René Magritte The voice of blood 1948

— Elon Musk (@elonmusk) May 15, 2026https://twitter.com/elonmusk/status/2055299836145254860?s=20

https://twitter.com/nicksortor/status/2055411483526181048?s=20 https://twitter.com/EricLDaugh/status/2055645786923282637?s=20BREAKING:

— Crypto Tice (@CryptoTice_) May 15, 2026

The new Fed Chair just signaled a major shift.

Kevin Warsh says QE is fueling inflation.

The Fed's massive balance sheet is part of the problem.

"The Fed should exit markets outside of crises."

This is not Powell talking.

This is a completely different philosophy.… pic.twitter.com/YIFbnESoAs

The IRGC can bleed people profoundly before they squeal.

• Tehran Claims US Faces Escalating Economic Fallout From ‘War Of Choice’ (ZH)

Iranian Foreign Minister Abbas Araghchi warned Saturday that the United States would face mounting economic fallout from its “war of choice” against Iran, as both sides appear settled into a long game of waiting to inflict the most severe economic and political damage on the other. In a post on X, Araghchi said Americans would bear the escalating financial costs of the conflict with Tehran. “Put aside gas price hike and stock market bubble. Real pain begins when U.S. debt and mortgage rates start to jump,” he wrote in English. This isn’t the first time Iranian officials and state media have tried to directly appeal to the American public.Read more …

Araghchi also pointed to growing economic strain inside the United States, saying auto loan delinquencies had already climbed to their highest level in more than 30 years. “This was all avoidable,” he added, framing the start of the conflict as Trump’s ‘war of choice’ in the Middle East. Of course, the Pentagon has a big card to play too, as on Saturday US Central Command (CENTCOM) announced that four vessels in the Hormuz area were “disabled to ensure compliance.” In an official statement it said that that since the imposition of a naval blockade on Iranian ports, 75 commercial vessels have been redirected and four others disabled to “ensure compliance”. There is no doubt the US naval blockade is putting immense economic pressure on the Iranian government, society, and the energy sectors as crude shit-ins loom, or are in progress…

The internal Iranian regime narrative has shifted markedly in the past 72 hours. Multiple officials have now openly acknowledged Iran’s structural gasoline deficit, war-damaged energy infrastructure, and the urgent need for consumption management.

— Miad Maleki (@miadmaleki) May 16, 2026

Fuel shortages and tightened…One Saudi-funded source alleges of the tightening hardship situation inside Iran: Fuel shortages and tighter rationing are pushing drivers across Iran into a growing gasoline black market, with citizens describing long lines at gas stations and sharply inflated prices in messages sent to Iran International. The accounts describe growing frustration over restricted access to subsidized gasoline and arbitrary limits imposed by operators, leaving many motorists dependent on costly unofficial sales.

…Iran uses a subsidized fuel quota system controlled through electronic fuel cards. Every private vehicle receives a monthly gasoline allocation at discounted prices, while extra consumption is charged at higher rates. One citizen was cited in the same report as complaining: “One day there’s quota left on your card, the next day it says your quota is finished. They even steal the few drops of gasoline they give people.” The standoff drags on, amid reports the Trump administration is mulling resumption of the bombing campaign:

https://twitter.com/PressTV/status/2055259398931640510?ref_src=twsrc%5Etfw%7Ctwcamp%5Etweetembed%7Ctwterm%5E2055259398931640510%7Ctwgr%5E2be4e3dba3fd169c51e6df528881831460a20f72%7Ctwcon%5Es1_c10&ref_url=https%3A%2F%2Fwww.zerohedge.com%2Fmarkets%2Ftehran-warns-us-faces-escalating-economic-fallout-war-choice-hardship-mounting-inside-iran

However, US and Gulf media reports about the economic and political crisis inside Iran have often been somewhat exaggerated, in ‘hopes’ of anti-regime sentiment being stirred enough for some kind of new anti-government uprising. But that has yet to come, after months of war launched by the US and Israel. It seems Washington is still pinning its hopes on exactly this.

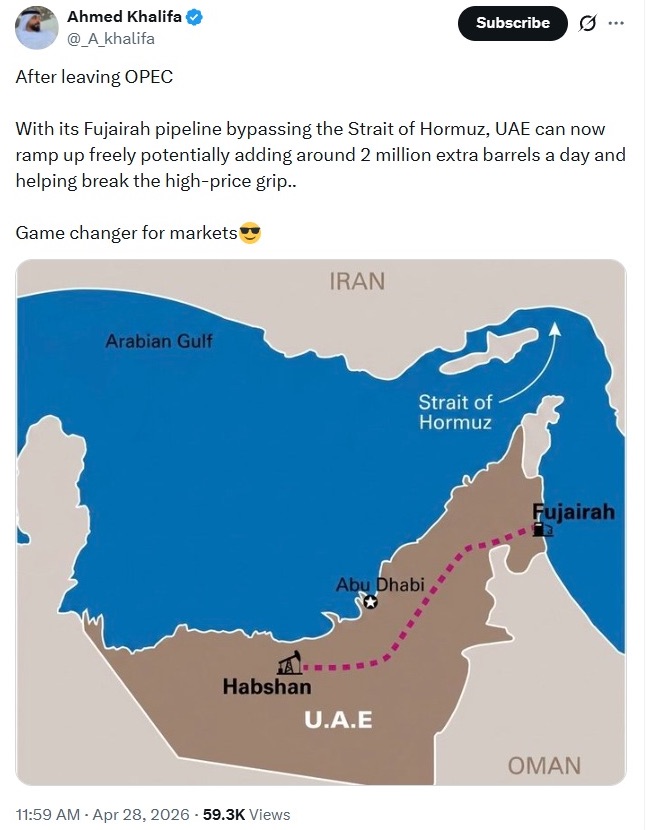

“Bahrain, Kuwait, and Oman joined Saudi Arabia and Qatar in rejecting the UAE plan.”

• Persian Gulf Countries ‘Refused’ UAE Call For Joint Attack On Iran (Cradle)

The UAE tried but failed to persuade neighboring states, including Saudi Arabia and Qatar, to take part in a coordinated military attack on Iran, Bloomberg reported Friday, citing sources familiar with the matter. UAE President Mohammed bin Zayed (MbZ) spoke by phone with Saudi Crown Prince Mohammed bin Salman (MbS) and other regional leaders to propose the coordinated attacks, shortly after the US and Israel launched the war on Iran on February 28, the sources said.Read more …

During the calls, MbZ argued that the states that formed the Gulf Cooperation Council (GCC) must act as a bloc to attack Iran alongside the US and Israel. However, his fellow Gulf leaders told him it was “not their war,” according to the report. When Saudi Crown Prince MbS refused to go along with the scheme, already shaky ties between the UAE and Saudi Arabia were further strained. The Saudi refusal also contributed to the Emirates’ decision to leave OPEC and OPEC+, the oil-producing cartel, and deepen its existing ties to Israel.The UAE ultimately carried out several strikes against Iran without support from other Gulf states in early March and in April. Iran targeted US bases and oil facilities in Saudi Arabia with drones in the first days of the war. Yet the kingdom focused its efforts on promoting Pakistani-mediated negotiations between Washington and Tehran. Qatar considered joining the UAE in an attack after Iranian missile strikes hit Doha’s Ras Laffan Industrial City, the world’s largest liquefied natural gas (LNG) facility, causing extensive damage and major fires, a Gulf official said. However, Doha also ultimately chose to de-escalate and throw its support behind negotiations.

Bahrain, Kuwait, and Oman joined Saudi Arabia and Qatar in rejecting the UAE plan. One source said US officials were aware of the UAE effort and that Washington pushed Saudi Arabia and Qatar to join a coordinated military response. On Thursday, the Financial Times (FT) reported that Saudi Arabia had “floated” the possibility of reaching a “non-aggression pact” between Iran and neighboring states modeled on the 1975 Helsinki Accords, which eased tensions during the Cold War in Europe.

The Saudi-proposed pact for the day after the US-Israeli war on Iran ends reportedly has support from several European capitals, which view it as “the best way to avoid future conflict” and have urged Arab states to support it.The British daily cites an unnamed Arab diplomat who says that such a pact would be welcomed “by most Arab and Muslim states, as well as by Iran,” although severe concerns remain about Israel’s continued threats to reignite the war regardless of any deal.

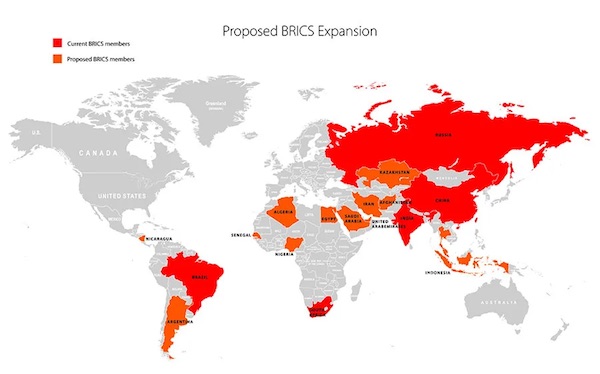

Meanwhile, the two-day meeting of BRICS foreign ministers in New Delhi ended on Friday without a joint statement due to “differing views” on the US-Israeli war against Iran and the current situation in West Asia. The foreign ministers expressed “their respective national positions and shared a range of perspectives,” according to a statement issued by India.

The statement added that one member state had “reservations” about issues related to Gaza, as well as security in the Red Sea and the Bab al-Mandab Strait. Iranian Foreign Minister Abbas Araghchi said during the meeting that “Iran is a country that cannot be divided. The era of American dominance is over.” He also singled out the UAE for blocking the ministerial BRICS statement, and pointed out its “own special relationship with Israel.”

Love the photo.

• China Confirms Boeing Deal, Will Cut Select Levies & Expand Agri Trade (ZH)

One day after President Trump left Beijing, following his multi-day summit with Chinese President Xi Jinping, China’s Commerce Ministry released new details about agreements it had reached to purchaseU.S.. planes and farm goods.Read more …

CHINA, US REACH ARRANGEMENTS ON BUYING US PLANESThe exact wording “reach arrangements”s in the Bloomberg headline is important because it suggests a framework, a commitment, or a negotiated understanding, not necessarily a finalized purchase contract for Boeing commercial jets. Based on earlier reports, Trump said China agreed to buy 200 Boeing planes, with the total potentially rising to 750 aircraft. The next set of headlines shows that the Trump team and Beijing have reached a partial trade de-escalation package following the summit:

CHINA, US AGREE TO REDUCE LEVIES ON A RANGE OF PRODUCTS

CHINA TO EXPAND BILATERAL TRADE W/ US ON AGR AND OTHER PRODUCTS

CHINA VOWS TO EXPAND BILATERAL AGRI TRADE WITH USThe headlines point to a U.S.-China trade détente that is constructive for American industry, exporters, and U.S. farmers. Now the larger question is what Trump and Xi agreed to behind closed doors regarding Tehran and the reopening of the Strait of Hormuz.

U.S. and China Agree To Establish Trade And Investment Boards As Trump-Xi Summit Delivers Modest Wins. U.S. and Chinese leaders agreed to establish a new “Board of Trade” and a parallel “Board of Investment” during President DonaldTrump’ss two-day visit to Beijing – a summit that ended much as it began: with significant pageantry, warm personal rapport between the leaders, and modest, incremental progress on trade. The new boards aim to oversee bilateral purchases, manage trade differences, facilitate deals in non-sensitive sectors (with roughly $30 billion in goods identified), and provide a standing channel to prevent future escalations without constant high-level intervention.The boards were a pre-summit priority pushed by U.S. officials, including Treasury Secretary Scott Bessent and U.S. Trade Representative Jamieson Greer. They build on preparatory talks in South Korea that produced what both sides described as “generally balanced and positive outcomes.” Chinese state media, including Xinhua, highlighted the agreements as part of efforts to expand practical cooperation and maintain stable economic ties.

This development aligns with Xi Jinping’s broader push to reframe the bilateral relationship as one of “constructive strategic stability” – a new guiding vision intended to provide predictability for the next three years and beyond, emphasizing cooperation as the mainstay while allowing for “moderate competition” and “manageable differences.” Xi described it as a positive, sound, constant, and enduring stability that should translate into concrete actions.

“The MAGA wing of the party is the party now. Neither Vance nor Rubio can distance themselves from that if they try.”

• Vance or Rubio in 2028 Have to Be ‘the Bridge to the Future’ (Tim O’Brien)

People have asked Secretary of State Marco Rubio if he plans to run for president in 2028, and his answer has been the same every time. Unequivocally, he endorses Vice President JD Vance, who is assumed to be the likely Republican standard-bearer. At the same time, given the way in which Rubio has been used, while rising to the occasion every time, you cannot ignore him. President Donald Trump has not shied away from praising both Vance and Rubio, but he has been substantially more effusive lately in his comments about Rubio. This has more than a few people in Washington, D.C., chattering.Read more …

Vance had the perfect response for now. But he won’t be able to say this a year from now. In addition to performing the duties of his office, Rubio has taken on any number of ad hoc jobs, knocking it out of the park every time. He knows how to demand and get every other country in the world to respect the U.S. once again. He’s seamlessly put an end to the massive grift that was USAID. Any one of his accomplishments is more than most who’ve run the State Department in recent memory, and he’s not done. Vance is in an even more unenviable position if you’re looking ahead to 2028. It’s the vice president’s job not to show up the president, while at the same time, he cannot wield power the way certain cabinet officials can. This makes it harder for Vance to remind Americans that he can be the alpha.Over the past 250 years, only six vice presidents ran for and won the presidency. And only four won the highest office as an incumbent vice president. They were John Adams, Thomas Jefferson, Martin Van Buren, and George H.W. Bush. Richard Nixon and Joe Biden both eventually were certified as the winners of presidential elections, but not as part of an incumbent administration. When Nixon was the incumbent, he famously ran against John F. Kennedy in 1960 and lost. Biden got pushed aside in 2016 for Hillary Clinton and never got the chance to use his office as a springboard for the presidency. Instead, he was “elected” in 2020 by getting roughly 20 million more votes than any other Democrat candidate before or after. And he did all that by campaigning from his basement, hugging children uncomfortably, and telling stories about “Corn Pop.”

If I were named head of elections, one of the first things I’d do is organize a search party for those missing 20 million voters. Kamala Harris could have used them in 2024. The last incumbent vice president to graduate directly into the Oval Office was Bush. To say that’s not easy to do is an understatement. Playing second-fiddle for four years prior to a run for the highest office in the land can allow voters to forget how strong you are as an independent candidate at the top of a ticket. These are the challenges Vance faces, specifically, but not just Vance. Both he and Rubio will have to be their own men and try to step out from under the long shadow that Trump has cast. Both will have to combat the baggage that the left has continually heaped on Trump and everyone associated with his administration.

Trump created the America First movement. He created and defined Make America Great Again (MAGA). The MAGA wing of the party is the party now. Neither Vance nor Rubio can distance themselves from that if they try. Quite frankly, it would be dumb to try. Contrary to what the legacy media and the left do to frame Trump’s years as “chaos” or a failure, he has been wildly successful, and Americans know it. If Trump can bring the Iran situation under control, get some sort of election integrity guardrails in place, energy prices would come down, inflation would stabilize, and the prospects for a Republican 2028 election victory would be easier to foresee. Who would want to distance themselves from that?

Still, neither Vance nor Rubio can be another Donald J. Trump. They have to carve their own niche, while maintaining some continuity between MAGA and the next Republican administration. Another factor to consider is Trump himself. While he would not want his underlings taking credit for what he did, he also would not want them distancing themselves from MAGA to create their own identity for 2028. That’s a delicate balance. The smartest thing a Vance or a Rubio or even a Vance-Rubio ticket could do in the run-up to 2028 is to map out a comprehensive narrative and progression from MAGA to what’s next. I mean, if you just finished making America great again between 2024 and 2028, you don’t want to use MAGA as your rallying cry now. You need something new and fresh, but you want to stay true to America First.

Former Republican Tennessee governor and U.S. senator Lamar Alexander is coming out with a new autobiography, and he’s making the book tour rounds right now. He recently talked to Politico about the book and his life in politics. To be sure, Alexander represents everything about the Republican establishment that we conservatives are working to get past. He represents a Republican era where the GOP allowed the Democrats to make the rules even when the Republicans won. Kind of like what Senate Majority Leader John Thune (R-S.D.) is doing right now.

Still, Politico asked him if he could have beaten incumbent President Bill Clinton had he gotten the GOP’s nomination instead of Bob Dole. Alexander’s answer is debatable on whether he could have beaten Clinton, but he observed something critical that can’t be overlooked when considering what Vance or Rubio would need to do to win in 2028.

He said, “It would have been hard. I thought I could do better than Dole. I said to Dole: ‘Don’t let [Clinton] have the bridge to the future.’ And Clinton took it and won it.” For either Vance or Rubio, that’s the challenge. To be a part of the Trump administration running for the presidency, you still have to come up with your own brand that’s new and different, while respecting the Trump political lineage and embracing the Trump record.

The rationale has to be: “We need more than four years” to accomplish all the things we set out to accomplish. We can’t go backward. Most importantly, they will need to take ownership of the whole “bridge to the future” brand (as a concept, not as a slogan) before any Democrat gets to it. Trump did just that with “Make America Great Again.” Vance or Rubio can do it and needs to do it pretty soon. The Republican nominee in 2028 must be perceived by the electorate as America’s bridge to a brighter future.

I thought about it, and I decided I’m NOT going to complain.

• Attractive Young Women Are Now The New Face Of The ‘Far-Right’ (ZH)

The Telegraph has published a piece so tone-deaf it reads like self-parody. According to the outlet, the “far-right” is no longer the domain of bald men in boots and tattoos. No, it’s now being led by “strikingly telegenic young women” who dare to look good on camera while warning about mass migration, grooming gangs, and cultural replacement. Three foreign activists – Ada Lluch, Valentina Gomez, and Eva Vlaardingerbroek – were banned from entering Britain for a Tommy Robinson rally, and the Telegraph can’t stop gushing over how “pretty” this makes the movement look. The government has banned at least seven foreign voices from attending the rally, including the women highlighted by the Telegraph.Read more …

Not so long ago, the stock image of someone from the far-Right was easily summoned: they’d be male, obviously, and very probably bald, and questionable tattoos.

— The Telegraph (@Telegraph) May 15, 2026

The face of the far-Right, it seems, is changing – and it’s becoming a good deal prettier ⬇️https://t.co/K8xXWHSdgK pic.twitter.com/irtXPyGD9X

Critics point out the blatant double standard: pro-Palestine marches with openly extremist rhetoric are often tolerated, while a native-focused demonstration drawing tens or hundreds of thousands draws preemptive visa blocks on speakers. Kier Starmer’s government waves in unvetted migrants and certain extremists but draws the line at articulate critics of mass migration. The Telegraph profiles the banned women in breathless detail. Catalan activist Ada Lluch has called out “complete invasion” of western democracies, American influencer Valentina Gomez warned about “rapist Muslims taking over,” and Dutch commentator Eva Vlaardingerbroek spoke of “the rape, replacement and murder of our people.”All three were barred from the UK, along with several other activists. Meanwhile, the government continues to wave in the very people these women are warning about. The Telegraph also warns about attractive home-grown women, including British influencer Saskia Teague. With over 100,000 Instagram followers, she mixes “happy happy happy” selfies with calls for “England for the English,” mass deportations, and an end to shame-free multiculturalism. The Telegraph acts shocked that she also praises her “Anglo-Saxon hair” and rejects the idea she’s being “used” by men.

Of course the usual suspects are wheeled out to clutch pearls. Hope Not Hate researcher Alex MacKinnon calls it a “glamorisation” effort to shed the “violent thug image.” Institute for Strategic Dialogue’s Hannah Rose says looking desirable builds followers and fits the ideology that women should be “aesthetically pleasing.” The implication is that these women can’t possibly believe what they’re saying – they must be grifting or being manipulated. Because in the eyes of the legacy media, no normal young attractive woman could possibly notice what’s happening to her country.

This is the same media that files stories on “far-right” threat while ignoring grooming gang scandals, no-go zones, and skyrocketing violence against women and girls. The Telegraph even admits the shift comes from young people “profoundly disaffected with mainstream parties” and disillusioned with modern life. Yet instead of asking why that disillusionment exists, they obsess over Instagram filters and “zhuzhing” the image. Prime Minister Keir Starmer has today claimed he’s all about “championing peaceful protest” while simultaneously blocking entry to those he dislikes. Starmer declared:

“I’ll always champion peaceful protest. But the Unite the Kingdom march organisers are peddling hatred and division,” then admitting that “We’ve already blocked visas for far-right agitators who want to come here to spew their extremist views.”

“Tina Peters, a 73-year-old woman with cancer, was given a nine year jail sentence in Colorado because she caught the Democrats CHEATING..”

• Colorado Governor Commutes Whistleblower Tina Peters’ Sentence (Salgado)

Colorado 2020 election whistleblower Tina Peters finally received some good news. Peters ended up at the epicenter of national controversy when she reportedly allowed an unauthorized person to access voting equipment in Mesa County in order to expose apparent election irregularities. Gov. Jared Polis (D-Colo.) granted Peters a commutation and parole as of June 1, based on a May 15 press release. Peters is a Gold Star Mother who lost her son, a Navy SEAL, in 2017.Read more …

It appears that the commutation might be due to her backing down somewhat from her previous allegations and efforts to expose apparent election fraud in Colorado back in 2020, when she was an election clerk. It is worth noting that a Democrat who tried to forge a thousand ballots in New Jersey received a sweetheart deal, sparing him any prison time, while Peters received almost a decade in prison as her sentence for trying to call attention to voting irregularities.A statement on X posted on Peters’ account thanked Polis, expressed hopes for the future, and criticized people who had tried to storm the jail in support of her case. It said: I made mistakes, and for those I am sorry. Five years ago I misled the Secretary of State when allowing a person to gain access to county voting equipment. That was wrong. I have learned and grown during my time in prison and going forward I will make sure that my actions always follow the law, and I will avoid the mistakes of the past…

Upon release, I plan to do my best through legal means to support election integrity and based on my own personal experiences to elevate the cause of prison reform to help ensure the detention system is more fair and equitable for people of all ages. My experiences have given me a perspective that plan to share with others to improve Colorado’s corrections system. I am grateful for a second chance and an earlier release, and I look forward to doing good in the world.

Tina Peters https://twitter.com/EricLDaugh/status/2055393588754727270?s=20

President Donald Trump, who has repeatedly called for Colorado to let Peters go altogether, reacted to the news on Truth Social with just two words: “FREE TINA!” In March, he strongly condemned the sentence Peters received for challenging the 2020 election. “Tina Peters, a 73-year-old woman with cancer, was given a nine year jail sentence in Colorado because she caught the Democrats CHEATING on the Presidential Election of 2020. FREE TINA!” he insisted.

A couple of days after that, Trump reflected again on the double standard Democrats impose, letting truly dangerous criminals go free while aggressively targeting their political opponents. “For years, Democrats ignored Violent and Vicious Crime of all shapes, sizes, colors, and types. Violent Criminals who should have been locked up were allowed to attack again. Democrats were also far too happy to let in the worst from the worst countries so they could rip off American Taxpayers,” he wrote.

“Democrats only think there is one crime – Not voting for them!” Trump continued. “Instead of protecting Americans and their Tax Dollars, Democrats chose instead to prosecute anyone they can find who wanted Safe and Secure Elections. Democrats have been relentless in their targeting of TINA PETERS, a Patriot who simply wanted to make sure that our Elections were Fair and Honest. Tina is sitting in a Colorado prison for the ‘crime’ of demanding Honest Elections. FREE TINA!”

And now for something completely different.

• A Society Without God Is a Society Without Truth (Josh Hammer)

Next Thursday evening, Jews will celebrate the holiday of Shavuot. This holiday, which occurs seven weeks and one day after Passover (hence the name Shavuot, which literally means “weeks”), commemorates perhaps the most transformative event in all of human history: the revelation of the Word of God to the ancient Israelite nation. It was at Mount Sinai, congregated at the base of the smoking and trembling mountain, that God promised the Israelites they would be a “kingdom of princes and a holy nation” if they accepted and maintained fidelity to His covenant. In unison, before they had even received the Ten Commandments, the Israelites responded, “All that the Lord has spoken we shall do!”Read more …

The Divine Revelation at Sinai fundamentally changed the relationship between mankind and truth. Before Sinai, mankind had understood truth as inherently subjective, subject to the ever-changing whims of the volatile gods. Now, after Sinai, there could be no such moral confusion. The one, true God — He who had created the universe and fashioned mankind in His image — had revealed His Will. Moral relativism and idolatry were now out. Moral objectivity and monotheism were now in. For the first time, there was a fixed barometer by which to judge man’s moral conduct, devise laws and political institutions, and live one’s day-to-day life more generally.Because of the breadth and depth of its impact and lasting influence, the Divine Revelation at Sinai was the logical starting point for what we now call Western civilization. Writing thousands of years later at another inflection point in human history, Alexander Hamilton wrote in The Federalist No. 31: “In disquisitions of every kind, there are certain primary truths, or first principles, upon which all subsequent reasonings must depend.” In the United States specifically, and in Western civilization more generally, it was long obvious what those “primary truths” and “first principles” actually meant: the Word of God Himself. Such a properly anchored and oriented society is uniquely suited to improve mankind’s lot and advance human flourishing.

Crucially, only such a properly anchored society can claim to comprehend the truth — let alone assert that certain truths are “self-evident,” as we recall every Independence Day. Because when God falls by the wayside, truth does as well. Recent events underscore the point.

In a Washington Post op-ed earlier this month, Gregory Conti, a politics professor at perennially top-ranked Princeton University, lamented: “Several years ago, one of my colleagues at Princeton University hosted a lecture on religion and free speech. The talk didn’t seem to be landing with the students. Finally, he realized why: The speaker had made repeated reference to the Ten Commandments, and several students didn’t know what they were.” Conti noted that Princeton students are often smart and driven, but they lack basic religious literacy — even the difference between the Old and New Testaments. In short, many of America’s future leaders do not even recognize the “primary truths” and “first principles” upon which our civilization rests.

There is a clear casualty of this ignorance: our ability to accept reality and the truth. Consider, for example, the shocking inability to do precisely that among far too many members of America’s more avowedly secularist political party, the Democrats. A whopping 42% of Democrats believe the attempted assassination of Donald Trump in Butler, Pa., in July 2024 was staged. A similarly galling 34% of Democrats believe the same about the recent attempted assassination of Trump and his Cabinet members at the White House Correspondents’ Dinner in Washington, D.C. There is, of course, zero evidence to support either belief. One might as well believe in Bigfoot, or that Neil Armstrong’s moon landing was fake.

Nor is this merely a left-leaning sociological phenomenon. There are plenty of Americans who have heterodox or perhaps even nominally right-leaning political views who have also lost touch with basic reality, allowing their brains to be rotted by mass consumption of delusional conspiracies and AI-driven online slop. We call them Candace Owens and Tucker Carlson fans.

There can be nothing good down this road. Only a society that is rooted in, and oriented toward, the eternal and the transcendental can ever hope to cultivate decent, truth-seeking citizens. When a free people loses the ability to discern between truth and fiction, rightness and wrongness, justice and injustice, there can only be only misery, despair and destruction. We’re losing that because, for far too long, we’ve been missing God. There is no better time than the run-up to America’s semiquincentennial — when we will celebrate the assertion of the self-evident truths that birthed the nation — to find Him once again. Frankly, America’s survival for another 250 years depends on it.

“..enforce the law, arrest people who commit crimes, get the crackheads off the streets, and make sure firefighters are funded and ready to do their jobs. Once upon a time, these weren’t partisan issues.

• Everything Is Awesome About This Spencer Pratt Ad (Matt Margolis)

Admittedly, I haven’t been paying much attention to the Los Angeles mayoral race, but a LEGO-animated campaign ad caught my attention, and I just had to write about it. The ad, published this week in support of Spencer Pratt’s 2026 campaign for mayor of Los Angeles, is making the rounds online, and for good reason. It’s a parody of “Everything Is Awesome” from The Lego Movie, set against a LEGO-animated cityscape that tells the dirty truth about the city under Karen Bass’s leadership. It opens with a scene that cuts straight to the truth: a man assaulting a police officer on a city street.Read more …

Everything is awful; everything is hell when you’re part of the scene. Karen Bass is awful and burning down our streets. Welcome to Los Angeles, where the criminals have more protections than the cops. Then there’s the drug crisis, which the ad renders in haunting, almost absurd LEGO detail: drug zombies shambling through city streets, needles and feces littering the sidewalks, and not a city official in sight to do anything about it. And Bass herself? The ad shows the incumbent mayor flying over her burning city — laughing.And if you know anything about Bass, you know that’s not an exaggeration for effect. It’s a pretty accurate metaphor for her tenure. While neighborhoods smoldered during the January 2026 wildfires, Bass was abroad on a “diplomatic” trip. The city she governs has deteriorating public safety, a growing homeless population, and a drug crisis that officials have been dancing around for years. The “root cause” crowd keeps hunting for some undiscovered reason people are living on the streets surrounded by needles, as if the answer isn’t staring them in the face every morning on their commute.

I don’t know much about Pratt, but he lost his own home in the Palisades Fire. He’s not running for mayor as part of a vanity campaign; he is running because he has personally experienced the consequences of Bass’s leadership. While Bass lives in a city-owned mansion insulated from the consequences of her decisions, Pratt lives in a trailer, making the case that those in charge don’t have to deal with the mess they’ve created. The second half of the ad flips the script, painting Pratt as the man who will actually do something to save the city. And the best part is that his platform isn’t complicated: enforce the law, arrest people who commit crimes, get the crackheads off the streets, and make sure firefighters are funded and ready to do their jobs. Once upon a time, these weren’t partisan issues.

This may be the song of the summer. pic.twitter.com/bxdB1eVCsy

— Adam Scheidler (@Scheidsa) May 14, 2026

You don’t need to be a Lego Movie fan to appreciate the video. Does Pratt have a chance? He might. A new Emerson College poll shows Bass at 30% support, with Pratt surging to 22% just weeks before the June 2 primary, up 12 points since March. The top two finishers advance to a November runoff, which means Pratt is very much in this race. Honestly, this is a race worth watching. Karen Bass failed her city, and if she can still get reelected, it will tell you everything about Democrat voters.

“Heavy missiles of this class are specifically designed to launch even under conditions of an incoming nuclear strike on their deployment area.”

• Sarmat: The Missile Meant To Make Any Enemy Think Twice (Kornev)

On May 12, 2026, Russia carried out the second successful launch of its newest heavy liquid-fueled intercontinental ballistic missile, the Sarmat. The launch marked another major milestone in the flight-testing program for Russia’s next-generation strategic missile system. Following the test, Russian President Vladimir Putin announced that the first regiment equipped with Sarmat ICBMs would officially enter combat duty by the end of 2026.Read more …

A ballistic missile of this class is being developed in modern Russia for the first time. The Sarmat is intended to replace the Soviet-era Voevoda missiles, which until now have remained the most powerful ICBMs ever deployed. Thanks to the immense power of its liquid-fuel rocket engines, the Sarmat is expected to carry an unprecedented payload – between 10 and 14 medium-yield thermonuclear warheads, each with an estimated yield of around 700 kilotons, or potentially up to five maneuverable hypersonic glide vehicles similar to those used in the Avangard system.Conventional ballistic warheads can be deployed together with penetration aids designed to overwhelm missile defense systems. However, maneuverable hypersonic glide vehicles present an entirely different challenge. Modern missile defense systems are effectively incapable of intercepting such weapons, making the Sarmat a uniquely formidable retaliatory strike platform. In 2022, Vladimir Degtyar, CEO of the Makeyev Design Bureau, announced that serial production of the fifth-generation RS-28 Sarmat ICBM had officially begun in Russia. “The missile system has already entered serial production and is fully supplied with the necessary materials and manufacturing equipment,” he stated.

According to Russian officials, the new ICBM will significantly strengthen the country’s strategic deterrent capability for the next 40 to 50 years. The Sarmat is believed to have a range of at least 12,000 kilometers while carrying roughly 10 tons of payload, including its post-boost vehicle and warheads. However, the missile is also reportedly capable of striking targets by approaching from the opposite direction – flying over the South Pole and effectively circling the globe. While such a trajectory would reduce the missile’s payload capacity, it would still allow for multiple nuclear warheads to reach their targets. The missile is also expected to achieve exceptional accuracy, with a probable circular error measured at no more than roughly 150 meters.

Preparations for deploying the first operational Sarmat missiles began back in 2023 at the missile division in Uzhur, located in southern Krasnoyarsk Krai. The process of replacing the aging Voevoda missiles with Sarmat systems is expected to continue for at least four to five years, if not longer. In addition to Uzhur, Sarmat missiles are also expected to be deployed near Dombarovsky in the Orenburg region.

In total, Russia is expected to field at least 50 hardened silo launchers for the Sarmat system, making it the most powerful and lethal component of the country’s nuclear retaliatory forces – a true weapon of retaliation. Heavy missiles of this class are specifically designed to launch even under conditions of an incoming nuclear strike on their deployment area. In theory, dozens of Sarmat missiles could leave their silos while under nuclear attack, carrying a combined total of roughly 500 warheads capable of devastating any potential adversary.

Over the coming years, the Sarmat is expected to complete its full flight-test program and receive multiple payload configurations. One variant will reportedly carry traditional MIRVed ballistic warheads similar to those used on the Voevoda system. Another, more advanced configuration would deploy hypersonic maneuverable glide vehicles developed by NPO Mashinostroyenia. At present, no existing missile defense system is considered capable of reliably intercepting such weapons.

What makes these glide vehicles so difficult to defeat is their flight profile. Unlike traditional ballistic warheads, they travel along a relatively low, flattened trajectory at hypersonic speeds near the edge of the atmosphere while retaining the ability to maneuver both in altitude and direction. As a result, they are detected much later than conventional reentry vehicles and are extraordinarily difficult to intercept due to their unpredictable maneuvering. The Sarmat may be able to carry more than a dozen standard warheads, but likely no more than three to five hypersonic glide vehicles. Nevertheless, such payloads would presumably be reserved for the highest-priority strategic targets – and, according to Russian military doctrine, those targets would be struck with near certainty.

RINOs trying without Trump endorsement are having a hard time.

• Trump Blasts Lauren Boebert for Campaigning with DeceptiCON Thomas Massie (CTH)

Thomas Massie is cut from the same Republican cloth as his dear friend, Ron DeSantis and his recent advocate Tucker Carlson. Like DeSantis and Carlson, Massie is a master manipulator who uses carefully crafted wedge points to divide the electorate and position himself for maximum benefit. Colorado Representative Lauren Boebert has been campaigning and trying to support Massie as the potential for him to lose a primary race is very real. This puts Boebert on the opposite side of President Trump on a very important matter of principle. Massie has accused President Trump of protecting Jeffrey Epstein’s enablers.Read more …

PRESIDENT TRUMP – “Is anyone interested in running against Weak Minded Lauren Boebert in Colorado’s Fourth Congressional District? You remember Lauren moved to the District when it became obvious that she couldn’t win in her original Congressional District (The Third!) — A Carpetbagger, indeed! Boebert is campaigning for the Worst “Republican” Congressman in the History of our Country, Thomas Massie, of the Great Commonwealth of Kentucky, and anybody who can be that dumb deserves a good Primary fight! Even though I long ago endorsed Boebert, if the right person came along, it would be my Honor to withdraw that Endorsement and endorse a good and proper alternative. Just let me know, or announce your Candidacy, and I will be there for you!” ~ President DONALD J. TRUMP

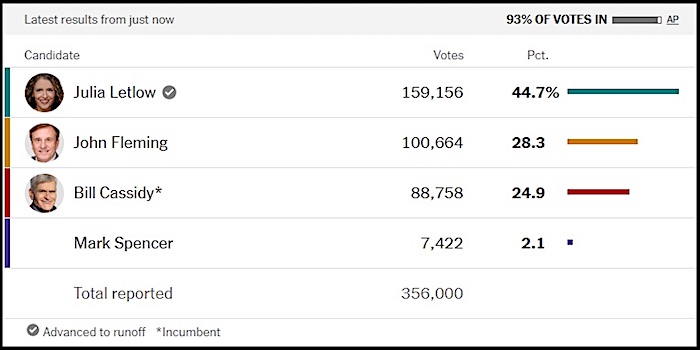

Trump-endorsed competition.

• Incumbent Senator Bill Cassidy Loses His Senate Seat in Primary (CTH)

–Unless something remarkable changes drastically, it looks like incumbent Republican Senator Bill Cassidy has come in third place, which means he has lost his Senate seat in the primary race. The runoff will be between Trump-endorsed Julia Letlow and State Treasurer John Fleming (June 27th).Read more …

Senator Bill Cassidy has lost his seat.

Changing maps seems to be Democrats’ only option.

• Supreme Court Delivers Devastating Blow to Democrats Gerrymandering (Margolis)

The Supreme Court rejected Virginia Democrats’ emergency appeal to revive their gerrymandered Virginia congressional map on Friday, delivering a final, fatal blow to their efforts in the state. The justices issued a brief order with no explanation. Still, the outcome was hardly surprising — the federal courts don’t typically wade into rulings made by state courts on state constitutional matters, and that’s exactly what happened here.Read more …

Virginia Democrats had passed new congressional maps through the General Assembly and pushed through a ballot referendum to lock those maps in. Voters narrowly approved it in April. But the Virginia Supreme Court ruled that Democrats violated the state constitution’s process for referring amendments to voters, specifically an “intervening-election requirement” that the General Assembly simply ignored. The result? Null and void. “This violation irreparably undermines the integrity of the resulting referendum vote and renders it null and void,” Justice D. Arthur Kelsey wrote in the majority opinion.https://twitter.com/EricLDaugh/status/2055421432411123879?s=20

Had the maps survived, they would have been a huge boon for the Democrats in the redistricting wars, giving the party a potential net gain of 4 seats. Democrats lost because they couldn’t be bothered to follow the rules they wrote. The attempt to appeal to the United States Supreme Court was a desperate Hail Mary bound to fail, and even Gov. Abigail Spanberger saw the writing on the wall and revealed she was no longer pushing to gerrymander the state.None of this happened in a vacuum. Democrats spent years redrawing maps in blue states, systematically eliminating Republican-held districts wherever they could. For a long time, Republicans largely played defense. That changed last year when Texas made its move, redistricting mid-decade and sparking the current national battle. California Gov. Gavin Newsom, auditioning for the 2028 Democratic presidential primaries, decided to respond by getting California to pass its own new map. Democrats tried to do the same in Virginia, but they cut constitutional corners and paid for it.

Overall, the redistricting wars have not gone well for the Democrats, and making matters worse for them, last month, the high court ruled that racial gerrymandering was unconstitutional, clearing the way for red states in the South to eliminate majority-minority districts that had long served as reliable Democratic strongholds. Democrats have now lost on multiple fronts simultaneously, and they’ve spent — I mean, wasted — millions of dollars in the process.

“The Supreme Court of the United States has affirmed what we always knew: you cannot violate the Constitution to change the Constitution..”

• Supreme Court Rejects Attempt To Revive Virginia Congressional Map (ZH)

Hammering the last nail in the coffin of what could have been a significant midterm factor, the US Supreme Court on Friday rejected Virginia Democrats’ request to use a new congressional district map, which was drawn to flip four House seats into Democratic control. As is typical in this kind of “emergency” ruling, the court provided no legal rationale or vote count — however no dissents were noted. The new map was expected to dramatically alter the composition of Virginia’s US House delegation, boosting Democrats from their current slim 6-5 edge to 10-1 domination. For context, in 2024 presidential balloting, Virginia voters were split 52% for Democrat Kamala Harris and 46% for Donald Trump.Read more …

On May 8, the Virginia Supreme Court denied a request from Democrats and state officials to lift a lower-court order blocking certification of the April 21 redistricting referendum. Voters approved the Democrat-accommodating map by a 52-to-48 margin, but a Virginia circuit court declared the referendum null and void, saying Democrats had run afoul of state constitutional measures that exist to fend off partisan gerrymandering. After that setback, Democrats sought to salvage their new map with an appeal to the US Supreme Court, which has now failed. Two days earlier, Gov Abigail Spanberger had already waved a white flag of sorts, implying that Virginia’s May 12 deadline for map changes made the emergency request to the US Supreme Court something of a moot point.“What needs to happen is we need to focus on the task at hand, which is winning races in November,” she said. “I believe, somewhat doggedly, that we will [gain] two to four seats in the House of Representatives. … That is my goal. That is what I know is possible.” However, after the ruling, she opportunistically lashed out at the Supreme Court: Virginia Gov. Abigail Spanberger, a Democrat, criticized the decision, which she said had the effect of nullifying “the votes of more than three million Virginians.” “As Governor, I will make sure voters know when and how to cast their votes this year. Because our votes are how we choose the representation we deserve,” she wrote on X.

The Supreme Court of the United States has now joined the Supreme Court of Virginia in choosing to nullify an election and the votes of more than three million Virginians.

— Governor Abigail Spanberger (@GovernorVA) May 16, 2026

These Virginians made their voices heard — casting their ballots in good faith to push back against a…

The lead respondent, Virginia state Sen. Ryan McDougle, a Republican, who is also legislative commissioner for the Virginia Redistricting Commission hailed the new ruling. “The Supreme Court of the United States has affirmed what we always knew: you cannot violate the Constitution to change the Constitution,” the state lawmaker wrote on X.The Virginia battle was part of a nationwide saga that started last year, when Texas Republicans redrew their congressional map to gain seats, straying from what had been a fairly (but not thoroughly) universal norm that saw states refrain from redistricting that wasn’t driven by once-a-decade census results. Following the lead of California Democrats who undertook their own maneuvers to offset the Texas map, the Virginia leftists who gained full control of state government in 2025 responded with a constitutional amendment allowing the General Assembly to temporarily redraw congressional districts outside the normal 10-year cycle — specifically to “restore fairness” if other states gerrymandered (bases on the convoluted implication that varied wrongs against the citizenry of multiple states can add up to a national right).

Despite the implosion of the Virginia Democrats’ scheme, and the view that the net result of the redistricting war will flip seats to the GOP column, prediction-market participants lean heavily toward Democrats wresting control of the House from Republicans, who currently have a 217-212 edge over the Democrats. (One representative is an independent and there are five vacant seats owing to deaths and resignations.)

It was mostly a Dem game in the past.

• Republican Lead In Redistricting Race is About To Get Bigger (Ben Whedon)

The Supreme Court’s decision in Louisiana v. Callais saw the justices narrow Section 2 of the Voting Rights Act and disallow race-based congressional districts. With the dust on redistricting mostly settled, Republicans appear poised for a double-digit swing of House seats in their favor in the 2026 midterms, at least if all goes according to plan. The Supreme Court’s decision in Louisiana v. Callais saw the justices narrow Section 2 of the Voting Rights Act and disallow race-based congressional districts. The move triggered map redraws across the South and is expected to result in more than a dozen seats moving toward the GOP, at least in time for 2028.Read more …

Democratic countermeasures, meanwhile, have hit a judicial brick wall, with the Virginia Supreme Court striking down that state’s ambitious redraw, saving four Republican seats. The U.S. Supreme Court refused Friday to intervene, leaving Democrats out of legal options. The collective shifts are poised to move the needle rightward and put the House in play for November, potentially handing the White House an opportunity to defy historical trends and retain control of Congress. Here’s a look at where the midterm situation stands:

Louisiana

The state’s maps have been the subject of legal scrutiny for years, leading to a challenge that culminated in the recent Supreme Court decision. Gov. Jeff Landry, R-La., has suspended elections in the meantime to allow the legislature to implement a new slate. The state Senate passed a redraw earlier this week with five Republican-leaning districts and one Democratic-leaning seat, though the House has yet to approve it.South Carolina

Several Republican state senators joined with Democrats to vote down a redistricting plan that would have eliminated the state’s sole Democratic-leaning congressional district, which longtime Rep. Jim Clyburn represents. The measure needed a two-thirds majority to pass. GOP Gov. Henry McMaster subsequently called a special session of the legislature to reconsider the matter. At most, the state lawmakers could add a single Republican-leaning district to the state’s delegation. South Carolina now sends six Republicans and one Democrat to the lower chamber.Alabama

Lawmakers appear poised to approve a slate of House maps that would eliminate one of the state’s two Democratic-leaning districts. GOP Gov. Kay Ivey called the legislature into special session for the redraw, despite initially indicating that she would not do so. The proposed redraw stopped shy of the clean Republican sweep that activists sought, though a later redraw could result in that outcome. Though Republicans have yet to fully approve the new slate, Ivey has also called special primaries for the districts she expects will be affected.Mississippi

GOP Gov. Tate Reeves appeared this week to pour cold water on the prospect of the state redrawing its maps in time for the 2026 midterms, saying repeatedly that he expected the legislature to redraw the maps sometime “between now and 2027.” Prior to the Supreme Court ruling in Callais, he had called a special session of the legislature to consider redistricting, but he canceled it this week. Mississippi currently has three Republicans in Congress and one Democrat. Rep. Bennie Thompson, D-Miss., currently represents a district that includes much of the Mississippi River delta and a large portion of the state’s black population.Georgia

Gov. Brian Kemp has called a special session of the legislature, though he expects the state will only change its maps in time for 2028 and therefore not impact control of the GOP-controlled House in November. Georgia boasts 14 House seats, five of which are under Democratic control. Depending on the redraw, the state could likely see a swing of two seats toward the GOP in the long term.Tennessee

State lawmakers successfully passed a new set of maps this month that eliminated the last Democratic-leaning district, which was centered on Memphis. Democratic Rep. Steve Cohen on Friday announced an end to his reelection campaign, citing the redraw and the changes to his district.Texas

The Texas redraw ostensibly kicked off the redistricting fight and represented the single-largest gain for Republicans, with as many as five seats shifting toward the GOP as a result. With the court challenges to the new map largely settled, the GOP is expected to make those gains in the Lone Star state in November.Florida

Florida passed a redrawn House map within days of the Callais ruling, shifting its 20-GOP and eight-Democrat-seat lineup to 24 GOP and four Democrats. The state has skewed heavily toward Republicans since President Donald Trump first won the battleground in 2016. It is now regarded as a reliably Red state.Missouri

The state Supreme Court this month permitted Missouri to use its maps, which include seven Republican districts and one Democratic seat. State lawmakers managed to eliminate a second Democratic seat with the redraw.North Carolina

North Carolina lawmakers approved a revised set of maps in late 2025 that netted Republicans one seat in their delegation. Democrat Gov. Josh Stein did not have the authority to veto the legislation. In the 1990s, Republicans struck a deal with Democrats that exempted redistricting from the governor’s authority, Politico reported.Ohio

In October 2025, the state’s redistricting commission approved a redraw in which Republicans gain an edge in 12 districts, while Democrats led in three. Republicans now have 10 seats and are expected to gain up to two in 2026 as a result of the redraw, according to the Ohio Capital Journal.Virginia

The state Supreme Court struck down a redistricting referendum that would have seen the state shift from six Democrats and five Republicans, to 10 Democrats and one Republican. The court found that the process for advancing the referendum violated the state constitution, without ruling on the maps themselves. Though Democrats appealed to the U.S. Supreme Court, opponents of the redraw were confident the Supreme Court would not take the case. Speaking on the “Just the News, No Noise” television show this week, former GOP Virginia Attorney General Ken Cuccinelli opined that the justices would speedily knock it down.“I think the chief justice has really just asked for briefs as a courtesy. This is going nowhere,” he said. “They have no jurisdiction. And I don’t think you will even see. I don’t think you will literally get a word out of a single justice. I think it will just be summarily rejected with no comment or anything else.”He was proven right on Friday evening, when the Supreme Court declined to hear the matter.

Utah

Utah’s maps became the subject of legal scrutiny at the state level, resulting in a court order that created a Democratic-leaning district in the otherwise, reliably Republican state. Though state lawmakers have explored revisions, including a statewide referendum, to their own laws to allow for eliminating the new district, it is likely that Democrats will secure a pickup in November.California

State Democrats reacted furiously to Texas’s redraw and organized a statewide referendum to change their congressional maps with the aim of countering Texas. The referendum was successful and Democrats are expected to gain a total of five seats from redistricting, representing their single largest gain this cycle.The bottom line

Republicans have already approved maps accounting for a gain of 14 seats over the 2024 maps. And three states in the South may each add one in the near future. With Democrats gaining six from California and Utah, the GOP appears poised for a net swing of at least eight but as high as 11, which could prove decisive to holding the House.

https://twitter.com/Real_RobN/status/2055337924527624296?s=20 https://twitter.com/JoshHall2024/status/2055428011638575195?s=20

SNOWDEN SET TO CRUSH COMEY, CLAPPER & BRENNAN! Trump Delivers FULL Pardon & Hero’s Welcome

— QThestorm (@17QStorm) May 15, 2026

Breaking from Washington — Edward Snowden is coming home as a HERO!

Under President Trump’s leadership, the legendary NSA whistleblower is finalizing a game-changing clemency deal.… pic.twitter.com/Avsr1Y7wDF

BREAKING: Our autopsy study, which found that 100% of published myocarditis deaths following COVID-19 vaccination were CAUSED BY THE VACCINE, just WON Wiley’s Top-Viewed Article Award.

— Nicolas Hulscher, MPH (@NicHulscher) May 15, 2026

An IMMEDIATE FDA Class I Recall of mRNA injections is REQUIRED. https://t.co/wQj5oZ5Ah6 pic.twitter.com/4YwLvPTMm4

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.