DPC Fisher schooners at ‘T’ wharf, Boston 1904

A principle commonly known as Gresham’s law, though it can be dated as far back as Biblical times, not just the 16th century its namesake lived in, states that bad money drives out good money. It was used to address what happens when bits of metal are ‘shaved’ off coins, or alloys with cheaper metal are introduced, or counterfeits: people tend to keep what is perceived as ‘good’, more valuable, and spend what is seen as ‘bad’, and cheaper.

The obvious ‘trick’ for both issuers of money and anyone handling it is to make the bad sufficiently indistinguishable from the good, so people don’t notice they’re being duped. The end of the gold standard, in its various phases throughout various parts of the world, was a solid step in that direction, as was the introduction of fiat money. Essentially, there was (is) no good money anymore; it no longer represents a physical value, just a belief. So much for Gresham’s law ..

Of course there are still precious metals and other valuable materials, but if fiat money comes in unlimited quantities, it can and will all be bought, just like politicians. So you might say there’s still a bit of Gresham left after all. You might also say that not only gold and politicians are bought with fiat money, so is everybody who works a job and gets paid with it.

Seen in this light, and in the relentless logic of it, it’s a miracle that the ‘sociopath’ who brought back Gresham’s law in its full splendor didn’t arrive much earlier. That sociopath is debt, in the words of Andy McNally, chairman of Berenberg Bank UK. Not that governments and the world of finance never used debt, or let it accumulate, but if you look at the hockeystick graphs that describe all kinds of debt everywhere today, there’s no denying that in its present form it’s a rather recent phenomenon.

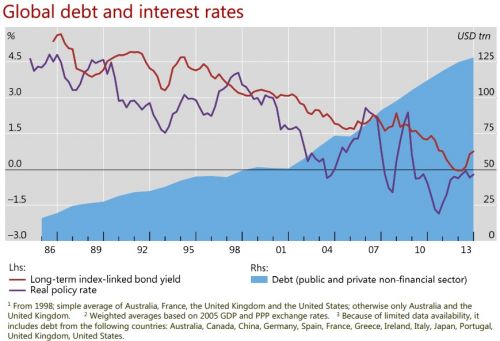

Debt today breeds inequality, since some people have access to it at very low interest rates, while others do not. Even if you pay ‘only’ 5% on your mortgage, your bank pays just 0.5%. And that’s merely the beginning. The value of the products of your labor are being distorted, manipulated and eaten alive whole by what others, from behind their luxurious desks, borrow at the flick of a switch and the stroke of trading keyboard. What then is your labor worth? Not much. And its value is necessarily declining.

If money is what you get paid for the work you do, then debt is not money. Or should not be. But the two are sufficiently indistinguishable that you can’t tell the difference. So someone who wants the fruits of your labor can pay you with debt, with something he himself never lifted a finger for. If debt were money, that would not be possible. Nor would it if you could tell the two apart.

The difference between debt and equity is the same as that between debt and money. And McNally wrote a great piece on how debt drives out equity in our world, and reaffirms Gresham’s law.

How Debt The Sociopath Used Its Seductive Charms To Kill Innocent Equity, Provider Of Social Justice

It’s nearly 60 years since Imperial Tobacco’s pension fund manager, George Ross-Goobey, gave his landmark speech with a simple message – company shares represent something that grows, so stand a better chance of rewarding pensioners with a comfortable retirement. Not just that, but he also pointed out that the interest on the shares was higher than on the gilt-edged bonds that his colleagues all “knew” were safe. [..] The back end of 2012 was an equally historic moment for UK pensioners. For the first time in more than half a century, their retirement funds once again held more bonds than equities.

These two events are like front and back cover to one of the greatest murder stories of our age. Equity, in the very broadest sense, has been killed. [..] The culprit was obvious from the start – it was the debt that done it. The word “equity” comes from “aequitas”, the Latin concept of justice, equality, fairness and conformity. It should be no surprise, therefore, that the privation of equity finance in society is leading to an extreme concentration of wealth and a general sense of injustice, unfairness and a feeling that some are not quite playing by the rules.

After a long history of capitalism’s broadening ownership through 19th century land reform and 20th century home-ownership, its finest trait has been thwarted by the greatest sociopath of all time. Our productive assets are debt-financed like never before and, although it flatlined after the Second World War, inequality’s sudden upsurge after 1971 tallies curiously well with credit creation. The numbers are staggering. The UK’s banks’ assets have gone from 70% of national income in 1970 to more than 450% today.

Debt’s cohorts often pointed to this “financial deepening” as a clear sign that finance was being democratised. But once debt outgrew its natural purpose – a mortgage perhaps – the death of equity was a certain outcome. [..] Since 1987, the debt of UK companies has gone from 45% to more than 90% of GDP. For the six years running up to the crisis, the UK equity market actually used to get money out of companies, rather than putting it in. Like all good sociopaths, debt befriended the most unsuspecting accomplices. Tax, governments, accountants, actuaries, regulators, banks and even cultural values all fell under the spell of debt, keeping productive equity out of the hands of the many.

[..] Gordon Brown’s canning of the dividend tax credit was the final nail in equity’s coffin. One actuary calculates the impact on UK pension funds at more than £100bn but, more importantly, it has left equities less attractive for investors and debt finance more attractive for companies. The banks were soon incentivised to advise on debt before equity. Companies with secure balance sheets make for bad investment banking clients – much better to lend to them at 5% and fund that debt at 0.5% than find them some equity finance and send them on their way.

Governments and regulators around the world bought into the “safety” that debt claimed to offer. When debt stopped returning their call, politicians of all shades soon cried for credit to flow again. Regulators set the tone for financial advisers – equity is risky, debt is safe. Eventually debt mesmerised the greatest accomplice of all – our cultural values. [..] Debt financed impatience and gave us permission to live beyond our means. It destroyed our sense of partnership and reduced relationships to mathematics rather than shared endeavour.

When the inquest into the death of equity is held, and the economists, central bankers, politicians and regulators have given their evidence, the jury will endure an expert witness on the basic difference between debt and equity. They are not merely different forms of finance, as debt would have us believe. They embody different incentives and rewards that define how we operate as a society.

The financial rewards of economic progress are always returned through the equity, not the debt, which is why only the few who defied debt’s charm now get most of the rewards. The jury will see how debt duped us all and deprived us of one of the most powerful forces in society. We should have financed our productive assets with as much equity as possible, whenever possible. Equity aligned owners of assets with their custodians: it was fair and impartial. It was even-handed. It was effective. It was the purest form of finance.

Just like 99% of our ‘money supply’ is made up of credit, 99% of all debt is bad. Not in the sense that it can’t be paid back, but that it distorts our lives, even if we don’t always understand how that works. Why can’t you pay for a house with your labor, why do you need a loan to do it? Because the others do it that way. Which drives up prices so much, you have to as well.

Central banks today are the sociopath debt’s main accomplices. They lower rates to near zero and hand out the stuff like Halloween candy. To banks, who, if they feel like it, hand it to you at a rate at least ten times higher than what they pay. It may seem to work as long as those rates are so low. But if equity markets are basically dead, then who’s going to finance the real economy? There’ll be no-one left.

Lip service.

• BIS: Global Markets Euphoria Does Not Reflect Economic Reality (Finfacts)

The Bank of International Settlements (BIS) says in its annual report which was issued Sunday that the current global markets euphoria does not reflect economic reality and its general manger warned on interest rates that: ” if they persist too long, ultra-low rates could validate and entrench a highly undesirable type of equilibrium – one of high debt, low interest rates and anaemic growth.” The BIS is the bank for central banks and is the oldest international financial organisation, having been founded in Basel, Switzerland in 1930. The annual report says: “The overall impression is that the global economy is healing but remains unbalanced. Growth has picked up, but long-term prospects are not that bright. Financial markets are euphoric, but progress in strengthening banks’ balance sheets has been uneven and private debt keeps growing. Macroeconomic policy has little room for manoeuvre to deal with any untoward surprises that might be sprung, including a normal recession.”

“Financial markets are euphoric, in the grip of an aggressive search for yield…and yet investment in the real economy remains weak while the macroeconomic and geopolitical outlook is still highly uncertain,” said Claudio Borio, the head of the BIS’s monetary and economic department. The BIS said growth is still below its precrisis levels and while the world economy expanded 3% in the first quarter of 2014 compared with a year earlier – weaker than the 3.9% average growth rate between 1996 and 2006, in some advanced economies, output, productivity and employment remain below their precrisis peaks. “Good policy is less a question of seeking to pump up growth at all costs than of removing the obstacles that hold it back,” the bank said pointing to the recent upturn in the global economy as a precious opportunity for reform while warning that policy needed to become more symmetrical in responding to both booms and busts.

Global markets are currently “under the spell” of central banks and their unprecedented accommodative monetary policies, it said and warned that returning to normal monetary policy too slowly could also be dangerous for government finances. “Keeping interest rates unusually low for an unusually long period can lull governments into a false sense of security that delays the needed consolidation,” it said, as the glut of cash encourages cheap government borrowing.

Andy McNally is chairman of Berenberg Bank UK.

• How Debt the Sociopath Killed Innocent Equity, Social Justice (McNally)

It’s nearly 60 years since Imperial Tobacco’s pension fund manager, George Ross-Goobey, gave his landmark speech with a simple message – company shares represent something that grows, so stand a better chance of rewarding pensioners with a comfortable retirement. Not just that, but he also pointed out that the interest on the shares was higher than on the gilt-edged bonds that his colleagues all “knew” were safe. It was a hard sell, but he clearly had all the skills you need to succeed in modern finance. Imperial Tobacco’s retirees had a better old age than most, not least Ross-Goobey himself, who retired with a handsome pension and, supposedly, a limitless supply of his favourite cigar.

The back end of 2012 was an equally historic moment for UK pensioners. For the first time in more than half a century, their retirement funds once again held more bonds than equities. These two events are like front and back cover to one of the greatest murder stories of our age. Equity, in the very broadest sense, has been killed. This is no Agatha Christie novel, however. Although there are many discredited witnesses, clues, red herrings and disguises, there is no “Least Likely Suspect”. The culprit was obvious from the start – it was the debt that done it.

Debt.

• Hong Kong’s China Debt Trap (MarketWatch)

All eyes this week will be on Hong Kong’s protest march for democratic reform, with numbers expected to be swollen by Beijing’s recent hardening stance towards the territory. But how soon will Hong Kong have another gripe to take up with its sovereign as more alarms sound over a massive lending boom to mainland China? This potential debt trap is increasingly on the radar of investors after a succession of cautionary comments from analysts and regulators about mainland-bound loans from Hong Kong-based banks. The latest came from Moody’s last week, as they reiterated an earlier warning about the risks in the rapid expansion of Hong Kong banks’ lending to mainland Chinese entities.

The exposure of Hong Kong to the mainland grew by 29% in 2013 to 2.3 trillion Hong Kong dollars ($297 billion), accounting for 20% of total banking assets, Moody’s said. This, they said, poses credit challenges as it increases banks’ exposures to China’s economic and financial vulnerabilities, as well as pressuring some of the banks’ liquidity profiles and capitalization levels. Both the IMF and the Hong Kong Monetary Authority have also recently flagged similar concerns about the wall of money Hong Kong was sending into a slowing and fragile-looking Chinese economy. Earlier this year, brokerage Jefferies described a “parabolic” rise in lending to mainland China, which it saw as a looming problem for Hong Kong. From almost zero in 2009, this lending has reached 150% of Hong Kong’s GDP.

This surge illustrates that we are talking about a relatively new phenomenon which has coincided with massive quantitative easing by the world’s top central banks, along with a series of measures by China to internationalize its currency. This also means that assessing the level of risk when these two very different financial systems come together puts us in somewhat unchartered territory. What we do know is Hong Kong’s lending is by far the largest. Earlier this month, Fitch Ratings calculated that Hong Kong’s exposure to the mainland had reached $798 billion. This compared to a total of $400 billion for banks elsewhere in the Asia-Pacific region – mainly Australia, Japan, Macau, Taiwan and Singapore.

Debt.

• China Debt Set for Biggest Quarterly Gain in Two Years on Easing (Bloomberg)

Chinese sovereign bonds headed for their biggest quarterly increase in two years after the central bank eased monetary policy to spur economic growth. The government notes rose 2.4% since March, the most since the second quarter of 2012, a Bloomberg index shows. The yield on benchmark 10-year securities fell 45 basis points to 4.05% this quarter through June 27, according to ChinaBond data. The yield on the 4.42% debt due March 2024 was steady today at 4.07% as of 10:48 a.m. in Shanghai, National Interbank Funding Center figures show. Premier Li Keqiang said this month authorities would ensure growth of at least 7.5% in 2014 after year-on-year expansion dipped to 7.4% in the first quarter from 7.7% in the preceding three months. The People’s Bank of China has cut some lenders’ reserve requirements twice this quarter and the State Council has announced a ‘mini-stimulus’ program including tax relief for small companies and increased spending on railways.

“The PBOC’s policy direction is to guide interest rates lower to ensure growth,” said Zhang Guoyu, a Shanghai-based analyst at Orient Futures Co. “If it continues to want lower financing costs to benefit the real economy, the 10-year yield may have further downside.” The official Purchasing Manufacturing Index (CPMINDX) may have climbed to 51 in June, the highest level this year, according to a Bloomberg News survey ahead of the statistics bureau’s data release tomorrow. Targeted cuts in reserve requirements have helped companies’ profitability, although the foundation for recovery isn’t solid, Caixin magazine reported on its website yesterday, citing Zhang Jianhua, head of the PBOC’s Hangzhou branch.

• Slowing China Economy Dims Profit Outlook to 2012 Low (Bloomberg)

The most-actively traded Chinese companies in the U.S. are on pace to report the smallest profits in two years as growth in the world’s second-largest economy decelerates to the slowest since 1990. Analysts covering stocks listed on the Bloomberg China-US Equity Index estimate that on average they will post earnings of $5.64 per share this year, which would be the lowest profits reported since 2012, data compiled by Bloomberg show. They’ve cut revenue forecasts by 7.9% in the past 11 weeks. Earnings and sales projections are falling as economists surveyed by Bloomberg estimate China’s gross domestic product expansion will slow to 7.4% this year, the weakest pace in 24 years, after back-to-back annual increases of 7.7%.

While the government has implemented tax breaks, accelerated spending and cut some banks’ reserve requirements, investors are concerned that officials aren’t doing enough to stem a decline in real estate prices and boost private consumption. “What we’re seeing now is the near-term impact of the adjustment in expectations as these policies get implemented,” Alan Gayle, senior investment strategist, who helps oversee about $50 billion for RidgeWorth Investments, said by phone from Atlanta on June 27. “They’re trying to slow down some of the more inflationary real-estate related sectors and improve overall average standards of living.”

• Is China Manufacturing Data Due For A Dip? (CNBC)

Chinese manufacturing data could disappoint this week amid weakness in the economy and that may just be the beginning, analysts told CNBC. A rebound in export orders in recent months boosted China’s manufacturing sector amid a weaker yuan and signs of a recovery in the U.S., one of China’s major trading partners. But some analysts told CNBC they are worried that the underlying risks to China’s economy would spill over to the country’s manufacturing sector, derailing the recent positive trend. “I’m going to take the under,” said Joe Magyer, senior analyst at The Motley Fool, referring to expectations for official purchasing managers’ index (PMI) data out on Tuesday, which he expects to start to reflect weakness in China’s economy. The final reading for HSBC’s PMI data is also due Tuesday.

Last week a flash reading for the HSBC manufacturing data hit a seven-month high of 50.8, up from 49.4 in May, marking the first time the figure crossed the 50 level – the dividing line between expansion and contraction – this year. Meanwhile, official PMI rose to a five-month high of 50.8 in May. But Magyer warned the positive run could end soon. “I know a lot of people think the mini stimulus that’s been going on is going to help but China has been fueled by such an expansion in credit over the past few years any incremental stimulus isn’t going to have much of an effect,” he said, referring to recent targeted reserve requirement ratio (RRR) cuts for banks in weaker sectors of the economy, such as agriculture.

Magyer flagged China’s real estate market as another major risk, amid signs of cooling. Revenue from property sales for the January-to-May period dropped 8.5% on year, while data from Chinese real estate website Soufun show May land sales fell 45% on year and transaction value fell 38%. “When you look at some of the key drivers of China right now one of them is real estate,” said Magyer. “Pricing for real estate in China has finally stalled… and that’s important because 20% of the economy is related to real estate and when you look at all the iron ore that’s piling up in ports I think you have a pretty good reason for that. [The reason] could be [that] one of the major components of the economy is cooling off,” he added.

Vultures.

• Argentina at Brink of Default as $539 Million Payment Due (Bloomberg)

Argentina is poised to miss a bond payment today, putting the country on the brink of its second default in 13 years, after a U.S. court blocked the cash from being distributed until the government settles with creditors from the previous debt debacle. The nation has a 30-day grace period after missing the $539 million debt payment to seek an accord with a group of defaulted bondholders led by billionaire Paul Singer’s NML Capital and prevent a default on its $28.7 billion of performing global dollar bonds. Both Argentina and NML have said that they’re open to talks. A decade-long battle between Argentina and holdout creditors from the country’s $95 billion default in 2001 is coming to a head. The U.S. Supreme Court on June 16 left intact a ruling requiring the country pay about $1.5 billion to holders of defaulted debt at the same time it makes payments on restructured bonds.

Argentina last week transferred funds to its bond trustee to pay the restructured notes, only to have U.S. District Court Judge Thomas Griesa order the payment sent back while the parties negotiate. The judge’s decision “closes Argentina’s options to finally force it to negotiate,” said Jorge Mariscal, the chief investment officer for emerging markets at UBS Wealth Management, which oversees $1 trillion. “Argentina should now stop using these delay tactics and get serious.” Argentina took out a full-page advertisement in yesterday’s New York Times saying that Griesa favored the holdout creditors and was trying to push Argentina into default. The ruling “is merely a sophisticated way of of trying to bring us down to our knees before global usurers,” Argentina said. “But he will not achieve his goal for quite a simple reason: The Argentine Republic will meet its obligations, pay off its debts and honor its commitments.”

Debt.

• Emerging-Market Companies Vulnerable on $2 Trillion Debt Binge (Bloomberg)

Emerging-market companies that took on more than $2 trillion of foreign borrowing since 2008 are vulnerable to an evaporation of funding at the first sign of trouble, according to the Bank for International Settlements. Bond investors willing to lend generously when conditions are good can pull out in a crisis or when central banks tighten monetary policy, analysts led by Claudio Borio, head of the monetary and economic department, wrote in the BIS annual report. Emerging-market companies that lose access to external debt markets may then be forced to withdraw bank deposits, depriving domestic lenders of funding as well, they said.

Low interest rates and central bank stimulus in developed nations, combined with a retreat in global bank lending, have encouraged emerging-market borrowers to raise debt abroad, according to the Basel, Switzerland-based BIS, which hosts the Basel Committee on Banking Supervision that sets global capital standards. Demand for higher-yielding securities also helped suppress borrowing costs for riskier issuers. “Like an elephant in a paddling pool, the huge size disparity between global investor portfolios and recipient markets can amplify distortions,” the analysts wrote. “It is far from reassuring that these flows have swelled on the back of an aggressive search for yield: strongly pro-cyclical, they surge and reverse as conditions and sentiment change.” Loose financing conditions “feed into the real economy, leading to excessive leverage in some sectors and overinvestment in the industries particularly in vogue, such as real estate,” according to the report.

“If a shock hits the economy, overextended households or firms often find themselves unable to service their debt.” Emerging-market companies sell bonds mainly through foreign units, exposing them to currency risk, the BIS said. The true size of their borrowing could also be masked as foreign direct investment, making it a “hidden vulnerability,” according to the report. With emerging markets becoming more important to the global economy and financial system, any stress affecting them will probably hurt developed nations, too, it said. “The ramifications would be particularly serious if China, home to an outsize financial boom, were to falter,” the analysts wrote. That would hurt commodity exporters that have seen strong credit and asset price increases drive up debt and property prices, as well as other nations still recovering from the financial crisis, the BIS said.

If you can make people believe in perpetual growth, perpetual motion should be an easy one.

• The Delusion of Perpetual Motion (Hussman)

The central thesis among investors at present is that they are “forced” to hold stocks, given the alternative of zero short-term interest rates and long-term interest rates well below the level of recent decades (though yields were regularly at or below current levels prior to the 1960s, which didn’t stop equities from being regularly priced to achieve long-term returns well above 10% annually). The corollary is that investors seem to believe that as long as interest rates are held near zero, stocks will continue to advance at a positive or even average or above-average rate. It’s certainly true that from a psychological standpoint, the Federal Reserve has induced the same sort of yield-seeking speculation that drove investors into mortgage securities (in hopes of a “pickup” over depressed Treasury-bill yields), fueled the housing bubble, and resulted in the deepest economic and financial collapse since the Great Depression.

This yield-seeking has clearly been a factor in encouraging investors to forget everything they ever learned from finance, history, or even two successive 50% market plunges in little more than a decade. But the finance of all of this – the relationship between prices, valuations and subsequent investment returns – hasn’t been altered at all. As the price investors pay for a given stream of future cash flows increases, the long-term rate of return that they will achieve on their investment declines. Zero short-term interest rates may “justify” the purchase of stocks at higher valuations so that stocks promise equally dismal future returns. But once stocks reach that point, investors should understand that those dismal future returns will still arrive.

Let me say that again. The Federal Reserve’s promise to hold safe interest rates at zero for a very long period of time has not created a perpetual motion machine for stocks. No – it has simply created an environment where investors have felt forced to speculate, to the point where stocks are now also priced to deliver zero total returns for a very long period of time. Put simply, we are already here. Based on valuation measures most reliably associated with actual subsequent market returns, we presently estimate negative total returns for the S&P 500 on every horizon of 7 years and less, with 10-year nominal total returns averaging just 1.9% annually. I should note that in real-time, the same valuation approach allowed us to identify the 2000 and 2007 extremes, provided latitude for us to shift to a constructive stance near the start of the intervening bull market in 2003, and indicated the shift to undervaluation in late-2008 and 2009.

Good history lesson.

• The Mythical Banking Crisis and the Failure of the New Deal (Stockman)

The Great Depression thus did not represent the failure of capitalism or some inherent suicidal tendency of the free market to plunge into cyclical depression – absent the constant ministrations of the state through monetary, fiscal, tax and regulatory interventions. Instead, the Great Depression was a unique historical occurrence – the delayed consequence of the monumental folly of the Great War, abetted by the financial deformations spawned by modern central banking. But ironically, the “failure of capitalism” explanation of the Great Depression is exactly what enabled the Warfare State to thrive and dominate the rest of the 20th century because it gave birth to what have become its twin handmaidens – Keynesian economics and monetary central planning.

Together, these two doctrines eroded and eventually destroyed the great policy barrier – that is, the old-time religion of balanced budgets – that had kept America a relatively peaceful Republic until 1914. To be sure, under Mellon’s tutelage, Harding, Coolidge and Hoover strove mightily, and on paper successfully, to restore the pre-1914 status quo ante on the fiscal front. But it was a pyrrhic victory – since Mellon’s surpluses rested on an artificially booming, bubbling economy that was destined to hit the wall. Worse still, Hoover’s bitter-end fidelity to fiscal orthodoxy, as embodied in his infamous balanced budget of June 1932, got blamed for prolonging the depression. Yet, as I have demonstrated in the chapter of my book called “New Deal Myths of Recovery”, the Great Depression was already over by early summer 1932.

At that point, powerful natural forces of capitalist regeneration had come to the fore. Thus, during the six month leading up to the November 1932 election, freight loadings rose by 20%, industrial production by 21%, construction contract awards gained 30%, unemployment dropped by nearly one million, wholesale prices rebounded by 20% and the battered stock market was up by 40%. So Hoover’s fiscal policies were blackened not by the facts of the day, but by the subsequent ukase of the Keynesian professoriat. Indeed, the “Hoover recovery” would be celebrated in the history books even today if it had not been interrupted in the winter of 1932-1933 by a faux “banking crisis” which was entirely the doing of President-elect Roosevelt and the loose-talking economic statist at the core of his transition team, especially Columbia professors Moley and Tugwell.

Ph.

• Climate Change Goes Underwater (Bloomberg)

When it comes to climate change, almost all the attention is on the air. What’s happening to the water, however, is just as worrying — although for the moment it may be slightly more manageable. Here’s the problem in a seashell: As the oceans absorb about a quarter of the carbon dioxide released by fossil-fuel burning, the pH level in the underwater world is falling, creating the marine version of climate change. Ocean acidification is rising at its fastest pace in 300 million years, according to scientists. The most obvious effects have been on oysters, clams, coral and other sea-dwelling creatures with hard parts, because more acidic water contains less of the calcium carbonate essential for shell- and skeleton-building. But there are also implications for the land-based creatures known as humans.

It’s not just the Pacific oyster farmers who are finding high pH levels make it hard for larvae to form, or the clam fishermen in Maine who discover that the clams on the bottom of their buckets can be crushed by the weight of a full load, or even the 123.3 million Americans who live near or on the coasts. Oceans cover more than two-thirds of the earth, and changes to the marine ecosystem will have profound effects on the planet. Stopping acidification, like stopping climate change, requires first and foremost a worldwide reduction in greenhouse-gas emissions. That’s the bad news. Coming to an international agreement about the best way to do that is hard.

Unlike with climate change, however, local action can make a real difference against acidification. This is because in many coastal regions where shellfish and coral reefs are at risk, an already bad situation is being made worse by localized air and water pollution, such as acid rain from coal-burning; effluent from big farms, pulp mills and sewage systems; and storm runoff from urban pavement. This means that existing anti-pollution laws can address some of the problem. States have the authority under the U.S. Clean Water Act, for instance, to set standards for water quality, and they can use that authority to strengthen local limits on the kinds of pollution that most contribute to acidification hot spots. Coastal states and cities can also maximize the amount of land covered in vegetation (rather than asphalt or concrete), so that when it rains the water filters through soil and doesn’t easily wash urban pollution into the sea. States can also qualify for federal funding for acidification research in their estuaries.

Better start packing, guys.

• Scotland Has Billions of Barrels of Shale Deposits Under Its Cities (Bloomberg)

Scotland may have billions of barrels of shale oil and gas buried under the country’s most densely populated areas, geologists said today. Scotland’s central belt, running between Glasgow and Edinburgh, may have 80.3 trillion cubic feet of gas in place and 6 billion barrels of oil, a report by the British Geological Survey said. While it’s not an estimate of how much can be extracted, if only a fraction of that amount was drilled it could transform prospects for Scottish oil and gas output.

The oil and gas industry is central to the debate on Scotland’s independence before a referendum in September. The yes campaign says existing fields in the North Sea will underpin the economy of an independent Scotland, while supporters of a no vote say declining production from offshore reserves leaves the country vulnerable. The U.K. government is offering tax breaks to shale drillers to spur development of the resource as North Sea reserves dwindle The Bowland basin in northern England may supply local natural gas demand for half a century at extraction rates of 10% similar to U.S. fields, according to a report last year.

Home › Forums › Debt Rattle June 30 2014: Bad Debt Drives Out Good Money