Kathimerini Trump and Evolution Jan 25 2017

https://twitter.com/GOP_is_Gutless/status/2079537430412038619?s=20The most incredible journey 🇺🇸 https://t.co/vMmnmcFFAY

— Monica Crowley (@MonicaCrowley) July 22, 2026

https://twitter.com/AdamMoczar/status/2079630710390784310?s=20🚨BREAKING 🅱️: In a jaw-dropping disclosure, former U.S. President Joe Biden and his son, Hunter Biden, pocketed $10 million in Burisma bribes. Moreover, Biden has tried to bury explosive evidence that the Bidens took $5 million each to kill a Ukrainian corruption probe… pic.twitter.com/wZ8L8dAqSF

— Q The Storm Rider (@Q_TheStormRider) July 21, 2026

“Iran [..] has not backed down in the face of Trump’s fresh threats… “

Of course not. Threats are Iran’s language. They react to threats with threats.

They react to the reaction to threats, provided those are not more threats.

• IRGC: Strike Iran’s Infrastructure, We’ll Shut Off The Gulf’s Power (ZH)

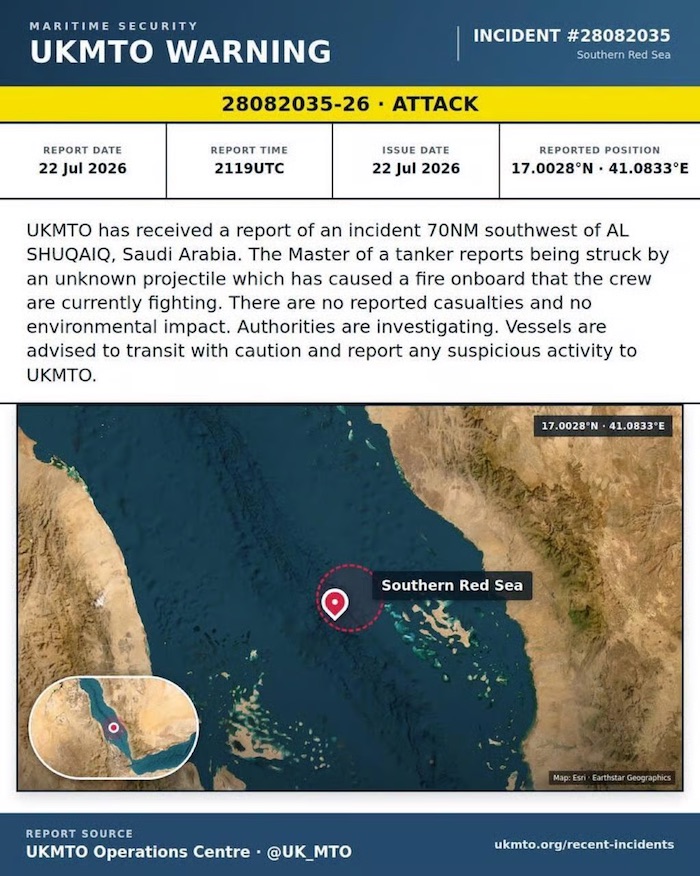

Oil gained after Iran-backed Houthi militants said they targeted two Saudi Arabian tankers in the Red Sea, escalating the Middle East conflict and threatening deeper supply disruptions. Brent spiked above $95 in post-settlement trading. The Houthis attacked the two vessels with missiles and drones for violating a blockade imposed in the Red Sea, identifying the tankers as Encelia and Layla, the rebel group said. UK Maritime Trade Operations said a vessel was hit southwest of Saudi Arabia’s Al Shuqaiq, causing a fire on board. UKMTO didn’t identify the ship.Read more …

The first attacks on tankers in the Red Sea opens up a new front in the Middle East conflict, which has snarled traffic through the Strait of Hormuz following a flare-up in violence.Iran Responds to Trump Ultimatum: We’ll Turn The Lights Off In Gulf

A top IRGC official has responded to Trump’s Bridge attack for each shipping attack ultimatum. Iranian IRGC Aerospace Commander Mousavi has threatened that Iran will cut off electricity to America’s Gulf Allies if Iranian bridges or power plants are attacked, Tasnim News Agency. “If the Americans target an Iranian bridge or power plant, Iran will respond by striking infrastructure and bridges across the region, including energy facilities in which the United States has interests,” the official said according semi-official news agency Tasnim.“The Americans should by now, after these past ten days, be fully convinced that Iran strikes wherever it decides to strike. Therefore, any such gamble by Trump will once again end in his embarrassment,” the IRGC commander added. Separately, Iran’s deputy foreign minister briefed 25 European ambassadors and charges d’affaires in Tehran on the status of the conflict. “I reminded them that in the 40-day war, we imposed a severe defeat on the aggressors. In this new round of military aggression as well, we will resolutely defend our homeland and national interests,” Kazem Gharibabadi posted on X.

“These wars have created no strategic gains for America and only endanger regional and global peace and security. I also said that Europe is expected to safeguard the United Nations Charter and international law and to condemn aggression,” he added. Iran has continued to sound an “eye for an eye” theme, and has not backed down in the face of Trump’s fresh threats…

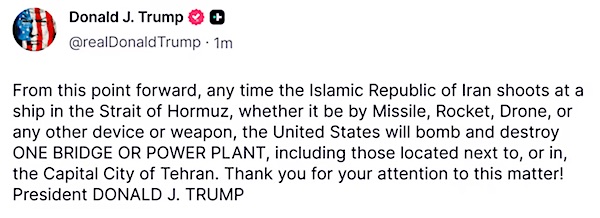

More telegraphing of intent from President Trump in the below Truth Social Post… he said the US military will “bomb and destroy” one bridge or power plant – including in Tehran – each time the Iranian military shoots at a ship in the Strait of Hormuz. This comes a day after he unveiled the US military plans to conduct a large bombing of Iran’s Pickaxe Mountain nuclear complex, which is heavily fortified.

But the Iranians have already long demonstrated they won’t alter course in the face of such threats, especially bluster from Trump over social media, and so this unlikely to be any kind of fix for Washington, as Tehran has vowed to keep control of Hormuz at all costs. The Pentagon has argued that things like bridges are ‘dual use’ as the Iranian military uses them to get supplies from one region to another, while international monitors have highlighted the potential for war crimes. The Iranians have in turn widened attacks on Gulf states to include key civic infrastructure, like water desalination plants (in Kuwait) – each time their own infrastructure gets hit.

* * *

Amid continued fighting which has included explosions heard in Tehran overnight and in the south, Iran’s leadership has condemned the Trump administration’s “obsessive focus on Kolang Kouh where no nuclear activity is taking place is nothing more than a fabricated pretext for aggression, destruction, and sabotage,” according to Foreign Minister spokesman Esmail Baghaei in a post on X, referring to Pickaxe Mountain.

He pointed out that all of Iran’s nuclear activity has long been fully declared to the IAEA, and so the repeat threats out of Washington to mount a major attack on it is a “flagrant violation” of UN charter and international law. Trump had said the day prior that the US military will be hitting Pickaxe mountain “pretty soon very heavily and there is nothing they can do about it.”Even some supporters have quested why the US Commander-in-Chief would so casually telegraph his intentions, saying the Pentagon loses an operational edge in revealing such plans.

There’s been a lot of sudden focus on Pickaxe Mountain, though it had largely been absent from all prior media coverage of the war, due to Israeli intelligence feeding it to US mainstream press. “Israeli intelligence believes Iran moved thousands of uranium-enrichment centrifuges into tunnels deep inside a mountain last fall, Israeli and U.S. officials say, a development that would heighten concerns that Tehran could reconstitute its nuclear program,” The Wall Street Journal wrote Tuesday.

“Israel passed along the intelligence findings to the U.S., saying the centrifuges were transferred to the Pickaxe Mountain site last fall after the 12-day war in June when American and Israeli strikes pummeled Iran’s three main nuclear sites,” it added. And now, by all accounts, more aircraft, refueling planes, and heavy military hardware continue to be transferred from Europe and into the Central Command area of responsibility.

Who do you think pulls the strings here?

• Ukraine’s Army Chief Latest To Fall Victim To Zelensky’s Risky Reshuffle (ZH)

Zelensky strikes again in another major military firing, amid his promised big cabinet and military ‘reshuffle’. The Ukrainian president announced Tuesday that he was dismissing Oleksandr Syrsky, commander-in-chief of country’s army, and appointing joint forces commander Mykhailo Drapaty in his place. Syrsky was in the post for nearly two-and-a-half years, since February 2024. “I have decided that the new Commander-in-Chief of the Armed Forces of Ukraine will be Mykhailo Drapaty… I am grateful to Oleksandr Syrsky and to each of our warriors for Ukraine’s strong front-line positions,” Zelensky unveiled in a post on Telegram.Read more …

The decision comes just days after popular 35-year old defense minister Mykhailo Fedorov was sacked, despite his reputation for orchestrating the ramped-up drone war on Russia. And the defense chief’s removal had come soon on the heels of Prime Minister Yulia Svyrydenko’s surprise ousting last week, upon which Zelensky in a suggested a broader government overhaul was underway. “Ukraine is changing its political strategy,” he made clear. President Zelensky’s Tuesday evening address included mention that he had offered former defense minister Mykhailo Fedorov a “decent post” to oversee the technological ‘component of the state.The remark of taking care of Fedorov is a clear attempt to calm masses of Ukrainians who took to the streets in a rare wartime protest over his shock removal. Zelensky has said he is doing all of this as part of a new strategy to take the war to Russia and its territory. “A significant path has been walked, Ukraine’s defense continues, and every soldier deserves proper respect,” Zelensky said. “I am grateful to Oleksandr Syrsky and to every one of our soldiers for Ukraine’s strong front-line positions.”

“Tomorrow we will formalize all decisions. Ukraine must emerge from this situation stronger, and it will become harder for Russia,” he said. The past week has witnessed some high drama within the top echelons of defense ranks, as Kyiv Post explains:

Fedorov said after his dismissal that he had pushed for Syrsky’s removal, accusing the commander-in-chief of blocking military reforms, and calling for changes in the military’s top leadership while defending his own record on robotics, drones and air defense. Under Fedorov’s tenure, Ukraine deepened its reliance on unmanned systems for dangerous frontline missions. Since January, the military has carried out more than 50,000 logistics and evacuation missions using ground robotic complexes (GRCs) in order to preserve soldiers’ lives in high-risk situations.

In a rare personal column, Syrsky broke silence and apologized to ousted Fedorov, saying he had no knowledge of their conflict before it spilled into public view. “For me, it was a surprise to learn that the minister and I had a conflict. I saw our relationship as a working one, with difficult questions and different positions” Syrsky wrote. “If I offended someone with something: Mykhailo Albertovych [Fedorov], I’m sorry. I can be tough,” he continued.

When you’ve lost The Economist…

Ukraine’s government is in a crisis of its own making. Firing Mykhailo Fedorov, the reformist defence minister, has galvanised street protests. Calls to push out Oleksandr Syrsky, the commander-in-chief (pictured), who feuded with Mr Fedorov, are growing. Volodymyr Zelensky must… pic.twitter.com/Hr4SUNUlwM

— The Economist (@TheEconomist) July 20, 2026All of this raises serious questions for Ukraine’s current narrative that it now has the momentum against Russia. If things are going so well, then why undergo risky and drastic leadership changes. It could be that things are actually not going well and the nature of Ukraine’s drone warfare is necessarily limited in scope. It might get media-capturing hits on Russian oil depots, but Russian forces by many accounts keep grinding forward slowly and methodically on the front lines in the east.

Sundance says Zelensky firing popular figures makes no sense.

But:

Zelensky has nothing to say in Kiev, he doesn’t do the firing. The nazis control the country.

Their No. 1 concern is the corruption money flow. They shsre this concern with the western donors, who take their -growing- share.

Perhaps Ukraine is not doing nearly as well as we are led to believe.

NOTE: This is not Russia vs Ukraine, but Russia against the West.

• Zelenskyy Removes and Replaces Leading Military Officials (CTH)

I have not written about the recent events in/around Ukraine because none of it makes sense and all of the information flows through the prism of ‘western’ intelligence propaganda. According to Ukraine President Volodymyr Zelenskyy {SEE HERE}, he has removed and replaced the entire leadership apparatus of the Ukraine military. This follows his removal of 35-year-old Mykhailo Fedorov from the defense ministry last week {CITATION} that led to massive protests against Zelenskyy and armed forces Chief Gen. Oleksandr Syrskiy, who was also eventually replaced.Read more …

As the story is told the young Defense Minister Mykailo Fedorov was very well regarded and was the person responsible for the successful technological advancements in military drone use. 35-year-old Fedorov was a close working partner with Palantir head Alex Karp who is assisting Ukraine in their drone development and deployment. If the drone development and deployment was such a massive success, as pronounced in all western and Ukraine statements, then why would Zelenskyy remove such a critical and effective Defense Minister? This makes no sense.Additionally, if Chief General Oleksandr Syrskiy was such an effective combatant commander, and if Russia was indeed pushed back on their heels by both Syrskiy’s campaign and Fedorov’s drones, then why would Ukraine disrupt their entire military leadership apparatus while they are winning such well publicized victories. Again, none of this makes sense.bThese moves by President Zelenskyy are akin to President Trump firing Secretary Pete Hegseth and Joint Chiefs Chairman General Dan Caine, while saying they were doing an exceptional job on Operation Epic Fury in Iran. See the problem?

None of these moves by Ukraine President Zelenskyy make any sense against the background story of them having incredible success against Russia. You don’t replace the entire military leadership apparatus if things are going swimmingly. However, it seems that no one in western media even fathoms the obvious conflicts in the narrative. The young defense minister Fedorov, responsible for the well-publicized and celebrated victories in the use of drone warfare does not summarily get dispatched unless there is some underlying reason. Something is not adding up.

ZELENSKYY –” Today, the decisions on the changes in the leadership of the Armed Forces of Ukraine will be formalized – the relevant decrees are in preparation. Together with Mykhailo Drapatyi and Yevhenii Khmara, we determined that Major General Ihor Skybiuk will become the new Chief of the General Staff of the Armed Forces of Ukraine. He is a highly experienced officer who defended Ukraine shoulder to shoulder with the new Commander-in-Chief. It is important that all components of our Armed Forces continue to function in complete coordination. We also determined together how Oleksandr Syrskyi and Andrii Hnatov will continue serving in the defense of our country.”

Wall Street Journal – Ukrainian President Volodymyr Zelensky fired the country’s armed-forces chief in a major reversal after initially siding with Gen. Oleksandr Syrskiy in a row with a young defense minister closely associated with Ukraine’s growing prowess in drone warfare.

The Ukrainian leader announced his abrupt shift Tuesday evening following days of street rallies after he removed Mykhailo Fedorov from the defense ministry last week. After several meetings with senior military commanders, he replaced Syrskiy with another experienced officer, Maj. Gen. Mykhailo Drapatiy, who previously signaled his willingness to take a more innovative approach to breaking the deadlock on the battlefield. It could prove a pivotal moment in Ukraine’s four-year-long defense since Moscow’s full-scale invasion. {MORE}

Additionally, at the exact moment when 35-year-old Mykhailo Fedorov was fired from the Defense Ministry, U.S. influencer Laura Loomer, a woman of generally unstable disposition, set off to begin a propaganda campaign in Ukraine telling her audience it was time to defeat the Russian propaganda.What followed from Loomer’s arrival in Ukraine (still unfolding) is transparently an intelligence community assist paid propaganda effort to reverse her position on Ukraine and begin supporting the Zelenskyy regime.

Less than 24 hours after Loomer arrived in Kiev to begin broadcasting her pro-Zelenskyy propaganda effort, it was announced that FBI Director Kash Patel will be traveling to Russia {Citation}. “FBI Director Kash Patel is planning to visit Russia later this year, likely in mid-October, according to a U.S. official and a person familiar with the situation.” … “Patel is scheduled to visit Russia on Oct. 14-15, first stopping in Moscow and then St. Petersburg.”

“We have Mayor Mamdani, who pushed and is pushing an agenda of government-run supermarkets, abolishing private property rights, and seizing the means of production,” she continued. “…And that is exactly what they did in communist Cuba.”

• Congresswoman’s Blunt Message for the MSM on Democratic Socialism (Anderson)

“This is what radical leftism is. It may wear various different slogans and ideologies across place and time. They call themselves anti-capitalist or anti-imperialist, communist, anarchist, Marxist, but the fundamental character is always the same,” Marco Rubio said last week when he hosted the leaders of over 60 different countries to a ministerial on the “resurgence of transnational far-left terrorism.” He left out “democratic socialism,” but let’s face it. It’s all the same. And Rep. Nicole Malliotakis (R-N.Y.) spoke out about that today at a House Republican leadership press conference, warning about the rise of so-called “democratic socialists” and the reality for voters and the media.Read more …

Malliotakis would know. Her mother fled Cuba in 1959 as Fidel Castro took power. The Castro regime stole her family’s home and their small business, a gas station owned by her grandfather. She says her mother never saw her grandfather again after that. I’ve heard countless stories just like that from Venezuelan friends and acquaintances. Communism ruins families. “Communism destroys. It steals from the people,” Malliotakis said. “…people end up living in squalor and lack the basic needs that human beings need, and the people that run the regime live as kings. That’s the reality. It’s about power. It’s about consolidating power for a select few.”She pointed out that, sadly, that’s exactly what we’re starting to see here in the United States with the winners of several recent primaries and elections. “We have Mayor Mamdani, who pushed and is pushing an agenda of government-run supermarkets, abolishing private property rights, and seizing the means of production,” she continued. “…And that is exactly what they did in communist Cuba.”

The congresswoman pointed out that her Cuban mother says socialism is basically just a step toward communism. The government steals property and wealth and uses it to redistribute and create better lives for themselves, while their constituents suffer. She also pointed out that Democrats want to pack the Supreme Court, but that’s a move straight out of Hugo Chávez’s playbook. As I wrote yesterday, that’s one reason why Venezuela can’t have elections right now. The country’s Supreme Court is stacked in favor of the regime, and it will require dismantling the court, among other institutions, to get there.

Malliotakis also points out that voters are going to be in for a rude awakening if we continue to allow this type of behavior here in our country. “They can call themselves Democrat socialists, but the reality is that the Commie Caucus is coming to Congress,” she warned. But her best message, in my opinion, was for the press in attendance: “It’s going to be a rude awakening if we don’t all pay attention, and that includes the press. Think about what’s happening in those countries, where they’ve had socialism and communism. The press is the first one to go. When they finally consolidate that power, the media is the first one to go, and it [becomes] a state-run media.

The congresswoman concluded that it’s important for all of us to stand up to these radical threats, and she’s right. Our regular readers know that I spend most of my weeks knee-deep in Venezuela and Cuba, and I’ve gotten to know many people who lived in and had to leave these countries. They all tell the same tale: families destroyed, loved ones dying due to lack of food or medicine, friends arrested for daring to speak out, no jobs, poverty, malnourished infants and children, extended power outages, lack of clean drinking water, regime harassment, arbitrary detentions, and kangaroo courts, etc. Why on earth would anyone want to live like that? And don’t tell me it just wasn’t done correctly. The outcome is always the same.

Here are Malliotakis’ full remarks. They’re worth a watch. And I hope she and many other people in this country continue to speak out in the days ahead.

The Commie Caucus is coming to Congress. Here is what it means for you. pic.twitter.com/64gJcuWonm

— Rep. Nicole Malliotakis Office (@RepNicole) July 21, 2026

“In a country with some of the strictest gun laws in the world, we’ve seen a rise in leftists and radical Islamic violence in the UK using alternative means. Up until now, it’s been “knife violence,” which we all know means there is an epidemic in the UK of knives jumping out of their drawers on their own and stabbing people…”

• It’s Hammer Time! The Violent Left’s New Weapon of Choice. (O’Brien)

Ann Widdecombe was a 78-year-old former member of Parliament (MP), pro-life advocate, Reform UK spokesperson, and a conservative. Security video taken from inside her home in Haytor, Devon, which is in rural southwest England, captured her quietly sitting down by herself for lunch on July 8 around 12:30 p.m. That’s when 28-year-old UK citizen Joshua Kerry from South Yorkshire entered the picture. It seems he just walked into the home through the front door, a stranger to Widdecombe, approached her, and said, “Don’t suppose you have bank cards and ID?”Read more …

Without giving her much of a chance to respond, British prosecutors say he smashed the hammer into Widdecombe’s skull 21 times as she sat in her chair, after which he tipped her out of the chair and onto the floor of her house. Prosecutors say that Kerry spent two minutes in the house, wearing black gloves, before approaching and murdering Widdecombe in her kitchen and then taking her wallet before leaving the scene. Was this a random killing? It doesn’t seem to be.While Kerry is alleged to have committed robbery, and so far there have not been any significant revelations of Kerry’s religious or political leanings, prosecutors say he did drive nearly 300 miles to carry out a very targeted attack. As my colleague Catherine Salgado reported previously, British law enforcement had been investigating the crime as an act of terrorism. This leaves us to conclude at the very least that Kerry had a problem with Widdecombe’s politics, making him a leftist. The Blaze is reporting that this was a targeted assassination.

According to @theblaze, British pro-life leader Ann Widdecombe was killed in what investigators are reportedly treating as an assassination.

— Kristan Hawkins (@KristanHawkins) July 20, 2026

This is a heartbreaking reminder that defending the preborn can come at a tremendous cost.

Please join me in praying for the repose of…In a country with some of the strictest gun laws in the world, we’ve seen a rise in leftists and radical Islamic violence in the UK using alternative means. Up until now, it’s been “knife violence,” which we all know means there is an epidemic in the UK of knives jumping out of their drawers on their own and stabbing people. It’s not like people should be held to account for their own actions and motivations, right? You do remember how the innocent, young, British Henry Nowak died, don’t you?

Henry Nowak died the same way a civilization dies: abandoned, handcuffed by authorities who neither trusted nor cared for him, and accused of hate crimes he did not commit. His murder is as tragic as it is enraging. He should still be alive today, and he would be if the last few… https://t.co/e3HkjzWzwU

— JD Vance (@JDVance) June 5, 2026Nowak died as he bled out in handcuffs, while British police made sure his knife-wielding killer was OK. Since guns aren’t as available to the British citizenry to defend themselves, nor as accessible to their would-be killers, the murdering class has had to innovate. While knives have been the murder weapon of choice, another throwback to more barbaric times has emerged – the hammer. That’s what Kerry allegedly used against Widdecombe, and it’s what a group called Palestine Action is promoting as a new means to employ “direct action.”

78-year-old Ann Widdecombe was bashed on the head repeatedly with a hammer until she died.

— Andy Ngo (@MrAndyNgo) July 21, 2026

Palestine Action is advertising "direct action" training for people who want to take up militant action using hammers. pic.twitter.com/JOIQrZYiBjIt’s probably no coincidence, but the hammer in the group’s graphic looks an awful lot like the hammer and sickle of the old Soviet Union, the hammer of communism, and the hammer that leftists from around the world rally around. If recent events are any indication, it seems that the hammer has transitioned from mere symbol to preferred weapon. (By the way, don’t try to log onto PalestineAction.org. My anti-virus software warned me of a potential phishing threat there. You don’t want to risk having someone invade your computer and wreak havoc.)

CNN described Palestine Action as “a UK-based organization that aims to disrupt the operations of weapons manufacturers connected to the Israeli government.” “It was founded by Huda Ammori and climate activist Richard Barnard in 2020, when the group took its first action to shut down the UK operations of Elbit Systems – Israel’s largest weapons manufacturer – and stated its commitment to ‘ending global participation in Israel’s genocidal and apartheid regime,’” CNN reported.

So, while in America the left continues its ongoing and long-term campaign to disarm gun owners and kill the Second Amendment, you can see that in other countries gun confiscation hasn’t stopped the left from perpetuating the dark savagery that is in its heart. The left knows that it will never win and hold power through popularity. Instead, it will win power through deception and violence, and it will hold power through force and violence. At the moment, that force has come in the form of its favorite tool, the hammer.

Mamdani knows this. But he can score cheap points.

• New York City Hall Has No Business Running Its Own Foreign Policy (David Manney)

New York City communist Mayor Zohran Mamdani spent months promising to arrest Israeli Prime Minister Benjamin Netanyahu. His lawyers finally delivered the answer anybody familiar with American law could see coming. “We do not have the independent legal authority to enforce this warrant,” Mamdani admitted Tuesday.His administration reviewed “every avenue” for using the International Criminal Court warrant if Netanyahu visits New York for the United Nations General Assembly in September. City lawyers found no legal path, proving that Mamdani’s campaign pledge was never within the mayor’s power.Read more …

Mamdani still called Netanyahu a war criminal and demanded that the federal government join the ICC and execute the warrant, while also declaring Netanyahu unwelcome in New York. I hate to be the one to break it to the Democratic Socialist, but mayors don’t decide who enters the United States. They don’t join international courts, recognize foreign warrants, conduct diplomacy, or set federal criminal policy.All Mamdani can do is offer his opinion, but City Hall has no separate foreign policy.Neither the United States nor Israel is a party to the Rome Statute, which created the ICC. Congress also barred state and local agencies from cooperating with ICC requests, providing support to the court, or helping surrender people to its custody.

(2) shall not prohibit—(A) any action permitted under section 7427 of this title; or (B) communication by the United States of its policy with respect to a matter. (b) Prohibition on responding to requests for cooperation

Notwithstanding section 1782 of title 28 or any other provision of law, no United States Court, and no agency or entity of any State or local government, including any court, may cooperate with the International Criminal Court in response to a request for cooperation submitted by the International Criminal Court pursuant to the Rome Statute.

(c)nProhibition on transmittal of letters rogatory from the International Criminal Court

Notwithstanding section 1781 of title 28 or any other provision of law, no agency of the United States Government may transmit for execution any letter rogatory issued, or other request for cooperation made, by the International Criminal Court to the tribunal, officer, or agency in the United States to whom it is addressed.

The ICC issued its warrant in November 2024, alleging Netanyahu committed war crimes and crimes against humanity during the Gaza war. Israel rejects the court’s jurisdiction and denies the allegations. The warrant doesn’t charge Netanyahu with genocide, even though Mamdani repeatedly calls him the “architect” of one. UN week creates another legal problem. The 1947 United Nations Headquarters Agreement requires federal, state, and local authorities to avoid obstructing representatives traveling to and from UN headquarters. Reuters:

Netanyahu traditionally travels to New York every September for the annual gathering of world leaders at the United Nations General Assembly. Israel responded to Mamdani’s comments on Sunday in an X post that called the ICC a kangaroo court and the arrest warrant against Netanyahu bogus. “Mamdani appears interested in diverting public attention from his follies and attacking the leader of the Jewish state and the only democracy in the Middle East,” it said.

The ICC was established in 2002 and has international jurisdiction to prosecute genocide, crimes against humanity and war crimes. The United States and Israel are not members of the court. Mamdani, who took office in January, said during his mayoral campaign that he would have police arrest Netanyahu if he set foot in New York City. Last November, shortly after Mamdani’s election victory, the mayor-elect and Trump held an unexpectedly friendly meeting in the White House even though they had previously traded insults. New York City can’t invite the world’s governments to Manhattan and then let its mayor select which leaders may safely attend.

President Donald Trump ended any remaining uncertainty Monday. Netanyahu “will not be arrested, in any way, shape, or form,” while in the United States, Trump said. Mamdani’s admission should close the matter. Instead, he used his retreat to demand federal action, preserving the political theater after conceding he couldn’t deliver his promise.New Yorkers were told their mayor would direct the NYPD to arrest a foreign prime minister. Months later, he acknowledged he lacked the authority from the beginning. Lawyers had to study a campaign pledge before Mamdani would admit that municipal power ends well before international diplomacy begins.

City Hall already has enough work. New Yorkers expect police protection, clean streets, safe subways, working schools, affordable housing, and competent public services. They didn’t elect a secretary of state. The U.S. government already has one. Mamdani can condemn Netanyahu as often as he chooses; he can support the ICC, criticize Israel, and urge Congress to change federal law. He still can’t turn personal ideology into municipal authority. His own legal review settled the issue. City Hall has no business running its own foreign policy, and Mamdani now admits he has no power to carry out the threat that helped build his political brand.

“It had become more the socialist caucus, and most of the leadership was socialist Democrats. I didn’t feel comfortable in it.”

• House Democrat Blows the Whistle on Socialist, Antisemitic Takeover (Margolis)

I’ve said before that I don’t like using the term “progressive” to describe the Democrat Party, its ideology, or its positions. Why? Because it suggests improvement or progress. At the very least, it’s a poor euphemism, but it’s more deliberately deceptive if you ask me. “By calling itself progressive,” it implies every position it takes is a positive one. Sorry, I can’t do that.Read more …

CNN’s Van Jones noted this very thing earlier this week. The commentator and former Obama administration official argued that Democratic Socialists of America-aligned candidates and their agenda are “regressive,” not “progressive.” Jones warned that the party’s drift toward socialism, hostility toward police, and open contempt for Israel is scaring off the centrist voters Democrats need to win elections. Even a guy who spent years defending this party on cable news can see the cliff it’s walking toward.Rep. Steve Cohen (D-Tenn.) also figured this out last year, and he did something about it. Cohen revealed to CNN this week that he left the Congressional Progressive Caucus last year. “I just found it to be not the same caucus I joined in 2007,” Cohen said. “It had become more the socialist caucus, and most of the leadership was socialist Democrats. I didn’t feel comfortable in it.”

That’s not a stray complaint from a bitter retiree. Cohen came to Congress in 2007 and aligned himself with J Street, a left-leaning Jewish organization that supports a two-state solution and has long rivaled the traditional pro-Israel lobby. Even that didn’t keep him in step with where his caucus went. “There certainly were not people who were so anti-Israel when I started, and there are within the progressive caucus now,” he said, describing a party that traded coalition politics for ideology.

Cohen announced last year that he wouldn’t seek re-election after the new district drawn and approved by Tennessee’s Republican legislature made his chances of reelection nearly impossible, but it’s quite clear he saw a much bigger problem brewing. “I foresaw it getting really nasty and antisemitism getting into it,” he said. He’d already watched that antisemitism spread through his party’s rank and file up close, which is exactly why the socialist caucus stopped feeling like home.

Cohen was one of only 22 Democrats willing to censure Rep. Rashida Tlaib after she defended the “from the river to the sea” chant in a video accusing President Joe Biden of enabling a Palestinian “genocide.” Tlaib hasn’t spoken to him since. A sitting congresswoman froze out a colleague for objecting to genocide rhetoric aimed at Israel, and her own party barely blinked.

Make no mistake about it: Cohen didn’t quit his caucus over redistricting maps. He quit because the socialists took over and brought their antisemitism with them. The Democrat Party didn’t get more “progressive.” It got more socialist, and more left-of-center people are noticing and doing something about it. Not only did Cohen leave the House Progressive Caucus, but Bill Maher says his vote is up for grabs in 2028. And if Democrats fail to win the House in November, you’ll know why.

The Dems have no face. Mamdani is New York, not America.

• Why Aren’t the Democrats Walking Away With the Midterms? (Rick Moran)

By all rights, Democrats should be blowing Republicans out of the water in these midterm elections. Donald Trump’s approval numbers are underwater, and on issues, Democrats hold an advantage on which party is better able to handle the economy. The Iran War is becoming more unpopular by the week, and inflation is beginning to tick up as a result. Republicans are trusted far more on immigration, but in a true, bitter irony, Trump has slowed the illegal wave at the border to a trickle, making it far less of an issue. So why aren’t the Democrats winning big? Ron Brownstein, a veteran political reporter, is noticing it too.Read more …

Trump’s job approval rating has plummeted below the level that triggered midterm wave elections vs Clinton 94, W. Bush in 2006, Obama in 2010 & Trump himself in 2018. And yet most surveys do not show Dems establishing a clear advantage in the key races that will decide control. https://t.co/MYxrsDilxy

— Ronald Brownstein (@RonBrownstein) July 19, 2026In Trump I, Ds won ~90% of voters who disapproved of him in most House/Senate races. In polls now, they usually win far fewer of them. That's the biggest yellow light for Ds in 26. But can Rs really hold so many more voters down on Trump thru Nov? My take https://t.co/9lmafPzfCc

— Ronald Brownstein (@RonBrownstein) July 19, 2026This gentleman has the answer for Brownstein and any Democrat who actually wants to win in November (LANGUAGE WARNING):

It’s because for some of us who are tired of the Trump chaos can’t vote for the dems when they are bat shit freaks. I can not ever vote for the loony dem state candidate in Texas. Waaayyy to many bad policy beliefs. Not moderate at all. So I’m voting for the alternative who has…

— Huckleberrycrew5 (@AnneDAngelo5) July 19, 2026Voters may not love Republicans. They may not like what’s happening in the economy, in Iran, and with inflation. They may not like Trump very much. But there’s one reason that, against all odds, Republicans could very well end up holding their slim majority in the House and even increase their margin in the Senate. Voters hate Democrats more. In an election where all of the issues are breaking the Democrats’ way, Republicans have two huge issues they can throw at Democrats that may very well scare enough voters to give the GOP an advantage.

The first is a gift from the Democrats: their acquiescence in an attempted coup of their party by the Democratic Socialists of America (DSA). Republicans will call them “communists.” The DSA doesn’t care what you call them as long as you vote for them.The Democrats are gambling, like all mainstream parties in history faced with a radical left surge, that once the kooks help the rest of them get elected, they will control them, tame them, and channel their energy into productive, constitutional avenues. Good luck with that because it worked so well in Russia and Germany in the 20th century.

Meanwhile, Republicans are going old school with a 1950s-era, genuine anti-communist “Red Scare” campaign. b“We’re fighting right now in Congress over whether we’re going to maintain our status as a constitutional republic or we’re going to trade that in, dismantle the foundations, and go down this dark road of death to communism,” Speaker Mike Johnson (R-La.) said in a press conference at the Republican National Committee. b“These crazy little mini-Mamdanis who are popping up all around the country, they are a danger to you and your family.”

The Hill: bHouse Majority Leader Steve Scalise (R-La.) drew attention to the Democratic Party’s ideological battle in those primaries, with the insurgent left-wing candidates defeating those favored by House Minority Leader Hakeem Jeffries (D-N.Y.). He was clear that Republicans saw those leftist candidates as useful to campaign against. “In swing districts, it draws an incredibly sharp contrast between our incumbent Republicans who are working to make life more affordable for working families against these communists who want to literally defund the police,” Scalise said.

He was referencing the Democratic Socialists of America (DSA) platform, which calls for “steps towards fully abolishing the police and prison system which protects the rich and jails the poor” and “amnesty for all immigrants regardless of status.” bI really hope they bring back Doo-wop and Elvis (yes, he’s still alive). While they’re at it, making my crew cut popular again would be fine with me. Democrats are doing all the heavy lifting for Republicans. The GOP doesn’t have to demonize the Democrats when the donks are doing a darn fine job of it on their own.

At some point Dems are going to have to grapple with the reality that in the face of all of Trump and Republicans’ manifest horribleness and incompetence, people aren’t rushing toward the Democrats. If you think the DSA stuff is helping, you’ve never talked to a swing voter. https://t.co/9LgLHkwnYf

— Sarah Longwell (@SarahLongwell25) July 19, 2026The trick for Republicans will be to find a way to get their supporters to the polls. Right now, the enthusiasm gap is concerning, but why isn’t it larger, asks one political science professor. “I don’t think that things are looking very good for Republicans,” said Rob Alexander, a political science professor at Bowling Green. “The enthusiasm gap that we’re seeing is unsurprising. Maybe the most surprising thing is that it’s not higher in favor of Democrats.”

The professor also noted what the GOP isn’t saying in the campaign. “It’s just all negative, negative, negative. There’s very little ‘we’re building the American dream, and things are better.’ It’s more ‘those guys are bad,’” Alexander said. “It seems to be the tactic that we’re settling into as we move on, and it’s going to be a really ugly fall throughout the country.”

“This is what America needs to be strong, successful, and resilient. “

• American Manufacturing One Year After One Big Beautiful Bill (Chris Queen)

It’s been about a year since President Donald Trump signed the One Big Beautiful Bill into law, and over that 12-month period, we’ve seen the positive outcomes from the act. One of those is an American manufacturing renaissance. A new report from the National Association of Manufacturers (NAM) demonstrates how the tax cuts from this bill have spurred growth in manufacturing: Manufacturing is the economic engine of the United States. Led by the 13 million people who make things in America, manufacturing succeeds when backed by policies that make it easier to build, hire, and expand.Read more …

H.R. 1 embodies that commitment. By signing H.R. 1 into law, President Trump gave manufacturers the foundation, competitiveness, and certainty to invest—in new facilities and equipment, jobs and wage growth, cutting-edge research, and our global competitiveness.This law is a once-in-a-generation investment in manufacturers, and it did not happen by chance. As pro-growth tax policies approached expiration, putting 6 million jobs at risk, manufacturers rallied to make our voices heard. Congress not only kept every one of the 10 major provisions for which the NAM advocated—they even added new provisions, all to strengthen manufacturing.One year after H.R. 1 became law, manufacturers have much to celebrate. Manufacturers in all 50 states are using H.R. 1 to invest in America. By NAM’s count, the Trump tax cuts have supported 6 million American jobs, saved $540 billion in wages for hardworking Americans, and contributed $1.1 trillion in GDP. “That’s the manufacturing economy a permanent, pro-growth tax code helps sustain — and manufacturers are delivering on the promise,” NAM says. The Working Families Tax Cuts in the One Big Beautiful Bill have seen concrete benefits in all 50 states. Investments in research and development, full deductions for facility expansion, and incentives to build in the U.S. have all spurred growth that’s hard to ignore or explain away.

From 11,000 jobs protected in Alaska to 708,000 jobs supported in California, every state is reaping the benefits of this unprecedented investment in the American workforce. NAM’s report gives case studies for all 50 states.The One Big Beautiful Bill’s provisions aren’t just for large corporations. Even small businesses like Winton Machine Company in Suwanee, Ga., are seeing the benefits. The 38-employee company is able to reinvest in its operations and innovate in its industry.

“As manufacturers, our ability to reinvest drives job creation, advances new technologies and supports our communities,” says CEO Lisa Winton. “I am committed to continue to help drive innovation and invest in the future manufacturing workforce here in the USA.” Louisiana’s Martin Sustainable Resources used the tax cuts, credits, and incentives to expand its facilities, upgrade its equipment, and make long-term investments. It’s planning for the future, thanks to these pro-growth policies.

“The Working Families Tax Cuts are helping to fuel modernization at our company,” says CEO E. Scott Poole. “Full expensing for facilities and equipment strengthens our ability to keep making long-term investments, and estate tax relief helps protect the continuity of a family-owned company rooted in Louisiana for generations.”“These results demonstrate the undeniable power of President Trump’s America First economic agenda,” reads the White House press release. “By putting American families and businesses first, the Working Families Tax Cuts are rebuilding American industrial strength, creating opportunity in every community, and delivering real results for real Americans.”

This is what America needs to be strong, successful, and resilient. It’s what can help sustain our economy in good and bad times. And I definitely voted for this. Trump’s tax cuts are helping American manufacturers build new facilities, upgrade equipment, create jobs, and plan for the future. That’s what an America First economy looks like, when policy moves beyond slogans and starts producing results.

“Considering the economy of the USA is ten-times larger than Canada, that’s quite a threat from Premier Doug Ford.”

• Ontario Premier Doug Ford Promises “to Dismantle the U.S” Economy (CTH)

Ontario Premier Doug Ford has a message to President Trump and to all Americans. Premier Ford promises to dismantle the U.S. economy if President Trump continues to threaten tariffs and trade sanctions.Considering the economy of the USA is ten-times larger than Canada, that’s quite a threat from Premier Doug Ford. WATCH:Read more …

Personally, I think all this back-and-forth banter is no longer worth the surface effort. It would be much easier, and now affirmed as constitutionally appropriate by the Supreme Court, if President Trump just executed a full trade embargo against all Canadian goods for a period of 60-days. Perhaps that way Canada will recognize just how vulnerable they are. Perhaps not, but it’s worth the effort. Just ban all imports and exports for 60-days and let’s see what happens.

“Donald Trump wants Canada to go and try to cut more favorable trade deals, so they will learn how good they had it.”

• USTR Jamieson Greer Outlines Details of Talking Points With Canada (CTH)

In the first half of this CNBC interview with U.S. Trade Representative (USTR) Jamieson Greer, the Ambassador walks through the reasoning, purpose and intent of the recently announced 50% tariff rate against Canadian imported goods. As noted by USTR Greer the Canadians are applying two separate metrics within their trade agreement with Europe and the USA. Toward Europe there are no limits and quotas on dairy products, toward the USA there are severe limits and quotas applied by third party brokers (co-ops owned by Canadian dairy farms) leveraged by the Canadian government. This is one example of Canadian duplicity.

Additionally, by the various provincial governments of Canada banning the import and/or sale of U.S. products, and with Canada putting caps and limits on automobiles, these USA trade actions are being confronted by the 50% countervailing duties against Canadian imports. Greer also calls ‘bulls**t’ on Carney’s double speak. WATCH:

The trade discussion with Canada returns at the 10:00 minute mark. Jamieson Greer notes we have always had trade issues with Canada for decades. There was a significant percentage of the population who are against offshoring jobs, which is what NAFTA essentially did in North America. It is also worth emphasizing that President Trump wants Canada to diversify. Both U.S. Ambassador Pete Hoekstra and President Trump have said, repeatedly, President Trump wants Canada to go make other bilateral deals with other nations. Why? Two main reasons.

#1) If Canada has to enter a bilateral trade agreement with another country, suddenly they learn what reciprocity means. They have to give something in order to get trade benefit. This is a completely new concept for Canada who have taken advantage of the USA for a long time with ZERO reciprocity in mind. This is what former Prime Minister Justin Trudeau was talking to Trump about in Mar-a-Lago (December ’24). In essence, Donald Trump wants Canada to go and try to cut more favorable trade deals, so they will learn how good they had it.

#2) If Canada cuts a trade agreement with, say, Europe, the terms of that FTA purchase in/out then become a standard in their trade allowances. This permits team USA to turn to Canada and say, “wait, we want the same terms”. We might even ask for most favored nation terms due to scale and scope. Canada is not prepared for this type of bilateral relationship at all. The CUSMA trade negotiator Dominic LeBlanc just discovered the problem following the current Canadian effort to diversify FTAs. Suddenly, LeBlanc has admitted quietly they have no response.

For around 40+ years (USTR Greer would argue 60+ years) Canada has benefitted from the U.S. economy purchasing their goods, allowing their businesses unlimited access to the U.S. market and yet simultaneously restricting the Canadian market from similar reciprocity. Those terms are no longer acceptable.

“Looking at the global automotive market, one conclusion is unavoidable: the end of the combustion engine is nowhere in sight.”

• The Death of the Cash Cow (Thomas Kolbe)

Looking at the global automotive market, one conclusion is unavoidable: the end of the combustion engine is nowhere in sight. The ideological crusade against Germany’s industrial backbone has merely led to the slaughter of the country’s automotive cash cows. The reasons behind the decline of Germany’s automotive industry will remain subject to debate. But one thing is clear: an energy policy detached from economic reality, driven by climate-apocalyptic ambitions, has harmed the industry at least as much as strategic mistakes at the management level.Read more …

A lack of cost flexibility and a German labor system rooted in the moral foundations of the post-war economic boom have made the adjustments necessary in the face of fierce competition from China, the United States and increasingly India far more difficult. German corporatism has also done companies a disservice by narrowing technological choices according to a familiar ideological compass. The end of the combustion engine is a collective product. Political leaders and institutional actors share the same conviction: pave the way with subsidies and taxpayer money toward a fully electric golden age.Meanwhile, almost quietly and somewhat embarrassingly, the industry has begun relocating production of its traditional combustion-engine models abroad. It is simply unhealthy for an economy to stand too close to the political fire. In times of crisis, companies are left exposed to the harsh winds of global competition — and so are the workers whose jobs disappear by the hundreds of thousands. The reality looks different from the political narrative. Around 95 percent of vehicles worldwide are still powered by traditional combustion engines. Among new registrations last year, fully electric vehicles accounted for roughly one quarter. Nearly two-thirds of newly registered vehicles still have a combustion engine under the hood. The remainder are hybrids.

There is no doubt that the long-term technological path is moving toward hybrid drive systems. Traditional combustion engines offer limited prospects for new investment. Nevertheless, this enormous market would have been the necessary cash cow for German automakers and their suppliers. The profits generated from combustion-engine vehicles could have provided the financial strength needed to invest in new technologies according to actual market developments.

This transformation would have taken place at the German home base if an ideological fervor among saturated urban elites had not emerged — a fervor that turned against the country’s own automotive industry and initiated a form of industrial self-destruction.The fundamental mistake lies in Germany’s corporatist model. The country rushed into an immature technology with flags flying high, encouraged by politicians who believed the future lay entirely beyond fossil fuels. The theory sounds attractive: borrow cheaply, pool government debt at Germany’s favorable financing conditions, create the necessary technological foundations and production capacities, and secure pole position in electric mobility from the beginning.

But the devil, as always, lies in the details. It would be the first time in economic history that a centrally planned strategy permanently moved ahead of market reality. The pressure on German manufacturers has grown since China succeeded not only in closing the technological gap with European producers, but in reopening it in certain areas to its own advantage. Beijing is also fighting the emerging weakness of its domestic economy with massive subsidy programs. It is therefore hardly surprising that German manufacturers have come under enormous pressure in the most important automotive market in the world.

At the same time, the consequences of Germany’s energy transition, sky-high energy costs, excessive regulation and rigid labor laws have made the domestic location increasingly unattractive for additional investment. The cash cows that policymakers had already written off are now grazing elsewhere. It is not the combustion engine that is disappearing — it is the value creation surrounding it. Volkswagen’s Passat is now produced in Slovakia rather than Emden. The new Volkswagen Transporter is built at Ford Otosan’s plant in Turkey, while Audi produces the Q3 in Hungary. Mercedes has moved a significant part of its compact-car production to Kecskemét.

Large premium SUVs from German manufacturers have for years largely rolled off production lines in the United States or Slovakia. The truth is simple: production takes place where the combustion engine generates the highest returns — and Germany is clearly no longer one of those locations. Around 130,000 jobs have been eliminated in Germany’s automotive industry in recent years. Once second-round effects are included, roughly half a million jobs may have been affected by the crisis. A lost position in core automotive production typically leads to two, if not three additional job losses along the supply chain and through declining purchasing power in the surrounding regions.Eastern Europe, economically held back by socialism until the end of the Cold War, now benefits from capital flowing out of the West.

“Across almost all 50 states, there’s a move toward moratoriums on building data centers as concerns about their potential impact grow…and they remain a political liability as the midterms approach.”

• Billion-Dollar Data Centers And The Growing Opposition (Janet Levy)

Nestled between the sere hills east of Sparks, Nevada, and a little off the U.S. Parkway (SR-439), Switch’s Citadel Campus is a Las Vegas company specializing in data centers. One building is already operational: Tahoe Reno 1, a high-security, futuristic industrial shed standing on endless rows of girders, with a roof designed to withstand 200-mile-per-hour winds.Read more …

Inside, thousands of servers process data for businesses that pay for space, bandwidth, and security. To dissipate the enormous heat from the servers and the generators powering the unit, several million gallons of water are circulated through hundreds of miles of tubing—this in the driest state in the U.S., where groundwater is declining at an alarming rate. The low-frequency hum and noise from the center can be heard nearly a mile away.Switch describes it as “the single largest colocation data center facility on the planet.” It has a footprint of 1.3 million square feet, roughly equivalent to 23 American football fields. Its power capacity—a metric of processing ability and the equivalent backup supply and cooling required—is 130 MW. For perspective, one megawatt can power 75 racks, each holding 21–42 servers, and power 500–1,000 homes.

When the eight planned buildings are ready, the 2,000-acre Citadel Campus, bounded by concrete walls, will offer a whopping 7 million square feet of server space and 650 MW of power capacity, making it the world’s most powerful data complex. Switch plans to develop it into an exascale ecosystem—with computers capable of quintillions of calculations per second, needed for AI and high-speed work, and power capacity running into several gigawatts.

As AI, cloud computing, and digital services touch all lives and demand for processing power grows exponentially, data centers are proliferating across the U.S. Over 3,000 centers are now operational, with 1,500 slated for development. While 87% of current centers are in urban areas, 67% of the newer ones are planned in rural areas, and 39% in counties with no centers.

In Nevada and elsewhere, communities, local and city governments, and legislatures are raising concerns about the significant environmental and quality-of-life impacts of data centers. In fact, Reno has a moratorium until August 2027 on approving data centers within the city. Surveys show that most Americans oppose data centers in their neighborhoods. The biggest concerns are acreage and water use; strain on power grids; air pollution from backup generators, although many centers claim to rely on green backups; and noise pollution, with the low-frequency buzz affecting humans even when it is inaudible.

Give Us Your Acres

Data centers of the future require vast acreage, so construction is naturally shifting toward rural areas. Concerns are mounting over the rapid conversion of farmland into industrial sites because farmland loss is usually permanent and significantly affects food production. In addition, profligate water use will affect the water table, and the arrival of power grid infrastructure and industrial activity could lead to the destruction of wetlands, grasslands, and ecosystems.Farmers are reporting—and refusing—tempting offers for their land, a generational asset to which they are deeply attached. Offers from Fortune 100 companies run into the double-digit millions. One offer for a Kentucky farm, where an undisclosed industrial development was planned, was $10 million, five times what the owner paid 30 years ago. Another farmer was told to name any price. Yet another was offered $33 million and told that details about the project would be provided if she signed a non-disclosure agreement.

The question is: How long will they be able to resist? With President Trump pushing for America to become an AI superpower, data centers are unlikely to be stalled. Staunch Trump supporters and Republicans in rural areas, already hurt by retaliatory tariffs from China and Canada, are unhappy. They are questioning and opposing this relentless encroachment. Even in cities and suburbs, data centers compete directly with residential development, driving up land prices and reducing the number of viable housing sites. In northern Virginia, data centers accounted for a disproportionate 30% of land development between 2013 and 2021. These trends, which will likely be seen in all states soon, will jeopardize the housing supply.

Give Us Your Power

Data centers are the most energy-intensive building types, consuming 10–50 times more energy per square foot than a typical commercial office. A single AI data center can use as much power as 100,000 homes, but the massive ones coming up can use up to 20 times that amount. In fact, by 2030, power demand is projected to reach 130 gigawatts—a gigawatt equals a million megawatts—about 13 times New York City’s peak summer power demand and 25-30% of the United States’s average power usage.Data center power consumption is set to triple, from 4% of U.S. usage in 2023 to 12% in 2028. Data centers aim for a PUE of 1.4–1.5 (power usage effectiveness), which is easier to understand as 67% of total consumption going to IT equipment. This is much better than general computing centers, where PUE is 2, meaning only 50% of the power consumed powers IT equipment. But general computing uses only 10–50 kW for smaller centers, up to 2 MW for campus-level hubs, and up to 5 MW for corporate centers.

Take Pollution in Return

The thousands of server racks in data centers must be cooled to prevent overheating and failure, requiring massive cooling systems of two types: immersion and water circulation. The first immerses equipment in special dielectric fluids, which can pose health risks from exposure. Water-based systems pollute the environment because their discharge contains coolants, biocides, corrosion inhibitors, concentrated minerals, and heavy metals. Noise from data centers reaches 96 decibels (dB) inside facilities, while generator noise can reach 105 dB, comparable to a jet flying overhead.By comparison, noise levels in quiet neighborhoods are 45–55 dB, and in mixed-use neighborhoods, 55–65 dB. Chronic exposure to noise above 65 dB can cause hypertension, headaches, nausea, insomnia, dizziness, and cardiovascular issues. Diesel-fueled backup generators at data centers emit nitrogen oxides (NOx), carbon monoxide, and particulate matter (PM2.5), all linked to asthma, respiratory disease, and heart disease. Communities near these facilities experience higher air pollution levels than the rest of the country. The power supply will be slow to meet demand, so data centers may rely more on backup generators, increasing pollution. P

roliferation and Opposition

The proliferation has begun. Virginia, which has 320 data centers, the most in the U.S., expects a total of 954. Texas will eventually surpass Virginia with 962. Northern Virginia houses 50 million square feet of data center space, has earned the moniker Data Center Alley, and serves as a backbone for Big Tech and AI development. The opposition has also begun. People have protested the noise and the constant hum from data centers in northern Virginia. There is also a surge in efforts to block data center construction, especially projects planned near residential areas. In northern Virginia, Blackstone was forced to abandon its 22 million-square-foot facility at the Prince William Digital Gateway.Time for a Rethink

A Reuters/Ipsos survey found that 57% of respondents opposed data centers, while a Gallup survey found that seven in 10 opposed them. Across almost all 50 states, there’s a move toward moratoriums on building data centers as concerns about their potential impact grow. New York, Georgia, Oklahoma, Vermont, and Virginia have introduced legislation to impose moratoriums or bans on new data centers.President Trump has strongly advocated data center development as a means to make America the AI leader. Other politicians have promoted data centers to drive economic growth. But they must reconsider, as data centers are now a political liability with voters.

https://twitter.com/DRPOOLQ17/status/2079351525286023495?s=20

For years, Anthony Fauci has dodged, deflected, and hidden behind a pardon.

— Rand Paul (@RandPaul) July 21, 2026

On July 29th at 8:30 am, that ends. Fauci will finally testify before my committee.

Mark your calendars. pic.twitter.com/eWyumReVyf

This product that everyone thinks is never going to happen is going to be the product that bankrupts Uber pic.twitter.com/b9vzFrscje

— Teslaconomics (@Teslaconomics) July 22, 2026

Support the Automatic Earth in wartime with Paypal, Bitcoin and Patreon.

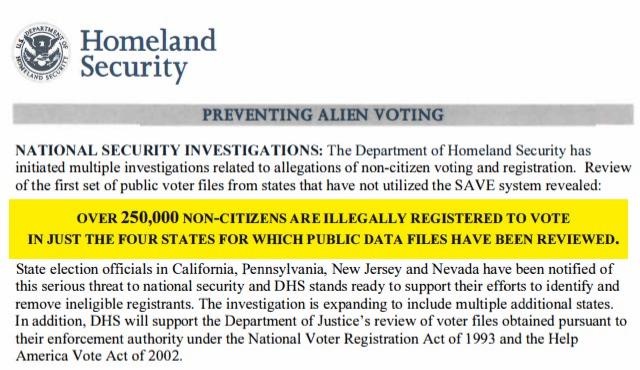

DHS Document (highlight added).

DHS Document (highlight added).