National Photo Co. Bond Vault 1914

“Treasury Department, Office of Comptroller of Currency — bond vault. Contains bonds to the value of $900 million securing government deposits and postal savings fund”

I’m not a technical analyst or a fundamental analyst or any other type of equity market analyst. What I am is just a guy who likes to think he can spot completely nonsensical propaganda when he reads or hears it.

You know, the type of non-stop propaganda that attempts to manage perceptions/expectations and convince “investors” that, while things are obviously very bad in the real economy, everything is still just hunky dory in the wonderful world of equities.

Case In Point

Some mainstream market analysts chimed in after the serial S&P ratings downgrades of nine Eurozone countries, and specifically the one-notch downgrade of France from AAA to AA+ (ratings outlook still negative), to say that the market had already “priced them in” and therefore they are really no big deal. S&P had put all of these countries on negative watch back in December before the latest and unsurprisingly innocuous EU Summit, so the downgrades were no surprise.

Here are just two examples of a very pervasive and perverse logic, presented by The Telegraph:

S&P cuts ratings of nine eurozone countries: reaction

Fabrice Seiman, head of Lutetia Capital, said:

“S&P is absolutely right. France is paying the price of 30 years of irresponsibility in public finances. French politicians on the right and on the left fell short of the job by not taking measures to reduce spending.”

I think this is already priced in. There should not be any sizable reaction, but there could be a technical reaction on the Franco-German spread. It should be limited to the long-term and if there is a reduction in spending.”

Bill O’Grady, chief market strategist at Confluence Investment Management, said:

“If France had been downgraded more than one level it would have precipitated a crisis. This is not good but it was anticipated, baked in. For oil it is probably a neutral event. If it raises concerns about a worsening economic environment it would be bearish.”

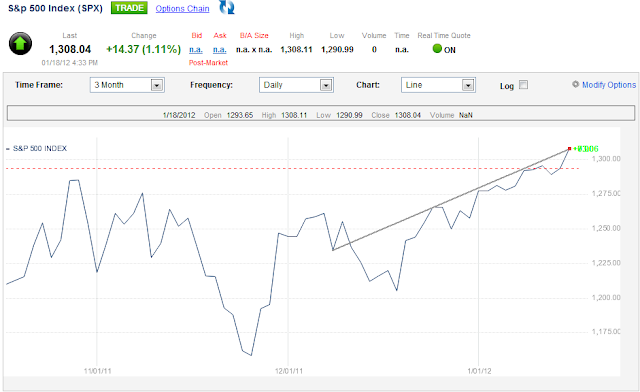

Ashvin: That logic does sound appealing on the surface and many others like to parrot it, but the first question to pop into my mind was this – how can the market “price in” very significant developments in Euro sovereign credit markets by steadily increasing in valuation since they became aware those developments would occur?? Since the S&P put a bunch of EZ countries on negative watch on December 5, 2011 and the EU Summit on December 9, the S&P500 has risen almost 6%.

That’s a boat load of downgrades the market appears to have priced in over the last month while very little “positive” news has come out of Europe. Now I’m confident that the initial reaction to my question above would be, “that’s a really simple and stupid question to ask!”. Fortunately, there are several great analysts out there who have reached similar conclusions about these equity markets, which have allegedly “priced in” everything under the Sun, and have provided us with slightly more nuanced arguments than my own.

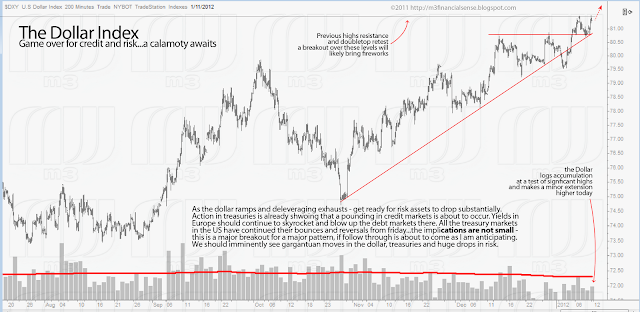

The U.S. Dollar (and Treasuries) has been increasing in value alongside U.S. equities, so the pundits should find it very difficult to explain the upwards “pricing in” market action of the last month by saying it is a nominal increase of shares priced in dollars. What we have is a very significant divergence between the dollar index and equities, as Charles Hugh Smith outlines in his piece, A Useful Fiction: Everybody Loves a Melt-Up Stock Market, and one that must close in the near future. The following charts of the dollar index ($DXY) and 5-year Treasuries are from M3 Financial Analysis:

The truth is that the very notion of the market “pricing in” events as the investor collective becomes aware of them is flawed. In the comprehensive TAE classic of 2010, Fractal Adaptive Cycles in Natural and Human Systems, Nicole Foss delves into Robert Prechter’s theory of “Socionomics” (among other things) and how it can explain market valuations as a function of endogenous factors, such as the collective mood of investors, rather than exogenous events relayed by “the news”.

Bob Prechter’s socionomics model combines Elliott’s observed fractal patterns with an understanding of human herding behaviour, comprising a comprehensive challenge to prevailing notions such as the Efficient Market Hypothesis by reversing causation and recognizing the role of emotional/irrational behaviour as the prime market driver. While the real economy demonstrates negative feedback loops, finance is thoroughly grounded in positive feedback.

Ashvin: Mish Shedlock also touched on this concept in a post earlier this week. He illustrated that, at best, the market should be viewed as a contrarian indicator for future economic trends due to its function as a gauge of extreme sentiments, and, at worst, it shouldn’t be viewed as an indicator of anything at all.

Cherry Picking Timeframes on Alleged Leading Indicators; Big Change In LEI on January 26

“The stock market is not a leading indicator of the economy. Rather, the stock market is a coincident indicator of sentiment towards equities.

…

Far from being a leading indicator, on an absolute basis the S&P has a perfect track record of peaking right before or just as a recession starts. This is just as one might expect from a gauge of equity sentiment which tends to peak right before a downturn in the economy (with everyone extrapolating good times forever into the future).

…

On a percentage change basis, the S&P 500 is not leading, not lagging, and not coincident. Instead it is completely useless mush.”

Ashvin: It’s not just the “fringe bloggers” drawing these conclusions about the market, but also such “reputable” financial institutions as UBS. Granted, the well-intentioned bankers over there also point out that the French downgrade, among others, was expected and shouldn’t affect near-term credit spreads too much. Instead, they choose to focus on the effects it will have on the state of realpolitik in Europe’s core, and how that is certainly not something which is “priced in” at all. Indeed, only market shills and fools can even pretend to separate the two (finance and politics).

UBS Explains Why AAA-Loss Is Actually Relevant

“France has not only lost its AAA status. Critically, France has lost AAA status at a time when Germany has not. France also retains a negative outlook against a stable outlook for Germany, compounding the distinction. The relative decline of France’s credit rating is something that has potential political implications.

There are parallels here to the relative positions of the UK and the US in 1949, in the wake of sterling’s devaluation against the dollar. The devaluation was simply a confirmation of economic reality, but the visible confirmation of that shift in relative economic reality served as a defining moment in the shift of the bilateral relationship in political terms.

Since the foundation of the Coal and Steel Community in 1951, the history of (continental) European politics has been essentially a story of France and Germany holding each other in check. Indeed, this was the explicit aim of the ECSC’s founders. With the downgrading of France relative to Germany, there is now a de jure as well as a de facto inequality between the two states. The ability of France to act as a counterbalance to Germany in economic decision-making has been compromised.

In the wake of the downgrade of the EFSF, it is clear that the actions of S&P have elevated the role of Germany (and perhaps, to a lesser degree, the Netherlands) in any collective economic decisions within the Euro area. Any economic decision that requires money to be spent will require wholehearted German endorsement if rating agency determined credit credibility is to be maintained. The bargaining power of Germany in the economic councils of Europe has been correspondingly increased.”

Ashvin: So if the equity markets are “pricing in” anything, it’s the pure hope that all of these downgrades of countries, banks and corporations will continue to be glossed over by bond markets, that political/economic imbalances in Europe haven’t been exacerbated, that the Greek government and its creditors aren’t helplessly struggling to reach a “voluntary” debt reduction deal before a technical default in March becomes inevitable, that China/India aren’t facing “hard landings” and that the U.S./U.K. economies will not be dragged down by their own housing markets, corporate [lack of] earnings, unemployment trends or any of the above.

Some people will tell you that the only thing the markets need to keep their manic phase intact is the inevitable QE money printing that the Fed will officially announce, which has conveniently been “just around the corner” for almost a year now. Despite those consistent predictions of QE3, I made clear that I didn’t expect the Fed to relent in 2011, and many of the same financial and political reasons underlying that expectation still stand. The primary reasons being the conundrum reflected by the fact that the S&P is still hovering around 1300 (and oil around $100/bbl), which makes the marginal benefits of QE very slim, and the politically volatile situation in the run-up to November’s elections.

On the other hand, the financial threats from the Euro crisis and a strong dollar (weak euro) have clearly intensified over the last few months, and the ECB is even more constricted from printing than it has ever been (at least for anything other than sub 3-year sovereign paper through its indirect LTRO, which still doesn’t reflect net cash entering EZ bond markets). Perhaps these developments will finally convince the Fed to “pull the trigger” on QE3, but then many questions still remain – how many trillions are needed to boost “risk appetite” for more than a few weeks and what happens when those trillions are perceived as “not enough”?

Like I said at the beginning, I’m not any sort of market analyst, but there do seem to be a whole slew of developments starting to weigh on collective investor sentiment right now, which will only get heavier in the upcoming weeks and months. No one can tell you that any of these negative and ongoing developments herald an imminent market crash or how exactly they will impact shares. What I can say with confidence, though, is that none of them are insignificant bumps in the road. They certainly did not “remove any uncertainty” from the markets and they have in no meaningful way been “priced in” by these markets either.

Home › Forums › Don’t Be Fooled: Nothing’s Priced In