Christopher Helin Fisk Service garage, San Francisco 1934

Last week we saw that China exports were down 18% in February and 6.6% in March, and that US mortgage originations are at their lowest level in 14 years. This week, the scary numbers just keep rolling in. Still, markets are up because Beijing has claimed a 7.4% GDP growth rate for 2014, and initial jobless claims in the US are falling somewhat, and most of all because everyone wants to believe in the recovery because they’re to scared of the alternative. If and when countries like Greece and Italy still have sky-high unemployment numbers and can nevertheless sell sovereign debt at puny yields, something’s definitely out of balance.

There’s a giant casino out there that poses as a solid investment vehicle that allows you to put your money in well-run and well-running enterprises that are working hard to produce what the public wants and needs, but in reality stock prices no longer reflect what companies do, but what their stocks do. It’s a hot air snake oil gold rush pyramid , and as long as the music plays you got to keep on dancing. There was a time when P/E ratios mattered, but it’s so yesterday to talk about those. It only takes a rumor of a gold seam some place out west for all of them to saddle up their wagons and chase the trail. It may go too far, at this point, to kill it mass hysteria, but it’s getting there. And the scary numbers just continue to flow in.

BusinessWeek says this (I adapt headlines at times to catch relevant details):

China Home Values Drop 7.7%, New Construction Down 25.2%

Most worrisome, however, is the clear cooling of China’s property market. The value of homes sold, 1.1 trillion yuan, dropped 7.7%. Broader property sales including commercial buildings reached 1.33 trillion yuan, down 5.2%. New property construction amounted to 291 million square meters, dropping 25.2% – that’s the worst first-quarter performance since 2009 and a signal that property developers are worried about sales over the rest of the year. [..] Urban real estate investment amounts to more than 10% of China’s economy.

New property construction in China fell 25.2%! In an economy that depends on real estate investment for 1 in every 10 dollars (and for far more on exports which also plunge), What was that number again, 90,000 property developers in China but only 30,000 viable concerns? And Beijing intends to let them go in a soft landing? Obviously, most people are not selling when values of homes that change hands fall by 7.7%, but as always some will have to.

And with each domino sold, another domino tumbles. China has been overbuilding in a wild craze and it’s hard to see what it can do next to stop prices from falling further. It could intentionally halt additional building activity, and create less supply while hoping for enough demand, but that would hammer both developers and builders, and push many Chinese out of relatively well paying jobs. It will probably try and find a golden middle road, but it’s all too easy to get those wrong. And then you get more of this:

Chinese Police Confront Trust Investors Demanding Repayment

Chinese investors demanding their money back from a troubled 973 million-yuan ($156 million) high-yield product in Shanxi province were confronted by police in front of a China Construction Bank branch. People wearing white masks with the words “despicable bank” and “pay back our money” were among at least 30 investors facing special-forces officers in dark uniforms in Taiyuan city, about 521 kilometers (324 miles) southwest of Beijing.

The nation’s second-largest bank is the custodian of the Songhuajiang River No. 77 trust, which missed six payments as of last month, according to the Economic Observer. “We have been cheated by CCB,” said Wang Fengying, 60, a Shanxi resident who said her husband had invested 1 million yuan in the product. “Our parents are very old. We need the money for their medical bills and to buy a home for my child. We are so miserable and they won’t even let us demand our money back.” The unrest underscores the stress in China’s $1.75 trillion trust industry [..]

Using special forces on your own people, certainly when they have legitimate complaints, is something every government should be cautious about. But it’s clear that if it concerns your 2nd biggest state(!) bank, there’s a risk any which way you choose to go. Still, what’s going to happen when there are protesters like this in a 100 cities, and in larger numbers? Sure, these people may have sought unrealistic returns on their investment, but to what extent can you hold that against them when it concerns a bank that belongs to the state?

John Rubino reports that Japan has major troubles in selling its sovereign bonds, with trade volume down by 70%, and a day and a half of no trade at all. If only the central bank buys government bonds, other investors move away. Until they get better yields. But in the case of Japan, with its behemoth state debt, higher yields very quickly turn into behemoth problems. It’s no accident that this happens just as Abenomics runs into its very predictable roadblock, precipitated though not caused by the April 1 sales tax rise, but it may well signify the beginning of the end of Tokyo being able to run the nation bond sales alone.

Bank of Japan Only Buyer Left for 10-Year Japanese Government Bonds

Here’s something you don’t see very often: For a day and a half this week, the Japanese government’s benchmark 10-year bonds attracted not a single successful private sector bid. At today’s artificially-depressed yields, no one wants this paper — except of course the Bank of Japan, which is buying up the bonds with newly-created yen. As the Gulf Times noted:

The Bank of Japan’s massive purchases of government debt hit a milestone this week, sucking liquidity out of the market to such an extent that the benchmark 10-year bond went untraded [..] for more than a day and a half. Trade volume in the benchmark cash bonds so far this month dropped to less than one trillion yen, down about 70% from the same period last year.

These are the most important fixed income instruments of the world’s third biggest economy, and the only entity willing to own them is the government that issues them. The rest of the world now refuses to lend money for ten years at 0.6% to a government whose debt is 200% of GDP and rising, which leaves Tokyo with only two choices: monetize virtually all its future borrowing or allow interest rates to rise and pay two or three times as much in interest going forward. The latter choice would hobble, if not cripple, an economy that can only function when borrowed money is nearly free.

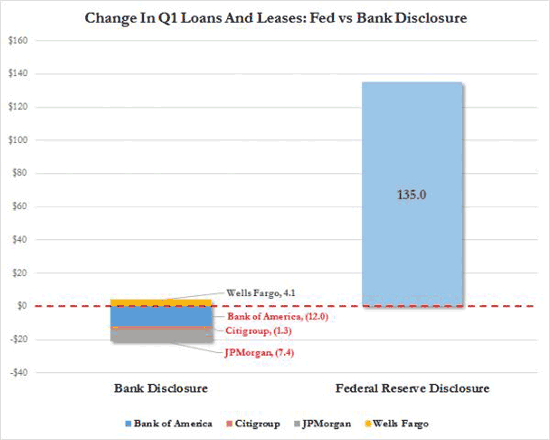

And if we turn stateside, Tyler Durden has found a “little” discrepancy that should raise a few BIG questions. The Fed has reported a hefty rise in loans and leases at US banks, but the banks’ own numbers show nothing of the kind. This is “only” the big 4 banks, which are good for 42% of all loans outstanding, so in theory the other, smaller banks, could be behind the rise the Fed talks about, but that would mean the shareholders of JPMorgan, Wells Fargo, BoA and Citi need to fire the asses of their executives for letting such a huge piece of their market slip away. It seems more likely that the Fed is not telling the truth here.

Is The Fed Fabricating Loan Creation Data? (Zero Hedge)

One of the more bullish “fundamental” theses discussed in recent weeks, perhaps as an offset to the documented record collapse in mortgage origination – because without debt creation by commercial banks one can kiss this, or any recovery, goodbye – has been the so-called surge in loans and leases as reported weekly by the Fed in its H.8 statement. This is indeed notable because as we have shown in the past, for nearly five years, total loans and leases within the US commercial system remained virtually unchanged from a level of about $7.3 trillion [..]

Of course, if the data represented by the Fed, which supposedly is a sample of call reports distributed to commercial banks, is accurate,[..] it would slowly allow the elimination of the Fed’s artificial conditions and removal of the central-planning umbrella.

And logically, since the Fed’s data is sourced by the banks themselves, what the Fed is representing and what the banks report quarterly should be in rough alignment. Unfortunately it isn’t. [..] … the Top 4 banks held some $3.14 trillion in loans and leases at March 31. So far so good. But what is not so good is that the change of this number in the first quarter is not an increase even remotely comparable to what the Fed makes those who read its H.8 statement believe it is. Quite the opposite. As the chart below shows, in the first quarter, of the Big 4 banks, only Wells Fargo reported an increase – a tiny $4 billion to be exact – in its loans and leases portfolio. All the other banks… saw a decline in their loans and leases holdings. We show this on the chart below.

We are of course bombarded on a daily basis with twisted, made up and simply untrue stories and interpretations through the media and government officials. But that will necessarily backfire, because once it’s revealed that you make it all up as you go along, at some point trust and confidence will disappear from the markets. It would be much preferable for everyone, except of course for those who profit most from the fantasy “news”, if markets returned to honesty. Thing is, how would we get there? The big media are not going to do any truthfinding, those days are long gone, their present role is much more profitable. It’s going to take either a major crash or a country saying we’ve had enough of this. Meanwhile, has there ever been a time when the entire globe refused to restructure their debts and return to a financial system people could trust?

PS: for those of you who didn’t recognize it, David Bowie years ago had an album called Scary Monsters (and Super Creeps)

Stories about central bank limitations are starting to come in. Interesting development.

• Central Banks’ Ability To Influence Markets Is Waning (Spiegel)

Since the financial crisis, central banks have slashed interest rates, purchased vast quantities of sovereign bonds and bailed out banks. Now, though, their influence appears to be on the wane with measures producing paltry results. Do they still have control? Once every six weeks, the most powerful players in the global economy meet on the 18th floor of an ugly office building near the train station in the Swiss city of Basel. The group includes United States Federal Reserve Chair Janet Yellen and her counterpart at the European Central Bank (ECB), Mario Draghi, along with 16 other top monetary policy officials from Beijing, Frankfurt, Paris and elsewhere.

The attendees spend almost two hours exchanging views in a debate chaired by Bank of Mexico Governor Agustín Carstens. Waiters serve an exquisite meal and expensive wine as the central bankers talk about the economy, growth and market prices. No one keeps minutes, but the world’s most influential money managers are convinced that the meetings help expand their knowledge in important ways. “We learn what makes our counterparts tick,” says one attendee. These closed-door meetings, which are held on Sunday evenings, have a long tradition. But ever since many central banks lowered their interest rates to almost zero, bought up sovereign debt and rescued banks, a new, critical undertone has crept into the dinner conversations.

Monetary experts from emerging economies complain that the measures taken by Europeans and Americans are pushing unwanted speculative money their way. Western central bankers say they have come under growing political pressure. And recently, when the host of the meetings — head of the Basel-based Bank for International Settlements Jaime Caruana — speaks in one of his rare public appearances, he talks about “chronic post-crisis weakness” and “risk.” Monetary institutions, says Caruana, are at “serious risk of exhausting the policy room for manoeuver over time.”

Listen and weep.

• The Voice Of The Moon: A Rare Interview With Ilargi (KMO)

KMO welcomes Ilargi of The Automatic Earth to the C-Realm to talk about the sorry state of watchdog journalism, the unhelpful rhetoric of American politicians and pundits around Vladimir Putin’s actions with regard to Ukraine, the media’s failure to examine the US role in bringing down the Yanukovich government, and the fragility of the Chinese economy given its dependence on a shadow banking system which has provided it with a vital life-line of credit. KMO begins and ends the episode with some thoughts on the suicide of Michael C. Ruppert.

• Is The Fed Fabricating Loan Creation Data? (Zero Hedge)

One of the more bullish “fundamental” theses discussed in recent weeks, perhaps as an offset to the documented record collapse in mortgage origination – because without debt creation by commercial banks one can kiss this, or any recovery, goodbye – has been the so-called surge in loans and leases as reported weekly by the Fed in its H.8 statement. This is indeed notable because as we have shown in the past, for nearly five years, total loans and leases within the US commercial system remained virtually unchanged from a level of about $7.3 trillion, first attained when Lehman filed for bankruptcy. And it doesn’t take a PhD in monetary theory to figure out that this lack of credit revival (alongside the historic collapse in shadow bank liabilities) is precisely what the Fed’s endless QE programs had been, at least on paper, trying to avert.

Of course, if the data represented by the Fed, which supposedly is a sample of call reports distributed to commercial banks, is accurate, then it would be a welcome development to the economy as it would indicate that finally lending conditions are easing, and demand for money is rising at the retail level as opposed to just the institutional (where it is merely used to buy risk assets). In other words, it would slowly allow the elimination of the Fed’s artificial conditions and removal of the central-planning umbrella. It would also indicate inflation may finally be returning to the economy (as opposed to just food and energy prices).

And logically, since the Fed’s data is sourced by the banks themselves, what the Fed is representing and what the banks report quarterly should be in rough alignment. Unfortunately it isn’t. Now that the Big 4 commercial banks – JPM, Wells, Bank of America and Citi – have reported their March 31 numbers, we can compile not only what the total amount of outstanding loans was as of the end of Q1, but more importantly, what the change in the quarter was.

What we learn is that the Top 4 banks held some $3.14 trillion in loans and leases at March 31. So far so good. But what is not so good is that the change of this number in the first quarter is not an increase even remotely comparable to what the Fed makes those who read its H.8 statement believe it is. Quite the opposite. As the chart below shows, in the first quarter, of the Big 4 banks, only Wells Fargo reported an increase – a tiny $4 billion to be exact – in its loans and leases portfolio. All the other banks… saw a decline in their loans and leases holdings. We show this on the chart below.

We admit that we have taken a sampling of banks, even if it is the four biggest banks in the US, those which account for 42% of all loans outstanding, and a complete analysis would require complete data from not only regional banks, but also foreign banks operating in the US. However, if the four best capitalized banks, flush with trillions in Fed excess reserves, are indicating on their own that they are nowhere near lending at the level the Fed is telegraphing, and are in fact reducing their loans outstanding, why should the others be more generous in their lending activities?

Which brings us to the question: is the Fed fabricating loan level data? Or, less dramatically, is the Fed merely once again goalseeking its weekly “data” to account for a world in which deposit expansion is no longer running at the pace seen in pre-taper days. It would be logical that the one “plug” the Fed would adjust to balance off its model is to boost lending activity, which would explain why the Fed is suggesting lending is surging.

• Bank of Japan Only Buyer Left for 10-Year Japanese Government Bonds (John Rubino)

Here’s something you don’t see very often: For a day and a half this week, the Japanese government’s benchmark 10-year bonds attracted not a single successful private sector bid. At today’s artificially-depressed yields, no one wants this paper — except of course the Bank of Japan, which is buying up the bonds with newly-created yen. As the Gulf Times noted:

The Bank of Japan’s massive purchases of government debt hit a milestone this week, sucking liquidity out of the market to such an extent that the benchmark 10-year bond went untraded for more than a day, the first time in 13 years. Data from the BoJ late on Monday showed its holding of Japanese government bonds topped ¥200tn ($1.96tn), or about 20% of outstanding issuance – up by more than half from ¥125tn about a year ago. The fall in market liquidity looks set to intensify as the BoJ has vowed to continue its aggressive buying for at least another year, with market players expecting it to expand its easing some time later this year.

The BoJ stepped up its bond buying last April when Haruhiko Kuroda became its governor, vowing to take radical easing steps to end deflation once and for all. The increasing dominance of the BoJ in the market, however, resulted in shortage of tradable bonds in the market, reducing trading flows between market players. The current 10-year cash bonds saw its first trade of the week yesterday afternoon, having gone untraded for more than a day and a half. Trade volume in the benchmark cash bonds so far this month dropped to less than one trillion yen, down about 70% from the same period last year.

What exactly does this mean? Well, it’s definitely weird. These are the most important fixed income instruments of the world’s third biggest economy, and the only entity willing to own them is the government that issues them. The rest of the world now refuses to lend money for ten years at 0.6% to a government whose debt is 200% of GDP and rising, which leaves Tokyo with only two choices: monetize virtually all its future borrowing or allow interest rates to rise and pay two or three times as much in interest going forward. The latter choice would hobble, if not cripple, an economy that can only function when borrowed money is nearly free.

• China Seen Cracking on Property Controls (Bloomberg)

China’s slump in property sales and construction is spurring speculation that the government’s four-year-old campaign of real-estate controls will start to crack. Citigroup Inc. sees “targeted easing” including on home purchase restrictions, while Bank of America Corp. says smaller cities may see looser rules. Centaline Group, parent of China’s biggest real-estate brokerage, says some cities are inclined to adjust policies such as the level of scrutiny of buyers. A 25% plunge in new-building construction helped drag economic growth in the first three months of this year to the slowest in six quarters, adding pressure on Premier Li Keqiang to avert a deeper slowdown.

While the government last night announced more support measures including lower reserve requirements for rural banks, Li reiterated that the nation isn’t considering stronger stimulus. “The housing sector now poses the biggest downside risk to the Chinese economy,” said Yao Wei, China economist at Societe Generale SA in Hong Kong. “The next batch of policy announcements is likely to be housing policy relaxation at the local government level.”

The value of property sales in the first quarter fell 5.2% from a year earlier and unsold completed properties jumped 23% from a year earlier to 521.6 million square meters, the bureau said.

• China Home Values Drop 7.7%, New Construction Down 25.2% (BusinessWeek)

Most worrisome, however, is the clear cooling of China’s property market. The value of homes sold, 1.1 trillion yuan, dropped 7.7%. Broader property sales including commercial buildings reached 1.33 trillion yuan, down 5.2%. New property construction amounted to 291 million square meters, dropping 25.2% – that’s the worst first-quarter performance since 2009 and a signal that property developers are worried about sales over the rest of the year.

“The property sector witnessed broad-based weakening, from home sales, new starts, land acquisition to secured funding for investment,” write Ding Shuang and Shen Minggao, economists at Citigroup in Hong Kong, in a report released on Wednesday. “The data confirms anecdotal reports of market correction in some smaller cities.” Urban real estate investment amounts to more than 10% of China’s economy.

“We should keep in mind that the external environment remains complicated and volatile, and the national economy still faces downward pressure,” the statistics bureau said in a statement. “China had a weak Q1 – and Q2 will be weaker in our view,” Stephen Green, chief China economist at Standard Chartered in Shanghai, predicts in a note today.

• Chinese Police Confront Trust Investors Demanding Repayment (Bloomberg)

Chinese investors demanding their money back from a troubled 973 million-yuan ($156 million) high-yield product in Shanxi province were confronted by police in front of a China Construction Bank branch. People wearing white masks with the words “despicable bank” and “pay back our money” were among at least 30 investors facing special-forces officers in dark uniforms in Taiyuan city, about 521 kilometers (324 miles) southwest of Beijing. The nation’s second-largest bank is the custodian of the Songhuajiang River No. 77 trust, which missed six payments as of last month, according to the Economic Observer.

“We have been cheated by CCB,” said Wang Fengying, 60, a Shanxi resident who said her husband had invested 1 million yuan in the product. “Our parents are very old. We need the money for their medical bills and to buy a home for my child. We are so miserable and they won’t even let us demand our money back.” The unrest underscores the stress in China’s $1.75 trillion trust industry as loans sour in an economy that grew at the slowest pace in six quarters. A product distributed by Industrial & Commercial Bank of China to raise funds for a troubled coal miner was bailed out in January to avert what would have been the first trust default in at least a decade.

Bring in Rob Ford …

• Troubled Co-Op Bank’s Ex-Chairman Charged For Crack, Crystal Meth (Bloomberg)

Paul Flowers, the former chairman of Co-Operative Bank Plc, was charged with possession of cocaine, crystal meth and ketamine, almost a month after the lender said it would post a full-year loss of as much as £1.3 billion ($2.2 billion). Flowers, 63, is scheduled to appear at a criminal court in Leeds, England, on May 7 to face the charges, the U.K. Crown Prosecution Service said in a statement today. Flowers, who was arrested in November as part of a drug investigation after he was filmed buying crack cocaine by a U.K. newspaper, was released on bail, West Yorkshire Police said in a statement.

“I have concluded that there is sufficient evidence and it is in the public interest to charge Paul Flowers with possession of Class A and Class C drugs relating to an incident on Nov. 9, 2013,” prosecutor Clare Stevens said in the statement. Regulatory and government probes are also in the works after the Mail on Sunday newspaper reported Nov. 17 that Flowers bought crystal meth and crack cocaine. Flowers, a Methodist minister, was Co-Op Bank’s chairman from March 2010 until June of last year.

Co-Operative Group Ltd., the bank’s parent, ceded control of the lender to bondholders in October to help plug a £1.5 billion capital shortfall. The bank said last month it will raise an additional £400 million after discovering a capital shortfall tied to mounting legal and restructuring costs.

Funny idea with a big risk.

• High-Frequency Fightback Starts in Foreign Exchange (Bloomberg)

Foreign-exchange dealers say they have the solution to the high-frequency trades eroding banks’ profits across financial markets. A currency-dealing platform known as ParFX, established in 2011 by firms from Deutsche Bank to Citigroup was approached last month by banks asking if its technology could be applied to other asset classes, Chief Executive Officer Dan Marcus said. The system works by pausing trades at random to prevent dealers with high-powered computers from jumping in front of investors and gaining an advantage. “These banks do need to trade foreign exchange because it’s their business and they’re hedging their currency exposure across the world,” London-based Marcus said in an April 15 interview. “They would rather trade in an environment that they can trust.”

High-frequency trading is coming under unprecedented scrutiny with the publication last month of Michael Lewis’s book “Flash Boys,” investigations by U.S. regulators and tough new rules approved this week by the European Union. Dealers use technology to execute orders in thousandths or even millionths of a second, profiting from tiny discrepancies in security prices across different trading venues. Relatively light regulation and high volumes make the $5.3 trillion-a-day foreign-exchange market a prime target for high-frequency traders. More than 35% of spot currency volume in October was by speed traders, up from 9% five years earlier, according to Boston-based consultancy Aite Group LLC.

“The idea of randomizing is, I guess, a potential solution,” John Adam, product manager at New-York based Portware LLC, which offers systems for high-frequency trading, said in an April 15 phone interview. “It’s placing a lot of faith in the randomizing, really. If somebody can figure out a pattern in that randomizer algorithm, that would be immensely problematic.”

• US Financial Showdown With Russia Is More Dangerous Than It Looks (AEP)

The United States has constructed a financial neutron bomb. For the past 12 years an elite cell at the US Treasury has been sharpening the tools of economic warfare, designing ways to bring almost any country to its knees without firing a shot. The strategy relies on hegemonic control over the global banking system, buttressed by a network of allies and the reluctant acquiescence of neutral states. Let us call this the Manhattan Project of the early 21st century. “It is a new kind of war, like a creeping financial insurgency, intended to constrict our enemies’ financial lifeblood, unprecedented in its reach and effectiveness,” says Juan Zarate, the Treasury and White House official who helped spearhead policy after 9/11.

“The new geo-economic game may be more efficient and subtle than past geopolitical competitions, but it is no less ruthless and destructive,” he writes in his book Treasury’s War: the Unleashing of a New Era of Financial Warfare. Bear this in mind as Washington tightens the noose on Vladimir Putin’s Russia, slowly shutting off market access for Russian banks, companies and state bodies with $714bn of dollar debt (Sberbank data). The stealth weapon is a “scarlet letter”, devised under Section 311 of the US Patriot Act. Once a bank is tainted in this way – accused of money-laundering or underwriting terrorist activities, a suitably loose offence – it becomes radioactive, caught in the “boa constrictor’s lethal embrace”, as Mr Zarate puts it. This can be a death sentence even if the lender has no operations in the US. European banks do not dare to defy US regulators. They sever all dealings with the victim.

Get out!

• Europe’s Half-Baked Banking Union (Bloomberg)

Europe is putting the finishing touches on a new banking union, with the aim of restoring confidence in the euro area’s banks, reviving lending and ensuring the common currency’s survival. It’s a step forward that doesn’t go nearly far enough. In approving a raft of banking-union legislation this week, the European Parliament has ratified an important understanding: If the member states of the euro area want to share a currency, they’ll have to share some risks and responsibilities. Among other things, they must pool the resources needed to rescue a bank whose collapse could overwhelm a government’s finances, as well as create a central authority to supervise banks throughout the euro area.

Unfortunately, the new laws fall short. Consider the Single Resolution Fund, set up to help recapitalize banks if their losses exceed what their shareholders and creditors can absorb. It will contain 55 billion euros, with authority to borrow more in an emergency. The euro area’s largest banks have assets exceeding 1 trillion euros, and borrowing from private investors would be difficult in a crisis. Rescuing a bank that big would require a lot more money.

The banking union was also supposed to guarantee deposits throughout the euro area. That way, concerns about one country’s ability to make good on its guarantees wouldn’t cause depositors to flee, as happened in Greece and Spain in 2011. That provision has been dropped, apparently because countries have their own deposit-insurance plans. So in a crisis, it could happen again that a euro in a Greek bank (say) would be worth less than a euro in a German bank. That isn’t what “common currency” was supposed to mean.

Europe is cheering the good news, car sales fell off a cliff for a few years, but turns out it’s all not what it seems.

• Europe’s Car Sales Show Artificial Growth On Price-Slashing (Reuters)

Europe’s car sales recovery may be taking hold, according to registrations data published on Thursday, but a confidential industry survey shows the pickup is failing to halt a price war. Discounts outgrew first-quarter sales, according to the data seen by Reuters, casting doubt on the strength of the recovery and earnings outlook for carmakers in the region. Registrations rose 10.4% in March, the Association of European Carmakers said, rounding off an 8.1% gain for the first three months, after six straight years of contraction.

But average retail incentives jumped 12% to almost 2,750 euros ($3,800) per vehicle in the five biggest markets, the findings of a major market researcher show. “There should be significant concern about artificial growth,” said Ernst & Young senior automotive partner Peter Fuss, citing discounts, government incentives and cut-price sales of unused vehicles as ‘nearly new’. The industry’s bottom line “continues to be under severe pressure”, he said.

PSA Peugeot Citroen saw its European sales volume rise in line with the market last month and for the first quarter overall. The French carmaker – which disappointed investors this week with a recovery plan targeting a 2% operating margin for 2018 – is also among the heaviest price-slashers. Retail discounts topped €3,000 per Peugeot vehicle, according to the survey data, and more than €3,750 per Citroen across Germany, Britain, France, Italy and Spain, where combined registrations grew slightly slower than Europe as a whole.

Plenty tricky. Why, for instance, do they recall 2.6 million cars if they are not liable for what’s wrong with them? And who’s still at GM who was involved in the decision to save the $0.98 per vehicle that killed a whole bunch of people?

• GM Seeks Immunity From Ignition Lawsuits (Reuters)

General Motors Co said it would ask a U.S. court to bar lawsuits related to actions before its 2009 bankruptcy, signaling a tougher stance toward legal claims stemming from its recent recall over faulty ignition switches. GM has said it is protected from liability for claims related to incidents that occurred before it exited bankruptcy in 2009, and has taken steps to raise those issues with the court by filing motions to stay recall-related lawsuits while it asks that bankruptcy court to clarify the extent of that protection.

In a filing with the U.S. District Court for the Southern District of Texas on Tuesday, GM asked for a stay on litigation related to ignition claims until a judicial panel on multidistrict litigation decides on a motion to consolidate the case with other lawsuits and the bankruptcy court rules on whether the claims violate GM’s 2009 bankruptcy sale order. The company earlier filed a similar motion with the U.S. District Court for the Northern District of California seeking a stay on pending litigation.The plaintiffs in those cases have claimed they bought or leased vehicles that had an ignition switch defect. The defect has been linked to the deaths of at least 13 people and the recall of 2.6 million GM vehicles.

Go China!

• China’s Ban Of GMO Grain To Cost US Farmers $6.3 Billion (Bloomberg)

China’s rejection of U.S. grain grown with seeds genetically modified by Syngenta AG may cost U.S. growers as much as $6.3 billion in losses through August 2015, a U.S. trade group estimated. The Asian nation turned away at least 1.45 million metric tons of corn since late November, “substantially greater” than the 908,800 reported by the Chinese government, the National Grain & Feed Association, based in Washington, said today in a statement. The grain contained a gene developed by Basel, Switzerland’s Syngenta, and that MIR 162 variety hasn’t been approved by China.

The “zero-tolerance policy” by China has cost as much as $2.9 billion in corn, distiller grain and soybean revenue, the U.S. group said, and as much as an additional $3.4 billion may be lost in the 12 months starting Sept. 1 after Syngenta offers another modified corn seed still to be approved by China and several other countries. “All of us are very hopeful that China will soon approve” the MIR 162 trait, Randall Gordon, the president of the trade group, said in a telephone interview. “Growers need to weigh the benefits of the access to new technology with what their markets are.”

Great title. Such a scary disease.

• We’re Aliens In Ebola’s World (Sanjay Gupta)

It’s hard not to be nervous, standing outside the Ebola isolation wards. The wards are a cluster of unassuming white tents in the middle of a large field, not far from the center of the city. Each is just big enough to hold around 10 cots. Two layers of zippers keep the outside from getting in, and more importantly here – the opposite. Nobody goes inside the tent without spending 15 minutes putting on isolation gear. The nurse handing over my garb calls it my “space suit. I can’t help but think that going into an Ebola isolation ward is a little bit like going to the moon. In H.G. Wells’ “The War of the Worlds,” seemingly invincible invaders from Mars are laid low by Earth’s microbes, for which they have no defense. With Ebola, we humans are the invaders. The sense of being an alien in the world of this virus is jarring.

Outside the tent, the air is sticky and has a distinctive smell of bleach. The bleach is in large plastic jugs; people use it liberally to wash their hands. It mixes with the smell of smoke, wafting from an enormous pit in the ground, full of smoldering ashes. I am told everything that comes out of these wards is burned: the suits we’re wearing, the sheets off the cots, even the human waste. Take no chances. Nothing kills better than fire. After the 2012 Ebola outbreak in Uganda finally ended, medical teams scorched the earth. The patients inside the tent are infected with one of the most deadly pathogens in the world. Ebola has no treatment, no vaccine and no cure.

There are at least five different strains of Ebola, and in past outbreaks, this virus – the Zaire strain – has killed as many as nine out of 10 people it infects. Men and women, young and old. Ebola does not discriminate. I geared up with Tim Jagatic, a physician from Ontario. He wants to give me an idea of what it is like to walk in his boots. He is with Doctors Without Borders, and he has been here for three weeks, almost since the beginning of the outbreak. This trip is his first time seeing Ebola. Jagatic is a different kind of doctor. He doesn’t just care for patients; he risks his own life to help save theirs. Sometimes, neither patient nor doctor makes it. Since the beginning of this Ebola outbreak, 112 people have died in Guinea and 13 in neighboring Liberia; at least 17 have been health care workers, according to the Centers for Disease Control and Prevention and the World Health Organization.

Do disagree! Go the comments section and let rip!

• The 15 Best North American Novels Of All Time (Telegraph)

The Scarlet Letter, Moby Dick, The Adventures of Huckleberry Finn, The House of Mirth, The Call of the WIld, The Grapes of Wrath, Independence Day, The Colossus of Maroussi, The Catcher in the Rye, Fear and Loathing in Las Vegas, Beloved, All the Pretty Horses, The Heart is a Lonely Hunter, Fugitive Pieces, We Need to Talk About Kevin.

Also rans: Uncle Tom’s Cabin, The Great Gatsby, For Whom the Bell Tolls, Rabbit, Run, The Color Purple, The Human Stain, White Noise, The Bonfire of the Vanities, The Shipping News, Infinite Jest.

Made me smile.

• Snowden Makes Surprise Appearance At Putin’s Press Conference (BI)

Former National Security Agency contractor Edward Snowden made a surprise appearance Thursday at Russian President Vladimir Putin’s annual televised call-in with the nation. His appearance offered Putin the chance to defend Russian surveillance, implicitly gaining Snowden’s approval. Considering the tightly controlled circumstances of the rogue agent’s asylum in Russia, it has been widely seen as a PR stunt. New York Times Moscow-based reporter David Herszenhorn called it a “stunning in-your-face move” by the Kremlin.

“Does Russia store, intercept, or analyze, in any way, the communications of millions of individuals, and do you believe that simply increasing the effectiveness of intelligence or law enforcement investigations can justify a place in societies rather than subjects under surveillance?” Snowden asked Putin. Putin said he would answer by talking as one professional spy to another, noting his past as a KGB agent and Snowden’s past in the NSA before he leaked thousands of documents exposing U.S. surveillance programs.

“Our intelligence efforts are strictly regulated by our law,” Putin said, according to a translation by Russia Today. “… You have to get a court permission to stalk a particular person. We don’t have a mass system of such interception. And according to our law, it cannot exist. “Of course, we know that criminals and terrorists use technology for their criminal acts, and special services have to use technical means to respond to their crimes. Of course, we do some efforts like that. But we do not have a mass scale, uncontrollable effort like that. I hope we won’t do that.”

• The Richest Man In Asia Is Selling Everything In China (Simon Black)

Here’s a guy you want to bet on– Li Ka-Shing. Li is reportedly the richest person in Asia with a net worth well in excess of $30 billion, much of which he made being a shrewd property investor. Li Ka-Shing was investing in mainland China back in the early 90s, way back before it became the trendy thing to do. Now, Li wants out of China. All of it. Since August of last year, he’s dumped billions of dollars worth of his Chinese holdings. The latest is the $928 million sale of the Pacific Place shopping center in Beijing– this deal was inked just days ago.

Once the deal concludes, Li will no longer have any major property investments in mainland China. This isn’t a person who became wealthy by being flippant and scared. So what does he see that nobody else seems to be paying much attention to? Simple. China’s credit crunch. After years of unprecedented monetary expansion that has put the economy in a precarious state, the Chinese government has been desperately trying to reign in credit growth. The shadow banking system alone is now worth 84% of GDP according to an estimate by JP Morgan. The IMF pegs total private credit at 230% of GDP, jumping by 100% in the last few years.

Historically, growth rates of these proportions have nearly always been followed by severe financial crises. And Chinese leaders are doing their best to engineer a ‘soft landing’. If they’re successful, the world will only see major drops in global growth, stocks, property, and commodity prices. If they fail, the spillover could become pandemic. This isn’t important just for Asian property tycoons like Li Ka-Shing. Even if you don’t know Guangzhou from Hangzhou from Quanzhou, there are implications for the entire world.

Home › Forums › Debt Rattle Apr 17 2014: Scary Numbers (and Super Creeps)