Esther Bubley Sign at the National Zoological Park, D.C. May 1943

The story itself may at times feel repetitious and belonging to a different era, but in the case of Ukraine it’s certainly applicable: another country is being given the Shock Doctrine treatment; it’s by no means restricted to South America in the 1970s. Ukrainians have hit the streets for months, and about a hundred of them got taken out cold by nobody knows who, just to end up with a government handpicked by American powerbroker kingmakers, a government, moreover, that will only be in place for a very limited time, until the upcoming elections, but which by the time it recedes into the background will have signed away everything not bolted down, to the IMF and its western handlers.

Former PM Yulia Tymoshenko, who got very rich in a very disputable way through a gas delivery monopoly, just today announced her candidacy in the elections, as Dmytro Yarosh did earlier this week, the leader of the Right Sector that saw one of its lieutenants shot to death a few days ago by a Ukraine police whose allegiance one might pose a question or two about, like so many things Ukraine related. That will make for a nice field of candidates. Don’t count on “Yats” being on of them, his job is to sell the country to the west and vanish into a nice plush job for, say, the World Bank.

And while it’s of course not yet 100% clear what the EU/US plans are with Ukraine, since at first sight the country doesn’t possess that much of real and immediate value. The heavy industry that might attract some interest is all in the eastern part where the population is predominantly ethnic Russian, and it has a whole lot of the most fertile soil – black earth – in the world, but that’s not exactly a fungible resource. The only store of value then would seem to be the Gazprom pipelines that run underneath the country’s land. If these pipelines are what the west is after, they are after war, because Russia will never give up control of them (and there’s no reason why it should).

It was announced today that Ukraine will get an $18 billion loan from the IMF. The Maidan protesters would do good to read the fine print, but they don’t really have much of a say anymore, do they? They had a lot more of that before Yats was installed. But would you take a look at all the other goodies, all theirs just for singing over control over their lives:

The IMF agreement will clear the way for a planned €1.6 billion ($2.2 billion) in emergency aid from the European Union, EC President Barroso said. The EU has also pledged project loans and grants that could reach €11 billion over 7 years. The European Bank for Reconstruction and Development said today that it would increase investments in Ukraine to €1 billion a year and resume lending for state-run projects. Ukraine is also awaiting $1 billion in loan guarantees and $150 million in direct assistance from the U.S. “This represents a powerful sign of support from the international community for the Ukrainian government as we help them stabilize and grow their economy and move their democracy forward,” the White House.

Sounds like a lot of money provided you don’t pay attention. And every penny is welcome. As Yats put it: “The country is on the edge of economic and financial bankruptcy. [..] “This package of laws is very unpopular, very difficult, very tough”. Yes, he said laws. As in cast in stone. In return for the IMF package, Ukraine under an unelected PM is signing up for a kind of austerity Greece would be jealous of. It will also sign away any and all control of its own economy. For what if you do pay attention is really not that much money. Ukraine already owes $13.6 billion in total in just the next 11 months alone, by far most of it to Russia.

Maybe the west can try and poke the Russian bear some more over that. While Ukraine heating gas prices will rise by 50% on May 1. May 1 is one thing, but wait till winter comes, by which time the squeeze of IMF induced austerity has set in, the cost of living has exploded and a civil war between heavily armed nationalist militia from pro- versus anti Russian forces is either on the brink of breaking out or already a foregone fact. Who’s going to prevent widespread slaughter in the country then? There’s only Putin, isn’t there? Who would have to enter the country to do that. And if he does …

Maybe it’s time for us westerners to whistle back the rhetoric and war mongering that’s being committed by those who claim they represent us. To mix in a nuance or two with the propaganda we’re being bombarded with in our media. Because if we don’t, chances are things are going to be perpetrated in our name that we should feel deeply ashamed of. And we can’t after all keep saying forever that we didn’t know. Really guys, you’re ready to let this happen in your name?

• Beware The Distressed Credit “Canary In The Coalmine” (Zero Hedge)

The credit cycle is called a "cycle" because, unlike the business cycle (which the Fed has convinced investors no longer exists), it 'cycles'. At some point the re-leveraging of the balance sheet – remember more cash on the balance sheet but even morerer debt (as we noted here) – requires risk premia that outweigh even the biggest avalanche of yield-chasing free money. It appears, as Bloomberg's James Crombie notes, that point may be approaching as yield premiums for U.S. distressed debt hit a five-year high on March 25, according to Bank of America Merrill Lynch.

h/t @jtcrombie

BAML’s distressed debt index was at a spread of 2,483 basis points — the highest level since March 18, 2009 when it was at a spread of 2,609 basis points.

US corporates saw profit growth slow to almost zero last year and on an EBIT basis it has been flat for some time now. Earnings quality, rather than improving is actually deteriorating, as indicated by the increasing gap between official and pro-forma EPS numbers. As a consequence, following a long period of overspending and in the absence of a strong pick-up in demand, corporates will have to spend less and not more.

Finally, as a consequence of such anemic growth, corporates have been gearing up their balance sheets in an effort to sustain EPS momentum via the continuing use of share buybacks. With markets up substantially in 2013 executing those share buybacks has become increasingly expensive. Little wonder companies have to borrow so much to continue executing them.

• U.S. Jobs Market Dropouts Increasingly Likely To Stay Out (Reuters)

A growing number of Americans quitting the labor force are likely gone for good, offering a cautionary note to the Federal Reserve as it tries to gauge how tight the jobs market is and how quickly to raise interest rates. For a long time, data suggested a significant portion of the decrease in labor force participation was because many job seekers had grown frustrated with their search and had given up looking. If the job market tightened enough, the thinking went, these Americans would be lured back to hunt for work again. But a different picture is now emerging. Data shows participation in the past few years has fallen mainly because Americans have retired or signed up for disability benefits.

“The data suggest that the recent exits from the labor force have been more voluntary in nature than was the case in 2009, when the economy was weak and job prospects were dire,” said Omair Sharif, senior economist at RBS. According to economists who have analyzed Labor Department data, 6.6 million people exited the workforce from 2010 and 2013. About 61% of these dropouts were retirees, more than double the previous three years’ share.

People dropping out because of disability accounted for 28%, also up significantly from 2007-2010. Of those remaining, 7% were heading to school, while the other 4% left for other reasons. In contrast, between 2007 and 2010, retirees made up a quarter of the six million people who left the labor force, while 18% were classified as disabled. About 57% were either in school or otherwise on the sidelines. ”

This suggests the current drop in the labor force is more structural in nature,” said Sharif. If so, there is less hope of luring people back to hunt for work as the jobs market tightens, as many Fed officials believed would be the case. And the U.S. central bank, which has held benchmark rates near zero since December 2008, will likely need to push them up sooner than they would have otherwise. “It is not clear whether the overall participation rate will increase anytime soon, given that the underlying downward trend due to retirements is likely to continue,” said Shigeru Fujita, an economist at the Federal Reserve Bank of Philadelphia.

• Spooked By Defaults, China Banks Begin Retreat From Risk (Reuters)

Some of China’s struggling firms are finally getting the reception that regulators have been hoping for — a cold shoulder from banks in the form of smaller and costlier loans. Reuters has contacted over 80 companies with elevated debt ratios or problems with overcapacity. Interviews with 15 that agreed to discuss their funding showed that more discriminate lending, long a missing ingredient of China’s economic transformation, has become a reality. Up against a cooling Chinese economy and signs that authorities will not step in every time a loan goes bad, banks are becoming more hard-nosed and selective about whom they lend to.

There are signs that even state-owned firms, in the past fawned over by lenders for their government connections, have to contend with higher rates, lower lending limits and more onerous checks by banks. “Interest rates are going up 10% for the entire industry,” said Wang Lei, a finance department manager at PKU HealthCare Corp. “Obtaining loans is getting difficult and expensive.”

PKU HealthCare, which is controlled by Peking University and makes bulk pharmaceuticals, has struggled to remain profitable. Its debt-to-EBITDA (earnings before interest, tax, depreciation and amortization) ratio exceeded 60 at the end of September, four times the average for listed Chinese companies from the sector.

To be sure, several companies with strong balance sheets and profits reported no significant changes in their funding conditions. That in itself is a welcome sign that banks are finally differentiating between the strong and the weak, more aware that they are on the hook for losses if businesses fail. China’s first-ever domestic bond default earlier this month when solar equipment maker Chaori Solar missed its payment and regulators refused to step in, drove that message home. “It was a wake-up call for lenders,” said Christopher Lee, managing director and the head of greater China corporate ratings at Standard & Poor’s. “There is no such thing as a risk-free investment.” [..]

Some gauges of China’s corporate debt are already flashing red. Non-financial firms’ debt jumped to 134% of China’s GDP in 2012 from 103% in 2007, according to Standard & Poor’s. It predicted China’s corporate debt will reach “stratospheric levels” and become the world’s largest, overtaking the United States this year or next. Fearing a wave of defaults as China’s economy cools after decades of rapid growth, regulators in the past two years told banks to cut off financing to sectors plagued by excess capacity such as steel and cement. [..]

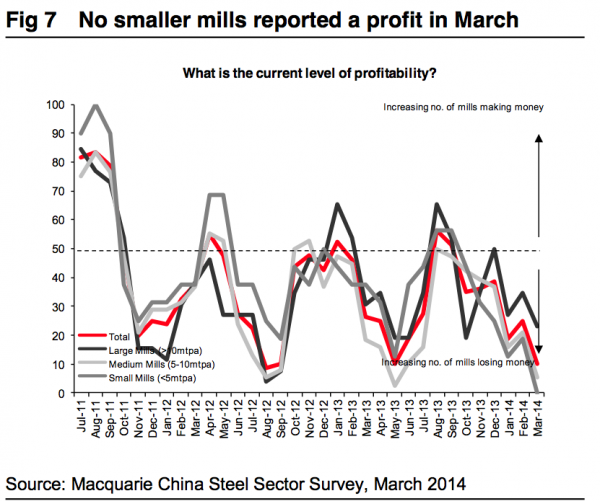

• Default Risks Surge At China Steel Mills (FT)

Chinese steel mills were suffering a medley of woes in mid-March as sales slowed, production levels slumped and profits plunged, according to an investment bank survey published on Tuesday that foreshadows the rising risk of debt defaults in the world’s largest steel producer.

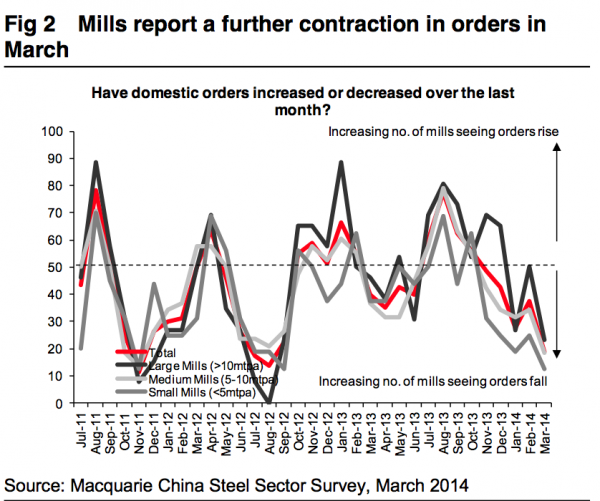

Macquarie Commodities Research, quoting a proprietary survey of Chinese steel mills and traders conducted in mid-March, found that large, medium and small steel mills were all enduring a contraction in orders compared to the same period in February, and profits had declined to historic lows.

“Looking at profitability, it is clear why the smaller mills are making the largest cuts (in production) – for the first time in the history of the steel survey not one smaller mill reported that they are making money,” a Macquarie report on the survey said (see chart).

Colin Hamilton, analyst at Macquarie Capital (Europe), said that March usually brought an improvement in the key metrics of steel orders, production levels and profits relative to February as the economy revs up following the Chinese new year holidays. This year, however, has been defined by the deepening gloom besetting the industry.

Macquarie researchHamilton said debt defaults in the steel industry are a distinct likelihood, given that Beijing is “trying to change the mindset” so that at least some of those companies that deserve to fail do fail.

“I don’t think the government would mind if we saw a few more defaults (in the steel industry),” Hamilton said, noting the failure of a privately-owned steel mill, Haixin Steel, to repay loans that fell due this month.

Speaking earlier this month following the default of a solar company on its bond interest payment, Li Keqiang, premier, said defaults were “unavoidable”, though he did not indicate which industries were most at risk.

Reinforcing the sense that economic activity thus far in March has been at a low-ebb, the HSBC manufacturing purchasing managers’ index, announced on Monday, fell for a fifth successive month to its lowest level since July last year. The month’s reading was 48.1, below the 50 point threshold that nominally divides contraction from expansion.

This is consistent with a contraction in steel orders seen in the Macquarie survey for all sizes of steel mill – large, medium and small (see chart).

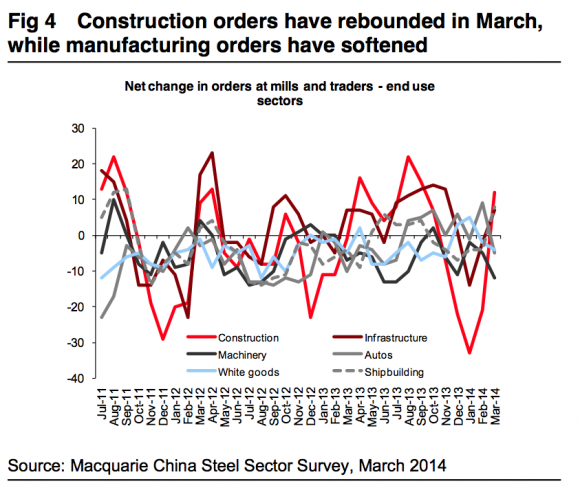

Macquarie Commodities ResearchHamilton said that although orders in aggregate were down in mid-March compared to mid-February, there were clear signs that construction-related orders for steel products have rebounded (see chart). This is likely to result in increased activity at small mills, whose fortunes are closely tied to construction.

Macquarie Commodities ResearchThe survey showed, unsurprisingly, that mills plan to purchase less iron ore over the next month than they did during the last survey. Iron ore inventory is still falling among smaller mills and is now also falling at mid-sized mills, while the larger mills have seen small increases, the report said.

For coking coal, purchasing plans are similar, with most mills indicating a desire to cut volumes – only the larger mills remain in the market. Combined coking coal imports across January and February were 7.9m tonnes, down 27 per cent year on year.

• Chinese Developers Seek Alternative Financing As Investors Grow Wary (Reuters)

China’s property developers are turning to commercial mortgage-backed securities and looking at other alternative financing as creditors grow more discriminating in the face of rising concerns about the country’s real estate and debt markets. Bond buyers are shying away from second-tier developers because property sales have cooled as the economy slows. The expected bankruptcy of a local developer and the country’s first domestic bond default this month have heightened scrutiny of borrowers.

The property companies have a renewed sense of urgency to raise capital after U.S. Federal Reserve Chairman Janet Yellen indicated the central bank, which sets the tone globally for borrowing costs, may raise interest rates as early as the spring of 2015, sooner than many investors had anticipated. Higher rates mean higher borrowing costs, both for the companies and for their home-buying customers.

Highlighting the search for alternative funding avenues, property fund MWREF Ltd earlier this month issued the first cross-border offering of commercial mortgage-backed securities (CMBS) since 2006. The offer was priced at a yield lower than two dollar bonds issued last week, IFR, a Thomson Reuters publication, said. “The market will see more of these products,” said Kim Eng Securities analyst Philip Tse in Hong Kong. “It’s getting harder to borrow with liquidity so tight in the bond market. It’s getting harder for smaller companies to issue high-yield bonds.”

The notes, issued through a MWREF subsidiary, Dynasty Property Investment, were ultimately backed by rental income from nine MWREF shopping malls in China and were structured to give offshore investors higher creditor status than is normally the case with foreign investors. MWREF is managed by Australian investment bank Macquarie Group Ltd.

The head of investor relations for Beijing Capital Land, which is mainly focused on middle- to high-end residential development and high-end commercial property, said the company would look at new ways to fund its business. Beijing Capital was the first Hong Kong-listed developer to issue dollar senior perpetual capital securities last year, an equity-like security that does not dilute existing shareholders. “As market liquidity is changing constantly, we have to keep adapting and exploring different funding channels,” said Bryan Feng, the head of investor relations.

Chinese regulators last week allowed developers Tianjin Tianbao Infrastructure Co. and Join.In Holding Co. to offer a private placement of shares, opening up a fund raising avenue that had been closed for nearly four years. New rules were also unveiled last week allowing certain companies to issue preferred shares, including companies that use proceeds to acquire rivals. “As liquidity tightens and developers see more pressure…they may consider M&A via preferred shares,” said Macquarie analyst David Ng.

• How Rumor Sparked Panic And Three-day Bank Run In Chinese City (Reuters)

The rumor spread quickly. A small rural lender in eastern China had turned down a customer’s request to withdraw 200,000 yuan ($32,200). Bankers and local officials say it never happened, but true or not the rumor was all it took to spark a run on a bank as the story passed quickly from person to person, among depositors, bystanders and even bank employees. Savers feared the bank in Yancheng, a city in Sheyang county, had run out of money and soon hundreds of customers had rushed to its doors demanding the withdrawal of their money despite assurances from regulators and the central bank that their money was safe.

The panic in a corner of the coastal Jiangsu province north of Shanghai, while isolated, struck a raw nerve and won national airplay, possibly reflecting public anxiety over China’s financial system after the country’s first domestic bond default this month shattered assumptions the government would always step in to prevent institutions from collapsing. Rumors also find especially fertile ground here after the failure last January of some less-regulated rural credit co-operatives.

Jin Wenjun saw the drama unfold. He started to notice more people than usual arriving at the Jiangsu Sheyang Rural Commercial Bank next door to his liquor store on Monday afternoon. By evening there were hundreds spilling out into the courtyard in front of the bank in this rural town near a high-tech park surrounded by rice and rape plant fields. Bank officials tried to assure the depositors that there was enough money to go around, but the crowd kept growing. In response, local officials and bank managers kept branches open 24 hours a day and trucked in cash by armored vehicle to satisfy hundreds of customers, some of whom brought large baskets to carry their cash out of the bank.

Jin found himself at the bank branch just after midnight to withdraw 95,000 yuan for his friend from a village 20 kms (12 miles) away. “He was uncomfortable. It was late and he couldn’t wait, so he left me his ID card to withdraw his cash,” Jin said. By Tuesday, the crisis of confidence had engulfed another bank, the nearby Rural Commercial Bank of Huanghai. “One person passed on the news to 10 people, 10 people passed it to 100, and that turned into something pretty terrifying,” said Miao Dongmei, a customer of the Sheyang bank who owns an infant supply store across the street from the first branch to be hit by the run. [..]

• IMF announces $14-$18 billion rescue for Ukraine (AFP)

The International Monetary Fund announced on Thursday a $14-$18 billion bailout for Ukraine to avert bankruptcy for the crisis-hit country amid its escalating standoff with Russia. The agreement in principle, worth the equivalent of 10.8-13.1 billion euros, is tied to tough reform conditions which will have a big impact on the Ukrainian economy and people.

The Fund’s Ukrainian mission chief Nikolai Georgiyev said the rescue would form the central part of a broader package released by other governments and agencies amounting to $27 billion (19.6 billion euros) over the next two years. Georgiyev said the actual size of the “standby agreement” would be determined only once the new Western-backed leaders of Ukraine implemented the reforms the Fund had sought in vain from the cabinet of Kremlin-backed president Viktor Yanukovych.

That government was toppled in February by three months of protests. “The programme will be approved by the IMF board when the steps that I mentioned are implemented,” Georgiyev told reporters after holding a decisive round of talks with Ukrainian President Arseniy Yatsenyuk on Wednesday. “We expect (the approval) by the end of April.”

The package announced by the Fund is only slightly smaller than that $15-20 billion (10.9-14.5 billion euros) requested by the former Soviet state’s new leaders when Georgiyev’s mission first arrived in Kiev on March 4. The Fund has made an immediate end to Ukraine’s costly gas subsidies one of its main conditions for the programme’s approval It also wants the central bank to stop propping up the Ukrainian currency and for the government to cut down on corruption and red tape.

Georgiyev called these two steps as a more committed effort to fight bureaucratic red tape and state corruption “the foundation for stable and sustainable growth”. The IMF programme was announced one day after the Ukraine’s state energy company Naftogaz said it would increase domestic heating gas prices by 50% on May 1. Naftogaz added that rates for district heating companies would go up by 40% on July 1 and that further rate increases were likely in the coming years. [..]

• European Banks Feel Effects Of Crimea Crisis, Austria Bears Brunt (NY Times)

After the Cold War ended in the early 1990s, Viennese banks pushed aggressively into the newly open markets of Eastern Europe, as if rebuilding the old Hapsburg Empire one A.T.M. at a time. The banks of Vienna were not the only Western lenders seeking to stake out the former Soviet bloc, of course. But the Austrians, for reasons of geography and history, bet big on Eastern Europe and Russia. Now, as regional tensions with Russia rise, Austrian banks risk being caught in the financial and geopolitical crossfire.

The way things play out for Austria could have implications for the broader European Union, whose members since the outbreak of the Crimean crisis have urged caution in imposing sanctions. The worst case is that European banks would lose their subsidiaries in Russia amid escalating tit-for-tat reprisals or that it would become impossible to do business there. Whatever happens, analysts expect any Western banks with a presence in Russia — including American ones like Citigroup and JPMorgan Chase — to have their profits squeezed in a market that until recently had been quite lucrative.

All told, the European banks are vulnerable to Russia for about $194 billion, according to Deutsche Bank, compared with about $37 billion for American banks. The financial links to Russia help explain why Europeans have been reluctant to impose sanctions. For Europe as a whole, there is also a danger that the crisis will ricochet back in ways that are impossible to predict. “We keep a close eye on potential indirect effects, as they might have a more substantial impact than direct exposures to these countries,” said Andreas Dombret, a member of the executive board of the Bundesbank, the German central bank.

For Austria, the effects are direct — and already being felt. Two of the country’s biggest banks — Raiffeisen Bank International and Bank Austria, a unit of the Italian lender UniCredit — have large Ukrainian and Russian operations. While other European banks are also present in Russia, notably the French bank Société Générale, Austria’s exposure — nearly $17 billion — is the largest in relation to the overall size of its banking system, at 1.4% of assets.

The exposure would be even larger if the Erste Group, Austria’s biggest bank by assets ahead of Bank Austria and Raiffeisen, had not left Ukraine last year. It was part of an exodus from Ukraine and Russia by foreign investors discouraged by corruption and poor economic growth in those countries. Well before Russia annexed the Crimean peninsula, Raiffeisen and Bank Austria were plagued by a surge in bad loans and sinking profitability throughout Eastern Europe. Nearly a third of Raiffeisen’s approximately 1.2 billion euros worth of loans in Ukraine are classified as being in default or in arrears.

• Merkel Not Ready To Back Economic Sanctions Against Russia (RT)

The West has not yet reached a stage where it will be ready to impose economic sanctions on Russia, German Chancellor Angela Merkel said, stressing that she hopes for a political solution to the stalemate over Ukraine crisis. The chancellor said she is “not interested in escalation” of tensions with Russia, speaking after Wednesday meeting with the South Korean president in Berlin. “On the contrary, I am working on de-escalation of the situation,” she added, as cited by Itar-Tass. Merkel believes that the West “has not reached a stage that implies the imposition of economic sanctions” against Russia, advocated by US President Barack Obama. “And I hope we will be able to avoid it,” she said.

Berlin is very much dependent on economic ties with Russia with bilateral trade volume equaling to some 76 billion euros in 2013. Further around 6,000 German firms and over 300,000 jobs are dependent on Russian partners with the overall investment volume of 20 billion euros. Germany is currently the European Union’s biggest exporter to Russia. German car manufacturing companies are likely to suffer first if sanctions against Russia become more substantial, as about half of German exports to Russia are vehicles and machinery.

Volkswagen, BMW, and lorry maker MAN all have Russian operations, with VW willing to inject another €1.8 billion in its Eastern European segment by 2018, the Local reports. Opel, a German car maker which sold over 80,000 cars in Russia in 2013, last week said that the company was “already feeling the stresses and strains from the changing course of the ruble,” Karl-Thomas Neumann, boss of car makers Opel, told Automobilwoche magazine. On the retail side, German Metro stores wanted to take its Russian subsidiary public this year, but the plan is now imperiled, Der Spiegel reported.

Earlier this month Germany’s KfW development bank canceled a contract with Russia’s VEB bank worth €900 million in investment initiatives for mid-sized companies. Under the deal Germans were to have invested €200 million in Russia. In addition, Germany is heavily dependent on Russian energy with around 35% of its natural gas imports coming from Russia.

• Russia’s actions in Crimea ‘completely understandable’ – German ex-chancellor (RT)

Moscow’s actions in the Crimea are comprehensible, former German chancellor, Helmut Schmidt said, criticizing the Western reaction to the peninsula’s reunification with Russia. President Vladimir Putin’s approach to the Crimean issue is “completely understandable,” Schmidt wrote in Die Zeit newspaper where he’s employed as an editor. While the sanctions, which target individual Russian politicians and businessmen, employed by the EU and the US against Russia are “a stupid idea,” he added.

The current restrictive measures are of symbolic nature, but if more serious economic sanctions are introduced “they’ll hit the West as hard as Russia,” Schmidt warned. He also believes that the refusal of the Western countries to cooperate with Russia in the framework of the G8 is a wrong decision. “It would’ve been ideal to get together now. It would certainly do a lot more to promotion of peace than the threats of sanctions,” the ex-chancellor explained. But the G8 itself isn’t that as important as the G20, in which Russia remains a member, he added.

According to Schmidt, the situation in Ukraine is “dangerous because the West is terribly upset” and it’s “agitation” leads to “corresponding agitation among Russian public opinion and political circles. The ex-chancellor refused to speculate of the possibility of Russian troop deployment to eastern parts of Ukraine, but added that the West “shouldn’t fuel Russia’s appetites.”

• Fed Rejects Five Banks’ Capital Plans (WaPo)

Citigroup and two banks with substantial Massachusetts operations, Santander and RBS Citizens, are facing questions about their ability to ride out another calamity in the financial markets. The Federal Reserve said Wednesday the banks, plus British giant HSBC and Zions Bank, need to resubmit their proposals to pay billions of dollars to shareholders after officials said they found weaknesses in their capital plans. The other 25 banks subject to the review were given approval to move ahead with plans to increase their dividend payouts, which analysts have pegged at about $75 billion.

In the aftermath of the financial crisis, regulators insisted that banks sock away enough capital — cash, investor equity, and other assets — to cushion against losses and stave off future taxpayer bailouts. Congress mandated that regulators give banks an annual checkup and granted the authority to stop banks from paying out capital in the form of dividends, stock buybacks, and other practices.

As an improving economy and deep cost cuts bolster profits, banks have been eager to lavish investors with excess capital. Regulators remain cautious about such plans. ‘‘With each year we have seen broad improvement in the industry’s ability to assess its capital needs,’’ Fed Governor Daniel Tarullo said. ‘‘However, both the firms and supervisors have more work to do as we continue to raise expectations for the quality of risk management in the nation’s largest banks.’’

RBS Citizens and Santander are the second- and third-largest retail banks in Massachusetts. Both banks had capital cushions above the Federal Reserve’s requirements. The Fed, however, found that Citizens lacked the appropriate practices for estimating revenue and losses under severe economic and financial market stress. The Fed objected to Santander’s plan to increase dividend payments to its shareholders, which would reduce the bank’s capital because of deficiencies in how the bank identified and managed risk. Both banks are subsidiaries of European companies. Citzens is a unit of Edinburgh-based Royal Bank of Scotland. Santander Holdings USA, based in Boston, is owned by Spanish financial giant Santander SA. [..]

• Fed’s Bullard Sees Bubble Ahead (MarketWatch)

St. Louis Federal Reserve Bank President James Bullard said Thursday that the key risk for U.S. economy would be a bubble forming as the central bank removes monetary-policy accommodations, while he also raised concerns about financial stability in the U.S. economy. “I don’t see a major bubble right now, but one will form as we are trying to remove the accommodation in the years ahead, because that’s what exactly had happened in the 2004-2006 period,” Bullard told the Credit Suisse Asian Investment Conference in Hong Kong. “I do think that’s a key risk going forward,” he said.

Bullard related the risk to the situation in 2006, the housing prices had already started to peak at the same time as the central bank was in a tightening cycle. “Just because you are moving away accomodation doesn’t mean the risk of bubble forming is going away,” he said. Bullard also emphasized that financial stability concerns are “looming large,” as policy makers are thinking about how to accommodate those concerns. He said macroprudential tools, which have been strengthened, can be used to address emerging bubbles. Bullard is a non-voting member of Federal Open Market Committee this year.

• Housing Boom To Drag UK Back Into Crisis (Telegraph)

Britain’s property obsession has left the country at risk of another major financial shock, the former head of the City watchdog has warned. Lord Adair Turner, the ex-chairman of the Financial Services Authority (FSA), said mortgage and commercial property lending in advanced economies had played a “central role” in almost all financial crises and post-crisis recessions.

Much of the investment in the advanced world was now focused on real estate, he added. While he said this was an inevitable part of a modern economy, it also increased the risk of another boom and bust. “We have made it incredibly favourable to buy houses,” Lord Turner told The Telegraph. “The supply issue is very important and we’ve got to increase the supply of housing because otherwise we are just piling up very strong incentives to buy housing, very strong incentives to borrow money to buy housing but against a fixed supply. “If you do that the only thing that can give is the price.”

Lord Turner also said he was “worried” that the UK was “developing a recovery which is simply returning to the very issues that led us to this problem in the first place. “Even the Office for Budget Responsibility has said the only way we’re going to get growth back in the next five years is for the [debt to income ratio] to go all the way back to 170pc again. If in five years time debt has gone back up to 170pc, and if interest rates have returned to 3pc, 4pc or 5pc, then a lot of people are going to be struggling.”

• Spain’s Oil Deposits And Fracking Sites Trigger Energy Gold Rush (Guardian)

Spain is already the world’s largest olive oil producer but now it’s looking to a very different kind of oil to pull it out of economic decline: petroleum. The discovery of two significant offshore deposits, and prospects for fracking in many areas, have triggered a black-gold rush, with demand for exploration permits up 35% since 2012. A report published this week by Deloitte says the oil industry could create 250,000 jobs and constitute 4.3% of GDP by 2065. The report is based on an estimate of 2bn barrels of oil and 2.5bn cubic metres of gas.

The oil companies estimate that the deposits in a series of oilfields off the Canaries, the latest of which was confirmed last week, amount to 500m barrels of crude. Deloitte predicts that Spain could become a gas exporter by 2031 while producing 20% of the oil it consumes. With 6 million people unemployed and an economy that shows only feeble signs of recovery, the Spanish government seems ready to brush aside environmental concerns and give the green light to the oil companies. These are led by the Aberdeen-based oil and gas exploration company Cairn Energy and the Anglo-Turkish firm Genel Energy, headed by the former BP boss Tony Hayward. So far, 70 licences have been granted to explore both shale gas and conventional resources.

The main offshore deposits lie between Lanzarote, in the Canary Islands, and Morocco, and in the Bay of Valencia, close to Ibiza. As both the Canaries and Ibiza are places of great natural beauty whose principal industry is tourism, there is intense opposition to the plans. Opposition is so fierce in Ibiza that the Eivissa diu no (Ibiza says no) movement has succeeded in creating a united front across the entire political spectrum, taking in environmental groups and hoteliers, and has won the support of celebrities [..]

Last month, more than 20,000 people marched in Ibiza (which has a population of 132,000) to oppose the exploration, and thousands signed a petition to the European commission demanding a halt to sonic exploration that was producing 250-decibel booms every 10 seconds, day and night, over a period of three months. As well as breaking the safe limit, of 180 decibels, the booms damage fisheries and bird life, the protesters say. David Sala, a spokesman for the Ibiza says no movement, said: “Just because we have the technology to exploit nature, we can’t continue to use technology that destroys the environment and, by extension, ourselves.”

Paulino Rivero, president of the Canary Islands regional government, wrote to the Spanish prime minister, Mariano Rajoy, last month telling him that he plans to hold a referendum on the issue, posing the question: “Do you agree with the oil exploration off the coast of our islands authorised by the multinational Repsol?” The Spanish government’s only response was to remind Rivero that referendums are illegal under the constitution.

Spain depends on imports for 99% of its oil and gas needs. Aside from some coal mines in the north, the country, has never been blessed with energy resources. It has a highly developed hydroelectricity industry – only China and the U.S. have built more dams – and its ageing nuclear power stations meet 20% of demand. Until recently, it was investing heavily in renewables. Wind power now provides 20% of the grid and solar 3%, but the current government has lost its enthusiasm for renewables, and has made drastic cuts in subsidies.

Home › Forums › Debt Rattle Mar 27 2014: How The West Went To War