DPC The shores of Biscayne Bay, Miami, Florida 1910

That’s not a bad metaphor to work with. “Conditioned to catch the falling knife”. The expression comes from the investment world, but it describes a much larger world today pretty accurately.

Investors use it to describe people who see a stock fall, rapidly, from for instance $50 to $20, call the low, and decide it’s a good buy, only to be stuck with huge losses (the knife that cuts their hand) as it goes down all the way to 25 cents.

Tyler Durden quotes Bloomberg’s Richard Breslow as saying this about financial markets:

Conditioned To Catch The Falling Knife

“ … there is this enormous consensus in all ideas and positions, everyone knows that central banks are there and driving everyone’s positioning“; my friend Bob Savage said yesterday:

“We’ve been trained to catch the falling knife by the central banks, one of those trading strategies that will work until it doesn’t and when the knife slips you will really have a taper tantrum.

It’s becoming harder and harder to look at the news and then guess what markets did in response [..] the expectation tends to be much more logical than the reaction.

If you look at how markets are trading, they move ahead of a central bank meeting, or a strong or weak number, then everyone is caught with the same position and you end up being right but proven wrong.”

Just like most of today’s investors are Pavlovians potty trained by central banks, most people don’t have opinions of their own on most other issues either; some never did, some recently lost them, but all of them are shaped by media and politics, not innate critical thinking.

It may seem that this is something of all times, but there is a difference, since as one’s exposure to media rapidly increases, so does the influence they have, or the way in which they have it.

In earlier days, most people’s opinions were formed by the communities they lived in, the churches they visited, the schools they attended – if any -, albeit admittedly in ways no less nefarious than the present ones.

But in those days far fewer people were even under the impression that they indeed did form their own opinions – who could read and write? – and were capable of critical thinking.

Now, just about everyone does, and that makes for a different view of the world of the individual. And a different approach to manipulation for opinion makers, of both the individual and the masses.

I’ve often talked with friends about how and why 100 years ago people went into World War 1 in Europe’s battlefields from all over the world. How all those Canadian boys got to be killed over in Belgium and France. And how none of us could imagine doing anything like that in this day and age.

But people then did, partly because the risk of dying wasn’t perceived as being as high as it turned out to be, but certainly also because of community pressure, shaped by schools and churches. If all boys in town go, who are you to stay behind?

Things have changed. We are to a much larger extent individuals now. We live in smaller family units, with much more space per capita and therefore much less direct interaction with others.

We also have had a lot more education, and feel that entitles us to pass judgments. We think school has provided us with objective ideas about the world.

But that’s where the pinch is. We are being fed preconceived ideas from day one – though that’s never what they’re called – and few of us can shake them.

To name an example, there are very few people who will tell you a particular TV ad for a detergent makes them buy the product, but that ad wouldn’t be there if it didn’t work, ergo: who buys the stuff? We have Freud and Jung and their findings of the sub- and unconscious to thank for that.

So how does a government today go about justifying going to war? How does it create an “enormous consensus in all ideas and positions”? It’s not that hard, when you think about it.

Political ideas and ideologies, and politicians themselves, can all be sold to the individual, and the masses, the same way detergent is. By appealing to the unconscious. The means through which ideas are transferred may have changed, but the “pillars” they are based on have not. Jung spent a lot of time working on archetypes, and the bogeyman stands out as a prime example of that. If you give the enemy a name and a face, the job’s half done.

Add to that that the enemy and his people do terrible things to babies, eat them, bury them alive, the image has always worked wonders, and still does. Throw in horrid abuse of women and it’s clear sailing. Rinse and repeat. Lots of rapid repetition, something our present media are ideally suited for. Repetition works miracles, in politics as it does in advertizing. It’s not a huge stretch to say that repetition outweighs evidence.

That’s how Saddam Hussein, Gadaffi and Osama Bin Laden, and today Vladimir V. Putin, have become household names in the US and Europe. And everyone recognizes their portraits too. Though Saddam was never proven to have had WMD, there’s no evidence for Bin Laden’s involvement in 9/11, and Putin so far is merely an unsubstantiated evil media figurehead as well.

People at a certain point simply feel sure that they “know”. Because they’ve seen the names and faces so many times a day, confirming their earlier preconceptions. It has precious little to do with critical thinking. It has to do with what everyone around them says.

To get back to the falling knife, investors – potty trained as they are – all think they’re going to come out winners, even though they know they can’t all win, and even though they know all of their friends and competitors think the exact same way they do, and make the same decisions.

That is the herd mentality. Perhaps not an archetype as such, but, if anything, something even older and more deeply engrained in our brains. What Richard Breslow says is that the vast majority of investors will end up catching the knife in their bare hands, and it’s going to hurt something bad. ” … everyone is caught with the same position and you end up being right but proven wrong”

That is, but of course, exactly what will happen to all of us who blindly follow our politicians and their cleverly disguised media messages on our bogeyman enemies and the wars we have to wage against them.

All we want is to be right in the end, that is to say, we want to conform to the meme common to our herd, and whether or not that will prove us wrong is not on our radar.

Still, just as investors will get burned by blindly following every single move and every single word that comes out of the Fed, we will all get burned and cut and hurt by following every word our politicians and media rinse and repeat. We risk doing quasi irreparable damage to our relations with various people in Russia and Iraq and many other places around the world, who don’t want us as their enemies anymore than we want them, just because our “leaders” seek to advance their agenda’s by demonizing these people.

It’s a dangerous sort of deceit, which doesn’t start when war, be it physical or trade or any other kind, is declared, it starts with how and why we elect the people who have the power to declare it in our name.

And then “when the knife slips you will really have a taper tantrum.”, or in other words, when you find out your Pavlovian preconceptions (yes, you!) have been awfully off the mark, you still have to deal with the consequences, and they may hurt. Whether it’s oil that’s no longer delivered, so you’re cold and miserable and stuck where you are and everything runs to a standstill, or it’s someone attacking your communities because the leaders you elected chose to attack theirs halfway around the world, you may find you’re the one who ends up catching that knife.

And then, inevitably, maybe someday you’ll realize that what you’ve caught, and got cut by, and have fallen into, is your own knife. You threw it up into the air. And you were conditioned to catch it.

• Conditioned To Catch The Falling Knife (Zero Hedge)

The numbers out last night were once again largely on the weak side of disappointing, with very little reaction and even less of an intuitive reaction. As Bloomberg’s Richard Breslow writes, this is the downside of everyone having the same positions. Simply put, we’ve been trained to catch the falling knife by the CBs, one of those trading strategies that will work until it doesn’t and when the knife slips you will really have a taper tantrum. Via Bloomberg’s Trader’s Notes…

Some strategists are even finding good news in the euro area growth data, noting that it is impressive there is any growth at all when none was expected, unlike U.S. where 1H numbers disappointed — some people just don’t like black and white analysis. As we have mentioned before, it seems there is this enormous consensus in all ideas and positions, everyone knows that central banks are there and driving everyone’s positioning, my friend Bob Savage said yesterday: “we’ve been trained to catch the falling knife by the central banks, one of those trading strategies that will work until it doesn’t and when the knife slips you will really have a taper tantrum.”

It’s becoming harder and harder to look at the news and then guess what market did in response – although it’s a fun game to play at 3 in the morning when you can’t sleep. May perhaps be better to consider not so much trading the reaction to events, instead trade movements in anticipation thereof, trade the expectation, then go into the number flat, the expectation tends to be much more logical than the reaction. If you look at how markets are trading, they move ahead of a central bank meeting, or a strong or weak number, then everyone is caught with same position and you end up being right but proven wrong.

Welcome to the new normal.

Two articles about a serious hiccup in the oil that keeps the engine sputtering along.

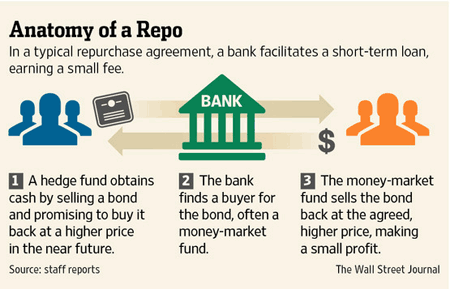

• Banks Retreat From Repo Market That Keeps Cash Flowing (WSJ)

A critical part of the plumbing that keeps money flowing through the financial system is experiencing turmoil as new regulations prompt banks to step back from the multitrillion-dollar “repo” market. The large and opaque market for repurchase agreements helps keep finance and trading moving, allowing hedge funds, investment banks and other financial firms to borrow and lend short-term funds, often overnight. But there have been increasing signs of trouble. Big banks, which act as middlemen between borrowers and lenders, have been pulling back. In recent weeks, senior bankers have said they are reluctant to participate in the market because of regulatory requirements that make repo trading more expensive. Goldman Sachs reduced its repo activity by about $42 billion in the first six months of this year, citing capital requirements. Barclays cut back lending through repos and similar agreements by roughly $25 billion, to $289 billion in the first half of the year.

Bank of America and Citigroup made first-half reductions in repo lending of about $11.4 billion and about $8 billion, respectively. J.P. Morgan’s repo lending stayed roughly flat. Repos function as short-term loans, which are backed by collateral, such as a U.S. government bond. Borrowers agree to sell the bonds to another party for cash, with the promise to repurchase the bond at a slightly higher price some time in the future. Borrowers are often hedge funds and lenders are typically money-market funds. The banks’ pullback could make it harder for hedge funds to borrow, and money-market funds may have fewer places to invest. Investors generally may find it harder to find a trading partner for hedges or short sales. Risks posed by the repo market are the focus of a conference on Wednesday sponsored by the Federal Reserve Bank of New York. The diminishing role of banks in repos “could exacerbate swings in markets when interest rates rise” or other financial turbulence emerges, said Barclays analyst Joseph Abate.

• From A Flood Of Treasury Debt To A Scarcity Of Repo Collateral (Stockman)

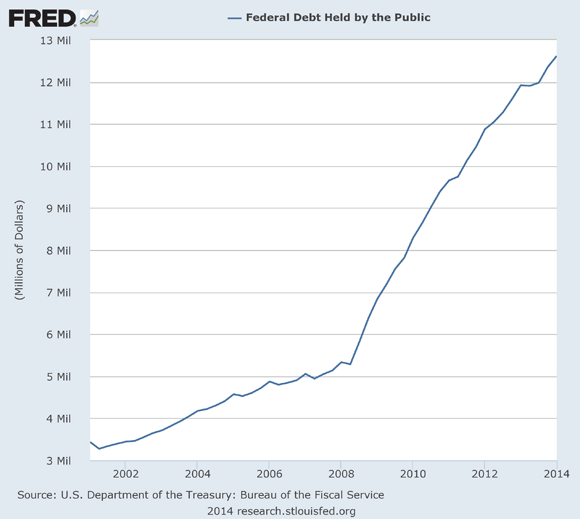

Here’s a shocking tidbit. The Fed’s financial repression policies have so contorted the government bond market that repo on 5-year treasuries has recently been trading at a negative 25 basis points. That’s right. The hunger for good collateral is so great on Wall Street that some players are willing to lend short-term cash at a negative rate in order to get their hands on Uncle Sam’s debt paper. Now that’s some kind of financial deformation. For the past 14 years, in fact, Washington has been spewing red ink at unprecedented rates. Since the year 2000, publicly held treasury debt has soared from $3.5 trillion to about $12.6 trillion at present. And its first cousin—–defacto government debt issued by GSE’s such as Fannie and Freddie—-has exploded from $2 trillion to more than $6 trillion. So in theory, the markets should be floating on a sea of “good” collateral.

But that’s where this century’s massive outbreak of central bank money printing comes in. In their lunatic quest to stimulate jobs and growth through ultra-low interest rates, the central banks have absorbed massive amounts on government debt through their QE operations. The US central bank alone has expanded its balance sheet from $500 billion to nearly $4.5 trillion since the time of the dotcom bust in 2000. That means that enormous amounts of otherwise available collateral has been stuffed in the vaults of the state’s monetary central planning agency. During the final phase of QE, in fact, the Fed has focused its purchases on the so-called “belly” of the curve, scarfing up huge amounts of treasury paper in the 3-7 year maturity range. Accordingly, it has created an enormous and insensible scarcity which, in turn, has driven the yield on the 5-year treasury note to the absurd level of 1.6%.

Now the fact of the matter is that US treasuries are taxable; the current CPI rate is running at 2%; and it has averaged 2.4% over the last decade and one-half. So the real after-tax return on the 5-year note is deeply negative. Needless to say, nothing like that could happen in an honest free market for debt that was not pegged and administered by the Fed. Moreover, the Fed has had a lot of central bank help in creating this destructive artificial scarcity in the government debt market. Altogether, the central banks of the world and their sovereign investment fund affiliates own about $6 trillion or nearly half of the publicly held US treasury debt. It has simply been stuffed in the central bank vaults which function as a convoy of monetary roach motels: The bonds go in, but they never come out!

Yeah, let’s start complaining about the meth running out.

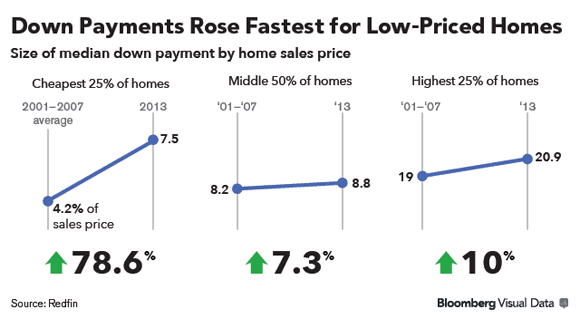

• More Money Down Adds to U.S. First-Time Buyer Blues (Bloomberg)

The challenges facing prospective buyers of the least expensive homes in the U.S. are getting harder to overcome. Already beset by stagnant wages, growing student debt and competition from investors who are snapping up listings, those looking to purchase moderately priced houses must also provide more cash up front. The median down payment for the cheapest 25% of properties sold in 2013 was $9,480 compared with $6,037 in 2007, the last year of the previous economic expansion, according to data from 25 of the largest metro areas compiled by brokerage firm Redfin Corp. The higher bar is a symptom of still-tight credit that is crowding out first-time buyers even as interest rates remain near historical lows. Younger adults, who would normally be making initial forays into real estate, are among those most affected, weakening the foundations of the housing market and limiting its contribution to economic growth.

“The numbers tell the story of why we have millions of potential homeowners who are renters or living with their parents,” said Susan Wachter, a professor of real estate and finance at the University of Pennsylvania’s Wharton School. “What has changed is the ability to become an owner. And that’s changed through a down payment that’s more than doubled.” [..] Mortgage originations dropped last quarter to the lowest level in 14 years, contributing to a decline in total consumer debt, the Fed of New York reported today. Mortgage originations decreased by $46 billion in the second quarter to $286 billion, marking the lowest level of new mortgage activity since 2000, the data show. Banks don’t want to make loans to borrowers they consider to be riskier because they’re worried about having to buy back the loans, said Mike Calhoun, president of the Center for Responsible Lending. And if they do give mortgages to borrowers who have lower credit scores, they’ll require a larger down payment to offset that risk, he said.

Germany should get out of the eurozone just as much as Italy should. Much better for both.

• End of the Wirtschaftswunder? Germany’s Sudden Slowdown (Reuters)

The German soccer team’s romp to victory in last month’s World Cup was hailed at home as a symbol of the country’s emergence as a confident global economic power. But in an ironic twist, the feel-good triumph in Brazil may have come at a time when Germany’s new “Wirtschaftswunder”, or economic miracle, is coming to an end. In recent weeks, the economy that proud German politicians have taken to describing as a “growth locomotive” and “stability anchor” for Europe, has been hit by a barrage of bad news that has surprised even the most ardent Germany skeptics. The big shocker came on Thursday, when the Federal Statistics Office revealed that GDP had contracted by 0.2% in the second quarter. The euphoria that we’ve seen, the perception that the German economy is booming is simply misplaced,” said Marcel Fratzscher, director of the DIW economic institute in Berlin. So why is Germany suddenly ailing? The standoff with Russia over Ukraine has received its fair share of blame in the German media.

But that conflict may not hit the economy with full force until the third quarter. It was only last month that Europe stung Moscow with economic sanctions, prompting a tit-for-tat response from Russian President Putin. In reality, economists and some government officials acknowledge, there are deeper reasons for the recent downturn. And they have little to do with the spike in geopolitical tensions in eastern Europe or the Middle East. They start at home, where Chancellor Angela Merkel’s abrupt exit from nuclear energy after the Fukushima disaster in Japan and aggressive push into renewables has unnerved German industry. A recent overhaul of the country’s complex renewable energy law has done little to alleviate uncertainty over future policy or assuage fears about German energy competitiveness. “Energy intensive industries in particular have lost confidence in the future of Germany as a business location,” said Thomas Mayer, a former chief economist at Deutsche Bank. “I think this is a major issue that will burden German industry for years to come.”

Would QE have been good for Europe? Put it this way: has the US really reached escape velocity, or is that just an illusion brought about by debt, an illusion that will crack as soon as interest rates go up?

• Germany Is Itself A Victim Of EMU Austerity Fanatics (AEP)

So now we learn. Germany had a double-dip recession last year without telling us. This could soon turn into triple-dip after contraction of 0.2% in the second quarter. German bond yields are pricing in stagnation as far as the eye can see. 10-year Bunds fell below 1% this morning for the first time in history, and far below levels seen during the deflationary episodes of the Second Reich in the late 19th Century. The bond markets are flashing deflation warnings, but they are also indicting the European authorities for gross incompetence. Professor Paul De Grauwe from the London School of Economics says policy elites have misdiagnosed the fundamental cause of Europe’s chronic slump and its failure to recover. They are treating a demand crisis as if it were a supply crisis, imposing “reforms” – an Orwellian touch – that can only exacerbate EMU-wide distress in the short-run. “They are doing everything they can to stop recovery taking off, so they should not be surprised if there is in fact no take-off,” he said.

“It is balanced-budget fundamentalism, and it has become religious. We know from the 1930s that if everybody is trying to pay off debt and the government then deleverages at the same time, the result is a downward spiral,” he said. “The rigidities in the European economy have been there for ages. They have absolutely nothing to do with the problem we face today.” The claim that Spain’s recovery validates the EMU strategy of retrenchment and reform makes you want to weep. To the extent that Spain has reached self-sustaining take-off – questionable given the collapse of investment and the damage from labour hysteresis – it is largely because Spain is pursuing a beggar-thy-neighbour wage squeeze policy, just as Germany did nine years ago with such malign effects for the eurozone as a whole. This displaces the contractionary pressures into France and Italy. “You can do this in one country but it can’t possibly be a model for the whole eurozone. If everybody does this it leads to generalised deflation, and that is what we are seeing,” he said.

Too late.

• France Calls On ECB To Act As Eurozone Growth Grinds To A Halt (Guardian)

France piled pressure on the European Central Bank to do more to boost growth on Thursday after news that economic activity across the 18-nation single currency area came to a halt in the second quarter. With France registering zero growth for a second successive quarter, Michel Sapin, the country’s finance minister, halved his growth forecast for this year, abandoned the deficit reduction target and said it was up to the Frankfurt-based ECB to respond to an “exceptional situation of weak growth and weak inflation across the eurozone”. Sapin’s demand came as the latest figures from Eurostat, the European Union’s statistical agency, showed that problems in the single currency’s Big Three economies – Germany, France and Italy – resulted in no increase in eurozone gross domestic product in the three months to June. That compares with an increase of 0.2% in the first quarter.

But financial markets saw no immediate prospect of the ECB launching its own money creation (quantitative easing) programme until next year at the earliest, amid concerns that countries such as France and Italy would row back on structural reform if fresh growth-boosting stimulus policies were introduced. The interest rate – or yield – on 10-year German bonds briefly fell below 1% for the first time as dealers anticipated a protracted period of low growth, low inflation and low interest rates. Markets already knew that Italian output had contracted by 0.2% in the second quarter but were surprised by a similar-sized fall in Germany, which was hurt by a more challenging climate for its key export sector.

France made it clear it blamed foot-dragging on the part of the ECB for the failure of the eurozone’s second-biggest economy as it reduced its growth forecast for 2014 from 1% to 0.5% and ditched the 1.7% forecast for 2015, saying it would not expand by much more than 1%. Francois Hollande’s government had negotiated special dispensation from Brussels to run a budget deficit of 3.8% of GDP this year rather than 3%, but Sapin said it was the ECB’s fault that this would not be hit. “We must adapt the pace of deficit reduction to the exceptional situation … of growth that is too weak everywhere in Europe and the exceptional situation of inflation that is too weak across Europe,” Sapin told Europe 1 radio. He also used an article in Le Monde to urge the ECB to do more to combat the threat of deflation and to reduce the level of the euro. “The truth is that, as a direct consequence of sluggish growth and insufficient inflation, France will not meet its public deficit target this year despite a complete control of spending.”

What else could they possible do?

• France Risks EU Deficit Clash After Scrapping Targets (Bloomberg)

The French government abandoned its 2014 deficit targets after the economy unexpectedly failed to grow for a second straight quarter, risking a clash with European partners striving to meet their own fiscal goals. Finance Minister Michel Sapin said that European policy is partly to blame for the lack of expansion in the region’s second-biggest economy. French gross domestic product stagnated in the three months through June, national statistics office Insee said today in Paris. Economists forecast a 0.1% gain, a Bloomberg survey showed. Sapin’s comments will fan a debate about France’s repeated inability to meet European Union fiscal rules it helped write, with Germany advocating reforms and prudent spending to help meet deficit targets and other EU members led by Italy seeking more budgetary leeway. The European Commission has already allowed France to delay deficit targets twice in the wake of the region’s sovereign debt crisis. “There are European causes and there are French causes for the lack of growth,” Sapin said on Europe 1 radio. “The rules allow flexibility for the situation we are facing.”

Wait a minute: if not consumer spending or exports, where did the UK get its (was it 5.1%?! UPDATE: it was 3.1%, just raised to 3.2%) growth number from?

• UK Exports To EU Are ‘Dead In The Water’ (BBC)

The UK’s economic recovery is unlikely to be export driven as its biggest trading partner is “dead in the water”, a Bank of England policymaker has said. In a rare interview by a Monetary Policy Committee member, David Miles told the BBC it was “pretty difficult” to see UK exports growing because of economic problems in the eurozone. But he said the UK’s recovery was no longer being led by consumer spending. Earlier official figures showed eurozone GDP was flat. Professor Miles told Radio 5 Live’s Wake up to Money, UK export growth had been “pretty disappointing” over the last two or three years. He said the “single biggest factor” behind the lack of export growth had been that demand in the eurozone had been close to zero during that time. Professor Miles added: “So our single biggest export market has been, I’m tempted to say, dead in the water. It hasn’t been growing at all. And it’s pretty difficult in that environment to see exports growing very strongly. So the recovery, very welcome as it is, has been a bit dependant on consumer spending.”

The Bank policymaker’s comments highlight the difficulties the government faces in its attempts to re-balance the economy and boost exports. The government wants UK exports to reach £1trn in value a year by 2020 and for 100,000 more UK companies to be exporting by the end of the decade. In his March Budget statement, the chancellor announced help for firms to encourage more investment and exports. The annual 100% tax allowance for business investment was doubled to £500,000 and will run to the end of 2015. The amount of government credit available to support overseas sales was also doubled, to £3bn. “We’re not going to have a secure economic future if Britain doesn’t earn its way in the world,” Mr Osborne said at the time. “We need our businesses to export more, build more, invest more and manufacture more.” Professor Miles’ remarks followed official figures released on Wednesday showing average wages grew at their slowest annual pace since records began in 2001.

Germany, France and Italy are 2/3 of the Eurozone economy. That 2/3 contracted.

• Europe’s Economy Is Broken (Bloomberg)

Investors were expecting bad numbers, but not this bad: Europe’s economies stalled in the second quarter, new figures show. How much longer will Europe’s policy makers just stand there? Since the global financial crisis of 2008, the U.S. and the U.K. have seen output grow more slowly than in previous recoveries. That’s nothing to boast about. Still, six years on, gross domestic product is higher in both countries than it was at the pre-crisis peak. Europe’s output remains 2.4% below that benchmark. And the gap isn’t closing. All three of the euro area’s biggest economies — Germany, France and Italy — are failing. Germany’s output actually fell in the second quarter. So did Italy’s, for the second consecutive quarter. (Whether this is a new recession for Italy or a continuation of the old one is debatable.) The European Central Bank currently forecasts a rise in euro-area output of 1% this year. Expect that to be revised down next month.

With inflation in the euro area running at 0.4% — way below the ECB’s target of less than but close to 2%, and far too close to outright deflation — why isn’t the ECB trying harder to ease monetary policy? Its official answer is that it adopted new measures in June, including an expanded program of support for bank lending. These, it says, should be given time to work. Patience is often a virtue in central banking, but not in this case. The ECB’s measures in June were timid, and the risks are increasingly skewed toward deflation and further prolonged stagnation or worse. The euro area needs quantitative easing of the kind applied by the U.S. Federal Reserve and the Bank of England. The case for this has been strong for months; now it’s overwhelming. The ECB is nervous because outright QE faces political and legal obstacles. One way or another, those issues will have to be resolved — and that’s what ECB President Mario Draghi needs to start saying. Whatever it takes, Mr. Draghi.

Nothing blip about it.

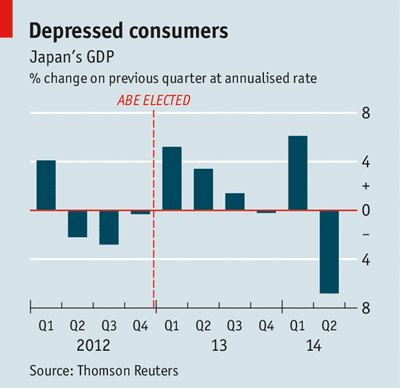

• Japan’s Sudden, Sharp Contraction May Be More Than A Blip (Economist)

The government of Shinzo Abe, Japan’s prime minister, has put a brave face on the news that GDP shrank by 1.7% in the second quarter of this year. Akira Amari, the economy minister, blamed the fall, of an annualised 6.8%—the steepest since the earthquake and tsunami that pummelled Japan in 2011—on the decision to raise the consumption tax from 5% to 8% in April and said the economy will rebound. Not everyone is so sanguine. Worryingly, private consumption plunged by 5% from the previous quarter. Besides having stocked up ahead of the tax rise, households are feeling squeezed by higher prices in the shops. Mr Abe’s most vaunted achievement has been to reverse years of stubborn deflation, a strategy that depends on wages rising. Yet in real terms they fell by 3.2% year-on-year in the second quarter, the steepest drop in 18 quarters, according to Barclays Research in Tokyo.

Most analysts expect Japan’s increasingly tight labour market to push wages up in the coming months, but many of the jobs created under Mr Abe are “non-regular”, with lower pay and benefits. That will embolden critics of Abenomics, who claim that it is enriching corporations and investors and leaving the rest behind. The signs for Mr Abe are ominous: his popularity has fallen below 50% for the first time since he took office in December 2012. The Bank of Japan has pumped billions of dollars into the economy to buy up government debt, which has driven the yen down against the dollar. Yet exports have been sluggish; the main impact of the cheaper yen seems to have been to push up the price of Japan’s imported-fuel bill. The new data also complicate Mr Abe’s pledge to raise the consumption tax by a further two%age points next year. Everyone remembers the effect of a previous tax hike, from 3% to 5%, in 1997. Then, a recovering economy tumbled back into recession.

But as income sources for the shadow banks are repleted through government policies, the highly leveraged products they hold risk blowing up in domino fashion.

• China’s Savers Put Record $2.1 Trillion in Wealth Products (Bloomberg)

Chinese households increased the amount of savings diverted into wealth-management products to a record 12.7 trillion yuan ($2.1 trillion) as the government tries to manage risks from an explosion in shadow banking. The outstanding value rose 24% in the first half from the end of last year, the China Banking Wealth Management Registration System said on its website today. The average annualized return was 5.2%, compared with 3% for benchmark one-year deposits. As signs emerge of weakening demand and rising default risks for higher-yield trust products, sales of the wealth products may keep surging. For banks, a more than 12-fold increase in the value of the products since 2009 is pushing up funding costs, threatening to weigh on profits. “Compared with trust products, wealth-management products are less risky,” Cao Yang, an analyst at Shanghai Pudong Development Bank Co., said by phone.

China’s government is trying to contain risks outside the formal banking system while sustaining growth as the property market slumps and the economy heads for the slowest expansion since 1990. Trust companies’ assets under management fell in June, the China Trustee Association said Aug. 11. Investors have protested outside some banks this year after delays in trust-product payments. Wealth-management products typically require a minimum investment of 50,000 yuan, while trusts target wealthy clients with a minimum investment of 1 million yuan. Today’s number compares with a 44% gain in the value of the wealth products in 2013, according to the China Banking Regulatory Commission. Almost 70% of the outstanding value of the wealth funds was invested in bonds, the money market and bank deposits as of the end of June, according to today’s report. About 23% were in so-called non-standard credit assets, such as loans.

From a 1.4% increase in January to 1.2% in July to 0.4% now. Pretty fast. What’s next?

• Bank of Japan Mulls Cutting 2014 Growth Forecast – Again (Bloomberg)

The Bank of Japan may cut its growth forecast for this fiscal year for a fourth time, as exports fail to bolster an economy weakened by April’s sales-tax increase, according to people familiar with the central bank’s discussions. The expansion for the 12 months through March 2015 is likely to be lower than the 1% median forecast of BOJ board members, said the people, who asked not to be named because the talks are private. Growth is likely to be 0.4%, according to the median estimate in a survey of 24 economists by Bloomberg News on Aug. 13-14.

Another downward revision when the board reviews its outlook in October would underscore waning momentum in the world’s third-biggest economy. Governor Haruhiko Kuroda faces increased pressure to boost his unprecedented stimulus after Japan’s deepest contraction in more than three years in the second quarter, according to economists at Citigroup Inc. and Morgan Stanley MUFG Securities Co. “We think the BOJ will have no option but to revise down its projections again,” said Takeshi Yamaguchi, an economist at Morgan Stanley MUFG Securities Co. The weaker outlook contrasts with the government’s decision last month to raise its assessment of the economy for the first time in six months. The downturn in demand that followed the sales-tax increase was easing, the Cabinet Office said in a report on July 17.

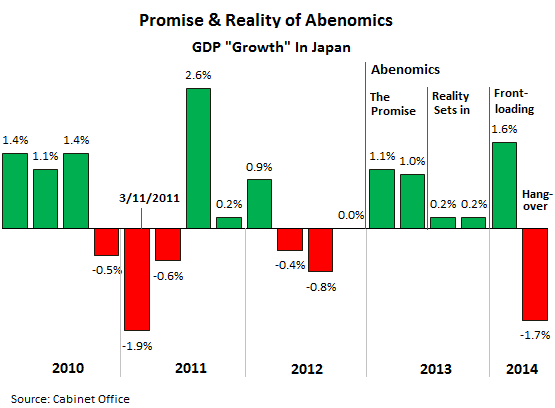

• The Flame-Out Of Abenomics, in One Crucial Chart (WolfStreet)

Abenomics had its moments. At first, given the soaring stock market and the feel-good atmosphere, the economy perked up, growing in the first half of calendar year 2013 at a nice clip. Then stocks tanked, optimism faded. Promise, hype, and hope were replaced by reality and by “inflation without compensation.” Hence near stagnation in the second half of 2013. Then a miracle happened: The effective date of the consumption tax hike, April 1, the beginning of Japan’s fiscal year, moved closer and triggered a historic bout of frontloading by consumers and businesses alike. In an environment where money in low-risk investments earned nothing, and where inflation was rising, the government had handed consumers and businesses a way to save 3% at every major purchase. It’s like 3% risk-free income. For households, it was tax-free! Frontloading turned into a frenzy. And GDP jumped 1.6% in the January-March quarter. It was the finest moment of Prime Minister Shinzo Abe’s regime, and Abenomics apologists scattered across the globe, praising his endless wisdom.

Then in the April-June quarter (Q1 in Japan), a terrific hangover set in. More than a hangover.GDP plunged 1.7% from prior quarter, an annual rate of -6.8%, the Cabinet Office reported. It was the worst decline since January-March 2011 when the earthquake and tsunami on March 11, and the subsequent triple meltdowns at the Fukushima nuclear plant, nearly brought the Japanese economy to a halt, freezing up supply chains and transportation systems. Thousands of aftershocks, some of them serious earthquakes in their own right, continued to wreak havoc for months. Electricity was in short supply…. Those were terrible months. During that tragic quarter, GDP plummeted 1.9%.That GDP in the April-June quarter this year was just two notches less terrible (-1.7%) is a sign that it wasn’t just a hangover from a bout of frontloading. It ate up not only the entire growth of the January-March quarter (+1.6%) but also half of the growth of the September-December quarter (+0.2%). It’s not a pretty picture:

Note the sudden impact of the stimulus after the earthquake in 2011, followed by its big fade that lasted four quarters. That’s how stimulus works. Then, in the first half of 2013, the beginning of the Abenomics era, the economy got high on promise, hype, and hope and on money-printing. In the second half, reality set in, and the economy languished. And so far in 2014, the net effect of frontloading and hangover is that GDP has actually declined. The last quarter was ugly throughout. Consumption by households dropped 5.2%, and excluding “imputed rent,” 6.2%. Consumers drastically cut back on buying big-ticket items and confronted steep price increases while their incomes stagnated. Private residential investment plunged 10.3%. Only government consumption ticked up. But that’s not the whole story to the GDP fiasco: Imports had soared during the quarter, compared to the same period a year earlier, while exports limped along. So the trade deficit for the quarter ballooned by 23.6% year over year.

“The more interesting mystery is how the ISIS fighters learned how to use Uncle Sam’s advanced weaponry so quickly. Perhaps the CIA knows.”

• Washington’s Iraq Puzzle Palace Keeps Getting Curiouser (Stockman)

Not surprisingly, after the US had “liberated” Iraq from 90 years of dictatorship—democracy took hold with lightening speed subsequent to the 2011 departure of American GIs. The “rule of the majority”—that is, the Shiite majority—-soon ripped through most governmental institutions, but especially the military. In short order the “Iraqi” army became a Shiite army. Hence the precipitous surrender and flight from the battles of Mosul and other northern cities. That was Sunni and Kurd territory—–not a place where Shiite soldiers wanted to be shot dead or caught alive. The more interesting mystery is how the ISIS fighters learned how to use Uncle Sam’s advanced weaponry so quickly. Perhaps the CIA knows. It did train several thousand anti-Assad fighters in its secret camps in Jordan in preparation for Washington’s “regime change” campaign in Syria. Undoubtedly, in the fog of war—-especially the sectarian wars in the Islamic heartland that have been raging for 13 centuries—it is difficult to have friend and foe vetted effectively.

But effective vetting or no, the purpose of training Sunni fighters in Syria was to achieve a key Washington strategic objective. Namely, to breakup and disable the fearsome “Shiite Crescent”, ranging from Hezbollah in Lebanon through Assad’s Alawite-Shiite regime in Syria to the seat of the Axis-Of-Evil itself—-the purportedly nuke seeking Shiite theocracy of Iran. To be sure, the CIA had re-certified as recently as 2008 that the Iranians had disbanded a few incipient nuclear weapons experiments years earlier. Likewise, the medieval mullahs who rule Iran had issued fatwas against a nuclear weapons program in any form. But so great was the Shiite threat deemed to be by Washington that both Secretary of State Hillary Clinton and the peace president himself announced the Assad “must go” peacefully or Washington would wage war against him. And this was all part of the grand scheme of disabling the fearsome Shiite Crescent.

“It’s very difficult for the EU to squeeze Islamic State through sanctions because the group is selling oil in a global market through Turkey, and is doing so at a 75% discount of about $25 a barrel …”

• EU Weighs Oil Steps Against Islamists While Arming Kurds (Bloomberg)

European Union governments are set to explore ways to squeeze the finances of Islamist militants bolstered by oil fields captured during their advance through Iraq. EU foreign ministers due to attend an emergency meeting in Brussels today plan to consider options on oil-market measures and the direct supply of arms to Kurdish forces fighting Islamic State in northern Iraq, an EU official told reporters, asking not be named because the discussions are private. Representatives of the 28 EU governments are stepping up their collective response with the U.S. to the cross-border threat posed by Islamic State that has prompted thousands of Yezidis and Christians to flee their advance. Iraq and Ukraine are on the agenda for the talks called by EU foreign-policy chief Catherine Ashton, scheduled to start at noon.

The EU will have an uphill struggle to curb the militants’ revenue from oil, Philipp Chladek, a London-based energy analyst at Bloomberg Intelligence, said by phone. “It’s very difficult for the EU to squeeze Islamic State through sanctions because the group is selling oil in a global market through Turkey, and is doing so at a 75% discount of about $25 a barrel,” he said. On Ukraine, the foreign ministers will discuss the outlook for international humanitarian aid for eastern areas of the country, where government forces are fighting pro-Russian rebels, and the impact of Russia’s recent ban on imports of some EU foods. The ministers will probably stop short of expanding sanctions against Russia imposed as a result of its encroachment in Ukraine, the EU official said yesterday.

Key line: “European energy companies will have to agree major contract revisions when purchasing Russian natural gas”…

• Ukraine Approves Law On Sanctions Against Russia (Reuters)

The Ukrainian parliament approved a law on Thursday to impose sanctions on Russian companies and individuals supporting and financing separatist rebels in eastern Ukraine. The government has already prepared a list of 172 citizens of Russia and other countries, and of 65 Russian companies, including gas export giant Gazprom, on whom they could impose sanctions “for financing terrorism”. After Thursday’s vote, Prime Minister Arseny Yatseniuk told parliament that Ukraine had taken a historic step. “By approving the law on sanctions, we showed that the country is able to protect itself,” he said. “The law should give a clear answer to any aggressor or terrorist who threatens our national security, our government and our citizens.” Ukraine said on Monday that European energy companies will have to agree major contract revisions when purchasing Russian natural gas if parliament approved sanctions on Gazprom.

So who’s paying and arming them? Or should we say: who’s actually doing the fighting?

• Ukraine’s Broke Military Is Underpaid and Undertrained (BW)

A group of men and a few women clad in neat, matching camouflage uniforms and combat boots walk through an airport, presumably on their way to the front. As the soldiers make their way toward their gate, people around them rise in applause. A message appears on the screen: “Come back alive,” along with directions for contacting Ukraine’s volunteer brigades and donating to the military. The video commercial shows the army Ukraine would like to have: a streamlined, battle-ready group that’s a source of pride for the country. But it also hints at the fighting force that Ukraine has today: one with a heavy reliance on support from volunteer soldiers and donations from across the country to help keep it properly outfitted. “At the beginning of March, there was nothing,” says Oleksiy Melnyk, an analyst with Razmykov Center, an independent think tank in Kiev. When Russia annexed Crimea about a month after the EuroMaidan uprising, the interim government had limited options.

To prevent the loss of Ukraine’s eastern Donetsk and Lugansk regions to pro-Russia separatists, the government has reinstated the military draft and launched a national campaign asking for donations to replenish the military’s depleted coffers. Thus far the donation campaign has raised more than $11.7 million, according to the BBC. Volunteers, many spurred on by a rise in patriotism in the wake of the Maidan protests, have also helped to boost the armed forces’ numbers. The National Guard has integrated former members from Maidan’s self-defense forces into its ranks. Other informal fighting battalions have emerged in recent months that are sometimes very loosely affiliated with, or entirely independent from, official government forces. The emergence of such battalions is a reflection of how weak Ukraine’s military was at the beginning of the eastern conflict. “I think the only reason that these battalions get a chance is because at this time, three months ago, the Ukrainian government was ready to accept probably any help it could get,” says Melnyk.

And he’ll keep on making the deals, one by one.

• Putin Says Russia Should Aim To Sell Energy In Roubles (Reuters)

President Vladimir Putin said on Thursday Russia should aim to sell its oil and gas for roubles globally because the dollar monopoly in energy trade was damaging Russia’s economy. “We should act carefully. At the moment we are trying to agree with some countries to trade in national currencies,” Putin said during a visit to the Crimea region, which Moscow annexed from Ukraine earlier this year.

Hungary is in an interesting location.

• Europe “Shot Itself In The Foot” With Russia Sanctions: Hungary PM (Reuters)

The European Union has shot itself in the foot economically with the sanctions its has imposed on Russia over Ukraine, Hungarian Prime Minister Viktor Orban said on Friday, calling for a rethink of policy. “The sanctions policy pursued by the West, that is, ourselves, a necessary consequence of which has been what the Russians are doing, causes more harm to us than to Russia,” Orban said in a radio interview. “In politics, this is called shooting oneself in the foot.”

Scarier by the day.

• Evidence Suggests Ebola Toll Vastly Underestimated (Reuters)

Staff with the World Health Organization battling an Ebola outbreak in West Africa see evidence the numbers of reported cases and deaths vastly underestimates the scale of the outbreak, the U.N. agency said on its website on Thursday. The death toll from the world’s worst outbreak of Ebola stood on Wednesday at 1,069 from 1,975 confirmed, probable and suspected cases, the agency said. The majority were in Guinea, Sierra Leone and Liberia, while four people have died in Nigeria. The agency’s apparent acknowledgement the situation is worse than previously thought could spur governments and aid organizations to take stronger measures against the virus. “Staff at the outbreak sites see evidence that the numbers of reported cases and deaths vastly underestimate the magnitude of the outbreak,” the organization said on its website. “WHO is coordinating a massive scaling up of the international response, marshaling support from individual countries, disease control agencies, agencies within the United Nations system, and others.”

Misleading numbers: you can’t maintain a stable grid with more than 15% intermittent energy. So Germany can only be this “green” because its neighbors, on the same grid, are not.

• Germany Gets 31% of Its Electricity From Renewables (BW)

As Europe struggles to ease its dependency on Russian gas, Germany is getting ever greener: During the first half of 2014, the nation generated 31% of its electricity from renewable energy sources, according to a recent report by the Fraunhofer Institute. Excluding hydro, renewables accounted for 27% of electricity production, up from 24% last year. “Solar and wind alone made up a whopping 17% of power generation, up from around 12% to 13% in the past few years,” according to Renewables International, which provides a helpful rundown of the Fraunhofer report. The country’s solar power plants increased total production by 28% compared with the first half of 2013, while wind power grew about 19%. Germany still derives most of its energy from coal, though consumption of brown coal dropped 4%. Power from natural gas fell 25%, while nuclear power decreased by only about 2%.

The U.S. produces far more renewable energy than Germany in terms of quantity. But as a % of total energy production, America falls short. In 2013 wind accounted for 4% of total electricity generation, and solar made up 0.23%, according to the U.S. Energy Information Administration. Geothermal was at 0.41%; biomass, 1.48%. Germany’s government and population are famous for their environmental zeal. “Green, do-gooding Germans have long been at the sharp end of jokes, often for good reason,” writes Rose Jacobs in her Newsweek piece, “Doing It the German Way.” “Their water conservation efforts were so enthusiastic in the 1990s and early 2000s that by 2009 sewage systems were suffering from too little water running through them.”

Home › Forums › Debt Rattle Aug 15 2014: Conditioned To Catch The Falling Knife