smaller cities in the interior, as we reported last month: “We believe that a sharp property market correction could lead to a systemic crisis in China, and is the biggest risk China faces in 2014. The risk is particularly high in third and fourth- tier cities, which accounted for 67% of housing under construction in 2013,” he said.

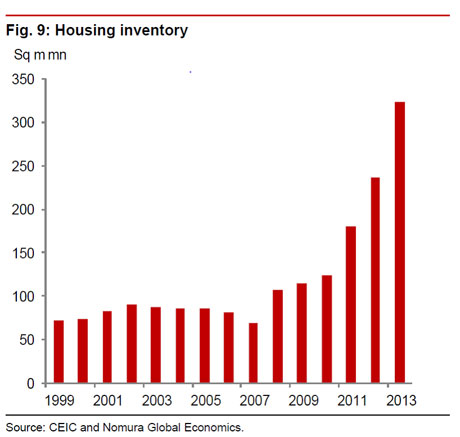

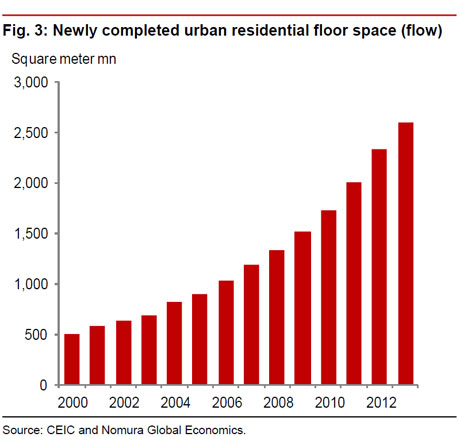

Nomura said residential construction has jumped fivefold from 497m square metres in new floor space to 2.596m last year. Floor space per capita has reached 30 square metres, surpassing the level in Japan in 1988. Land sales and property taxes provided 39% of the Chinese government’s total tax revenue last year, higher than in Ireland when such “fair-weather” taxes during the boom masked the rot in public finances.

There is a huge problem in all this. The International Monetary Fund says China is running a budget deficit of 10% of GDP once the land sales are stripped out, and has “considerably less” fiscal leeway than assumed. The state finances are not what they seem.

This does not necessarily mean that China will spiral into crisis. David Li Daokui – former adviser to the Chinese central bank – told me the nuclear trump card of the authorities is the Reserve Requirement Ratio, currently 20%. They can inject up to $2 trillion into the banking system if need be by slashing the RRR to single figures. It was 6% in the late 1990s. The question is whether President Xi Jinping wishes to take his lumps now by pricking the speculative bubble and forcing capitulation – hopefully in a controlled deleveraging – or whether he will blink as his predecessor famously did in the summer of 2012 and let rip with another round of stimulus.

Blinking stores up greater trouble later. Credit has already grown to $25 trillion. Fitch says China has added the equivalent of the entire US and Japanese banking systems combined in five years.

On balance it is better for China to get the trauma over and done with sooner rather than later. But the rest of the world should be under no illusions as to what it means. This policy decision – should President Xi stay the course – is equivalent in global scale to the decision by Fed chief Benjamin Strong to pop the US speculative bubble in 1928, causing a commodity slump that was transmitted worldwide through the dollar based currency system (Inter-War Gold Standard) and which later snowballed into something far worse. The US was then the world’s rising creditor power, with foreign reserves above 6% of global GDP, almost exactly the same as China’s holdings today. When China sneezes … you will catch a cold, wherever you are.

“China is a case of bastardized socialism on credit steroids [..] But what it can’t do is walk the bubble back to stable ground”

• Beijings Tepid Efforts To Slow The Credit Boom Are Springing Giant Leaks (Stockman)

China is a case of bastardized socialism on credit steroids. At the turn of century it had $1 trillion of credit market debt outstanding – a figure which has now soared to $25 trillion. The plain fact is that no economic system can remain stable and sustainable after undergoing a 25X debt expansion in a mere 14 years. But that axiom is true in spades for a jerry-built command and control system where there is no free market discipline, meaningful contract law, honest economic information or even primitive understanding that asset values do not grow to the sky.

Nor is there any grasp of the fact that the pell-mell infrastructure building spree of recent years is a one-time event that will leave the economy drowning in excess capacity to produce concrete, steel, coal, copper, chemicals and all manner of fabrications and machinery, such as backhoes and cranes, which go into roads, rails and high rises. The borrowing, building and speculating mania in China has obviously gotten so extreme that even the new regime in Beijing has been desperately trying to cool it down. But this will end up as a catastrophic failure—not the “soft landing” brayed about by Wall Street bulls who do not have the slightest comprehension of the difference between free market capitalism and the phony “red capitalism” that has been confected by the party-controlled apparatus of the massive, intrusive, bureaucratic and hierarchically-driven Chinese State.

At bottom the fatal error among China bulls is the failure to recognize that the colossal boom and bust cycle that China is undergoing is not symmetrical. The much admired alacrity by which the state guided the export boom after 1994 and the infrastructure boom after 2008 is not evidence of a superior model of governance; its only proof that when credit, favors, subsidies, franchises and speculative windfall opportunities are being passed out freely and to everyone, when there are all winners and no losers (e.g. China’s bankruptcy rate has been infinitesimal), a statist regime can appear to walk on water.

But what it can’t do is walk the bubble back to stable ground. The boom phase unleashes a buzzing, blooming crescendo of enterprising, investing, borrowing and speculating throughout the population that cannot be throttled back without resort to the mailed fist of state power. But the comrades in Beijing have been in the boom-time Santa Claus modality for so long that they are reluctant to unleash the economic gendarmerie.

=======

That’s partly because their arrogance blinds them to the great house of cards which is China today, and partly because they undoubtedly understand that the party’s popularity, legitimacy and even viability would be severely jeopardized if they actually removed the punch bowl. Just look at the angry crowds which mill about when a bankrupt entrepreneur skips town and locks up his factory sans all the equipment; or when developers are forced to discount vastly over-priced luxury apartment units they sold to middle class savers/speculators; or when banks attempt to disavow repayment responsibility for “trust products” they sold out the backdoor through affiliates; or the growing millions of rural peasants who have been herded into high-rises without jobs after their land was expropriated by crooked local officials and developers trying to make GDP quotas and a quick fortune, respectively.

In short, the Chinese population “can’t handle the truth” in Jack Nicholson’s memorable line. They by now believe they are entitled to a permanent feast and have every expectation that they party and state apparatus will continue to deliver it. As a result, Beijing has resorted to a strategy of tip-toeing around the tulips in a series of start and stop maneuvers to rein-in the credit and building mania.

But these tepid initiative have pushed the credit bubble deeper into the opaque underside of China’s red capitalist regime, meaning that its inherent instability and unsustainability is being massively compounded. The billiard balls that have been bouncing around the table since Beijing attempted to throttle lending by the Big State banks a few years ago provides a dramatic example.

In round one the big banks attempted to avoid credit growth ceilings by taking a leaf out of Citigroup’s playbook, and opened up back-door affiliates which operated off-balance sheet in the world of so-called shadow banking. These affiliates peddled “trust products” which were essentially high yield CDs that returned double or triple the regulated ceiling on regular bank deposit accounts. And how were these back door affiliates to earn a profit when paying say 12% for funds? No problem! The loan departments of the big state banks kindly referred their shaky credits and borrowers desperately underwater to their back-door affiliates who then presented such dodgy supplicants with an offer they couldn’t refuse.–namely, 20% money for 12 or 24 months as an alternative to being shut-off by the parent bank

So the credit house of cards was just enlarged, extended and riddled with more repayment cliffs just around the next corner. From a standing start in 2010, trust product loans and other shadow banking credit extensions have exploded to upwards of $6 trillion.

But here’s the thing. The credit bubble is now migrating into the land of zombie borrowers such as coal mine operators who have always been heavily leveraged but now face plummeting demand and sinking prices owing to Beijing’s unavoidable crackdown on pollution and the rapid slowing of the BTU-intensive industrial economy. Moreover, the $6 trillion in shadow banking loans are the opposite of long-term debt capital: they are ticking time bombs in the form of 12-24 month credits that are being accumulated in a vast snow-plow of maturities that will only intensify the eventual crisis.

To be sure, the state banking regulators have belatedly launched a campaign to crack-down on the explosion of shadow banking loans, but already the proof of the inherent asymmetry in China’s bubble/bust cycle is in. New credit extension is now migrating to the last refuge of an aging bubble–namely, non-financial corporations are plowing vast sums of cash into speculative lending. As the following excerpts from the Wall Street Journal show, such lending has now reached epidemic proportions, and is a direct rebuke to the tepid and well-telegraphed efforts of Beijing to rein in China’s monumental credit bubble:

These company-to-company loans, known as entrusted lending, have emerged as the fastest-growing part of China’s shadow-banking system, which provides credit outside of formal banking channels.The increase in entrusted loans last year was equivalent to nearly 30% of local-currency loans issued by banks—almost double the portion in 2012. The jump is all the more pronounced since China’s total social financing, a broad measure of overall new credit, shrank 561.2 billion yuan over the same period, largely because other forms of shadow credit declined as Beijing sought to rein in runaway debt growth.

It’s all in the mind. That is. Abenomics is. Says Abe.

• Is Japan Totally F##ked? (Zero Hedge)

We have detailed the straitjacket into which the Japanese have been strapped for the past two decades numerous times in the last few years (in great detail here) but as Grant Williams leaned back in his most comfortable chair after reading an article about proposed changes to the GPIF (Government Pension Investment Fund), Japan’s public pension fund; the thought popped into his mind – “Japan really is totally f##ked.” What led him to that well-thought-out and eruditely expressed conclusion? Read on… In an interview with CNN’s Fareed Zakaria earlier this year, Abe explained the true significance of the third arrow:

“What is important about the third arrow, structural reform, is to convince those who resist the steps I am taking and to make them realize that what I have been doing is correct, and by so doing, to engage in structural reform.”

Read that again.Yes folks, the important part of structural reform in Japan is to convince people that Abe is correct. If he can convince them he is right, they will have engaged in structural reform. Confused? You should be. This is how Japan works — or doesn’t. Immigration reform has been widely recognized as the only answer to Japan’s crippling demographic problem for well over three decades. Nothing has been done about it. How about the “Wage Surprise” — increasing wages on a national basis — hailed by Abe as the key to lifting Japan out of the doldrums, and a key feature of Abenomics?

Doh?! Markets will eventually tire of Abe’s continual promises that more is coming, so he desperately needs to somehow break the entrenched deflationary attitude in Japan. (WSJ): In a survey of 1,000 consumers on March 29-30 by broadcaster Fuji News Network, 69% said they had not made any special purchases ahead of the sales tax rise, and 77.4% said they didn’t feel an economic recovery was under way. Good luck with that attitude problem, Shinzo. This week we got a look at how Abe is faring with one of his promises, that of guaranteed 2% inflation. Core CPI (excluding food and energy) rose 1.3% in March — unchanged from the previous month and lower than analyst forecasts. Of course, that was taken as a sign that further easing by the BoJ would be forthcoming…

And round and round it goes… until it stops. The briefcase in Pulp Fiction ONLY works because we DON’T find out what is in it. Abe’s third arrow can be loaded into the bow, but it can’t be fired once and for all, because if it IS fired, the game is up. There will still be continual promises of more to come, and markets may buy into that for a while; but, like all central bank-induced “boom times,” Abenomics has a shelf life, and that is nearing an end. The changes at the GPIF are potentially disastrous, and Kuroda’s BoJ and Abe’s government are desperately trying to MacGyver their way out of an impossible situation, armed only with hollow promises and faith, when what they really need is duct tape and a Swiss army knife.

Abenomics is a plan by which to change Japanese behaviour; but as anyone who has spent any time in that wonderful, perplexing country will tell you, the Japanese do NOT change their behaviour — even when facing a demographic disaster. Sorry, but Abenomics is actually nothing at all.

Take note.

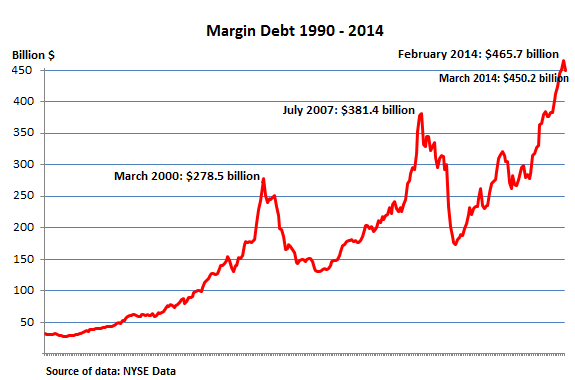

• The Last Two Times Margin Debt Reversed From High All Hell Broke Loose (TPit)

The last two times when margin debt reversed and fell after a record-breaking spike, all hell broke loose. In 2000, it was simultaneous. In 2007, it was delayed by a few months. Today, on the surface, everything is still hunky-dory. The Dow is just fractions below its all-time high that it set on Wednesday. But beneath the surface, parts of the stock market are already coming unglued, and holders of momentum stocks have been eviscerated. The Nasdaq Biotech Index had beautifully shot up along an exponential curve. Then the hot air hissed out of it, and it swooned 21% in six weeks. The index includes big players, like Biogen, not just startups with big dreams and no drugs.

After some buying on the dip, the index closed on Thursday down “only” 15%. But that hasn’t saved smaller momentum stocks: Exelixis is down 58% from its 52-week high and 92% from its all-time high shortly after its IPO in early 2000; Halozyme is down 60% from its high in early January. And so on. In the social media space, the bloodletting has been ugly. The Social Media ETF SOCL is down 23%, but stronger stocks like Facebook (down 16% from its high a month ago) paper over individual fiascos, like Twitter, which has plummeted 48% from its peak last year to below its IPO price. Other momentum stocks are getting annihilated: Amazon down 25% since January, Netflix down 27% in just two months. From their peaks, Pandora crashed 39%, Gogo 63%, and Imperva, a Big Data security outfit, 65%.

Then there’s the “Cloud,” the single most hyped miracle-sector last year. Escalator up, elevator down. Workday, which sells cloud-based corporate software, went public in late 2012 and soared. Two months ago, it sprung a leak and the hot air hissed out of it. It’s down 36%. Veeve, which sells cloud-based healthcare software, has crashed 60% from its November high, shortly after it had gone public. Salesforce is down 22%. ServiceNow lost 30% over the past two weeks. LinkedIn reported a loss after hours on Thursday and got hammered. It’s now down 40% from its peak last September. Jive Software is down 71% from its high in 2012.

They aren’t just outliers. They’re included in the index of 37 publicly traded cloud companies that VC firm Bessemer Venture Partners put together and updates on a weekly basis. From the beginning of the data series in January 2012 to February 27, 2014, the index had soared 129%. But in the two months since then, the index gave up more than half of its gains and lost $58 billion in market cap!

• Marc Faber: A Big Correction Will Hit US Markets This Year (CNBC)

Technology stocks may have suffered a sell-off in the last few weeks, but the U.S. market as a whole is still set for a dramatic correction this year, Marc Faber, the market watcher known as “Dr. Doom” told CNBC Wednesday. The editor and publisher of The Gloom, Boom and Doom Report said that he personally favors emerging market securities that are still “cheap,” adding that he had even made investments in Iraq last year. “We had already a big break in the market but we haven’t had yet the big break in the overall market,” he said.

In early April, the wider technology sector was hit by a selloff in momentum stocks which saw the Nasdaq Composite Index fall below 4,000 points for the first time since early February. Momentum stocks are fast-rising stocks which can unexpectedly reverse when investors fear they have overshot and a bubble is brewing. The Nasdaq Composite suffered its worst weekly hit since June 2012, and recorded its longest weekly losing streak since late 2012. Telecommunication, social media, and biotechnology companies were all part of the move lower, but Faber believes this selling will eventually hit the wider indexes, with energy and utility companies seeing a sharp pullback. Faber reiterated his concerns that equities were facing a crash that could be worse than the financial world saw in 2008.

“I believe it is too late to buy the U.S. stock market,” he said. Faber questioned the future returns of these U.S. stocks, highlighting that record low interest rates and high valuations mean companies will not be able to give back bumper returns to their investors. “In general, I think individual investors have excessively optimistic expectations about their future returns,” Faber said. The notable bear also underlined his belief that emerging markets provide a more suitable option for more profitable investments. He added that he has parked cash in countries such as Vietnam, Iraq, Malaysia, Thailand, and Singapore.

Presented without comment.

• Pray To The God Of Hockey Sticks … (Zero Hedge)

Big topic.

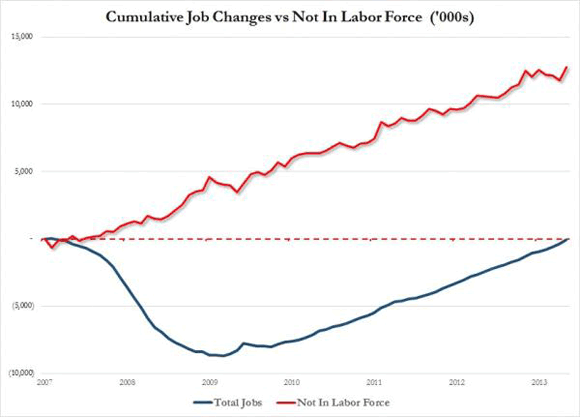

• Workforce Participation at 36-Year Low as Jobs Climb (Bloomberg)

Even the strongest job growth in two years isn’t enough to entice more people into the labor force, one of the biggest conundrums of the U.S. economic expansion. The share of the working-age population either employed or seeking a job declined in April for the first time this year, helping drive the unemployment rate down to 6.3%, the lowest since September 2008. At 62.8%, the so-called participation rate matches the lowest since March 1978. A shrinking workforce saps the U.S. of the manpower needed to boost the expansion to a higher level, keeping the world’s largest economy merely plodding along. It also undercuts the theory that sustained growth alone will be enough to attract more Americans, from students to people discouraged over employment prospects, back into the hunt for jobs.

“It doesn’t seem like the improving job market is really pulling people back into job-seeking,” said Michael Feroli, chief U.S. economist at JPMorgan Chase & Co. in New York. “It is kind of a sobering message about the supply side of the economy and the economy’s potential growth rate.” The decline in participation from 63.2% in March came as fewer Americans entered the work force, while the number of people who have given up the search for employment remained close to the average for the last year. There were 783,000 of these so-called discouraged workers in April, compared with 835,000 a year earlier.

The number of people coming into the workforce — by either landing a job or starting a search for work — plunged to 5.84 million in April, the fewest since November 2008, according to figures from the Labor Department. The 14% decrease from the prior month’s 6.79 million was the biggest since 1995. Those leaving the labor force, which include retirees, people who choose to take care of family members and those pessimistic about finding employment, totaled 6.66 million, little changed from the 6.42 million averaged over the prior 12 months. “It wasn’t so much that more people left, it was that a lot fewer than average entered,” Karen Kosanovich, an economist at the Bureau of Labor Statistics, said in an interview.

Still a Big topic.

• Labor Force Drop-Outs Outnumber US Jobs Recovered Since Depression (Zero Hedge)

While we expect much media coverage of the fact that as of the end of April, total jobs have risen to 138,252K or just 98,000 jobs shy of the December 2007 highs when the depression started (which means that the next jobs report will finally show a full recovery of the jobs lost in the past 6 years), another fact which will not receive nearly as much attention is that the cumulative increase in Americans who have, over the same period, dropped out of the labor force has more than “made up” for the job gains. In fact, it may come as a surprise to most, that since the peak of the depression in February 2010, when the job number dropped to 129.7 million and has been rising ever since, the average monthly number of job adds is 172K. And what about the average monthly number of people who drop out of the labor force since February 2010? 175K, or a virtually perfect mirror image.

Well, the EU/US supported Right Sector has started killing civilians in the east.

• ‘Europe Should Shun Russia Sanctions on Economic Cost’ (BusinessWeek)

Any “sensible” European Union citizen should oppose further sanctions on Russia because of the economic cost for Europe, EU Commissioner Olli Rehn said. “It would harm everybody, the Europeans and the Russians,” Rehn, the European Commissioner for Economic Affairs, said in an interview in Vienna today. Yet “it can only be avoided if Russia is committed to avoiding aggravation and escalation of this crisis,” he said. As EU governments weigh economic sanctions on Russia for failing to stop separatists in Ukraine, the slowing Russian economy is already having a “negative impact” on Finland and Austria, Rehn said. That economic fallout probably will spread to Germany, Poland and the Baltic countries, he said.

Ukraine’s conflict escalated as the army sent armored vehicles and artillery today in a bid to retake the eastern town Slovyansk, a stronghold of pro-Russian separatists. Russian President Vladimir Putin had demanded Ukraine pull back troops as his forces remain massed across the border. “Everybody should try to reduce tension in eastern Ukraine and thus try to prevent an escalation of this regional crisis into a European-wide crisis,” said Rehn, who is on leave from his EU post while running for a seat in European Parliament elections starting May 22.

Even before the U.S and EU imposed sanctions on Russia, the weaker Russian ruble cut sales at Finnish tax-free shops on the border by about 30% compared with a year earlier, Rehn said. The ruble declined 0.7% against the dollar today, trimming the Russian currency’s advance over the past five days to 0.5%. The ruble’s 8.3% retreat this year is the second-worst after Argentina’s peso among 24 developing-country peers monitored by Bloomberg. “From the standpoint of the European Union, I think it is important we show unity in this crisis,” Rehn said. “We have to stand united because if we were disunited, we know Russia would be very skillful in playing that game against European countries.”

Anyone surprised raise your hands.

• Oil Industry, US Government Woefully Unprepared For Spill In Arctic (RT)

A new study says there is a lack of both scientific data and preparedness on the part of private and public entities to properly address an oil spill in the Arctic Ocean, which global powers and industry expect to exploit for energy exploration. Climate change is thawing sea ice in the Arctic, opening up new opportunities for energy development. Approximately 30% of the world’s undiscovered natural gas and about 15% of its untapped oil lie in the Arctic. But the majority, 84%, of the estimated 90 billion barrels of oil and 47.3 trillion cubic meters of gas remain offshore.

Waiting for eager energy developers are some of the world’s most extreme weather conditions “and environmental settings, limited operations and communications infrastructure, a vast geographic area, and vulnerable species, ecosystems, and cultures,” the National Research Council wrote. The five countries with territorial claims in the Arctic – Canada, Denmark, Norway, Russia, and the United States – have stated intentions to develop these reserves, if they haven’t begun already. Yet the National Research Council’s new study – funded by US federal agencies and the leading trade group for the oil industry, the American Petroleum Institute – found that energy companies currently lack Arctic oil spill response plans, as it is their responsibility to address such an event.

That said, public entities often take the lead in spill response actions, yet the US government does not have infrastructure capabilities in place despite its rush to establish dominance in the region. “The lack of infrastructure and oil spill response equipment in the U.S. Arctic is a significant liability in the event of a large oil spill,” the report states. “Building U.S. capabilities to support oil spill response will require significant investment in physical infrastructure and human capabilities, from communications and personnel to transportation systems and traffic monitoring.”

The “significant investment” on infrastructure could come from public-private partnerships, the report suggests, though the politics of offering industry further subsidies may be problematic. Adequate research into what awaits industry in the extreme cold of Arctic waters is also lacking, the report said. There is little understanding of how the low temperatures would affect both spilled oil and commonly-used techniques to reverse the effects of a spill, such as the spread of chemical dispersants. The report goes as far as suggesting that the only way to know is to conduct a controlled oil spill.

Home › Forums › Debt Rattle May 4 2014: A Stampede Of Elephants In The China Shop