Pablo Picasso Interieur au Pot de Fleurs 1953

HHS Secretary RFK Jr. Reveals How Trump Controls BOTH Parties—And Why Washington Fears Him

"The industry isn’t fighting me—they know the free ride is over. The real opposition? Media proxies and a Democratic Party that no longer stands for anything except opposing Trump." — HHS… pic.twitter.com/QnvG2QDeM6

— Camus (@newstart_2024) August 5, 2025

16%

https://twitter.com/EricLDaugh/status/1952716496523710784

Pelosi

https://twitter.com/TRUMP_ARMY_/status/1952699081832140896

2018

2018. James Comey and Stephen Colbert smear Trump by discussing the "unverified" details of the Steele dossier.

This was all planned and scripted. Comey knew the dossier was fiction and that it was paid for by the Clinton campaign. He is there to slander Trump.

Evil stuff. pic.twitter.com/pgdlloSPla

— MAZE (@mazemoore) August 5, 2025

Ratcliffe: On July 31 2016, the FBI started an investigation into candidate Trump. 6 days before, Russian intelligence “predicted” that would happen. They didn’t guess. They had read the playbook.

I’m early today. Could have posted -most of- this last night. My timezone here is E(D)T+6. Maybe more later. A whole day ahead.

X thread.

The highest ranking US government official in history who’s -openly- gay.

Who was involved in breaking the Bank of England.

Nice interview.

• Your Wages Aren’t Rising By Accident. They’re Rising By Design (Nas)

The numbers are staggering.Household income growth hit 0.7-0.8% in April alone. Real wages for hourly workers rose almost 2% in just 5 months. Bessent dropped this bombshell: “No president has done that before.” But here’s where it gets interesting… Blue-collar wage growth is at its highest level since Trump’s first term. Under Biden? It plummeted. Now it’s back up “just in a few months.” The reason is simple… Bessent revealed the hidden mechanism behind exploding wages: It’s not about minimum wage laws or government mandates. It’s about strategic displacement of cheap labor. “12 or 20 million illegal aliens coming out of the workforce” creates massive wage pressure upward. The manufacturing revolution is here.

Only 9% of Americans work in manufacturing. But here’s what they don’t tell you: Manufacturing jobs deliver “much stronger wage growth than the service economy.” Trump is rebuilding America’s industrial base by design. The negotiation strategy is working brilliantly. 75+ nations are bringing “their best offers” to Treasury. When Trump threatened 50% EU tariffs, European leaders called within hours. Tariffs aren’t just revenue. They’re leverage that gets results. Here’s the secret Wall Street doesn’t want you to know. For decades, they’ve had “a great run” while Main Street struggled. Bessent’s mission? “Now it’s Main Street’s turn to also participate.” The policy shift is already working… The economic data proves it: CPI: 0.1% (best since 2020) PPI: 0.1% (best since 2021)

Recession predictions: Dead wrong Reality: “Economy is very strong” But there’s a deeper story here… Bessent’s opened up about his backstory. His father went broke twice. Young Scott got his first job at age 9 – putting out beach umbrellas and busing tables. “That’s why I am so focused on the debt here and having responsible finances.” This isn’t just policy – it’s personal vendetta against financial recklessness. “We are not going to make the same mistakes my family did.” He’s treating America’s economy like he wished someone had treated his family’s finances. The Wall Street vs Main Street war is real. For years, coastal elites thrived while middle America got “hollowed out.” Bessent’s solution? Bring back strategic industries: steel, semiconductors, pharmaceuticals.

“We got to bring them back home.” Hamilton’s original tariff strategy had two purposes:

• Finance the treasury

• Protect nascent industries

Trump added the third leg: negotiation leverage. This is economic warfare disguised as trade policy. And it’s working. The results speak for themselves: Manufacturing emphasis + immigration control + tariff leverage = exploding wages. It’s not magic. It’s applied economics. And workers are seeing the benefits in real time. This is the economic revolution hiding in plain sight. While media focuses on political drama, actual policy is reshaping American prosperity. Your wages aren’t rising by accident. They’re rising by design.Bessent

Actually, he ruled himself out.

“I asked him just last night, ‘Is this something you want?’ [Bessent said], ’Nope, I want to stay where I am.’ He actually said, ‘I want to work with you.’ It’s such an honor’. I said, ‘That’s very nice. I appreciate that.’””

• Trump Rules Out Scott Bessent As Fed Chair (NYP)

President Trump took Treasury Secretary Scott Bessent off his list of possible candidates to helm the Federal Reserve next year and joked about selecting CNBC anchors for roles with the central bank Tuesday. Trump, 79, claimed he has four finalists in mind to replace current Fed Chair Jerome Powell, whose term ends in May 2026. “I love Scott, but he wants to stay where he is,” Trump told “Squawk Box” of Bessent. “I asked him just last night, ‘Is this something you want?’ [Bessent said], ’Nope, I want to stay where I am.’ He actually said, ‘I want to work with you.’ It’s such an honor. I said, ‘That’s very nice. I appreciate that.’” Bessent’s name had been floated for weeks as a possible successor to Powell, with the Treasury secretary refraining from publicly ruling himself out.

Trump has long fumed at Powell for his reluctance to slash interest rates, bashing him as “too late” and “highly political.” Still, the president has denied that he will attempt to dismiss Powell before his term ends. Critics and legal experts have cast doubt on whether the president even has the authority to fire the Fed chair, who has reportedly insisted he will not resign despite the criticism. “In the end, there are numerous people that are qualified. Everyone on your phone right now, in terms of at your beautiful studio, would be very qualified in my opinion,” Trump quipped about replacing Powell. “You guys are better than most of the people that do it for a living.” During the wide-ranging interview, Trump riffed about two widely reported contenders to take over the Fed — National Economic Council Director Kevin Hassett and former Fed board member Kevin Warsh.

Over the weekend, Hassett told NBC’s “Meet the Press” that he has the “best job in the world” and is “really well placed at the National Economic Council” but did not rule out accepting the job if Trump asked. Warsh, who served on the Fed’s Board of Governors from 2006 to 2011, was passed over by Trump in favor of Powell during his first term. “Both Kevin Warsh and Kevin Hassett are very good candidates for the Fed,” Trump said, before adding that “I have two other people” under consideration without specifying who those were. The president views Powell’s insistence on keeping interest rates elevated as undermining efforts to refinance the roughly $9 trillion in US debt. However, some economists have defended Powell, noting that the annual inflation rate remains above the Fed’s 2% goal.

During its meeting last week, the Fed’s Federal Open Market Committee, which makes interest rate decisions, opted to leave its benchmark rate between 4.25% and 4.5%. Trump is also dealing with the fallout from an underwhelming employment report, which found only 73,000 jobs were added in the month of July and revised the figures for May and June down by a whopping 258,000 jobs. Hours after the report came out, Trump dismissed Bureau of Labor Statistics Commissioner Erika McEntarfer, accusing her of fudging the numbers. “Squawk Box” co-host Joe Kernen noted to the president that the soft job market could hasten the Fed’s decision to lower interest rates. “It’s not what I want,” Trump shot back. “I don’t want that. I wanted it a year ago. I wanted it a long time ago. Jay Powell is highly political. And I think, you know, I call him ‘Too late.’”

In both Epstein and Giuffre’s cases, it is reported non-stop that they committed suicide. In both cases, there are serious questions about that.

• Clintons, ex-AGs and FBI Directors Subpoenaed For Epstein Testimony (NYP)

House Republicans subpoenaed nearly a dozen former federal officials and politicians — including Bill and Hillary Clinton — as well as records from the Department of Justice on Tuesday amid an expanding probe into the deceased pedophile Jeffrey Epstein. The officials — including former FBI Directors James Comey and Robert Mueller as well as six ex-US attorneys general — were compelled to testify before the House Oversight Committee. Oversight Chairman James Comer (R-Ky.) announced the move less than two weeks after DOJ officials interviewed Epstein’s late accomplice Ghislaine Maxwell, who is serving a 20-year sentence in a federal prison for conspiring to sexually abuse young girls. “The facts and circumstances surrounding both Mr. Epstein and Ms. Maxwell’s cases have received immense public interest and scrutiny,” Comer wrote in all of the letters.

“While the Department undertakes efforts to uncover and publicly disclose additional information related to Mr. Epstein and Ms. Maxwell’s cases, it is imperative that Congress conduct oversight of the federal government’s enforcement of sex trafficking laws generally and specifically its handling of the investigation and prosecution of Mr. Epstein and Ms. Maxwell.” The investigation kicked off after President Trump faced backlash over a two-page memo, released by his DOJ and FBI July 6, that found a “systematic review” of evidence uncovered no Epstein “client list” of rich and well-connected associates implicated in his sickening crimes. Epstein, 66, committed suicide in his Manhattan jail cell Aug. 10, 2019, multiple federal and independent medical investigations determined, but his well-documented links to Hollywood stars, high-powered attorneys, politicians and influential business leaders have caused furious speculation for years.

Trump’s current attorney general, Pam Bondi, had indicated a client list was “sitting” on her desk for the review in February — and that the FBI’s New York Field Office was “in possession of thousands of pages of documents related to the investigation and indictment of Epstein.” But the July 6 memo said threre was “no credible evidence found that Epstein blackmailed prominent individuals as part of his actions” and no “evidence that could predicate an investigation against uncharged third parties.” The FBI-DOJ document also noted that Epstein’s crimes impacted “over one thousand victims.” On July 17, Trump posted on Truth Social: “Based on the ridiculous amount of publicity given to Jeffrey Epstein, I have asked Attorney General Pam Bondi to produce any and all pertinent Grand Jury testimony, subject to Court approval.” “This SCAM, perpetuated by the Democrats, should end, right now!” he added.

Trump also told reporters of the public’s right to previously undisclosed Epstein information: “Anything that’s credible, I would say, let them have it.” Deputy Attorney General Todd Blanche interviewed Maxwell July 24 and 25 at the US attorney’s office in Tallahassee, Fla., before she was shuttled to a spacious correctional center in Bryan, Texas, last week. Maxwell — who was given limited immunity — answered every question about “100 different people,” according to her lawyer, Oscar David Markus. The discussions came amid speculation that the former Epstein associate’s legal team could be seeking clemency for their client, who was convicted in December 2021 and sentenced in June 2022. Her lawyers have already appealed her conviction to the US Supreme Court, arguing that she should have been off limits to prosecutors under a plea agreement reached when Epstein was first charged with sex crimes. The justices will consider her petition in late September.

The disgraced financier had to register as a sex offender after pleading guilty to Florida charges of soliciting sex from a minor in 2007, but went on to host lavish parties and enjoy professional relationships with associates like Prince Andrew and Microsoft founder Bill Gates. Bill Clinton rode on Epstein’s private jet abroad, nicknamed the “Lolita Express,” several times. Hillary Clinton has been asked to appear Oct. 9, while Bill Clinton was ordered to sit for his deposition on Oct. 14 Mueller’s deposition is scheduled for Sept. 2; Comey’s is scheduled for Oct. 7. Also summoned were former President Joe Biden’s AG Merrick Garland, Trump AGs Bill Barr and Jeff Sessions, former President Barack Obama’s AGs Loretta Lynch and Eric Holder as well as former President George W. Bush’s AG Alberto Gonzalez. Barr [..] is set to be deposed Aug. 18, Gonzales on Aug. 28, Lynch on Sept. 9, Holder on Sept. 30 and Garland on Oct. 2. The Justice Department has been given until Aug. 19 to turn over the “full, complete, unredacted Epstein Files.”

“We believe that the right move is the grand jury, but not if it’s in DC. That’s felony dumb.”

“The sad situation is that no one remotely right of center would get a fair trial in Washington, D.C. That’s not just sad, it’s true—and it’s criminal..”

• Here Comes The Find Out Phase: Russia Collusion Hoax Grand Jury Is On (Taft)

DOJ leaks reveal that U.S. Attorney General Pam Bondi has green-lighted a grand jury to investigate the Russia Collusion hoax. I’d say that this is a BLOCKBUSTER! BAM! BREAKING story, and it IS a HUGE MOVE, but you read PJ Media to get context and insight, so there are questions. Here’s the nut of the exclusive report by Fox News on Monday evening: “EXCLUSIVE: Attorney General Pam Bondi directed her staff Monday to act on the criminal referral from Director of National Intelligence Tulsi Gabbard related to the alleged conspiracy to tie President Donald Trump to Russia, and the Department of Justice is now opening a grand jury investigation into the matter, Fox News Digital has learned. Bondi personally ordered an unnamed federal prosecutor to initiate legal proceedings and the prosecutor is expected to present department evidence to a grand jury, which would allow the department to secure a potential indictment, according to a letter from Bondi reviewed by Fox News Digital and a source familiar with the investigation. ”

Gabbard’s concerns are republic-shaking ones but not the only ones. Fox Digital reported: “The DOJ confirmed two weeks ago it received a criminal referral from Gabbard. The referral included a memorandum titled “Intelligence Community suppression of intelligence showing ‘Russian and criminal actors did not impact’ the 2016 presidential election via cyber-attacks on infrastructure” and asked that the DOJ open an investigation. Hmmm? While this skeletal report telegraphs a few clues, Bondi’s team has leaked that the AG’s team is acting on Gabbard’s criminal referrals, but there’s no word about the possibly even more concrete referrals from CIA Director and former U.S. federal prosecutor John Ratcliffe. Both sets of allegations are serious, but why leave Ratcliffe’s referrals out of the story?

Here are the allegations he referred to pertaining regarding John Brennan, James Comey, James Clapper, and Hillary Clinton:

• Lying under oath to Congress or federal investigators

• Abuse of office and politicization of intelligence by advancing unsubstantiated claims and manipulating intelligenceGabbard’s referrals based on the documents she released underscored the conspiracy and its treachery. While that oversight could be because Bondi is caught up between the signal and the noise, what she could be doing is holding her powder. The reason behind that could be what constitutional lawyer and Fox News host Mark Levin said on Sunday Morning Futures with Maria Bartiromo–and it is important. Bartiromo asked, “How would you be handling this case?” And Levin held a clinic.

Today on @SundayFutures with @MariaBartiromo , "Life, Liberty and Levin" Host Mark Levin @marklevinshow spoke about accountability sought for the Russia collusion origins@FoxNews pic.twitter.com/4XKM3XqKFR

— SundayMorningFutures (@SundayFutures) August 3, 2025

I’ll break down what Levin said. It makes sense to those who resist the urge to make the perfect the enemy of the good. “I think it doesn’t help us as to what laws might have been violated. Who cares? Right now, you need to dig in to find out who did what, then you’ll figure out what laws have been violated. We know laws were violated. You’re not bringing charges yet; you’re not bringing a bill of indictment yet. You have to conduct an investigation. I mean, I can think of laws that I haven’t even mentioned. What about federal campaign finance laws? What they did to Donald Trump in Manhattan is a ruse … really? Those are campaign violations. That[‘s] for another day.

What should happen now, for me, my view, the Department of Justice should be making a list of every potential witness or participant. They should immediately receive a letter that a criminal investigation has begun, and they are to preserve all records whether they are to preserve all records—whether they took public records with them—whether they took private records with them, and that includes the long list of texts and emails and on and on and on. What you’ll find, then, is that you are going to find a lot of collusion between the Department of Justice, the FBI, the CIA, the White House—the whole damned bunch of them—and the media.”

Levin is in the camp of preserving documents now and getting to the prosecution later. Sounds great to me. The other huge issue the announcement fails to address is WHERE this grand jury will be convened. Will this grand jury be convened in the Southern District of Florida, where the Mar-a-Lago raid took place, or in the lost land of Washington, D.C. where there is ZERO chance that ANY Democrat would be found GUILTY of any crime? The right answer is Florida. Monday night’s move was huge, but only if Bondi is as careful as a cat stalking a bird. Meow. I told you we wouldn’t punk you. We believe that the right move is the grand jury, but not if it’s in DC. That’s felony dumb. The sad situation is that no one remotely right of center would get a fair trial in Washington, D.C. That’s not just sad, it’s true—and it’s criminal.

“The report said that then-President Barack Obama didn’t want Hillary’s scandal to taint his legacy..”

• DOJ To Present Russiagate Hoax To A Grand Jury For Criminal Charges (ZH)

Attorney General Pam Bondi has directed that the Justice Department move forward with a probe into the origins of the Trump-Russia investigation, following the recent release of documents about collusion between the Obama administration and the 2016 Hillary Clinton campaign. Bondi has directed a prosecutor to present evidence to a grand jury after referrals from the Trump administration’s top intelligence official, a person familiar with the matter said Monday. Fox News first reported the development. It was not clear which former officials might be the target of any grand jury activity, where the grand jury that might ultimately hear evidence will be located or which prosecutors — whether career employees or political appointees — might be involved in pursuing the investigation.

It was also not clear what precise claims of misconduct Trump administration officials believe could form the basis of criminal charges, which a grand jury would have to sign off on for an indictment to be issued. In one batch of documents released last month, Gabbard disclosed emails showing that senior Obama administration officials were aware in 2016 that Russians had not hacked state election systems to manipulate the votes in Trump’s favor. Sen. Chuck Grassley, the Republican chairman of the Senate Judiciary Committee, also released a set of emails last week. The emails were part of a classified annex of a report issued in 2023 by John Durham, the special counsel who was appointed during the first Trump administration to hunt for any government misconduct during the Russia investigation.

According to the annex, an FBI informer identified as “TI” provided the bureau in 2016 with two intelligence reports, which described “confidential conversations” between then-Democratic National Committee Chair Debbie Wasserman Schultz and two people at the George Soros-funded Open Society Foundation: Leonard Bernardo and Jeffrey Goldstein. The report said that then-President Barack Obama didn’t want Hillary’s scandal to taint his legacy. Accordingly, “To solve the problem, the President puts pressure on FBI Director James Comey through Attorney General Lynch, however, so far without concrete results.”

The same report also said that Comey favored Republicans, and that the FBI didn’t have any evidence against Clinton—because she deleted her emails. While the FBI informant’s intelligence wasn’t corroborated at the time, the FBI indeed closed its investigation into Clinton without recommending charges. Republicans have particularly focused on a July 27, 2016, email in Durham’s newly declassified annex that claimed that Hillary Clinton had approved a plan during the heat of the campaign to link Trump with Russia. Durham’s own report took pain to note that investigators had not corroborated the communications as authentic and said the best assessment was that the message was “a composites of several emails” the Russians had obtained from hacking.

Possible. Still, it’s not about the outcome, but about the process. Did Ursula fight for Europeans? Looks like she didn’t raise a single finger.

• The EU-US Deal Is Positive and the Only Realistic Alternative (Lacalle)

The agreements the United States has signed with its main trading partners are both positive and realistic. They demonstrate that, in 2024, the world was not a trade paradise of spontaneous cooperation among free-market companies as per David Ricardo’s ideal, but rather a statist system filled with barriers against US businesses and political efforts to pick winners and losers. The controversy surrounding the agreement between the United States and the European Union can only be explained for three reasons: animosity toward any achievements of the Trump administration, ignorance about the only realistic alternative, or because critics of the deal were genuinely satisfied with the protectionism and European barriers in place in 2024.

Critics of the deal must answer two questions: What was the only real alternative? The only real alternative was a collapse in European exports, a loss of competitiveness versus Japan, the United Kingdom, South Korea, and other partners, greater offshoring of companies, and, crucially, keeping existing European trade barriers. What would the critics have done? Critics must explain how they would have achieved supposedly better deals when global export leaders have signed agreements like that of the European Union. They need to share with us what essential information they have that the EU negotiators do not, reportedly enabling them to achieve better conditions than Japan, the United Kingdom, South Korea, Indonesia, Vietnam, the Philippines, Saudi Arabia, Qatar, Australia, China, and others. Is it reasonable to think that EU negotiators were stupid or reckless and did not weigh all options to achieve a beneficial agreement?

Claiming that the agreement with the United States is detrimental is, inadvertently, to defend the trade barriers with Europe’s main global partner as if they were wonderful and should be preserved. It also stems from a fantastical vision of global trade, imagining that the US market could be replaced by others. What’s worse is that some seem to believe all of this is Trump’s fault—a favourite in today’s economic analysis—and that in four years, a Democratic president or a softer Republican will return everything to the way it was in 2024. This is a mistaken vision. Biden kept all the tariffs from the Trump and Obama administrations and increased several of them.

Why wasn’t there a significant outcry when the EU implemented substantial trade barriers or when Democratic presidents established tariffs? The outrage frequently conceals bias against Trump and conveniently overlooks Europe’s persistent imposition of new barriers on US products. Why wasn’t there an outcry over the EU’s tariffs on US chemicals, agriculture, livestock, automobiles, and manufacturing equipment – or over the 2030 Agenda, the New Green Deal, the CO2 tax, and all the constant excessive regulation? It took Draghi to remind us that the EU imposes more hidden tariffs on itself than the United States does.

“Law Enforcement Tools to Interdict Troubling Investments in Abodes”.

• GOP Could Bring Down Adam Schiff and Letitia James with LETITIA Act (Margolis)

It looks like Senate Republicans aren’t just talking tough on corruption—they’re laying the groundwork for real accountability, and Democrats like Sen. Adam Schiff and New York Attorney General Letitia James may finally have reason to worry. Sen. John Cornyn has introduced the Law Enforcement Tools to Interdict Troubling Investments in Abodes—or the LETITIA Act, pointedly named after the New York AG herself. But this isn’t just a symbolic jab. The bill represents a serious move to expand criminal liability and, more importantly, stiffen penalties for public officials who abuse their positions for personal gain—specifically through shady dealings like mortgage or tax fraud.

There’s no mistaking the intent behind this legislation. Letitia James is famous for her partisan pursuit of President Trump, yet she herself now entangled in a federal investigation over mortgage fraud. But the real intrigue emerges with the bill’s potential impact on Adam Schiff—the very same Schiff who for years cloaked himself in the language of integrity while leading partisan witch hunts against Trump and his allies. The tables may be turning. Details in the public record are damning. Housing authority Bill Pulte has accused Schiff of falsifying bank documents and misrepresenting primary residences across multiple states to secure more favorable mortgage terms. These aren’t garden-variety clerical mistakes—they’re deliberate moves that, under Cornyn’s proposal, would be subject to mandatory prison terms.

If signed into law, the LETITIA Act would slap public officials convicted of bank fraud, loan or mortgage fraud, or tax fraud with minimum sentences—one year for bank or loan fraud, six months for tax fraud—ratcheting up to five years for repeated patterns of abuse. No more tepid reprimands or backroom wrist-slaps for insiders who get caught. So, is this the moment where the Senate GOP draws a legal bullseye on Adam Schiff? Cornyn makes no effort to hide his intention to empower President Trump and authorities to finally “hold crooked politicians like New York’s Letitia James accountable for defrauding their constituents, violating their oath of office, and breaking the law.” The context leaves little doubt: this bill is meant not just as a warning to all but as a calibrated legislative knife aimed specifically at the likes of James and Schiff—high-ranking Democrats who have made a career out of prosecuting their rivals and hoisting the banner of unassailable virtue.

Adam Schiff, having cultivated an image as the tireless force against corruption and chaos, now finds that the same legal tripwires he spent years setting for others could be lying directly in his path. The Justice Department hasn’t pressed charges yet, but the bill puts a powerful tool in their hands—one designed to close the loopholes that have too long separated members of the political elite from real-world accountability.

When law’s hammer falls, it must strike without favoritism. The message from Senate Republicans is unmistakable: if Schiff is guilty of the mortgage fraud allegations leveled against him, he should face the same jail time and personal ruin the system eagerly imposes on anyone outside the Beltway. The LETITIA Act, if passed and enforced, tears down the shield of privilege, daring to answer the question: Will Adam Schiff finally be held legally accountable? The answer may come sooner rather than later. For now, the Senate GOP has set the stage. The only thing left is for the Justice Department to decide whether it will step up and bring the same intensity to prosecuting Schiff as he did to others.

“Those who dared to challenge the regime were met not with due process, but with the full force of a weaponized federal machine.”

• ‘Biden’s DOJ Secretly Targeted Trump’s Inner Circle (Margolis)

There are new, disturbing revelations about the weaponization of the federal government against former Trump officials that demand attention. Just weeks before returning to the White House, officials who served President Donald Trump during his first term discovered they had been swept up in a politically charged dragnet under orders from the Biden administration. Google, following a legal process that the FBI triggered, quietly collected personal information from their accounts, only alerting the targets after the fact, and only because the court-imposed gag order had finally lifted. Dan Scavino, now White House Deputy Chief of Staff, received one of these anonymous yet chilling notifications from Google.

“Google received and responded to a legal process issued by the Federal Bureau of Investigation compelling the release of information related to your Google account. A court order previously prohibited Google from notifying you of the legal process…” The Orwellian undertone cannot be missed. Scavino described it as “Biden lawfare” in action, calling it “a small taste of the INSANITY that many of us went through—right here in the United States of America. LAWFARE at its finest. A Complete and Total Disgrace!!!!!” According to Fox News Digital, soon after Scavino’s post, Kash Patel, who now serves as FBI Director, revealed he too received one of these covert warnings. This wasn’t a one-off; this was a coordinated campaign of intimidation. Jeff Clark, acting administrator at the Office of Information and Regulatory Affairs, also stepped forward, stating he got a similar message.

“Indeed, a whole Jack Smith team was assigned to go through my emails after there was a privilege review.” Clark didn’t stop there; he exposed how the “group of lawyers ignored my religious pastor privilege, marital privilege, and other privileges and basically shipped all they could to Jack Smith. But it still cost me tens of thousands to try to protect my communications.” Smith, the former special counsel whom Merrick Garland handpicked, got the green light to relentlessly pursue Donald Trump and his allies through a series of politically charged investigations. His mandate? To criminalize Trump’s efforts to challenge the highly questionable 2020 election results and, later, to go after him over the possession of classified documents at Mar-a-Lago, despite a long history of former officials handling such matters without prosecution.

Smith’s team rolled through personal data with utter disregard for privacy and protected communication. “My medical records and other private communications had nothing to do with the 2020 election,” Clark said. “They were no one’s business. But it didn’t matter to these thugs with law degrees and the willingness to abuse government power.” This was vengeance dressed up in legal jargon. And once again, we’re staring down undeniable proof that under Biden’s watch, the law wasn’t blind; it was a weapon aimed squarely at his political enemies. The administration didn’t treat the Constitution as a safeguard but as an obstacle to ignore. Those who dared to challenge the regime were met not with due process, but with the full force of a weaponized federal machine. This is the legacy of the Left’s “justice”: intimidate, isolate, and destroy.

The countries you seek to sanction will need oil regardless, but they will have to pay a higher price. That lifts global oil prices, so Russia gets paid more.

• Sanctions On Russia’s Partners ‘Obvious Next Step’ – US NATO Envoy (RT)

Targeting Russia’s partners with sanctions and tariffs is the “obvious next step” in US efforts to mediate the Ukraine conflict, Washington’s ambassador to NATO, Matthew Whitaker, says. Moscow has stated that it is open to talks, holding three rounds of US-mediated negotiations with Kiev in the past two months that resulted in major prisoner swaps and settlement proposals. It views the conflict as a Western proxy war and has said the hostilities would end if Kiev accepts neutrality and demilitarization. US President Donald Trump has expressed frustration with delays in settlement efforts and threatened to place 100% tariffs and secondary sanctions on Russia’s trade partners if a deal is not reached by August 8.

“President Trump’s been clear that this war needs to end… And… is creating the environment that Russia will come to the table and negotiate a ceasefire,” Whitaker told Bloomberg TV on Monday.“Secondary sanctions and tariffs against those that are paying for this war, like China, India, and Brazil, by buying the oil that Russia is producing, is an obvious next step to try to bring this war to an end.” While Trump has acknowledged that new sanctions might prove ineffective, Whitaker said Washington sees targeting Russia’s oil trade as worth trying. “I think this is going to really hit them where it counts, and that is in their main revenue source, which is the sale of oil to these countries,” he stated.

On Monday, Trump threatened New Delhi with new tariffs unless it halts Russian oil purchases. India has refused to take part in the sanctions on Russia, calling its energy trade a matter of national interest. Moscow has faced waves of Western sanctions since the Ukraine conflict escalated in 2022. It has condemned them as illegal and counterproductive, adding that they have largely failed, as Russia redirected most of its trade to Asia, with China and India now its biggest energy buyers. Russian officials say the sanctions will not alter the course of the conflict and have downplayed Trump’s threats, adding that the country has built “immunity” after years of sanctions.

Matthew Whitaker, US ambassador to NATO, discusses the Netherlands contributing €500 million ($579 million) to Ukraine’s defense as part of a US initiative on "Balance of Power" https://t.co/HqmzRv4NHY pic.twitter.com/Uq1pOt00ag

— Bloomberg TV (@BloombergTV) August 4, 2025

I call BS on Moody’s. They appear to play politics.

Tariffs may influence where money flows in America, but the money stays in the country. Part is used to pay down the debt, part flows back to the people.

Likewise, fewer immigrant jobs means more American jobs. Maybe they get paid more, but that money, too, stays in the country.

How can this add up to a recession? There’s simply a shift in money flows.

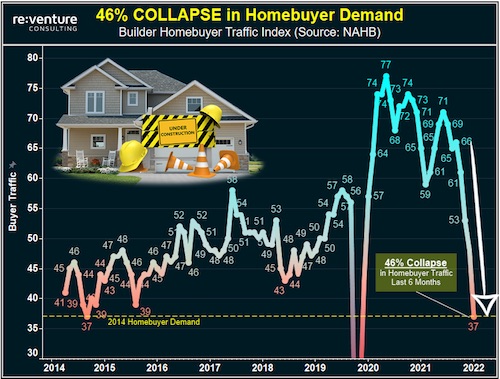

• US ‘On Precipice’ Of Recession – Moody’s (RT)

US President Donald Trump’s tariffs and immigration policy are pushing the economy toward a downturn, Moody’s chief analyst, Mark Zandi, has warned. He described the US as “on the precipice” of a recession.The warning followed a Bureau of Labor Statistics report showing the US added an average of just 35,000 jobs a month from May to July – less than a third of last year’s pace and the weakest since 2020. Experts say the slowdown signals weakening economic growth. Other indicators have also been bleak: June consumer spending rose only 0.1% after inflation, prices climbed 2.7% year-on-year – the highest since February – and factory activity contracted for the fourth straight month as orders and jobs fell.

“The economy is on the precipice of recession. That’s the clear takeaway from last week’s economic data dump,” Zandi wrote on X on Sunday. “Consumer spending has flatlined, construction and manufacturing are contracting, and employment is set to fall.”He warned that inflation above target leaves the Federal Reserve little room to revive growth, especially under Trump’s policies.“It’s no mystery why the economy is struggling; blame increasing US tariffs and highly restrictive immigration policy,” Zandi stated. “The tariffs are cutting increasingly deeply into the profits of American companies and the purchasing power of American households. Fewer immigrant workers means a smaller economy.”

Since returning to office, Trump has tightened restrictions on illegal immigration, planning to deport 4 million people over four years – a move many warn will trigger severe labor shortages. He has also imposed tariffs on hundreds of US trade partners, framing them as a “reciprocal” strategy to secure better trade terms, protect jobs, revive manufacturing, cut deficits, and fund tax relief. Zandi is not alone in warning of the risks. Fed Chair Jerome Powell has cautioned that tariffs could sharply raise both inflation and unemployment. The Economic Policy Institute estimated that Trump’s mass deportations plan could destroy nearly 6 million jobs. Trump’s alma mater, the University of Pennsylvania’s Wharton School, warned that deportations would shrink most worker paychecks, cut GDP, and further swell the already massive federal budget deficit.

“..a contract for electronic warfare systems at an intentionally inflated price, with the group receiving illegal benefits worth 30% of the contract amount.”

• Ukrainian Officials Busted In ‘Large-Scale’ Military Bribery Scheme (RT)

Several senior Ukrainian officials have been detained on suspicion of receiving up to 30% in kickbacks from military contracts, anti-corruption agencies have announced. The arrests came just days after Ukrainian leader Vladimir Zelensky was forced to abandon his attempts to restrict the independence of the anti-graft agencies.In a statement on Saturday, the National Anti-Corruption Bureau of Ukraine (NABU) and the Specialized Anti-Corruption Prosecutor’s Office (SAPO) said they had uncovered a “large-scale” corruption scheme involving contracts for the purchase of drones and electronic warfare systems for the Ukrainian army.

Ukrainian media has identified three of the four suspects – Aleksey Kuznetsov, an MP with Zelensky’s Servant of the People party, former Lugansk Governor Sergey Gayday, and Rubezhansky district head Andrey Yurchenko. Between 2024 and 2025, the group allegedly created a scheme to steal budget funds allocated by local governments for defense needs. One part of the scheme involved awarding a contract for electronic warfare systems at an intentionally inflated price, with the group receiving illegal benefits worth 30% of the contract amount.

A separate contract for FPV drones, worth around $240,000, was allegedly overpriced by around $80,000, with the company’s officials later handing over kickbacks to members of the group, the investigators said. The same day, Zelensky stated that he had met with the heads of NABU and SAPO to discuss the scandal, calling it “absolutely immoral” and thanked the agencies for their good work. Two weeks earlier Zelensky had attempted to bring both bodies under government control only for street protests to force him to sign off on their independence last week.

“Europe is no longer the center of the world it once was. It has become a theater, not a director, of global affairs.”

• Europe’s Last Security Project Is Quietly Collapsing (Lukyanov)

This week marks the 50th anniversary of a landmark event in European diplomacy. In 1975, the leaders of 35 countries, including the United States, Canada, and almost all of Europe, gathered in the Finnish capital Helsinki to sign the Final Act of the Conference on Security and Cooperation in Europe (CSCE). The agreement capped years of negotiation over peaceful coexistence between two rival systems that had dominated world affairs since the end of the Second World War. At the time, many believed the Final Act would solidify the postwar status quo. It formally recognized existing borders – including those of Poland, the two Germanys, and the Soviet Union – and acknowledged the spheres of influence that had shaped Europe since 1945. More than just a diplomatic document, it was seen as a framework for managing ideological confrontation.

Fifty years later, the legacy of Helsinki is deeply paradoxical. On the one hand, the Final Act laid out a set of high-minded principles: mutual respect, non-intervention, peaceful dispute resolution, inviolable borders, and cooperation for mutual benefit. In many ways, it offered a vision of ideal interstate relations. Who could object to such goals? Yet these principles were not born in a vacuum. They were underpinned by a stable balance of power between the NATO and the Warsaw Pact. The Cold War, for all its dangers, provided a kind of structure. It was a continuation of the Second World War by other means – and its rules, however harsh, were understood and largely respected. That system no longer exists. The global order that emerged after 1945 has disintegrated, with no clear replacement.

The post-Cold War attempts to graft a Western-led system onto the rest of Europe succeeded only briefly. The OSCE, which evolved from the CSCE, became a vehicle for imposing Western norms on others – a role it can no longer credibly perform. Despite the growing need for cooperation in an unstable world, the OSCE today exists mostly in theory. The notion of ‘pan-European security’ that underpinned the Helsinki Process has become obsolete. Processes are now fragmented and asymmetric; rivals are unequal and numerous. There is no longer a shared framework to manage disagreements. That hasn’t stopped calls to revive the OSCE as a political mediator, particularly amid recent European crises. But can an institution forged in a bipolar world adapt to the multipolar disorder of today?

History suggests otherwise. Most institutions created in the mid-20th century have lost relevance in periods of upheaval. Even NATO and the EU, long considered pillars of the West, face mounting internal and external pressures. Whether they endure or give way to new, more flexible groupings remains to be seen. The fundamental problem is that the idea of European security itself has changed – or perhaps disappeared. Europe is no longer the center of the world it once was. It has become a theater, not a director, of global affairs. For Washington, Europe is increasingly a secondary concern, viewed through the lens of its rivalry with China. American strategic planning now sees Europe mainly as a market and an auxiliary partner, not a driver of global policy.

“They use Ukrainian artifacts to raise money. With African artifacts, they just do business.”

• Colonial Theft vs. Wartime Fundraising: The Double Standard of Western Museums (Sp.)

Europe’s museums and not just British ones hold artifacts stolen during colonial rule, forming part of Europe’s wealth, says Yamb Ntimba, political philosopher and founder of the Kheper think tank. These objects are displayed because Europe lacks its own heritage of such diversity, using others’ culture to fuel its economy and tourism. “But with Ukrainian artifacts, the situation is different. They are being used to stir sympathy among the public for Ukraine. That sympathy supports government actions to provide Ukraine with weapons and money.” African artifacts serve as trophies of conquest, displayed in Europe to showcase past dominance over Africa and reinforce a sense of superiority, the commentator believes.

“As for Ukrainian artifacts, I see it as manipulation. They manipulate the minds of their people to create an emotional basis for supporting Ukraine. They send weapons, give money, dispatch soldiers. This is an entirely different path. There are no parallels. It should be clear to everyone: Africa is not Ukraine, and Ukraine is not Africa,” he tells Sputnik. “The exhibition of Ukrainian artifacts is nothing but a fundraising operation. This will be special revenue used to support the war in Ukraine. But people should know that these museums, earning £3.4 billion, get at least 40% of it from African artifacts. That’s money Africa loses simply because our artifacts are there. They do not share these funds with Africa. They use Ukrainian artifacts to raise money. With African artifacts, they just do business.”

4 Paul Craig Roberts aticles in a row. Oh well, let’s have it. He’s shifting away frrom blaming Trump and Putin for everything under the sun.

“..civilization has been replaced by a short-term agenda to maximize short-term profits regardless of cost.”

• Thank God for Robert F. Kennedy (Paul Craig Roberts)

For at least two decades it has been an unassailable hard scientific fact that mercury in vaccines is highly toxic and responsible for serious injuries and child development problems. But campaign contributions from the criminal pharmaceutical industry to the whore US Congress and the whore American media living on Big Pharma advertisements put profits before health and life. Honest scientists were demonized as “anti-vaxers” and threatened with loss of employment. The scientifically ignorant American population was indoctrinated that vaccine critics, such as Robert F. Kennedy, were threats to the health and lives of their children.

Their own doctors, dumbshit shills of the pharmaceutical industry, told them that only 54 doses of vaccines filled with mercury could save their children, and the ignorant parents believed them. Consequently, a plethora of childhood afflictions never previously seen characterize the deceptively imposed vaccine era. Robert F. Kennedy, son and nephew of his CIA-murdered father and uncle, has used his authority as Secretary of Health to remove mercury from vaccines used in America. This accomplishment in itself justifies the Trump presidency. In my opinion, the pharmaceutical corporations comprise a criminal conspiracy against the American people in which profits come before health. The only solution is to nationalize the pharmaceutical industry and to get Big Pharma money out of health policy and health education.

My “socialist” recommendation will shock free-market libertarians who continue to hold on to their naive faith that private business can do no wrong. As a life-time libertarian I have been taught by endless examples over the course of my long life of profit-driven private business totally failing every public interest, including, peace, health, and truth. Can any honest libertarian find any redemption in the privately owned media? Is there any example anywhere of a state controlled media worst than CNN, the New York Times, Bloomberg? Did Hitler or Stalin have a journalist worse than Jake Trapper?

The reason I think that Western civilization or its remnants will not survive much beyond my lifetime is that civilization has been replaced by a short-term agenda to maximize short-term profits regardless of cost. Corporations make decisions on short-run stock prices, Governments make decisions based on quarterly employment and GDP numbers which are so poorly calculated as to be worthless. Prosecutors make decisions based on maximizing their conviction rates. Judges make decisions based on clearing their court dockets. No one in the West makes decisions based on the relevant issues that confront us.

Justice demands that Big Pharma and its whore media accomplices be held accountable in class action law suits for negligence in exposing millions of Americans to unnecessary mercury injections. If I had to bet, I would bet that in the agreement Kennedy achieved to ban mercury from vaccines, there is a clause that Big Pharma admits nothing and cannot be sued. In America money is power, not truth, not justice. Money can only be overthrown by violence. Karl Marx said that violence is the only effective force in history. Was he correct?

“Is Trump’s over-the-top confidence a guise to hide his submissiveness to Israel? Is Netanyahu the real boss?”

• I Run The Country and The World”: Donald Trump (Paul Craig Roberts)

“I run the country and the world” Donald Trump says in Atlantic interview. The whore media is making much out of this. However, when you think about it, Trump’s over-lthe-top expression of confidence is easy to understand. He came back from, and triumphed over, the worst combination of political and personal blows imaginable.

Some Senate Rinos voted to convict him on the House impeachment charges; Republicans allowed Democrats to steal his re-election; Republicans supported the Democrats’ “insurrection” charges and the kangaroo trials of supporters who attended the January 6 rally; a corrupt New York court (are there any honest courts in NY?) tried to steal his NY properties; golf tournaments blacklisted his golf courses; a corrupt Justice (sic) Department, CIA, and FBI working with Hillary Clinton orchestrated a frame-up of Trump with the Russiagate hoax; corrupt Democrat prosecutors in NY and Georgia prosecuted him on false charges; week after week the whore media served the attacks on Trump, emphasizing the four indictments and speculating on his time in prison. From all of this and more, Trump came back, took control of the Republican Party, mobilized the electorate, and decisively defeated the Democrats.

Trump deserves his confidence. He has done good things. He has stopped the immigrant invasion whether or not the Men in Black allow him to deport the illegals. He has recalled the Democrats’ DEI policy of intentionally discriminating against white people, especially heterosexual males, whether or not the corrupt Democrat civil service abides by his ruling. He has enabled Health Secretary Robert Kennedy to chip away at Big Pharma’s control over health policy that puts profits before health. He has enabled his Director of National Intelligence to expose the criminal actions of the Obama Five who weaponized law against democracy.

Trump’s confidence has produced huge accomplishments for which we should be very appreciative. But Trump must not let his confidence get over-the-top in his dealings with Russia, China, and Iran. The ultimatum Trump delivered to Putin is both nonsensical and dangerous. It has probably convinced Russia that war is inevitable. If indications are reliable that Putin, finally, is equipping Iran with the S-400 air defense system, US and Israeli attacks on Iran are ceasing to be an option. And someone needs to tell Trump that his tariffs on China fall on the offshored production of US corporations. It is the offshored production of US firms that is the main cause of the US trade deficit with China. On this front the Trump administration seems to lack economic competence. His tariff threats to the entire world come across as bullying.

Before we get disillusioned with Trump, think about what it would be like under the Democrats: open borders, weaponized law, DEI discrimination against white people and merit, no limits on Big Pharma’s profits -before- health policy, persecutions of Christians. In effect, an all-out attack on what remains of American society. Trump’s biggest failure is on the Israel front. He has continued Washington’s policy of enabling Israel’s genocide of Palestine, military attacks on Iran, and absorption of parts of Syria into Greater Israel. The question is raised: Is Trump’s over-the-top confidence a guise to hide his submissiveness to Israel? Is Netanyahu the real boss?

“Trump issues meaningless ultimatums that show that Trump is not sincere about ending tensions with Russia.”

• Is Trump Taking Us to War? (Paul Craig Roberts)

I need to be more empathetic with Putin’s hopes. Sometimes I, too, let hopes run away with me. Yes, I was wrong to hope President Trump would normalize relations with Russia. Perhaps Trump intended to do so, until the men in black knocked on his door and told him that he was not allowed to takeaway the enemy that justified the power and profit of the military/security complex. In the era of nuclear weapons it makes perfect sense to be on good terms with other nuclear powers. Mutual suspicions and high tensions can result in catastrophic consequences. Russia has not threatened us and clearly has no territorial ambitions. Putin’s ambition is a mutual security agreement with the West.For some reason Trump won’t consider it. Perhaps the situation is one of armament profits taking precedence over life.

Trump doesn’t negotiate. He delivers ultimatums with punishments attached for non-compliance. Never during the Cold War did an American president issue an ultimatum to the Soviet leader. What is Putin supposed to comply with? Trump hasn’t told us or Putin. It seems that Trump intends for Putin to make a deal with Zelensky to end the conflict. But how can Putin do this when Zelensky has said that his terms are for Russia to give back Donbas, Crimea, and pay war reparations, when Zelensky is no longer officially the president and has no authority to negotiate for Ukraine, and when Zelensky is merely the proxy that Washington is using in its war with Russia?Trump says it is not his war. Perhaps, but it is Washington’s war, and Trump is the president in Washington. So it is Trump’s war.

Trump can stop the war by ending weapons delivery, financing, and diplomatic cover, but Trump has not done so. Trump can stop the conflict by sitting down with Putin, understanding what Putin means by “the root causes of the war,” and addressing these issues, but Trump has not done so. Instead, Trump issues meaningless ultimatums that show that Trump is not sincere about ending tensions with Russia. Clearly, ultimatums are not the way to normalize relations.

As far as I can tell, the media have not asked Trump what the agreement is or what parts of the agreement are unacceptable to the Russians. It is reckless to issue threats to Russia in an atmosphere so tense. Putin’s efforts to avoid real war have been misinterpreted as irresolution, thus resulting in more provocations. Putin’s avoidance of war is leading to a larger war. At some point the provocation will go too far. Maybe it will be the missiles that Trump and the Germans are talking about firing at Moscow. This is the dangerous situation that urgently needs to be resolved, not the conflict in Ukraine. If the root causes are addressed, the war goes away.

“The principle goal of US foreign policy is to prevent the rise of any country that can serve as a constraint on US unilateralism.”

• A Catastrophic War Seems Inevitable (Paul Craig Roberts)

Yesterday, August 4, Nima and I discussed on Dialogue Works the three iron constraints on the US government that seem to guarantee the world is heading into catastrophic war. https://www.youtube.com/live/AdnUdbcfp3U One constraint is the US foreign policy doctrine of US hegemony over the world, known as the Wolfowitz Doctrine: The principle goal of US foreign policy is to prevent the rise of any country that can serve as a constraint on US unilateralism. This doctrine targets Russia and China. As President Trump recently declared to the Atlantic magazine, ” I run the country and the world.” This is a statement of hegemony. Another constraint is the US military/security complex, a heavy political campaign contributor, which needs enemies, such as Russia, China, Iran, to justify its massive budget and power.

A third constraint is the blackmail power over the US and entire Western world of Epstein’s honey-trap Mossad operation that has films of members of the ruling class having sex with underaged persons. Wrapped up in these chains, no Western leader can undertake action to avoid war.Russian President Putin has contributed to the coming catastrophic war by his ignoring of provocations in the hope that in the end he would secure a mutual security agreement with Washington that would end the tensions that threaten both countries. Putin’s hopes were fruitless, because they ignored the Wolfowitz doctrine, the power of the US military-security complex, and Israel’s blackmail power over the government in America.

In A.P.J. Taylor’s history, The Origins of the Second World War, Taylor points out that the war, which no one intended, including Hitler, resulted from diplomatic blunders, the consequences of which no one understood.Today the same kind of blunders are being repeated, building tensions instead of reducing them. To these tensions Trump adds egomania, which is blinding. The failure of leadership will end in disastrous war.

OK

https://twitter.com/NextNewsNetwork/status/1952523611631223064

RFK

RFK Jr. Reveals: Gardasil Vaccine 37x More Lethal Than Cervical Cancer It Prevents

"Gardasil is probably the single worst mass vaccine that we've ever seen. Vaccine targets millions of pre-teens and teens, for whom the risk of dying from cervical cancer is zero. Nobody in… pic.twitter.com/rr7mJX5gtQ

— Camus (@newstart_2024) August 4, 2025

You've been lied to.

Artificial dyes, seed oils, and ultra-processed foods are destroying your health…

Here are 7 poisons RFK Jr. is banning:

1) Seed Oils pic.twitter.com/DHwf3JO5a5

— Jake Gilman (@jakeglmn) August 5, 2025

Marik

"Chemotherapy Is A Hoax & A Scam Perpetuated By Big Pharma To Make Money At The Expense Of People Who Suffer."

Dr Paul Marik, MD"Chemotherapy Doesn't Save Lives, It Reduces Life….But It Generates Billions Of Dollars."

"Chemotherapy Causes Metastasis, It Spreads Cancer."… pic.twitter.com/NBN6wVdCws

— Valerie Anne Smith (@ValerieAnne1970) August 5, 2025

Note

The moment they stopped printing ‘United States Note’ and replaced it with ‘Federal Reserve Note’ was the moment America changed forever pic.twitter.com/Bd7jlPqxrt

— illuminatibot (@iluminatibot) August 5, 2025

Medical officer reveals Covid Vaccine related HEART ISSUES skyrocketing in active duty Naval officers.

Myocarditis rises 151%

Pulmonary heart disease up 62%

Ischemic heart disease up 69%

Heart Failure increased a whopping 973% pic.twitter.com/rpeIQ63UcU

— healthbot (@thehealthb0t) August 5, 2025

https://twitter.com/EricLDaugh/status/1952454331296350587

Box

https://twitter.com/buitengebieden/status/1952632263125995766

lizard

In 1934 LA Times reports that they found a reptilian city under Los Angeles when excavating pic.twitter.com/jij0A6nIjv

— illuminatibot (@iluminatibot) August 5, 2025

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.