DPC “Ice fountain on Washington Boulevard, Detroit” 1906

More debt than savings.

• 1 In 3 Americans On Verge Of Financial Ruin (MarketWatch)

The rich keep getting richer. The rest of us aren’t so lucky. According to a survey released Monday by Bankrate.com of more than 1,000 adults, 37% of Americans have credit card debt that equals or exceeds their emergency savings. “These numbers mean that three out of every eight Americans are teetering on the edge of financial disaster” — thanks to the fact that many of these folks might be hard-pressed to pay for an emergency should one arise, says Greg McBride, Bankrate.com’s chief financial analyst. “Not only do most of them not have enough savings, they’ve all used up some portion of their available credit — they are running out of options.” That’s particularly problematic considering that emergencies happen more often than you might think.

A 2014 survey by American Express found that half of all Americans had experienced an unforeseen expense in the past year — some of which could be considered an emergency. Indeed, 44% of those who had an unforeseen expense(s) had one for health care and 46% for car trouble — two items that for many Americans are must-pay items, as you need a car to get to work and your health expenses are usually not optional. Some groups — for example, the 30 to 49 age group — are in worse off than others when it comes to credit card debt and savings. This group is in particularly rough shape, likely it faces child-related and mortgage expenses. For consumers, the ideal situation is to have no credit card debt and at least six months of savings in an emergency fund (more if you have dependents), experts say. But the reality is that most of us don’t have even close to that (just 58% of Americans have more emergency savings than credit card debt, the Bankrate survey revealed).

The good news: If you have no emergency savings, or more debt than savings, experts say you can remedy that situation. Some recommend paying off your credit card debt first (focus on paying as much as you can on the highest-interest-rate debt and the minimums on all others) and then building up savings, but others say you should try to do both at once. “When you have high interest credit card debt, I recommend saving just enough to cover short-term emergencies (your washer or dryer breaks, your car needs new brakes) — that might be one or two thousand dollars,” says Doug Bellfy at Synergy Financial Planning. “Then attack the credit cards and only then go back and complete building your emergency fund.”

Wan McCormick at Reliable Alliance Financial agrees with the split strategy: “Based purely on the numbers, one might recommend to focus on the high-interest rate credit debt since it costs more money out of pocket…however, oftentimes, unexpected events happen, and without an emergency fund, consumers with high-interest rate debts usually resort back to loans and most frequently, the credit card, since it is the easiest form of accessing money,” he says. To do both at once, McBride recommends setting up a direct deposit with part going into savings and part toward your credit card.

What makes ECB QE likely to fail.

• BofA Leads Charge Into Bonds as Banks Hoard $2 Trillion (Bloomberg)

What do America’s banks know about the state of the U.S. economy that has them hording ultra-safe bonds? Growth is on a tear, hiring is the strongest in decades and households are the most upbeat since 2011. Yet banks such as Bank of America Corp. keep plowing their burgeoning deposits into U.S. government and related debt – pushing the industry’s holdings past $2 trillion – instead of lending it all out. Part of the buildup has to do with rules that require banks to hold more high-quality assets in the wake of the worst financial crisis since the Great Depression. But it also reflects that borrowers, particularly among Americans scarred by the housing bust, are still repairing their finances rather than going into debt to splurge on big-ticket items. And that, may mean the U.S. recovery isn’t quite as robust as all the upbeat data would suggest.

“Banks have so much cash,” said Peter Tchir, the New York-based head of macro strategy at Brean Capital. “Lending has loosened, but it is still just simpler for banks to own Treasuries.” While the buying may help to contain any jump in Treasury yields as the Federal Reserve moves toward raising interest rates, what it says about loan demand also has implications for how soon benchmark borrowing costs will rise this year. Minutes from the Fed’s January meeting released last week said than many policy makers were in favor of keeping rates lower for longer to avoid jeopardizing the recovery. Yields on five-year U.S. notes, which dropped as low as 1.15% last month, have since climbed as job and wage gains boosted the outlook for U.S. growth. They ended at 1.59% last week.

Investing in government bonds is proving to be a profitable move for banks. They’re making over a 100 basis-point spread by purchasing five-year Treasuries as opposed to leaving idle cash parked at the Fed where they earn only 25 basis points. U.S. commercial banks held $2.83 trillion in cash as of Feb. 11, up from $2.57 trillion at the end of last year. Having cash invested in five-year Treasuries is also netting banks an attractive spread over what they are paying depositors. The gap between the spread of the government yield over the average deposit rate for the four largest U.S. banks is above its norm over the past decade. For Bank of America that gap is about 1.44 %age points, according to data compiled by Bloomberg.

Interesting, but…

• Can A Bitcoin-Style Virtual Currency Solve The Greek Financial Crisis? (Guardian)

There’s almost no upside to a eurocrisis. You become part of a rolling maul of politicians, journalists and economists ripping and gouging at each other, both in private and on Twitter. The only advantage of being there is that it forces you to think laterally about money. Soon – if the Greek crisis is not resolved – one of the most audacious pieces of lateral thinking ever could get a try-out: a parallel digital currency, issued by the Greek government, modelled on Bitcoin, but with a crucial difference. In orthodox economics, money barely figures. It’s just there, acting as a lubricant to supply and demand. The assumption is: markets create money, and the state’s role is to make sure it’s not fake or diluted.

Bitcoin is an audacious attempt to create money beyond the control of any state. It is a digital currency, in the form of a limited number of tokens. It is championed by people who would, if they could, return to a gold standard – where states are obliged to limit the amount of money in the economy. What these money fundamentalists worry about is states creating so much money that booms and busts become inevitable and inflation erodes wealth. In this sense, Bitcoin’s aim is to function as “digital gold”. If things go badly for Greece, finance minister Yanis Varoufakis has said he would consider creating a parallel digital currency, using Bitcoin’s digital security and transparency, but doing the exact opposite of what the money fundamentalists intend.

Let’s recap the problem. The Greek debt is unpayable; the austerity required to pay it down is socially unbearable. So whether it’s this week or in six months’ time, there will come a point when Athens cannot meet conditions acceptable to the European Central Bank. Then, the normal sequence would be: bank closures, capital controls, an angry standoff and ultimately a Greek default. If you insert a parallel currency into this sequence, you can delay the moment of default and gain a lot of leeway. Varoufakis outlined, in a detailed blog post 12 months ago, how a Bitcoin-like virtual currency could be used to get around the ECB’s refusal to boost demand through quantitative easing. Just like Bitcoin, it would be exchangeable one for one with euros.

But it would be issued by the state – and if you were prepared to hold it for two years, you would earn a profit paid for by taxes. For this reason, Varoufakis called it “future-tax coin”. If the Greek government issued a parallel digital currency, and forced banks and businesses to use it, this would boost the money supply in defiance of the policy of the European Central Bank, said Varoufakis. In addition, he predicted, the currency would provide “a source of liquidity for the governments that is outside the bond markets, which does not involve the banks and which lies outside any of the restrictions imposed by Brussels or the various troikas”.

“There can be no compromise… between a slave and a conqueror, the only solution is freedom..”

• Greece Debt Deal: Reforms Will ‘Combat Tax Evasion’ (BBC)

Greece will crack down on tax evasion and streamline its civil service in its bid to secure a bailout extension, minister of state Nikos Pappas says. The government is working on a package of reforms that it must submit to international creditors on Monday. If the reforms are approved, Greece will be granted a vital four-month extension on its debt repayments. Mr Pappas said the reforms being proposed would take the Greek economy “out of sedation”. “We are compiling a list of measures to make the Greek civil service more effective and to combat tax evasion,” he told Greece’s Mega Channel. He added that talks this week would be “a daily battle… every centimetre of ground must be won with effort”. The agreement reached on Friday with European finance ministers extends Greece’s financial rescue programme by four months – but creditors gave Athens till Monday to come up with a list of reforms.

The reforms must then be approved before eurozone members ratify a bailout extension on Tuesday. Many analysts have described Friday’s agreement as a climb-down and one prominent Syriza euro-MP has expressed his frustration. In a blog Manolis Glezos, a 92-year-old wartime resistance hero, said: “I apologise to the Greek people because I took part in this illusion.” “There can be no compromise… between a slave and a conqueror, the only solution is freedom,” Mr Glezos said. On Saturday Greek Prime Minister Alexis Tspiras said in a televised address that his government had “won a battle, not the war”. If the reforms are approved and the deal stands, the immediate risk of Greece running out of money would be removed, giving the country time to negotiate further to change the terms of the bailout.

Can they get to it?

• Greece Draws Up €7.3 Billion Tax Hit List Aimed At Oligarchs And Criminals (AFP)

Greece has drawn up a €7.3bn tax hit list aimed at the country’s oligarchs and lucrative smuggling industry, a German newspaper said, as part of reform proposals due to its creditors. European finance ministers on Friday gave Athens just over three days to draw up a list acceptable to its international creditors in exchange for a four-month extension of its debt bailout. The German tabloid Bild reported that the Greek government hopes to garner €2.5bn in tax receipts from the fortunes of powerful Greek tycoons, citing sources close to the hard-left Syriza government. A similar amount would be drawn from back taxes owed to the state by individuals and businesses, Bild said. The report said an additional crackdown on illegal smuggling of petrol and cigarettes would yield another €2.3bn for the government coffers.

Greece’s government is walking a tightrope between its commitments to European creditors and its electoral pledges to end austerity in a country struggling to recover from severe economic crisis. Two previous rounds of talks ended in acrimony with Greece accusing Germany and other hardline EU member states of sabotaging a deal. To win Friday’s hard-fought deal, Athens pledged to refrain from one-sided measures that could compromise its fiscal targets and had to abandon plans to use some €11bn in leftover European bank support funds to help restart the Greek economy. “Europe has some breathing space, nothing more, and certainly not a resolution. Now it’s up to Athens,” German foreign minister Frank-Walter Steinmeier told Bild. “The fundamentals – namely assistance in exchange for reform – must remain the same.”

How much resistance will there be from the rich?

• Greece Scrambles To Finalise Fiscal Reform List (Guardian)

Greek government officials are racing to complete a list of reform proposals that will be scrutinised by the country’s international creditors this week as Athens seeks an extension to its €240bn (£177bn) bailout.Finance ministry experts have spent the weekend finalising the fiscal and structural measures that Athens’ left-led government will submit under the terms of an agreement reached at a eurozone summit last Friday. Yanis Varoufakis, the Greek finance minister, sent draft proposals to creditors at the EU, the ECB and the IMF on Sunday, in order to receive feedback before making a formal submission by Monday’s deadline. If the reforms are accepted, Friday’s tentative agreement for a vital four-month loan extension will go ahead.

“We are compiling a list of proposals to make the Greek civil service more effective and to combat tax evasion,” the minister of state, Nikos Pappas, told Mega TV on Sunday. Claiming Greece was “at the start of a new phase” as it prepares for a four-month reprieve that will allow it to devise its own economic agenda, the politician said the inventory would include labour law reforms and changes to legislation regarding non-performing loans. Both are seen as especially sensitive for a nation worn down by five years of gruelling austerity – the price of its rescue funds. Alexis Tsipras’s government, catapulted into power a month ago, is playing a delicate balancing act between placating the bodies keeping Greece afloat and sticking to the anti-austerity policies on which it was elected.

In Friday’s outline agreement, the administration won time, “ownership” of its reform programme, and a sizeable reduction in the scale of its primary surplus – the difference between state expenditure and income once interest payments are stripped out. It was also forced, however, to give considerable ground in agreeing to an accord that staved off the prospect of a financial collapse, with the Greek banking system relying on ECB support. Concessions included seeking an extension to the bailout and agreeing to further oversight from the EU, ECB and IMF. Capital flight on the day the deal was announced had reached €1bn as worried depositors rushed to withdraw funds from accounts.

Highlighting the difficulties the government would almost certainly face, the German finance minister, Wolfgang Schäuble, conceded on Friday that Athens would have “a hard time explaining the deal to Greek voters”. On Sunday, that premonition appeared to come true. There were signs of dissent within Tsipras’s radical left Syriza party over the concessions made in Brussels. Piling on the pressure, the veteran leftist, second world war hero and Euro MP, Manolis Glezos, not only lambasted the deal but called on Greeks to rise up against it. “I apologise to the Greek people that I cooperated in this illusion,” the 92-year-old wrote on his blog. “Some claim that as part of a deal you have to back down. First of all, there can be no compromise between the oppressor and oppressed, just as there cannot between the slave and the tyrant, the only solution is freedom.”

Good question.

• Who Made Germany Europe’s Boss? (Bloomberg)

There are two main lines of analysis about Germany’s role in the European Union. The first, favored by populist euro-skeptic politicians, is that Germany seeks to reverse the setbacks of the 20th century and rule Europe by other means. The second, popular with political commentators and other members of the European elite, is that German guilt over the setbacks of the 20th century inhibits it from exercising the leadership that the EU actually needs. If the past several weeks are any guide, reports of German inhibitions have been exaggerated. We’ll see whether Friday’s tentative agreement over Greece sticks. Tomorrow, Athens is to present a list of measures to the so-called troika, with which Greece’s new government vowed not to deal. If the supervisors sign off, the plan must go to various national parliaments for approval, including Germany’s.

This thing isn’t over yet. Whatever the outcome, Germany’s role in the stand-off has been striking. The struggle between Greece and the euro-zone finance ministers has been reported as though it were a battle between Greece and Germany, with the rest looking on. This was an impression that German officials went out of their way to reinforce. Last Thursday, as another in an extended series of final deadlines loomed, Greece presented an amended proposal for discussion. Euro-zone officials were guardedly optimistic, saying its letter could be a basis for negotiation; the Dutch chairman of the so-called euro group of finance ministers, Jeroen Dijsselbloem, called another meeting to discuss it. Meanwhile a German government spokesman dismissed the document out of hand: “The letter from Athens is not a substantive proposal for a solution,” he ruled; German officials called the letter a “Trojan horse.”

German Finance Minister Wolfgang Schaeuble continued to declare that Greece already had an assistance program, so there was nothing to discuss. He dared Greece to defy the troika and suffer the consequences. The Financial Times reported: Mr Schaeuble declines to publicly discuss Grexit, he has repeatedly said that Greece can choose to leave the €172bn financing programme – with all that implies. “I’m ready for any kind of help, but if my help is not wanted, that’s fine,” he said recently. By the way, I think when he said “my help,” he was talking about the euro group’s help. It began to seem plausible – which came as a surprise to me, I admit – that the German government actually wanted the euro system to split. Some German officials, again according to Financial Times, have been advocating that very course. Hawkish German officials accept what they call “the amputated leg theory,” which says Greece should be cut off like a gangrenous limb to spare the rest of the eurozone body.

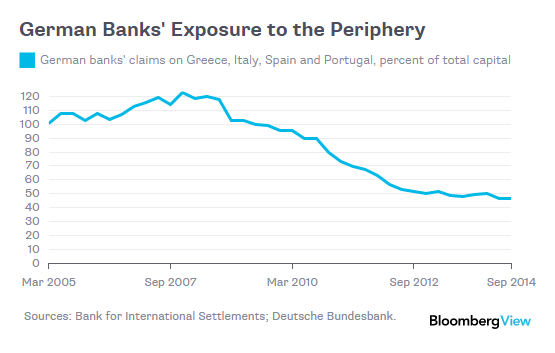

How German banks were saved.

• Why Germany Might Not Be Bluffing in Greece (Bloomberg)

As Europe’s high-stakes debt negotiations with Greece reach an impasse, Germany has appeared surprisingly willing to drive the country out of the euro, regardless of the potentially dire repercussions for Italy, Portugal, Spain and the entire currency union. One possible explanation for Germany’s brinkmanship: Its banks have a lot less to lose than they once did. When the European debt crisis first flared up in 2010, Germany’s finances were closely linked to those of the euro area’s more economically fragile members. Its banks’ claims on Greece, Italy, Portugal and Spain – including money lent to governments and companies – amounted to more than €350 billion, about equal to all the capital in the German banking system. If the periphery countries had forced losses on private creditors, which they arguably should have done, Germany would have had to recapitalize its banks or face an immediate meltdown.

The picture is very different now. The ECB, the IMF and other taxpayer-backed creditors have pumped hundreds of billions of euros of loans into the periphery countries, making it possible for German banks to extract themselves with minimal damage. Thanks in part to this back-door rescue, the banks have also been able to raise some capital. As a result, they are in much better shape to withstand a Greek disaster. As of September 2014, their claims on Greece, Italy, Portugal and Spain had declined to about €216 billion, or 46% of capital. The upshot: Greece is left with more debt than it can pay, and Germany – with its banks effectively bailed out – has one less pressing reason to give Greece a break. Hardly the right incentives for a happy ending.

“The last thing Greece needs right now is another public turn of the screw.”

• The Greek Debt Deal: Victory Or Defeat? (Guardian ed.)

ALexis Tsipras campaigned for office on the promise that he could both end Greece’s subservience to the humiliating fiscal and political conditions that the European Union had imposed on the country and keep Greece in the eurozone. Greeks wanted an end to austerity, and they wanted to retain the euro, seemingly contradictory desires. But they could have both, the Syriza leader implied, if they voted for a bold government ready to go to Brussels and take the game to the edge. A Greek exit from the euro would be such a huge disaster that the EU would, if pushed hard, be ready to give in. The Greeks went to Brussels and pushed, but in the end it was they who gave in.

They got a few concessions, particularly on the primary surplus they are required to run, and some cosmetic changes in what things are called, the old vocabulary having become untouchable. But the same reality lies beneath. Greece still has to put together a schedule of reforms, to be presented on Monday and discussed over the week. On the face of it, Greek and EU objectives in this area are close: Syriza is pledged to battle tax evasion, to remodel the civil service, to streamline business regulation, and to create an accurate property register, for example. But the Germans want detail, not rhetoric. It is not beyond the realms of possibility that the EU, under pressure from Germany and other northern countries, will send any programme back for more work if it feels it lacks substance.

The EU would do well to resist that temptation, or to disguise the process in some way if it does, however. The last thing Greece needs right now is another public turn of the screw. For the moment, at least, Greeks seem to be in a mood to give Syriza credit for trying to change the terms of what is not now to be called the bailout, and getting them softened in such a way as to give the government a little more flexibility in domestic spending. Mr Tsipras claims a “victory”. Greeks know there has been no victory, but they also know that the odds were heavily against Greece, and that the effort, although perhaps foolhardy, had to be made by a government that had made the promises it had.

“One way or another they will manage to strike a compromise on the list of measures required for the extension of the program.”

• Greece’s Tsipras Is on a High Wire (Bloomberg)

Greek Prime Minister Alexis Tsipras walks another high wire over the next 24 hours as he tries to come up with financial measures that satisfy both the demands of euro-region creditors and his anti-austerity party. After talks in Brussels between officials from the 19 euro members concluded late on Feb. 20 with an agreement to extend bailout funds for four months, the government in Athens now has until the end of Monday to complete a list of policies in return for the continued funding. Finance chiefs will then decide whether the proposals go far enough or trigger another round of emergency negotiations this week. “The stakes are too high for the euro area and mostly for Greece, as the country’s economy and especially banking system may face an imminent collapse,” said Panos Tsakloglou at Athens University of Economic and Business.

“One way or another they will manage to strike a compromise on the list of measures required for the extension of the program.” The agreement potentially frees up money to meet some of the pledges made by Tsipras before disgruntled Greeks catapulted his Syriza party into power almost a month ago. The outcome may still prove politically bruising for him after he was forced to ditch plans to take back control of Greece’s beleaguered finances so he could raise wages and pensions. The new policies remain subject to validation by the IMF, the ECB and the EC, the institutions collectively known as the troika from which Tsipras vowed to break free. The 40-year-old premier began the task of selling domestically the provisional deal to extend bailout funds after securing the reprieve from the prospect of national insolvency.

“We won a battle, but not the war,” he said in a nationally televised address on Saturday. “The difficulties, the real difficulties, not only those related to the discussions and the relationship with our partners, are ahead of us.” While the government has discussed the measures with the institutions, the proposals are Greek and haven’t been put forward by creditors, Finance Minister Yanis Varoufakis said after a cabinet meeting the same day. There is no disagreement and “we are almost certain that we will get a yes from the institutions,” he said. The European Commission is currently involved in constructive talks with its Greek partners after Friday’s decisions, a spokeswoman said on Sunday.

Politics. Throw Podemos under the bus.

• Spain Said to Lead EU Push to Force Terms on Greece (Bloomberg)

As euro-region finance ministers turned the screw on Greece in Friday’s talks, the group’s usual enforcer, Wolfgang Schaeuble of Germany, was eclipsed by Spain’s Luis de Guindos, according to two people with direct knowledge of the talks. De Guindos took the toughest line with Greek Finance Minister Yanis Varoufakis as the bloc forced forced him to adhere to the terms of the country’s existing bailout to retain access to official financing, the people said, asking not to be named because the conversations were private. When the group rejected Schaeuble’s call for a Tuesday meeting to scrutinize Greece’s plans to meet those conditions, De Guindos insisted, winning agreement for a teleconference, they said.

The Spanish government is particularly sensitive to the fortunes of the Syriza government in Greece because the party’s Spanish ally, Podemos, has surged to the top of some recent polls. A victory for Varoufakis would have strengthened Podemos’s argument that De Guindos’s boss, Prime Minister Mariano Rajoy, was wrong to impose austerity on Spain. The Spanish government “has always been constructive but it has to defend its interests,” Guindos said on Friday. “A climate is developing in which the new Greek government is adapting to the rules that affect us all.” A spokeswoman for De Guindos said Spain is in favor of dialogue and flexibility within the existing rules and has shown its solidarity with Greece by contributing €26 billion euros to its bailout at a time when its own financing conditions were not good.

Struggling to fend off a sovereign default, the Greek government acceded to European demands that it respect the conditions of its existing bailout package at Friday’s meeting in Brussels. The Greek government must submit a list of economic measures it will undertake by Monday and finance chiefs will then decide whether the proposals go far enough. De Guindos, at times raising his voice, railed against Varoufakis in Friday’s meeting, telling him he has to win the trust of his euro-region counterparts and learn how politics is conducted at the European level, one of the people said. De Guindos has been in the running to replace Jeroen Dijsselbloem of the Netherlands as head of the euro-region finance ministers’ group when the Dutchman’s term expires this year.

Math.

• Why Greece Will Never Repay Its Debt (CNBC)

European officials should accept that Greece may never repay its $366 billion debt, analysts told CNBC, even if the troubled economy secures a bailout extension. Greek debt is not repayable in this life, Kingsley Jones, founder and CIO of Jevons Global, told CNBC on Monday: “We have to be realistic here. Greek debt is now 175% of gross domestic product (GDP); it’s higher than it was when this whole business first started.” “Just look at Japan. It has government debt rapidly approaching 300% of GDP. One day, that debt pile simply implodes. It is not ever going to be repaid, nor will the Greek debt. There is no use standing on the high moral ground,” Jones said.

Athens’ current bailout program with European creditors requires Greece to reduce its debt to below 110% of GDP by 2022. The program was extended for another four months in a last-minute deal on Friday, failing to meet ruling party Syriza’s request for an official haircut, or reduction, on outstanding debt – a promise that brought the leftist party to power last year. However, final confirmation of Friday’s bailout extension hinges on the list of reforms Prime Minister Alexis Tsipras submits on Monday. “The terms of the current agreement pretty much require Greece to attempt to run a primary budget surplus over 4% for well over a decade…No country with an unhealthy economy has ever managed to do that. So, we think that the current terms that are required of Greece are frankly pretty unrealistic,” Jones added.

Raise taxes?

• Rebuilding Crumbling America Shouldn’t Wait (Bloomberg)

If Washington were a rational place, a major measure to rebuild roads, bridges, ports and airports would be a slam-dunk. Few doubt the need. The U.S. has underinvested in infrastructure: It was ranked 12th in the World Economic Forum’s Global Competitiveness Report for 2014-2015. Road repair needs are pervasive, a quarter of bridges require upgrades, the fast-rail system falls further behind other countries every year. There is a broad consensus that infrastructure investment is a significant job-creator. It is embraced by the Chamber of Commerce, the AFL-CIO and many governors and mayors of both parties. Republican congressional leaders want selective big accomplishments to prove they can govern. President Barack Obama wants a few more successes in his final years. Infrastructure is one of the very few areas where they’re on roughly the same page.

Moreover, the Highway Trust Fund, which finances federal transportation projects, expires in May. Yet there is little reason to be sanguine. There likely will be a short-term fix for the highway fund. But the necessary longer-term systemic investments will be kicked down the road, a casualty of partisan gridlock. The logical approach to extending the fund would be to raise the 18.4 cents a gallon gasoline tax that is dedicated to transportation. It hasn’t been increased in more than two decades and gasoline prices today are at a five-year low. It was the patron saint of low taxes, Ronald Reagan, who lauded these kinds of “user fees.”

Yet today’s Republicans recoil at any tax increase. And Democrats fear that it would be used against them (Obama ducked it in his budget). And they worry that working and middle-class citizens would be hardest hit by the tax, though there are ways to soften that impact. The president’s budget proposed a one-time 14% tax on the almost $2 trillion in foreign earnings that U.S. companies hold overseas. Obama would use those proceeds for infrastructure. Additionally, he proposed a 19% tax on future foreign earnings as part of a reform of corporate taxes. Privately, the administration acknowledges that this is an opening bargaining position and that it would have to accept a lower rate to get Republicans on board. Last year, House Ways and Means Committee Chairman Dave Camp had a proposal with an 8.75% top rate.

Where could it possibly lead?

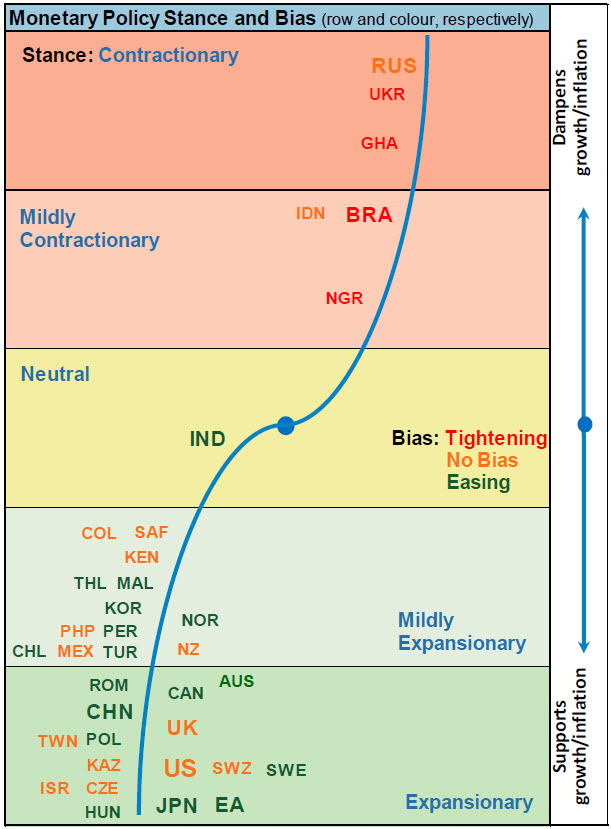

• Global Central Bank Easing Quadruples In 2015 (Zero Hedge)

Thanks to global disinflationary pressures driven by the savings glut, an oil glut, and universally high (peak) debt levels (crushing the transmission mechanisms of textbook economists), central planners have gone full ease-tard in 2015. From a ‘balanced’ 10 easing, 9 tightening bias (~1:1) in December, Morgan Stanley illustrates in the following chart there are now 16 central banks easing and only 4 with a tightening bias (4:1) as it appears the one-trick pony brigade are trying moar of what didn’t work the first, second, and last times in an effort to prove this time is different… With so many central planners piling up in the lower left corner… and global growth expectations crashing… when oh when does the world wake up to smoke and mirrors they have been witnessing and, as Marc Faber recently warned, lose faith in central bank omnipotence?

“.. the only chance for Europe to get rid of the United States protectorate and become, in the words of General de Gaulle, a ‘Free Europe’.”

• French Analyst Calls For France-Germany-Russia Alliance (TASS)

France and Germany, following the historical tradition, should work on forming an alliance with Russia, prominent French writer and political journalist Eric Zemmour said in newspaper comments on Friday. “NATO is doing its utmost to present Russia as an enemy of the West and thereby justify its existence,” Zemmour wrote in Le Figaro Magazine. “Fortunately, France and Germany in due time blocked Ukraine’s accession to NATO, and that’s a positive fact,” the journalist said. “Now when they finally coordinated their positions on establishing relations with Moscow, they should not stop halfway and should move towards forming a tripartite alliance with Russia,” he said, recalling numerous efforts in the past by “kings, emperors and presidents” of the three countries to set up such an alliance.

The analyst stressed that the tripartite bloc “will be the only chance for Europe to get rid of the United States protectorate and become, in the words of General de Gaulle, a ‘Free Europe’.” “An alliance with Russia is absolutely necessary to fight against Islamists in Syria, Libya, Iraq, Mali, Central African Republic, Nigeria, Pakistan and Afghanistan, where these extremists are trying not only to erase all the traces of a Western and Christian presence, but to pave the way for carrying the war into the European territory,” Zemmour added.

Light in darkness.

• Homeless Britons Are Turning To The Sikh Community For Food (BBC)

“We come here because we get food… A hot meal. It’s a luxury for me.” John Davidson is 55 and homeless. He is one of 250 people who have just received a hand-out of hot soup, drinks, chocolate bars and other supplies from the Sikh Welfare and Awareness Team van parked up on the Strand in central London on a cold Sunday evening. The Swat team, as they’re known, park at the same spot every week so a group of volunteers from the Sikh community can hand out vital supplies. Homeless people, who overwhelmingly are not Sikh, patiently wait in line to be served. For the volunteers handing out food here, this is more than just good charitable work. For them this is a religious duty enshrined by the founder of the Sikh religion, Guru Nanak, over 500 years ago.

At a time of deep division by caste and religious infighting between Hindus and Muslims in India, Guru Nanak called for equality for all and set forward the concept of Langar – a kitchen where donated produce, prepared into wholesome vegetarian curry by volunteers, is freely served to the community on a daily basis. Today, thousands of free Langar meals are served every day in Sikh temples throughout the UK. The Guru Singh Sabha Gurdwara in Southall, thought to be the biggest Sikh temple outside of India, says it alone serves 5,000 meals on weekdays and 10,000 meals on weekends. Every Sikh has the duty to carry out Seva, or selfless service, says Surinder Singh Purewal, a senior member of the temple management team. “It means we’re never short of donations or volunteers to help prepare the Langar.”

In recent times the Langar meal has acted as a barometer for the state of the economy. After the 2008 recession many Sikh temples reported a surge in the numbers of non-Sikhs coming in for the free Langar meals. It’s now common to see non-Sikhs inside the temple, Purewal says: “We don’t mind it. As long as people show respect, are not intoxicated and cover their heads in line with our traditions, then everyone is welcome.” The Swat team say they decided to take the concept of Langar outside its traditional setting in temples and out onto the streets when they saw a growing homelessness problem in London. Randeep Singh who founded SWAT says: “When you go to the temple, what’s the message? The message is to help others, help your neighbours. That’s what we are doing.”

Home › Forums › Debt Rattle February 23 2015