Vincent van Gogh Laboureur dans un champ 1889

Or, as yours truly phrased it 2 weeks ago: The Biggest Ponzi in Human History. But the writer makes a big mistake when she says “this will be passed on to the next generation via inheritance or transfer”. It won’t, because prices will plunge. What will be passed on is the debt.

• The Largest Transfer Of Wealth In Living Memory (OD)

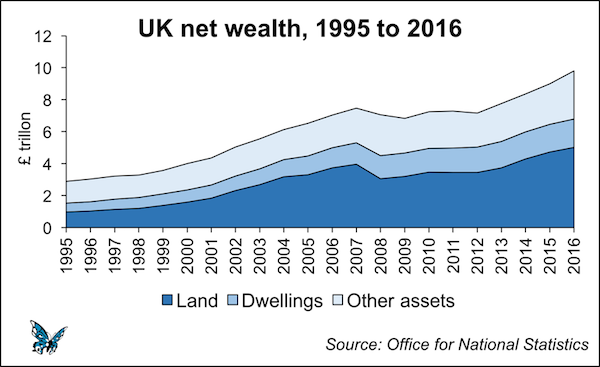

Last week, the Office for National Statistics (ONS) released new data tracking how wealth has evolved over time. On paper, the UK has indeed become much wealthier in recent decades. Net wealth has more than tripled since 1995, increasing by over £7 trillion. This is equivalent to an average increase of nearly £100,000 per person. Impressive stuff. But where has all this wealth come from, and who has it benefitted? Just over £5 trillion, or three quarters of the total increase, is accounted for by increase in the value of dwellings – another name for the UK housing stock. The Office for National Statistics explains that this is “largely due to increases in house prices rather than a change in the volume of dwellings.” This alone is not particularly surprising. We are forever told about the importance of ‘getting a foot on the property ladder’.

The housing market has long been viewed as a perennial source of wealth. But the price of a property is made up of two distinct components: the price of the building itself, and the price of the land that the structure is built upon. This year the ONS has separated out these two components for the first time, and the results are quite astounding. In just two decades the market value of land has quadrupled, increasing recorded wealth by over £4 trillion. The driving force behind rising house prices — and the UK’s growing wealth — has been rapidly escalating land prices. For those who own property, this has provided enormous benefits. According to the Resolution Foundation, homeowners born in the 1940s and 1950s gained an unearned windfall of £80,000 between 1993 and 2014 alone.

In the early 2000s, house price growth was so great that 17% of working-age adults earned more from their house than from their job. Last week The Times reported that during the past three months alone, baby boomers converted £850 million of housing wealth into cash using equity release products – the highest number since records began. A third used the money to buy cars, while more than a quarter used it to fund holidays. Others are choosing to buy more property: the Chartered Institute of Housing has described how the buy-to-let market is being fuelled by older households using their housing wealth to buy more property, renting it out to those who are unable to get a foot on the property ladder. And it is here that we find the dark side of the housing boom.

House prices are now on average nearly eight times that of incomes, more than double the figure of 20 years ago. It’s unlikely that house prices will be able to outpace incomes at the same rate for the next 20 years. The past few decades have spawned a one-off transfer of wealth that is unlikely to be repeated. While the main beneficiaries of this have been the older generations, eventually this will be passed on to the next generation via inheritance or transfer. Already the ‘Bank of Mum and Dad’ has become the ninth biggest mortgage lender. The ultimate result is not just a growing intergenerational divide, but an entrenched class divide between those who own property (or have a claim to it), and those who do not.

The dream is dead.

• How The American Dream Turned Into Greed And Inequality (WEF)

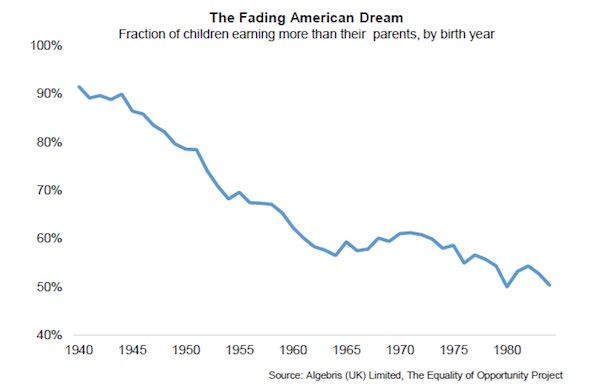

[..] the idea that every American has an equal opportunity to move up in life is false. Social mobility has declined over the past decades, median wages have stagnated and today’s young generation is the first in modern history expected to be poorer than their parents. The lottery of life – the postcode where you were born – can account for up to two thirds of the wealth an individual generates.The growing gap between the rich and the poor, the old and the young, has been largely ignored by policymakers and investors until the recent rise of anti-establishment votes, including those for Brexit in the UK and for President Trump in the US. This is a mistake. Inequality is much more than a side-effect of free market capitalism.

It is a symptom of policy negligence, where for decades, credit and monetary stimulus shortcuts too easily substituted for structural reform, investment and economic strategy. Capitalism has been incredibly successful at boosting wealth, but it has failed at redistributing it. Today, without a push to redistribute wealth and opportunity, our model of capitalism and democracy may face self-destruction. The widening of inequality has deep historical roots. Keynes’ interventionist policies worked well during the post-war recovery, as fiscal stimulus for the reconstruction boosted demand for US goods from Europe and Japan. But soon the stimulus faded. The U.S. found itself with declining growth and rising inflation at a time when it was mired in the Cold War and Vietnam conflicts. The baby boomer generation demanded higher living standards.

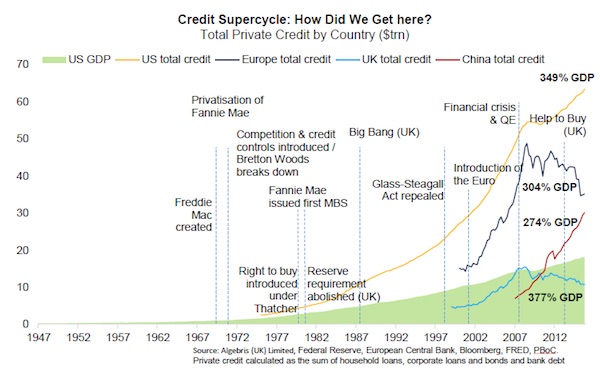

The response was the Nixon shock in 1971: a set of policies which moved away from the gold standard, initiating the era of fiat money and free credit. Credit was the answer to declining growth and rising inequality: if you couldn’t afford university, a new house or a new car, Uncle Sam would lend you the key to the American Dream in the form of that extra loan you needed. Over the following decades, state subsidies to private credit became popular, spreading to the U.K. and Europe. It was the start of debt-based democracies. Private debt outgrew GDP four times in the US and Europe over the following decades up to the 2008 financial crisis, accompanied by the deregulation of financial markets and of banks. The rest is history: nine long years after the crisis, our economies are still healing from excess debt, and regulators are still working on strengthening our financial system. Inequality, however, has deepened even further. Has capitalism failed?

Very good from Chris Hamilton.

• The Fed Destroyed Functioning American Democracy and Bankrupted the Nation (CH)

Against the adamant wishes of the constitutions framers, in 1913 the Federal Reserve System was Congressionally created. According to the Fed’s website, “it was created to provide the nation with a safer, more flexible, and more stable monetary and financial system.” Although parts of the Federal Reserve System share some characteristics with private-sector entities, the Federal Reserve was supposedly established to serve the public interest. A quick overview; monetary policy is the Federal Reserves actions, as a central bank, to achieve three goals specified by Congress: maximum employment, stable prices, and moderate long-term interest rates in the United States. The Federal Reserve conducts the nation’s monetary policy by managing the level of short-term interest rates and influencing the availability and cost of credit in the economy.

Monetary policy directly affects interest rates; it indirectly affects stock prices, wealth, and currency exchange rates. Through these channels, monetary policy influences spending, investment, production, employment, and inflation in the United States. I suggest what truly happened in 1913 was that Congress willingly abdicated a portion of its responsibilities, and through the Federal Reserve, began a process that would undermine the functioning American democracy. How, you ask? The Fed, believing the free-market to be “imperfect” (aka; wrong) believed it should control and set interest rates, determine full employment, determine asset prices; not the “free market”. And here’s what happened:

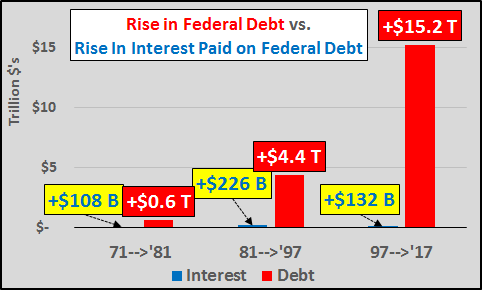

• From 1913 to 1971, an increase of $400 billion in federal debt cost $35 billion in additional annual interest payments.

• From 1971 to 1981, an increase of $600 billion in federal debt cost $108 billion in additional annual interest payments.

• From 1981 to 1997, an increase of $4.4 trillion cost $224 billion in additional annual interest payments.

• From 1997 to 2017, an increase of $15.2 trillion cost “just” $132 billion in additional annual interest payments.

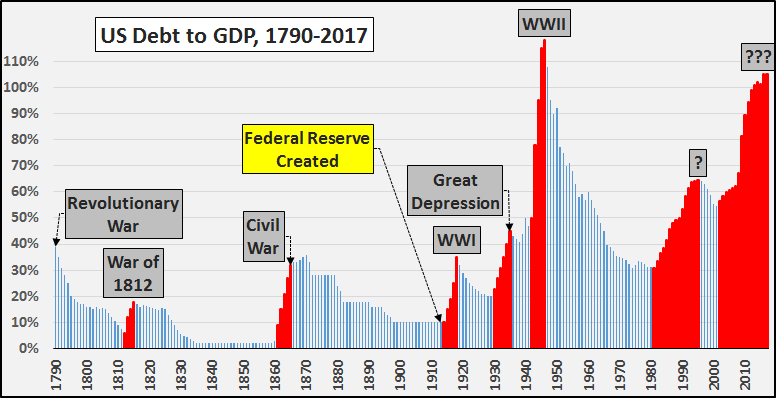

[..] As the chart below highlights, since the creation of the Federal Reserve the growth of debt (relative to growth of economic activity) has gone to levels never dreamed of by the founding fathers. In particular, the systemic surges in debt since 1981 are unlike anything ever seen prior in American history. Although the peak of debt to GDP seen in WWII may have been higher (changes in GDP calculations mean current GDP levels are likely significantly overstating economic activity), the duration and reliance upon debt was entirely tied to the war. Upon the end of the war, the economy did not rely on debt for further growth and total debt fell.

Perhaps the biggest mystery is why the (formerly) left got so involved with it.

• The Fatal Flaw Of Neoliberalism: It’s Bad Economics (Rodrik)

We live in the age of neoliberalism, apparently. But who are neoliberalism’s adherents and disseminators – the neoliberals themselves? Oddly, you have to go back a long time to find anyone explicitly embracing neoliberalism. In 1982, Charles Peters, the longtime editor of the political magazine Washington Monthly, published an essay titled A Neo-Liberal’s Manifesto. It makes for interesting reading 35 years later, since the neoliberalism it describes bears little resemblance to today’s target of derision. The politicians Peters names as exemplifying the movement are not the likes of Thatcher and Reagan, but rather liberals – in the US sense of the word – who have become disillusioned with unions and big government and dropped their prejudices against markets and the military.

The use of the term “neoliberal” exploded in the 1990s, when it became closely associated with two developments, neither of which Peters’s article had mentioned. One of these was financial deregulation, which would culminate in the 2008 financial crash and in the still-lingering euro debacle. The second was economic globalisation, which accelerated thanks to free flows of finance and to a new, more ambitious type of trade agreement. Financialisation and globalisation have become the most overt manifestations of neoliberalism in today’s world.

That neoliberalism is a slippery, shifting concept, with no explicit lobby of defenders, does not mean that it is irrelevant or unreal. Who can deny that the world has experienced a decisive shift toward markets from the 1980s on? Or that centre-left politicians – Democrats in the US, socialists and social democrats in Europe – enthusiastically adopted some of the central creeds of Thatcherism and Reaganism, such as deregulation, privatisation, financial liberalisation and individual enterprise? Much of our contemporary policy discussion remains infused with principles supposedly grounded in the concept of homo economicus, the perfectly rational human being, found in many economic theories, who always pursues his own self-interest.

Wonder what Xi is thinking.

• China Home Sales Fall by Most in Almost Three Years on Curbs (BBG)

China’s new home sales fell by the most in almost three years last month, adding to signs of cooling as local governments keep rolling out curbs to limit price increases. Sales by value dropped 3.4% from a year earlier to 909 billion yuan ($137 billion), according to Bloomberg calculations based on data released Tuesday by the National Bureau of Statistics. That was the biggest year-on-year decline since November 2014. Signs of a property slowdown, including price rises in fewer cities in September, may concern policy makers who want to avoid any sharp economic deceleration. The government is grappling with fueling growth while containing runaway home prices.

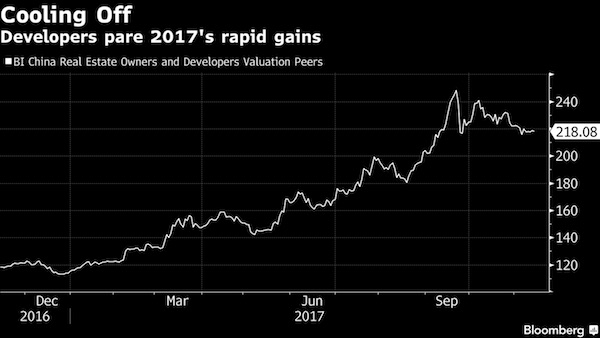

President Xi Jinping last month renewed a yearlong call that homes are built “to be inhabited’’ and not for speculation, in his speech at the twice-a-decade Communist Party Congress, inking the language in one of the nation’s top policy frameworks. Investment in real estate development slowed, growing 5.6% last month from a year earlier, down from a 9.2% increase in September, according to Bloomberg calculations. A Bloomberg Intelligence index of Chinese real-estate owners and developers slipped 0.3%. It’s up 89% this year. The data came amid signs of the government easing financing for property developers and as economic releases for October pointed to a moderating economy.

Excellent takedown of Australia’s dying economic model.

Australia’s Whole Economy Is Built On China Buying Our Stuff

• Australia’s Whole Economy Is Built On China Buying Our Stuff (News.com.au)

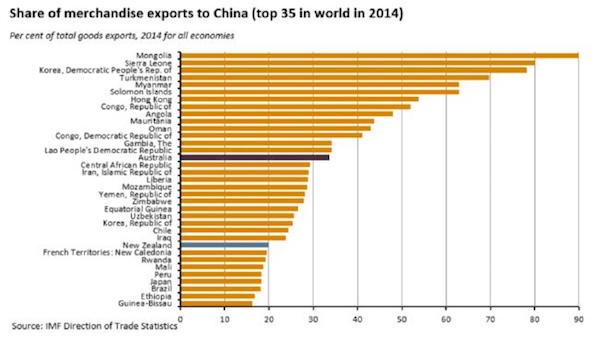

I recently watched the federal Treasurer Scott Morrison proudly proclaim that Australia was in “surprisingly good shape”. Indeed, Australia has just snatched the world record from the Netherlands, achieving its 104th quarter of growth without a recession, making this achievement the longest streak for any OECD country since 1970. I was pretty shocked at the complacency, because after 26 years of economic expansion, the country has very little to show for it. For over a quarter of a century our economy mostly grew because of dumb luck. Luck because our country is relatively large and abundant in natural resources, resources that have been in huge demand from a close neighbour — China. Out of all OECD nations, Australia is the most dependent on China by a huge margin, according to the IMF.

Over one-third of all merchandise exports from this country go to China including all physical products and things we dig out of the ground. Outside of the OECD, Australia ranks just after the Democratic Republic of the Congo, Gambia and the Lao People’s Democratic Republic and just before the Central African Republic, Iran and Liberia. Does anything sound a bit funny about that? As a whole, the Australian economy has grown through a property bubble inflating on top of a mining bubble, built on top of a commodities bubble, driven by a China bubble. Unfortunately for Australia, that “lucky” free ride is just about to end. Societe Generale’s China economist Wei Yao recently said: “Chinese banks are looking down the barrel of a staggering $1.7 trillion worth of losses”. Hayman Capital’s Kyle Bass calls China a “$34 trillion experiment” which is “exploding”, where Chinese bank losses “could exceed 400% of the US banking losses incurred during the subprime crisis”.

A hard landing for China is a catastrophic landing for Australia, with horrific consequences to this country’s delusions of economic grandeur. The initial rally in commodities at the beginning of 2016 was caused by a bet that more economic stimulus and industrial reform in China would lead to a spike in demand for commodities used in construction. That bet rapidly turned into full-blown mania as Chinese investors, starved of opportunity and restricted by government clamp downs in equities, piled into commodities markets. This saw, in April of 2016, enough cotton trading in a single day to make a pair of jeans for everyone on the planet, and enough soybeans for 56 billion servings of tofu. Market turnover on the three Chinese exchanges jumped from a daily average of about $78 billion in February to a peak of $261 billion on April 22, 2016 — exceeding the GDP of Ireland.

It’s the people.

• Austerity, Not Brexit, Has Doomed The Tory Party (G.)

What is destroying the Conservatives is not outside forces, nor the cack-handed pricking of a gusher of ministerial ineptitude. No, the fundamental cause is their own economic strategy of austerity. Of cutting taxes for the wealthy, while cutting public services and social security for the rest. Of rewarding the owners of capital, while punishing those who rely on their labour. Of claiming to have fixed the economy, while tanking voters’ living standards. Austerity is now the thudding drumbeat behind every ministerial misstep, from a family holiday with the Netanyahus to a fauxpology over Nazanin Zaghari-Ratcliffe. It is what unites these individual Westminster outrages into an outline of a ruling party no longer fit for office. By forcing an arbitrary limit on already severely constrained Whitehall and town hall budgets, it renders meaningful government close to impossible.

This is what makes next week’s autumn budget from Philip Hammond so crucial. If the Tories wish to regain any credibility, they will have to ditch the very strategy that defines them. In the days immediately following this summer’s general election, I asked a number of leading figures in Labour how they managed to pull off one of the biggest surprises in postwar political history and rob May of her majority. Their answers all circled back to one thing: austerity fatigue. After seven straight years of seeing their kids’ school classes get bigger and their parents’ hospital waits grow longer, voters were ready for an anti-austerity party leader such as Jeremy Corbyn. Austerity has done more than tear up the public realm; it has imposed private misery on millions of households.

The age of austerity has been the era of the foodbank, the zero-hours contract, the privately rented slum. Unless there is a miracle, the economists at the Resolution Foundation project that the 2010s will be the worst decade for wage growth since the Napoleonic wars of the early 1800s.

But but.. the petrodollar!

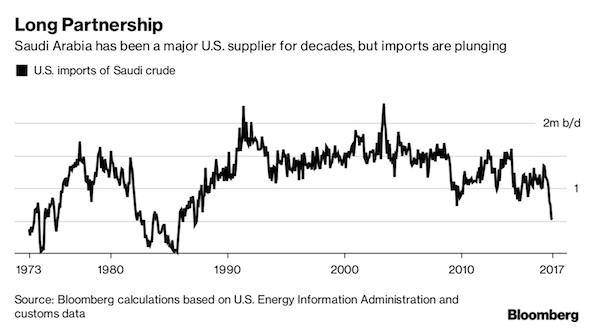

• Saudi Retreat From U.S. Oil Market Cuts Exports to 30-Year Low (BBG)

For a generation, the huge, whitewashed storage tanks at America’s largest oil refinery in Port Arthur, Texas, have stored almost nothing but Saudi crude. The plant is owned the Saudi Arabia’s state-run oil company, Aramco, and since it first bought a stake in 1988, the Motiva refinery guaranteed the kingdom a strategic foothold in the world’s largest energy market. The tankers carrying millions of barrels a month of Arab Light crude from the Saudi export terminals to Port Arthur were testament to the strength of the energy and political ties binding Riyadh and Washington. All of a sudden, there are very few Saudi ships arriving in Texas. Since July, Aramco has constricted supply, attempting to drain the crude storage tanks at Motiva – and many others across America -part of a plan to lift oil prices, even at the cost of sacrificing its once prized U.S.

While Motiva is most affected, the rest of the U.S. oil refining system, from El Segundo in California to Lake Lake Charles in Louisiana, has also taken a hit. The result: Saudi crude exports into America fell to a 30-year low last month. “The drop is huge,” said Amrita Sen, chief oil analyst at consultant Energy Aspects Ltd. in London. “It’s not just that Saudi exports are low, but they have been low for several months.” At a stroke, the freedom from Saudi oil that’s been a rhetorical aspiration for generations of American politicians, from Jimmy Carter to George W. Bush, is within reach – even if it’s largely the choice of supplier rather than the customer. The U.S. imported just 525,000 barrels a day of Saudi crude in October, the lowest since May 1987 and down from 1.5 million barrels a day a decade ago, according to Bloomberg News calculations based on custom data.

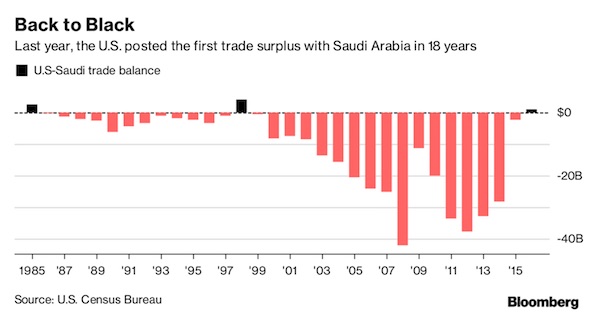

The combination of falling Saudi oil exports into the U.S. last year, cheap crude and higher exports of American weapons had already turned upside-down the trade relationship between the two countries. Last year, the U.S. enjoyed its first trade surplus with Saudi Arabia since 1998 — only the third in 30 years, according to data from the U.S. Census Bureau. The sharper cuts in oil exports since the summer will likely amplify that trend.

“..the United Arab Emirates had planned a military invasion of Qatar with thousands of US-trained mercenaries [..] but it was never carried out as Washington did not give the green light to it..”

• Arab States Spent $130 Billion To Destroy Syria, Libya, Yemen (PressTV)

Algerian Prime Minister Ahmed Ouyahia says some regional Arab states have spent $130 billion to obliterate Syria, Libya and Yemen. Ouyahia made the remarks on Saturday at a time when much of the Middle East and North Africa is in turmoil, grappling with different crises, ranging from terrorism and insecurity to political uncertainty and foreign interference. Algeria maintains that regional states should settle their differences through dialog and that foreign meddling is to their detriment. Syria has been gripped by foreign-sponsored militancy since 2011. Takfirism, which is a trademark of many terrorist groups operating in Syria, is largely influenced by Wahhabism, the radical ideology dominating Saudi Arabia.

Libya has further been struggling with violence and political uncertainty since the country’s former ruler Muammar Gaddafi was deposed in 2011 and later killed in the wake of a US-led NATO military intervention. Daesh has been taking advantage of the chaos in Libya to increase its presence there. Yemen has also witnessed a deadly Saudi war since March 2015 which has led to a humanitarian crisis. Last Month, Qatar’s former deputy prime minister Abdullah bin Hamad al-Attiyah said the United Arab Emirates had planned a military invasion of Qatar with thousands of US-trained mercenaries. The UAE plan for the military action was prepared before the ongoing Qatar rift, but it was never carried out as Washington did not give the green light to it, he noted. In late April, reports said the UAE was quietly expanding its military presence into Africa and the Middle East, namely in Eritrea and Yemen.

As I wrote yesterday, insanity.

• EU Countries Agree To Create A European Mega-Army (R.)

France and Germany edged toward achieving a 70-year-old ambition to integrate European defenses on Monday, signing a pact with 21 other EU governments to fund, develop and deploy armed forces after Britain’s decision to quit the bloc. First proposed in the 1950s and long resisted by Britain, European defense planning, operations and weapons development now stands its best chance in years as London steps aside and the United States pushes Europe to pay more for its security. Foreign and defense ministers gathered at a signing ceremony in Brussels to represent 23 EU governments joining the pact, paving the way for EU leaders to sign it in December. Those governments will for the first time legally bind themselves into joint projects as well as pledging to increase defense spending and contribute to rapid deployments.

“Today we are taking a historic step,” Germany’s Foreign Minister Sigmar Gabriel told reporters. “We are agreeing on the future cooperation on security and defense issues … it’s really a milestone in European development,” he said. The pact includes all EU governments except Britain, which is leaving the bloc, Denmark, which has opted out of defense matters, Ireland, Portugal and Malta. Traditionally neutral Austria was a late addition to the pact. Paris originally wanted a vanguard of EU countries to bring money and assets to French-led military missions and projects, while Berlin has sought to be more inclusive, which could reduce effectiveness. Its backers say that if successful, the formal club of 23 members will give the European Union a more coherent role in tackling international crises and end the kind of shortcomings seen in Libya in 2011, when European allies relied on the United States for air power and munitions.

There are a few things we need to stop doing, urgently.

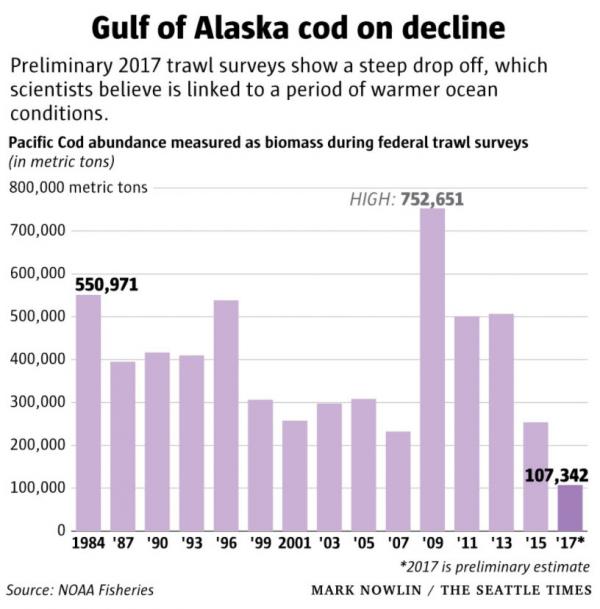

• Fisheries Collapse On US West Coast: “It’s The Worst We’ve Seen” (SHTF)

The Gulf of Alaska cod populations appears to have taken a nose-dive. Scientists are shocked at the collapse and starving fish, making this the “worst they’ve ever seen.” “They [Alaskan cod] get weak and die or get eaten by something else,” said NOAA’s Steve Barbeaux. The 2017 trawl net survey found the lowest numbers of cod on record forcing scientists to try to unravel what happened. A lot of the cod hatched in 2012 appeared to survive, but by 2017, those fish were largely gone for the surveys, which also found scant evidence of fish born in subsequent years. Many of the cod that have come on board trawlers are “long skinny fish” according to Brent Paine, executive director of United Catcher Boats. “This is a big deal,” Paine said. “We just don’t see these (cod) year classes disappear from one year to the next.”

The decline is expected to substantially reduce the gulf cod harvests that in recent years have been worth — before processing — more than $50 million to Northwest and Alaska fishermen who catch them with nets, pot traps, and baited hooks set along the sea bottom. Barbeaux says the warm water, which has spread to depths of more than 1,000 feet, hit the cod like a kind of a double-whammy. Higher temperatures sped up the rate at which young cod burned calories while reducing the food available for the cod to consume. And many are blaming “climate change” for the effects on the fish, although scientists aren’t directly correlating the two events. “They get weak and die or get eaten by something else,” said Barbeaux, who in October presented preliminary survey findings to scientists and industry officials at an Anchorage meeting of the North Pacific Fishery Management Council.