Taylor Deluxe Kauneel auto trailer, Bay City, Michigan May 1936

An absolute must read by Lynn Stuart Parramore.

• “We Are Starting To Break Down”: Why So Many Americans Feel Traumatized (Salon)

Recently Don Hazen, the executive editor of AlterNet, asked me to think about trauma in the context of America’s political system. As I sifted through my thoughts on this topic, I began to sense an enormous weight in my body and a paralysis in my brain. What could I say? What could I possibly offer to my fellow citizens? Or to myself? After six years writing about the financial crisis and its gruesome aftermath, I feel weariness and fear. When I close my eyes, I see a great ogre with gold coins spilling from his pockets and pollution spewing from his maw lurching toward me with increasing speed. I don’t know how to stop him. Do you feel this way, too?

All along the watchtower, America’s alarms are sounding loudly. Voter turnout this last go-round was the worst in 72 years, as if we needed another sign that faith in democracy is waning. Is it really any wonder? When your choices range from the corrupt to the demented, how can you not feel that citizenship is a sham? Research by Martin Gilens and Benjamin I. Page clearly shows that our lawmakers create policy based on the desires of monied elites while “mass-based interest groups and average citizens have little or no independent influence.” Our voices are not heard.

When our government does pay attention to us, the focus seems to be more on intimidation and control than addressing our needs. We are surveilled through our phones and laptops. As the New York Times recently reported, a surge in undercover operations from a bewildering array of agencies has unleashed an army of unsupervised rogues poised to spy upon and victimize ordinary people rather than challenge the real predators who pillage at will. Aggressive and militarized police seem more likely to harm us than to protect us, even to mow us down if necessary. Our policies amplify the harm. The mentally ill are locked away in solitary confinement, and even left there to die. Pregnant women in need of medical treatment are arrested and criminalized. Young people simply trying to get an education are crippled with debt. The elderly are left to wander the country in RVs in search of temporary jobs. If you’ve seen yourself as part of the middle class, you may have noticed cries of agony ripping through your ranks in ways that once seemed to belong to worlds far away.

[..] A 2012 study of hospital patients in Atlanta’s inner-city communities showed that rates of post-traumatic stress are now on par with those of veterans returning from war zones. At least 1 out of 3 surveyed said they had experienced stress responses like flashbacks, persistent fear, a sense of alienation, and aggressive behavior. All across the country, in Detroit, New Orleans, and in what historian Louis Ferleger describes as economic “dead zones” — places where people have simply given up and sunk into “involuntary idleness” — the pain is written on slumped bodies and faces that have become masks of despair. We are starting to break down.

Brilliant piece by buddy Jim: “All of these evil systems have to go and must be replaced by more straightforward and honest endeavors aimed at growing food, doing trade, healing people, traveling, building places worth living in, and learning useful things.”

• Buy the All Time High (James Howard Kunstler)

Wall Street is only one of several financial roach motels in what has become a giant slum of a global economy. Notional “money” scuttles in for safety and nourishment, but may never get out alive. Tom Friedman of The New York Times really put one over on the soft-headed American public when he declared in a string of books that the global economy was a permanent installation in the human condition. What we’re seeing “out there” these days is the basic operating system of that economy trying to shake itself to pieces. The reason it has to try so hard is that the various players in the global economy game have constructed an armature of falsehood to hold it in place — for instance the pipeline of central bank “liquidity” creation that pretends to be capital propping up markets.

It would be most accurate to call it fake wealth. It is not liquid at all but rather gaseous, and that is why it tends to blow “bubbles” in the places to which it flows. When the bubbles pop, the gas will tend to escape quickly and dramatically, and the ground will be littered with the pathetic broken balloons of so many hopes and dreams. All of this mighty, tragic effort to prop up a matrix of lies might have gone into a set of activities aimed at preserving the project of remaining civilized. But that would have required the dismantling of rackets such as agri-business, big-box commerce, the medical-hostage game, the Happy Motoring channel-stuffing scam, the suburban sprawl “industry,” and the higher ed loan swindle.

All of these evil systems have to go and must be replaced by more straightforward and honest endeavors aimed at growing food, doing trade, healing people, traveling, building places worth living in, and learning useful things. All of those endeavors have to become smaller, less complex, more local, and reality-based — rather than based, as now, on overgrown and sinister intermediaries creaming off layers of value, leaving nothing behind but a thin entropic gruel of waste. All of this inescapable reform is being held up by the intransigence of a banking system that can’t admit that it has entered the stage of criticality. It sustains itself on its sheer faith in perpetual levitation. It is reasonable to believe that upsetting that faith might lead to war.

The numbers are getting insane.

• The Dismal Economy: 148 Million Government Beneficiaries (Lance Roberts)

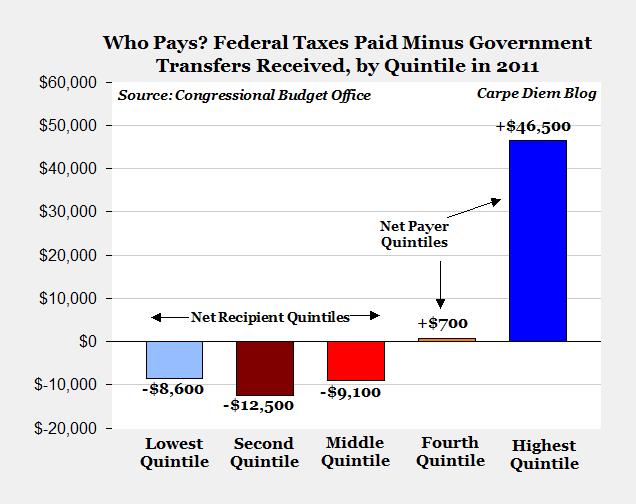

.. the Federal Reserve has stopped their latest rounds of bond buying and are now starting to discuss the immediacy of increasing interest rates. This, of course, is based on the “hopes” that the economy has started to grow organically as headline unemployment rates have fallen to just 5.9%. If such activity were real then both inflation and wage pressures should be rising – they are not. According to the Congressional Budget Office study that was just released, approximately 60% of all U.S. households get more in transfer payments from the government than they pay in taxes.

Roughly 70% of all government spending now goes toward dependence-creating programs. From 2009 through 2013, the U.S. government spent an astounding 3.7 trillion dollars on welfare programs. In fact, today, the percentage of the U.S. population that gets money from the federal government grew by an astounding 62% between 1988 and 2011. Recent analysis of U.S. government numbers conducted by Terrence P. Jeffrey, shows that there are 86 million full-time private sector workers in the United States paying taxes to support the government, and nearly 148 million Americans that are receiving benefits from the government each month.

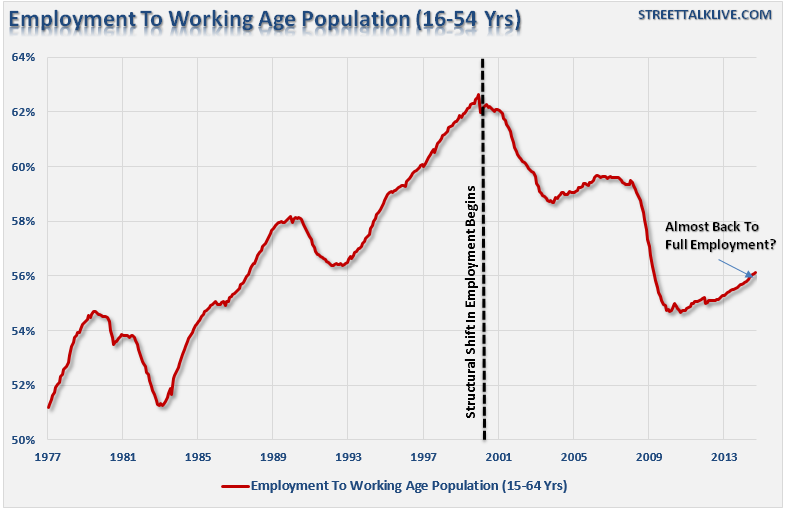

Yet Janet Yellen, and most other mainstream economists suggests that employment is booming in the U.S. Okay, if we assume that this is indeed the case then why, according to the Survey of Income and Program Participation conducted by the U.S. Census, are well over 100 million Americans are enrolled in at least one welfare program run by the federal government. Importantly, that figure does not even include Social Security or Medicare. (Here are the numbers for Social Security, Medicaid and Medicare: More than 64 million are receiving Social Security benefits, more than 54 million Americans are enrolled in Medicare and more than 70 million Americans are enrolled in Medicaid.) Furthermore, how do you explain the chart below? With roughly 45% of the working age population sitting outside the labor force, it should not be surprising that the ratio of social welfare as a percentage of real, inflation-adjusted, disposable personal income is at the highest level EVER on record.

This is how you can pretend to have a recovery.

• The Mystery Of America’s “Schrodinger” Middle Class (Zero Hedge)

On one hand, the US middle class has rarely if ever had it worse. At least, if one actually dares to venture into this thing called the real world, and/or believes the NYT’s report: “Falling Wages at Factories Squeeze the Middle Class.” Some excerpts:

For nearly 20 years, Darrell Eberhardt worked in an Ohio factory putting together wheelchairs, earning $18.50 an hour, enough to gain a toehold in the middle class and feel respected at work. He is still working with his hands, assembling seats for Chevrolet Cruze cars at the Camaco auto parts factory in Lorain, Ohio, but now he makes $10.50 an hour and is barely hanging on. “I’d like to earn more,” said Mr. Eberhardt, who is 49 and went back to school a few years ago to earn an associate’s degree. “But the chances of finding something like I used to have are slim to none.” Even as the White House and leaders on Capitol Hill and in Fortune 500 boardrooms all agree that expanding the country’s manufacturing base is a key to prosperity, evidence is growing that the pay of many blue-collar jobs is shrinking to the point where they can no longer support a middle-class life.

In short: America’s manufacturing sector is being obliterated: “A new study by the National Employment Law Project, to be released on Friday, reveals that many factory jobs nowadays pay far less than what workers in almost identical positions earned in the past.

Perhaps even more significant, while the typical production job in the manufacturing sector paid more than the private sector average in the 1980s, 1990s and early 2000s, that relationship flipped in 2007, and line work in factories now pays less than the typical private sector job. That gap has been widening — in 2013, production jobs paid an average of $19.29 an hour, compared with $20.13 for all private sector positions. Pressured by temporary hiring practices and a sharp decrease in salaries in the auto parts sector, real wages for manufacturing workers fell by 4.4% from 2003 to 2013, NELP researchers found, nearly three times the decline for workers as a whole.

How is this possible: aren’t post-bankruptcy GM, and Ford, now widely touted as a symbol of the New Normal American manufacturing renaissance? Well yes. But there is a problem: recall what we wrote in December 2010: ‘Charting America’s Transformation To A Part-Time Worker Society:”

.. one of the most important reasons for lower pay is the increased use of temporary workers. Some manufacturers have turned to staffing agencies for hiring rather than employing workers directly on their own payroll. For the first half of 2014, these agencies supplied one out of seven workers employed by auto parts manufacturers. The increased use of these lower-paid workers, particularly on the assembly line, not only eats into the number of industry jobs available, but also has a ripple effect on full-time, regular workers. Even veteran full-time auto parts workers who have managed to work their way up the assembly-line chain of command have eked out only modest gains.

“QE only misallocates capital toward more speculation and low-quality debt .. ”

• Overvalued, Overbought, Overbullish, Extremely Vulnerable Markets (Hussman)

.. iwhen concerns about default are rising, default-free, low-interest rate money is not considered to be an inferior asset, and as a result, its increased availability does not provoke risk-seeking behavior. If we observe narrowing credit spreads and stronger uniformity in market internals, we will be able to infer a shift toward risk-seeking (and in turn, a greater likelihood that monetary easing will provoke further speculation). That won’t make stocks any cheaper, and downside risk will still need to be managed, but our immediate concerns would be less dire. At present, current market conditions and the lessons of history encourage us to be aware that very untidy market outcomes could unfold in very short order. [..] QE only misallocates capital toward more speculation and low-quality debt (primarily junk and leveraged loan issuance), without much impact on real growth. [..]

The upshot is this. Quantitative easing only “works” to the extent that default-free, low interest liquidity is viewed as an inferior holding. When investor psychology shifts toward increasing risk aversion – which we can reasonably measure through the uniformity or dispersion of market internals, the variation of credit spreads between risky and safe debt, and investor sponsorship as reflected in price-volume behavior – default-free, low-interest liquidity is no longer considered inferior. It’s actually desirable, so creating more of the stuff is not supportive to stock prices. We observed exactly that during the 2000-2002 and 2007-2009 plunges, which took the S&P 500 down by half in each episode, even as the Fed was easing persistently and aggressively. A shift toward increasing internal dispersion and widening credit spreads leaves risky, overvalued, overbought, overbullish markets extremely vulnerable to air-pockets, free-falls, and crashes.

It hurts to see Canada become so much like the US in so many ways.

• Canada Moving Toward American-Style Inequality (CTV)

A prominent U.S. political economist says Canada is moving toward American-style inequality, and believes austerity economics and tax cuts for corporations are making the problem worse. Robert Reich, the secretary of labor during Bill Clinton’s presidency, now writes extensively on income equality and was in Canada this week speaking at an event for the Broadbent Institute. “The United States economy and the Canadian economy are going on parallel courses,” Reich said in an interview on CTV Question Period. With Japan moving into an official recession and much of Europe still mired in a slowdown, there’s still an idea that countries need to cut government spending during the recovery.

That kind of thinking, Reich says, has the effect of worsening the ratio of debt to the total economy. “Austerity economics does not work,” Reich said. “If you slow down the economy because government is cutting down so much that there’s not enough demand to keep the economy going, then you end up with a worse ratio of debt to GDP.” The U.S. and Canadian economies are growing too slowly, he says. And many wealthy people or corporations, he said, are putting their money in places where they can get the highest return – but that kind of investment isn’t what creates jobs. “Without customers, businesses are not going to create jobs,” he said.

“The long-term cycle points to the dollar moving higher and the euro declining into 2016, while commodities move lower through 2016 and 2017.”

• Oil Seen Dropping Another $30 by ICAP on Commodity, Dollar Cycle (Bloomberg)

New York-traded crude oil will probably drop another $30 in the next two years as long-term cycles in commodities and currencies converge, no matter what happens at this week’s OPEC meeting and Iran nuclear talks, according to brokerage United-ICAP. West Texas Intermediate crude, the U.S. benchmark, has collapsed five times since the contract’s introduction in 1983, said Walter Zimmerman, chief technical strategist for United-ICAP in Jersey City, New Jersey. The plunges in 1986, 1991, 1998, 2001 and 2008 coincided with an OPEC price war, recessions and financial crises, and were also tied to cycles in commodities or the dollar, said Zimmerman, who was calling for a drop in oil prices as early as April. “This time we have both.”

“Crude is heading lower, with the high $40s or low $50s being touched by 2017,” Zimmerman said. The long-term cycle points to the dollar moving higher and the euro declining into 2016, while commodities move lower through 2016 and 2017, he said. The average drop during the previous five major declines was about 62%, according to Zimmerman. Oil prices have dropped 32% from the year’s high in June amid slower economic growth and surging production in the U.S. and OPEC members. The Bloomberg dollar index is up 10% since the low in May and the euro is down 12%. The Bloomberg Commodity Index dropped 17% to a five-year low this month.

“What is the profitability of this production like? It’s from $65 to $83 per barrel. Now when the price of a barrel of oil has fallen below $80, shale gas production becomes unprofitable.” said Putin.”

• Market Manipulation Of Oil Prices Backfires On Those That Start It: Putin (RT)

The modern world is interdependent and there is no guarantee that sanctions, a sharp fall in oil prices, or the depreciation of the ruble won’t backfire on those who provoked them, says Russian President Vladimir Putin. “If undercharging for energy products occurs deliberately, it also hits those who introduce these limitations. Problems arise, they will continue to grow, worsening the situation, and not only for Russia but also for our partners, including oil and gas producing countries,” said Putin in an interview to TASS. The Russian leader suggested that the fall in oil prices is due to the sharp increase in the production of shale oil and gas by the United States, but questioned its commercial viability. “What is the profitability of this production like? It’s from $65 to $83 per barrel. Now when the price of a barrel of oil has fallen below $80, shale gas production becomes unprofitable.” said Putin.

The President said he sees objective reasons for the decline in oil prices. “The supply has increased from Libya, surprising as it may seem it produces more, Iraq as well, despite all the problems … ISIS sell oil illegally at $30 per barrel on the black market, Saudi Arabia increased its production and consumption decreased due to a period of stagnation or, say, a decrease compared with the forecasts of global economic growth,” he said. Talking about the Russian economy and the weakening ruble, Putin said the situation with oil prices doesn’t hit the budget as hard as expected. “…we are confident in solving social issues. Including the ones of the defense industry. Russia has its own base for import substitution,” he said. “Thank God, we’ve received a lot from previous generations, and that we’ve done much to modernize the industry over the past decade and a half. Does it damage us? Partly, but not fatally,” Putin concluded.

SocGen is way off target here, any benefits will vanish along the way. The biggest problem all around today is deflation. Lower oil prices will exacerbate the problem, not solve it. People are simply not going to drive twice as much.

• Global Growth To Get $200 Billion Kick From Oil Price Crash (Telegraph)

Global economies are set for a lift of more than $200bn (£127.4bn) within the next year, thanks to a “once in a generation downturn” in oil prices. Brent – an oil classification that serves as a global benchmark – has already plummeted by as much as 30pc from a peak of $115 a barrel in June. The decline of oil, and the effect that has on lower energy costs, will serve to boost growth and keep inflation contained, according to French bank Societe Generale. The lender’s economists have calculated that a $20 a barrel fall in oil prices could increase global output by an extra 0.26 percentage points after the first year of the shock, with producers in North America and Asia reaping much of the benefit.

This decline in oil has been “a major correction” said Michael Haigh, head of commodities research at the French bank. The downturn differs from previous falls because of its root cause – an oversupply of oil that “is not temporary in nature”, Mr Haigh argued. “We believe that we’re in the middle of a very fundamental change in the oil markets – the type of change that only happens every decade or two”, he added. Oil’s recent fall to around $80 a barrel has been driven “by both weak demand and increased supply”, said Michala Marcussen, Societe Generale’s global head of economics. A marked increase in Libyan oil production alongside a structural rise in US volumes, as a result of the shale boom in North America, have contributed to higher supply. With energy accounting for approximately 9pc of global inflation, a reduction in oil prices should also result in more subdued price growth.

If Brent Crude fell as low as $70 a barrel, this would reduce Societe Generale’s forecast for UK inflation by 0.3 percentage points for the whole of next year. But gains from weaker prices are unlikely to act as a panacea for nations suffering from lower growth. “Policy makers hoping that low oil prices will salvage growth should think twice,” Ms Marcussen cautioned. “In particular euro area leaders would do well to act resolutely on the European Central Bank’s calls for structural reforms at an accelerated pace.”

” .. a 3% increase in government bond rates would result in a change in the value of outstanding government bonds ranging from a loss of around 8% of GDP for the U.S. to around 35% for Japan.”

• How The Fed Has Boxed US Into An Easy-Money Corner (Satyajit Das)

Despite the Federal Reserve ending its purchases of Treasury bonds, U.S. monetary policy remains accommodative — and will be for a long time to come. The downside is too great. Withdrawing fiscal stimulus would slow economic activity. Reduction in government services and higher taxes hits disposable incomes, especially when wage growth is stagnant. In turn, this leads to a sharp contraction in consumption. Slower growth, exacerbated by high fiscal multipliers, makes it difficult to correct budget deficits and control government debt levels. Accordingly, the Fed’s ability to reverse an expansionary fiscal policy is restricted, at best, corroborating economist Milton Friedman’s sarcastic observation: “There is nothing so permanent as a temporary government program.”

The Fed is basically stuck. Its ZIRP and QE policies are difficult to change. Normalization of interest rates, reducing purchases of government bonds, and the reduction of central bank holdings of securities, all risk risks higher rates and reduced available funding for economic expansion. Low rates, meanwhile, allow overextended companies and nations to maintain or increase borrowings. Central banks also cannot sell government bonds and other securities held on their balance sheet. The size of these holdings means that disposal would lead to higher rates, resulting in large losses to the central bank as well as commercial banks and investors. The reduction in liquidity would tighten the supply of credit, destabilizing a fragile financial system.

In 2013, the Federal Reserve’s tentative “taper,” in effect a slight reduction in bond purchases, triggered market volatility. Resulting higher mortgage rates slowed the rate of refinancing of existing mortgages and the recovery of the housing market. A 1% rise in rates would increase the debt-servicing costs of the U.S. government by around $170 billion. A rise of 1% in G-7 interest rates would increase the interest expense of the G-7 countries by around $1.4 trillion. Higher interest rates would also affect indebted consumers and corporations. In the U.S., for example, a 1% increase in interest rates, according to a McKinsey Global Institute Study, would increase household debt payments collectively to $876 billion from $822 billion, a rise of 7%. According to the Bank of International Settlements, a 3% increase in government bond rates would result in a change in the value of outstanding government bonds ranging from a loss of around 8% of GDP for the U.S. to around 35% for Japan.

“But it was a good week for anyone interested in understanding how this secretive institution works. Or doesn’t.”

• The Week That Shook the Fed (Gretchen Morgenson)

The Federal Reserve Board prefers to operate in a shroud of secrecy, and its officials really don’t like having to answer to anybody. So it was fascinating to learn last week that the Fed is embarking on a soul-searching campaign. Its inspector general will take up the astonishing questions of whether the Fed’s big-bank examiners have what they need to do their jobs and whether they receive the support of their superiors when they challenge bank practices. Or, as the Fed put it, whether “channels exist for decision-makers to be aware of divergent views” among the Fed’s bank examination teams. Asking such questions is an about-face for the Fed, whose officials have long maintained that it is the most sophisticated and enlightened of financial regulators. And given that the Fed received extensive new regulatory powers under the Dodd-Frank financial reform law, it is troubling indeed that it may not be certain that its bank examiners have what they need to do their jobs.

The Fed announcement looks an awful lot like damage control. It came late Thursday afternoon, directly after one Senate hearing that was critical of Fed practices and before another on Friday. It also came after a bill proposed by Senator Jack Reed, a Rhode Island Democrat, that would change the way the head of the most powerful of the 12 district banks — the Federal Reserve Bank of New York — is appointed. Currently, the president of the New York Fed is selected by its so-called public board members — those not affiliated with financial institutions. Senator Reed’s proposal would give the president of the United States, with Senate approval, responsibility for naming the president of the New York Fed. Clearly, last week was not a good one for the Fed. But it was a good week for anyone interested in understanding how this secretive institution works. Or doesn’t.

The periphery is loaded with zombies.

• Eurozone Yields Hit Record Lows: Is ECB Trumping Reality? (CNBC)

It’s hard to believe it’s just a few years since countries like Ireland and Spain had to go cap-in-hand to international lenders – at least if you look at their bond yields. Ireland’s 10-year bond yield, usually reflective of a country’s economic performance, hit a record low of 1.477% Monday, while Spanish 10-year bond yields fell below 2% for the first time ever. Ireland is expected to have one of the strongest economic rebounds in the euro zone, with 3.7% growth in GDP this year, according to Deutsche Bank forecasts. Yet it is also facing plenty of headwinds. There are increasing concerns that the current administration may not last for its maximum five-year term, as disputes over water charges and the recording of phone calls to police stations have destabilized the coalition.

Taoiseach Enda Kenny’s Fine Gael party would get just 22% of the vote now, down from 36% in the 2011 elections, according to a Red C/Sunday Business Post opinion poll published at the weekend. Polls suggest a large swing towards Sinn Fein, formerly better known as the political wing of the Irish Republican Army but now a growing voice of dissent from the main parties in Dublin. Independent candidates, often campaigning in direct opposition to a single government policy, have also been boosted by the waning popularity of the two traditionally dominant parties, Fine Gael and Fianna Fail. The troika of the International Monetary Fund, European Commission and ECB, who bailed-out Ireland and its banks during the credit crisis, warned on Friday that its current budget “makes less progress than desirable” towards reducing its budget deficit – and that its recovery is at risk if there is a further slowdown in the euro zone.

“This would be a radical change in the structure of the global financial system.”

• German Bond Yields To Trump Japan As ECB Battles Deflation (AEP)

German bond yields are to fall below Japanese levels and plumb depths never seen before in history as Europe becomes the epicentre of global deflationary forces, according to new forecast from the Royal Bank of Scotland. “We are seeing `Japanification’ setting in across Europe,” said Andrew Roberts, the bank’s credit strategist. “We expect 10-year Bund yields to cross the 10-year Japanese government bond and we are amply positioned for such an outcome.” Mr Roberts said it is a “weighty win-win” situation for investors. If the European Central Bank launches full-blown quantitative easing, it will almost certainly have to buy large amounts of German Bunds, and these are becoming scarce. “Net supply in Germany is zero since they are in budget surplus this year and next, and they have written a balanced-budget amendment into their constitution. There are simply fewer and fewer Bunds to buy, and everybody wants them,” he said.

It is assumed that if the ECB buys sovereign bonds, it will have to buy them evenly in accordance with its capital “key”. This implies that 28pc would have to be German debt. Yet if the ECB fails to deliver on hints that it will expand its balance sheet by €1 trillion, the damage would be so enormous that Europe would be sucked into a depressionary vortex, according to the bank. Bund yields would fall for different reasons, as debt markets began to reflect a Japanese-style deflation trap. The bank’s credit team is betting that the ECB will act more quickly and on a greater scale than widely assumed, launching purchases of corporate bonds as soon as early December and full sovereign QE in February once the European Court has ruled on a previous debt rescue plan (OMT). “We think Germany will be dragged to the table, kicking and screaming all the time,” said Mr Roberts.

Japanese yields are just 0.45pc, which is steeply negative in real terms now that ‘Abenomics’ is driving up Japan’s inflation rate. This is a deliberate strategy to whittle away a public debt that has reached 245pc of GDP. German yields are 0.78pc. RBS expects the two bonds to cross as Japanese yields rise while German yields fall. This would be a radical change in the structure of the global financial system.

Some German court at some point will strike Draghi down.

• Bundesbank’s Weidmann Warns Of ‘Legal Limits’ On Further Moves By ECB (Reuters)

The European Central Bank could encounter “legal limits” if it pursued additional steps to combat low inflation, the president of Germany’s Bundesbank said on Monday, calling for a focus on growth rather than any government bond buying. “Instead of focusing on the purchasing program, we should focus on how you find growth,” Jens Weidmann told an audience in Madrid, when asked about the possibility of the ECB buying government bonds, a step known as quantitative easing. He warned that it would be difficult to pursue such steps to tackle low inflation. “Of course there are other measures which are more difficult, because they are untested, because they are less clear … and of course they hit the legal limits of what you can do,” said Weidmann, who sits on the ECB’s Governing Council. “This is why discussions are so intense,” he added.

There is nothing good left for Greece in the eurozone. It’s as simple as that.

• Greece Bailout Talks Resume Amid Concerns Over Exit (Reuters)

Greece’s government will resume stalled talks with EU/IMF lenders in Paris on Tuesday, as Athens pushes to conclude a crucial review by inspectors so it can make an early exit to an unpopular bailout programme. Athens had set a 8 December deadline to complete the review. But talks floundered over a projected budget gap for next year and EU/IMF inspectors did not return as expected to Athens this month, leading to concerns that a delayed review would derail Greece’s plan to quit its bailout by the end of the year. The two sides will meet in Paris “to advance the review and examine the framework for the day after”, the bailout ends, the Greek Finance Ministry said in a statement. A ministry official declined to say if the talks would continue beyond Tuesday, but said the bailout would not be extended past the end of the year.

Greece’s government has staked its own survival on abandoning the €240bn (£190bn) bailout programme, which has entailed unpopular austerity measures, ahead of schedule. Prime minister Antonis Samaras needs to push through his candidate in a presidential vote in February to avoid being forced to call early elections; he is is hoping that leaving the bailout will help win him enough support to survive the vote. But the final bailout review, like most reviews before it, has struggled amid rows over reforms and austerity cuts. Athens and its foreign lenders have been at loggerheads over the projected deficit for next year, with the lenders arguing Greece will miss the target of 0.2% of gross domestic product because of a new payback plan for austerity-hit Greeks who owe money to the state. The Greek government, however, has so far resisted changes demanded by the inspectors, going so far as to submit its 2015 budget to parliament last week without the approval of lenders.

Brexit or Grexit, if one leaves more will follow.

• Britain’s EU Retreat Means German Hegemony Warns Prodi (AEP)

Britain is already a lame duck within the EU’s internal governing structure and is losing influence “by the day” in Brussels, even before David Cameron holds a referendum on withdrawal. This self-isolation has upset the European balance of power in profound ways, leading ineluctably to German hegemony and a unipolar system centred on Berlin. It is made worse by the near catatonic condition of France under Francois Hollande. Smaller states no longer form clusters of alliances around a three-legged diplomatic edifice made up of Germany, France, and Britain. They are instead scrambling to adapt to a new European order where only one state now counts. So too is the EU’s permanent civil service and the institutional machinery in Brussels and Luxembourg. Such is the verdict of Roman Prodi, the former Italian premier and ex-president of the European Commission.

I pass on his thoughts because the Brexit debate in the UK invariably dwells on what the consequences might or might not be for Britain, while taking it for granted that Europe itself would somehow sail on sedately as if nothing had changed. But everything would change, and we can already discern it. “France is ever more disoriented and Britain is losing power by the day in Brussels after its decision to hold a referendum on EU membership,” he said. “All the countries that previously maintained an equilibrium between Germany, France, and Britain (from Poland, to the Baltic States, passing through Sweden and Portugal) are regrouping under the German umbrella,” he told the Italian newspaper Il Messaggero. “Germany is exercising an almost solitary power. The new presidents of the Commission and the Council are men who rotate around Germany’s orbit, and above all there is a very strong (German) presence among the directors, heads of cabinet and their deputies. The bureaucracy is adapting to the new correlation of forces,” he said. [..]

The EU is either a treaty club of democracies and equals, or it is nothing.

As Abe said at some point last year: all it takes for Abenomics to succeed is for people to believe in it. Well, they don’t. So now what, Shinzo?

• BOJ Minutes Show Bazooka Is All About The Message (CNBC)

Latest minutes from the Bank of Japan (BOJ) released Tuesday reveal that the central bank’s surprise move in October to expand its already-massive stimulus program was about sending the message that it will do whatever it takes to “conquer deflation.” “The BOJ intended to send a strong message, beyond the financial markets, to jolt the wider economy,” said Shun Maruyama, Chief Japan Equity Strategist at BNP Paribas. “Consumer and business leaders remain unmoved by monetary policy.” Consumer inflation looks set to stall at around 1%, half of the BOJ’s stated target, he added, noting capital investments are picking up but not by enough to boost economic growth.

The BOJ’s commitment to pull the country out of two decades of deflation remains “unshakable”, according to the minutes from its policy meeting on October 31, when the central bank expanded its asset purchase program by 30 trillion yen to 80 trillion yen. “If no policy action was taken at this meeting, this could be understood as a breach of the commitment (to achieve its inflation target of 2%), thereby possibly impairing the Bank’s credibility significantly,” said one board member. The members that supported further monetary easing argued that the BOJ needed to “convey the bank’s unwavering resolve to conquer deflation.” In a tight ballot, five members backed the latest measures, and four voted against.

The BOJ kept its goal to boost the inflation rate to 2% by next year, but falling oil prices could put the target in question. When stripped of the effect of April’s consumption tax hike, Japan’s core inflation rate rose 1% in September from the year-ago period, its lowest pace in nearly a year. “The year-on-year rate of increase in the CPI (all items less fresh food) was likely to be at around 1% for some time, mainly due to the effects of the decline in crude oil prices,” board members said.

The hoarding meme in economics is a red flag. Bernanke’s Asian ‘savings glut’ all over again.

• Kuroda Tells Japan Inc. to Stop Hoarding Cash as Costs to Rise (Bloomberg)

Bank of Japan chief Haruhiko Kuroda urged business leaders to use profits more productively, saying hoarding cash will become costly as the central bank stamps out deflation. Companies could boost investment in facilities and jobs, taking advantage of a weaker yen, Kuroda said today in a speech in Nagoya. At the same time, the BOJ will continue to spur price gains, adjusting its unprecedented easing policy as needed to achieve its inflation goal, he said. Japanese companies are headed toward their highest profits ever as a weaker yen resulting from the BOJ’s stimulus boosts Toyota and other exporters. Japan Inc. holds near-record cash while capital spending in the second quarter was more than 50% lower than a peak in the first three months of 2007. “Kuroda is making it clear it’s companies’ turn to act,” said Mari Iwashita, an economist at SMBC Friend Securities.

“Capital spending, wages and price settings are all vital for the BOJ but are out of its hands. Kuroda must convince companies the economy will get better and deflation will end.” Kuroda last week secured a wider board majority for easing that the BOJ boosted on Oct. 31, and warned the central bank’s key gauge of inflation could fall below 1% after the world’s third-largest economy slid into recession. Falling prices over two decades of stagnation made holding cash a viable option for companies looking for safety and real returns on capital. The BOJ has been making steady progress in shaking a “deflationary mindset,” Kuroda said. Kuroda called on business leaders to take “action” that looks toward an economy that has overcome deflation. “As a corporate strategy, using their profits in a more productive manner is imperative,” Kuroda said. “I have great interest in developments in wages and price settings through spring of next year.”

“Guess what the hedge fund firms are doing now? Hunting for new, less skeptical customers.”

• Hedge Funds Lose Money for Everyone, Not Just the Rich (Bloomberg)

When Douglas Kobak was an adviser at a large brokerage firm, he suggested his wealthiest clients buy a hedge fund promising to be “a very conservative alternative to bonds.” Then the credit crisis hit in 2008, the fund imploded and investors got 45 cents on the dollar — as long as they promised not to sue. Since then, mediocrity is more common than blow-ups. Hedge funds have lagged behind stocks while still charging fees of up to 2% of assets and 20% of gains. For the rich and their advisers, “the sex appeal of hedge funds has worn off,” says Kobak, now head of Main Line Group Wealth Management. Guess what the hedge fund firms are doing now? Hunting for new, less skeptical customers.

While only those with at least $1 million are allowed to invest in hedge funds, anyone can buy a mutual fund with a hedge fund strategy. Unfortunately, these “alternative” funds come with the same disadvantages hedge funds have: high fees, inconsistent performance and strategies that take a PhD to decipher. By starting alternative funds, mutual fund companies get a chance to bring in revenue they’re losing to cheap index funds and exchange-traded funds. In a deal announced Nov. 18, Blackstone Alternative Asset Management is coming up with hedge-fund-like products for mutual fund company Columbia Management. They’ll join 11 other U.S. mutual funds and ETFs classified by Bloomberg as “alternative,” which together hold $68 billion in assets. One in five of those assets is held by the largest fund, the MainStay Marketfield Fund. Started in 2007, it’s one of the oldest alternative funds, and one of the most disappointing.

After a good start from 2007 to 2009, the fund mostly matched the stock market in 2010 and 2011, and then lagged behind it in 2012 and 2013. This year, it has dropped almost 11%, a mirror image of the S&P 500’s 11.6% gain. Unreliable and disappointing performance is getting to be as common among alternative funds as among hedge funds. The Bloomberg Global Aggregate Hedge Fund index is up 2% year-to-date. The average return of an alternative fund open to all investors is 1.1%, behind the inflation rate. High-quality corporate bonds have returned 70% more than the median alternative fund over the last three years. The stock market has brought in eight times as much as alternatives. And these blah results don’t come cheap. The MainStay Marketfield Fund has been losing money while charging an expense ratio of 2.6% per year. That’s pricier than 99% of all funds, though it’s not as extreme among alternative funds. They charge an average of 1.74% per year, 20 times as much as the cheapest index funds.

“Goldman Sachs, the Wall Street bank where Dudley was chief U.S. economist for a decade.”

• Dudley Defense Leaves Senators Unimpressed as Fed Scrutiny Rises (Bloomberg)

Federal Reserve Bank of New York President William C. Dudley’s defense of his record on financial supervision is unlikely to appease lawmakers seeking to tighten their oversight of the central bank. In a tense exchange with Senator Elizabeth Warren at a Nov. 21 hearing, Dudley rejected her assertion that there had been a “long list” of regulatory failures at the New York Fed. Warren, a Massachusetts Democrat, suggested that if Dudley doesn’t fix a “cultural problem” at the bank, “we need to get someone who will.” While the Senate doesn’t have the authority to appoint or remove Fed presidents, the exchange was a sign of growing frustration among Republicans and Democrats alike. Republicans, who have been critical of the Fed’s loose monetary policy, will take control of the Senate in January, adding to pressure on the Fed from Democrats who see the central bank as too close to the Wall Street banks it supervises.

“The Fed is as vulnerable as any time since the 1980s,” when then-Chairman Paul Volcker drew the ire of politicians for driving up interest rates to levels that threw the country into a recession, said Karen Shaw Petrou, managing partner of Federal Financial Analytics. The next Congress will be “really challenging for the Fed.” Last week’s hearing before a subcommittee of the Senate Banking Committee was prompted by allegations made by a former New York Fed bank examiner, Carmen Segarra, who said her colleagues were too deferential to Goldman Sachs, the Wall Street bank where Dudley was chief U.S. economist for a decade.

She headed the board of directors as the money laundering and organized crime (those are the charges) were going on. And of course now says she had no idea. Which makes one wonder what she has no idea of now she leads the government. Ignorance doesn’t come high on a president’s list of job qualifications.

• Even Brazil’s President Is Involved In The Petrobras Scandal (CNBC)

Energy giant Petrobras is engulfed in a corruption scandal that could prove to be Brazil’s biggest, threatening to engulf the country’s most senior politicians—including its president. Even the company is not downplaying the events. In a news release last week to explain why it had delayed its upcoming financial report, Petrobas said it was “undergoing a unique moment in its history, in light of the accusations and investigations of the “Lava Jato Operation” (Portuguese for “Operation car wash”) being conducted by the Brazilian Federal Police, which has led to charges of money laundering and organized crime.” CNBC takes a look at the facts behind the scandal and the implications for other oil companies and Brazil itself. [..]

Petrobras executives are alleged to have paid politicians for contracts, using money skimmed from company profits. The head of the country’s budget watchdog, Joao Augusto Nardes, has said the kickbacks may total as much as 4 billion Brazilian reais ($1.6 billion), according to the WSJ. The company has neither confirmed nor denied the allegations. It has hired independent auditors to investigate further, in addition to the official investigation by the Brazilian Federal Police. The country’s most senior politicians are implicated, including recently re-elected President Dilma Rousseff, who previously headed the Petrobras board of directors.

Der Spiegel provides a lengthy history of how failure decided the future of Ukraine, and the German magazine doesn’t spare Merkel.

• Summit of Failure: How the EU Lost Russia over Ukraine (Spiegel)

One year ago, negotations over a Ukraine association agreement with the European Union collapsed. The result has been a standoff with Russia and war in the Donbass. It was an historical failure, and one that German Chancellor Angela Merkel contributed to.

Only six meters separated German Chancellor Angela Merkel and Ukrainian President Viktor Yanukovych as they sat across from each other in the festively adorned knight’s hall of the former Palace of the Grand Dukes of Lithuania. In truth, though, they were worlds apart. Yanukovych had just spoken. In meandering sentences, he tried to explain why the European Union’s Eastern Partnership Summit in Vilnius was more useful than it might have appeared at that moment, why it made sense to continue negotiating and how he would remain engaged in efforts towards a common future, just as he had previously been. “We need several billion euros in aid very quickly,” Yanukovych said. Then the chancellor wanted to have her say. Merkel peered into the circle of the 28 leaders of EU member states who had gathered in Vilnius that evening. What followed was a sentence dripping with disapproval and cool sarcasm aimed directly at the Ukrainian president.

“I feel like I’m at a wedding where the groom has suddenly issued new, last minute stipulations.” The EU and Ukraine had spent years negotiating an association agreement. They had signed letters of intent, obtained agreement from cabinets and parliaments, completed countless diplomatic visits and exchanged objections. But in the end, on the evening of Nov. 28, 2014 in the old palace in Vilnius, it became clear that it had all been a wasted effort. It was an historical earthquake. Everyone came to realize that efforts to deepen Ukraine’s ties with the EU had failed. But no one at the time was fully aware of the consequences the failure would have: that it would lead to one of the world’s biggest crises since the end of the Cold War; that it would result in the redrawing of European borders; and that it would bring the Continent to the brink of war. It was the moment Europe lost Russia.

Even Reuters cheerleading can’t prevent this.

• In Wake Of China Rejections, GMO Seed Makers Limit US Launches (Reuters)

China’s barriers to imports of some U.S. genetically modified crops are disrupting seed companies’ plans for new product launches and keeping at least one variety out of the U.S. market altogether. Two of the world’s biggest seed makers, Syngenta and Dow AgroSciences, are responding with tightly controlled U.S. launches of new GMO seeds, telling farmers where they can plant new corn and soybean varieties and how can the use them. Bayer CropScience told Reuters it has decided to keep a new soybean variety on hold until it receives Chinese import approval. Beijing is taking longer than in the past to approve new GMO crops, and Chinese ports in November 2013 began rejecting U.S. imports saying they were tainted with a GMO Syngenta corn variety, called Agrisure Viptera, approved in the United States, but not in China.

The developments constrain launches of new GMO seeds by raising concerns that harvests of unapproved varieties could be accidentally shipped to the world’s fastest-growing corn market and denied entry there. It also casts doubt over the future of companies’ heavy investments in research of crop technology. The stakes are high. Grain traders Cargill and Archer Daniels Midland, along with dozens of farmers, sued Syngenta for damages after Beijing rejected Viptera shipments, saying the seed maker misrepresented how long it would take to win Chinese approval. In the weeks since Cargill first sued on Sept. 12, Syngenta’s stock has touched a three-year low. ADM in its lawsuit last week alleged the company did not follow through on plans for a controlled launch of Viptera corn. Syngenta says the complaints are unfounded.

Home › Forums › Debt Rattle November 25 2014