davefairtex

Forum Replies Created

-

AuthorPosts

-

davefairtex

ParticipantIlargi –

“Gold and Silver. With 30% losses over the past 2 years, it is now official that for most people it’s been a bad advice for a long time.”

Calling this “bad advice for a long time” reminds me of how smug those goldbugs acted when silver hit 50. Its probably wise to wait until the full market cycle is complete before taking a victory lap. As we know, two years of downward move (or in the case of SPX, four years of move off the lows of 666) does not a complete cycle make.

ParticipantViscount –

“Mish, you didn’t invest. You gambled and you lost.”

I’m not sure why you are blessing us with a note clearly addressed to Mish. Perhaps sending it to him directly would be a more effective way to communicate with him?

ParticipantIlargi –

Armstrong basically agrees with what you just said – at least a version of it. He says there are a large number of dollar short positions out there, and so if we take what you two are saying together, the money fleeing the emerging markets is going to unwind these shorts. That deflation is rapid financial-market deflation rather than the stuff associated with more normal mortgage, business, and consumer loan deflation, so it appears in the market prices (including commodities – including gold) in real time.

It will be particularly interesting to see the NYSE margin data covering this period. Pity it lags by a month. It will help to confirm the hypothesis.

One of the indicators of the start of the 2008 downturn was a downturn in NYSE margin loans.

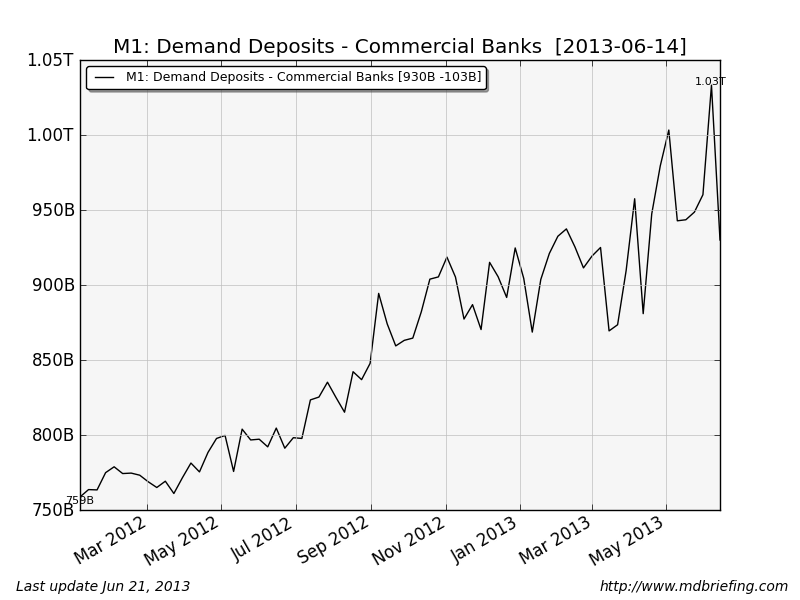

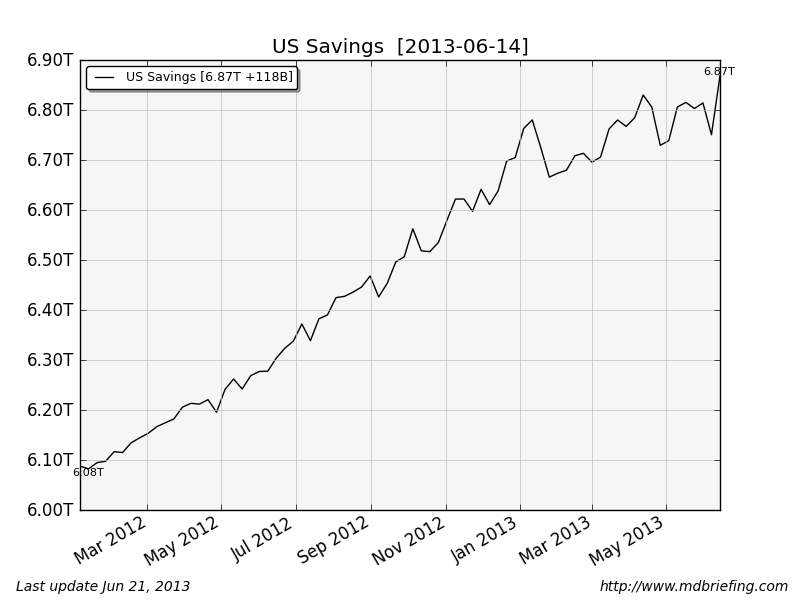

After watching how various reporters (and even otherwise really smart analysts) use FRED timeseries, I’ve come to the conclusion that sometimes they really don’t know what they’re doing. Or – they look at one particular area without attempting to understand the system as a whole. That’s what I think happened with Ambrose and his M1 chart. If you look at M2, you’ll see that the money supply including savings accounts is actually tracking up.

I agree with you about the velocity. Printed money acts to inflate the bond market, and then goes to sleep in Excess Reserves where it gets 0.25% – beating 3 month treasury yields of 0.06%.

Speaking of which, that’s another FRED chart I object to. The hyperinflationists use the BASE money chart (which includes excess reserves) to suggest hyperinflation is inevitable. Its not saying that at all. Excess Reserves is all about getting 0.25% at the Fed rather than 0.06% at the Treasury or 0.12% by lending it overnight to some other random bank that you probably don’t trust anyway.

ParticipantSo you guys all know I’m a chart guy. I was intrigued by the chart of US M1 and dug into it deeper to figure out what was going on.

Turns out, the issue was Demand Deposits at Commercial Banks.

Then I dug into it a little deeper, and noticed that the 108 billion dollars in demand deposits that vanished, seemed to appear in the savings accounts at commercial banks! It turns out that SAVINGS isn’t just savings, but its also money market deposit accounts, and the like.

Deflation is still happening, I believe – but this chart isn’t the smoking gun. All the commodities dropping, bonds dropping, and equity markets dropping at the same time – that’s the smoking gun.

Likely international capital flows are an important component of this as well. If we chart forex rates in the emerging markets, we can see that money is fleeing there, and running to Japan and the US. But clearly not into US bonds or equity, likely into cash vehicles of some sort.

Although, oddly, its not showing up in demand deposits, as I would expect. Where all that money is going is a bit of a mystery. However, its not a mystery as to where it is coming from, or what effect the capital flight is having on the markets.

I also think emerging market central banks are selling treasury bond holdings in an attempt to limit the change in rates. I’m positive that’s happening in Brazil. These guys have massive US treasury holdings, and their sales are (again likely) swamping Fed QE buying, causing our rates to rise.

ParticipantI think the dollar demise will await the failure of other, less systemically important nations. Failure moves from the periphery to the core – but only after the periphery has taken its beating first.

The grand move in the US stock market is partially about international capital flows into the US (which have reversed recently), and partially about extremely low interest rates being very profitable for US companies. Along with low wages paid to US employees too, of course. They sell a lot of stuff overseas, pay low interest rates, pay low wages, and as a result make historically better-than-average profits. So naturally the stock market goes up.

I’m watching the indicators; we aren’t quite yet there for a move down, but things are definitely looking worrisome. Projections of 10-year annual returns are currently predicted to be about 3.5%/year (based on two different methods – both of which have done well historically in predicting longer term market returns), including dividends of 2.2% that says SPX will likely be only 15% higher 10 years from now. Given the market’s annoying habit of dropping 30-40% during corrections, this would seem to be a bad bargain. Or more colloquially, picking up nickels in front of steamrollers.

And I believe these projections to be optimistic, since the models have never experienced peak oil, etc.

However, only one of my five indicators has turned down. Patience.

ParticipantMy guess is, the current US equity market buoyancy is about significant money flows from overseas. I say this because at least lately, while the SPX goes up, the US dollar is also going up too. If you imagine that world money is a zero sum game (long term it isn’t, but in the short term it is) for the US market to rise, that money has to “come from” somewhere else to bid the prices higher.

Could be cash, bonds, or international flows.

My claim is, money is coming from Japan and Europe. (I’d think China too, but that’s not supported by currency movements).

This tallies with Armstrong’s claims that money will flow from periphery to core as things get worse. Its not evidence of hyperinflation, its evidence of capital flight.

In the modern age, inflation is caused by private borrowing (i.e. an increase in bank credit) which largely isn’t happening right now. Government printing such as it is blows an asset bubble in the place where it ends up going – namely bonds – and then ends up parking in Excess Reserves which have zero velocity, hence the declining M2V.

Excess Reserves (Base Money) aren’t any more powerful than regular money because the Reserve theory of central banking isn’t correct.

Its risky right now to attempt to “front-run” central banks (assuming they are buying) and buy equities at their all-time highs. Same thing with bonds at the tag end of a 30 year bull market. Just my opinion.

ParticipantThanks for all the replies. I guess we are one hundred blind men all trying to describe the elephant by touch – but what other way can we find wisdom in this world except through sharing personal experience?

Today I was reminded of this in my class. After a long discussion (where I got to learn new words like “unemployed” and “fired”) my teacher finally asked me, “if there are so many people not working in America, why does everyone want to go there?”

On the one hand, statistics. Perhaps 15% actual unemployed/underemployed in the US versus 0.5% unemployed in my current country of residence. On the other hand, my friend, who landed at JFK with about $500 a year ago, found a job working under the table at a restaurant in about two weeks. For quite some time, he lived in an “apartment” (about 100 sq ft) for perhaps $250/month. Did you know you could find such a place in Queens for $250/month? I certainly didn’t. Now he’s about to enroll at a junior college. This is not an unusual story – its actually a common one. My teacher knowing this asked me, “is everyone in America lazy?”

An interesting question, especially coming from Asia where the unemployment rate might be 0.5%, but the hours are long and – to put it bluntly, if you don’t work (and your family isn’t there to rescue your ass), you don’t eat. What could I tell her? Americans are habituated to serving the machine? Debt sucks up any excess wealth?

How do you explain such a situation to someone who would, most likely, do well in such an environment if parachuted in by some accident of fate?

Unfortunately, my vocabulary failed me. I could not explain. Then again, I’m not even sure if it were all in English I could have explained.

What does this have to do with the Euro? I’m not sure. I get the sense that the Europeans don’t particularly want to go back to status quo ante – cold war, nationalism, wars of 1914, 1939, and the poverty of the periphery that somehow got magically fixed by credit and the harmonization of the continent that somehow made it more acceptable for a guy in Germany to buy a beach house in Spain whereby both sides felt they gained.

There’s something in the eurozone that we shouldn’t lose, I feel. How can we keep the good stuff and toss out the stuff that clearly doesn’t work? Is it even possible?

ParticipantIt occurs to me that instead of lambasting people for wanting to stay inside the eurozone, we might want to figure out why they want to stay there.

Is it the freedom to travel within the zone?

The ability to escape your current (lame) economy?

The ability to move your money to someplace safe? (ex Cyprus)

Having the Germans manage your Central Bank, ensuring your savings doesn’t vanish in a flurry of printing?

The protection of being under the protection of such a big state, in a region that’s had a long history of war?

US size-envy?What is it about the eurozone that keeps people from just chucking it all out?

I’m not advocating a position, I’m really curious – and since I don’t live there, my speculations are even less informed than they usually are.

ParticipantZombie money. I like it.

Perhaps that’s why interest rates are so low. All that zombie money floating around looking for yield, looking for a place to hide. Money vastly in excess of actual savings or surplus, extracted from the bubble, kept alive through extend and pretend, only partially attached to actual income able to service the attached debt.

Its an interesting concept.

April 21, 2013 at 10:54 am in reply to: Nicole Foss In Australia: It's No Use Trying To Build A Better Dinosaur #7455ParticipantThe Fed is a bank. All the big players have accounts. Imagine you are one of them, and you own 100 billion in treasury bills. The Fed comes to you one day and says “gosh I’d like to buy those treasury bills from youu, and in exchange, I’ll give you 100 billion dollars.” You agree.

How does the Fed pay you? It credits your account at the Fed with 100 billion dollars.

Where did it get this “money” from? It didn’t. It just changed the numbers in your account – in the “up” direction. That’s the Fed’s super power. It can credit anyone’s account with any amount it feels like.

Of course the rules of the game require the Fed to account for all this crediting.

Now then, as the seller you *could* use this money to buy stuff with. You could withdraw this money from your account, and buy buildings, or bribe congressmen, or whatever. Or you could keep it at the account at the Fed. $1 in new credit money in your Fed account spends exactly the same as the green FRN in your pocket that you earned selling apples on the street.

Of course, by crediting your account with $100 billion new dollars of “credit money” the Fed instantaneously reduces the value of dollars everywhere by some percentage. More credit money is “out there” now, and no new things were created. That devaluation is why people call it “money printing” and they object to it.

April 17, 2013 at 12:07 am in reply to: Nicole Foss In Australia: It's No Use Trying To Build A Better Dinosaur #7428ParticipantHelen –

Did you listen to the interview? I did. Nicole didn’t talk about lowering carbon footprints, she spoke about finance and effectively trying to get ordinary people to realize that they’d better start claiming some of the real wealth before their claims vanish.

Reminds me of a student answering a question in class without actually reading or understanding the material. Said student ends up looking silly. Doesn’t help the credibility of the atta-boy for whoever Rob Hopkins is, either.

ParticipantTriv –

If you don’t go for my “an appearance of an Appeal to Authority” concept, that’s perfectly ok with me. I was simply trying to humbly suggest a way for you to communicate your important message more effectively – with more power, if you will – and I tried to put it in language you might appreciate. Clearly I did not succeed in doing this. I’ll try once more.

It is still my opinion that a large number of quotes in an article tends to obscure meaning rather than illuminate, and it conveys the feeling (to me at least) that the author feels he needs help from elsewhere to make his point. This isn’t up for debate – it’s how I feel. Clearly you feel differently, and that’s ok! Nobody will ever “win” this debate, because its just two opinions. (I only make this point because it appears that you do view this as a debate that can be won rather than just two people’s opinions)

To my mind, a room full of 100 items on 10 tables makes it more difficult to actually see and appreciate any one item. That same room, with 1 item on 1 table – that 1 item really stands out. Sometimes, less really is more. But I have friends that have a room with 10 tables full of 100 knicknacks. Not my style, but perhaps it is yours.

Perhaps – to put it in your language – a bit of icing is a tasty accent, but a whole lot of icing makes everything taste like icing. And the more quotes I run into in an article, the quicker I zone out. Now that’s just me, but is that really the effect you are looking for?

Again, my opinion. This is the last time I’ll mention it! I’m really just trying to help, and I recognize its all just based on my opinion. Apologies if I have offended.

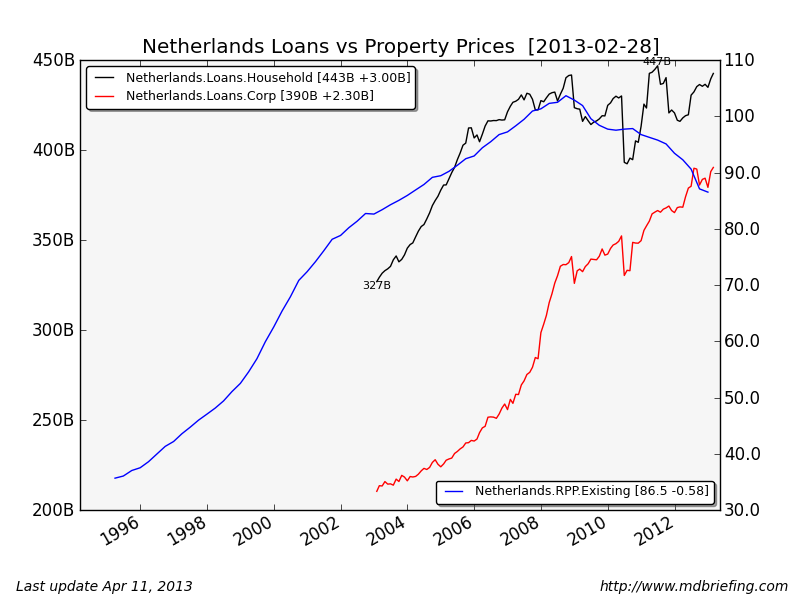

ParticipantOk, I know you’re all secretly wishing you had a CHART to tell you what’s really going on in the Netherlands. So here it is! The only sad part of the tale is, I don’t have data for the loans going back any further than 2003, so we can’t see as clear a correlation with debt and property values as we’d like.

Still, you can get an idea of the size of the property bubble (blue line, right axis = residential property prices), and how much popping it has done to date. Since this is Ilargi’s article, I’ve given him his property data going back to 1995. He likes his bubbles as large as possible! Kidding Ilargi.

The Netherlands is actually one of my “property bubble” cases on my eurozone property page.

https://mdbriefing.com/eu-rpp.shtml

Participant

ParticipantTriv –

One comment. Fewer quotes are better. Employing a bucketload of quotes in my opinion gives your post the unfortunate appearance of an Appeal to Authority, as if your facts alone aren’t able to stand on their own.

Participantbackwards –

Thanks for your kind words!

It does indeed appear that there is an actual conspiracy here – one where a significant percentage of well-connected deposits were given time to flee prior to the denouement.

In retrospect, it was very interesting how much talk there was initially about Russian Mobsters. I think they ended up being the useful distraction – and perhaps even the bag-holders. No mention was made of the hot money from the eurozone banks that had already left. I guess that would have spoiled the whole thing though.

The Dog that Didn’t Bark, as it were.

ParticipantT-Bear –

Please stop acting like a troll. I think Trivium is sometimes interesting, and sometimes a bit eccentric, but he’s usually polite – and polite discourse is the mark of a civilized man.

I certainly prefer to read his stuff over yours.

Just my opinion.

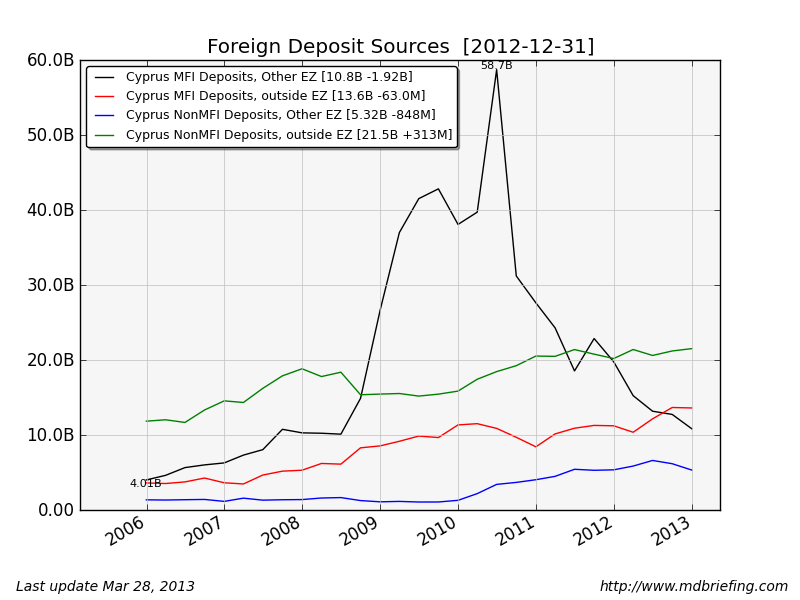

ParticipantI have been doing a lot of work in recent days poring over charts of the deposits of the banks in the eurozone. And I have some interesting conclusions.

There are 3 main groups with bank deposits: other banks, households, and corporations.

1) Households tend to be quite slow – last even – to move deposits

2) Banks tend to be very fast to move deposits.

3) Corporations fall somewhere in between.So homeowners deposit money mostly for safety and partially for interest, corporations do it for both safety and ease of doing business – but why do banks deposit money in other banks? It almost doesn’t make sense.

Its all about higher interest rates. If you are a German bank, paying very low rates (0.55%) for your overnight deposits, you can (if you are a nimble and clever banker) deposit those same funds in a Cyprus bank and receive quite a bit more. How much more? Depends on the risk you want to take:

German Overnight Deposit: 0.55%

Cyprus Overnight Deposit: 1.1%

Cyprus Savings Deposit: 2.8% (1 year, redeemable at notice)

Cyprus Time Deposit: 4.9% (1 year, agreed maturity)And if the Bank of Cyprus doesn’t go under, this is FREE MONEY. Its what bankers do – “make the spread”.

So with this in mind, take a look at the following chart of “foreign deposit sources” in Cyprus.

Black line: Eurozone Banks

Green line: Companies & people outside the EZ (Russian Mobsters, British…Mobsters?)

Red line: Banks outside the eurozone

Blue line: Companies & people within the EZ

Look how rapidly the black line has plummeted!

My guess is, banker overnight deposits were removed rapidly, while banker time deposits left more slowly. But the goal was, for the eurozone bankers to retrieve all their money, prior to the bail-in.

I have always wondered “why wait” to resolve these banks? If we know the banks in Cyprus are in trouble, why play games?

If you had control over the process, and didn’t want your (CORE) banks to suffer losses (since they would most definitely be “uninsured depositors”), putting off resolution until those cross-border deposits were all safely back home would make a great deal of sense. And then once they were gone – bam. The gate comes down.

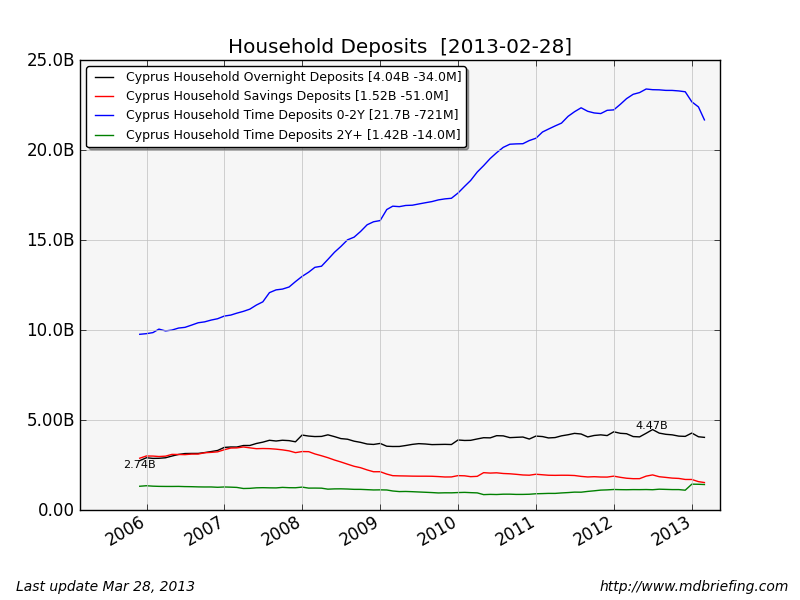

In contrast to how the foreign banks reacted, here’s what the households did in Cyprus – the regular people.

Participant

ParticipantSkip’s point is a good one. Gold may be money (in that its a store of value) but it acts more like a foreign currency at the shopping center. Namely, to spend it, you must first

a) convert it into the local currency, and when this happens, you

b) receive a variable-sized haircut on its quoted valueThat’s because we’re not on the gold standard any longer – when exchange rates were fixed between gold and the dollar.

And the less cash there is – say we have a bank holiday – the bigger the haircut will be for people trying to sell gold.

But even today when things are calm you expect to lose 3% on the spread for gold eagles.

I’m not saying gold is bad, far from it. But I’m saying “gold is not money.” Take your gold bar to Whole Foods and see just how much you can get. Same reaction if you take a stack of Yen. “WTF is this, and can you please bring me some dollars?”

Everything has its place – and I totally agree with Skip, cash has its own merits, and it is not to be sneered at. And at the point that it becomes obvious that it is important – it will be way, way too late to get some.

Participantgurusid –

Amen. I absolutely love that routine.

“An argument isn’t just saying NO IT ISN’T!”

“Yes it is.”

“NO IT ISN’T!!”And when I notice myself participating in and/or contributing to that completely ego-driven chest-beating I’m-right-you’re-wrong dynamic…time to withdraw and use my energy for something more productive/constructive. Like watching my favorite Monty Python skits, for instance!

By the way skipbreakfast – nice topic!

ParticipantAlan –

I can see this will turn into one of those “internet discussions” I love so much.

If you had a chart or two – or even a fact or two – I might continue. If you were a seeker after the truth, ditto. But as it stands now, I think I’ll bow out now. You win, you’re much smarter than me, congratulations!

Best of luck shorting the buck.

Participantalan –

I’m passingly familiar with the whole “big money is gonna” argument regarding how it will eventually run and hide in gold.

The 17 trillion euros in deposits, and the additional 17 trillion euros currently in euro-denominated bonds cannot possibly fit into the gold market. There’s just not enough liquidity there.

My guess is rather than trying to race through the tiny door, they’ll go for the bigger one the way they always have done – US treasury bonds. Its a deep, liquid market, freely available and indeed, getting bigger every day. Analysts who live in the US sometimes focus on the problems here, without realizing that problems elsewhere are much, much worse.

I recognize this is solely my own opinion and not based on anything other than observing marginal market movements in these two areas over the past five years of turbulence.

Rather than the Big Money, I think it’s the medium-sized money that will end up in physical gold. People who could conceivably cart a reasonable fraction of their personal wealth in the trunk of their car may well choose gold as a part of their “go to hell” plan, especially as confiscation increases, repression increases, state surveillance increases, and interest rates remain at 0%. That makes sense to me.

Gold’s big win: portability, concentrated wealth, international acceptance, hedge against government repression. But once you get into the ton weight range of anything ($100 bills: $90 million/ton, gold: $38 million/ton, silver $684k/ton, nickel $7k/ton) its no longer portable and/or concealable. At that scale the hedge factor no longer works. You can’t swim the Rio Grande with a ton of anything.

I will say though, the concept of having 10 tons of nickels in your backyard does have one virtue: any thief who wanted to steal them would take a LONG TIME and a LOT OF WORK to remove them from your place. But converting the value yourself – somewhat problematic. At $3.70/pound, buying many food items likely requires more pounds of nickel than you will receive in food!

I suppose its good exercise though. But I can only imagine the looks the cashiers at your favorite store will give you when you arrive with your $100 (26 pounds) in nickels *again* this week.

If you make money with your nickel storage plan, I say: you earned it.

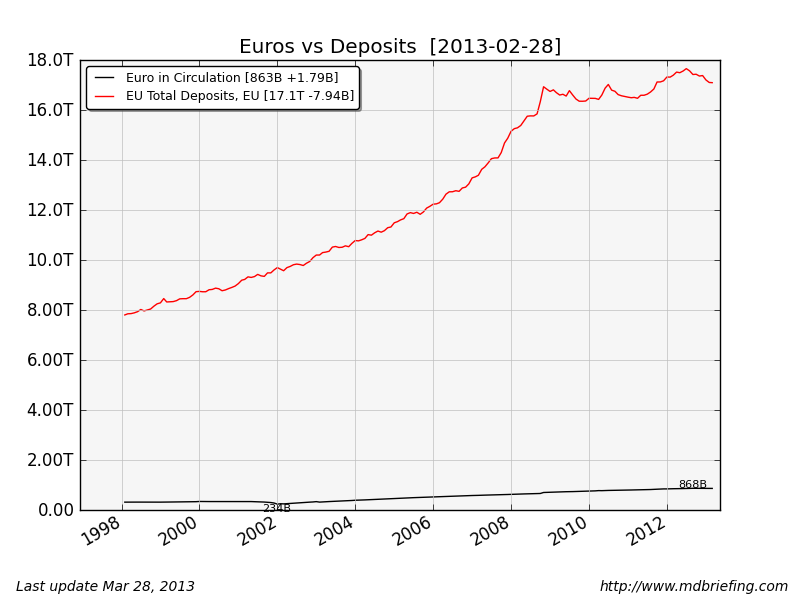

ParticipantSkip is right about cash. Here’s a chart (naturally) showing total currency and total eurozone bank deposits.

For the math-impaired, that’s about 20 euros in deposits for every euro in cash.

ParticipantIt is a bit alarming to see how well Mr Wilders is doing, and while Holland is actually faring relatively well. If and when things take a turn for the worse, I suspect he would only gain support.

When mainstream politicans are seen clearly to be bought off by the moneyed interests its the fringe that the people end up turning towards. Sometimes the fringe can be good, and other times, not so much.

ParticipantLooks like after all that was said and done, they’ve decided to resolve the two ill banks in Cyprus the standard way, with insured depositors being protected, bondholders and uninsured depositors taking losses together. Amazing! It’s a first!

What’s more, normal savers in OTHER Cyprus banks aren’t having to pay for the stupid lending decisions made by the two large bad banks. This of course concentrates losses at the two banks that bought way too many Greek sovereign bonds, but I personally think that’s just fine.

https://www.reuters.com//article/2013/03/25/us-eurozone-cyprus-text-idUSBRE92O02920130325

1. Laiki will be resolved immediately – with full contribution of equity shareholders, bond holders and uninsured depositors – based on a decision by the Central Bank of Cyprus, using the newly adopted Bank Resolution Framework.

2. Laiki will be split into a good bank and a bad bank. The bad bank will be run down over time.

3. The good bank will be folded into Bank of Cyprus (BoC), using the Bank Resolution Framework, after having heard the Boards of Directors of BoC and Laiki. It will take 9 billion Euros of ELA with it. Only uninsured deposits in BoC will remain frozen until recapitalization has been effected, and may subsequently be subject to appropriate conditions.

4. The Governing Council of the ECB will provide liquidity to the BoC in line with applicable rules.

5. BoC will be recapitalized through a deposit/equity conversion of uninsured deposits with full contribution of equity shareholders and bond holders.

6. The conversion will be such that a capital ratio of 9 % is secured by the end of the program.

7. All insured depositors in all banks will be fully protected in accordance with the relevant EU legislation.

8. The program money (up to 10 billion Euros) will not be used to recapitalize Laiki and Bank of Cyprus.

Participantskip –

I think where we differ is one of viewpoint and expectation.

As I’ve said before, I see the future as a continuum of possibilities, one of which includes your EOW (in fits and starts) scenario. But that’s not the same thing as being certain that EOW is the only possibility. I will take what comes, and adapt as things become more clear.

Great example. Some people were dead certain The Final Crash was going to occur in 2008-2009. That didn’t happen. These people (and I include myself in here) were unable to correctly interpret events in real time. The takeaway for me from that event is, I believe it is best to remain mentally flexible and avoid confirmation bias. That way, I can clearly see what is actually happening rather than misinterpreting current events because I’m viewing everything through the lens of false certainty.

People who are certain of a future outcome tend to fall into confirmation bias. Its a very rational response – why on earth would you spend time considering evidence that something ISN’T happening when you are 100% certain that it will? Of course that’s a only a dangerous mental place to be if your job is to successfully interpret events and see what is really happening.

Its good to be out of debt. Its also good to have cash lying around, be in good physical shape, have a stash of food just in case, own as much of the critical bits of your life as reasonably possible, and be mentally and emotionally flexible enough to adapt to whatever change comes along.

Now for particulars.

Depositors (of course) under 100k aren’t innocent. But they WERE promised immunity, the bondholders knew they were taking a risk position, had no such promise, and these bondholders were compensated for the risk they were taking through years of interest payments. It just makes sense the ones NOT promised immunity take losses and the ones promised immunity do not. It conforms with my sense of justice.

Will this fix everything, everywhere, suddenly making everything all better? Of course not. But its the right thing to do in this situation. My opinion, of course. And the future can be left to take care of itself.

Participantskip –

One last note. Götterdämmerung has not yet arrived. It may – or may not – ever arrive. So I am not going to act as if it is a present reality unless and until such a thing comes to pass. We still have trash collection, police (more or less), and paved roads. I will therefore continue to advocate that losses be apportioned largely along lines I consider to be reasonable.

In the case of Cyprus, I advocate that their banking system that has been acting as a safe-harbor for offshore money gets thrown under the bus and the small depositors on Cyprus get saved – given that explicit promises on that exact point were made to small depositors. Perhaps after the end of times actually hits I’ll feel differently, but until that catastrophe strikes, I’m cool with how things are proceeding today.

Participantskip –

As always you make me think. However!

I’m going to paraphrase one of my favorite quotes from Dr. Strangelove: at this moment, Cyprus is choosing between two admittedly regrettable, but nevertheless distinguishable outcomes: one, where they live up to their promises to little depositors, and the other, where they swipe money from everyone regardless of the guarantees that came before.

In this article: https://www.reuters.com//article/2013/03/23/us-cyprus-parliament-idUSBRE92G03I20130323

there is discussion about the reasons why Cyprus originally wanted to include everyone in the losses: protecting their offshore banking establishment. Now it appears that is off the table. And I think that’s a good thing.

Even though there will be losses going forward, we can still choose societally better and worse ways of apportioning them. I think this process is happening now in Cyprus.

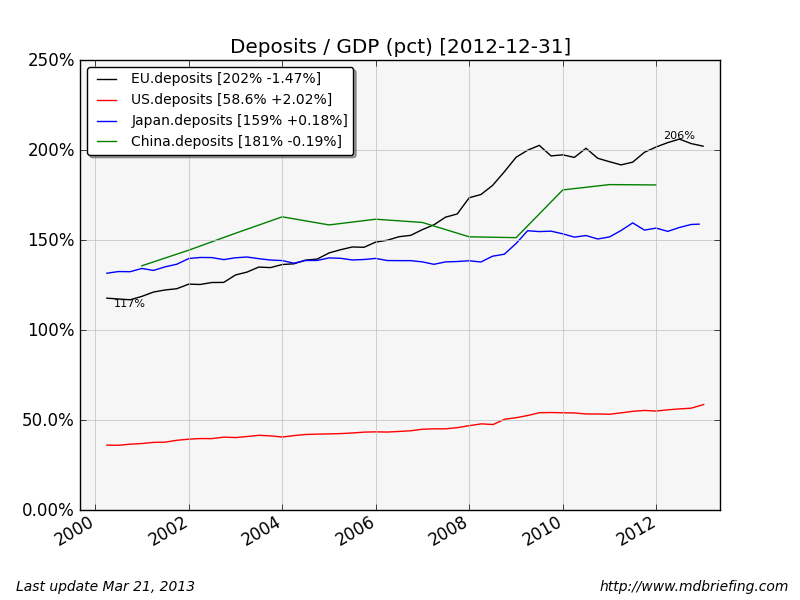

Just as a matter of interest, I wanted to see what the overall liabilities looked like in each area’s banking system. Here is a chart (of course) of what I found. The eurozone has deposits equal to 203% of their annual GDP, while the US has deposits equal to 59% of GDP. Europe’s banking system is massive, which means practically speaking when all of our property bubble chickens come home to roost, their uninsured depositors are going to take proportionally larger losses.

Because Cyprus was heavily exposed to Greek debt which has already defaulted (you cannot pretend-away a sovereign default) and its banking system was really huge relative to its GDP, it is operating as the canary in the coalmine – the earliest losses, in a place least able to cope.

Regarding bondholders. I am familiar with who owns bonds. Largely, it’s not grandma – if it is, its Rich Grandma who can generally deal. It might be grandma’s pension fund, but the professionals managing the diversified portfolio of bonds in her pension fund have a much higher level of experience about these things than grandma herself has in managing her own deposits. And mostly it is top-10% types, like you and me, who can more easily absorb the losses.

Again, two regrettable but distinguishable outcomes: one where you soak grandma herself, and another where you hurt a percentage of grandma’s diversified pension fund – the better to educate those pension fund managers about where to invest grandma’s pension money.

Of course the lesson that really bad losses have the potential to hurt everyone is there for all to learn. If and when losses get more severe, everyone is going to be invited into the problem-solving circle. So to speak.

ParticipantNassim –

Not knowing what tomato prices were prior to the eurozone admission, I can’t comment other than – perhaps your elderly lady could grow a few tomato plants? They’re so easy, and nothing beats a home-grown tomato. I think food engineers have GMOed all the taste out of tomatos these days.

But I digress. 🙂 And I really don’t mean to trivialize the struggles of someone on a fixed income. I just happen to like home grown tomatos.

My mom is retired, and CALSTRS (the manager of her pension) is looking more and more tenuous since the crash. They’re expecting a 7.5% ROI each and every year and even with that expectation, they’re going to go broke in about 30 years. If they were to assume no growth, I wonder how long they’d last.

ParticipantIn the US, in a bank bankruptcy, depositors have seniority over all other liabilities as the result of a law passed in 1993 called “depositor preference.” This law was put in place to help reduce losses to FDIC during a bank resolution process. It also reduces losses to depositors above the insured limit.

This is relatively unique to the US – not many other nations have such a law in place.

When a bank goes down in the US, the FDIC rolls in, sells all the assets, writes checks to insured depositors, and with whatever cash remains, pays off creditors in order of precedence. With depositor preference, that means all those remaining UNINSURED depositors are paid fully, before any other creditor – including junior and senior bondholders – sees a dime. The amount paid to the rest of the creditors depends on how bad those assets are.

What *should* happen in Cyprus depends on how they legally treat depositors in a bankruptcy. If a depositor is an unsecured creditor, wow, tough luck for them, they stand in line along with the junior bondholders. If they have depositor preference laws in place, then the bondholders should be completely wiped out before those depositors – even the uninsured depositors – lose a nickel.

Of course once the government steps in and circumvents the usual processes, then they get to pick winners and losers, just like we did when TARP parachuted billions in equity buys across the US banking system in 2008-2009.

If depositors are unsecured creditors, and they do end up getting thrown under the bus in this process, then I suspect a price will be paid eurozone-wide as small depositors remove their money at the first sign of trouble in their nation’s banking system. If you can avoid a 6% “wealth tax” on your insured deposits by simply withdrawing your money, heck, why not?

Is this the effect they were looking for?

Deposit guarantee programs were put in place to instill confidence and stop bank runs. With that confidence “impaired” by this new wealth tax – a service fee for the privilege of having your money in that fine banking institution – all I can think of is “unintended consequences.”

I’ll take cash, thanks. No wealth tax yet on cash.

As for the moral argument – I’m quite comfortable picking small depositors (especially the ones given a guarantee of protection by the government) over bondholders who were “the smartest guys in the room” who signed up for risk when they made their investment.

This ethical discussion reminds me of the argument that the majority of the blame for the housing bubble should be placed on home buyers. Bankers have been in the business of making loans for 400 years. Its not rocket science – there are well-established principles of doing business. Basically: don’t make a loan that can’t or won’t be paid back. So in that transaction, who was the smartest guy in the room? The guy who takes out a home loan 5 times in his life, or the company that has processed thousands if not millions of loans before?

Sure, without a greedy mark there is no con. But I’m quite comfortable placing the vast majority of the responsibility on the con men. Especially when “the con” is their entire business model.

But that’s just me.

Participantskip –

Its a nice theory, but it will founder on the rocks of international geopolitics. Russia appears to be shopping for naval bases in the Mediterranean, and if Cyprus leaves the eurozone and readopts its Pound, Russia underwriting that Pound would seem like a natural way for them to support all that KGB money AND obtain a nice base in a sunny climate.

That doesn’t even take into account any of the petroleum resources thought to be hiding under the seabed nearby the island.

ParticipantCHS at oftwominds.com suggested that Cyprus might be a test run, and if the people don’t revolt, the technique will be applied in other bank failures. If people do revolt, well the deal will be hastily renegotiated, and no harm done.

Of course, it could also be “the best idea they had at the time” – something that would sell to the German taxpayer.

Certainly none of us were in the room when it went down so we can’t really know for sure.

Participantalan, pipefit –

Nicely done guys. Since a nickel is always worth 5 cents, the government by law has put a floor on its value. And if hyperinflation hits, the metal in a nickel will appreciate in value! That’s a trade that only has upside to it!

However, there is an aspect of practicality here. In the physical PM community, silver is considered to be a bit too weighty to be a convenient wealth savings vehicle. Nickel is 100 times worse!

1 pound of silver: $421

1 pound of nickels: $4.53

1 ton of silver: $842,459

1 ton of nickels: $9,060Can you imagine saving $9000 in nickels? At 5 grams each, you get 90 nickels per pound, and 181,200 nickels per ton.

An $18,000 car could be bought with two tons of nickels! 331 pounds to pay your $1500 rent!

But if you ignore the logistics and storage aspect, its a no-lose trade. And there aren’t many of those around.

Coinflation says the nickel is worth about 101% of face value right now. The real deal is pre 1982 pennies, which are 232% of face.

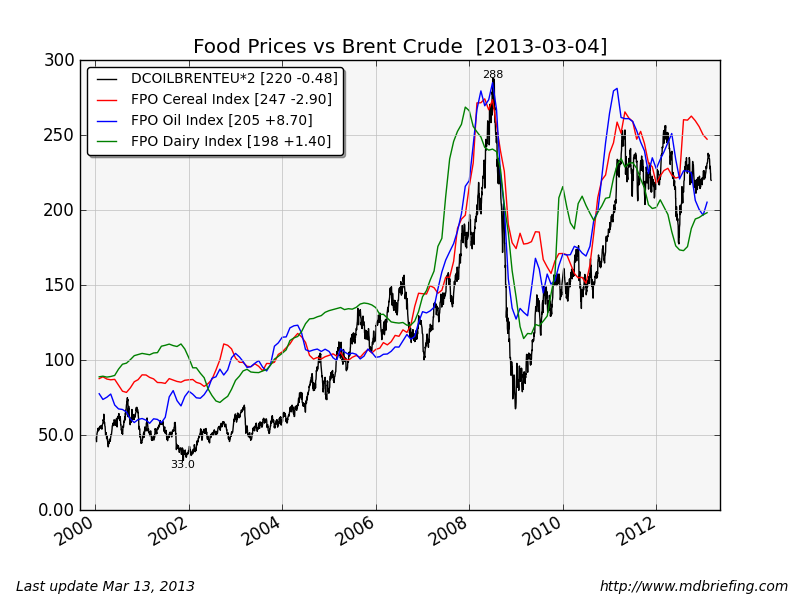

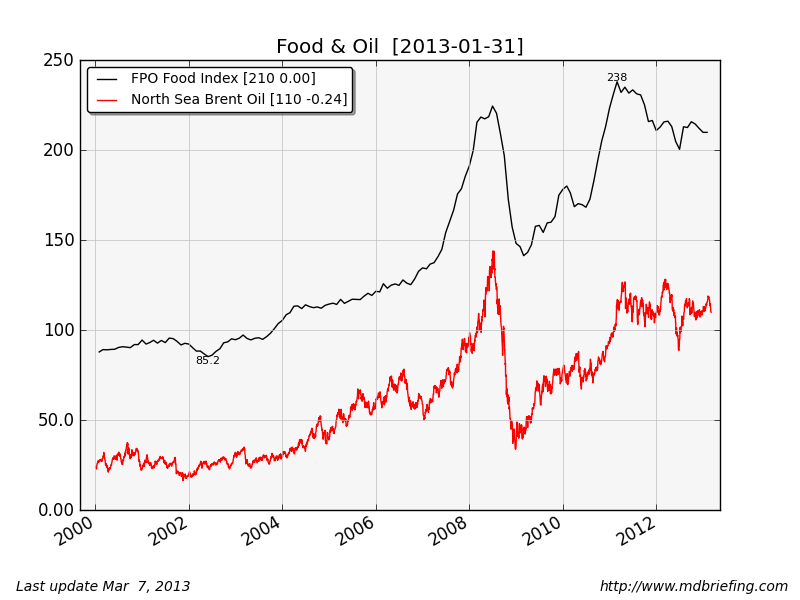

Participantalan –

gurusid already beat you to it with that observation, and you’re both right, oil (at least in the case of 2007-2008) isn’t leading the charge. Oil & food are clearly correlated, but its not oil out in front.

Can the move of both oil & food be traced to the GAAP deficit? The original thesis was that GAAP deficits were alleged to be massive money creation leading to hyperinflation – 7 trillion per year. I claimed that GAAP deficits do not cause price increases, because no actual money is created by such a deficit – and actual money creation chasing actual goods & services is required to create monetary inflation.

Yet something drove huge price increases in the 2006-2008 timeframe. And those price increases which have been filtering through the economy over the past 3 years make people think Fed money printing is doing it, makes some people think about stagflation and hyperinflation and so on. But I don’t think thats the case. I think its something else.

I wouldn’t mind figuring out what it is. Expectation of peak oil? Its all conjecture.

Participant@gurusid –

I’ve been outcharted! My charts cannot yet do two y-axis settings, sadly, so I have to reduce myself to scaling things by hand.

However! I happen to have data, specifically the five timeseries components that together make up the FPO Food Price Index: meat, dairy, cereal, oil, and sugar.

So it turns out that neither meat nor sugar correlate well with oil. So I eliminated them from the chart. What remains of course are dairy, cereal, and oils.

I totally see what you mean about some of these things leading rather than following oil. I didn’t see that before – your chart made that more visible. I think I need to go off and write some code!

So that leading behavior I can’t explain. These days sometimes I see some commodities move almost in lock step intraday – I think some big hedge funds put on trades and/or have computers that encourage this sort of correlation but that’s just a guess on my part.

I’m sure droughts cause things to become uncorrelated. [I looked at some charts offline]. Yeah, looking at wheat & corn, they definitely split directions in later 2012, and for whatever reason corn is much more weakly correlated with crude than wheat.

It could be gambling by the big banks, hedge funds, and commodity index funds causing things to move largely in lock step. If people want a “commodity fund” they get all of them, which would cause them to move in unison to some degree.

Bottom line, I don’t think the primary thing moving “stuff” prices around at retail is the GAAP deficit, or any sort of monetary policy decision-making at the Fed.

But perhaps someone can show me a chart that shows otherwise.

Participant@pipefit –

“If you look around, you will always be able to justify just about any statement with a chart or three.”

If everyone involved in the discussion is being intellectually honest, that’s not true. There is fact, and then there’s lies. Given a particular chart, either the data is accurate, or not. If the data behind the chart is accurate, and the data is presented with every attempt to properly represent the truth in context, and the people are operating in good faith, then the discussion can be an honest one

That is the kind of discussion we’re having, right?

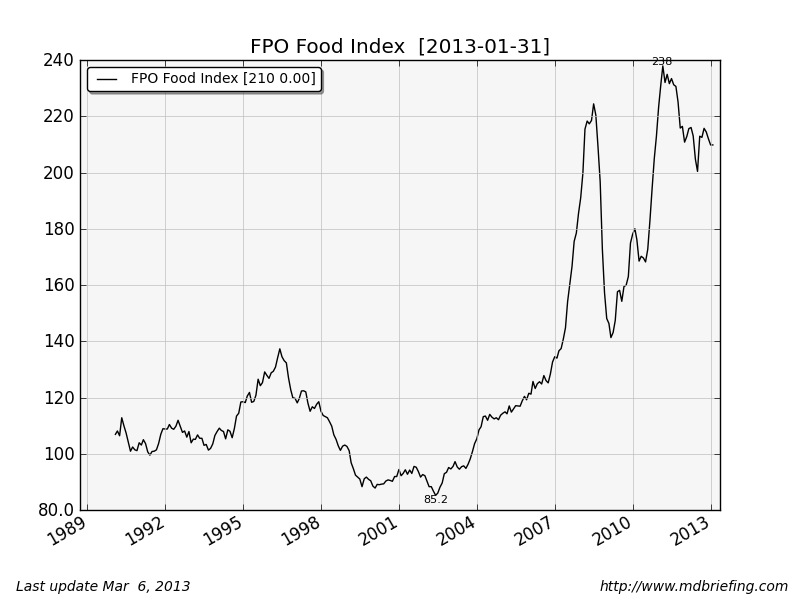

So I believe there is an important question to answer underlying your whole hyperinflation mindset. That is, why the heck have food prices gone nuts since about mid 2005?

I happen to have a chart on this (naturally) and indeed it shows that food has gone up perhaps 230% since 2000, and perhaps more shockingly, about 60% over the two years of 2007-2008. While 60% isn’t hyperinflationary, its definitely disturbing. But then what happened after? If we eliminate the 2009-2010 period, food isn’t much more expensive now than in 2008. That 30% per year move hasn’t continued.

How does John Williams explain this? Its all monetary? Hyperinflation? GAAP deficits? Fed money printing? None of it washes. Our GAAP deficit hasn’t changed since 2008 – if anything, its gone up. Money printing hadn’t happened in 2008 yet. So what then?

My explanation: its oil – at least 80% anyway.

Of course it could be speculation to some degree as well. But since the marginal barrel of oil is now about $60-$80 per barrel, and since there’s no decline in demand, the oil price has to rise accordingly. And where oil goes, food follows, since food production is energy intensive.

So. Did food prices rise primarily because of GAAP deficits and Fed money printing? My gut says no. GAAP deficits do not seem to be causal. The chart would look quite different – there would be a continued steady upside pressure. My conclusion: its all about oil, with perhaps some leveraged speculation to throw in a bit of added oomph on both the upside and the downside.

But these are my charts. Please feel free to bring out your 3 charts. I will assume you too are being intellectually honest, and are not trying to deliberately deceive me. And you can challenge my charts, tell me why I’m wrong, and we can work to get at the truth.

That is why we’re here, right?

ParticipantTrivium –

Yes great video. Gives me a new appreciation for Mr. Grillo. Ilargi had good things to say about him a few weeks ago, but there’s nothing like a video that really brings the lesson home. If a picture = 1000 words, a video = a whole book.

Especially one from 1998. I was completely asleep back then.

ParticipantThanks for your kind words about my charts!

Its my goal to remain as evidence-driven as possible given the limitations of the data we have available. That’s what my charts are all about. I have been continually surprised by the various crisis outcomes, and my data collection is an attempt to avoid as much as possible such surprises in the future.

I do agree that you are more bearish than I am. That said, I definitely assign a non-zero probability of your scenario occurring. If events unfold the way you describe, it will certainly lead to the outcome you predict. I see things unfolding along a continuum of possible outcomes, and I get more clarity as to likelihood as events unfold.

I have to say how much I enjoy these discussions. Often someone’s question or comment will cause me to think, or run off and search my data to see if its true or not.

I did a simple study of debt burden and payment burden in the US on this page at my site:

mdbriefing.com/us-rpp.shtmlIt shows that the Fed has successfully reduced the payment burden for homeowners in the US – back to pre-bubble levels, but the vast majority of the debt burden remains. In other words, they’re underwater, but at least they aren’t experiencing the pain.

The cost: interest income for savers, about 500B per year just wiped out. Sorry grandma.

What’s almost equally fascinating to me is that even with payments set so incredibly low, home mortgage total loan amounts outstanding are still deflating.

Participant@pipefit –

“as a result of the failure of the average rube to figure that out, the average rubes aren’t setting aside money either”

The average rube is both more and less clever than you give him credit for. They know what’s happening, and their widespread failure to set aside money is thus completely inexplicable.

When non-retired adults were asked in 2010, “Do you think the Social Security system will be able to pay you a benefit when you retire?” 36% said YES, and fully 60% said NO.

Of course the survey goes on to highlight the incredible wish-impulse for free lunches that American citizens have displayed for far too long. But they DO know there’s a problem.

https://www.gallup.com/poll/1693/social-security.aspx

“It is a lot easier for the fed to just print $85 billion a month, and for Congress to deficit spend $7 trillion a year.”

The Congress is deficit-spending about 900 billion a year these days, not 7 trillion. The missing 6 trillion is all just promises. Same as my promise to pay you a trillion dollars by next Tuesday. It only matters when Tuesday rolls around. At that point, I’ll likely default – what happens when an unsustainable promise comes due. But didn’t you feel happy over the weekend? Yet no money was created. The only thing created by my promise was your feeling of happiness.

Money – something that is used to buy goods & services in the real economy – is created in two ways:

1) it is borrowed into existence by a willing borrower

2) it is printed by the FedThat’s it. Promises don’t fall under either heading.

Participant@pipefit –

GAAP budget deficits are not money creation. The GAAP deficit is just about promises. No actual money is created.

Thought experiment. If I promised you 10 trillion dollars to be delivered next tuesday, no actual money would be created until tuesday rolled around. Same thing here. The US government has promised to deliver social security & medicare payments, and that’s where the GAAP deficit comes from. GAAP is about accounting for promises. Presumably, we should be putting money aside every year so we can make good on those promises, but we aren’t.

But that’s not the same thing as creating money. Money creation comes from borrowing to fund a CASH deficit.

ParticipantViscount –

Now now, that position hemorrhaging is your own fault for not using stops. The couple of shorts I tried were stopped out basically even. Now its time to wait for the market to show its hand again.

High volume down days and low volume up days are an indication of a possible top. The words “indication” and “possible” are the key. If this stuff were a sure thing, we’d all be absurdly rich swapping stories on a beach.

The fat bit is your own fault as well. Try self control. 🙂

Last point; as much as I watch it, the world is not the market. The market reflects (ideally at least) profits – and expectation of profits – of the public companies. Welfare of people, on the other hand, isn’t included, such as the 26% unemployed in Spain, for instance. Nor is sustainability.

In the US, government borrow & spend of a trillion a year is making everything look better than it actually is. As long as that continues, that’ll put a floor supporting corporate profits. The moment we have to reduce spending back to the old more sustainable levels pre-2008, we’ll drop into recession faster than you can say “sequester.”

Hope that helps.

-

AuthorPosts