Jean-Léon Gérôme Slave market 1866

Here’s the story in a nutshell: Ultra low interest rates mark a shift away from people’s wealth residing in their savings and pension plans, and into to so-called wealth residing in their homes, which are bought with ever growing levels of debt. When interest rates rise, they will lose that so-called wealth.

It is grand theft auto on an unparalleled scale, and it’s a piece of genius, because while people are getting robbed in plain daylight, they actually think they’re winning. But as I wrote back in March of this year, home sales, and bubbles, are the only thing that keeps our economies humming.

We haven’t learned a thing since March, and we haven’t learned a thing for many years. People need a place to live, and they fall for the scheme hook line and sinker. Which in a way is a good thing because the economy would have been dead without that ignorance, but at the same time it’s not because it’s a temporary relief only and the end result will be all the more painful for it.

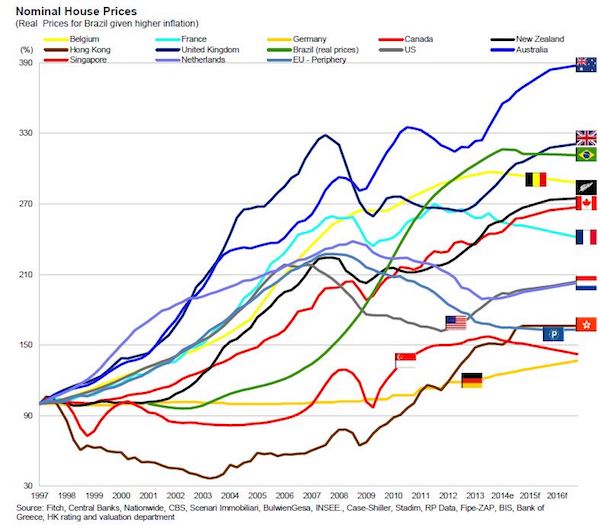

Whatever Yellen decides as per rates, or Draghi, it doesn’t really matter anymore, this sucker’s going down something awful. This is a global issue. Housing bubbles have been blown not only in the Anglosphere, though they are strong there, many other countries have them as well, Scandinavia, Netherlands, even Germany and France. It’s what ultra low rates do.

First, here’s what I said in March:

Our Economies Run On Housing Bubbles

What we have invented to keep big banks afloat for a while longer is ultra low interest rates, NIRP, ZIRP etc. They create the illusion of not only growth, but also of wealth. They make people think a home they couldn’t have dreamt of buying not long ago now fits in their ‘budget’. That is how we get them to sign up for ever bigger mortgages. And those in turn keep our banks from falling over.

Record low interest rates have become the only way that private banks can create new money, and stay alive (because at higher rates hardly anybody can afford a mortgage). It’s of course not just the banks that are kept alive, it’s the entire economy. Without the ZIRP rates, the mortgages they lure people into, and the housing bubbles this creates, the amount of money circulating in our economies would shrink so much and so fast the whole shebang would fall to bits.

That’s right: the survival of our economies today depends one on one on the existence of housing bubbles. No bubble means no money creation means no functioning economy.

What we should do in the short term is lower private debt levels (drastically, jubilee style), and temporarily raise public debt to encourage economic activity, aim for more and better jobs. But we’re doing the exact opposite: austerity measures are geared towards lowering public debt, while they cut the consumer spending power that makes up 60-70% of our economies. Meanwhile, housing bubbles raise private debt through the -grossly overpriced- roof.

This is today’s general economic dynamic. It’s exclusively controlled by the price of debt. However, as low interest rates make the price of debt look very low, the real price (there always is one, it’s just like thermodynamics) is paid beyond interest rates, beyond the financial markets even, it’s paid on Main Street, in the real economy. Where the quality of jobs, if not the quantity, has fallen dramatically, and people can only survive by descending ever deeper into ever more debt.

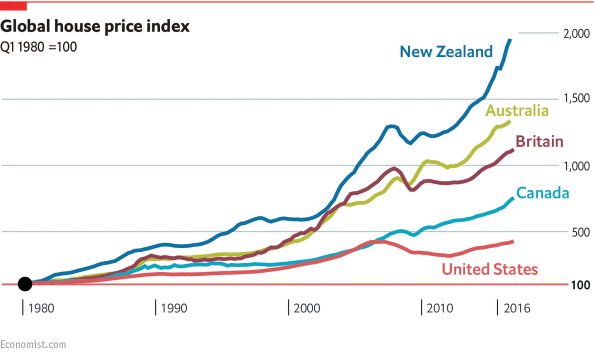

Australia’s housing boom has been a thing of beauty, with New Zealand, especially Wellington and Auckland, following close behind. UBS now says the Oz bubble is over. Prices are still rising quite a bit though.

Fresh New Zealand PM Jacinda Ardern has announced new policies to deter foreign buyers from purchasing more property in the country. She may not like what that does to the country’s economy. Most new Zealanders can no longer afford property in major centers, and forcing prices down this way will expose many present owners to margin calls and foreclosures.

Moreover, because Australian banks own their New Zealand peers, if the Aussie boom is really gone, these banks are going to get hit so hard they’ll take down New Zealand with them. Close your eyes and put your fingers in your ears.

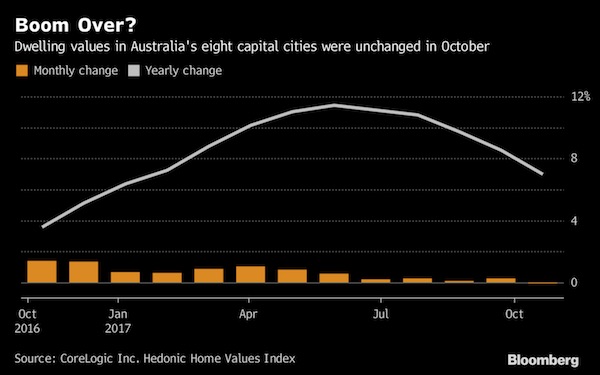

Australia’s Housing Boom Is ‘Officially Over’

The housing boom that has seen Australian home prices more than double since the turn of the century is “officially over,” after data showed prices now flatlining, UBS said. National house prices were unchanged in October from September, while annual growth has slowed to 7% from more than 10% as recently as July, CoreLogic data released Wednesday showed. “There is now a persistent and sharp slowdown unfolding,” UBS economists led by George Tharenou said in a report. “This suggests a tightening of financial conditions is unfolding, which we expect to weigh on consumption growth via a fading household-wealth effect.”

An end to Australia’s property boom will be welcome news for first-time buyers, who have struggled to break into the market after surging prices propelled Sydney past London and New York to be the second-most expensive housing market. Less impressed may be property investors, already squeezed by regulatory lending curbs that drove up mortgage rates. The cooling housing market may encourage the Reserve Bank to keep interest rates at a record low. A rate hike would be undesirable as it would put further downward pressure on dwelling prices, said Diana Mousina, senior economist at AMP Capital Investors.

But perhaps a bigger, and more surprising, story is shaping up in the US. Looks like the American housing bubble is back with a vengeance. It’s always amusing to see claims that this is due to a lack of supply. The real problem is not supply, but artificially fabricated demand. Fabricated by low rates. Though the NAR is not known for its accuracy (it’s a PR firm), this Bloomberg piece is still relevant.

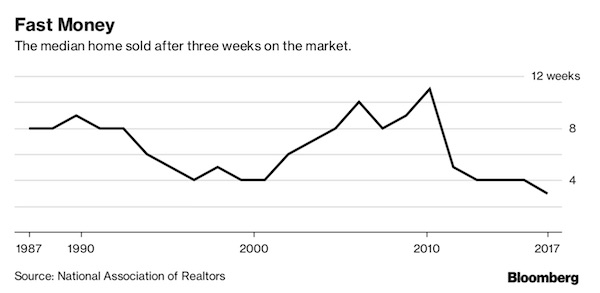

Homes Are Getting Snapped Up at the Fastest Pace in 30 Years

Homes are sitting on the market for the shortest time in 30 years, according to an annual report on homebuyers and sellers published today by the National Association of Realtors. The typical home spent just three weeks on the market, according to the report, which focused on about 8,000 homebuyers who purchased their home in the year ending in June. That was down from four weeks in the year ending June 2016 and 11 weeks in 2012, when the U.S. housing market was still reeling from the foreclosure crisis.

It was the shortest time since the NAR report began including data on how long homes spend on the market, in 1987. Buyers are snapping up homes quickly at a time when for-sale listings are in short supply, forcing them to compete. The number of available properties declined in September, according to NAR’s monthly report on existing home sales, marking the 28th consecutive month of year-on-year decline in inventory. In addition to moving fast, buyers also had to pony up to close the deal. 42% of buyers paid at least the listing price, the highest share since the NAR survey started keeping track in 2007.

Where the fine bubble plan runs astray is in affordability. Ultra low rates can encourage sales, but that also raises prices, and if and when wages do not keep up there must be a point where you hit a wall. In the US that wall is fast approaching, suggests Tyler Durden:

US Homes Have Never Been More Unaffordable

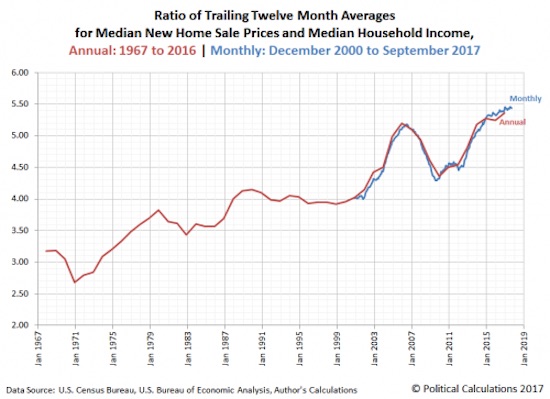

Just under a year ago, US home prices finally surpassed their prior all time highs, one decade after the 2006 bubble… and haven’t looked back since. Which, all else equal, would be great news for America, where the bulk of middle-class wealth is not in the stock market contrary to conventional wisdom, but in its biggest, and most illiquid asset-cum-investment: one’s home. There is just one problem: while house prices are once again hitting new all time highs every month, household incomes have failed to keep up; in fact, as the Political Calculations blog shows, in the past two years there has been a distinct trend in home affordability, or lack thereof.

[..] starting in September 2015, the TTM average median new home sale price in the U.S. has been rising at an average rate of $906 per month. That’s the good news; the bad news is that in terms of affordability, the ratio of the trailing twelve month averages of median new home sale prices to median household income in the U.S. has risen to an all time high of 5.454, which following revisions in the data for new home sale prices, was recorded in July 2017. The initial value for September 2017 is 5.437. In other words, the median new home in the US has never been more unaffordable in terms of current income.

Never more unaffordable is a bold statement, but it’s probably correct. The graph only goes back as far as 1987, but that should do. Another angle on the same issue, also from Tyler:

Home Prices In All US Cities Grow Faster Than Wages… And Then There’s Seattle

US national home prices are up 6.07% YoY in August – the fastest rate since June 2014. We note this data is for August – before the hurricanes. Seattle (up 13.2%), Las Vegas (up 8.6%), and San Diego (up 7.8%) were the top three cities in terms of year-over-year price appreciation; all cities showed gains of at least 3%. Pushing home prices to a new record high…

“Home-price increases appear to be unstoppable,” David Blitzer, chairman of the S&P index committee, said in a statement. “At the same time, “measures of affordability are beginning to slide, indicating that the pool of buyers is shrinking, and the Fed’s interest-rate hikes are likely to push mortgage rates higher over time, “removing a key factor supporting rising home prices,” he said.

There’s nothing anyone can do to raise wages, and while Yellen may claim not to understand why wages and inflation refuse to shine, it’s not that hard. Whatever is called a job these days is America didn’t use to be labeled that. We’ve all been conned into redefining what a job is, but the benefits and security and all that have still vanished. So what can people afford? They can’t even afford to rent anymore:

Renting In The US Has Never Been More Unaffordable

Over the weekend, when looking at the record high ratio in median new home sale prices to household incomes in the US, we concluded that US homes have never been more unaffordable for the average American. What about renting? Isn’t it intuitive that if buying a house has never been more expensive, then at least renting should be cheap(er). Unfortunately no, because not only is renting not cheap(er) in either absolute or relative terms, but when observed through the prism of the only thing that matters, namely disposable income, renting – just like buying a house – has never been more unaffordable.

Now remember what I said before: millions upon millions see their savings and pensions melt away before their eyes, while at the same time they are forced to spend ever more on housing costs. And when that scheme hits the wall, the economy will remember it’s alive only because of the housing bubble, and then croak. Leaving both renters and owners without jobs and eventually places to live.

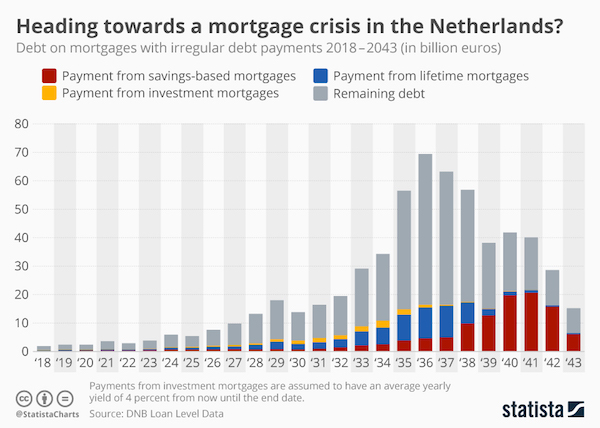

A lovely example of where all this is heading comes from a Statista report on the Netherlands 3 weeks ago. The Dutch have tons of interest-only mortgages, just like the Australians, but you can take this graph as a general model for what many of not most countries that have low interest rates and thus housing bubbles, will face:

Heading Towards A Mortgage Crisis In The Netherlands?

Bank it or bust. In October 2017, the Dutch Central Bank (DNB) issued a warning on mortgages in the Netherlands. They claimed that almost 55% of the aggregate Dutch mortgage debt consisted of interest-only and investment-based mortgage loans, which did not involve any contractual repayments during the loan term. As prices in the the European housing, or residential real estate, market increase and mortgage rates decrease due the Asset Purchase Programme (APP) of the ECB, interest-only mortgages became more and more popular.

In addition, the Dutch government encouraged home ownership for many years, offering tax exemptions on Dutch mortgage payments alongside other benefits for homebuyers in the Netherlands. Consequently, the total mortgage debt from households in the Netherlands increased from approximately €548 billion in 2006 to approximately €664 billion in 2016. However, the debts must still be repaid when the interest-only mortgages expire.

The DNB stated there could be a risk that the households in question may not have the means to repay their debts before or when their loans expire, risking a new mortgage crisis. Lenders, they say, must actively alert customers to this risk and help them find a suitable solution. Unfortunately, the value of mortgages in 2017 is forecasted to increase with approximately 3.9% compared to 2016.

The debt accumulation is insane. Combine that with the wholesale erosion of savings and pensions, and you have an economy with either a lot of foreclosures and homelessness in its future, or a bankrupt banking system. More people should, before purchasing property, be shown graphs like that. But that would kill the bubble scheme, wouldn’t it?

Is there a way out of this mess? Well, there is in theory. Just grow your economy, and your wages etc., by let’s say 6.8% per year for decades on end. Problem with that is it’s possible only in a country like China, and that only because whatever Beijing says the growth rate is, goes. But that doesn’t make it real. Still, it entices Chinese grandmas into buying apartments.

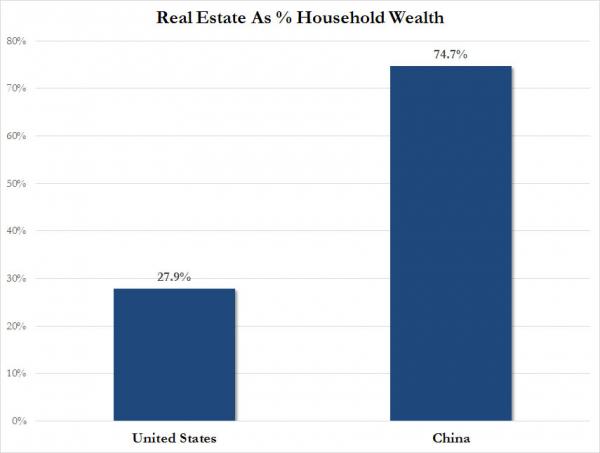

What Beijing doesn’t tell them, or us, is how much debt the grandmas have gone into by now to buy all those new nice and shiny apartments. But since stocks and bonds are still not their thing, it’s all they have. Property in China is all on red. In the US about one quarter of household wealth is in housing, in China it’s three quarters.

So no, there’s no way out. My best guess is the first country to deal with this in an aggressive manner will be the -relative- winner. All others are goners. The governments and politicians who’ve lured their people into this biggest Ponzi in human history will probably be long gone when the house comes down, and if they know what’s good for them will have moved to some street with no name in a land far away.

Home › Forums › The Biggest Ponzi in Human History