Arthur Rothstein Home of worker in strip coal mine, Cherokee County, Kansas May 1936

A very impressive procession of hearses, containing the first 40 of the 298 caskets that will have to be ‘processed’, is going on as I speak in Holland, and has been for hours of slow driving, broadcast on live national TV. It’s a 100 mile or so distance, with thousands upon thousands of people along the route paying respect, from the airport where they landed form Ukraine to the facilities where they’ll be identified.

Which in the most ‘fortunate’ cases can be done in hours, in others may take weeks, and in yet others may never be conclusive. At least on the surface, the Dutch are doing everything right when it comes to honoring and respecting the people who died on MH17, and those who mourn them.

Still, when the bodies left Charkov earlier today, there were speeches by the Dutch and Australian ambassadors and other officials, all entirely in the spirit of what the moment and the victims deserve and are entitled to, but there was one noteworthy dissonant, which was even picked up by a Dutch reporter who wasn’t there to give his own opinion, but nevertheless opined that he thought it was very out of line for Ukraine Vice PM Groysman to use the occasion, which was intended to honor the victims only, to once again start off on a bitter, and frankly shameless, rant against Russia and Putin.

Ugly. But not unexpected. It goes to show that we really no longer know who our friends are. And as I said the other day, that goes for the whole Russia and Ukraine situation as much as it goes for the economy and the crisis it’s in. There are far too many Americans and Europeans who still think their governments are their friends. Which in Holland today is very tempting, because there’s this whole display of ‘correct mourning’ going on that draws in just about everyone simply on the fact that emotions must go somewhere, and they are easily guided into a shared platform, because people are drawn to that.

But they are, in the slipstream of those shared emotions, just as easily drawn towards venting anger at a perceived common enemy; it is easy to manipulate – emotionally vulnerable – people’s genuine grief into a blame game directed at a common enemy, even if you have no evidence that enemy did anything wrong, or even had anything to do with the acts that made them your enemy in the first place.

This is not something we had to wait for Sigmund Freud to discover for us; people have known since they were much more primitive primates how this works. Group – or mass- psychology works like a charm if you press the right buttons in a group. And it may have had benefits in the days of David vs Goliath, where a seemingly weaker party won the day against a stronger one. But it also has a dark side. When people are vulnerable, you can make them believe just about anything.

“We” follow the side that’s been pre-chosen for us in the ongoing Ukraine battle by our governments, i.e. US and EU. Who started getting heavily involved in Ukraine a number of years ago, and began to put the pedal to the metal when then-President Yakunovych declined to sign a deal that would have delivered Ukraine into a perhaps not all that advantageous partnership with the EU.

That’s when the West joined the Maidan protest in an aggressive way. By then, though, it had already spent a princely sum of $5 billion supporting all sorts of movements that had one thing in common: they were against Russia. Or more specifically: against Putin. Who refused to kowtow to Brussels and Washington.

With the help of a number of not-so-squeaky-clean groups in Ukraine, the Maidan side won: the elected president fled. US-handpicked guys – dare we say puppets – took over, and launched ferocious attacks against those amongst their own compatriots in the east of the country who didn’t want to bow to American and European rule, if only because it was announced very transparently by the new rulers in Kiev that they would be considered second hand citizens, if they would be allowed to live.

The eastern, Russian-speaking population, chose to align with Russia. A choice that so far cost many thousands of them their lives. Killed by their own government’s army, aided by US secret service agents and mercenaries, on their very own land they, and their ancestors, grew up on.

Blaming Putin for what has happened, not just to MH17 but to anything and everything in Ukraine over the past year and change, is way too easy. Putin, or let’s say Russia, has not been the aggressor, the west, i.e. have. Putin was fine with the way things were before. He thought Yanukovych was a stupid clown, but at least his oil interests were safe with that clown.

He acted just like the US and EU did and do to this day in 100+ different countries: as long as the prevailing government do what you want, you leave them in place. In Yanukovych’s case, it was gathering insane riches and bankrupting his nation, but at least never renditioning or mass murder. In many countries “we” support, wholesale slaughter is the order of the day, and has been for many decades. Whether it’s Saudi Arabia or Iraq or Chili or the Congo, we have built our wealth of supporting regimes that are willing to kill their neighbors so our interests are served.

It’s completely senseless to even try and deny that. But we are still led, in our justified grief and anger, towards hate for the very people we have set up to being killed by armies we ourselves finance. Call them devils, call them terrorists, proclaim they have no souls or they eat firstborn children. It’s as old as the first primates. It’s politics.

But it’s also the epitomy of disrespect. For those of you who have died, and who deserve for you to put in your best effort to find out who killed them. Not point fingers and not deliver any evidence. And disrespect for those who are being killed on your name – yes, that would be you -, so a political power game can be played over your heads and theirs. And down the line, your kids can be sent to go and murder the kids of those who were never your enemy other than in your politicians’ chants and games.

Your politicians are not your friends. But they are very good at pretending they are, especially in circumstances where you are – and they always know when that is – most vulnerable. The fact that all you’ve heard and read so far, a week after MH17 came down, is insinuations, and not a single shred of proof, should tell you all you need to know as far as your leaders’ credibility is concerned. They have nothing.

The most damning, or should I really say most entertaining, showcase is that is this conversation between Associated Press reporter Matt Lee and US State Department Deputy Spokesperson Marie Harf. What Harf is saying, for the good listener, is that the entire State Department assessment of the MH17 situation is based on social media posts from the Ukraine government.

Which just happens to have issued more lies and fabricated videos and and and than anyone else involved. BUK rocket movements Kiev said were ‘rebel rockets’, but which proved to be on Kiev controlled territory, black boxes they said were tampered with that were not, etc etc. Not one thing I can think of Kiev said has proven to be true. But they’re our governments’ installed puppets, so we listen to them.

If there’s no other way to find out who your friends are, at least this conversation should make it abundantly obvious to you who is not. Marie Harf may have lost her job on this, but she still said it. This is the kind of thing I find hard to believe when I see it, but I think maybe most people fail to see what’s actually being said. Then again, in an emotionally laden environment, it’s perhaps easy to miss out on essentials.

My uncle’s at the evenin’ table, makes his living runnin’ hot cars

Slips me a hundred dollar bill, says

“Charlie you best remember who your friends are.”Straight Time, Springsteen

Yeah, that’s it, keep Russia alive …

• Economic Meltdown Scenario Piles Pressure On Russia And The West (Guardian)

Oil prices above $200 a barrel. Energy shortages in western Europe. The return of recession to the still-fragile global economy. A slump in Russia. That’s the fear haunting policymakers as they contemplate how to respond to the shooting down of MH17 over eastern Ukraine last week. The meltdown scenario can be easily sketched out. Every global downturn since 1973 has been associated with a sharp rise in the price of energy. Russia is one of the world’s biggest energy suppliers and is responsible for about one-third of Europe’s gas. America’s economic recovery from the deep recession of 2008-09 has been weak by historic standards, while the European Union’s has barely got going. [..]

Given the public outrage at the loss of life on MH17 some increase in the severity of the sanctions looks inevitable. In Brusselson Tuesday, there was talk of imposing restrictions on capital movements from Russia and of curbs on exports of defence and energy technology. These measures would certainly increase the pain for Russia, and would run the risk that Putin would retaliate by choking off oil and gas exports to the west, looking instead to energy-hungry China as an alternative market. Slater estimates that UK growth next year would be 1% lower than expected were Russia to halt gas supplies through Ukraine, with the impact felt through higher energy prices, higher inflation, falling share prices and weaker consumer confidence. Closing the gas taps could then trigger the “phase three sanctions” being resisted by many EU countries, including Germany, France and Italy.

These would target entire sectors of the Russian economy, blocking their exports to the west and preventing them doing business with companies in the European Union and North America. It is this prospect that has prompted fears of rapidly rising oil prices. Slater calculates that Russian energy exports to the rest of the world could be cut by as much as 80%, with less than half the shortfall made up by the Opec oil cartel. “In such a scenario, world oil prices could soar above $200 per barrel and gas prices would also rise steeply.” Julian Jessop at Capital Economics notes that the biggest losers from this would be Russia, already in recession. Other suppliers would have an incentive to keep prices low in order to grab Russia’s energy customers. The west could draw down on strategic oil supplies to limit the impact of the loss of Russian supply.

There are no markets left, just an artificial look-alike.

• Why The Markets Don’t Care What Happens In The World (MarketWatch)

A plane carrying close on 300 innocent people gets shot down along one of the most sensitive borders in the world. Israel invades Gaza, reigniting the deepest wounds in the Middle East, and potentially sparking another regional conflict. A few hundred miles away, a militant insurgency threatens to turn Iraq into a full-blown terrorist state. The world has not been short of things to worry about in the last week, or the news bulletins short on drama and conflict. But how did the financial markets react? A few stocks got marked down, and gold made one of its reflex moves upwards. Yet on the whole, they barely registered any reaction. It was as if nothing of significance had happened. There is a message in that, and an interesting one. The markets are no longer interested in what happens in the rest of the world. The days when geopolitics could impact the prices of stocks, bonds, commodities or currencies in any significant way have been consigned to the past.

There are two possible explanations for that: firstly that there are not any wars or revolutions any more that can dramatically change the outlook for the global economy; and secondly, that the markets are so pumped up by quantitative easing, and easy money from the central banks, that anything else that happens pales into triviality by comparison. The truth is probably somewhere in between. Either way, investors can safely ignore war and politics from now on when they are structuring their portfolio. The declining interest of the financial markets in what is happening around the world has been evident for some time. The Arab Spring that saw governments fall across the Middle East was probably the last set of uprisings to make any real impact, but even that was largely restricted to frontier indexes such as Egypt, and they don’t count for a great deal in the greater scheme of things. But it has been most noticeable this year. It is not as if the past few months have been short on drama.

The Russian annexation of Crimea, and possible capture of eastern Ukraine, marks the first major re-drawing of national orders within Europe in many years. It could easily turn into the beginning of a new period of conflict between Russia and Western Europe — the opening salvos of a new Cold War. Likewise the militant uprising in Iraq could easily result in the creation of a terrorist Islamic state in a country with some of the largest oil reserves in the world, and which only 10 years ago the U.S. considered so strategically important it invaded to bring down what it regarded as a rogue regime.

Tension between the Israelis and the Palestinians is hardly anything new: the invasion of Gaza is merely the latest in a long and bitter history of conflict. Even so, it remains one of the most disputed regions in the world, and one where any military action threatens a wider conflagration. Not so long ago, geopolitical events such as those would have provoked wild swings in the financial markets. After the 9/11 attacks on Washington and New York, the stock market fell dramatically. The Iraqi invasion of Kuwait sparked a wave of selling, and the Middle Eastern conflicts of the 1970s sent the oil price soaring and the stock market crashing.

• State Dept. MH17 Assessment Based on Kiev Social Media Propaganda (RT)

State Department Deputy Spokesperson Marie Harf described Russia’s statements on MH17 plane crash as “misinformation” – but when reporters asked her whether Washington would be releasing their intelligence and satellite data, Harf only replied “may be.” So far the US has been backing its statements by social media and “common sense.”

Yeah, Putin really fears US courts ….

• Putin’s Ukraine Woes Compounded by $103 Billion Yukos Claim (Bloomberg)

Russia will discover next week how much it may be asked to pay for the confiscation a decade ago of Mikhail Khodorkovsky’s Yukos Oil Co., then the country’s biggest oil producer. The Permanent Court of Arbitration in The Hague will rule on July 28 on a $103 billion damages claim the company’s former owners filed against Russia in 2007, Tim Osborne, head of GML Ltd., former holding company of Yukos, said by e-mail. Court official Willemijn van Banning said by phone she couldn’t comment on the date for the ruling. The potential multibillion-dollar punitive award comes as Russian President Vladimir Putin risks further U.S. and European sanctions after the downing of a Malaysian passenger jet in eastern Ukraine that killed 298 passengers and crew. The Obama administration has blamed the plane’s downing on pro-Russian rebels, who deny any involvement.

A substantial award of damages “would add to Putin’s sense of being backed into a corner and that the West is out to get Russia,” Masha Lipman, an independent political analyst based in Moscow, said by phone. “Whether a coincidence or not, it will be seen as more than a coincidence.” GML has a good chance of winning partial damages, according to Gus Van Harten, a professor specializing in arbitration at York University’s Osgoode Hall Law School in Canada. There’s “very limited room” for appeal and Russia will resist paying, so any amount awarded would trigger a global legal battle to seize state property, including assets of OAO Rosneft, which acquired most of Yukos in a series of forced auctions, Van Harten said. Putin has said his opponents are using the crash for “selfish political gains.” The EU warned yesterday that it may restrict the country’s access to capital markets and sensitive energy and defense technologies.

Super dollar.

• Jobs Hold Sway Over Yellen-Carney as Central Banks Set To Split (Bloomberg)

Before the Federal Reserve and fellow central banks go to work raising interest rates, they first need others to go to work. That’s the signal from policy makers worldwide, as even those whose mandates focus on inflation put the health of labor markets at the heart of their decision making. The approach leaves investors bracing for global monetary policies to diverge after the post-crisis embrace of easy money. Accelerating job creation — and the hope this will spur wages — leaves the U.S. central bank and the Bank of England preparing for higher rates by the end of 2015. At the other end of the spectrum, double-digit unemployment in the euro area and stagnant pay in Japan mean stimulus remains the only option.

“Strength in the labor market is a key factor in the change in thinking about when the first rate hikes may occur,” said Nariman Behravesh, chief economist in Lexington, Massachusetts, for IHS Inc. “There’s a huge differentiation in performance now. The frontrunners are speeding up.” Investors are starting to tune in to the end of synchronized monetary policy, with economists at Goldman Sachs Group Inc. saying shifts in hiring during the past eight months worked well as a simple predictor of rate expectations. The forward curves for the U.S. and U.K., which gauge investor expectations for rates, show the most-pronounced steepening as unemployment in both countries has fallen to the lowest levels in more than five years. By contrast, the euro-area’s 11.6% jobless rate remains close to a record 12% as investors bet its benchmark will stay low until at least 2016.

Oh, exciting!

• Draghi Faces German Hard Line on Avoiding Deflation (Bloomberg)

The deutsche mark is dead. Long live the deutsche mark. That’s the view from Germany’s central bank, which is resisting a weaker euro, introduced in 1999, and opposing the most aggressive strategies Mario Draghi could deploy to ignite growth in Europe, says Simon Derrick, chief market strategist at Bank of New York Mellon Corp. Derrick sees parallels with the early 1990s when Germany refused to surrender its hard money dogma even as it transmitted pain elsewhere. The 18-member euro area’s emergence from a two-year recession is proving sluggish, with inflation about a quarter of the ECB target and unemployment above 20% in Spain and Greece. Back in 1992, the U.K. was under German pressure to live with the high interest rates demanded by the Exchange Rate Mechanism, a slipway to the single currency, even if it punished the British economy.

In the end – and under fire from billionaire investor George Soros – the U.K. buckled. It allowed sterling to slump and interest rates to decline, paving the way for a 15-year expansion. In 1993, with France in recession, the Bundesbank was unwilling to accelerate rate cuts for fear that would harm the deutsche mark. By July, the need for a weaker franc persuaded meant Europe’s leaders to allow their currencies to trade more flexibly as they sought to keep the euro project alive. Fast forward to today: Germany’s intransigence is again in play as Draghi, the Italian president of the European Central Bank, mulls whether to enact quantitative easing to prevent deflation. He has cut interest rates to record lows and pledged fresh loans for banks last month to little effect so far.

Super dollar!

• China’s Terrifying Debt Ratios Poised To Breeze Past US Levels (AEP)

The China-US sorpasso is looming. I do not mean the much-exaggerated moment when China’s GDP will overtake America’s GDP – which may not happen in the lifetime of anybody reading this blog post – as China slows to more pedestrian growth rates (an objective of premier Li Keqiang.) The sorpasso may instead be the ominous moment when China’s debt ratios overtake the arch-debtor itself. I had presumed that this inflection point was still a very long way off, but a new report from Stephen Green at Standard Chartered argues that China’s aggregate debt level has reached 251% of GDP, as of June. This is up 20%age points of GDP since late 2013. The total is much higher than normal estimates, though it tallies with what I have heard privately from officials at the IMF and the BIS.

Mr Green – a highly-respected China veteran – includes total social financing (TSF), offshore cross-border bank borrowing (a story that we are going to hear a lot about), bond issuance, shadow banking of various kinds, and government debt. The ratio has risen by 100%age points of GDP over the last five years. As Fitch has argued out in the past, this is more than double the rise seen in Japan over the five years before the Nikkei bubble burst in 1990, or in the US before subprime blew up in 2007, or in Korea before the Asian financial crisis. It is the speed of the rise that worries credit rating agencies and regulators – including many at the Chinese central bank – as much as the volume itself. Though China is scary on both fronts. It has pushed debt to $26 trillion, more than the entire commercial banking systems of the US and Japan combined. The scale obviously has global ramifications. The FT’s Jamil Anderlini points out here that the figure is very high for an emerging economy.

Mature economies can handle a higher debt ratio for all kinds of reasons, not least because they have large assets to offset their liabilities. British figures of household debt look much more threatening than they really are because the debt is mostly for mortgages, and is balanced by high levels of equity and wealth. Total debt levels in the US are 260pc (if you assume that the Fed will never unwind QE, which I do). So unless the Politburo gets a grip very fast, and this too would be dangerous, it may catch the US by next year. This does not mean that China is about to crash. It has a state-controlled banking system. Therefore any bust scenario will play out in a different way, probably through much lower growth and two decades of Japanese-style extend and pretend. As the BIS implied in its annual report: almost the entire world has now been drawn into the Ponzi scheme of unsustainable debt. We can inflate some of it away, or we can deflate into defaults and creditor haircuts. Pick your poison.

This is going so wrong…

• China May Avoid Second Bond Default, Thanks To Bailout (MarketWatch)

China may avoid its second-ever corporate bond default due to a bailout by a local government, Chinese media said Tuesday. Huatong Road & Bridge Group, a privately held construction firm, said in a statement last week that it was uncertain whether it could pay the principal and interest on a 400-million-yuan ($64 million), 1-year bond when it reaches maturity on Wednesday. According to a 21st Century Business Herald report, the company had sent several tranches of funds “one after another” to the Shanghai Clearing House in order to cover the bond payment, but it was still short of the amount needed. However, the newspaper quoted an unamed source as saying that there was “no big problem” of a possible default, as the Shanxi provincial government appeared to have stepped in to coordinate the collection of company’s accounts receivable from local governments.

A possible default could harm concurrent efforts by the Shanxi government to convince the central bank to allow state-owned banks more lines of credit for investment projects in the province, the report quoted an expert as saying. Huatong Road & Bridge had cited the fact that its chairman, Wang Guorui, was under investigation in disclosing its financial troubles, according to the 21st Century Business Herald report. And while the company didn’t elaborate, the newspaper said Wang had been accused of illegal coal-mining activities. In March, Shanghai Chaori Solar Energy Science & Technology said it failed to make a full interest payment on a corporate bond it had issued, becoming the first onshore bond to default in China’s history.

Well, that’s surprise.

• China’s Net Forex Sales Suggests Capital Outflows (MarketWatch)

China’s central bank and financial institutions sold a net 88.28 billion yuan ($14.2 billion) of foreign currency in June, compared with a net purchase of 38.657 billion yuan in May, according to calculations by Dow Jones from central bank data. June is the first month of net sales after ten months of net purchases, suggesting capital started to flow out of China. The banking system’s foreign-currency purchase position totaled 29.45 trillion yuan at the end of June–lower than 29.54 trillion yuan at the end of May, People’s Bank of China data showed. The data include purchases and sales by commercial banks and other financial institutions but mostly reflect transactions by the central bank. Most analysts view the figures as a proxy for inflows and outflows of foreign capital as most foreign currency entering the country is generally sold to the central bank.

Did you notice?

• Everything In Your House Is Getting Cheaper To Buy (MarketWatch)

Maybe you haven’t noticed, but it’s a great time to buy all the things you need to fill up your house: Furniture, appliances, electronics, dishes and pots and pans. People tend to pay attention to the prices of things they buy all the time, like gasoline, milk and meat. But who can remember what it cost them the last time they bought a washing machine? Fortunately, the Bureau of Labor Statistics does keep track. The BLS reported Tuesday that prices of consumer durable goods have fallen 1.5% in the past year, the steepest decline since the depths of the recession in 2009. This isn’t a new trend: The prices of durable goods have been falling pretty steadily since peaking in 1997, and now they are as cheap as they were in 1988, after adjusting for the constant improvements manufacturers have been making to their products. What’s striking is how pervasive the price declines are. It’s not just a few items that are pulling down the average; prices are falling for almost every sort of durable good that consumers buy.

Here are the latest numbers from the BLS: Prices of major appliances are down 7.9% in the past year, the largest decline on record. Laundry-equipment prices are down 8.6%. Furniture and bedding prices are down 2.5% in the past year. Window coverings, rugs and other linens are down 2.1%. Clocks and lamps are down 6.9%. TVs are down 15%. Audio-equipment prices are down 2.4%. Telephone-equipment prices are down 7.7%. Camera prices are down 6.7%. Dishes and flatware are down 6.3%. Cookware prices are down 4.7%. Computers are down 6.3%. Tools and other hardware prices are down 1.5%. Toys are down 6.5%. Sporting goods are down 1.3%. Jewelry prices are down 4.5%. Medical equipment prices are down 1.1%. New car prices are down 0.4%. Auto parts are down 1.2%.

Yeah, but far too big to fail. $55 trillion in derivatives?!

• Deutsche Bank Suffers From Litany of Reporting Problems (WSJ)

An examination by the Federal Reserve Bank of New York found that Deutsche Bank’s giant U.S. operations suffer from a litany of serious financial-reporting problems that the lender has known about for years but not fixed, according to documents reviewed by The Wall Street Journal. In a letter to Deutsche Bank executives in December, a senior official with the New York Fed wrote that reports produced by some of the bank’s U.S. arms “are of low quality, inaccurate and unreliable. The size and breadth of errors strongly suggest that the firm’s entire U.S. regulatory reporting structure requires wide-ranging remedial action.”

The criticism from the New York Fed represents a rebuke to one of the world’s biggest banks, and it comes at a time when federal regulators say they are increasingly focused on the health of overseas lenders with substantial U.S. operations. The Dec. 11 letter, excerpts of which were reviewed by the Journal, said Deutsche Bank had made “no progress” at fixing previously identified problems. It said examiners found “material errors and poor data integrity” in its U.S. entities’ public filings, which are used by regulators, economists and investors to evaluate its operations. The problems ranged from data-entry errors to not taking into account the value of collateral when assessing the riskiness of loans.

The shortcomings amount to a “systemic breakdown” and “expose the firm to significant operational risk and misstated regulatory reports,” said the letter from Daniel Muccia, a New York Fed senior vice president responsible for supervising Deutsche Bank. The New York Fed has various tools at its disposal to address shortcomings by banks it regulates. It can issue private letters demanding action, as it did with Deutsche Bank, or, in more severe cases, impose restrictions on banks’ activities. The letter, which hasn’t been previously reported, ordered senior Deutsche Bank executives to ensure steps were taken to fix the problems. It also said the bank might have to restate some of the financial data it has submitted to regulators.

Krugman? Still have to talk about him?

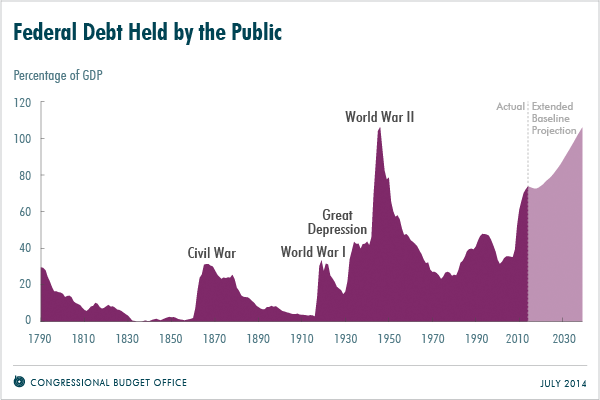

• Krugman’s Latest Debt Denial: His Magic Numbers Don’t Cut It (Stockman)

Professor Krugman is at it again—–conjuring fairy tales about a benign long-term fiscal outlook. Notwithstanding that the public debt has surged from 40% to 75% of GDP during the six short years since 2008, he claims there is no reason to fret and that there is no debt spiral anywhere in the future. In part that’s because the Keynesian priesthood has declared that interest rates have down-shifted on a permanent basis. CBO has therefore dutifully incorporated this assumption into its long-term projections:

This (interest rate) markdown has the effect of making the budget outlook — which was already a lot less dire than conventional wisdom has it — look even less dire. But there’s a further point worth emphasizing: the CBO has just declared an end to the debt spiral.

Even accepting CBO’s “rosy scenario” outlook (see below), it’s not evident that it has declared an end to the debt spiral. In fact, it projects publicly-held treasury debt to soar from $12 trillion today to about $52 trillion by 2039. Most people would judge that a spiral. Indeed, as shown in the CBO graph below based on “current policy”, the public debt ratio is heading sharply upwards to more than 100% of GDP.

So how does professor Krugman turn this dismal chart into an “all clear” reassurance–when it actually shows public debt heading to above WWII levels at a time when the baby boom is at peak retirement? Well, it seems that Krugman unearthed two numbers in a 182 page report that purportedly render harmless the $52 trillion of bonds, notes and bills that CBO projects will need to find a home at the historically low interest rates it forecasts for the next 25 years.

So we turn to Table A-1 on page 104 of the CBO report, and we learn that for the next 25 years CBO projects an average interest rate on federal debt of 4.1 percent and an average growth rate of nominal GDP of 4.3 percent. And this means no debt spiral at all.

A GDP growth rate higher than the average carry cost of the public debt sounds all good, but here’s the thing. Given outcomes during the 21st century to date, there is simply no plausible reason to believe that nominal GDP can grow at a 4.3% CAGR for the next 25 years. In fact, since the pre-crisis peak in early 2008, nominal GDP has grown at only a 2.5% CAGR, and even during the last two years when “escape velocity” was expected any day, the compound growth rate has been only 3.0%. Indeed, during the entire 14 years of this century—encompassing nearly two complete business cycles – nominal GDP has expanded at just 3.8% per annum. Needless to say, when you are crystal balling a quarter century ahead, CAGRs make a big difference, and that’s profoundly true of the Federal budget. Specifically, revenue is highly sensitive to nominal GDP growth because it is always money income, not real GDP, that is on the radar screen of the tax-man.

Oh well, at least Québec doesn’t look like the moon yet.

• Alberta Oil Clout Dominating Canada’s Unbalanced Economy (Bloomberg)

In Canada’s economy there’s Alberta, and there’s everywhere else. The oil- and gas-rich western province was responsible for all of the country’s net employment growth over the past 12 months, adding 81,800 jobs while the rest of Canada lost 9,500. Alberta’s trade surplus, C$7.4 billion ($6.9 billion) in May, almost matched the deficit rung up everywhere else. If growth trends over the past decade continue, Alberta would pass Quebec to become the country’s second-largest provincial economy in three years, according to data compiled by Bloomberg. “Alberta is already by far the strongest province economically, and higher oil prices will only exacerbate the regional split,” Benjamin Reitzes, a senior economist at BMO Capital Markets in Toronto, said in a telephone interview.

Alberta’s growing power is doing more than putting energy ahead of manufacturing exports such as Ontario’s cars and Quebec’s aircraft. It’s drawing tens of thousands of young people to the province, seeking energy jobs with some of the country’s highest salaries. It’s also posing a challenge to policy makers: Oil wealth has led to a stronger Canadian dollar, squeezing Ontario and Quebec manufacturers. Canada’s central bank is keeping interest rates near historic lows, looking for a weaker currency to boost exports. “We see a two-track economy,” Bank of Canada Governor Stephen Poloz said at a July 16 press conference after his decision to extend the longest interest-rate pause since the 1950s. Canada’s non-energy exports have disappointed, he said, holding back growth. At the same time, “energy exports have indeed been quite strong and we expect that to be a continuing trend.”

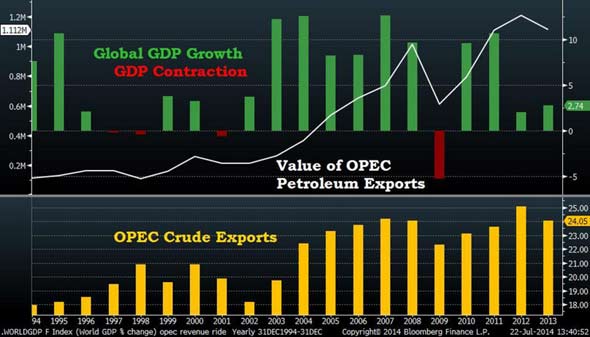

Export Land.

• OPEC’s Two-Decade Ride on Global Growth Stalls (Bloomberg)

For the past two decades, growth in the global economy spelled higher revenues for the Organization of Petroleum Exporting Countries. Not any more. The CHART OF THE DAY shows how last year was the first since 1993 that the value of OPEC’s total crude exports didn’t track the direction of global gross domestic product. The bottom panel shows how the group supplying about 40% of the world’s oil fetched lower average prices and also shipped fewer barrels year on year.

Production among OPEC’s 12 members fell 2.5% to average 31.6 million barrels a day last year, data from OPEC’s Annual Statistic Bulletin showed on July 18. Libya’s output slumped 31% amid political protests at oilfields and export terminals. Output from Iran, whose exports are subject to international sanctions, fell by 4.4%. The group’s members also consumed about 1% a day more domestically. “It’s three factors that have combined to give them, as they say, $100 billion less,” said Leo Drollas, an independent oil consultant in Athens and former chief economist at the Centre for Global Energy Studies. “The increase in the internal consumption, the slight fall in the price, and the fall in production in some members.”