John Vachon Soft drinks and war bonds truck, Montgomery AL March 1943

The age of financial innnovations found such an exalted high priest in Alan Greenspan that in his days as Fed governor he couldn’t stop talking about the dangers of regulating them, even though that was in his job description, and even though he had far too little detailed knowledge of them. His sidekicks over at the Treasury, Bob Rubin and Larry Summers, made sure their friends at Citi and JPMorgan had nothing to fear from the US government in this regard either, just as Glass-Steagall was repealed.

That’s how we got see the spread of a zillion kinds of securities and derivatives, and that’s why the vast majority of them were lauded as being highly beneficial for the economy, and therefore for all of us. Many of these instruments were and are being touted as insurance policies for the finance industry, in the same way farmers had been able to buy crop insurance since the days of old.

But that’s at best only part of the story. For instance, whether the hugely popular credit default swap may or may not initially have been ‘invented’ to serve as an insurance tool in the financial markets, is hardly interesting or relevant. What’s more important is that it very rapidly became, while it got cheaper as its popularity soared, a way for corporations and financial institutions to hide, and get rid of, their debts and liabilities.

In somewhat simplified terms, once you can claim that you have insurance against potential losses on your assets, you no longer have to carry reserves against the risk of these losses. At the height of the crisis this made many a balance sheet look a whole lot better than it really was .

And that situation continues to this day. Even if conditions have changed, and been adapted. A lot of the riskiest paper has been bought up by central banks since 2008. That buying spree, too, continues. This has lowered the risks – of credit defaults – substantially, at least for now and at least in the eyes of the industry.

And since the central banks have not only taken on a lot of the worst risk, but also made sure stock markets have been propped up and interest rates kept low, and moreover are today even increasingly purchasing stocks and bonds themselves, asset prices are skyhigh and risk assessments are ultra low. Stocks, bonds, securities have all been bought up with central banks’ thin air money in such quantities that central banks have become the markets instead of regulating them.

The reality of central bank stimulus measures, such as QE 1,2,3,x, is as different from perception as that of credit default swaps. And their aim and function are very similar: to hide from sight the risks that exist inside the financial system. Both for CDS and for QE this so far works like a charm. The dark side is, however, that if no-one knows the real value of any assets anymore, they have no way of gauging the risks involved either.

Central banks’ policies today are geared towards one goal, and one only: that no-one will find out what anything at all is really worth. The very fact that the Chinese, Japanese, European and American central banks engage in this behavior in the first place should raise flaring red flag suspicions about actual values.

Both QE and CDS – along with many other “securities” – are weapons of mass deception. We live in a global economic system that has been intentionally deprived of the means to find out what assets are worth, and that’s not a coincidence. The system couldn’t survive in its present state if there were price discovery; real values and losses may have been hidden, but they haven’t gone away.

Values may have been artificially inflated, and losses artificially limited, but nothing of the underlying reality has changed. Quite the contrary: decisions are being made on a daily basis by governments, companies and individuals, based on the false assumptions about values, risks and losses that result from financial innovations specifically designed to produce an artificial portrait of where we stand.

The consequence is that no-one truly knows where they stand anymore, but almost everyone thinks they do, thinks that we’re in a rough patch, but otherwise doing fine, that we’re growing, just at a temporarily slow pace. While in reality, we haven’t grown in years, and have very little chance of doing so in the next decade, at least.

We don’t like the idea that everything we see that looks and feels good in this regard needs to be borrowed from somebody’s future. So we ignore it. We’re a sad lot, really, we can’t face our own truth. We’d rather sell our souls for a lie that makes us feel better for a fleeting moment. We all like to think our homes, our pensions, our investments are worth more than they are.

QE, CDS et al are “innovations” designed to take advantage of that.

“There’s something going on in derivatives land … ”

• The Market Has Never Been More Fearful Of An Extreme Event (Zero Hedge)

“There’s something going on in derivatives land,” is the warning from ADM’s Andy Ash and as Paul Mylchreest notes the relationship between VIX and SKEW suggests the options market is pricing in the possibility of a major market event. The process enables professionals to maintain the illusion of calmness in VIX while hedging their positions (as they attempt to unwind as we have shown). Whether this ‘event’ is a crash or melt-up is historically unclear but given the taper and the trend of the last few years, we suspect the former more likely that the latter.

Via ADM Investor Services’ Paul Mylchreest: “A rather thought-provoking chart which we’ve been looking at is the ratio of the SKEW (the chance of an extreme or outlier event, i.e. OTM versus ATM options) versus the VIX (the expectations for more ‘normal’ day-to-day volatility – the price of hedging implied by ATM options)… and is an indicator of how the market is pricing the possibility of a potential black swan event. You can see how extended we are right now… (actually at record highs)

We can’t help wondering when Bill Gross tells the world that he is selling volatility, whether he is, in fact, selling ATM vol and buying OTM vol ??? While (curiously) 2000 didn’t register, the two previous highs in the SKEW/VIX ratio were 1994 and 2007 which turned out to be pivotal dates in terms of changes in market direction. One up and one down… Which does it look like this time?

Abenomics is a disaster.

• Bank of Japan At Risk Of QE Failure (CNBC)

The unprecedented quantitative easing (QE) program the Bank of Japan launched last year to revive the country’s stalled economy could be at risk of failure, Oxford Economics says. “Economic activity has indeed picked up since the QE program began early last year, but there are now serious warning signs that this progress may not be maintained,” Adam Slater, senior economist at Oxford Economics wrote in a report. The central bank’s large-scale asset purchases were designed to boost money supply growth, asset prices and inflation expectations while holding down interest rates. However, broad money growth slowed markedly in recent months and is now negative in real terms, a clear danger sign. “Higher inflation expectations have done little to boost credit demand so far, as continued aversion to debt among firms and households may be blunting the effectiveness of this channel,” he said.

In May, the broadest money supply measure grew just 2.7% on year, according to Oxford Economics. With headline inflation running at 3.2% in May, real broad money growth is negative. “This risks generating a significant economic slowdown – a slowdown in real broad money growth was a lead indicator of the downturns in 1998, 2005, 2009 and 2012,” Slater said. Meanwhile, the impact of monetary stimulus on asset prices is waning. QE aims to boost economic activity through shifting asset prices; for Japan, the two key prices are the stock market and the exchange rate. “Both of these asset prices have moved the ‘right way’ as a result of the QE program – stocks are up, and the exchange rate is down. But the big moves were a year ago or more, so the impact is starting to wane,” Slater said. Japan’s benchmark Nikkei 225 has declined over 6% so far this year, after rising nearly 60% last year. The yen, meantime, has appreciated over 3% against the U.S. dollar, following 21% depreciation last year. [..]

“The Bank of Japan should have ensured that monetary stimulus was sufficiently strong to offset the drag from the consumption tax rises. Recent developments in broad money and credit suggest they have failed to do so, and recent communications do not suggest any urgency on the part of the BOJ to act,” he said. “The case for delaying the second planned consumption tax rise (scheduled for 2015) is growing increasingly strong,” he added. Ultimately, the BOJ’s inaction risks turning the QE program from a qualified success into a failure. “We have long expected the BOJ to add to its QE program but had generally assumed this would be a measured decision aimed at heading off lingering downside risks to growth and inflation. Now, the danger is increasing that this will instead be a tardy response to a significant deterioration in economic conditions,” he said.

And then came the ….

• Dollar Volatility at Record Low on Bets Fed to Keep Zero Rates (Bloomberg)

Expectations for price swings in the dollar-yen currency pair fell to a record as signs of an uneven U.S. economic recovery fueled bets the Federal Reserve will keep borrowing costs at unprecedented lows. The dollar was poised for declines this quarter against most of its 16 major counterparts before U.S. reports this week that economists said will show new home sales slowed and gross domestic product contracted more than earlier estimated. The pound was about 0.2% from the strongest level since 2008 before Bank of England Governor Mark Carney testifies today to U.K. lawmakers.

Taiwan’s dollar gained as quarterly equity inflows climb toward the most since 2009. “You would need to see some prospect of change in the trajectory of U.S. monetary policy” before you see any pickup in volatility, said Emma Lawson, a senior currency strategist at National Australia Bank Ltd. in Sydney. “We don’t expect the dollar to deteriorate, but equally, it’s not expected to really take off until we get some indication of a change.”

Only expensive homes sell, because only the rich got richer.

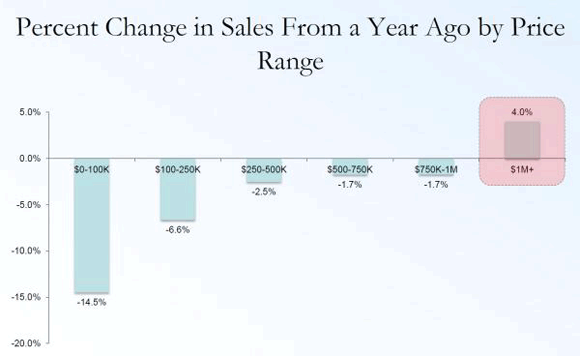

• Guess Who Is Propping Up The US Housing Market (Zero Hedge)

Moments ago the NAR released its May data, which on first blush was widely lauded as bullish: the topline print came at a 4.9% increase, rising from 4.65MM to 4.89MM, above the 4.74MM expected. Great news… if only on the surface. So what happens when one drills down into the detail? As usual, we focused on the last slide of the NAR breakdown, located at the very end of the supplementary pdf for good reason, because what it shows is hardly as bullish. So how does this “housing recovery” in which the NAR has proclaimed the “sales decline is over” look on a granular basis. The answer is below, and it is even worse than the April data. It also explains why first time buyers have dropped to even further cycle lows of just 27%, down from 29% both a month and year ago.

This is bad because while in April there was a modest increase sales in house buckets from $250 all the way up to $1MM +, in May the only bucket that had an increase in sales from a year ago was that exclusively reserve for the ultra-richest, i.e., those who benefit the most from the Fed’s non-trickle downing wealth effect policies. In fact, on a price bucket basis, the May data was unformly worse than April!

It shouldn’t be used for Abe’s political purposes.

• ‘Japan Pension Fund Should Hold Cash After Dumping Bonds’ (Bloomberg)

The world’s biggest pension fund should consider sitting on cash after selling Japanese sovereign bonds, said the government’s top adviser on the overhaul, after the Topix (TPX) index of stocks rebounded 10% amid anticipation of retirement-plan buying. While the Government Pension Investment Fund must take the opportunity to sell debt amid central-bank stimulus that is holding down yields, there’s less pressure to invest the proceeds, said Takatoshi Ito, who led a panel that advised the government on overhauling the 128.6 trillion yen ($1.3 trillion) fund. GPIF should avoid buying into markets that have rallied on bets its purchases will boost prices, he said. “It’s OK if there’s a gap in timing between selling JGBs and buying Japanese stocks and overseas assets,” Ito, a professor at the National Graduate Institute for Policy Studies in Tokyo, said in a June 19 interview.

“If they hold cash and short-term bills, they also have the option of buying back some bonds after yields finish rising.” The Topix surged 10% from a May 21 low through yesterday, outpacing a global stock rally, as investors speculated that inflows from the world’s biggest pension fund would accelerate. GPIF may change its strategy as soon as August, and putting 20% of its assets into local stocks wouldn’t be too much, Yasuhiro Yonezawa, who heads its investment committee, told the Nikkei newspaper this month. GPIF should cut its target holdings of domestic bonds to 40% from 60%, while boosting local shares to 20% from 12%, Ito said. After completing his role advising on pensions, Ito currently heads a Ministry of Finance panel working on reviving Japan’s capital markets.

The whole economy will have huge problems with rising rates.

• Bond Market Has $900 Billion Mom-and-Pop Problem When Rates Rise (Bloomberg)

It’s never been easier for individuals to enter some of the most esoteric debt markets. Wall Street’s biggest firms are worried that it’ll be just as simple for them to leave. Investors have piled more than $900 billion into taxable bond funds since the 2008 financial crisis, buying stock-like shares of mutual and exchange-traded funds to gain access to infrequently-traded markets. This flood of cash has helped cause prices to surge and yields to plunge. Now, as the Federal Reserve discusses ending its easy-money policies, concern is mounting that the withdrawal of stimulus will lead to an exodus that’ll cause credit markets to freeze up. While new regulations have forced banks to reduce their balance-sheet risk, analysts at JPMorgan Chase & Co. (JPM) are focusing on the problems that individual investors could cause by yanking money from funds.

There’s a bigger risk “that when the the Fed starts hiking in earnest, outflows from high-yielding and less-liquid debt will lead to a free fall in prices,” JPMorgan strategists led by Jan Loeys wrote in a June 20 report. “In extremis, this could force a closing of the primary market and have serious economic impact.” Last week, Fed Chair Janet Yellen said she didn’t see more than a moderate level of risk to financial stability from leverage or the ballooning volumes of debt. Even though it may be concerning that Bank of America Merrill Lynch index data shows yields on junk bonds have plunged to 5.6%, the lowest ever and 3.4%age points below the decade-long average, the outlook for defaults does look pretty good.

” … it will be 10 to 20 years before the potential growth rate rises”. Japan doesn’t have 10 to 20 years.

• Japan’s Abe Unveils ‘Third Arrow’ Of Reforms, Disappoints (Reuters)

Prime Minister Shinzo Abe unveiled a package of measures on Tuesday aimed to boost Japan’s long-term economic growth, from phased-in corporate tax cuts to a bigger role for women and foreign workers, but applause from investors is likely to be muted after Tokyo backpedaled on bolder reforms. Abe took office 18 months ago pledging to end deflation and generate sustainable growth with a three-pronged strategy of monetary easing, fiscal spending and reform. Experts say the latest installment of his so-called “Third Arrow” of long-term economic policies, most of which had been trailed in advance, is a step in the right direction, but want to see how they are fleshed out and implemented. Private economists surveyed by Reuters forecast that the plan could boost Japan’s potential growth rate by 0.2-1.5 percentage points from its current level of around 0.5%. But they noted that it would take time.

“Even after the government growth strategy is announced, various legislation must be enacted and it will take time for companies to begin to act. Therefore, it will be 10 to 20 years before the potential growth rate rises,” said Kenji Yumoto, vice chairman of the Japan Research Institute. Yumoto said it was possible, but very difficult, for Japan to hit the 2% growth level the government says is needed to reduce its mammoth public debt. Among the steps outlined so far is a future cut in Japan’s effective corporate tax rate – among the highest in the world – to below 30% over the next several years, and a promise to reform the $1.26 trillion Government Pension Investment Fund in ways likely to reallocate more money to the stock market.

At least it would be in tune with the entire casino theme.

• Better A Lucky Central Banker Than A Correct One? (CNBC)

Better a lucky governor than one who’s always right. At least, that’s what Mark Carney will be hoping for as he faces politicians on Tuesday – almost a year to the day since he took over as Bank of England Governor. After all, the Treasury Select Committee could find plenty of things to quiz Carney about. A starter for 10 would be his scattergun communication record on interest rates. His volte face on rates this month caused short-term borrowing costs to spike in the biggest one-day jump since 2009, back when the U.K. was in the midst of a financial crisis.

The Monetary Policy Committee minutes may say the Bank was surprised a rate rise hadn’t been factored in earlier – but most participants would argue they had simply trusted the governor. But it’s not just Carney’s credibility in the bond market that’s at question. The governor got it wrong on his unemployment target, on the pace of recovery in the U.K., and his fuzzy guidance has been, well, fuzzy, testing the patience of politicians and borrowers alike. Certainly, even Carney can’t pretend to have got it right in his forecasts about the pace of Britain’s recovery. Until recently, the “guidance” seemed to be that Carney was in no big hurry to raise rates – believing the economy was still fragile.

Just give everyone $1000 a month for life, that would be much cheaper.

• UK Living Wage Commission: End “National Scandal” Of Poverty (Telegraph)

Measures should be taken to cut the number of low-paid workers by a million to end the “national scandal” of poverty, according to a new report. A year-long study by the Living Wage Commission recommended a series of “low-cost” moves to tackle low pay, by building on the UK’s economic recovery. The commission, chaired by Archbishop of York John Sentamu, said increasing the pay of half a million public sector workers to the Living Wage could be more than met by higher tax revenues and reduced in-work benefits from a similar number of employees in private firms. Professional service firms such as accountancy, banks and construction companies could boost the pay of 375,000 workers if they agreed to pay the Living Wage, currently set at £8.80 an hour in London and £7.65 elsewhere, compared to the national minimum wage of £6.31, said the report.

The commission, made up of business, union and voluntary sector leaders, said extending the Living Wage depended on the Government adopting a goal to increase the voluntary take up of the companies payinh higher rate to at least a million more workers by 2020, otherwise families will continue to rely on food banks and “unsustainable debt”. Dr Sentamu said: “Working and still living in poverty is a national scandal. For the first time, the majority of people in poverty in the UK are now in working households. “The campaign for a Living Wage has been a beacon of hope for the millions of workers on low wages struggling to make ends meet. If the Government now commits to making this hope a reality, we can take a major step towards ending the strain on all of our consciences. Low wages equals living in poverty.”

Dr Adam Marshall, director of policy and external affairs at the British Chambers of Commerce, said: “The return to economic growth means that many employers are now looking again at increasing levels of pay for their employees after a tough period for business. “Many thousands of companies already pay their employees a Living Wage, and many more have an aspiration to do so. As the recovery gathers pace, they should be supported and encouraged to make this happen without facing compulsion or regulation, which could lead to job losses and difficulties – particularly for younger people entering the labour market.

I think it’s Brussels that’s dragging down Europe.

• France And Germany ‘Dragging Down’ Eurozone Recovery (Telegraph)

They are meant to be the powerhouses of Europe, but the latest figures show that the “core” economies of France and Germany are faltering while growth in the rest of the eurozone is at its strongest since pre-recession levels. France’s economy was hit by a steep downturn, and in Germany the pace of expansion was at its weakest in eight months, according to a flash reading of most recent Purchasing Managers’ Index (PMI) report by Markit. Across “peripheral” Europe – including the countries that were hit the hardest by the global financial crisis – output accelerated and growth is at the strongest since August 2007. Chris Williamson, chief economist at Markit, said that these divergent trends between the “core” and “peripheral” countries of Europe were a “big concern”.

He said: “Although the survey suggests the eurozone as a whole should grow by at least 0.4pc in the second quarter, France appears to be entering a renewed downturn after GDP stagnated in the first quarter. “Germany meanwhile looks set to grow by 0.7pc or more in the second quarter, albeit with signs that the upturn is starting to lose momentum again. “It is the rest of the region, outside of France and Germany, which – as a whole – is seeing the strongest growth momentum at the moment, highlighting how the ‘periphery’ is recovering.” The PMI report showed that in France, business contracted for the second month running ad suffered the steepest downturn with headcounts cut at the fastest rate since February. Despite the slow increases that were recorded in both the manufacturing and service sectors in Germany, the latter remained optimistic about prospects for output growth in the year ahead, with positivity hitting a three year high.

Trojan horse story.

• Berlin Is Playing With Fire Over The EU’s Top Job (Open Europe)

The fight over the appointment of the next European Commission President has reached fever pitch and left David Cameron facing the prospect of being the first EU leader ever to be outright outvoted on the matter. It would set a range of unfortunate precedents for the UK – as a new Open Europe briefing explains here. However, it would also set a very worrying precedent – and be a big gamble – for Berlin. Many representatives of Germany’s chattering classes have chosen to throw their weight behind the idea of “Spitzenkandidaten” – the notion that the European Parliament, rather than EU leaders, appoints the Commission President. Somehow, Jean-Claude Juncker has been depicted as the “people’s choice” and David Cameron the chief enemy of democracy.

There are a range of complicated reasons behind this odd series of events, including Merkel’s own coalition partner, the SPD, successfully cornering her over her decidedly lukewarm support for a candidate she herself had endorsed. Now, it’s Europe’s worst kept secret that Italy’s Matteo Renzi and France’s Francois Hollande are looking for a horse-trade: their votes for Juncker are conditional on greater flexibility in the eurozone’s rules on budget deficits, the very opposite of what Merkel and most Germans want. This has led mega-tabloid Bild – that backed Juncker a few weeks ago – to blast the “shabby haggling” over Juncker’s candidacy. It argued: “Juncker should be warned and be made aware that he must not be a chief at the mercy of Southern Europe.”

The irony of a process intended to boost transparency now being concluded via various backroom deals should not be lost on anyone. However, for Germany it also poses two huge risks going forward. First, this may set a troublesome anti-Ordnungspolitik precedent. A candidate to head the European Commission with an alleged “public mandate” who promised the Mediterranean block goodies in return for support under Qualified Majority Voting (meaning that Germany, like the UK, has no veto) surely must be Berlin’s worst nightmare. What if the next Commission President chosen by the Eurobond friendly European Parliament campaigns on a platform of debt pooling and laxer fiscal rules (on the latter, the Commission does have a key role). Berlin is just about to give away even more control over one of its key post-World War pillars.

These guys already cooperate much more than they compete; they have the same goals. My bet is some sort of merger comes out of this and then a name change, in the same fashion that Blackwater became Academi, a brilliant name for an ordinary bunch of mercenaries. Wonder what they paid the guy who came up with it.

• Monsanto Said to Have Weighed $40 Billion Syngenta Deal (Bloomberg)

The desire to avoid U.S. corporate taxes has now spread to agricultural giants – as a dead deal shows. Monsanto, the world’s largest seed company worth $64 billion, recently explored a takeover of $34 billion Swiss rival Syngenta in a transaction that would have allowed the U.S. firm to move its tax location to Switzerland. The deal, which is now defunct according to people familiar with the matter, is another sign of how U.S. firms in many sectors are trying to avoid corporate taxes by moving their headquarters overseas. U.S. drugmaker Pfizer Inc. pursued U.K.- based AstraZeneca Plc, offering as much as $117 billion before abandoning the deal, while North Chicago, Illinois-based AbbVie. is chasing Dublin-based Shire for $46.5 billion.

Monsanto and Syngenta held preliminary talks with advisers in the past few months about a combination before Syngenta’s management decided against negotiations, said the people, who asked not to be identified because the talks were private. Company officials also spoke informally with each other about a potential deal, two of the people said. There were concerns about the strategic fit, antitrust issues and relocating the company to Switzerland for tax reasons, they said. The talks, which valued Syngenta at more than $40 billion, fizzled out in late May, one of the people said. An additional concern was that U.S. politicians would close the inversion loophole, thereby removing that benefit, another person said.

How to communicate collapse.

• Answers to Tough Questions (Dmitry Orlov)

1. How can we communicate the reality of collapse to family and friends in ways that are constructive rather than destructive and find helpful ways to reflect our “endarkenment” in our everyday behavior?

“In many cases I don’t think it’s possible to communicate the reality of collapse to family and friends, because some people are simply unable to shake themselves loose from the dominant paradigm of endless growth, and will go to their graves believing that a return to growth is just around the corner, regardless of all evidence to the contrary. There are many intelligent, educated people—chairmen of central banks and professors of economics—who believe in infinite growth, even though it is mathematically impossible, and they are educated in math. Given this level of denial, how can I even start to communicate collapse to my wife if she believes in infinite growth, while neither of us are professors of economics?” “If friends and family have a vested interest in the status quo, they will stay with it. It doesn’t matter if it’s crumbling or increasingly insecure. It’s a bit like the scenario depicted in E.M. Forster’s old story ‘The Machine Stops.’

Inertia and reluctance to make abrupt changes is a major factor—not only for others but for oneself. And exactly what alternative is on offer? Jettison one’s attachment to the current status quo—for what exactly? What is one to do if one has a job and needs it to put food on the table? The consequence is that as the ship goes down, the passengers remain willfully oblivious, and even the few who do know what’s going on are confused about what is to be done.” “If you can’t fix this problem then you are on your own—and lost. It took each of us a lifetime to build our closest family relationships and we are not going to be able to walk out on them and start afresh. It also took us a long time to get to our individual understandings of where we are in terms of collapse, and there is no shortcut—so the answer is patience, mutual tolerance, and facilitating the learning process in one’s nearest circle.”

“I’ve warned everyone I know about imminent collapse. Now I no longer have any friends. But seriously, I approach it from a different angle altogether, where preparing for collapse becomes logical from the standpoint of offering a less threatening reality. For example, start by discussing medicinal plants as a way of resolving health issues. Then extend that discussion to freedom from expensive doctors and costly pharmaceuticals. Then project it further to the joys of developing the personal security and independence from large bureaucratic systems, Before you know it, you can talk about collapse without ever dropping the ‘C’ word.”

In cases like this, it’s safe to take the worst case scenario, because things always get even worse than that.

• Britain’s Nuclear Clean-Up Bill May Soar To $370 Billion (Telegraph)

The bill for cleaning up Britain’s nuclear waste has topped £110bn, after a £6.6bn increase in the cost estimate for work required over the next 120 years The Nuclear Decommissioning Authority said that the biggest increase derived from a fresh assessment of the work required at Sellafield, the country’s biggest and most toxic nuclear site. Sellafield, in Cumbria, is now estimated to cost £79.1bn to clean up, but the NDA warned that the total would “increase significantly next year” once it had fully assessed a new “performance plan” for the site.

The NDA controversially renewed a contract with Nuclear Management Partners to manage Sellafield despite fierce criticism from MPs on the Public Accounts Committee and the National Audit Office of the company’s performance. The NDA’s annual report and accounts make clear the huge scale of uncertainty that exists over the ultimate bill for Britain’s civil and military nuclear waste. It says it has “reviewed a number of scenarios with a range of possible outcomes” and found that “the estimated cost could have a potential range from £88bn to £218bn”. The figure of £110bn is on an “undiscounted” basis. Once discounted, the total is £65bn.

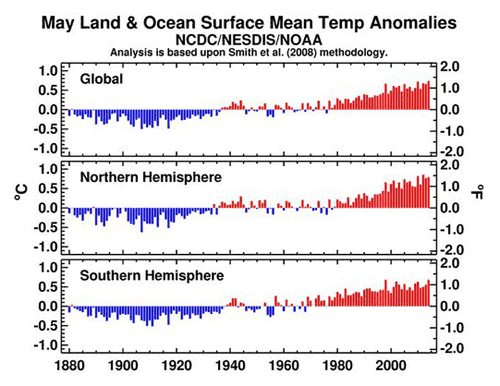

• World Posted Warmest May on Record as Oceans Heat Up (Bloomberg)

The world had its warmest May in more than a century as the planet’s oceans also set a record for heat, the National Oceanic and Atmospheric Administration said. The globe’s combined land and sea temperature for May was 59.93 degrees Fahrenheit (15.5 Celsius), or 1.33 degrees warmer than the 20th century average, breaking the mark of 1.3 degrees set in 2010, NOAA said in a monthly climate report today. “The globally averaged temperature over land and ocean surfaces for May 2014 was the highest for May since record keeping began in 1880,” the agency said. “The last below-average global temperature for May occurred in 1976 and the last below-average temperature for any month occurred in February 1985.”

The oceans contributed the most to the overall temperature, with a record of 62.4 degrees, while the period from January to May was the fifth-warmest start to any year, NOAA said. In the Arctic, ice covered 4.9 million square miles, 4.6% below the 1981-2010 average, or the third-smallest extent for May since record-keeping began in 1979, NOAA’s National Snow and Ice Data Center said. Antarctic sea ice covered 4.6 million miles, the most for May on record.

• Welcome to the New Warm Normal: Global Temps Break Another Record (Bloomberg)

The average temperature of Earth’s surface last month exceeded all other Mays before it, since recordkeeping began in 1880, according to new data from the National Oceanic and Atmospheric Association. The monthly temperature was 1.33 degrees Fahrenheit higher than the average May. That may not seem like much, but on a planetary scale, it’s huge. It ties the highest departure from average for any single month, in weather records that predate electric lights in Manhattan. But the truly disturbing part isn’t that we’ve hit a new record. It’s that we live in a season of new records. This may be the the new warm normal.

To find previous hottest Mays, you don’t have to search far; four of the five hottest Mays on record have occurred since 2010. More difficult is finding a cool May. The last time the month fell below its 20th-century average was 39 years ago. The planetary hot streak is driven by rapidly rising levels of greenhouse gases in the atmosphere since the industrial revolution. Global warming is already being felt around the world, resulting in bigger heat waves, rising seas and changing patterns of precipitation. No one under age 30 has been alive for a single month when the planet’s average surface temperature was below average.

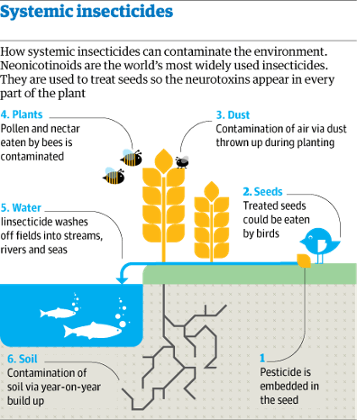

The more it’s clear that and why we should leave ban chemicals from our soils and food, the more power the old chemical giants like Monsanto and Bayer get.

• Insecticides Put World Food Supplies At Risk (Guardian)

The world’s most widely used insecticides have contaminated the environment across the planet so pervasively that global food production is at risk, according to a comprehensive scientific assessment of the chemicals’ impacts. The researchers compare their impact with that reported in Silent Spring, the landmark 1962 book by Rachel Carson that revealed the decimation of birds and insects by the blanket use of DDT and other pesticides and led to the modern environmental movement. Billions of dollars’ worth of the potent and long-lasting neurotoxins are sold every year but regulations have failed to prevent the poisoning of almost all habitats, the international team of scientists concluded in the most detailed study yet. As a result, they say, creatures essential to global food production – from bees to earthworms – are likely to be suffering grave harm and the chemicals must be phased out.

The new assessment analysed the risks associated with neonicotinoids, a class of insecticides on which farmers spend $2.6bn (£1.53bn) a year. Neonicotinoids are applied routinely rather than in response to pest attacks but the scientists highlight the “striking” lack of evidence that this leads to increased crop yields. “The evidence is very clear. We are witnessing a threat to the productivity of our natural and farmed environment equivalent to that posed by organophosphates or DDT,” said Jean-Marc Bonmatin, of the National Centre for Scientific Research (CNRS) in France, one of the 29 international researchers who conducted the four-year assessment.

“Far from protecting food production, the use of neonicotinoid insecticides is threatening the very infrastructure which enables it.” He said the chemicals imperilled food supplies by harming bees and other pollinators, which fertilise about three-quarters of the world’s crops, and the organisms that create the healthy soils which the world’s food requires in order to grow. Professor Dave Goulson, at the University of Sussex, another member of the team, said: “It is astonishing we have learned so little. After Silent Spring revealed the unfortunate side-effects of those chemicals, there was a big backlash. But we seem to have gone back to exactly what we were doing in the 1950s. It is just history repeating itself. The pervasive nature of these chemicals mean they are found everywhere now. “If all our soils are toxic, that should really worry us, as soil is crucial to food production.”

We ditched the precautionary principle in favor of profits long ago. There’s a price to pay for that.

• Autism, Developmental Delays Linked To Pesticide Exposure During Pregnancy (RT)

Exposure to several common agricultural pesticides during pregnancy increases the risk of developmental delays and autism in children by two-thirds, a new study found. While researchers did not say pesticides cause autism, a direct link is plausible. Researchers at the University of California, Davis’ MIND Institute tracked associations with specific classes of pesticides (including organophosphates, pyrethroids and carbamates) and later diagnoses of autism and developmental delay in children. They used maps from the California Pesticide Use Report (1997-2008) and the addresses of expectant mothers to track women’s exposure to agricultural pesticide spraying during their pregnancies. Developmental delay, in which children take extra time to reach communication, social or motor skills milestones, affects about four% of US. kids, the authors wrote.

The Centers for Disease Control and Prevention estimates that one in 68 children has an autism spectrum disorder (ASD), also marked by deficits in social interaction and language. Of the 970 children covered by the study, 486 had an ASD, 168 had developmental delays and 316 had typical development. “We mapped where our study participants’ lived during pregnancy and around the time of birth. In California, pesticide applicators must report what they’re applying, where they’re applying it, dates when the applications were made and how much was applied,” principal investigator Irva Hertz-Picciotto, a MIND Institute researcher and professor and vice chair of the Department of Public Health Sciences at UC Davis, said in a statement. “What we saw were several classes of pesticides more commonly applied near residences of mothers whose children developed autism or had delayed cognitive or other skills.”

The Northern California-based Childhood Risk of Autism from Genetics and the Environment (CHARGE) Study was published online in Environmental Health Perspectives. It found that approximately one-third of the study participants lived in “close proximity” (just under one mile) of commercial pesticide application sites. “This study of ASD strengthens the evidence linking neurodevelopmental disorders with gestational pesticide exposures, and particularly, organophosphates and provides novel results of ASD and DD associations with, respectively, pyrethroids and carbamates,” the researchers said in the study. Proximity to organophosphates at some point during gestation was associated with a 60% increased risk for ASD, researchers said.

Home › Forums › Debt Rattle Jun 24 2014: QE And CDS Are Weapons Of Mass Deception