W.H. Jackson Rice Creek near Brown’s Landing, Putnam County, FL 1890

Something tells me I make get into trouble with my Czech and Slovak friends – and readers – over this, but I was still struck by the following interview with former Czech prime minister and president Václav Klaus. I know he’s not uncontroversial, hence the anticipated ‘trouble’.

What Mr. Klaus says in this interview with the Daily Spectator’s Neil Clark is so clear and correct and to the point and glaringly obvious on what is wrong with Europe these days, that his words provide an overriding sense of remembering something that was never there, of what we’ve been missing for years now from leading European politicians. And then we can, and should, wonder why that is, why that sanity has gone MIA.

Europe, or rather Brussels, has become a political-religious cult that tolerates no doubt and no discussion. Or, as Klaus says: “The EU is a post-democratic and post-political system.” . At present, there are no politicians in any of the 28(!) EU member nations, other than your right wing Marine Le Pens and Farages, and your non-aligned Beppe Grillos, who dare utter even one serious word of criticism of the grand EU project. The EU is good, and more EU is better.

And that’s all you need to know, that epitomizes precisely what’s so deeply wrong with the project, why it should be halted before things get even worse and even more people fall victim to the grandiose illusions of what has collapsed into nothing but yet another ordinary power game. That is, there is no dialogue left, it’s been utterly stifled, and that in turn is precisely why it will fail. Here’s Klaus:

NOTE: I’m not sure why the editors picked this title, the word monstrous is not in the text, and the URL tells me it was originally called Europe Needs Systemic Change. Which, admittedly, is less catchy.

Vaclav Klaus: The West’s Lies About Russia Are Monstrous

An interview with the former Czech president, possibly the West’s last truly outspoken leader

Václav Klaus has made a habit of saying things others shy away from saying, but it doesn’t seem to have done him much harm in the popularity stakes. Quite the opposite: the 73-year-old ardently Eurosceptic free-marketeer has legitimate claims to be regarded as the most successful ‘true blue’ conservative politician in Europe over the past 25 years. He was, after all, prime minister of the Czech Republic from 1992 to 1998 and then his country’s president for a further ten years, from 2003 to 2013.

[..] What effect does Klaus think a British referendum on EU membership — and the prospect of a UK withdrawal — might have for the Continent?

‘It would send a strong signal. I was very angry, even in the communist era, looking at Britain from the outside, from behind the Iron Curtain, that Britain decided to leave EFTA to join the EEC in the early 1970s.’

It was a Conservative prime minister, Edward Heath, who took that momentous step. What, I wonder, does Klaus think of the present Conservative leader’s line on Europe?

‘I have met Mr Cameron several times and I am not so sure about his credentials on the EU. I understand he must somehow reflect the division in the whole country and in his party, but nevertheless I don’t think that in a secret ballot in a referendum that he would vote yes [for Britain to remain in the EU] — but this is only my guesstimate.’

Listen to Klaus in full flow on the absurdities of the EU and it’s hard to think why any sane individual — on left or right — would want their country to stay in it.

‘A few days ago I studied the names of the EU commissioners under Mr Juncker, and their portfolios. We in my country say that 16 is already too high for having meaningful portfolios. But the EU now has 28, more than in any country in our part of the world. If you look at the names of those portfolios, I really don’t believe my eyes.

The former Estonian prime minister is a commissioner for digital markets. As an economist I really don’t know what the term “digital markets” means. Plus there is another, a German politician, Günther Oettinger, who is the commissioner for “digital economy and society”. We would laugh in the communist era to have such names for the members of our cabinet. I can’t imagine what these commissioners are doing.’

I put it to Klaus that in the bloated and bureaucratic EU economic model, we have the worst of all worlds — one which pleases neither genuine socialists, nor Thatcherite free-marketers, and he readily agrees. ‘What we have in Europe now is not the German Soziale Marktwirtschaft — the social market economy — but the German model deteriorated by another adjective, “ecological”.’

‘I started my political career after the fall of communism with a well-known slogan: “I want to introduce markets without adjectives.” There was a big fight in the country about this phrase. They said, “Klaus wants to introduce markets without social policy.” “No,” I said. “There can be a social policy, but the slogan means a market economy with an additional social policy and not a social market.”The sequence of the words is all important. At present we are going deeper and deeper and deeper into the ecological and social market economy.’

Whatever we decide to call the current system, he adds, it clearly isn’t working for Europe.

‘I am really shocked to see leading EU and European politicians pretending that everything is OK, which is ridiculous and funny,’ Klaus says. ‘I recently read an article by a well-known German economist, Professor Sinn, who has studied the situation in Italy. He presented statistical data which showed that GDP in Italy has declined by 9% since 2000. It’s unimaginable! I don’t think communist Czechoslovakia would have survived such a long-term decline. At the same time, industrial output declined in the same period by 25%! One quarter of the economy simply disappeared.’

Klaus believes the EU is beyond reform and has called for it to be replaced with an ‘Organisation of European States’ — a simple free trade association which would not pursue political integration. He recalls his own experience at the forefront of Czechoslovakia’s Velvet Revolution in 1989.

‘When we started to change my country we quite deliberately did not use the term “reform” — we used the word “transformation”, because we wanted a systemic change. Such a systemic change is needed in Europe today.’

It’s not just on the economy that Europe has got it wrong, says Klaus. He doesn’t agree with the western elite’s current hostility towards Russia, which he believes is based on a false and outdated view of the country.

‘I remember one person in our country who at one moment was minister of foreign affairs, telling me that he hated communism so much that he was not even able to read Dostoevsky. I have remembered that statement for decades and I am afraid that the current propaganda against Russia is based on a similar argument and way of thinking. I spent most of my life in a communist Czechoslovakia under Soviet domination.

But I differentiate between the Soviet Union and Russia. Those who are not able to understand the difference are simply not looking with open eyes. I always argue with my American and British friends that although the political system in Russia is different from the system in our countries and we wouldn’t be happy to live in such a system, to compare the current Russia with Leonid Brezhnev’s Soviet Union is stupid.’ ‘The US/EU propaganda against Russia is really ridiculous and I can’t accept it.’

Klaus wants to transfer other democratic decision-making powers back to the nation states.

‘I’m not just criticising the EU arrangements — at the same time I’m very critical of global governance and the shift to transnationalism. A week ago I was in Hong Kong and I criticised the naive opening up of countries without keeping or maintaining the anchoring of the nation state. Doing this leads either to anarchy, or to global governance.

My vision for Europe is a Europe of sovereign nation states, definitely. But we have already gone well beyond simply economic integration.

The EU is a post-democratic and post-political system.’

Klaus has spent his political career standing up for sovereignty and rejecting the dominant orthodoxies of the day. Unlike other leaders in the former Soviet bloc countries, he did not feel inhibited about criticising western policies when the Berlin Wall came down. He was one of the few to oppose the Clinton/Blair ‘humanitarian’ bombardment of Yugoslavia in 1999 (he was also strongly critical of the Iraq war).

Yet he feels the freedom to hold — and express — ‘unfashionable’ views in the West is now under increasing threat.

‘If you ask me whether I think liberty is under huge attack in Europe now, I would say yes. I feel repressed by not being allowed to express my views. I have permanent troubles with this. Suddenly I have discovered, for the first time in 20 years, having been invited to be a keynote speaker at a conference, that the organisers find out I have reservations about the EU, about same-sex marriages, about the Ukraine crisis, and they say, “We are very sorry, we have already found a different keynote speaker, thank you very much.” This is something I had experienced in the communist era but not in so-called free Europe. Only a very narrow range of opinions is now considered politically correct.’

It’s to fight this worrying trend that Klaus has decided to launch a new project. ‘I am planning, if we can get the money and people together, to start a new quarterly journal in 2015 called Europe and Liberty.’

It’s hard not to wish him well. In the not too distant past, Europe did have leaders who had clear and distinct visions: on the left, the likes of Sweden’s Olof Palme and Austria’s Bruno Kreisky; on the right, de Gaulle and Margaret Thatcher. You could agree or disagree but you could never say you didn’t know what they believed in, or that the views they held were not sincere. But they’ve been replaced by a generation of bland, uninspiring, consistently ‘on-message’ politicians.

Václav Klaus is different, a throwback to the days when our leaders did stand for something and weren’t afraid to speak their minds. Let’s hope he does not turn out to be Europe’s last conviction politician.

• Fisher: Fed To Release ‘Some Data That Will Knock Your Socks Off’ (Bloomberg)

The Federal Reserve mustn’t “fall behind the curve” as it weighs when to start raising interest rates, Dallas Fed President Richard Fisher said, citing strengthening U.S. growth and building wage-price pressures. Fisher, a vocal advocate for tighter monetary policy to protect against inflation, also said today that two soon-to-be-released economic reports from his Fed district would “knock your socks off.” “I don’t want to fall behind the curve here,” Fisher said in a Fox News interview. “I think we could suddenly get a patch of high growth, see some wage-price inflation, and that is when you start to worry.” Fisher dissented on Sept. 17 at the last meeting of the Federal Open Market Committee, when the Fed retained a pledge to keep rates near zero for a “considerable time” after its asset purchases halt at the end of next month.

He called U.S. second-quarter growth “uber strong,” referring to the upward revision last week to an annualized rate of 4.6% from 4.2% previously estimated, and said history had shown that wage pressures could accelerate when unemployment got below current levels of 6.1%. In addition, Fisher said surveys of wage-price pressures in the Dallas Fed’s district, which includes Texas, northern Louisiana and southern New Mexico, were the highest since before the recession, and other indictors were also buoyant. “We’re going to be releasing some data on Monday and Tuesday, our new surveys, that I think will just knock your socks off,” he said.

• Morgan Stanley Warns On Asian Debt Shock As Dollar Soars (AEP)

Debt ratios in developing Asia have surpassed extremes seen just before the East Asian financial crisis blew up in the late 1990s and companies have borrowed unprecedented sums in dollars, leaving the region highly vulnerable to US monetary tightening. Morgan Stanley said foreign debt in emerging Asia has soared from $300bn to $2.5 trillion over the last decade, creating the risk of a currency shock as the dollar surges to a four-year high and threatens to smash through key technical resistance. “High dollar liabilities do not bode well for emerging markets. In Asia (excluding Japan), the credit-to-GDP gap has reached levels higher than 1997,” it said. The US bank warned clients that local lenders in Asia have relied increasingly on the wholesale capital markets – a little like Northern Rock before 2007 – allowing them to expand credit faster than deposit growth. This leaves them exposed if liquidity dries up.

Asia’s credit-to-GDP gap measures how far loan expansion has pulled ahead of the underlying trend growth of the economy. It peaked at 10pc in 1997. This time a flood of cheap money from Western central banks and the Chinese authorities has pushed it to 15pc, clear evidence of credit exhaustion as productivity stalls and the region’s economic model looses steam. The bank’s currency team said the region could be hit on two fronts at once: a credit squeeze as rising US rates push up borrowing costs across the world, combined with an exchange rate squeeze on “short” dollar positions. The response to one complicates the other. Morgan Stanley’s technical analysts say the dollar is poised to break its thirty-year downtrend as the Fed turns hawkish. It expects the dollar index – a broad gauge of the dollar exchange rate — to surge towards 92 by next year if it breaks through resistance at 87. Such a move would be comparable to the global dollar shock that caused such strains twenty years ago.

The Asian Development Bank (ADB) warned last week that the area should brace for “tighter liquidity” and possible “capital outflows” as the US ends quantitative easing in October. “While the region’s bond markets have been calm in 2014, the risks are rising, including earlier than expected interest rate hikes by the Federal Reserve,” it said. The Fed was buying $85bn of bonds each month as recently as January. A fall to zero amounts to a major shift in global financial dynamics even before rates rise. The ADB said in its Bond Monitor that emerging Asia issued a record $1.1 trillion of local currency bonds in the second quarter of 2014, pushing the total stock to $7.9 trillion. Most debt is at maturities below thee years, creating roll-over risk. This does not include $1.5 trillion of cross-border bank loans and over $1.2 trillion in foreign currency bonds on latest estimates, mostly in dollars and owed by companies.

• Put Everything In Goldman Sachs Because These Guys Can Do What They Want (ZH)

When we first covered the Carmen Segarra lawsuit alleging the capture of the NY Fed by Goldman Sachs back in October 2013, we didn’t have much hope for justice to get done. We said that “while her allegations may be non-definitive, and her wrongful termination suit is ultimately dropped, there is hope this opens up an inquiry into the close relationship between Goldman and the NY Fed. Alas, since the judicial branch is also under the control of the two abovementioned entities, we very much doubt it.” Sure enough, the lawsuit was dropped (and no inquiry was opened) but not before it became clear that the very judge in charge of the case, U.S. District Judge Ronnie Abrams, was herself conflicted, after it was revealed that her husband, Greg Andres, a partner at Davis Polk & Wardwell, was representing Goldman in an advisory capacity.

Curiously, before she assumed her current office in March 2013, back in 2008 Abrams returned to Davis Polk herself as Special Counsel for Pro Bono. She had previously worked at the firm from 1994 to 1998. As a result of this fiasco, some wondered just how far do Goldman’s tentacles stretch not only at the money-printing (i.e., NY Fed) level, not only at the legislative level, but at the judicial as well. And then, on Friday, the Segarra case against the Federal Reserve branch of Goldman Sachs got a second wind, when as a result of another disclosure, ProPublica revealed “How Goldman Controls The New York Fed in 47.5 Hours Of “The Secret Goldman Sachs Tapes.” That is to say, nothing new was revealed per se, because as anyone who has read this website for the past 6 years knows just how vast Goldman’s network is not only at the Fed, but in that all important other continent too, Europe.

But before we put this topic to bed, here is Raúl Ilargi Meijer explaining why “The US Has No Banking Regulation, And It Doesn’t Want Any”

• Kiwi Intervention Drives Australian Dollar Down (SMH)

The Australian dollar fell close to a four-year low on Monday after the Reserve Bank of New Zealand confirmed it had intervened in currency markets last month. The local currency dropped as far as US86.84¢ in late trade after coming under pressure around midday when the RBNZ announced it sold a net $NZ521 million in August, the biggest sale since July 2007 Monday’s fall extended this month’s hefty sell-off to 7.25 per cent and took the Aussie to its lowest since January when it dropped to US86.60¢. The last time the currency traded below that level was in July 2010. The New Zealand dollar was hit even harder on Monday, slumping as much as 2 per cent to US77.09¢ – a one-year low – before part-way recovering to $US74.54¢. The Australian dollar was quick to follow the Kiwi down, but it was not as severely hit.

“The argument that the New Zealand dollar is overvalued, which the RBNZ has done and used it to justify its intervention, is very much the same case in Australia. It’s driven by a commodity price story,” RBS Morgans currency strategist Gregg Gibbs said. “[The strength of the greenback] has been the story in currency markets over the last month. You could argue that the RBNZ is coming in at a time of dollar strength to help get the wind behind their sails in getting the Kiwi lower and that certainly has helped.” There is no economic data on the calendar for Australia on Monday. Private sector credit is scheduled for release on Tuesday, retail sales on Wednesday and building approvals on Thursday. Both the Aussie and the New Zealand dollar came under pressure on Thursday when the Reserve Bank of New Zealand governor Graeme Wheeler released an unscheduled statement saying the Kiwi’s strength was “unjustified and unsustainable”.

• Greenberg Team to Grill Bernanke, Geithner on AIG Bailout (Bloomberg)

In Maurice “Hank” Greenberg’s telling, the $182 billion taxpayer bailout that saved American International Group (AIG) and perhaps all of Wall Street during the 2008 financial collapse was a government rip-off. It trampled the rights of shareholders, denying them more favorable terms offered to banks and companies that foundered during the meltdown, according to Greenberg, who built AIG into the world’s biggest insurer before leaving in 2005. Greenberg’s Starr International Co., AIG’s largest shareholder when the financial crisis struck, sued the government, calling its assumption of 80% of the insurer’s stock an unconstitutional “taking” of property that requires at least $25 billion in compensation. A trial of his claims begins today in Washington, where David Boies, Greenberg’s famed litigator, will question the architects of the bailout, including Ben Bernanke, Henry Paulson and Timothy Geithner.

“I think they’re going to lose,” Marcel Kahan, a New York University law professor who specializes in corporate finance and governance, said of Greenberg and Boies. “I think they realize they’re going to lose. But you never know what’s going to happen.” The complaint by Starr International, Greenberg’s Swiss-based investment company, doesn’t question the necessity of a rescue that began under Republican President George W. Bush and continued under Democrat Barack Obama. Rather, Starr claims AIG was singled out for punitive treatment that violated shareholders’ constitutional rights to due process and just compensation for their property. While Greenberg faces long odds of winning, he could succeed in putting the bailout on trial, a potential payback for the mistreatment he claims in his suit, Kahan said. “If you can depose Obama’s former Treasury secretary and high-level politicians, God knows what you will uncover that would be embarrassing for the Obama administration,” he said.

• Bill Black: Eric Holder Struck Our Every Time, Never Even Took A Swing (TRNN)

Eric Holder has surprised me. I always predicted that he would at least find one token case to prosecute some bank senior executive for crimes that led to the creation of the financial crisis and the global Great Recession. He’s actually going to leave without even a token conviction, or even a token effort at convicting. So, in baseball terms, he struck out every time, batting 0.000, but he actually never took a swing. So he was called out on strikes looking, as we would say in baseball. And I couldn’t believe that he would leave without at least having one attempted prosecution against these folks. So he hasn’t done the most–he never did the most elementary things required to succeed. He never reestablished the criminal referral process, which is from the banking regulatory agencies, who are the only ones who are going to do widescale criminal referrals against bank CEOs, because, of course, banks won’t make criminal referrals against their own CEOs.

Holder could have reestablished that criminal referral process in a single email on the first day in office to his counterparts in the banking regulatory agencies, and he’s going to leave never having attempted to do so. On top of that, if you’re not going to have criminal referrals from the agencies, the only other conceivable way that you’re going to learn about elite criminal misconduct of this kind is through whistleblowers. And as you mentioned, this administration, and Eric Holder in particular, are known for the viciousness of their war against whistleblowers. What the public doesn’t know – and it doesn’t know because of Eric Holder – is that in the three biggest cases involving banks – again, none of them, not a single prosecution of the elite bankers that drove this crisis–all three of those cases, against Citicorp, against JPMorgan, and against Bank of America, were made possible by whistleblowers.

Eric Holder was the czar at the Department of Justice press conferences in each of these three cases, and he and the Justice Department officials, the senior Justice Department officials, at those press conferences, never mentioned the role of the whistleblowers–never praised the whistleblowers and never used those press conferences as a forum for asking whistleblowers to come forward. And so your viewers should take a look at the Frontline special on this, where the Frontline producers made clear that as soon as word got out that they were investigating the area, dozens of whistleblowers came forward, and each of them had the same story: the Department of Justice had never contacted them.

• While ECB Struggles, Fed Sees Recovery (Reuters)

On one side of the Atlantic they’re trying to refill the punchbowl. On the other they’re getting ready to take it away. This week, investors may get a clearer idea why. The European Central Bank will spell out on Thursday its latest attempt to steer the euro zone away from the prospect of damaging deflation, following the latest snapshot of consumer price pressures on Tuesday. U.S. jobs numbers on Friday will probably confirm that the fast-recovering American economy has reached the point where the Federal Reserve can finally halt its massive bond-buying stimulus. The contrast between the U.S. and euro zone economies has grown increasingly stark, adding to the pressure on the ECB and European leaders to revive growth in their corner of the world.

U.S. Treasury Secretary Jack Lew last week laid bare Washington’s long-standing frustrations with the reluctance of European governments to increase public spending. The risk of the euro zone sliding into deflation and deeper stagnation is adding to the drag on the global economy from a slowdown in China, where authorities are trying to rein in lending, and concerns about conflict in the Middle East. But instead of fiscal action by European governments, it is action by the ECB that is the most likely spur for the region. After surprising markets with an interest rate cut at its September meeting and trying to get banks to take cheap loans to boost lending, the ECB on Thursday is due to give details of its plan to unblock corporate credit by buying repackaged loans.

• Political Reticence Blunts ECB’s Asset Purchase Plan (FT)

The European Central Bank will this week unveil details of its plan to save the eurozone from economic stagnation by buying hundreds of billions of euros-worth of private-sector assets. But one of the most crucial questions surrounding the purchases of bundles of loans, known as asset-backed securities, looks set to remain unanswered for some time. The governing council will meet in Naples, where it is expected on Thursday to reveal which asset-backed securities and covered bonds the central bank plans to buy to revive growth and boost inflation. Analysts say inflation is likely to have fallen to a five-year low this month. The purchases will work in tandem with the central bank’s offers of cheap four-year loans, under what it dubs its targeted longer term refinancing operations, to bloat its balance sheet by as much as €1tn between now and the end of 2016.

But one of the most vital pieces of information about the programme will almost certainly be missing. Whether the ECB can buy the riskier parts of securitisations, the so-called mezzanine tranches, is up to governments. With the new European Commission not yet in place, eurozone finance ministers are unlikely to discuss the issue until the end of October, with a decision weeks later. The early indications are that Germany and France will not support the plan. The ECB’s president, Mario Draghi, said earlier this month that the central bank would buy the safest slices of securitisations, known as senior tranches. But the ECB is cautious of taking too much risk on to the central bank’s balance sheet. To avoid that, Mr Draghi said the ECB would buy the mezzanine tranches only if governments would guarantee any losses.

• Quiet Build-Up of Greek Private Bad Debt Casts Long Shadow (Bloomberg)

To Aristides Belles, it’s clear what’s blocking Greece’s recovery: a quiet build-up of about €164 billion ($208 billion) in private bad debts. “The inability of Greek companies to repay their loans to banks and to the state is clearly holding back Greece’s return to growth,” said the chief executive officer of Athens-based Nireus Aquaculture, a producer of sea bream, sea bass and processed fish. “It’s more necessary than ever for all parties involved – banks, corporates and the state – to agree on an arrangement.” As Greece and its euro-area creditors meet tomorrow to review its progress ahead of another round of talks on repayment terms for its public debt, a less-visible crisis is looming on another front: bad debts of households and companies. The borrowings, amounting to about 90% of Greece’s gross domestic product, are weighing on the country’s hopes of recovering from the steepest and longest recession on record.

Non-performing loans at Greece’s banks have reached almost €80 billion, according to the country’s Growth and Competitiveness Minister Nikolaos Dendias. To top that, Greek households and corporations had overdue taxes of €69.2 billion in August, data from the public revenue secretariat show. Also, “collectible” social arrears to pension funds exceed €14.5 billion, according to labor ministry figures. “Some of this debt can never be recovered and should be written off,” said Panos Tsakloglou, a professor at the Athens University of Economics and Business who was Greece’s representative in the working group of senior euro-area finance ministry officials until June. Although Finance Minister Gikas Hardouvelis expects Greece to return to growth in the third quarter this year, the bad debt threatens to curb new lending needed to stimulate the economy.

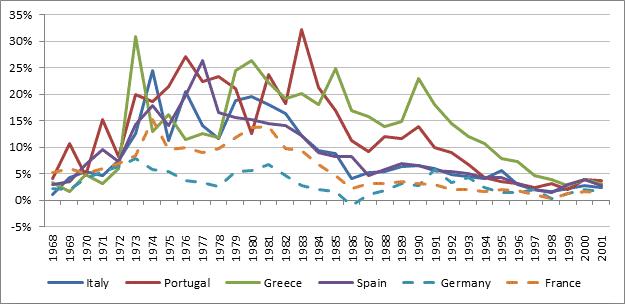

• Why Peripheral Eurozone Debt Is Toast (Tavares)

Can market forces prevail in the Eurozone? With another round of central bank intervention coming four plus years after the start of the Eurozone debt crisis, this is a question worth considering, at a time when the Southern Eurozone members – Italy, Spain, Greece and Portugal, which collectively account for over 30% of the GDP of the early adopters of the Euro as a whole – continue to struggle. This is a complex topic for sure, but a simple economic indicator can be used to help frame the situation. The Real Effective Exchange Rate, or “REER”, is a weighted average of a country’s currency relative to an index or basket of other major currencies adjusted for the effects of inflation. A country with higher inflation will seek to devalue its currency to maintain competitiveness in relation to its trading partners (the reverse also applies of course, but these days nobody seems to want a strong currency). The REER therefore provides a gauge of that country’s competitiveness in foreign markets.

Under a fixed foreign exchange regime, policy options are much more limited. A Eurozone member can become much less competitive relative to another member with a lower inflation rate. Stated differently, its REER will increase in that situation. This dynamic provides an insight as to how the Southern European countries got into trouble in the first place, and some of the challenges associated with its resolution. The oil shocks of the 1970s had very damaging effects in the southern contingent of the Eurozone, with inflation rates skyrocketing. Devaluations were therefore a necessity to regain competitiveness, although these also provided an inflationary feedback loop. In contrast Germany, and to a lesser degree France, more or less kept inflation under control during this turbulent period.

Figure 1: Historical CPI Inflation in Selected Eurozone Countries, 1965-2001 Source: https://www.inflation.euIt is important to understand this context, as these economies evolved out of a system that systematically used currency devaluation as a policy tool for many years. In the 1980s, Portugal, Greece and Spain formally joined the European Community, having just transitioned to a democratic system in the prior decade. A program to promote economic convergence with the European “core” was then implemented. This included the establishment of trading bands with other European currencies in order to avoid wild swings and competitive devaluations between trading partners, as well as facilitate greater economic integration going forward.

• The Ingredients of a Market Crash (John Hussman)

My sense is that a great many speculators are simultaneously imagining some clear exit signal, or the ability to act on some “tight stop” now that the primary psychological driver of speculation – Federal Reserve expansion of quantitative easing – is coming to a close. Recall 1929, 1937, 1973, 1987, 2001, and 2008. History teaches that the market doesn’t offer executable opportunities for an entire speculative crowd to exit with paper profits intact. Hence what we call the Exit Rule for Bubbles: you only get out if you panic before everyone else does.

Meanwhile, with European Central Bank assets no greater than they were in 2008, and more fiscally stable European countries quite unwilling to finance the deficits of unstable ones, the ECB has far more barriers to sustained large-scale action than Draghi’s words reveal. Moreover, to the extent that the ECB intends to buy asset-backed securities (ABS), which have a relatively small market in Europe, the primary effect (much like the mortgage bubble in the U.S.) will be to encourage the creation of very complex, financially engineered, and ultimately really junky ABS securities that can be foisted on the public balance sheet. Watch. In any event, even if such monetary interventions continue indefinitely, I have no doubt that we’ll have the opportunity to respond more constructively at points where we don’t observe upward pressure on risk-premiums and extensive deterioration in market internals.

I should be clear that market peaks often go through several months of top formation, so the near-term remains uncertain. Still, it has become urgent for investors to carefully examine all risk exposures. When extreme valuations on historically reliable measures, lopsided bullishness, and compressed risk premiums are joined by deteriorating market internals, widening credit spreads, and a breakdown in trend uniformity, it’s advisable to make certain that the long position you have is the long position you want over the remainder of the market cycle. As conditions stand, we currently observe the ingredients of a market crash.

• Billions Fly Out The Door At Pimco (WSJ)

Pacific Investment Management Co. suffered roughly $10 billion of withdrawals following the Friday departure of co-founder Bill Gross, a person familiar with the matter said, a sign of how quickly Mr. Gross’s surprise move is reshaping the bond-investing landscape. Pimco is bracing for more outflows on the heels of the veteran investor’s departure after months of internal strife over his leadership. At the same time, some managers say they remain committed to the firm. Some within the Newport Beach, Calif., investment firm are projecting it will lose at least $100 billion or more in assets due to withdrawals, the person familiar with the matter said, and some analysts peg the estimate higher. Pimco Chief Executive Douglas Hodge said in a statement his firm “manages nearly $2 trillion in assets, and we are confident that the vast majority of our clients will continue to stand with us.”

Pimco executives are confident the firm can thrive, according to interviews with executives and people familiar with the matter, partly because the firm has had good performance in many of its funds and now has more money to retain its stars and lure new talent. The flight of $100 billion, more assets than many mutual funds hold, could roil some parts of the bond market with limited trading activity, experts say, as Pimco sells assets to meet investor redemptions and other managers put new money to work. Rivals are trying to position themselves to attract some of the Pimco outflows. “There is a good chance that Pimco will lose its dominant position as a fixed-income manager as assets find their way into other investment managers, thereby leveling the playing field in fixed income,’’ said Gary Pollack, who helps oversee $12 billion as head of fixed-income trading in New York at Deutsche Bank’s private wealth-management unit.

• Yellen Aims to Mimic Greenspan on Jobs, Avoid Misfire on Bubbles (Bloomberg)

Janet Yellen looks to be taking one page out of Alan Greenspan’s playbook while tearing up another as she plots monetary strategy for 2015 and beyond. The Federal Reserve chair and her colleagues signaled this month they would be willing to push unemployment below its so-called natural rate — a feat Greenspan as chairman managed in the late 1990s without fanning much inflation. Yellen showed less desire to pursue her predecessor’s “measured” approach to raising interest rates in the mid-2000s, suggesting his strategy may have fostered complacency that made a small contribution to the financial crisis. The late 1990s “was a very good period for the U.S. economy, and Greenspan made the correct call on monetary policy,” said Michael Gapen, a former Fed official who is now senior U.S. economist for Barclays Capital Inc. in New York. On the other hand, “there is a general consensus the way they did policy wasn’t right” in the run-up to the housing bust that preceded the 2007-2009 recession.

Yellen stressed to reporters on Sept. 17 that the Fed’s actions would depend on how the economy evolves. “There is no mechanical” approach to carrying out policy, she said, adding that “many people” think the Fed relied too much on a lock-step strategy in the mid-2000s. James Bullard, St. Louis Fed president, is among those who argue that approach led to complacency about the Fed’s intentions and too much risk-taking by investors and home buyers. “The 2004 to 2006 tightening cycle was way too mechanical,” he said Sept. 23. “There was so much predictability there that I think it did foster asset-price bubbles.” Yellen’s strategy has its risks. A persistently easy monetary policy designed to push unemployment down could unleash unexpectedly strong wage and price pressures, leading to what former Fed Governor Laurence Meyer called the “nightmare” scenario of rising inflation expectations. It could also lead to distortions in financial markets — even without adoption of Greenspan’s lock-step rate increases — a danger some Fed officials warned about in a paper this month.

• Interest On Debt Grows Without Rain (Steen Jakobsen)

[‘Interest on debt grows without rain’ – Yiddish proverb] This proverb explains most of what goes on in policy circles these days. We are now watching Extend-and-Pretend, Episode VI: Promises for improvement amid ever growing debt levels. In brief, we’re still working with the same dog-eared script we were introduced to all of five years ago, when markets had stabilised in the wake of the financial crisis: maintain sufficiently low interest rates to service the debt burden. In other words, pretend to have a credible plan, but never address the structural problems and simply buy more time. But while we were able to get away with this theme for an awfully long time, the dynamic is now changing as the risk of low inflation (and even deflation) is a brick wall for the extend-and-pretend meme. Yes, interest does grow without rain, and the cost of maintaining and servicing debt grows especially fast in a deflationary regime. Mads Koefoed, Saxo Bank’s macro economist, projects US growth at around 2.0% for all of 2014.

That will be the sixth year with US growth near 2.0%, so despite lower unemployment and a record high S&P500, the economy has a hard time escaping that 2.0% level. Any talk of higher interest rates is hard to take seriously when US growth is going nowhere and world growth is considerable weaker than was expected back in January (or as recently as July, for that matter). It seems everyone has forgotten that even the US is a part of the global economy. The fourth quarter is always the most politically interesting time of year. Countries need to get their new budgets in order. The EU, IMF and World Bank will need to pretend they agree or accept the weaker data, which has to mean bigger deficits. It’s a tiresome exercise to watch denial-in-action as EU governments and other policymakers try to make something so obviously unpalatable go down easy in their internal reporting.

• Hong Kong Protesters Defy Tear Gas, Batons To Renew Democracy Call (Reuters)

Hong Kong democracy protesters defied volleys of tear gas and police baton-charges to stand firm in the center of the global financial hub on Monday, one of the biggest political challenges for Beijing since the Tiananmen Square crackdown 25 years ago. The unrest, the worst in Hong Kong since China resumed its rule over the former British colony in 1997, sent white clouds of gas wafting among the world’s most valuable office towers and shopping malls as the city prepared to open for business. Televised scenes of the chaos also made a deep impression on viewers outside Hong Kong, especially in Taiwan, which has full democracy but is considered by China as a renegade province which must one day be reunited with the Communist-run mainland.

The protests, led mostly by young tech-savvy students who have grown up with freedoms not enjoyed in mainland China, represent one of the biggest threats confronted by Beijing’s Communist Party leadership since it launched a bloody crackdown on pro-democracy student protests in Tiananmen Square in 1989. “Taiwan people are watching this closely,” Taiwanese President Ma Ying-jeou said in an interview with Al Jazeera. China rules Hong Kong under a “one country, two systems” formula which accords the territory limited democracy. The protesters are demanding Beijing give them full democracy, with the freedom to nominate election candidates, but China recently announced that it would not go that far.

Organizers said as many as 80,000 people thronged the streets over the weekend, after the protests flared on Friday night. No independent estimate of crowd numbers was available. Banks in Hong Kong, including HSBC, Citigroup, Bank of China, Standard Chartered and DBS, temporarily shut some branches and advised staff to work from home or go to secondary branches. The Hong Kong Monetary Authority (HKMA), the city’s de facto central bank, said it had activated business continuity plans, as had 17 banks affected by the protests. The HKMA said the city’s interbank markets and Currency Board mechanism, which maintains the exchange rate, would function normally on Monday. It said it stood ready to “inject liquidity into the banking system as and when necessary”.

• “How The Media Controls Britain” (Zero Hedge)

We have yet to read Owen Jones’ “The Establishment… And how they get away with it”, although Russell Brand’s take of the author has certainly piqued our interest: ”Owen Jones may have the face of a baby and the voice of George Formby but he is our generation’s Orwell and we must cherish him.” We do know, however, that the young author and Guardian columnist is one of those who are not afraid to think critically while accepting there is far more than meets the eye, and certainly than the controlled media would like revealed. To wit, from the book’s official blurb:

Behind our democracy lurks a powerful but unaccountable network of people who wield massive power and reap huge profits in the process. In exposing this shadowy and complex system that dominates our lives, Owen Jones sets out on a journey into the heart of our Establishment, from the lobbies of Westminster to the newsrooms, boardrooms and trading rooms of Fleet Street and the City. Exposing the revolving doors that link these worlds, and the vested interests that bind them together, Jones shows how, in claiming to work on our behalf, the people at the top are doing precisely the opposite. In fact, they represent the biggest threat to our democracy today – and it is time they were challenged.

• China’s One-Two Punch Could Hit Economic Growth (MarketWatch)

The strength of China’s long-term economic growth depends on whether it can accomplish two feats at the same time: purging corrupt officials while taking sweeping steps to restructure the economy.The risk? That the purge blunts the overhaul and the economy falters over time.A downturn in China would be a blow to the global economy, which counts on the Asian giant to suck in imports and provide opportunities for investment. That’s why the U.S., Europe and others in Asia are watching events in China so closely.China’s anticorruption drive began in late 2012 as a way to cleanse the ruling Communist Party and convince ordinary Chinese that the system isn’t rigged against them.

Investigators are targeting some of China’s most powerful officials and disciplining tens of thousands of lower-echelon officials who party investigators contend got used to padding their salaries. The worry now is that the headline-grabbing campaign could disrupt plans, launched the same year, to open the financial sector, reduce the role of bureaucrats, give rural residents more rights and limit the power of big state-owned firms, among other changes. A slowing of the economic overhaul would weaken growth prospects over the next decade, rather than strengthening them as Communist Party chief Xi Jinping intends.

One big problem: Mr. Xi must rely on bureaucrats across the country to enact the economic shifts, many of whom are being targeted in the corruption probe and fear what’s coming next.”Since publicly opposing reform is risky, officials will choose to drag their feet,” says Minxin Pei, a China specialist at Claremont McKenna College in California. He likens it to pilots following air-traffic rules to the letter and slowing the system to a crawl.Chinese officials describe the anticorruption push and economic overhaul as a one-two punch. First, frighten execs at state-owned firms and the bureaucrats who protect them. Then sock them with economic changes to clip their power. They will be too frightened to resist.

• Yuan-Euro Direct Trading Begins Tomorrow as China Promotes Usage (Bloomberg)

China will start direct trading between yuan and the euro tomorrow as the world’s second-largest economy seeks to spur global use of its currency. The move will lower transaction costs and boost use of yuan and the euro in bilateral trade and investment, the People’s Bank of China said today in a statement on its website. HSBC said separately it has received regulatory approval to be one of the first market makers when trading begins in China’s domestic market. The euro will become the 6th major currency to be exchangeable directly for yuan in Shanghai, joining the U.S., Australian and New Zealand dollars, the British pound and the Japanese yen. The European Central Bank is able to draw on a maximum 350 billion yuan ($57 billion) swap line from the PBOC under the terms of an agreement signed in October 2013. “It’s a fresh step forward in China’s yuan internationalization,” said Liu Dongliang, an analyst with China Merchants Bank. “However, the real impact on foreign exchange rates and companies may be limited as onshore trading volumes between yuan and non-dollars are still too small to gain real pricing power.”

• Russia Foreign Minister Calls For ‘Reset 2.0’ Of Relations With US (Guardian)

Russia’s foreign minister, Sergei Lavrov, has called for a “reset” with the United States, following statements by western leaders that their sanctions could be lifted if Russia works toward peace in Ukraine. In an interview with Russian Channel Five, Lavrov accused the west of setting off the Ukraine conflict in the pursuit of its own interests but also said Russia wanted to improve relations with the US. Western countries have imposed sanctions against Russia’s financial, oil and defence sectors over Moscow’s reported support for pro-Russian rebels in eastern Ukraine. Russia responded in August by banning food imports from Europe and North America. “The main problem is that we’re absolutely interested in normalising these relations, but it wasn’t us who ruined them. And now we need what the Americans will probably call a ‘reset,’” Lavrov said. “Something else will probably be thought up, ‘reset number two’ or ‘reset 2.0.’”

Lavrov was referring to President Barack Obama’s initiative in 2009 to improve ties between the former cold war enemies, which started off on the wrong foot when then secretary of state Hillary Clinton presented Lavrov with a badge labeled “reset” that was misspelled in Russian to read “overload”. Any progress on improving relations was soon again set back by the US Magnitsky Act banning Russian officials implicated in the death of the whistleblower Sergei Magnitsky and Moscow’s retaliatory ban on adoptions by American families. Lavrov’s comments come amid talk that the western sanctions against Russia over the Ukraine crisis could be softened or even lifted. Obama said last week US sanctions could be lifted if Russia “changes course” and stops its “aggression” in Ukraine, where it has been accused of providing men and weapons to rebels in the eastern part of the country.

• The Secret Weapon Of The Sheikhs To Open Oilfields To The World (Telegraph)

In response to Iran’s strategic grip over oil passing through the Strait of Hormuz, a new export route for crude from the Persian Gulf is growing on the coast of the Arabian Sea, with the potential to transform global energy markets. Giant tankers now queue in lines stretching for miles to load oil or refuel at Fujairah – a sleepy sheikhdom in the United Arab Emirates (UAE) – after the government invested billions of dollars into building a giant oil pipeline across the rugged Hajar mountains, with the aim of ending the potential stranglehold that Iran could place on the nation’s exports of crude. The 21-mile-wide Hormuz channel handles a third of the world’s oil-tanker traffic and connects the Persian Gulf’s sheikhdoms to the Arabian Sea. Fears that Tehran could choke off exports shipped through it have been a concern weighing on oil markets for decades. In 2008, worries that Iran would blockade the strait helped to send oil prices skyrocketing to a record $147 per barrel, a level not achieved since.

But the opening of a 240-mile long, 48in-wide export pipeline two years ago, linking the UAE’s biggest oil fields with the Arabian Sea has alleviated these concerns and could now transform Fujairah from a quiet port used by ships to refuel into a global energy trans-shipment hub. “Fujairah is the only emirate that has significant access to the ocean, and it has been on our eye to utilise this strategic position and location as an export route,” Suhail Al-Mazrouei, minister of energy for the UAE told The Daily Telegraph, on the sidelines of an energy forum hosted by The Gulf Intelligence. “The infrastructure that Fujairah now has today and will have in the future makes it a major city and a major destination for the energy sector.” The logic of shifting more export capacity outside the Gulf is also catching on with other exporters in the region. Oman is planning to build a new multi-billion-dollar oil export hub at Ras Markaz, about 450 miles south of the UAE.

Although the sultanate already loads and stores its own crude from outside the Gulf, the Ras Markaz will provide it with enough capacity potentially to export oil from other countries in the region. In addition, the government of the UAE plans to invest billions of dollars to build the largest facilities to import liquefied natural gas (LNG) in the entire Middle East at Fujairah to help meet surging domestic demand for electricity and desalinated water. According to Mr Al-Mazrouie, Fujairah is the most strategically secure location in the emirates to build the new facilities. “We are going to import LNG and the UK is already importing LNG so that makes the people of the UAE and the UK concerned about the security of the same commodity. “It is the same when you are talking about the utilisation of energy as a whole. I think energy, whether in the UK or Germany or here, is everyone’s concern.

Home › Forums › Debt Rattle Sep 29 2014: A Rare Sane European