Detroit Publishing Co. Japanese Rolling Balls, Coney Island, Cincinnati 1910

We’ve carried a lot of news on Japan’s deteriorating economic and financial situation so far this year (and before), but perhaps it’s now time to wonder how much longer until the rising sun comes apart at the seams. To date, the worst fears over a trend of deflationary pressures, diminishing wages and enormously bloated government debt were somewhat cooled by the assumption that the Japanese people were still avid savers, and so they would be able to withstand quite a bit of turmoil. But that may now have come to an end. And what happens after is very hard to tell, David Stockman calls it a financial no man’s land. What seems certain is that yields on government bonds will soar. Putting pressure on both government and households that will feel like suffocation. Japan has printed its way into survival for decades, and that escape route, the only one they had, looks to be blocked soon. Stockman:

How Japan Blew Its Savings Surplus: What A Keynesian Dystopia Looks Like

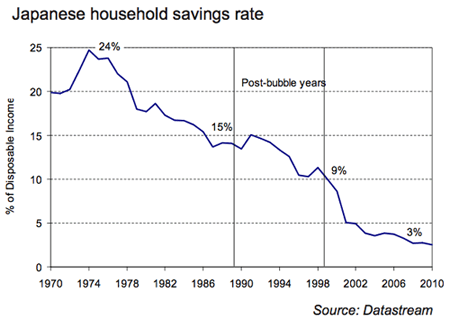

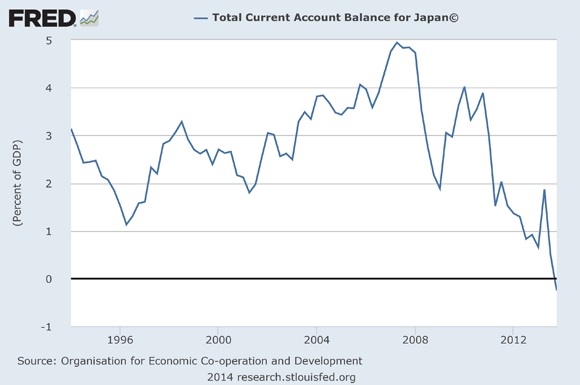

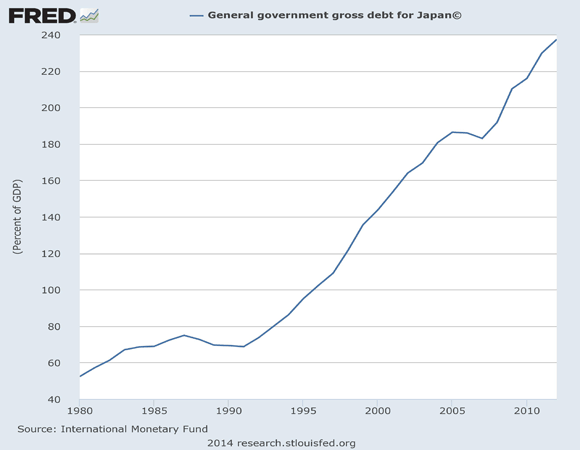

Financially speaking, Japan is fast becoming a Keynesian dystopia. Its entire economy is now hostage to a fiscal time bomb. Namely, government debt which already exceeds 240% of GDP and which is growing rapidly because even the recent traumatic increase in the sales tax from 5% to 8% does not come close to filling the fiscal gap. Moreover, even at today’s absurdly low and BOJ rigged bond rate of 0.6% nearly 25% of government revenue is absorbed by interest payments. Now comes the coup de grace. Japan’s savings rate has collapsed (see below) and its vaunted current account surplus is about ready to disappear.

This means Japan’s accounts with the rest of the world will cross-over into a “financial no man’s land”; it will be forced to steadily liquidate its overseas investments to pay its current bills—an investment surplus built up over the course of 50 years. But this will also reduce foreign earnings and thereby expand Japan’s growing deficit on current account. Accordingly, to finance its “twin deficits” it will have to attract massive amounts of foreign capital for decades to come—an imperative which will require a devastating rise in interest rates, perhaps as high as 4% according to one expert :

The yield on Japan’s benchmark 10-year government bond, now around 0.6%, could rise to 4% – a level unseen since March 1995 — should the current-account balance drop into deficit as public debt eclipses the nation’s savings, said Toshihiro Nagahama, chief economist at Dai-ichi Life Research Institute.

Needless to say, were the carry-cost of Japan’s towering fiscal debts to rise by even half that much it would be game over. Interest expense would absorb virtually 100% of current policy revenue, forcing the government to raise taxes over and over. One expert quoted in the Bloomberg article below says that a sales tax of 20% – nearly triple the recently enacted level – would be required to wrestle down the fiscal monster that would result from interest rate normalization.

Unless the government raises the sales tax to 20% or makes drastic reform on social welfare spending, this scenario is highly likely,” said Ogawa. “Higher interest rates will discourage domestic capital investment and spur the shift of production abroad, increasing the number of people unemployed.”

The above quote strongly hints why Keynesian dystopia is an apt description of what is emerging in Japan; and why that descriptor is also reflective of the financial horror show that is coming to our own financial neighborhood a decade or two down the road. As indicated above, the alternative to an economy killing 20% sales tax is “drastic reform of social welfare spending”. But the latter is not even a remote possibility. Japan’s population is both shrinking and also aging so rapidly that it’s fast on its way to become an archipelago of old age homes.

Here is what happened to the Japanese rate:

Japan savings rate as shown below has dropped from in excess of 20% during its 1970s and 1980s heyday as a mercantilist export power to only 3% today. When Japan’s retired population reaches nearly 40% of the total in the years ahead, this rate will obviously go negative as households liquidate savings in order to survive.

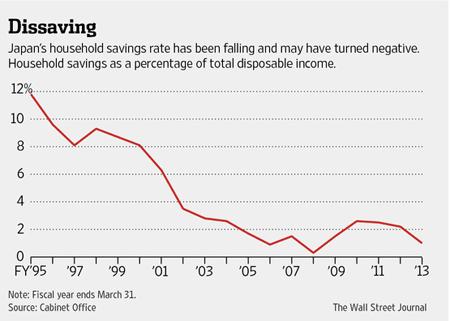

On May 14, the Wall Street Journal ran a piece by Eleanor Warnock that had an updated and slightly different chart, and that suggested savings in the fiscal year through March may have already been below zero:

Are Japanese Eating into Their Savings?

Once some of the world’s biggest savers, Japanese likely dipped into their savings and spent more than they made in the fiscal year through March, the first time Japan’s households have been in the red on an annual basis since World War II. Economists say that gross domestic product data due Thursday will suggest Japan’s household savings rate – the ratio of savings to disposable income – turned negative in the last fiscal year.

That’s because household spending likely jumped 2.4% on year in the period, according to forecasters, largely due to rush demand ahead of a sales-tax increase that took effect April 1. That would be the biggest rise in household spending in a fiscal year since 1996. Since disposable income remained flat, economists say, it was likely enough to help push the household saving rate into the red.

Teizo Taya, an economist and former member of the Bank of Japan policy board who estimates a negative savings rate of between 0.2 and 0.4% in the last fiscal year, says consumer spending might be strong enough to withstand the sales-tax hike. “If the decline continues, the current recovery may be able to continue even in the face of the tax hike,” Mr. Taya said. But there are sizeable risks as consumers become more spendthrift. One is that wages don’t rise concomitantly. That could leave Japanese saddled with debt and crush the newfound optimism.

“It’s not a very good thing for the household savings rate to fall in the red, as it’s a sign that consumers aren’t making enough,” said NLI Research Institute economist Taro Saito, who expects a negative savings rate of 0.4% in the just-ended fiscal year. Another risk for Japan, where public debt is more than three times annual national output, is that a negative savings rate leaves the economy more dependent on foreign financing. Japan boosters have long argued the country can sustain its large debt, the biggest among industrialized nations, because it can borrow from a large pool of domestic savings. Any change in that is a risk.

That last point there is the money quote: the government had been able to continue borrowing because Japanese savers bought its bonds. with a negative savings rate, it no longer can. And foreign investors won’t pick up the slack at an 0.6% rate. I’d also like to note that suggestions that an economy can recover because its people get poorer, don’t fly with me. That’s just economics mumbo jumbo. And we’re not done yet. Stockman continues:

What happened to Japan’s huge savings surplus? The government borrowed it! And wasted it on massive Keynesian stimulus projects that kept the LDP in power for decades but produced bridges and highways to nowhere that will be of no use to Japan’s retirement colony as it ages. And the adverse demographic tide is indeed powerful as shown by the curve below on Japan’s working age population. In a few short years what was a working age population that peaked at 88 million has dropped to 79 million; and it will plunge to below 50 million persons in the next two decades.

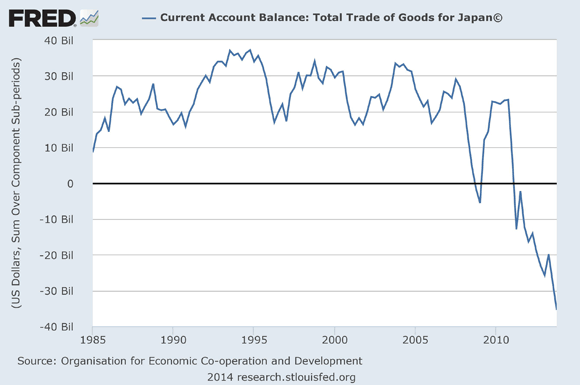

What the Keynesian witch-doctors who advised Japan to bury itself in fiscal stimulation after its financial crisis of 1989-1990 did not explain was how this inexorably shrinking working population could possibly shoulder the tax burden needed to carry Japan’s massive public debt. Yet there is no other way out of the Keynesian debt trap in which Japan is now impaled. As the current account, also shown below, continues to worsen, the need to import capital to fund the gap will drive interest rates sharply higher. The burden on Japan’s remaining taxpayers will become crushing.

I don’t find that Stockman’s arguments become stronger when his every second word is Keynesian, quite the contrary, but that’s his hobby horse right now. Not that he’s wrong, but we already got it, and this is not a game of pick your ideology; it’s much more. Stockman then has a pair of devastating and illuminating graphs:

… the graph below should be pasted on every US Congressman’s forehead. When the debt spiral goes too far – it becomes a devastating financial trap. And it cannot ultimately be solved with money printing because if carried to an extreme – even for the so-called reserve currency – it will destroy the monetary system entirely.

It should also never be forgotten that the drastic degeneration of Japan’s public finances happened in real time – within less than two decades after its leadership was bludgeoned into one fiscal spasm after the next by Keynesian officialdom in the US Treasury, the IMF, the OECD and elsewhere. And this is clearly a case of bad ideas imported from abroad. The generation of officials who lead Japan’s post-war miracle may have been hopelessly addicted to unsustainable models of mercantilist export promotion and currency pegging, but they were not believers in Keynesian borrow and spend.

It’s not just US Congressman who should look at the graphs above and below, it’s European leaders and Chinese party members too, and everyone else. You cannot fight too much debt with more debt. You can perhaps fight some that way, but not too much of it. And while nobody has the government debt that Japan has – as of yet -, how is any major country going to keep itself from going the exact same way if current trends hold?

And we’re still not done. Because Shinzo Abe’s hand is diving and delving deeper into the pockets of the world’s largest pension fund, and ordering it to sell off Japanese bonds into a market that really has just one buyer, the Bank of Japan. As if Abenomics wasn’t scary enough yet, or enough of a failure. This is the Wall Street Journal’s same Eleanor Warnock’s take:

Giant Japanese Fund Set to Invest More in Stocks, Foreign Bonds

Japan’s $1.26 trillion public pension fund will likely announce a boost to stock and foreign-bond investments in early autumn, the head of its investment committee said Tuesday, potentially sending tens of billions of dollars into new markets. A shuffle at the world’s largest pension fund would achieve one of Prime Minister Shinzo Abe’s objectives and could help invigorate Japan’s economy, which is beginning to emerge from a decadeslong era in which investors mostly avoided risk. [..]

She tries the positive spin approach, but does include a warning too:

The changes could raise uncertainty for tens of millions of Japanese who count on steady pension payouts in retirement. With its traditional focus on Japanese sovereign debt, the fund has performed relatively well in recent years despite extremely low debt yields, in part because the country’s deflationary environment was good for bonds. “The [Government Pension Investment Fund] shouldn’t be used as a tool for short-term-oriented intervention in asset markets. It’s not a piggy bank for short-term policy purposes. Each penny of the GPIF is pension money,” said Nobusuke Tamaki, a former fund official who now teaches at Otsuma Women’s University.

While David Stockman has no intention of taking any prisoners:

• Japan Pension Fund Plans Masssive Bond Dump Into Dead Market (Stockman)

So this is how it works. Japan has the most massive public debt in the world relative to national income, but the implicit aim of Abenomics is to destroy the government bond market. After all, if inflation goes to 2% or higher, government bonds yielding 0.6% will experience thumbing losses. Even the robotic Japanese fund managers no longer want to hold the JGB—- as evidenced by another session when no future contracts on either the 10-year or 20-year bond changed hands. As Zero Hedge noted,

You know things have got a little too strange when the largest government bond market in the world saw no futures trades in the morning session last night.We may complain in the US of falling volumes but none, zero, zip, nada is about as low as it gets; and that is how many trades occurred in the 20Y futures contract in Japan (and 10Y cash bond market). This is not the first time as Mizuho warned in Nov 2013 that “to all intents and purposes, there is no JGB market.” And this lack of trading on a day when major macro data printed far worse than expected … well played Abe … you entirely broke your bond market.

In effect, the BOJ is the bond market—that is, the buyer of first, last and only resort. Yes, there are upwards of $12 trillion of Japanese government debt and other obligations outstanding. In normal times, a bond market that didn’t trade in the context of such a massive overhang would have produced sheer panic and bedlam among officialdom. But not in this Keynesian day and age. The implicit assumption is that the BOJ can ultimately buy all the bonds ever issued and the massive outpouring of new bonds yet to come.

After endless prodding by the Abe government, Japan’s pension system (GPIF) will now begin to massively dump hundreds of billion of JGBs. This is being done, of course, to stimulate the Japanese economy by putting pensioners in harm’s way. The cash to be derived from this program of bond dumping will used to purchase Japanese and international equities, along with real estate, private equity, hedge funds and other “alternative asset” classes. And who will buy negative return bonds to be dumped by the GPIF? Why, the BOJ. In Japan, all financial roads lead to the printing press.

Both Japan’s government and its central bank demonstrate in living color what the limits are for governments and central banks when it comes to manipulating economies and markets. And it would be a very good idea for all their peers worldwide to take note. And all of their underlings too. But I have a hunch we will need to see this through to its bitter end before that happens. When its economy crashed early 1990s Japan made one fatefully horrible decision: to not cleanse its banks of their debts, to do basically no defaults or restructuring. And this is the price they’re going to be paying for that decision: once there are no buyers for their cheap debt anymore, the fall will be deep, steep and fast. The rapidly ageing population will see their pension provisions plummet in value, and everyone will see taxes rise more than they can presently imagine just to keep a semblance of a government in place. If we keep up the same approach, in Europe and the US, our foreland too will be no man’s land and nowhere.

• World Bank: ‘Time To Prepare For The Next Crisis’ (CNBC)

Bad weather in the U.S., the crisis in Ukraine, rebalancing in China and the anticipated rise in interest rates will hit global growth this year, according to the World Bank, which has urged countries to continue urgent reforms. The Washington-based organization, a United Nations agency which provides loans to developing countries, has downgraded its global growth estimates for this year to 2.8%, from a January forecast of 3.2%. “We are not totally out of the woods yet,” Kaushik Basu, the bank’s senior vice president and chief economist, said in a press release. “A gradual tightening of fiscal policy and structural reforms are desirable to restore fiscal space depleted by the 2008 financial crisis. In brief, now is the time to prepare for the next crisis.”

Developing countries singled out for special attention included Ghana, India, Kenya, Malaysia, and South Africa. The bank urged these countries to tighten fiscal policy and reinvigorate structural reforms. Growth for developing countries is now eyed at 4.8% this year, down from its January estimate of 5.3%, it said. China is expected to grow by 7.6% this year, it added, but said this would depend on the success of rebalancing efforts by its government and predicted wide “reverberations across Asia” if a feared hard landing occurred. “Growth rates in the developing world remain far too modest to create the kind of jobs we need to improve the lives of the poorest 40%,” President Jim Yong Kim said. “Countries need to move faster and invest more in domestic structural reforms to get broad-based economic growth to levels needed to end extreme poverty in our generation.”

• World Bank Cuts Global Growth Forecast After ‘Bumpy’ 2014 Start (Bloomberg)

The World Bank cut its global growth forecast amid weaker outlooks for the U.S., Russia and China, while calling on emerging markets to strengthen their economies before the Federal Reserve raises interest rates. The Washington-based lender predicts the world economy will expand 2.8% this year, compared with a January projection of 3.2%. The U.S. forecast was reduced to 2.1% from 2.8% while outlooks for Brazil, Russia, India and China were also lowered. The setbacks may be temporary: the 2015 estimate for world economic growth was unchanged at 3.4%.

“The global economy got off to a bumpy start this year buffeted by poor weather in the United States, financial market turbulence and the conflict in” Ukraine, the World Bank said in its Global Economic Prospects report yesterday. “Despite the early weakness, growth is expected to pick up speed as the year progresses.” Developed economies, where domestic demand is improving as fiscal pressure eases and labor markets recover, are providing the global expansion with momentum just as their developing counterparts fail to accelerate. The bank is projecting growth in China and Brazil will slow this year from 2013. In the report, the World Bank warned emerging markets that the next bout of financial unrest may catch them off guard, recommending smaller budget deficits, higher interest rates and measures to boost productivity.

Stockman’s original title: ‘All Japanese Financial Roads Lead To The Printing Press: How The Government Pension Fund Plans A Masssive Bond Dump Into A Dead JGB Market’.

• Japan Blew Its Savings Surplus To Enter Financial No Man’s Land (Stockman)

Financially speaking, Japan is fast becoming a Keynesian dystopia. Its entire economy is now hostage to a fiscal time bomb. Namely, government debt which already exceeds 240% of GDP and which is growing rapidly because even the recent traumatic increase in the sales tax from 5% to 8% does not come close to filling the fiscal gap. Moreover, even at today’s absurdly low and BOJ rigged bond rate of 0.6% nearly 25% of government revenue is absorbed by interest payments. Now comes the coup de grace. Japan’s savings rate has collapsed (see below) and its vaunted current account surplus is about ready to disappear.

This means Japan’s accounts with the rest of the world will cross-over into a “financial no man’s land”; it will be forced to steadily liquidate its overseas investments to pay its current bills—an investment surplus built up over the course of 50 years. But this will also reduce foreign earnings and thereby expand Japan’s growing deficit on current account. Accordingly, to finance its “twin deficits” it will have to attract massive amounts of foreign capital for decades to come—an imperative which will require a devastating rise in interest rates, perhaps as high as 4% according to one expert :

The yield on Japan’s benchmark 10-year government bond, now around 0.6%, could rise to 4% – a level unseen since March 1995 — should the current-account balance drop into deficit as public debt eclipses the nation’s savings, said Toshihiro Nagahama, chief economist at Dai-ichi Life Research Institute.

Needless to say, were the carry-cost of Japan’s towering fiscal debts to rise by even half that much it would be game over. Interest expense would absorb virtually 100% of current policy revenue, forcing the government to raise taxes over and over. One expert quoted in the Bloomberg article below says that a sales tax of 20% – nearly tripple the recently enacted level – would be required to wrestle down the fiscal monster that would result from interest rate normalization.

Unless the government raises the sales tax to 20% or makes drastic reform on social welfare spending, this scenario is highly likely,” said Ogawa. “Higher interest rates will discourage domestic capital investment and spur the shift of production abroad, increasing the number of people unemployed.”

The above quote strongly hints why Keynesian dystopia is an apt description of what is emerging in Japan; and why that descriptor is also reflective of the financial horror show that is coming to our own financial neighborhood a decade or two down the road. As indicated above, the alternative to an economy killing 20% sales tax is “drastic reform of social welfare spending”. But the latter is not even a remote possibility. Japan’s population is both shrinking and also aging so rapidly that its fast on its way to become an archipelago of old age homes. Japan savings rate has dropped from in excess of 20% during its 1970s and 1980s heyday as a mercantilist export power to only 3% today. When Japan’s retired population reaches nearly 40% of the total in the years ahead, this rate will obviously go negative as households liquidate savings in order to survive.

• Is Japan Turning to Voodoo Economics? (Bloomberg)

Sour grapes are in season in Tokyo as Shinzo Abe’s predecessor steps up and slams the prime minister’s tax plans. But beneath the bad feelings and twinge of regret, Yoshihiko Noda makes a very timely point when he accuses Abe of buying into Ronald Reagan’s debunked theories on trickle-down prosperity. “It’s a kind of voodoo economics,” Noda said of the “Abenomics” program that has thrust Japan back into the global spotlight. Noda made those comments, which are sure to irk Abe’s team, to my Bloomberg colleagues Chikako Mogi and Kyoko Shimodoi. The immediate context is Japan’s sales tax, which Noda’s short-lived 2011-2012 government agreed to raise in two steps to contain the world’s highest debt burden. In April, Abe’s government went ahead with the first hike to 8%, but there are questions about the second move to 10% next year.

If the hike doesn’t take place, Noda warned, that “would imply that Japan’s fiscal management strategy will collapse, and the market perception risks are huge.” But far more interesting is Noda’s critique of Abe’s corporate-tax plan. Yes, the nearly 36% levy is among the highest in the world and bringing it down could make Japan a more attractive investment destination. But, as Noda asks, won’t lowering corporate taxes make higher consumption taxes a wash? Absolutely, and the folks at Moody’s and Standard & Poor’s won’t be fooled by this fiscal bait-and-switch. The bigger question is Abe’s faith in the Reagan-era ideology of lowering corporate taxes and reducing levies on profits in order to boost growth, tax revenue and, by extension, living standards. In November 2012, Tokyo unleashed one of modern history’s greatest gestures of corporate welfare, driving the yen down 20%. Nineteen months on, have companies shared the wealth? Nope.

• Giant Japanese Fund Set to Invest More in Stocks, Foreign Bonds (WSJ)

Japan’s $1.26 trillion public pension fund will likely announce a boost to stock and foreign-bond investments in early autumn, the head of its investment committee said Tuesday, potentially sending tens of billions of dollars into new markets. A shuffle at the world’s largest pension fund would achieve one of Prime Minister Shinzo Abe’s objectives and could help invigorate Japan’s economy, which is beginning to emerge from a decadeslong era in which investors mostly avoided risk. “I personally think that we need to complete [the new portfolio] in September or October,” Yasuhiro Yonezawa, head of the Government Pension Investment Fund’s investment committee, said in an interview. “There’s no reason to be slow.” Mr. Yonezawa outlined a tentative plan for a portfolio shift that would raise the allotments of the fund’s assets to go into domestic stocks, foreign bonds and foreign stocks by five%age points in each category.

The aim is twofold: to boost returns to ensure Japanese retirees get the payouts they expect, and to stimulate risk-taking at home by funneling money into growing Japanese businesses. That is in tune with the prime minister’s pro-growth “Abenomics” policies. Since taking office in late 2012, Mr. Abe has exhorted the pension fund to rethink its long-standing conservative investment strategy. Currently, domestic stocks and foreign stocks are each targeted to get about 12% of the fund’s investment. Under the baseline scenario outlined by Mr. Yonezawa, those figures would rise to 17% each, while the portion allotted to foreign bonds would rise to 16% from 11%. Domestic bonds would fall to 40% from 60%, and the portfolio would likely include a new category for alternative investments in areas such as infrastructure, he said. [..]

The changes could raise uncertainty for tens of millions of Japanese who count on steady pension payouts in retirement. With its traditional focus on Japanese sovereign debt, the fund has performed relatively well in recent years despite extremely low debt yields, in part because the country’s deflationary environment was good for bonds. “The [Government Pension Investment Fund] shouldn’t be used as a tool for short-term-oriented intervention in asset markets. It’s not a piggy bank for short-term policy purposes. Each penny of the GPIF is pension money,” said Nobusuke Tamaki, a former fund official who now teaches at Otsuma Women’s University.

• Japan Pension Fund Plans Masssive Bond Dump Into Dead Market (Stockman)

So this is how it works. Japan has the most massive public debt in the world relative to national income, but the implicit aim of Abenomics is to destroy the government bond market. After all, if inflation goes to 2% or higher, government bonds yielding 0.6% will experience thumbing losses. Even the robotic Japanese fund managers no longer want to hold the JGB—- as evidenced by another session when no future contracts on either the 10-year or 20-year bond changed hands. As Zero Hedge noted,

You know things have got a little too strange when the largest government bond market in the world saw no futures trades in the morning session last night.We may complain in the US of falling volumes but none, zero, zip, nada is about as low as it gets; and that is how many trades occurred in the 20Y futures contract in Japan (and 10Y cash bond market). This is not the first time as Mizuho warned in Nov 2013 that “to all intents and purposes, there is no JGB market.” And this lack of trading on a day when major macro data printed far worse than expected… well played Abe… you entirely broke your bond market.

In effect, the BOJ is the bond market—that is, the buyer of first, last and only resort. Yes, there are upwards of $12 trillion of Japanese government debt and other obligations outstanding. In normal times, a bond market that didn’t trade in the context of such a massive overhang would have produced sheer panic and bedlam among officialdom. But not in this Keynesian day and age. The implicit assumption is that the BOJ can ultimately buy all the bonds ever issued and the massive outpouring of new bonds yet to come. Otherwise how can you explain the Wall Street Journal article posted below.

After endless prodding by the Abe government, Japan’s pension system (GPIF) will now begin to massively dump hundreds of billion of JGBs—so that it can reduce its bond holding from 60% of its $1.3 trillion portfolio to 40%. This is being done, of course, to stimulate the Japanese economy by putting pensioners in harm’s way. The cash to be derived from this program of bond dumping will used to purchase Japanese and international equities, along with real estate, private equity, hedge funds and other “alternative asset” classes. And who will buy negative return bonds to be dumped by the GPIF? Why, the BOJ. In Japan, all financial roads lead to the printing press.

Not good. Faith based finance.

• Americans Warming Up to Credit Card Debt Again (Financial Sense)

A few days back we posted this chart on Twitter that clearly indicates an increase in US consumer spending.

One of the questions discussed was “how is this increased spending financed?”. It’s a fair question, given the painfully slow wage growth in the US. On Friday we got our answer. US consumer credit outstanding spiked way above expectations. While the media focused on the jobs report, this was the key news item:

Unlike in previous Fed reports that showed consumer credit growth driven by student loans and to a lesser extent auto finance, we saw something new this time around. The increase was caused by a jump in revolving credit. Americans are warming up to using plastic again.

Not that big a deal, China has hardly any reserves.

• China’s Record Oil Hoarding Seen Keeping Crude Above $100 (Bloomberg)

China is hoarding crude at the fastest pace in at least a decade, shielding itself from supply disruptions and helping keep prices above $100 a barrel. The country imported a record volume in April as it emulates steps taken by the U.S. in the 1970s to create a strategic petroleum reserve, government data show. Chinese President Xi Jinping is building stockpiles as his nation clashes with Vietnam over resources in the South China Sea and faces potential risks to oil sales from Russia, Africa and the Middle East because of sanctions and violence. The purchases are helping drive oil prices higher, according to Barclays Plc, Citigroup Inc. and Nomura Holdings Inc. As China’s thirst for crude grows with the expansion of its emergency stockpiles and refining, the International Energy Agency estimates that the Asian nation is poised to surpass the U.S. as the world’s largest oil consumer by 2030.

“This panicked stockpiling is one of the ways that geopolitical tensions can actually tighten physical oil markets,” Seth Kleinman, a London-based analyst at Citigroup, said yesterday by e-mail. “This buying spree is partly driven by the infrastructure needs of China’s ongoing refinery expansion, but also reflects the rise in geopolitical tensions.” West Texas Intermediate crude, the U.S. benchmark, gained about 9% over the past year to $104.35 a barrel on the New York Mercantile Exchange, while Brent, the marker for more than half the world’s oil, climbed about 5% to $109.52 on the London-based ICE Futures Europe exchange. China bought more than 600,000 barrels a day of surplus crude from January to April, a record for that time of the year based on data compiled by Bloomberg from Chinese statistics tracked since 2004. The surplus supplies are calculated by subtracting refinery runs from the combined total of net imports and domestic production.

UK must leave EU, and it will, so let’s get it done.

• There Is Life After Europe, But Let Us Stop The Triumphalism (AEP)

My chief objection to the CER report is the implicit assumption that the EU would carry on as before after Britain left, as if nothing had happened. This is implausible. The EU is already in existential crisis. The Front National won the French elections with calls for an immediate restoration of the franc and a referendum on Frexit. The Franco-German axis that has held the project together for 50 years has broken down. By launching the euro before the EMU states were ready or able to withstand the rigours of monetary union, and then letting the North-South chasm widen each year, they have led the region into depression and mass unemployment. There is no way out of this under any of the policies being advanced.

The Fiscal Compact ensures that it will go on for another decade or more. This is an intolerable situation. Italy’s Matteo Renzi is already spoiling for a fight. It is far from clear what the EU will look like in 2017 when Britain holds its referendum (unless Labour wins). By then the global cycle of economic expansion might be over, with Europe back in another deep recession before it had ever really shaken off the last one. British withdrawal would not only puncture the EU Project’s aura of historic inevitability but would also change the internal chemistry of the Union. Germany would be placed in a position of hegemony that it does not want, and that would subvert EU cohesion.

It would make France’s subordination even harder to endure, and embolden the Souverainiste camp to look for other solutions. The pro-market states of northern and eastern Europe that tuck in behind Britain would lose their footing. The whole enterprise would become even more unstable at a time when it has already lost its charisma as a motivating idea for the European peoples. I reject the premise that the EU would be calling the political shots in such circumstances, or that Britain would necessarily be a supplicant pleading for terms. The residual EU would be in such crisis that it too would have to tread with extreme care, assuming it was able to come up any coherent terms at all.

The new fad.

• Drugs And Prostitution To Push UK Economy Up By 5% (Guardian)

Britain’s economy could be as much as £65bn bigger – almost 5% – when new GDP figures are published in September incorporating items such as prostitution and drug dealing under new statistical rules. The Office for National Statistics said its latest estimate was that GDP in 2009 was 4.6% higher than previously stated on the back of the planned improvements in measuring the size of the economy. The update will be part of a more inclusive approach to GDP that comes into force in September to comply with EU statistical rules and to “provide the best possible framework for analysing the UK economy and comparing it with those of other countries”. But economists said the change in the size of GDP in official figures, which is unlikely to change the pace of growth in the economy, meant little in reality.

“On paper the economy is £65bn bigger – which is massive. But it is purely an accounting treatment. These activities have always been there – particularly research and development activities – they just weren’t necessarily taken into account in GDP previously,” said Alan Clarke, an economist at Scotiabank. “In isolation, if the economy is 4.6% bigger and nothing else changed, the public finances would look much better – since we tend to look at borrowing relative to GDP or debt relative to GDP. That would be the equivalent of public finances alchemy but we know that the ONS is going to adjust the way it accounts for debt as well – and this is going to be revised higher – so there is no free lunch here.”

People are scared of homes. Just wait till prices come down again.

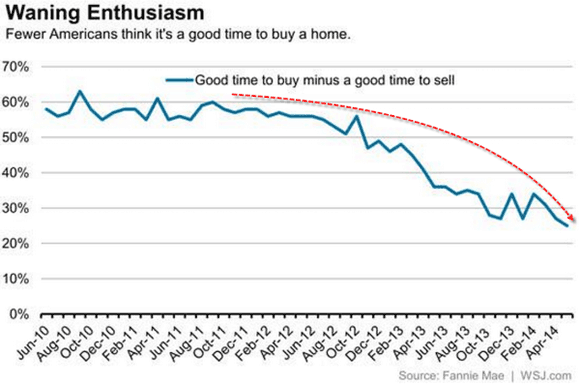

• The Fed-Induced Demise Of The American Dream (Zero Hedge)

Thanks to free and abundant credit to those at the front of the line, home prices have soared in the last few years as “smart” hedge fund managers have bought homes-to-rent in a yield-grab with both hands and feet. This – as we have noted numerous times – priced out the ‘real’ buyer; who this time, instead of being driven by a “fear of missing out”, would rather not play (only to be left holding the bag). Another unintended consequence courtesy of The Fed’s “main-street-helping” actions that has destroyed the American Dream for a declining middle class. Fewer Americans think it’s a good time to buy a home than at any time in the last 4 years… “recovery”! The trickle-down is not working… the middle-class is tapped out (and releveraging just to get by)… and the Fed’s key transmission mechanism to the masses (housing) has now been broken… let’s hope the market doesn’t drop ever again (or the economy).

No way out. Stuck.

• Fed Prepares to Keep Super-Sized Balance Sheet for Years to Come (Bloomberg)

Federal Reserve officials, concerned that selling bonds from their $4.3 trillion portfolio could crush the U.S. recovery, are preparing to keep their balance sheet close to record levels for years. Central bankers are stepping back from a three-year-old strategy for an exit from the unprecedented easing they deployed to battle the worst recession since the Great Depression. Minutes of their last meeting in April made no mention of asset sales. Officials worry that such sales would spark an abrupt increase in long-term interest rates, making it more expensive for consumers to buy goods on credit and companies to invest, according to James Bullard, president of the Federal Reserve Bank of St. Louis. That “is a widespread view in parts of the Fed, I think, and in financial markets,” Bullard said in an interview last week. While he disagrees with that perspective, it “won the day.”

The Fed is testing new tools that would allow it to keep a large balance sheet even after it raises short-term interest rates, a step policy makers anticipate taking next year. They would use these tools to drain excess reserves temporarily from the banking system. “It is pretty clear they are anticipating operating in a situation with a lot of reserves and a high balance sheet for a long time,” said former Fed governor Laurence Meyer, a co-founder of Macroeconomic Advisers LLC, a St. Louis-based forecasting firm. The strategy, which would make the Fed one of the biggest players in money markets, carries risks. In a time of crisis, investors could flock to safe short-term instruments created by the Fed, potentially starving the rest of the financial system of funding.

“The whole situation has created a lot of uncertainty,” said Karl Haeling, head of strategic debt distribution at Landesbank Baden-Wuerttemberg in New York. “The Fed is increasingly stepping into what had been a private-sector function.” The Fed’s asset purchases have expanded its balance sheet to 25% of gross domestic product from 6% at the start of 2007. Central banks from Japan to the U.K. also will have to develop strategies for operating with large portfolios. For example, the Bank of England’s is 24% of GDP, up from about 6% in 2007.

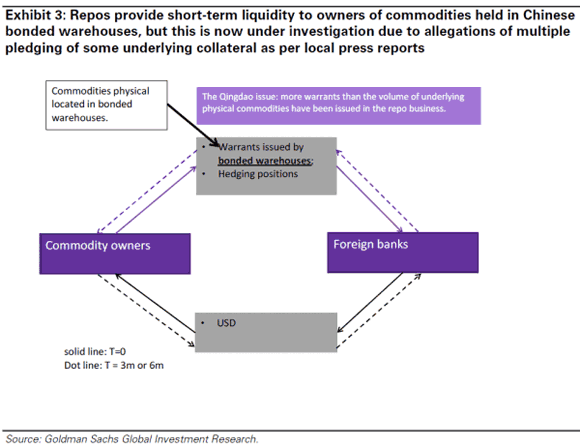

• China’s Rehypothecation Scandal In One Chart (Zero Hedge)

Remember how small Greece was and how it wasn’t relevant to US stocks… until suddenly it got close to breaking up the EU and the world’s markets slumped. Remember how small subprime was? Remember how Lehman was not a ‘big’ bank? We hear the same “why would that impact us?” chatter now about the China rehypothecation scandal and we suspect the outcome will be just as dramatic a “whocouldanode” moment for many. The problem, as this chart so simply explains, is “more warrants than the volume of the underlying physical commodities have been issued in the repo business” and that is a problem for every foreign bank that was tempted into China’s carry trade (which is “every” bank). Simply put – the collateral that I promised you on my loan… I also promised to between 10 and 30 other people… but we’re good right?

The “repo” business in commodities in China is similar to any other “repo” business in the financial markets. Generally speaking, the repo is a short-term FX funding vehicle, whereby a commodity owner first sells the commodity warrants issued by bonded warehouses (paired with an equal amount of short positions) to banks, then buys the package back from the banks in 3 to 6 months. It is a way for commodity traders/refiners to gain access to foreign banks’ balance sheets and improve liquidity efficiently. The Qingdao situation alleges the issuance and pledging of more warrants than the underlying physical commodity. Were this to have occurred, foreign banks may be exposed to asset write-offs due to potential collateral shortages and/or losses. As a result, some foreign banks may have reduced or suspended their commodities repo business in China, and could be undertaking further investigation as to whether to make any suspension permanent.

In a world where central banks have encouraged levered carry trades everywhere, a crack in the virtuous circle – such as we are seeing in China’s fractional-reserve commodity financing deal business – will rapidly lead to a sell first (unwind first), think later mentality.

• That Was Then, This is Now (Jim Kunstler)

A hundred years ago, Buffalo was widely regarded as the city of the future. The boon of electrification made it the Silicon Valley of its day. It was among the top ten US cities in population and wealth. It’s steel industry was second to Pittsburgh and for a while it was second to Detroit in cars. Now, nobody seems to know what Buffalo might become, if anything. It will be especially interesting when the suburban matrix around it enters its own inevitable cycle of abandonment. I’m convinced that the Great Lakes region will be at the center of an internally-focused North American economy when the hallucination of oil-powered globalism dissolves. Places like Buffalo, Cleveland, and Detroit will have a new life, but not at the scale of the twentieth century. On this bike tour the other day, I rode awhile beside a woman who spends all her spare time photographing industrial ruins.

She was serenely adamant that the world will never see anything like that era and its artifacts again. I tend to agree. We cannot grok the stupendous specialness of the past century, and certainly not the fact that it is bygone for good. When people use the term “post-industrial” these days, they don’t really mean it, and, more mysteriously, they don’t know that they don’t mean it. They expect complex, organized, high-powered industry to still be here, only in a new form. They almost always seem to imply (or so I infer) that we can remain “modern” by moving beyond the old smoke and clanking machinery into a nirvana of computer-printed reality. I doubt that we can maintain the complex supply chains of our dwindling material resources and run all those computer operations — even if we can still manage to get some electricity from Niagara Falls.

It’ll get much much worse still.

• China’s Environment Goes From Bad to Worse (BW)

Each year, China’s Ministry of Environmental Protection (MEP) releases a “state of the environment” report; it’s a rather grim annual ritual. For all the talk about China’s new “war on pollution” and money pouring into wind farms and river cleanup campaigns, the reality is that, according to most metrics, China’s environmental situation is getting worse, not better. Air pollution in China receives the most attention globally. Despite a recent stretch of fairly nice days in Beijing, according to the MEP’s report, in 2013 only three major Chinese cities met the government’s own standards for urban air quality. Water pollution—and water shortages—may be an even graver problem. The pollution level in several major rivers, including the Yangtze and its tributaries, has grown more severe since 2010.

Meanwhile 11% of the land in the Yangtze’s watershed and adjacent areas was watered by acid rain. 60% of groundwater-testing sites nation wide ranked as “poor” or “very poor” in water quality. Polluted irrigation water and deposition of evaporated heavy metals (mercury, for instance, vaporizes at high temperatures in coal-fired power plants) also taint cropland in China. According to a report released in April by the government, 16% of China’s total land area—and 19 of its agricultural land—is polluted. Heavy metals deposited in the soil can be absorbed by crops. Last May, the provincial government of Guangzhou revealed that 44% of rice samples it tested in local restaurants contained elevated levels of cadmium, which has been linked to the bone-weakening itai-itai disease in Japan.

How sad is that?

• Babies Pay for Detroit’s Fall With Mortality Rate Above Mexico (Bloomberg)

Detroit’s 60-year deterioration has taken a toll not just on business owners, investors and taxpayers. It’s meant misery for its most vulnerable: children and the women who bear them. While infant mortality fell for decades across the U.S., progress bypassed Detroit, which in 2012 saw a greater proportion of babies die before their first birthdays than any American city, a rate higher than in China, Mexico and Thailand. Pregnancy-related deaths helped put Michigan’s maternal mortality rate in the bottom fifth among states. One in three pregnancies in the city is terminated. Women are integral to the city’s recovery. While officials have drawn up plans to eliminate blight, curb crime and attract jobs, businesses and residents, they’re also struggling to save mothers and babies. The abortion patients awaiting ultrasounds at the Scotsdale Women’s Center and the premature infants hooked to heart monitors at Hutzel Women’s Hospital must be cared for before the bankrupt city can heal itself.

“Detroit is a bad place,” said Crystal Cook, 20, as she waited for an appointment at Scotsdale. Men in the city are “out of control. Most of them don’t have jobs, most of them couldn’t provide. Basically in Detroit, women have to do everything themselves.” The crisis transcends the personal, said Gilda Jacobs, a former state senator from suburban Huntington Woods who heads the Michigan League for Public Policy. “If you have families that are suffering, who aren’t going to work, who aren’t being trained for jobs, they’re never going to be taxpayers,” she said. “You need a holistic approach to improving a city. You need jobs, you need good infrastructure, you need transportation, you need good schools — and you need healthy human capital.” “We want every kid to get off to a healthy start,” said Mayor Mike Duggan, who ran the Detroit Medical Center before taking office in January. “There are lots of things we’ve got to fix, but this is one that’s important to me.”

Home › Forums › Debt Rattle Jun 11 2014: Japan Enters Financial Nowhere