Harris&Ewing Streamlined street car passing Washington Monument 1938

Difference is in 2001, 2008 there were no people as nuts as Draghi, Kuroda and Yellen. Or, if there were, they were not in charge.

• Not All Death Crosses Are Created Equal (BBG)

In a note to clients, Intermarket Strategy Chief Executive and Strategist Ashraf Laidi points out that the S&P 500’s 50-week moving average is falling below its 100-week moving average. This “statistically significant” death cross has only happened twice is the past two decades, Laidi points out. The first took place in 2001 and was followed by a 37% decline in the index, while the second pattern occurred in 2008 and preceded a 48% drop. With investors already growing increasingly nervous about prospects for equities, a death cross of grave proportions could give extra reason for caution.

“With luck, the rest of us outside China will have three or four more months to order our own affairs before the storm gathers.”

• China’s Communist Party Goes Way Of Qing Dynasty As Debt Hits Limit (AEP)

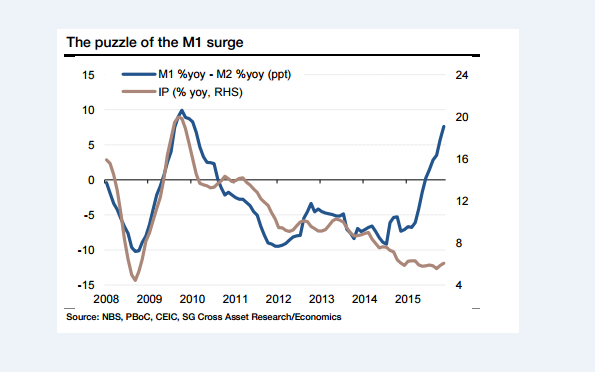

[..] The latest stop-go credit cycle began in mid-2015 and has since accelerated to an epic blow-off, with the M1 money supply now growing at 22.9pc, by the fastest pace since the post-Lehman blitz. Wei Yao from Societe Generale estimates that total loans rose by $1.15 trillion in the first quarter, equivalent to 46pc of quarterly GDP. “This looks like an old-styled credit-backed investment-driven recovery, which bears an uncanny resemblance to the beginning of the ‘four trillion stimulus’ package in 2009. The consequence of that stimulus was inflation, asset bubbles and excess capacity,” she said. House sales rose 60pc in April, despite curbs to cool the bubble. New starts were up 26pc. Prices jumped 63pc in Shenzhen, 34pc in Shanghai, 20pc in Beijing, and 18pc in Hefei. Panic buying is spreading to the smaller Tier 3 and 4 cities with the greatest glut.

It all has echoes of the stockmarket boom and bust last year. “Investors are convinced that the government will guarantee that housing prices won’t fall,” said Professor Zhu Ning from the Shanghai Advanced Institute of Finance, speaking to the South China Morning Post. It also sounds like Britain. There was a slight cooling in April but less than headlines suggested. The old measure of total social financing (TSF) slipped but this was more than offset by record bond issuance of $180bn. Together they reached a 26-month high. Capital Economics says budgeted funds must be disbursed by the end of this quarter under new finance ministry rules, implying another $310bn of bonds by late June. The fiscal boost will be ‘front-loaded’. The money will pile up in accounts and flood the economy over the late summer. If the usual time-lags hold, the mini-boom will last for a few more months. Then the trouble will start. Needless to say, markets may roll over long before the economy itself.

[..] .. this year the China bears may get their revenge, if they have any money left to play with. The rot in the country’s $7.7 trillion bond markets is metastasizing. Bo Zhuang from Trusted Sources said more than 100 firms cancelled or delayed bond issues in April due to widening credit spreads. Ten companies have defaulted this year, with the shipbuilder Evergreen, Nanjing Yurun Foods, and the solar group Yingli Green Energy all in trouble this month. But what has really spooked markets is the suspension of nine bonds issued by the AA+ rated China Railways Materials, the first of the big central SOE’s to signal default. “This has greatly weakened investors’ long-standing expectation of implicit government support,” he said.

Bo Zhuang said investors have poured money into bonds in the latest frenzy. The stock of corporate bonds has jumped by 78pc to $2.3 trillion over the last year. It is the epicentre of leverage through short-term ‘repo’ transactions, and it is now coming unstuck. “The experience with the stock market shows how difficult it can be to contain a reversal in leveraged bets. In our view, a bond market crisis would be much more destructive,” he said. With luck, the rest of us outside China will have three or four more months to order our own affairs before the storm gathers. Whether it is bumpy landing, a hard landing, or a crash landing, depends on who the “authoritative person” in Beijing turn out to be.

“..year-over-year price growth in tier-1 cities [..] 28.3%..”

• China’s Housing Bubble Is So Big, Goldman Will “Need A Bigger Chart” (ZH)

One of the stated reasons for the Shanghai Composite’s 1.3% drop (and it would have been worse had the PPT not launched its infamous last minute buying blitz) was also the most amusing one: the stock market bubble is in danger of popping even more as a result of a housing bubble that is now raging at a pace not seen since the last Chinese housing bubble, and thus threatens to soak up even more cash from China’s chronic gamblers-cum-speculators.

So just how high of a housing number did the NBS report that spooked stocks so much? Well, as Goldman summarizes, housing prices in the primary market increased 1.1% month-over-month after seasonal adjustment in April, higher than the growth rate in March. Out of 70 cities monitored by China’s National Bureau of Statistics (NBS), 63 saw housing prices increase from the previous month. On a year-over-year, population-weighted basis, housing prices in the 70 cities were up 6.9% (vs. 5.5% yoy in March). According to an alterantive set of calculations by MarketNews, aggregate home prices rose 12.4% Y/Y in April after rising 10.4% in March. Since both numbers are ridiculously high, we’ll just leave them at that.

However, it was not the overall market bubble that is troubling, but that focused on the most desired, top – or Tier 1 – cities. Here, April price growth was 2.6% month-over-month after seasonal adjustment, vs. 3.0% in March.

But the real shocker was that on a year-over-year price growth in tier-1 cities continue to rise however, reaching 28.3% vs. 26.0% yoy in March. In fact it is so bad that Goldman, which tried to show the surge in the second chart below, clearly needs a bigger chart. Incidentally, total property sales in tier-1 cities accounted for around 5% of nationwide property sales in volume terms, and around 15% in value terms (2015 data).

And the stunning charts: Home price inflation month over month

And year over year: to show the Tier 1 housing bubble, Goldman will need a bigger chart.

Can’t keep the dollar down forever.

• Emerging-Market Assets Under Pressure as Fed Minutes Lift Dollar (BBG)

Emerging-market stocks and currencies fell to two-month lows as the dollar got a boost from minutes of the Federal Reserve’s last meeting that showed officials want to raise interest rates in June. The MSCI Emerging Markets Index headed for its biggest two-day drop in two weeks after minutes of the April 26-27 meeting released Wednesday in Washington showed most officials judged it “likely would be appropriate” to hike next month provided incoming data are in line with a second-quarter pickup. China’s yuan, South Korea’s won, Malaysia’s ringgit and Taiwan’s dollar fell to the weakest levels since March, while Indonesia’s rupiah and Thailand’s baht reached February lows.

The release of the minutes and speeches by regional Fed bank presidents warning investors not to dismiss the chance of a June increase have seen the chance of such a move increasing to 32% from 4% at the beginning of the week, Fed Funds futures show. Developing-nation stocks have now wiped out all of their gains this year and there’s a risk of outflows accelerating if the dollar keeps strengthening. “Investors should avoid any additional investments in emerging markets because their currencies and stocks will be under huge pressure from the strong dollar,” said Komsorn Prakobphol at Tisco Financial in Bangkok. Energy stocks will probably be resilient as the oil price is being driven more by supply and demand dynamics, he said.

A gauge of the greenback against 10 peers was steady after jumping 0.8% overnight, the most since November. The Bloomberg Dollar Index has rallied 3.1% in May, on track for its best month since January 2015. Overseas investors have pulled $2.9 billion from Taiwanese stocks this month and close to a combined $1 billion from Indian, Indonesian and Thai bonds, exchange data show. “Asian currency weakness has been exacerbated by portfolio outflows from the region and we see little respite in the weeks and months ahead,” said Mitul Kotecha at Barclays in Singapore. The ringgit, baht, rupiah and, to an extent, the Taiwan dollar are the most vulnerable Asian currencies to a Fed rate increase, while India’s rupee and the Korean won are better placed, he said.

“It is undeniable that the euro has turned out to be an instrument of widespread impoverishment rather than shared prosperity.”

• The Case For Germany Leaving The Euro #Gexit (Bibow)

The case for or against a British exit from the EU – #Brexit – is headline news. For the moment the earlier quarrel about a possible Greek exit from the Eurozone – #Grexit – seems to have taken the back seat – with one or two exceptions such as Christian Lindner, leader of Germany’s liberal FDP. Most EU proponents are deeply concerned about these prospects and the repercussions either might have on European unity. Yet, while highly important, neither of them should distract Europe from zooming in on the real issue: the dominant and altogether destructive role of Germany in European affairs today. There can be no doubt that the German “stability-oriented” approach to European unity has failed dismally. It is high time for Europe to contemplate the option of a German exit from the Eurozone – #Gexit – since this might be the least damaging scenario for Europe to emerge from its euro trap and start afresh.

Germany’s membership of the Eurozone and its adamant refusal to play by the rules of currency union is indeed at the heart of the matter. Of course, it was never meant to be this way. And it was not inevitable for Europe to end up in today’s state of never-ending crisis that impoverishes and disunites its peoples. I have always supported the idea of a common European currency as I believed that it could potentially provide a monetary order that is far superior to the status quo ante of deutschmark hegemony: the Bundesbank – in pursuit of its German price stability mandate – pulling the monetary strings across the continent. While I have also always held that the euro – the peculiar regime of Economic and Monetary Union agreed at Maastricht – was deeply flawed, I kept up my hopes that the political authorities would reform that regime along the way to make the euro viable.

In this spirit I proposed my “Euro Treasury” plan that would, among other things, fix the Maastricht regime’s most serious flaw: the divorce between the monetary and fiscal authorities that is leaving all key players vulnerable and short of the powers required to steer a large economy like the Eurozone through anything but fair weather conditions, at best. Watching developments over in Europe from afar my hopes are dwindling by the day that the failed euro experiment will usher in reforms that could save it. Instead, the likelihood of some form of eventual euro breakup seems to be rising constantly. It is undeniable that the euro has turned out to be an instrument of widespread impoverishment rather than shared prosperity.

“For US investors it will become very different to follow.”

• Europe’s Troubled Push For Bank Bail-Ins (FT)

When Ignazio Visco, governor of the Bank of Italy, spoke in Florence this month, his focus turned to regulation. At a sensitive moment for Italian lenders, whose shares had collapsed over recent months, the governor chose to address what he called “regulatory uncertainty” in the wake of new European-wide rules for failing banks. “We must strike the right balance,” he said. “We should not rule out the possibility of temporary public support in the event of systemic bank crises, when the use of a bail-in is not sufficient”. Taxpayer support for banks, however, was precisely what the new European rules introduced at the start of this year aimed to avoid. To protect taxpayers, investors in banks bonds – mostly untouched during the bailouts of the last crisis – now face losses, or “bail-ins”.

The tension between the Italian central bank and European regulations is related to who owns this debt. In Italy, many retail investors hold exposed bank bonds, and a “bail-in” of small Italian banks in November last year was politically sensitive for this reason. But Mr Visco’s comments also reflect the challenges of implementing continent-wide rules in very different individual countries, with contrasting banking systems. So how else might this regulatory uncertainty, and the role of national governments, complicate a European vision for dealing with bank failure? Under the Bank Recovery and Resolution Directive (BRRD), European banks are now required to have a certain amount of bonds that are exposed to losses. The key issue is who suffers losses first. Whereas senior bank bonds ranked alongside depositors during the crisis, new bonds need to be subordinated to take losses.

But the actual instruments that count towards this measure are determined by national legislation. As a result, different countries have taken different approaches. Italy has raised corporate depositors above bondholders. France is currently legislating for a new class of bank debt, which will sit below depositors and existing senior bonds. In Germany, the law has been changed to subordinate outstanding senior bonds. In the UK, banks sell bonds from their holding companies, which will rank below other senior bank bonds. In the Netherlands, it is unclear how the rules will work. Robert Muller, treasurer at Rabobank, says the bank is strongly leaning towards the French approach, rather than the German. For investors, this represents a challenge. “At this point in time it’s very difficult for investors to see how this pans out,” says Mr Muller. “For US investors it will become very different to follow.”

Why am I thinking deck chairs? Anyway, can’t see Germany agree to spend its money on buying up loans.

• Euro Area Shifts Greek Focus to Debt Relief to Win IMF Support (BBG)

Euro-area officials are weighing a proposal to purchase loans that member states made to Greece in a move that would ease the nation’s debt burden, a precondition for the IMF’s involvement in a bailout program. Senior finance ministry officials held a conference call on Wednesday night to discuss ways to make Greece’s €321 billion of obligations sustainable, according to two people with knowledge of the talks. One option would be for the European Stability Mechanism, the euro-area’s financial backstop, to purchase loans individual euro nations made to Greece and reduce the interest payments, said the people, who asked not to be named because the discussions are private. About €52.9 billion of bilateral loans were made in 2010 and 2011.

Greece’s creditors are struggling to complete a review of the nation’s third bailout, which would pave the way for the disbursal of much-needed aid. The IMF has made its participation in the program contingent upon debt relief, a prospect euro-area finance ministers began discussing last week during an emergency meeting meant to resolve the impasse in unlocking the funds. Nations including Germany have said that the IMF needs to be involved in any future bailout program. The ESM is also considering purchasing the IMF’s loans as a way to give Greece a financial boost since its debt terms are more lenient than those of the Washington-based fund, according to a sustainability report prepared by the European institutions.

Buying back the IMF loans “amounts to debt relief,” European Commission Vice President Valdis Dombrovskis said in remarks in Brussels on Wednesday at a Politico conference. The officials mulled three debt-relief options during the call: have the ESM purchase bilateral loans made to Greece from individual countries; have the ESM purchase the IMF’s obligations; and extending the maturities of Greece’s debt and reducing the interest rates, one of the people said.

Economics is politics in disguise.

• All Economics Is Political (WSJ)

The models have been run and the numbers crunched: Bernie Sanders’s presidential platform, if enacted, would create 26 million jobs and 5.3% growth. An economist has done the calculating, and there’s no use arguing with mathematics. CNN’s headline reads: “Under Sanders, income and jobs would soar, economist says.” When I run that line by Russ Roberts, he replies with a joke: “How do you know macroeconomists have a sense of humor? They use decimal points.” Mr. Roberts is a fellow at the Hoover Institution, a University of Chicago Ph.D., and the gregarious host of EconTalk, a weekly podcast that celebrated its 10th anniversary in March. He is also an evangelist for humility in economics. “The world’s a complicated place,” he says. “We demand things from economics that it can’t provide, and we should be honest about that.”

What’s striking is Mr. Roberts isn’t talking only about politically contrived agitprop. Nobody believes that stuff: One of President Obama’s former economic advisers stirred ire from Sandernistas earlier this year when he said that getting Bernie’s agenda to add up requires assuming “magic flying puppies with winning Lotto tickets tied to their collars.” The deeper question is: How much better—more credible, or reliable, or falsifiable—are the economic forecasts pouring out of respectable think tanks, the White House and Congress? Mr. Roberts’s answer: not all that much. He cites the Congressional Budget Office reports calculating the effect of the stimulus package—for instance, one in late 2009 suggesting it had increased employment by between 600,000 and 1.6 million.

Leaving aside the incredible range of the estimate, how did the CBO come up with those numbers? Did it somehow measure employment in the real world? Nope: The CBO gnomes simply went back to their earlier stimulus prediction and plugged the latest figures into the model. “They had of course forecast the number of jobs that the stimulus would create based on the amount of spending,” Mr. Roberts says. “They just redid the estimate. They just redid the forecast. And you’re thinking, that can’t be what they really did.”

Definitely the new normal.

• 5 Banks Sued In US For Rigging $9 Trillion Agency Bond Market (R.)

Five major banks and four traders were sued on Wednesday in a private U.S. lawsuit claiming they conspired to rig prices worldwide in a more than $9 trillion market for bonds issued by government-linked organizations and agencies. Bank of America, Credit Agricole, Credit Suisse, Deutsche Bank and Nomura were accused of secretly agreeing to widen the “bid-ask” spreads they quoted customers of supranational, sub-sovereign and agency (SSA) bonds. The lawsuit filed in Manhattan federal court by the Boston Retirement System said the collusion dates to at least 2005, was conducted through chatrooms and instant messaging, and caused investors to overpay for bonds they bought or accept low prices for bonds they sold.

“Only through collusion could a dealer quote a wider spread than market conditions otherwise dictate without losing market share and profits,” the complaint said. “Defendants reaped millions of dollar(s) in profits at the expense of plaintiff and members of the class as result of their misconduct.” The proposed class-action lawsuit seeks triple damages, and follows probes by U.S. and European Union antitrust regulators into possible SSA bond price rigging.

[..] The lawsuit is one of many in the Manhattan federal court seeking to hold banks liable for alleged price-fixing in bond, commodity, currency, derivatives, interest rate and other financial markets. One such lawsuit, concerning competition in the credit default swaps market, led last September to a $1.86 billion settlement with a dozen banks. SSA bonds are sold in various currencies by issuers such as regional development banks, infrastructure borrowers including highway and bridge authorities, and social security funds. Many carry explicit or implicit backing from governments, and thus enjoy high investment-grade ratings.

Will Deutsche self-destruct?

• Another Year of Anger for Deutsche Bank’s Investors (BBG)

Deutsche Bank investors expressed their frustration with management at the company’s annual meeting a year ago. Weeks later, co-Chief Executive Officer Anshu Jain was gone. Now it’s Chairman Paul Achleitner and Jain’s replacement, John Cryan, who are set to feel the displeasure of shareholders when they gather in Frankfurt on Thursday. With revenue plunging and the need for capital mounting, some investors worry it may be just a matter of time before they’re asked to stump up and buy new stock. “The mood’s going to be bad, maybe even worse than at last year’s meeting,” said Klaus Nieding, vice president of DSW, a German firm that advises shareholders on company proposals.

Deutsche Bank shares dropped by more than half in the past year – erasing about $22.6 billion in market value – as plans to bolster capital and slash costs failed to revive confidence and profits shriveled across the industry. For Achleitner, a supervisory board dispute in April raised questions about his commitment to rooting out misconduct at Germany’s largest bank. Jain, 53, resigned in June after he and co-CEO Juergen Fitschen received the lowest approval rating in at least a decade in a vote at last year’s annual meeting. Fitschen, 67, will stand down on Thursday, leaving Cryan as sole CEO. Cryan, a British citizen who chaired the audit committee of the supervisory board before becoming co-CEO, has been outspoken about the company’s shortcomings, criticizing excessive pay, spiraling legal costs and outdated technology.

He suspended the dividend to bolster capital and pledged to shed about 9,000 jobs, or almost 10% of the workforce, and shrink the investment bank by scaling back the debt-trading empire built by Jain. While some investors applauded the cost reductions as long overdue, others expressed concern the cutting would eat too deeply into sales, especially during a trading slump. Debt-trading revenue, Deutsche Bank’s largest source of income, fell 29% in the first quarter from a year before, while net income dropped 61%. Cryan told analysts last month that his efforts to overhaul the company and settle outstanding legal matters may lead to a second straight annual loss. “The issue that we have is that we want to get an awful lot done this year,” he said.

Sorry for doing politics, but this is going to be a really big item. Question’s going to be: who can fill in for Hillary once she’s behind bars?

• First Look At Explosive Hillary Documentary, ‘Clinton Cash’ (NY Post)

Hillary Clinton says that when she and her husband moved out of the White House 15 years ago, they were “dead broke.” Today, they’re worth more than $150 million. In the new documentary “Clinton Cash,” it becomes all too clear how the former first couple went from rags to filthy rich — with the emphasis on filthy. As the movie shows, the Clintons are political Teflon dons compared with another Beltway power couple, former Virginia Gov. Bob McDonnell and his wife, Maureen. The McDonnells were convicted of accepting more than $150,000 in gifts from a businessman while the governor was in office. Meanwhile, the Clintons raked in 700 times that amount – $105 million – under the pretext of speaking fees while Hillary was in public office.

Yet while the McDonnells face time in the Big House, the Clintons are once again aiming for the White House. The documentary is based on a book by former Hoover Institution fellow Peter Schweizer and was just screened during the Cannes Film Festival. It is set to be shown in major US cities, including Philadelphia during the Democratic National Convention there in July. Schweizer’s research has withstood a year of intense scrutiny from critics because it is fact, not fiction. And the facts are compelling. The film whisks you around the globe, retracing how the Clintons personally pocketed six-figure speaking fees and collected billions of dollars for their family foundation. How? By trading on Hillary’s position as secretary of state and possible future president.

She and her ex-president husband sold out to titans, dictators and shady characters in Nigeria, Congo, Kazakhstan and the United Arab Emirates, not to mention at Goldman Sachs and TD Bank. Along the way, the Clintons betrayed the values they profess on the campaign trail: human rights, environmentalism and democracy. That’s why Schweizer is bringing the documentary to the Democratic convention — to show the party faithful how the Clintons used and abused their liberal principles to amass a fortune. The Clintons earned the bulk of their money from speaking fees. It was simple: Bill’s fees skyrocketed when Hillary became secretary of state in 2009, suggesting that countries and companies hiring him counted on getting more than just Bill — they also expected to land what his wife had to offer.

“The last month that wasn’t record hot was April 2015. ”

• Earth Breaks 12th Straight Monthly Heat Record (AP)

Earth’s heat is stuck on high. Thanks to a combination of global warming and an El Nino, the planet shattered monthly heat records for an unprecedented 12th straight month, as April smashed the old record by half a degree, according to federal scientists. The National Oceanic and Atmospheric Administration’s monthly climate calculation said Earth’s average temperature in April was 58.7 degrees (14.8 degrees Celsius). That’s 2 degrees (1. 1 degrees Celsius) warmer than the 20th century average and well past the old record set in 2010. The Southern Hemisphere led the way, with Africa, South America and Asia all having their warmest Aprils on record, NOAA climate scientist Ahira Sanchez-Lugo said. NASA was among other organizations that said April was the hottest on record. The last month that wasn’t record hot was April 2015.

The last month Earth wasn’t hotter than the 20th-century average was December 1984, and the last time Earth set a monthly cold record was almost a hundred years ago, in December 1916, according to NOAA records. “These kinds of records may not be that interesting, but so many in a row that break the previous records by so much indicates that we’re entering uncharted climatic territory (for modern human society),” Texas A&M University climate scientist Andrew Dessler said in an email. At NOAA’s climate monitoring headquarters in Asheville, North Carolina, “we are feeling like broken records stating the same thing” each month, Sanchez-Lugo said. And more heat meant record low snow for the Northern Hemisphere in April, according to NOAA and the Rutgers Global Snow Lab.

Snow coverage in April was 890,000 square miles below the 30-year average. Sanchez-Lugo and other scientists say ever-increasing man-made global warming is pushing temperatures higher, and the weather oscillation El Nino — a warming of parts of the Pacific Ocean that changes weather worldwide — makes it even hotter. The current El Nino, which is fading, is one of the strongest on records and is about as strong as the 1997-1998 El Nino. But 2016 so far is 0.81 degrees (0.45 degrees Celsius) warmer than 1998 so “you can definitely see that climate change has an impact,” Sanchez-Lugo said. Given that each month this year has been record hot, it is not surprising that the average of the first four months of 2016 were 2.05 degrees (1.14 degrees Celsius) higher than the 20th-century average and beat last year’s record by 0.54 degrees (0.3 degrees Celsius).

Complete and utter idiots. Everything that can go wrong, will. And then some.

• India To Start Massive Project To Divert Ganges And Brahmaputra Rivers (G.)

India is set to start work on a massive, unprecedented river diversion programme, which will channel water away from the north and west of the country to drought-prone areas in the east and south. The plan could be disastrous for the local ecology, environmental activists warn. The project involves rerouting water from major rivers including the Ganges and Brahmaputra and creating canals to interlink the Ken and Batwa rivers in central India and Damanganga-Pinjal in the west. The minister of water resources, Uma Bharti, said this week that work could start in a few days. A spokesperson from her department told the Guardian that the government is still waiting for clearance from the environment ministry. The project will cost an estimated 20 lakh crore rupees (£207bn) and take 20-30 years to complete.

The government of Narendra Modi, the prime minister, is presenting the project as the solution to India’s endemic water problems. For years, parts of India have suffered from devastating spells of drought. As average temperatures in India rise, and the growing population puts increasing demands on water resources, millions of people are without a reliable water supply. This year, 330 million Indians have been affected by drought. State governments used emergency measures to deliver water by train in the western state of Maharashtra; in other areas, schools and hospitals were forced to close, and hundreds of families were forced to migrate from villages to nearby cities where water is more easily accessible.

According to the National Water Development Agency, which will oversee the rivers project, “the water availability even for drinking purposes becomes critical, particularly in the summer months … On the other hand excess rainfall occurring in some parts of the country create[s] havoc due to floods.” The scheme is a pet project of Modi, who has made several promises to end India’s long-term water problems. In the first few months of his premiership, Modi’s cabinet revived the idea of linking 30 rivers across India. The water resources ministry spokesperson said: “The idea is old, but the Modi government has done all the work on it.” Plans to interlink rivers were drawn up in the 1980s by Indira Gandhi’s government, and were gathering dust as central governments repeatedly failed to win the approval of states. Now, with a supreme court mandate, and government backing, save the rubber stamp of the environment ministry, the project could get under way in a matter of days.

Home › Forums › Debt Rattle May 19 2016