“George Lane, served in the last war with the British Army from Vimy Ridge to the Occupation. Two of his sons are in the American Army, one with the Air Corps in Australia. His daughter volunteered for the Women’s Army Auxiliary Corps. Seven of his nephews are in the British Army”

With the Bank of England about to announce its latest set of desperate measures today, the first since the Brexit, I accidentally stumbled upon an article I wrote on January 16 2012, well over 4 1/2 years ago, in the Automatic Earth’s last days at Blogger. Posting it again here seems appropriate 5 weeks after the Brexit, because the article shows you that the referendum result did not come out of nowhere, no matter what many people claim. The British economy was already doing very poorly, and already failing millions of people, going into 2012.

Note: of course not all predictions made back then played out the way they were made, but I’m more interested in the overall picture. For instance, unemployment numbers are not as dire as forecast, but that hides the deterioration in the quality of jobs, and what they actually pay, much as that happens in the US. Bubbles in stocks and housing hide a lot too. David Cameron’s rule has been hard on the poorer British people, and it will take a long time for that to be corrected. I changed the coding just a little bit (Blogger vs WordPress), nothing big, so it looks a bit different. Here’s from early 2012, happy time travel:

Ilargi: There is a relative silence in the international financial press when it comes to Britain. The economic situation of continental Europe gets almost all the attention. Every now and then someone in France or Germany states that Britain, too, should be downgraded, like when S&P cut the ratings of 9 European countries, but such statements attract hardly any interest at all. This might not be overly wise, though.

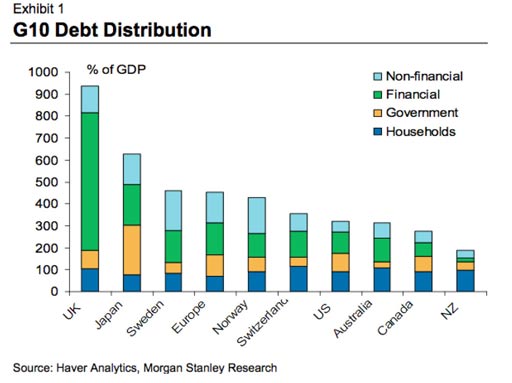

At the end of last year, Tyler Durden at ZeroHedge published a graph from Haver Analytics/Morgan Stanley that should probably have sounded alarm bells quite a bit louder than it did.

Still, this graph would seem to indicate that the only core issue in the UK is its outsize financial sector with its outsize debt. From time to time, however, news articles pop up that seem to indicate there’s more going on than trouble in the City of London.

I found this one alarmingly interesting, for instance, from James Hall in the Telegraph on January 4:

One million people take out emergency loans to pay mortgage

Almost one million Britons have taken out an emergency ‘payday’ loan to help pay their rent or mortgage in the last year, according to Shelter, the housing charity.

The high degree of borrowing highlights the ‘spiral of debt’ that people are falling into to keep a roof over their head, Shelter said. The charity also found that seven million Britons are relying on some form of credit to help pay their housing costs.

Campbell Robb, Shelter’s chief executive, said: ‘These shocking findings show the extent to which millions of households across the country are desperately struggling to keep their home.’

Ilargi: Payday loans to pay off your mortgage? Sounds like perhaps Britain has a substantial hidden real estate problem, a pre-shadow inventory one that could spiral out of control at a rapid clip.

On January 9, the same James Hall had this follow-up:

Six million households have only five days’ savings

Around six million households would be unable to survive for more than five days if they stopped being paid, such are the low levels of savings among Britons, new research shows.

A new report from First Direct, the bank, warns that one in three UK households have less than £250 in accessible savings. A fifth of all households have no savings at all.

The bank said that £250 is the equivalent of three days’ average monthly household take-home pay. With average monthly outgoing currently at £1,536, these savings would last just five days.

Ilargi: Obviously, the two groups, those that take out loanshark payday loans to keep a roof over their head, and those that live paycheck to paycheck, overlap each other to a large extent.

Still, what makes it striking is the sheer number of people affected. One million people need emergency loans to keep their families in their homes, while six million households have nothing whatsoever saved for a rainy day.

If we put the average household size at 2.5 people, that means that, out of 60 million living in Britain, 2.5 million are on the verge of losing their homes, and 15 million, or 25% of the population, risk having to cut on their basic needs, food and heating, if they hit even the slightest speedbump.

And what are the chances this situation will improve any time soon? It doesn’t look good; in fact it looks set to worsen. While there’s no lack of denial, an increasing number of voices admit that the British economy has already slipped back into recession. This is from the BBC this morning:

UK in recession say Item Club economic forecasters

The UK may have already slipped back into recession, economic forecaster the [Ernst&Young] Item Club has warned. The think tank said gross domestic product shrank in the final quarter of last year and would contract again in the current three-month period.

It said that even if the eurozone could resolve its problems the UK economy would grow by just 0.2% this year. It also predicted unemployment would rise by a further 300,000 to just below three million people. [..]

Meanwhile, the Chartered Institute of Personnel and Development said unemployment would stay above 2.5 million until at least 2016, peaking at 2.9 million next year. Chief economic adviser John Philpott said the jobless rate would rise to 8.8% at the end of next year. [..]

Another forecast from the Centre for Economics and Business Research said the UK would actually shrink this year by 0.4% and by a full 1% if the eurozone broke up.

Ilargi: Nor is it hard to find an ironic twist in all this. In what depicts a fast growing chain of events, Zoe Wood reports for the Guardian:

Royal Bank of Scotland pulls out of deal to rescue Peacocks

More than 13,000 retail jobs are on the line at value fashion group Peacocks after Royal Bank of Scotland walked away from restructuring talks at the heavily indebted retail chain.

Peacocks may have to appoint administrators after the state-backed lender had an abrupt change of heart about a deal to refinance the retailer’s £600m debt pile, which would have involved risking more money in the business. RBS and Barclays were in the driving seat of the complex debt-for-equity negotiations – which were said to involve 18 funds and lenders – as they are owed the most. Both banks are owed more than £100m.

Peacocks’ advisers have been trying to put together a rescue deal for months, but talks broke down at the weekend, leaving the future of the store, which has 550 branches and employs around 10,000 staff, hanging in the balance. [..] “It’s quite a complex deal,” said one insider. “It was all going well until RBS walked away last week. There are still conversations going on.” [..]

RBS is facing a series of tough decisions this year as a number of struggling high-street chains, including HMV and Clinton Cards, are reliant on its largesse. “Each company restructure is judged on its own merits, but clearly the difficult conditions that retailers face is an important factor,” said an RBS spokesman. [..]

A string of high-street chains including La Senza, Blacks Leisure and Barratts Priceless have called in administrators in recent weeks as trading failed to produce enough cash to cover costs such as rent and interest payments on loans.

Ilargi: With the country in a recession, but hardly anyone willing to concede that to date, least of all its government, it’s no wonder that things like this happen, mostly hidden from sight.

The ironic twist to it is provided by that fact that RBS is 70% owned by the British government, which has poured billions of pounds into the bank, and then lets it make decisions that cost 10’s of 1000’s of jobs.

I don’t want to get into a political debate about this; however, protecting banks with taxpayer funds, but not jobs, is a decision that is of course as political as it is ironic. Letting bailed out bank executives make decisions that cut all these jobs and at the same time pay themselves multi-million dollar bonuses is way beyond ironic.

But all of the above is just today’s prologue. I received an article yesterday that outdoes it all, and then some.

John Ross, Visiting Professor at Antai College of Economics and Management at Jiao Tong University in Shanghai writes a real stunner on his blog Key Trends in Globalisation:

The incredible shrinking UK economy

The magnitude of the blow suffered by the UK economy since the beginning of the financial crisis is very considerably minimized by not presenting it in terms of a common international yardstick. Gauged by decline in GDP, using a common international purchasing measure, dollars, no other economy in the world has shrunk even remotely as much as the UK.

As most countries produce only annualized GDP data it will be necessary to wait before a comprehensive global comparison can be made for 2011. However it is clear no substantial growth in dollar terms took place in the UK economy during that year – GDP at national current prices rose only 1.4 per cent between the 1st and 3rd quarters and the change in the pound’s exchange rate against the dollar during the year was a marginal 0.3 per cent.

Therefore there will have been no significant recovery from the UK data set out in Table 1 below, and the gap between the UK and other European economies, which form the next worst performing major group, is too great to have been qualitatively affected by changes in the Euro’s exchange rate – the Euro declined against the pound by only 3.3 per cent in 2011.

Table 1 shows that the fall in UK GDP in 2007-2010 was $562 billion compared to the next worst performing national economy, Italy, with a decline of $65 billion – i.e. the decline in UK GDP in the common measuring yardstick of dollars was more than 8 times that of the next worst performing national economy. Table 1 shows the 10 national economies suffering the greatest declines in dollar GDP.

It is also extremely striking that the UK’s decline was more than two and a half times that of the entire Eurozone.

The UK accounted for a somewhat astonishing 77% of the EU’s decline.

Expressed in percentage terms the situation is no better. Of all economies for which World Bank data is available only Iceland, with a decline in dollar GDP of 38.4%, suffered a worst percentage fall than the UK – even bail out economy Ireland, with a fall of 18.4%, outperformed the UK economy.

Two trends intersected for the UK’s performance to be so much worse than that of any other economy. First, contrary to the government’s anti-European rhetoric, UK economic performance in constant price national currency terms has been significantly worse than the Eurozone during the financial crisis (Figure 2). [..]

… between the beginning of 2008 and the beginning of 2012, the pound’s exchange rate has fallen by 21.0% against the dollar compared to the Euro’s 11.4% drop in the same period. The multiplicative effect of the severity of the relative drop in constant price GDP and the fall in the pound’s exchange rate accounts for the unequalled decline in UK GDP in dollars.

As at present the UK economy shows no substantial sign of recovery, the present UK government, which maintains a steadfastly ostrich like attitude towards Europe in particular, and most other countries in general, may argue that a measure in terms of dollars at current exchange rates is irrelevant – the UK currency is the pound and what counts is constant price shifts. Such an argument is false and an attempt to disguise the true scale of the decline of the UK economy.

The internationally unmatched decline in UK dollar GDP is a huge fall in real international purchasing ability. The far higher than targeted inflation in the UK during the last two years, which has substantially eroded the population’s living standards, is itself in part a reflection of the decline in the UK’s exchange rate and consequent raising of import prices. In short, the decline in the international purchasing power of the UK’s economy translates into a direct fall in real incomes.

It may also be seen that the government’s claim that the UK is outperforming Europe and the Eurozone is entirely without foundation even in constant price national currency terms. But when measured in terms of real international comparisons, i.e. in dollars, the UK’s performance is incomparably worse than Europe’s.

It appears extremely unlikely that the UK’s economy will escape from this circle of decline in the next period. The austerity policies pursued by the present UK government have substantially slowed the economic recovery that was taking place in 2009 and the first part of 2010 – between the 3rd quarter of 2010 and the 3rd quarter of 2011 the UK economy grew by only 0.5%. [..]

Even if any partial recovery takes place, for example by some increase in the exchange rate of the pound against the Euro, the sheer magnitude of the decline in the UK economy makes it implausible that this could be on a scale sufficient to reverse the fall in its relative international position.

Ilargi: Britain lost 20% of GDP from 2007 – 2011. Against this backdrop, and don’t let’s forget the over-600% debt to GDP ratio just for Britain’s financial sector, which will inevitably lead to more – calls for – bailouts, what is the Cameron government’s response?

First of all, austerity measures. Which will hit those people very hard who are in the bottom 25% or so who already have no savings, no nothing, to fall back on. And which will also lead to a rise in unemployment, which in turn will exacerbate the vicious problem circle.

Cameron also distances himself, and his country, from continental Europe, even though that is Britain’s main export destination. How smart is that?

Britain is a country of relatively large regional disparities as well as wealth disparities. The already rich center increasingly sucks up the remaining wealth of the periphery of society. There is then only one possible outcome of those one million people paying their rents and mortgages with payday loans: the British housing bubble will burst sooner rather than later.

Tax revenue has only one way to go as well. Down. So what will Cameron use to support the banks? How will he attempt to prevent a large scale repeat of last year’s Tottenham riots?

Looking at all this, we also need to wonder how much longer, and why in the first place, Britain is perceived as a safe haven, with its sovereign bonds – gilts – much sought after. Sure, Britain has its own currency and central bank, it can “print”, it can do QE 1001, but it’s not as if it hasn’t already tried that route. And still lost 20% of GDP.

Whatever it decides to do, it seems safe to presume that Britain might well steal some of the limelight away from Greece and Italy in the not too distant future.

Me in 2016 again for a moment: after reading this -I wrote it 55(!) months ago-, does the Brexit still surprise you?

Home › Forums › Brexit Redux: Quo Vadis Britannia?