Fred Stein Snow White 1946

These people are so stuck in their narrow field and views. Build more! is not an answer to any of this. Homes are grossly overpriced, and they will be ‘re-priced’.

• Who Will Buy Baby Boomers’ Homes? (CityLab)

Frequent sales put pressure on the market to produce homes catering to changing tastes among buyers. Nelson notes that the home building industry is now producing less than half the number of new houses it did in the mid-2000s. Though demand now outpaces supply, homeowners are hanging on to properties significantly longer—nine to ten years—because they owe more on their houses than they can get for them, their houses are worth less than before the recession, or they can’t find a home that meets their needs due to insufficient supply. “It’s not that Boomers are going to ‘age in place,’” says Nelson. “They’re going to be stuck in place, and they’re going to make the best of it.” Those who can afford it will remodel. Regardless of when it occurs, the great senior sell-off won’t affect every Boomer equally.

A large chunk of Millennials—Nelson posits around two-thirds—will want to buy suburban homes because they like the lifestyle, or because they will be priced out of cities like Washington, D.C. or Los Angeles, where housing costs are exorbitant. Most of the other third, he says, will want to live in central cities and the oldest, closest suburbs—though not necessarily downtown. The small percentage who prefer downtown living but cannot afford certain cities may move to more affordable ones, such as Philadelphia or Minneapolis. Nelson predicts that the fringe areas surrounding cities will bring the biggest headaches for Boomers looking to unload their houses. Because Millennials will be looking for small homes when they finally start to buy in larger numbers, the sprawling McMansions of the exurbs won’t be desirable to many of them.

“The Boomers in the exurbs are going to be in a real pickle,” says Nelson. “Even in a dynamic market like Washington, D.C. or other booming cities, the market for those homes is going to be soft.” Though Jennifer Molinsky, a senior research associate at Harvard’s Joint Center for Housing Studies, agrees that exurbs and rural areas will likely be vulnerable to the Boomer/Millennial housing mismatch, she’s not as pessimistic about the sell-off as a whole. “The Baby Boomers are a large generation,” she says. “Nothing they do is going to happen en masse.” She also believes that the Boomers who don’t age in place will demand an increasing array of housing options that will help spread out sales over time, decreasing the likelihood of a sudden glut of housing.

But many analysts do agree on one thing: More housing will need to be built for Millennials—and it needs to be scaled to their desires, not their parents’s. “Millennials are likely to prioritize different features in their homes, such as greener materials or in-law suites,” says Molinsky. And according to the Harvard Joint Center’s projections, nearly 90% of those looking for homes in 2035 will be under 35 or 70 and over—and both groups tend to buy less square footage. The challenge for local governments and developers, says Nelson, “is to anticipate these future needs and build different and smaller homes now—before getting trapped with too many larger homes later.”

Read more …

“In British Columbia, real estate and related fields such as construction and finance make up an astounding 40% of GDP..”

• Canada Completely Lost Its Mind Over Real Estate (McL)

The average selling price for all homes in the Greater Toronto Area, including houses and condos, surged to $916,567 in March, a 33% rise from the year before, according to the Toronto Real Estate Board. Since January alone, prices are up 19%. A lowly semi-detached house in the city is now worth more than $1 million. Prices are growing even faster in the surrounding suburbs. More first-time homebuyers and investors are looking to Barrie, Ont., a city about 100 km north of Toronto, where the average selling price jumped 33% compared to the year before.

[..] Canada is a country deeply reliant on real estate. The industry accounts for roughly 12% of its GDP. In British Columbia, real estate and related fields such as construction and finance make up an astounding 40% of GDP. Vancouver is seeing prices rise again after numerous efforts to cool the market. And in Alberta, not even a recession and a 9% unemployment rate did much damage to house prices in Calgary and Edmonton. “It’s surprising how well it has held up, given the severity of two years of contraction,” says Todd Hirsch, chief economist at ATB Financial.

[..] “Tight supply starts to become a justification for all outcomes,” says Beata Caranci, chief economist at TD Bank Group. If buyers are convinced supply is low, then the big price increases will seem logical, exacerbating their fear of missing out and pushing them to act irrationally. Toronto’s price surge did indeed coincide with a significant drop in listings, but that could be a result of psychology on the seller’s part. Some homeowners could be holding on to their properties in anticipation of prices rising even further. Families that would otherwise sell their homes to upsize could also be staying put simply because prices are so high, and competition is so fierce, that the hassle isn’t worth it. An influx of deep-pocketed foreign investors could also be taking properties off the market, especially since Vancouver implemented a 15% tax last year for foreign nationals. “I do believe that at least some investors went directly from Vancouver to Toronto,” Porter says. “That has played a role in launching Toronto, and some surrounding cities, into the stratosphere.”

Read more …

Way too late: “…the Bank of Canada needs to pay more attention to the housing issue because it is a huge threat to the entire economy.”

• The Bank of Canada Should ‘Cease and Desist’ (Mises)

“Beneath the symbol We’ll all assemble Oh how we’ll fly Oh how we’ll tremble”

– Captain Beefheart, “Ice Cream for Crow”

If interest rates are the symbol beneath which we all assemble, then there are some bad times ahead. But Canada’s “leading economists,” say interest rates are “too blunt a tool” to cool the housing market.This week, Governor Stephen Poloz as expected did not raise rates, but continues to face tough questions about the connection between low rates and the “hot” housing market. Of course, he deserves every hard question thrown at him. And it’s nice that journalists are actually starting to question the obvious connection between low-interest rates and the housing bubble. With Canadians across the country locked out of their local housing markets, and with foreign buyers using Canadian property to protect their wealth from destructive communist dictatorships, frustration needs an outlet and it looks as if Poloz and the BoC are, finally, in the crosshairs.

But that doesn’t mean Poloz will listen. After all, the central bank is supposed to remain “independent” from democratic government and popular opinion. Poloz is making his decisions based on his misunderstanding of the economy, not the will of the mob. As Avery Shenfeld, CIBC Capital Markets’ chief economist, told BNN in an email, “The Bank of Canada will likely stick to its view that house prices are best dealt with through macro-prudential policies particular to that market, with the interest rate setting used to steer the economy overall.” Meaning, let the banks and federal government deal with the issue. The BoC will do what it can, but it will not include raising rates. Raising interest rates will certainly “cool” the housing market, but it will also lead to some unintended consequences that would “hurt” the overall economy.

Remember, the BoC is stacked with Keynesians, who regard the “hangover theory” as implausible as the irrefutable Say’s Law. So if the Bank can’t or won’t raise rates, and leaving the price of interest to the free market isn’t even on the table, then what about a rate cut? Doug Porter, chief economist at BMO Capital Markets, also told BNN, “The BoC should cease and desist with talk of possible further rate cuts, which simply fuel the sense that rates are never going higher, and instead start warning that rates will someday rise.” That would be smart, we’ll have to see what tomorrow brings. So far, Bank of Canada governor Stephen Poloz has left real estate to the experts, meaning, not him. Capital Economics Senior Canada Economist David Madani told BNN that the “Bank of Canada needs to pay more attention to the housing issue because it is a huge threat to the entire economy.” But Poloz, like his predecessor before him, prefers “moral suasion.” Madani thinks the Bank should be using “much stronger language.”

Oh, how we’ll fly, oh how we’ll tremble.

Read more …

“67% of the US economy is dependent upon Americans spending money they don’t have on shit they don’t need.”

• Will Trump Accept Responsibility When This Shitshow Implodes? (Quinn)

Donald J. Trump has taken credit for making America’s economy great again. He’s been crowing about all the jobs being created, the soaring consumer confidence and record highs in the stock market. It’s all because the Donald has inspired Americans about our glorious future. But, a funny thing has been happening in the real world. The economy has gone into the shitter and GDP will be lucky to reach 1% in the first quarter of his presidency.

The bullshit consumer confidence surveys mean absolutely nothing. Feelings don’t mean shit.

What consumers do is what matters.

67% of the US economy is dependent upon Americans spending money they don’t have on shit they don’t need.

And they’ve dramatically reduced that spending. If consumers are so confident, why are a record number of major retailers going bankrupt and closing 3,500 stores in 2017? Mom and pop retailers have been shuttering for years.

If the narrative about a dramatically improving housing market was true, why would furniture store sales and building material store sales be falling?

Read more …

That’s a NO. Steve’s new book is out and available on Amazon. Valentin Schmid feels the need to insert his own opinion and veers way out of his depth by questioning Minsky’s instability theory.

• Can We Avoid Another Financial Crisis? (ET)

Keen answers the $1 trillion dollar question with a resounding “no.” This is because too many countries rode a wave of private debt explosion during the last boom, and are now in the equivalent of economic purgatory. Keen identifies China as the biggest threat. “They face the junkie’s dilemma, a choice between going ‘Cold Turkey’ now, or continue to shoot up (on credit) and experience a bigger bust later. China is undoubtedly the biggest country facing the debt junkie’s dilemma now. But it doesn’t lack for company,” he writes. Other countries with a high level of private debt and a reliance on debt to fuel economic demand -Keen calls them “debt zombies”- are Australia, Belgium, Canada, South Korea, Norway, and Sweden.

In total, the influence of China and these smaller economies is simply too great for the world to avoid a financial crisis. According to Keen, the solution within this layer of economic theory is more government regulation of the banking system and government deficits to counter a fall in private demand – which is essentially the policy response to the 2008 financial crisis. More aggressive options are quantitative easing in the form of ‘helicopter money’, where the central bank monetizes government debt, and the government then writes a check to households to either pay down debt or spend it in case there isn’t any debt to pay down. There could also be a more official debt jubilee where debt is simply forgiven.

“On its own, a Modern Debt Jubilee would not be enough: all it would do is reset the clock to allow another speculative debt bubble to take off. Currently, private money creation is a by product of the activities of a casino (Keynes, 1936, p. 159), rather than what it primarily should be: the consequence of the funding of corporate investment and entrepreneurial activity,” writes Keen. The ultimate objective would be for the government to counter excessive private debt bonanzas. Being an agnostic thinker, Keen also entertains concepts of government issued money and cryptocurrencies, although he doesn’t think they can eventually replace the banking system, partly because of scale, partly because of political resistance. “As long as that model holds sway over politicians and the general public, sensible reforms will face an uphill battle—even without the resistance of the finance sector to the proposals, which of course will be enormous.”

Read more …

China strangles itself to save its economy.

• China Finally Halts Outflows. Now What? (Balding)

Is China finally making headway in its battle against currency outflows? On the surface, yes: People’s Bank of China foreign exchange reserves are effectively unchanged since December at $3 trillion, and data for February released by the State Administration of Foreign Exchange showed a significant narrowing of net outflows of capital based on international bank settlements and sales. That’s a major accomplishment, given that yuan had been leaving the country at an average rate of almost $60 billion per month in the middle of last year. But how this turnaround was achieved raises some serious long-term questions for China. For one thing, it wasn’t driven by economic strength. Officially recorded payments and receipts are both down significantly across all categories.

Total foreign bank inflows are flat, while payments abroad were down by 15% through the first two months of the year. With total outflow payments from banks of $3.1 trillion in 2016, a 15% drop represents a large decline in absolute terms. In other words, balance wasn’t achieved by increasing exports or investment into China, but rather by preventing Chinese from buying from and investing in the rest of the world. Some of the government’s restrictions on currency-exchange transactions – such as cracking down on fake trade data and overpayments for imports – were justified and sensible. But others were more dubious and have led to significant distortions. Most banks, for instance, now can only pay for international transactions if they’ve balanced their books with a corresponding level of inflows.

Beijing-based banks are under particular pressure, required to bring in 100 yuan for every 80 they use to pay for overseas transactions. Unsurprisingly, given these regulations, official bank payments and receipts are now almost perfectly balanced. But accomplishing this has required major declines in foreign investment as well as triple-checking what used to be routine transactions of virtually any size. Foreign firms don’t have it much easier. Although China still officially permits foreign companies to move capital for standard operating transactions, such as dividend payments, more than a few firms have complained about not getting permission to do even that.

The risk is that foreign investment in China, which has declined, will fall even further if investors worry about not being able to bring profits back home. Similarly, stepped-up capital controls on Chinese looking to move cash abroad has increased the attractiveness of gray-market money changers in Hong Kong, who have little difficulty finding firms in China hoping to move large sums. Although their volumes have dropped somewhat, the money changers still do a thriving business selling U.S. dollars at a typical discount of 2% to 5% from the official rate.

Read more …

Where’s John McCain when you need him?

• Russia Could Soon Take Over A Chunk Of US Oil Infrastructure (Vice)

Russia may soon take control of American oil and gasoline infrastructure in a deal U.S. lawmakers warn represents a threat to energy security. Rosneft, Russia’s state-controlled oil company, could end up with a majority stake in Texas-based Citgo after the entity that owns Citgo, Venezuela’s state-owned oil and natural gas company PDVSA, used almost half of Citgo’s shares as collateral for a loan from Rosneft. In the midst of Venezuela’s ongoing economic crisis, PDVSA is reportedly in danger of defaulting on that loan. That means Rosneft, a company specifically named in U.S. sanctions levied against Russia after its 2014 annexation of Crimea, is poised to become one of the biggest foreign owners of American oil refining capacity. Rosneft is headed by Igor Sechin, a powerful crony of Russian President Vladimir Putin, and is often seen as a proxy for the Kremlin’s energy policies.

PDVSA put up as collateral about 49.9% of Citgo shares in exchange for a $1.5 billion loan from Rosneft in December. It had used the other half of Citgo as collateral for a bond deal two months before that. Should PDVSA default on its Russian loan, the Russians could relatively easily end up with a majority stake in Citgo by acquiring more PDVSA bonds on the open market. While the exact details and time-frame of the Rosneft loan remain murky, PDVSA successfully made $2.2 billion in payments on notes that matured April 12, sending ripples of relief through financial markets. Still, the possibility of default has set off alarm bells in Congress, where Republican and Democratic members of the House and Senate told Treasury Secretary Steven Mnuchin they see Russia’s potential acquisition of Citgo as a threat to the country.

“We are extremely concerned that Rosneft’s control of a major U.S. energy supplier could pose a grave threat to American energy security, impact the flow and price of gasoline for American consumers, and expose critical U.S. infrastructure to security threats,” six senators wrote in a letter to Mnuchin dated April 10. Those senators include Democrat Robert Menendez of New Jersey and Republicans Marco Rubio of Florida and Ted Cruz of Texas. [..] Citgo owns three large U.S. oil refineries in Louisiana, Illinois, and Texas with a combined capacity of almost 749,000 barrels a day, or a bit more than 4% of the total U.S. refining capacity of 18.6 million barrels a day. Citgo-branded fuel is available at more than 5,000 locally owned retail gas stations in 29 states. The company also controls pipeline networks and 48 oil product terminals.

Read more …

What Britain need is an election.

• Britain Set To Lose EU ‘Crown Jewels’ Of Banking And Medicine Agencies (G.)

The EU is set to inflict a double humiliation on Theresa May, stripping Britain of its European agencies within weeks, while formally rejecting the prime minister’s calls for early trade talks. The Observer has learned that EU diplomats agreed their uncompromising position at a crunch meeting on Tuesday, held to set out the union’s strategy in the talks due to start next month. A beauty contest between member states who want the European banking and medicine agencies, currently located in London, will begin within two weeks, with selection criteria to be unveiled by the president of the European council, Donald Tusk. The European Banking Authority and the European Medicines Agency employ about 1,000 people, many of them British, and provide a hub for businesses in the UK.

It is understood that the EU’s chief negotiator hopes the agencies will know their new locations by June, although the process may take longer. Cities such as Frankfurt, Milan, Amsterdam and Paris are competing to take the agencies, which are regarded as among the EU’s crown jewels. Meanwhile, it has emerged that Britain failed to secure the backing of any of the 27 countries for its case that trade talks should start early in the two years of negotiations allowed by article 50 of the Lisbon treaty. The position will be announced at a Brussels summit on 29 April. Despite a recent whistlestop tour of EU capitals by the Brexit secretary, David Davis, diplomats concluded unanimously that the European commission was right to block any talks about a future comprehensive trade deal until the UK agrees to settle its divorce bill – which some estimate could be as high as €60bn – and comes to a settlement on the rights of EU citizens.

[..] The European commission said earlier this month that talks about a potential trade deal would occur only once “sufficient progress” had been made on Britain’s €60bn divorce bill and the position of EU citizens in the UK and British citizens on the continent. It is understood diplomats representing the EU27 did discuss a definition of “sufficient progress”, but ultimately left it to the leaders to decide. An EU source said it was hoped that “scoping” talks on a deal, and a transitional arrangement on access to the single market, could start in the autumn. The EU’s negotiating position detailed in the European council’s so-called draft guidelines will also be redrafted to include mention of the European parliament’s role, in a sign that MEPs are angling to play a greater part in shaping the talks. Tusk’s team will “fine-tune” the guidelines ahead of a final meeting of diplomats on 24 April, an EU source said. A one-day summit of leaders will take place on 29 April in Brussels to sign off on the document.

Read more …

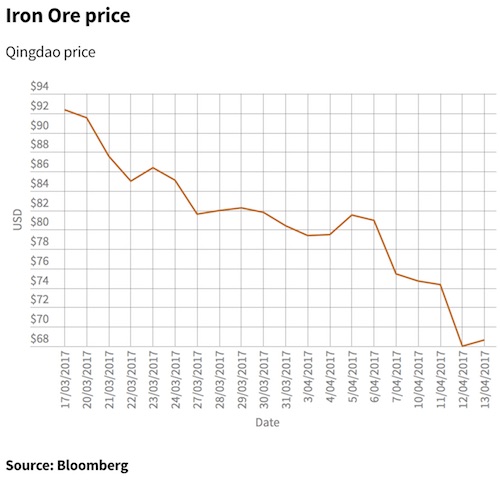

Not to worry though. Australia already has a new bubble going to replace it.

• The Dream Is Officially Over For Iron Ore (SMH)

Nev Power, the man who runs Andrew Forrest’s third force in iron ore, Fortescue, is something of an optimist. As the company’s share price was in freefall on Thursday he fronted up to media and investors putting a relatively positive spin on the outlook for prices of the commodity most pivotal to the health of the Australian economy. In previous periods Power has underestimated price falls and price gains and he now thinks it will settle at about $US60 ($79) to $US65 per tonne. Having ridden price rises in iron ore for more than a year, the big producers like Fortescue now need to reassure investors they are match fit to cope with the wild downward gyration in price. For the sake of the broader economy – and Fortescue shareholders – let’s hope he is right and we don’t reach the $US45 that the previous federal treasurer, Joe Hockey, predicted less than two years ago.

The trouble is that the myriad professional analysts and forecasters that follow this market have a significantly less rosy view of where the price will bottom out – more like $US50 a tonne. As prices have spiralled down over the past few weeks and the decline momentum has moved into full swing this week, the I-told-you-so cries have been louder than ever. As the price of iron ore irrationally moved up to more than US$94 in February – it was these bearish experts that were red faced. Today their predictions have been, at least in part, vindicated. It is now below $US70 and falling – a whopping 28% drop in a matter of weeks. To be fair the big producers including BHP Billiton and Rio Tinto have not been in denial about the iron ore price bubble – warning investors for more than a month that the recent prices have been something of a mirage.

Read more …

Is there anyone left in government who is not on the take?

• Brazil’s Odebrecht Paid $3.3 Billion In Bribes Over A Decade (R.)

Odebrecht, the Brazilian engineering company at the center of a historic corruption scandal, paid out a total of about $3.3 billion in bribes in the nine years through 2014, according to testimony cited by local media on Saturday. Through a department specifically established to pay politicians and other recipients for public works contracts, Odebrecht paid as much as $730 million annually in both 2012 and 2013, the years when bribe payments peaked, according to a spreadsheet that a former executive reportedly gave investigators as part of a plea deal. The $3.3 billion figure, and related annual tallies as laid out in the spreadsheet, were reported on Saturday by the G1 news site of the Globo media group and the Estado de S. Paulo, a leading newspaper.

A trove of plea deal testimony unsealed this week by a Supreme Court justice is shedding light on the extent and manner in which Odebrecht, once Latin America’s most successful engineering firm, routinely paid officials in Brazil and other countries in exchange for winning contracts. The testimony was unsealed as the justice, Edson Fachin, authorized investigations of eight government ministers, 12 governors and dozens of federal lawmakers implicated in the scandal, uncovered three years ago because of a kickback investigation at the state-run oil company Petrobras. Odebrecht, whose former chief executive has been jailed since 2015 because of the probe, negotiated a far-reaching plea agreement with Brazilian investigators last year, leading to testimony by about 80 company executives and employees.

Along with an affiliate, Odebrecht also agreed last year to pay at least $3.5 billion to U.S. and Swiss investigators for international charges related to the scandal. Earlier on Saturday, Estado de S. Paulo also reported that Brazilian authorities were investigating if any of the foreign kickbacks the company has already admitted to violated Brazilian law. The company made those payments in countries including Mexico, Ecuador, Peru and Angola.

Read more …

A whole new form of cashless society…

• Zimbabwe Cash Crisis: ‘Coins May Also Disappear’ (AllA)

Coins used to be for the piggy banks used by kids to save money given by their parents for break-time snacks at school. The adults normally kept a few of them when they got them from the grocery store as change. One normally didn’t have to keep lots of these because they broke pockets in the case of men, or made the handbag heavy for women. When the piggy bank became full, a way was always sought to turn the coins into “real cash” – crispy bank notes the parents would use to buy items of choice for the saving kids. Banks did not normally accept large amounts of coins, and these coins were often changed for notes in grocery shops or other retailers who had use for them for change.

In crisis-torn Zimbabwe, things have changed; coins are no longer for children’s piggy banks, they are now treasure items for adults who are failing to get cash from banks due to a worsening liquidity crunch in the economy. Banks are now dispensing large amounts of coins to depositors because they have run out of notes to honour their obligations to the banking public. At a bank in the capital last week, depositors waited in long queues to withdraw US$50 apiece in coins. “I’m at least relieved,” one depositor said, holding a plastic full of coins after a long wait in a bank queue. Bank notes have become a scarce commodity and coins have taken their place as a medium of exchange in the country. The $0,25 and $0,50 bond coins, which were introduced to ease a change problem that had been brought by use of hard currencies in 2009, have become choice monetary instruments in a liquidity-challenged economy.

[..] Economist, Christopher Mugaga, who is also the chief executive officer of the Zimbabwe National Chamber of Commerce, said the situation in the country was increasingly getting desperate. He warned that even the coins could soon become scarce on the market. He blamed the crisis on an erosion of confidence in the banking sector, which has resulted in people avoiding depositing their money with banks because of failure to withdraw it on demand. “When the bond notes were introduced, pressure was on the notes. People are also not banking hence for a every dollar, only $0,05 goes back into the banking system. So when you go back to the bank, you will not find the notes,” Mugaga said. “If the problem persists, coins may also disappear,” he warned.

Read more …

A very convenient blunder.

• Marine Le Pen Faces Wipe Out In French Election After Computer Blunder (E.)

A monumental computer blunder could cost Marine Le Pen the French general election as 500,000 citizens living outside of France have the chance to vote twice. Half a million people received duplicate polling cards in the post, which would allow them to cast two votes at the first round of the election, held on April 23. French authorities confirmed they would not be investigating the potential electoral fraud until AFTER the election, when retrospective prosecution may take place. This could crush Ms Le Pen’s dreams of surging to power, as most French nationals living outside of their country are not right wing – demonstrated by the fact many feel they depend on the EU to guarantee their stay in foreign countries.

Voting twice is a crime, but police will only find out if they run a check on the individual through their computer systems. The punishment can be up to two years in prison and a fine of about £13,500. France’s Interior Ministry has said it will not be invalidating the election because of the duplicate voting glitch, but with Bloomberg’s latest poll currently showing Mr Macron and Ms Le Pen polling at 22.8%, and far left Mr Melenchon at 18.3%, it is possible an extra 500,000 votes either way could swing the balance of power.

Read more …

The New York Times is way late and doesn’t even care to ask where all the money went.

• The Refugee King of Greece (NYT)

According to aid experts, more has been spent on the humanitarian response in Greece than on any refugee crisis in history. “Every year, Greece hosts 25 million tourists,” a frustrated aid worker told me, “and to date we have been given 800 million euros in funding for this crisis — but we can’t find proper accommodation for 50,000 people?” The crisis is, instead, the result of deliberate political choices. According to Louise Roland-Gosselin, the advocacy manager of Doctors Without Borders, “Europe has said: ‘We have had enough of this. It’s no longer our problem.’ There are too many elections in too many countries. Politicians are pandering to the right and saving their skins at the price of the refugees.”

As part of the deal with Turkey, the European Union agreed to relocate the refugees who were already stuck in Greece. But only 10% have been settled elsewhere, and member states are trying to weasel out of taking more. A family reunification program is supposed to be more effective, but the number of people being resettled under that program is shrinking, too. [..] The family, like thousands of others, arrived traumatized by war. Now they are being traumatized again, this time by European politics. Europe is doing this on purpose. It wants to dissuade other refugees from making the journey. But desperate people will keep coming, and will simply take greater risks than ever before. [..] By refusing to resettle refugees, Europe is whittling away at its commitment to human rights.

But Europe promised to protect those rights in the 1948 Universal Declaration of Human Rights, as well as in other treaties, charters and national laws. “These states are undermining their obligations — and these are the same states that created the human rights laws and ratified conventions,” says Sari Nissi, who heads up the International Committee of the Red Cross mission in Greece.

Read more …

The EU has lost its legitimacy. “Efforts by the European Union and its border agency FRONTEX to prevent loss of life at sea [..] have only resulted in more people drowning..”

• EU ‘Leaving Migrants To Drown’ Say Rescuers (Ind.)

More than 2,000 migrants trying to reach Europe were rescued from the Mediterranean on Friday, while at least one person was found dead, the Italian coastguard confirmed. A spokesperson for the service said 19 rescue operations by coastguards or non-governmental organisations had saved a total of 2,074 migrants on 16 rubber dinghies and three small wooden boats. The coastguard also confirmed that one person had died when the boats sank, but gave no details. The rescues come just days after a boat sank off the coast of Libya on Thursday. Ninety-seven refugees are missing, presumed drowned. According to the International Organisation for Migration (IOM), nearly 32,000 migrants have arrived in Europe by sea so far this year. More than 650 have died or are missing.

The number of migrants increased to a high of 5,079 for 2016, according the the IOM – despite a huge decline in numbers of migrant arrivals since 2014. Médecins Sans Frontières (MSF), a medical charity which has carried out hundreds of rescue operations in the Mediterranean since the beginning of the migrant crisis, has criticised Frontex, the European Border and Coast Guard agency, who operate official EU patrols on migration routes. MSF said in a series of tweets that NGOs were being forced to fill gaps in service provision left by the EU coastguard. “Frontex Director says it’s a paradox that a third of rescues are done by NGOs. We agree. Where are Frontex boats in a day like this?” MSF tweeted. “Many more people could have died in a day like this if we arrived a few hours later. We are where we’re needed, what’s the EU doing meanwhile?”

Friday’s rescue operations were performed entirely by NGOs. Mary Jo Frawley, a nurse who was involved in MSF’s patrols this week, said: “Efforts by the European Union and its border agency FRONTEX to prevent loss of life at sea through strengthened border control, increasing militarisation and a focus on disrupting smuggling networks has only resulted in more people drowning not fewer and has had little impact on the flows of arrivals. “This, combined with the lack of adequate EU search and rescue operations has meant that MSF and other humanitarian organisations have – in an unprecedented move – been forced to step in to avoid further loss of life.

Read more …