Unknown Fed Ponders Interest Rates 1917

A recovery built on ZIRP is not real.

• Fed Raises Interest Rates, Citing Ongoing US Recovery (Reuters)

The Federal Reserve hiked interest rates for the first time in nearly a decade on Wednesday, signalling faith that the U.S. economy had largely overcome the wounds of the 2007-2009 financial crisis. The U.S. central bank’s policy-setting committee raised the range of its benchmark interest rate by a quarter of a%age point to between 0.25% and 0.50%, ending a lengthy debate about whether the economy was strong enough to withstand higher borrowing costs. “With the economy performing well and expected to continue to do so, the committee judges that a modest increase in the federal funds rate is appropriate,” Fed Chair Janet Yellen said in a press conference after the rate decision was announced. “The economic recovery has clearly come a long way.”

The Fed’s policy statement noted the “considerable improvement” in the U.S. labour market, where the unemployment rate has fallen to 5%, and said policymakers are “reasonably confident” inflation will rise over the medium term to the Fed’s 2% objective. The central bank made clear the rate hike was a tentative beginning to a “gradual” tightening cycle, and that in deciding its next move it would put a premium on monitoring inflation, which remains mired below target. “The process is likely to proceed gradually,” Yellen said, a hint that further hikes will be slow in coming. She added that policymakers were hoping for a slow rise in rates but one that will keep the Fed ahead of the curve as the economic recovery continues. “To keep the economy moving along the growth path it is on … we would like to avoid a situation where we have left so much (monetary) accommodation in place for so long we have to tighten abruptly.”

The winners once again are money market mutual funds and broker-dealers. They profit whatever happens.

• Fed Removes Reverse Repo Cap to Ensure Control Over Rates (BBG)

The Federal Reserve removed the daily limit on aggregate borrowings through its overnight reverse repurchase facility, previously set at $300 billion, in a step designed to make sure the benchmark interest rate stays inside its new target range. The size of the facility will be “limited only by the value of Treasury securities held outright in the System Open Market Account that are available for such operations and by a per-counterparty limit of $30 billion per day,” the Fed said in a statement on Wednesday in Washington. The move came in conjunction with the Federal Open Market Committee’s decision to increase the target range for the federal funds rate by a quarter percentage point to 0.25% to 0.5%.

The Fed increased the interest it pays on overnight reverse repos to 0.25% from 0.05% to put a floor at the lower end of the range. It also raised the interest it pays on excess reserves held at the Fed to 0.5% from 0.25% to mark the upper end of the range. Fed reverse repos are conducted with money market mutual funds and broker-dealers and serve to drain excess liquidity from money markets. If investors offered to lend the Fed more money than the Fed was willing to borrow, the central bank wouldn’t be able to keep interest rates in its new target range. This happened in September 2014 on the final day of the quarter, driving rates below the Fed’s target range.

This is big in the background: “..by the time short term rates hit 1%, the Fed may have soaked up as much $4 trillion in liquidity.”

• Fed May Have To Drain $1 Trillion In Liquidity To Push Rates 25 bps Higher (ZH)

Two weeks ago, we cited repo-market expert E.D. Skyrm who calculated that moving general collateral higher by 25bps would require the Fed draining up to $800 billion in liquidity: “In 2013 on my website, I calculated that QE2 moved Repo rates, on average, 2.7 basis points for every $100B in QE. So, one very rough estimate moved GC 8 basis points and the other 2.7 basis points per hundred billion. In order to move GC 25 basis points higher, in a very rough estimate, the Fed needs to drain between $310B and $800B in liquidity.” That may be conservative. According to Citigroup’s latest estimate, the liquidity drain could be substantially greater. Here is the take of Jabaz Mathai

There will be a separate document from the NY Fed with details around the operational aspects of the liftoff. Of primary interest will be the size of the overnight reverse repo facility that the Fed will put in place to pull short rates higher. We don’t think it will be unlimited, but a size large enough that will keep short rates from falling below the 25bp floor – and the size could be as high as $1tn.

Putting this liquidity drain in context, the entire QE2 injected “only” $600 billion in liquidity in the span of many months, suggesting that as of tomorrow, the Fed may drain as much as 166% of its entire second quantitative easing operation overnight. Whether that liquidity is inert and can be easily released by banks, and more importantly, non-banks without resulting in any additional risk tremors is the first $640 billion question that the Fed is facing. The second, third and fourth? Assuming a linear relationship and another 3 rate hikes until the end of 2014, this means that by the time short term rates hit 1%, the Fed may have soaked up as much $4 trillion in liquidity. Here one thing is certain: a $1 trillion drain may not have a material impact when starting from a $2.6 trillion excess reserve base. $4 trillion, however, will leave a mark (the Fed’s entire balance sheet is $4.5 trillion) especially once the market starts to discount just how the rate hike plumbing takes place.

All of it true, except that it has nothing to do with the Fed.

• Fed Leaves China Only Tough Choices (BBG)

No one will blink if the Fed raises U.S. interest rates 50 basis points today, signaling an end to the cheap-money era. The U.S. central bank has telegraphed its move for months and while pockets of lingering weakness will spur some Fed watchers to challenge the decision, there’s little reason to believe such a small move will nudge the world’s biggest economy back into recession. A relatively easy decision for the Fed, however, is making life much harder for policymakers on the other side of the world. The People’s Bank of China has recently been burning through its $3.4 trillion stash of foreign-exchange reserves, spending nearly $100 billion a month to prop up the value of the yuan. Higher U.S. interest rates and a stronger dollar are sure to spur further capital outflows, especially given continued worries about the Chinese economy.

Chinese leaders seem willing to accept some mild depreciation while preparing for full liberalization of the yuan; in the future, the currency’s value may be determined against a basket of 13 currencies including the euro and yen, which would increase downward pressures. If the PBOC were to pull back now, however, the currency’s gentle glide could quickly turn into a nosedive. Given the dollar’s strength against emerging market currencies, a true free float could spark a devaluation of more than 30%. In that event, China would have few weapons at its disposal. In November, the yuan joined the IMF’s elite club of reserve currencies – a victory of great symbolic importance to Chinese leaders. If they imposed capital controls to halt the yuan’s downward slide, they’d suffer massive embarrassment, not to mention hard questions about their economic management skills.

China has little option but to continue muddling through, then, allowing the yuan to decline in value while working to moderate its pace. This certainly counts as currency “manipulation” in the eyes of Donald Trump and other presidential candidates. In this case, though, China isn’t defying the market so much as attempting to cushion market-driven dislocations. The dilemma highlights an uncomfortable truth: Unlike the Fed, whose rate hike is a classic low-risk decision, Chinese leaders today face only high-risk policy choices. And the best they can hope for in return is a degree of stability, not the go-go growth of earlier decades.

Previously, when China’s debt levels were low and the government was running large surpluses, investment opportunities were plentiful. Now credit is stretched. Fixed-asset overinvestment has left a capacity glut. Migration to cities is slowing, even as the working-age population has begun to decline. There are no more easy reforms. The changes China needs to implement – to stimulate competition, increase productivity, allocate capital more efficiently and spur innovation – all require wrenching sacrifices.

More debt is needed to achieve what the Fed wants, but paradoxically it will now get more expensive.

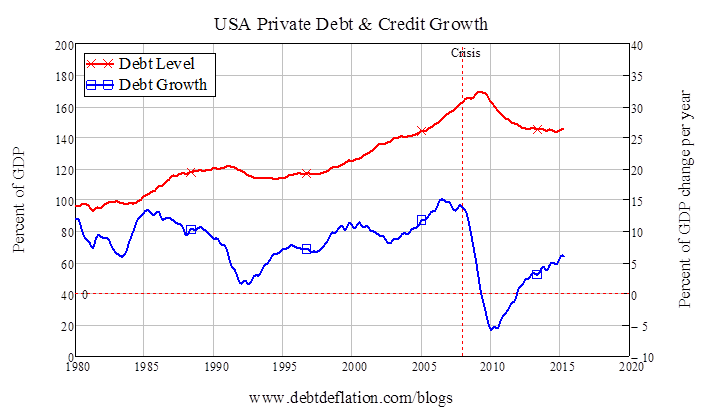

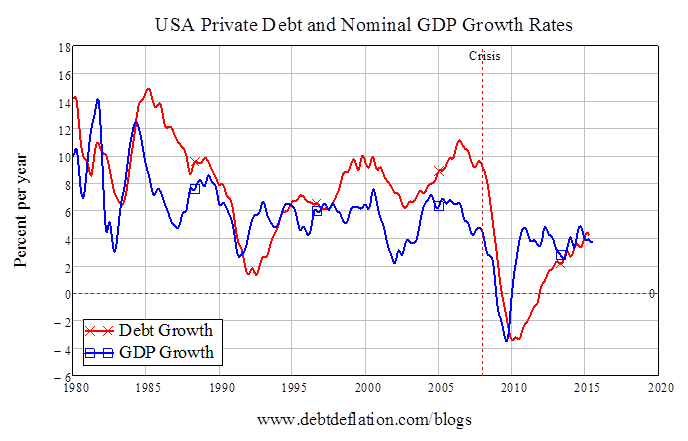

• The Fed By The Numbers – And Why They Are Wrong (Steve Keen)

2,3,4,5. Those are the 4 numbers you need to know to understand how The Fed thinks. Driven by its underlying model of the economy, The Fed thinks that the inflation rate should be 2%, the growth rate should be 3%, the Fed Funds Rate should be 4%, and the unemployment rate should be 5%. Then the economy is in what mainstream economists call “Equilibrium”, with all the key variables at their “Natural Rate”. Of course, it’s been some time since the economy has served up a set of numbers anything like that, but eight years after the economic crisis began, it’s sort of delivered on at least two of them: the unemployment rate is now spot on 5%, and the GDP growth rate is about 2.5%. Inflation remains the bugbear for The Fed (“why won’t it return to 2%?”), but today they are likely to bite the bullet and give the one variable they can control—the Federal Funds Rate—a slight nudge from its rock-bottom level of 0.25% up to 0.5%.

This is still a long way from The Fed’s 4% sweet spot, but after eight long years of near-zero, it is the first step—or so The Fed thinks—in a gradual return to “Equilibrium”. If only. The Fed will probably hike rates 2 to 4 more times—maybe even get the rate back to 1%—and then suddenly find that the economy “unexpectedly” takes a turn for the worse, and be forced to start cutting rates again. This is because there are at least two more numbers that need to be factored in to get an adequate handle on the economy: 142 and 6—the level and the rate of change of private debt. Several other numbers matter too—the current account and the government deficit for starters—but private debt is the most significant omitted variable in The Fed’s toy model of the economy.

These two numbers (shown in Figure 2) explain why the US economy is growing now, and also why it won’t keep growing for long—especially if The Fed embarks on a period of rate hiking. The economy is growing now because private credit is expanding at about 6% of GDP per year. This is a long way below the unsustainable rate of 15% per year that it hit just before the crisis began, but it’s enough to boost the economy a bit—and inflate asset markets a lot, since assets are what 90% plus of the borrowed money is actually spent on in the first instance. Unfortunately, that 6% rate of growth in GDP terms means that private debt is growing faster than nominal GDP—so the private debt to GDP ratio is rising once more (see Figure 3). And that can’t be sustained, because private debt is still very close to the levels that led to the last crisis. A growth rate at or below the growth rate of nominal GDP is sustainable. But a growth rate above that is not.

The dilemma this poses for The Fed—a dilemma about which it is blissfully unaware—is that a sustained growth rate of credit faster than GDP is needed to generate the magic numbers on which it is placing its current wager in favor of higher interest rates.

China steel output is falling too fast for even exports to keep up.

• Baltic Dry Index Plunges to Fresh Record Low Amid China Steel Slump (BBG)

The shipping industry’s most-watched measure of rates for hauling commodities plunged to a fresh record amid a persisting glut of ships and speculation weakening Chinese steel output could translate into declining imports of iron ore to make the alloy. The Baltic Dry Index fell 4.7% to 484 points, the lowest in Baltic Exchange data starting in January 1985. Rates for three of the four ship types tracked by the exchange retreated. China, which makes about half the world’s steel, is on track for the biggest drop in output for more than two decades, according to data compiled by Bloomberg Intelligence. Owners are reeling as China’s combined seaborne imports of iron ore and coal – commodities that helped fuel a manufacturing boom – record the first annual declines in at least a decade.

While demand next year may be a little better, slower-than-anticipated growth in 2015 has led to almost perpetual disappointment for rates, after analysts’ predictions at the end of 2014 for a rebound proved wrong. “It doesn’t help that Chinese steel production is about to see the most dramatic decline to the lowest in 20 years,” said Herman Hildan, a shipping-equity analyst at Clarksons Platou Securities in Oslo. “Demand growth is collapsing.” Rates for Capesize ships fell by between 13% and 15%, the Baltic Exchange’s figures showed. The ships are so-called because they can’t get through the locks of the Panama Canal and must instead sail through around South Africa or South America. Smaller Panamaxes, which can navigate the waterway, advanced 0.3% to $3,285 a day.

The two other vessel types that the Baltic Exchange monitors both declined. Owners are contending with a fleet whose capacity more than doubled over the past decade. At the end of last year, shipping analysts forecast rates for Capesize-class vessels would jump by about a third in 2015. By the start of this month, they were expecting a decline of about that magnitude.

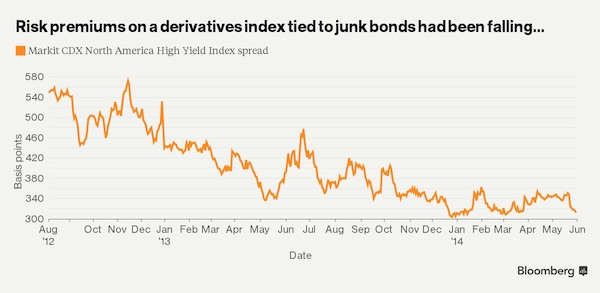

“..high-yield spreads are currently pricing in a 2008-like market selloff over the next five years.”

• This Junk Bond Derivative Index Is Saying Something Scary About Defaults (BBG)

Here is the Markit CDX North America High Yield Index.

Here is the Markit CDX North America High Yield Index on drugs defaults.

Any questions? Probably. Citigroup analysts led by Anindya Basu point out that spreads on the CDX HY, as the index is known, are currently pricing in an expected loss of 21.2%, which translates into something like 22 defaults over the next five years if one assumes zero recovery for investors. That is a pretty big number once you consider that a total of 41 CDX HY constituents have defaulted since the index really began trading in 2005, equating to about 3.72 defaults per year. A big chunk of those defaults (17) occurred in 2009 in the aftermath of the financial crisis. What to make of it all? Actual recoveries during corporate default cycles tend to be higher than the worst-case scenario of 0%. In fact, they average somewhere in the 26% range, which would imply 29 defaults over the next five years instead of 41.

So what? you might say. The CDX HY includes but one default cycle, and those types of analyses tend to underestimate the peril of tail risk scenarios (hello, subprime crisis). Citi has an answer for that, too. Using spreads from the cash bond market going back to 1991, they forecast the default rate over the next 12 months to be something more like 5% to 5.5%. (For comparison, the rating agency Moody’s is currently forecasting a 3.77% default rate.) “CDX HY spread levels are pricing in about a 21% loss over a five-year period, whereas the highest we have ever seen over a five-year period is 14.2%, and that included 2009,” Basu said in an interview. “Of course, the spread level includes a spread risk premium over and above the ‘pure default’ risk. Even from that perspective, we believe the risk being priced in is too much.” In fact, Citi says “high-yield spreads are currently pricing in a 2008-like market selloff over the next five years.”

A lot more attention needs to be paid to ‘evaporating money’. Which is really just virtual wealth disappearing.

• $100 Billion Evaporates as World’s Worst Oil Major Plunges 90% (BBG)

Colombia is nursing paper losses of more than $100 billion after its oil boom fell short of expectations, wiping out 90% of the value of what was once Latin America’s biggest company. From being the world’s fifth-most valuable oil producer at its zenith in 2012, worth more than BP, state-controlled Ecopetrol now ranks 38th. Its market capitalization has fallen to $14.5 billion, down from its peak of $136.7 billion. “They just haven’t found oil, it’s as simple as that,” Rupert Stebbings, the managing director of equity sales at Bancolombia SA, said from Medellin. “The whole oil sector got massively over-bought, and people assumed that one day they’d hit an absolute gusher.”

As the army wrested back territory from Marxist guerrillas over the last decade and a half, opening up more land for exploration, the outlook was bright for the oil sector in Colombia, which borders Venezuela, the nation with the world’s largest reserves. Ecopetrol’s share price soared to “irrational levels” as investors bet on surging output that then failed to materialize, Stebbings said. With shares in the oil producer still high, the government opted in 2013 to sell a stake in electricity producer Isagen SA rather than Ecopetrol. Finance Minister Mauricio Cardenas, who sits on the board of Ecopetrol, said in an August 2013 interview that the government didn’t want to sell a further stake in the company because its growth prospects were better than Isagen’s. Since then, Isagen shares have risen 4.2%, while Ecopetrol’s have fallen 74%.

The Isagen stake sale has yet to take place due to a series of legal challenges. Over the past year, Ecopetrol shares are down 55% in dollar terms, the worst performance among global oil drillers with a market capitalization over $10 billion. The company’s original 2015 production target of 1 million barrels of oil equivalent was changed to 760,000 barrels. Ecopetrol’s growth in oil production since 2006 is among the world’s best, with a 24% success rate in exploration in 2014, the company said. The Kronos-1 and Orca-1 discoveries in the Colombian Caribbean “opened a new exploration frontier,” it said. Despite some bright spots, including the gas discoveries, exploration budget cuts along with already-meager reserves are worrying, said Corredores Davivienda equity analyst Francisco Chaves.

A story far from over. Even if VW apparently has gotten the go-ahead for its ‘fix-it’ proposal.

• EU Anti-Fraud Arm Investigating Loans to VW to Develop Cleaner Engines (BBG)

The European Union’s anti-fraud office OLAF is investigating loans Volkswagen received from the European Investment Bank to produce cleaner engines. The authorities picked up the issue after EIB chief Werner Hoyer said in October the lender was looking into the loans itself in light of the emissions scandal. The credits were granted to Volkswagen to help fund the development of cleaner engines. “The fact that OLAF is examining the matter does not mean that the persons or entities involved have committed an irregularity,” the authority said in an e-mailed statement Wednesday. “OLAF fully respects the presumption of innocence and the rights of defense of the persons and entities concerned by an investigation.”

The probe adds to the long list of investigations the company is facing in the wake of its disclosure in September that it cheated on pollution trials with its diesel cars. The carmaker installed software in some 11 million vehicles worldwide which lowered the level of nitrogen oxides emitted when it detected the car was being tested. VW hasn’t been informed of the probe and is “astonished that the authority goes public with this information without informing those subject to the issue,” company spokesman Eric Felber said in an e-mailed statement. VW has been talking to the EIB, the EU’s development bank, on the issue for months and has disclosed how the money was used, he said. Brussels-based OLAF is responsible for investigating fraud, corruption and evasion of taxes, duties and levies that contribute to the EU’s budget.

“Austrian banks are typically banks engaged in RELATIONSHIP banking rather than TRANSACTIONAL. Therefore, they rely on customer deposits short-term and lend long-term.”

• Austria Started the Collapse in Great Depression. Will It Do so Again? (MA)

In 1931, the sovereign debt crisis and banking system collapse began in Austria with the failure of Credit Anstalt, which was partly owned by the Rothschilds. The bank was forced to absorb another bank and a secret loan was created in London off the books to hide the insolvency to do the merger for political purposes. When that failed to be enough, the whole scam was exposed and a CONTAGION spread as people wondered what government had manipulated behind the curtain. Now the IMF has come out and stated that Austria’s banks need to increase their capital buffers urgently. The capital buffers in Austria are thin and cannot withstand a crisis. Furthermore, the banks are still active in politically and economically risky countries, which is typically carried out to increase profits.

In reality, the IMF led to the loans granted by the banks in Swiss francs, which caused many borrowers to lose 30% when the peg broke. In some Eastern European countries, the potential losses by a state arranged forced conversion of Swiss franc into local currencies could be massive. This is being done because the borrowers now owe 30% more than what they borrowed due to currency risk. This situation will not magically evaporate for they are private loans. The Austrian banks are typically banks engaged in RELATIONSHIP banking rather than TRANSACTIONAL. Therefore, they rely on customer deposits short-term and lend long-term. These are not big investment banks as in New York. They have lost a fortune because of the Swiss/euro peg collapse.

The three major banks are Erste Group, Raiffeisen Bank International (RBI), and UniCredit subsidiary Bank Austria. These are the biggest lenders in Eastern Europe as a whole who have gotten caught up in the currency nightmare. The RBI has recently announced their withdrawal from certain markets following a serious currency related loss that the bank has written in the past year for the first time. Bank Austria checked the sale of its branch business. This coming banking crisis is all currency related. It is, of course, thanks to Brussels and their irresponsible design of the euro. Politics and economics do not go together.

They will blame the bankers, but they will never blame government. Hence, this is why we can no longer afford career politicians for they will NEVER accept responsibility for screwing up the economy for political gain. The Clintons are responsible for removing ALL restriction from the Great Depression upon the banks. They then eliminated the right to declare bankruptcy on student loans. Yet, the press will NEVER ask Hillary anything about that or the fact that her biggest contributors are the banks in NYC.

The headline is Tyler Durden’s take. I second it.

• US Humiliation Is Complete: Assad Can Stay (AP)

U.S. Secretary of State John Kerry on Tuesday accepted Russia’s long-standing demand that President Bashar Assad’s future be determined by his own people, as Washington and Moscow edged toward putting aside years of disagreement over how to end Syria’s civil war. “The United States and our partners are not seeking so-called regime change,” Kerry told reporters in the Russian capital after meeting President Vladimir Putin. A major international conference on Syria would take place later this week in New York, Kerry announced. Kerry reiterated the U.S. position that Assad, accused by the West of massive human rights violations and chemical weapons attacks, won’t be able to steer Syria out of more than four years of conflict.

But after a day of discussions with Assad’s key international backer, Kerry said the focus now is “not on our differences about what can or cannot be done immediately about Assad.” Rather, it is on facilitating a peace process in which “Syrians will be making decisions for the future of Syria.” Kerry’s declarations crystallized the evolution in U.S. policy on Assad over the last several months, as the Islamic State group’s growing influence in the Middle East has taken priority. President Barack Obama first called on Assad to leave power in the summer of 2011, with “Assad must go” being a consistent rallying cry. Later, American officials allowed that he wouldn’t have to resign on “Day One” of a transition. Now, no one can say when Assad might step down.

Russia, by contrast, has remained consistent in its view that no foreign government could demand Assad’s departure and that Syrians would have to negotiate matters of leadership among themselves. Since late September, it has been bombing terrorist and rebel targets in Syria as part of what the West says is an effort to prop up Assad’s government. [..] The two countries also have split on Ukraine since Russia’s annexation of the Crimea region last year and its ongoing, though diminished, support for separatist rebels in the east of the country. The U.S. has pressed severe economic sanctions against Russia in response and has insisted that Moscow’s actions have left it isolated. That wasn’t the case on Tuesday.

“We don’t seek to isolate Russia as a matter of policy, no,” Kerry said. The sooner Russia implements a February cease-fire that calls for withdrawal of Russian forces and materiel and a release of all prisoners, he said, the sooner that “sanctions can be rolled back.” The world is better off when Russia and the U.S. work together, he added, calling Obama and Putin’s current cooperation a “sign of maturity.” “There is no policy of the United States, per se, to isolate Russia,” Kerry stressed.

IMF seems ready to pay Russia after all.

• IMF Recognizes Ukraine’s Contested $3 Billion Debt To Russia As Sovereign (RT)

The executive board of the IMF has recognized Ukraine’s $3 billion debt to Russia as official and sovereign – a status Kiev has been attempting to contest. Russia is to sue Ukraine if it fails to pay by the December 20 deadline. “In the case of the Eurobond, the Russian authorities have represented that this claim is official. The information available regarding the history of the claim supports this representation,” the IMF said in a statement. Russia asked the IMF for clarification on this issue after Kiev attempted to proclaim the debt was commercial and refused to accept Moscow’s terms for the debt’s restructuring. The December 2013 deal, which envisaged Moscow buying $15 billion worth of Ukrainian Eurobonds ($3 billion in the first tranche), was officially struck between Ukraine’s then-head of state President Viktor Yanukovich and President Vladimir Putin.

In spite of this fact, some Ukrainian and US officials have been making statements contesting the status of the deal. The sovereign status of the debt means Ukraine may have to declare default as early as December 20, when the deadline expires – unless Kiev responds to Moscow’s restructuring plan. The IMF’s decision automatically came into effect on Wednesday evening, as no objections to treating the debt as sovereign had been voiced, TASS reported. Putin had earlier ordered that a lawsuit be filed against Ukraine if it failed to pay its debt within a 10-day grace period following the deadline. Russian Prime Minister Dmitry Medvedev said last Wednesday that he didn’t believe Kiev was going to pay. “I have a feeling that they [Ukraine] will not return anything [to us] because they are crooks,” Medvedev said. “They refuse to return the money and our Western partners not only render us no help, they are actually hindering our efforts.”

Meanwhile, the IMF decided on Tuesday to change its strict policy prohibiting the fund from lending “to countries that are not making a good-faith effort to eliminate their arrears with creditors.” The decision was criticized by Moscow, as it will apparently allow the IMF to continue doing business as usual with Kiev even if it fails to pay its sovereign debt to Russia. “We are concerned that changing this policy in the context of Ukraine’s politically charged restructuring may raise questions as to the impartiality of an institution that plays a critical role in addressing international financial stability,” Russian Finance Minister Anton Siluanov wrote in a Financial Times opinion piece.

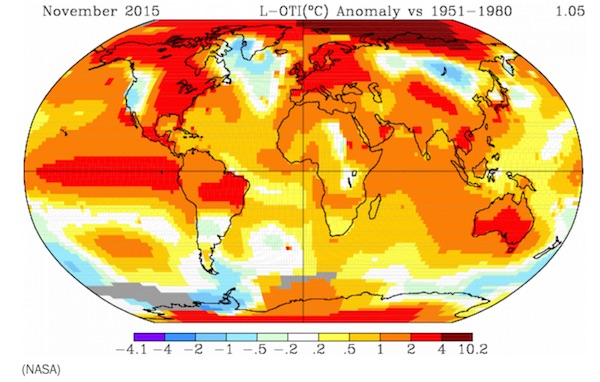

“..the Arctic, where temperatures were running anywhere from 4 to 10 degrees Celsius (7 to 18 degrees Fahrenheit) above average.”

• Earth’s Warmest November On Record By ‘Incredible’ Margin (WaPo)

Last month was the warmest November on record by an incredible margin, according to NASA measurements. The global average temperature for the month was 1.05 degrees Celsius, or about 1.9 degrees Fahrenheit, warmer than the 1951 to 1980 average. It’s also the second month in a row that Earth’s temperature exceeded 1 degree Celsius above average. It was just in October that our planet first exceeded the 1-degree benchmark in NASA’s records, dating to 1880. Prior to that, the largest anomaly was 0.97 degrees Celsius in January 2007. The recent measurements become even more significant in light of the recent Paris accord, in which 196 countries boldly agreed to limit the planet’s warming to “well below 2 degrees Celsius above pre-industrial levels and to pursue efforts to limit the temperature increase to 1.5 degree Celsius.”

The extraordinary warmth of October and November helped push this year well-past the 1-degree benchmark. We have known that 2015 is all but certain to be the warmest year on record, though we did not know by how much it would be. Given the November report, 2015 will eclipse last year as the warmest year on record by a huge margin. The Japan Meteorological Agency, which tracks the increasing global temperature, also concluded that last month was the warmest November on record since 1890, relative to the period from 1981 to 2010. El Niño played a large role in November’s — and the year’s — exceptional warmth. El Niño is an event marked by abnormally warm ocean temperatures in the equatorial Pacific.

The extent of the warm water is huge this year, stretching from the west coast of South America to past the international dateline, which divides the Pacific Ocean. As of November, temperatures in parts of this vast region were running as much as 4 degrees Celsius, or about 7 degrees Fahrenheit, above normal. But the Pacific Ocean wasn’t the warmest region of the globe in November — much of the warmth measured by NASA emanated from the Arctic, where temperatures were running anywhere from 4 to 10 degrees Celsius (7 to 18 degrees Fahrenheit) above average.

Ambrose sees climate change as a profit opportunity. That will never work. It will bring more problems than it solves. But in a world ruled by money even disaster looks like an opportunity.

• Even If The Global Warming Scare Were A Hoax, We Would Still Need It (AEP)

Chinese scientists have published two alarming reports in a matter of weeks. Both conclude that the Himalayan glaciers and the Tibetan permafrost are succumbing to catastrophic climate change, threatening the water systems of the Yellow River, the Yangtze and the Mekong. The Tibetan plateau is the world’s “third pole”, the biggest reservoir of fresh water outside the Arctic and Antarctica. The area is warming at twice the global pace, making it the epicentre of global climate risk. One report was by the Chinese Academy of Sciences. The other was a 900-page door-stopper from the science ministry, called the “Third National Assessment Report on Climate Change”. The latter is the official line of the Communist Party. It states that China has already warmed by 0.9-1.5 degrees over the past century – higher than the global average – and may warm by a further five degrees by 2100, with effects that would overwhelm the coastal cities of Shanghai, Tianjin and Guangzhou.

The message is that China faces a civilizational threat. Whether or not you accept the hypothesis of man-made global warming is irrelevant. The Chinese Academy and the Politburo do accept it. So does President Xi Jinping, who spent his Cultural Revolution carting coal in the mining region of Shaanxi. This political fact is tectonic for the global fossil industry and the economics of energy. Until last Saturday, it was an article of faith among Western climate sceptics and some in the fossil industry that China would never sign up to the COP21 accord in Paris or accept the “ratchet” of five-year reviews. They have since fallen back to a second argument, claiming that the deal is meaningless because China will not sacrifice coal-driven growth to please the West, and without China the accord unravels since it now emits as much CO2 as the US and Europe combined.

This political judgment was perhaps plausible three or four years ago in the dying days of the Hu Jintao era. Today it is clutching at straws. Eight of the world’s biggest solar companies are Chinese. So is the second biggest wind power group, GoldWind. China invested $90bn in renewable energy last year and is already the superpower of low-carbon industries. It installed more solar in the first quarter than currently exists in France. The Chinese plan to build six to eight nuclear plants every year, reaching 110 by 2030. They intend to lever this into worldwide nuclear dominance, as we glimpsed from the Hinkley Point saga. Home-grown energy is central to Xi Jinping’s drive for strategic security. China’s leaders know what happened to Japan under Roosevelt’s energy embargo in the late 1930s, and they don’t trust the sea lanes for supplies of coal and liquefied natural gas. Nor do they relish reliance on Russian gas.

Isabel Hilton from China Dialogue says the energy shift has reached a point where Beijing has a vested commercial interest in holding the world to the Paris deal. “The Chinese think they can dominate low-carbon technologies,” she said.

No, Bloomberg and EC, people fleeing warzones are not illegal immigrants. What’s illegal is calling them that.

• 159,792 Reasons for EU’s Flummoxed Refugee Policy (BBG)

Wanted: 159,792 beds, $2.4 billion, and incalculable amounts of political will. The bunks are for refugees, with the European Union having found new homes for a mere 208 out of a promised 160,000; the money is for humanitarian aid, with $3.7 billion delivered out of a pledged $6.1 billion; the political shortfalls will be on view at an EU summit in Brussels on Thursday. The refugee tide has strained Europe more than the debt crisis, overwhelming impoverished Greece, elevating the “immigrants out” slogan to official policy in much of eastern Europe, stoking the far right in the west, and allowing a growing cast of demagogues to equate the mostly Muslim refugees with Islamic State terrorists who killed 130 in a Paris rampage in November. As in the debt crisis, a reluctant Germany is the safety net.

The U.K. is sowing further disquiet as it pursues its own agenda of renegotiating the terms of its membership in the 28-nation bloc. “We have a difficult political landscape, which isn’t very conducive to putting decisions like refugee relocation into practice,” said Yves Pascouau, head of migration policy at the European Policy Centre in Brussels. New proposals such as the setup of a European Border and Coast Guard will come up at the two-day summit, but the focus is mainly on getting national leaders and EU bodies to do what they’ve pledged to do since migration shot to the top of the agenda early this year. “We need to speed up on all fronts,” EU President Donald Tusk said in a pre-summit letter to the leaders. The European Commission estimates that 1.5 million people crossed into Europe illegally between January and November, more than ever before.

Nothing about “stop the bombing”?!

• World Bank, UN Urge Sea Change In Handling Of Syrian Refugees Crisis (Guardian)

The World Bank and the UN refugee agency have called for a “paradigm shift” in the way the world responds to refugee crises such as the Syrian emergency, warning that the current approach is nearsighted, unsustainable and is consigning hundreds of thousands of exiled people to poverty. A new joint report from the bank and the UNHCR claims that 90% of the 1.7 million Syrian refugees registered in Jordan and Lebanon are living in poverty, according to local estimates. The majority of them are women and children. The refugees hosted in the two countries are particularly vulnerable as they cannot work formally and tend to be younger, less educated and have larger households.

The vast majority live in informal settlements rather than refugee camps, have few legal rights, and struggle to get access to public services because of the strains the unprecedented demand has put on the infrastructures of host countries. Although the report notes that current refugee assistance initiatives – such as the UNHCR cash assistance programme and the World Food Programme (WFP) voucher scheme – are “very effective”, it says that they are not a solution in themselves. “These programmes are not sustainable and cannot foster a transition from dependence to self-reliance,” say the study’s authors. “They rely entirely on voluntary contributions and, when funding declines, fewer of the most vulnerable refugees are able to benefit.

Moreover, social protection on its own does not foster a transition to work and self-reliance if access to labour markets is not available.” If refugees are to escape poverty, adds the report, they need to be economically integrated into local communities rather than merely offered short-term assistance.

It just keeps getting worse.

• Dozens Of Refugees Missing After Boat Sinks Off Lesvos, 2 Confirmed Dead (AP)

Greek and European border authorities have launched a search and rescue operation in the eastern Aegean Sea after reports that a boat carrying dozens of migrants sank off the island of Lesvos leaving two dead. The Greek coastguard says a helicopter, patrol boats and fishing boats are combing an area north of Lesvos for survivors, but no reliable information is yet available on how many people were on the boat and if anybody drowned. Boats from the European Frontex border agency were assisting. Greek state ERT TV said two people have been reported dead from Wednesday’s incident, and about 70 have been rescued.

Eat a live frog first thing in the morning, and nothing worse will happen to you the rest of the day.

– Mark Twain

Home › Forums › Debt Rattle December 17 2015