John Vachon Liquor store, Palacios, Texas May 1943

An amusing discussion is firing up ever more about what the ECB should do in the face of a – perceived or not – deflation threat. Many voices are clamoring for immediate action, claiming Mario Draghi et al may well already be too late, or even use words like “the spectacular idiocy of EMU policy”, as Ambrose Evans Pritchard does, who’s been on the topic for a very long time. IMF’s Christine Lagarde is a little less impolite and says: “More monetary easing, including through unconventional measures, is needed in the euro area.” Draghi yesterday showed an unexpected sense of humor when he responded to Lagarde: “The IMF has been very generous in its suggestions on what we should do.”

The vast majority of the “pro-action” favors the ECB engaging in US-style QE and seems to be predicated on the assumption the US QE has been a great success. But is it? The US jobs report that was just released proved to be another disappointment. Between population growth and the millions of people hovering in the grey area of looking but not looking, of having given up but someday might come back, any jobs growth number that comes in under 200,000 barely adds any jobs at all. And that is despite more trillions of dollars in QE stimulus than just about anyone is capable of calculating anymore.

One could argue a good case that QE US-style has far more zombie qualities than anyone should feel comfortable with. And that’s just a start. QE has boosted banks’ reserves with the Fed, making them look healthier than they really are, and inflated asset markets like stocks, real estate and land to fresh record levels even as so many more millions of Americans are out of work, working low-paying jobs or simply up to and over their necks in debt. And now, after 5-odd years of such raving success for the banking system but blatant failure for the American population, Europe should imitate this?

I’m not so sure that Draghi wouldn’t have gone the QE route if he could. But perhaps he can’t. Perhaps the issue at hand is that he has to contend with 28 different constitutions in the European Union. Whereas the Fed only has to flaunt one. As per former Reagan government official and fund manager David Stockman, who concludes an article this week whose title I shortened for our Daily Links to “The Fed’s Fiscal Circle Jerk” but which was originally called Yellen’s Dog Is Eating Homework Congress Didn’t Even Assign: Reflections On The Greatest Mission Creep Ever , says:

The Fed has seized power and is not about to let go – common sense be damned, and the constitution, too.

Stockman takes zero prisoners in explaining why in his view the Fed’s policies, QE and all, are as illegal as can be. Europeans would do well to take note, lest Draghi and/or the Brussels made men find a legal loophole around existing legal constraints to stimulus and monetary easing.

America is being run by an unelected gang of essentially self-perpetuating PhDs. The notion of an economics coup d’état is not so far-fetched. After all, the Eccles Building controls the levers of the nation’s fiscal policy; is the pied piper of the entire financial system; intentionally inflates financial bubbles which powerfully impact the distribution of wealth and income; and is the master builder of the nation’s towering edifice of $59 trillion in credit market debt that flattens growth, jobs and incomes on Main Street.

… the Fed’s QE policy amounts to a giant fiscal fraud. Even if it sticks to the taper, the Fed’s balance sheet will have expanded by 5X – from $900 billion to $4.5 trillion—in 70 months. Yet it has no intention whatsoever of unwinding this stupendous emission of fiat credit. Indeed, selling-down its massive piles of treasuries and MBS would ignite the mother of all melt-downs in the fixed income markets, which have gorged on over-valued paper that was priced by the Fed’s huge, artificial bid in the debt markets.

In other words: say goodbye to your pension. The Fed has taken it by incentivizing funds to buy zombified assets that will one day, we don’t know when but we do know why, implode.

So if this $4.5 trillion balance sheet is permanent, then the Fed’s post-crisis money printing spree amounts to a massive monetization of the public debt. To be sure, all of this was done in the name of rubbery abstractions like “accommodating” recovery, supporting the “labor market” and “stimulating” consumption and investment spending, but the real world effect was quite different and far more tangible: It allowed Washington to treat the financing cost of our $17.5 trillion national debt as a free good. In a world in which even the official inflation rate (CPI) has averaged 2.4% during the last 14-years, there is no other way to describe a policy that actually drove the 5-year Treasury note yield to a low of 75 bps, and pulled the weighted average cost of the total Federal debt down to about 2.5%—which is to say, zero, nichts, nada or nothing in real terms.

The meaning of “massive monetization of the public debt” is essentially that the public debt is being transferred to the public. In what Stockman labels a “fiscal circle jerk”. As has been clear since at least the Civil War, the Treasury could have cleared its debt “directly”, without a central bank acting as a middle man. But that would not have allowed for baking secret debt, which is many times higher than federal debt (think derivatives) to be included in the laundry.

… part of this fiscal scam is even more egregious than the Fed’s own acknowledgement that it’s artificially suppressing the treasury coupons. What the Fed is also doing is issuing second-hand “greenbacks”— those notorious non-interest bearing IOU’s that financed the Civil War. Since the crisis the Fed has returned $400 billion of “profits”, including $80 billion each in the last two years, to the US treasury, thereby off-setting upwards of 25% of the interest cost on the Federal debt.

… how is it that the Fed is more profitable than the wholesale, retail, entertainment, food service and hospitality industries of America combined? Self-evidently, its the magic of printing press money: The Fed buys treasuries and MBS with a coupon; pays for them by issuing new liabilities without a coupon; collects the spread which gets recorded as a “profit”; and then returns this ‘profit” to Uncle Sam at year-end. Had the Treasury Department dusted off Lincoln’s playbook, instead, it could have simply issued “greenbacks”, and dispensed with the round trip. In less polite company it might be called a fiscal circle jerk.

A great question that desperately needs to be answered: ” … how is it that the Fed is more profitable than the wholesale, retail, entertainment, food service and hospitality industries of America combined?” Answer it and you know what QE is: a scheme to let the government get ever deeper into debt “for free”, while at the same time propping up too big to fail bankrupt Wall Street zombies. And who do you think ends up paying?

Don’t be surprised if it all turns out to be an elaborate plan to pull the plug at a handpicked moment designed to unload all losses on the greater fools (re-)entering stock markets and housing in ever greater numbers. It’s a good idea to try and stay away from conspiracy theories, but just look at what’s happening here. Huge piles of debt are added to already historically large amounts of it, and all America has to show for it are weak jobs reports like the one issues today. Shouldn’t that make you wonder?

Based on its historic rate of expansion the Fed’s balance sheet would be about $1 trillion today. So during the past 70 months, the monetary politburo has issued about $3.5 trillion worth of Abe Lincoln’s “greenbacks”. But here’s the thing: Even as Lincoln took many matters in his own hands like suspending habeas corpus, closing newspapers and imprisoning dissenters, he did bother to get an act of Congress to print his paper money. And as much as the beltway bandits of today’s Washington have enjoyed the quasi-free financing of $9 trillion in new public debt since the crisis – even they would have never passed something called the “Greenback Authorization Act of 2009″.

At some point it might be appropriate to ask what exactly Congress is doing while this plays out. Stockman claims that it would have never passed a repeat of Lincoln’s plan, but doesn’t that mean that it should act, or have acted, now the Fed does just that through other means, and at much higher cost the people?

Then consider the orgy of debt issuance in the business sector. During the last year, every single record from the 2007 blow-off top has been exceeded. This encompasses $1.1 trillion of investment grade corporate debt, including a staggering $49 billion issue by Verizon to fund what was essentially an LBO of its own subsidiary. Next in line is about $600 billion in leveraged loans – more than 60% of which have been “cov-lite” style spit and prayer loans. And then there are $400 billion of new junk bonds proper, along with the return of that bell-ringer for speculative tops called leveraged recaps, wherein the LBO barons freight down their debt mules with even more debt in order to pay themselves a dividend.

In all, business sector debt stood at about $11 trillion on the eve of the 2008 crisis, and has now vaulted upward to $13.5 trillion. Yet nearly the entire gain has gone into the preferred financial engineering games of bubble finance—namely, LBOs, cash M&A deals and stock buybacks. Indeed, in the latter case the big corporates are now borrowing hand-over-fist to fund buybacks at nearly a $1 trillion annual rate. Compare that to investment in productive plant and equipment where real outlays are still running $100 billion or 8% below its late 2007 level.

At what stage do people making out like bandits get to be recognized for what they are, which is bandits? Is that only after the regime that allowed for them to do it gets toppled?

Needless to say, this massive leveraging and stripping mining of cash from the business economy is not the unseen hand of the free market at work. It is the consequence of the Fed’s very visible pegging and rigging of the financial markets. Fast money speculators are subsidized by the Greenspan/Bernanke/Yellen put, which drastically compresses the cost of market risk insurance and artificially fattens the margins on carry trades.

Maybe the cruelest part of this is that as people are glued to their new plasma screens, their homes are robbed empty behind their backs, and they repeat after their flat 2-D gurus that their lives are getting better. It’s the ultimate con-man’s dream: not just taking your dupes for all they have, but convincing them they benefit as you do it. They’ll be happy to let you take some more.

Likewise, also come the $5k Wall Street suits – streaming into America’s busted sub-prime neighborhoods fixing to become single family landlords. Yet without the Fed’s gift of cheap financing, there is not a snowball’s chance that these clueless spread-sheet jockeys would own a single, single-family home— let alone upwards of 500,000 at last count.

In short, the Fed has interposed itself throughout the very warp and woof of the nation’s business economy. It does this in a manner that makes a mockery of our purported mechanism of economic governance—that is to say, the spontaneous actions and decisions by millions of producers, consumers, investors and savers on the free market in response to honest price signals arising from the vineyards of commerce and industry. Instead, in a manner like the “caribou” soccer of 6-years olds, today’s economic actors have no choice except to ceaselessly chase the Fed around the economic fields.

Yeah, this is how US home prices are kept from scraping the gutter and letting millions of home “owners” default. The question is how long do you think it will last? There can’t seriously be anyone who thinks “they can do this forever”. Wouldn’t it make more sense that since “their” interests are 180 degrees different from yours, at some point in time they’ll be coming to take it away from you?

So where did the Fed get this mind-boggling grant of plenary power? Fed Chair Yellen explained it succinctly in a recent speech:

The U.S. economy is still considerably short of the two goals assigned to the Federal Reserve by the Congress of low and stable inflation and maximum sustainable employment.

Yellen was obviously referring to the Humphrey-Hawkins Act of 1977 – one of the most pernicious pieces of legislation ever enacted, and one I am proud to say I voted against as a freshman Congressman. Yet even in those halcyon days of Keynesianism, few in Congress believed that they had mandated the Fed to pursue rigid quantitative targets for inflation and unemployment – let alone precisely a 2% annual gain in the PCE less food and energy or 6.5% on the U-3 measure of unemployment, which didn’t even exist then.

By contrast even the voluble Senator from Minnesota saw the law as essentially an expression of congressional sentiment that it would be swell to have more jobs and less inflation. And most certainly, the Congressional majority that passed the act did not in its wildest imagination foresee that the route to the quantitative inflation and unemployment targets it didn’t mandate would be through the canyons of Wall Street and the made-up monetary doctrine of “wealth effects” as the surest route to their achievement.

Well, that may be true, David, but the Congressional majority are still sitting on their hands as it does indeed happen, like so many of those see nothing hear nothing monkeys. You can argue that they didn’t see it coming, but they can see it now …

So the last 35 years have brought the greatest exercise in mission creep ever undertaken by an agency of the state. That explains why the monetary politburo persists in its absurd quest to force more debt into an economy which is already saturated with $59 trillion of the same. To pretend, as does Yellen and most of the monetary politburo that they must plow ahead printing money at lunatic rates because Congress so mandated it, is the height of mendacity.

The Fed has seized power and is not about to let go – common sense be damned, and the constitution, too.

I hope you’ll let Stockman’s words sink in; that would be helpful when trying to understand why things may look up while they’re sinking fast and furious. And I wonder what Mario Draghi thinks about this. What can he do if he concludes he really can’t monetize the public debt of 28 different countries with 28 different constitutions? Lower interest rates? Yeah, right. There’s only one thing he can do, and he never will: restructure the debt of banks and nations alike. The option must appear to him in sleepless nights sometimes. Maybe a lot lately.

U6 even rose. What a incredible failure US fiscal policy is.

• US Jobs Report Misses Expectations (BI)

The March jobs report is out. The U.S. Bureau of Labor Statistics estimates 192,000 workers were hired to nonfarm payrolls in March, below Wall Street’s consensus forecast of 200,000. The entire gain was comprised of private-sector hires. February’s number was revised up to 197,000 from 175,000.

The unemployment rate was unchanged at 6.7%, defying the consensus estimate of a tick down to 6.6%. The labor force participation rate rose to 63.2% from 63.0%. The underemployment rate (U-6) rose to 12.7% from 12.6%. Average weekly hours worked rose to 34.5 in March from 34.3 in February. Average hourly earnings were unchanged after posting a 0.4% advance in February, missing expectations for an additional 0.2% rise. The year-over-year growth rate ticked down to 2.1% from 2.2%.

Well, nice headline …

• Draghi Talks QE, But Counts On Easter Bunny (MarketWatch)

European Central Bank President Mario Draghi did his best to talk down the euro on Thursday, touting discussions among policy makers on everything from rate cuts to negative deposit rates to, the big bazooka, quantitative easing. Indeed, Draghi offered up virtually the whole arsenal of conventional and unconventional policy measures the central bank could use if it ever becomes convinced that inflation will remain too low for too long. “There was an ample and rich discussion,” Draghi said.

The euro, which, to the ECB’s apparent chagrin, had traded near a 30-month high in the wake of Draghi’s news conference a month ago, duly fell, though it wasn’t a complete rout. Stocks perked up on the prospect of the ECB finally joining the asset-purchase party as the Fed grabs its coat and prepares to leave. Still, it’s hard not to sense reluctance below the surface. After all, while Draghi elaborated on the measures the ECB could deploy, an “ample and rich” discussion doesn’t really seem to imply there was a broad agreement on the merits of undertaking radical action.

And while Draghi emphasizes that policy makers are on high alert over the perils of prolonged low inflation, his opening statement offered no change in language describing how policy makers view the price outlook, saying that inflation expectations “over the medium to long term continue to be firmly anchored.” An unexpected March drop in the annual euro-zone inflation rate to 0.5% — well below the ECB’s target of near but just below 2% — was a jolt. Draghi didn’t put the entire blame for the drop from 0.7% in February on special factors, but he did argue that low energy prices and the timing of Easter needed to be take into account.

Draghi said inflation is expected to pick up in April partly due to volatility around service prices in the months of around Easter. He said inflation is expected to remain low through 2015 before pushing back toward levels closer to 2% toward the end of 2016. Draghi is the undisputed world champion of jawboning, as attested by the lasting drop in borrowing costs for Spain and Italy after his mid-2011 pledge to do “whatever it takes” to preserve the euro. (While that was followed by the creation of the ECB’s Outright Monetary Transactions program, the OMT has yet to be used.)

Bini Smaghi is old school ECB. Wonder what he did to get thrown out. Hardly anybody does down there.

• ECB Action ‘Couple Of Months’ Away (CNBC)

European Central Bank (ECB) President Mario Draghi is preparing the way for monetary easing, a former member of the central bank told CNBC on Friday, despite some dismay after the ECB’s failure to act this week. The ECB opted to hold its key interest rate at 0.25% on Thursday, as well as keep the rate on its deposit facility at zero. This was despite calls from the likes of the International Monetary Fund’s Christine Lagarde for action to combat disinflation, after euro zone inflation slipped to a 52-month low of 0.5% in March.

Lorenzo Bini Smaghi, an ex-member of the ECB executive board, forecast easing was coming, and said the delay was due to attempts by Draghi to build unanimity for action among the Governing Council’s 24 members. “I think he is gaining time for the argument to be won within the council,” Bini Smaghi told CNBC on Friday, from the Ambrosetti Forum in Italy. “The ECB is a bit different as a central bank; it needs to create a consensus, because a move by the ECB with a consensus is more credible than a move with a divided council. I think he needs the decision to mature within the Governing Council.”

Despite the inaction, Draghi emphasized in his news conference on Thursday that the ECB could act swiftly to instigate “unconventional” policy measures if necessary. He also flagged that both quantitative easing and negative deposit rates had been discussed at this week’s meeting. Bini Smaghi predicted that easing would materialize in “a couple of months”. “I think he is preparing the markets to understand that action will take place,” Bini Smaghi said. “Inflation is low; the exchange rate is high. So the time for action should be coming soon… Especially for debt reduction, for the deleveraging process, low inflation is really bad.”

Despite Smaghi’s confidence, economists were divided as to whether Draghi’s comments on Thursday signaled raised intent of instigating easing measures. Lee Hardman of Bank of Tokyo-Mitsubishi was in the yes camp. “The ECB clearly signaled that it is prepared to utilize unconventional monetary policy easing,” Hardman said in a research note on Friday. He added: “The increased likelihood of the ECB adopting more effective monetary easing measures ahead, which could lift inflation expectations and lower real yields, have increased downside risks for the euro.” However, Daiwa Capital Markets forecast policy would remain unaltered, based on Draghi’s Thursday comments. “While the ECB arguably remains excessively timid, we continue to expect policy to remain unchanged over coming quarters,” said Grant Lewis, Daiwa Capital Market’s head of research, in a note.

More insights from Stockman.

• Christine Lagarde Is Clueless: 70 Words Of Pure Keynesian Claptrap (David Stockman)

The world’s official economic institutions are run by people who believe in monetary fairy tales. The 70 words of wisdom below from IMF head Christine Lagarde are par for the course. She asserts that a new jabberwocky expression called “low-flation” is the main obstacle to higher economic growth in Europe and the DM areas generally and that it can be cured by more central bank money printing.

“The first obstacle is… the emerging risk of what I call “low-flation,” particularly in the Euro Area. A potentially prolonged period of low inflation can suppress demand and output—and suppress growth and jobs. More monetary easing, including through unconventional measures, is needed in the Euro Area to raise the prospects of achieving the ECB’s price stability objective. The Bank of Japan also should persist with its quantitative easing policy.”

Now there is not a shred of credible evidence that prolonged low CPI inflation causes workers to produce less, businesses to invest less or entrepreneurs to invent less. Since these are the fundamental ingredients of economic growth on the free market, the question recurs as to why Keynesian Kool-Aid drinkers like Lagarde (and the huge staff of IMF economists she lip-syncs) apparently believe that eroding the value of savings by say only 1% per year vs. 2% will “suppress demand and output”.

Obviously, even they can’t believe that falling prices alone cause “demand” to falter. After all, the price of flat-screen TVs, iPads and iPhones have plunged during the past several years, but demand has soared. During the past 27 months, for example, Apple’s revenues have surged from $29 billion to $58 billion per quarter.

And its not just tech gadgetry, either. Wal-Mart has been driving down the price of furniture, toasters and house-paint for years now, but it has never once complained that its revenue growth–which has been relentless for decades—-has been impaired because its customers are holding-off for even lower everyday prices next period. Indeed, at the product and commodity level the “low-flation” notion is positively ridiculous. US auto sales of 17 million annually in 2005 plummeted to about 11 million by 2009, but that was due to falling incomes and impaired credit status among marginal car buyers. During that period auto prices were not falling but steadily rising.

Ambrose is certain that Draghi is stupid. But while deflation is a serious threat, full-throttle QE is too.

• Immobile ECB ‘Playing With Fire’ As Deflation Draws Closer (AEP)

The European Central Bank has finally opened the door to quantitative easing after years of resistance, but brushed aside calls for immediate action to shore up southern Europe and avert a Japanese-style deflation trap. Mario Draghi, the ECB’s president, said the governing council had agreed unanimously to take emergency measures if inflation falls too low, a crucial signal that Germany’s two members will back the plans under certain conditions. “There was a discussion of QE: it was not neglected,” he said. Yet the bank left interest rates on hold at 0.25% and once again delayed cutting the deposit rate below zero, a step already taken by Denmark to boost lending and deter capital inflows.

Inflation fell to 0.5% in March, the lowest since the financial crisis in 2009. It is below the 1% level deemed to be the “danger zone” by Mr Draghi himself, yet the ECB has held five consecutive meetings without taking any further measures. This has allowed “passive tightening” to run its course as the euro rises. “The ECB is playing with fire by failing to act,” said Ashoka Mody, former head of the International Monetary Fund’s rescue mission in Ireland. “Europe faces an extremely serious problem and the window is basically closing for the peripheral economies. The inflation rate in Italy and Spain is now so low that it calls into question their ability to service their sovereign debts. They need 2% inflation to make it,” he said.

The IMF’s Christine Lagarde said this week that the world in in danger of a “low-growth trap” and called on the ECB to step up to its responsibilities. “More monetary easing, including through unconventional measures, is needed in the euro area,” she said. Repeated criticism from the IMF is ruffling feathers in Frankfurt, where the ECB’s hardliners view bond purchases as a covert rescue for countries that live beyond their means. “The IMF has been very generous in its suggestions on what we should do,” said Mr Draghi in a sarcastic tone.

Mr Draghi admitted that the ECB was caught off-guard by the sudden dip in inflation last month but insisted that the figures had been distorted by the timing of Easter. Inflation is expected to rebound in April and climb back slowly towards the bank’s target of 2% by late 2016. Lars Christensen, from Danske Bank, said Mr Draghi is trying to soothe markets and talk down the euro without doing anything. “The discussion over QE is meaningless when they haven’t even cut interest rates to zero or exhausted their normal tools,” he said. “Unless there is a real change in monetary policy, the eurozone will head into deflation and a Japanese scenario. The longer they keep saying that a revival of inflation is just around the corner, the harder it will be in the end,” he said.

More Ambrose. He loves QE.

• ECBs Deflation Paralysis Drives Italy, France And Spain Into Debt Traps

The European Central Bank has let it happen. Deflation has been running at an annual rate of -1.5% in the eurozone over the past five months, when adjusted for austerity taxes. Prices have been falling at a pace of 6.5% in Greece, 5.6% in Italy, 4.7% in Spain, 4% in Portugal, 3% in Slovenia and nearly 2% in Holland since September, based on my rough calculations (annualised) of Eurostat monthly data. The rise of the euro against the dollar, yen, yuan and the currencies of Brazil, Turkey and developing Asia, account for some of this imported deflation. Euroland’s trade-weighted index has risen 6% in a year.

But that is no excuse. It is the direct consequence of the ECB’s own monetary policy. Frankfurt could force down the euro at any time by signalling a determination to do something about its predicament. It has chosen not to do so, hoping that a few dovish words spoken without conviction will somehow turn the global tide. It is hard to judge at what point deflation becomes embedded in the system. Factory gate prices have been slipping since mid-2012. The pace quickened to -1.7% in February, the steepest decline since the Lehman crisis. But this time it is not the one-off effect of a financial crash. It is chronic, and more insidious.

Professor Luis Garicano, from the London School of Economics, said the economic models used to predict inflation seem to be breaking down, leading to serial misjudgments. “They need to take very serious action,” he told the Financial Times. Laurence Boone and Ruben Segura-Cayuela, from Bank of America, say their “inflation surprise” index keeps ratcheting lower as one shock after another hits the eurozone, while their gauge of “deflation vulnerability” has been flashing red for most EMU countries.

The effect is deeply corrosive even if the region never crosses the line into technical deflation. “Lowflation” near 0.5% can play havoc with debt trajectories if it goes on for long, ultimately throwing Europe back into a debt crisis.“The biggest threat to public debt dynamics is weaker-than-expected inflation. Merely lower than expected inflation, not even deflation, would lead to a significant deterioration in countries’ public finances,” they said. The bank said lingering “lowflation” would cause debt ratios to surge by 2018, rising 10%age points in France to 105% of GDP, 15 points in Italy to 148% and 24 points to 118% in Spain.

These countries face a Sisyphean Task. Whatever they achieve through austerity is overwhelmed by the greater power of debt-deflation. The same “denominator effect” – a debt burden rising faster than nominal GDP – would engulf the private sector as well, still the Achilles Heel for Spain, Portugal and Ireland. Moody’s says “lowflation” (0.5% to 1% until 2018) would “reignite concerns about debt sustainability”, tightening the vice on households and companies with fixed-rate debts. It would erode bank assets, risk fresh bank failures and hit life insurers through a mismatch in maturities. “Avoiding outright deflation does not fully shield the euro area from the shock: the combination of low growth and low inflation has significant implications for all sectors of the economy,” it said.

It’s good to note that the fall doesn’t go down in equal parts everywhere.

• About 20% of China’s Economy Is Shrinking: Xie (CNBC)

About 20% of China’s economy is shrinking and 80% is growing moderately, according to independent economist Andy Xie. Xie told CNBC Asia’s “Squawk Box” on Friday that a credit bubble in China’s economy is deflating, slowing, leading to weaker growth momentum.

China, the world’s number two economy, has not had a great start to the year. Economic data paints a picture of a slowing economy, with this week’s HSBC purchasing managers’ index showing manufacturing activity continuing to contract. Adding to concerns about the economic outlook was the first corporate bond default by a Chinese firm, Shanghai Chaori Solar Energy Science and Technology, last month. That default led to some talk about whether China is facing a ‘credit event’ or a ‘Lehman’ moment, a reference to the collapse of the U.S. investment bank in 2008 that contributed to the global financial crisis. “China’s credit event is not like the one we saw in the U.S.,” said Xie.

“When a credit bubble deflates, an economy is going to be in difficult shape for a long time. China is in better shape than most because China still has an export machine that depends on global demand. Household consumption is small part of GDP (gross domestic product) but it is stable,” he added. Xie said China’s economy was probably not growing at the 7.5% rate the government targets this year, but would not be drawn on an estimate. China’s economy grew 7.7% in the final quarter of last year from a year earlier, compared with a 7.8% expansion in the third quarter. Xie added that stimulus measures to bolster the economy were probably aimed at boosting sentiment.

• Growth Of China’s Shadow Banking Casts Light On Fault In System (Das)

Chinese debt concerns are complicated by two structural issues – the rise in borrowing by local governments and the increase in the role of the shadow banking system. Both sectors are testament to Chinese entrepreneurial spirit, but also point to deep problems in the financial system. Outside of security matters or foreign affairs, China’s provinces, regions and centrally controlled municipalities enjoy a degree of autonomy. After the global financial crisis in 2007/2008, the aggressive stimulus measures to boost economic activity required the central government to relax controls on local government spending programmes.

According to the World Bank, China’s local governments have responsibility for 80% of total spending but receive only about 40% of tax revenue. As local governments are not legally allowed to borrow, they created LGFV (local government financing vehicles), also known as UDICs (urban development and investment companies). These special purpose arm’s-length vehicles, which are separate from but owned or controlled by the local government, can borrow. The LGFVs generally borrow funds predominantly from banks (as much as 80% or more), with the remainder raised by issuing bonds or other equity-like instruments.

In recent times, with pressure on banks to curtail loans, LGFVs have borrowed from the shadow banking system. There are now more than 10,000 LGFVs in China, whose exact level of borrowings remains in dispute. There is concern about the quality of the underlying projects financed, which are sometimes expensive, politically motivated trophy ones. Many of the LGFVs do not have sufficient cash flow to service debt, being reliant on land sales and high property prices to meet obligations. Probably more than 50% of LGFVs have unsustainable debt levels.

In recent years, China has evolved its own substantial shadow banking system. There is the informal sector that encompasses direct lending between individuals and underground lending, often by illegal loan sharks that provide high interest loans to small businesses. The larger sector consists of a range on non-banking institutions, which are subject to various degrees of oversight. It involves direct loans of surplus funds by companies to other borrowers or trade credit (often for extended terms). It involves non-bank institutions such as finance companies, leasing companies or financial guarantors.

There are also more than 3,000 private equity funds, funded in part by foreign investors. An unknown number of micro-credit providers, consumer credit institutions and pawn shops provide personal credit. The largest portion of the non-banking institution sector is trust companies and wealth management products (WMPs). Trust companies that control more than $1.8 trillion (£1 trn) – 20% of GDP – finance riskier borrowers and transactions that banks cannot undertake due to regulations. Trust companies raise money from large investors and companies. The major attraction for investors is the high returns: about 9 to 12% a year compared with bank deposits rates in low single digits. After adjusting for the trust company’s fee of 1 to 2% of loan value, the ultimate borrower must pay about 10 to 15% a year for the funds, well above the 7 to 8% charged by banks.

Use Chinese zombie capital to prop US home prices up. What’s not to like?

• Zillow to Give Chinese Homebuyers Access to U.S. Listings (BusinessWeek)

Zillow Inc. agreed to make its U.S. property listings available to Chinese consumers through a partnership with a Beijing-based website. E-House Holdings Ltd.’s Leju real estate site will carry Zillow listings that include homes for sale by agent and owner, units in projects under construction and foreclosures and short-sale properties, Seattle-based Zillow said today in a statement. Chinese buyers spent more than $11 billion on U.S. real estate last year, with an average $425,000 purchase, Zillow said. The Leju-Zillow site, to be operated by the U.S. company, will be ready around midyear, according to the statement.

“Brokers and agents with listings on Zillow are now able to reach Chinese home shoppers who are ready to invest in the U.S. market, with no additional cost or effort,” Errol Samuelson, Zillow’s chief industry development officer, said in the statement. Zillow is seeking to expand usage on mobile devices for StreetEasy.com, its New York City listings site, as more apartment hunters and homebuyers shop while on the go, Chief Executive Officer Spencer Rascoff said in an interview last week. The company plans to reintroduce StreetEasy for the iPhone and add mobile applications for Android and iPads, he said.

Ha ha ha!

• Americans Only Take Half Of Their Paid Vacation (MarketWatch)

Americans are so busy looking over their shoulders at work, they only take half of their paid time off, according to a study released Thursday. Employees only use 51% of their eligible paid vacation time and paid time off, according to a survey of 2,300 workers who receive paid vacation. The survey was carried out by research firm Harris Interactive for the careers website Glassdoor. What’s more, 61% of Americans work while they’re on vacation, despite complaints from family members; one-in-four report being contacted by a colleague about a work-related matter while taking time off, while one-in-five have been contacted by their boss.

Workers appear to be getting more skittish when it comes to asking for time off. Although this is the first time Glassdoor asked questions about paid vacation and time off, a separate survey, “Vacation Deprivation,” carried out by Harris Interactive for travel site Expedia, shows that Americans left four days on the table within the past year, twice as many as in the previous year. That’s the equivalent of over 500 million lost vacation days per year.

Most American workers receive around 10 paid work days a year and six federal holidays, according to the Center for Economic and Policy Research, a nonprofit left-of-center think-tank in Washington, D.C. So based on Bureau of Labor Statistics’ current average weekly earnings, they’re leaving more than $1,300 on the table by only taking half their paid time off. Workers in the European Union are legally guaranteed at least 20 paid vacation days a year — and 25 or even 30 days a year in some European countries.

People not used to taking time off may not understand that paid vacation is actually built into their compensation package. Under the The Fair Labor Standards Act , the U.S. is also one of the few developed countries that doesn’t require employers to provide paid time off (see chart). Still, 91% of full-time U.S. workers receive paid vacation, according to the Center for Economic and Policy Research, but only 49% of low-wage workers – those in the bottom fourth of earners – get paid vacation.

Money line: “Mikhail Gorbachev, the Soviet president at the time, confirmed that there was a promise not to enlarge NATO” …

• The Expandables: How NATO ‘Conquered’ Europe (RT)

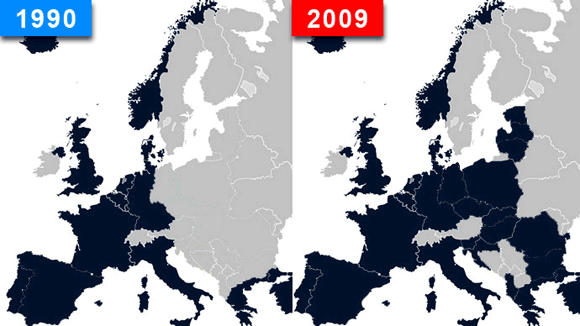

On the 65th anniversary of NATO, the debate over the organization’s expansion remains highly contentious, with some viewing it as a broken promise to Russia after the fall of the Iron Curtain. NATO, an intergovernmental military alliance based on the North Atlantic Treaty, was signed on April 4, 1949 when the US, Canada, Portugal, Italy, Norway, Denmark, and Iceland joined the members of the Treaty of Brussels to form the North Atlantic Treaty Organization.

The idea of the alliance was to provide defense against a prospective Soviet invasion. In the early 1950s, the focus of the communism vs. capitalism fight shifted to Asia, where a series of bloody proxy wars played a major role in convincing Europeans that the Soviet Union and its allies were extremely dangerous and had to be contained at all costs. Since the reunification of Germany, NATO has almost doubled in size – from 16 member states in 1990 to 28 currently. Most senior Russian officials feel tricked by NATO and accuse the West of not following through with its commitments made during German reunification negotiations, when NATO agreed not to expand to the East.

Mikhail Gorbachev, the Soviet president at the time, confirmed that there was a promise not to enlarge NATO, not even “as much as a thumb’s width further to the East.” But this commitment was never formally documented, and since then the alliance has grown drastically. The US ambassador to Moscow at the time, Jack Matlock, told RT he personally objected to NATO expansion as it was done. “We had no reason to expand the NATO military organization to the East until we had an agreement that would put Russia in a European defense structure,” he told RT’s Sophie Shevardnadze.

Still the only sane voice in America when it comes to Ukraine.

• Ron Paul: US Imposes Sanctions ‘Too Casually’ (RT)

Introducing sanctions against Russia is a faulty idea by the United States because it will encourage further backbiting between the two nations, former US congressman Ron Paul told RT. “If two countries get in war, one of the most important things they do is put on blockades, they prevent trade so the various countries can’t get their raw products,” he said. “What I keep thinking is why don’t we try to see it from the other perspective: How would we react if we couldn’t import something? What if China or Russia or somebody came in and said you cannot import certain things or we’re going to prohibit you from trading? And yet we too casually do that with others.”

Paul, the face of modern libertarianism and a former Republican presidential candidate, spoke to RT weeks after Crimeans voted to secede from Ukraine and join Russia. American lawmakers have decried the vote as invalid, calling it an annexation and violation of international law, and have introduced sanctions against the Russian economy. “Any type of sanctions or retaliation is detrimental to both sides. I’ve often thought that if people understood what was going on they’d express objections to these kinds of bickering back and forth,” the former congressman continued.

Paul said the geopolitical drama does not account for individual Ukrainians. “Governments get involved and they do dumb things and the people in the middle are always suffering so if they suspend anything it’s the little guy who usually gets punished,” he said. “If we’re talking about the average person, people who have jobs, they suffer the consequences and that’s very bad.”

Meanwhile NATO announced it would suspend cooperation with Russia over the ongoing crisis. The decision could affect cooperation on Afghanistan in areas such as training counter-narcotics personnel, maintaining Afghan air force helicopters, and a transit route out of the war-torn country. Other projects around fighting terrorism, drug trafficking, and dealing with the disarmament and non-proliferation of weapons of mass destruction could also be impacted.

Paul, a longtime critic of NATO, said that de-escalation should be the current priority for all parties involved. “I advocate not picking sides, so I see two sides going back and forth and my political position as an American is for our American government [to stop] picking sides and picking governments and interfering with elections,” he said. “De-escalation in my view would involve us minding our own business…in particular the Ukrainian people should be the ones who decide which way they want to go rather than the governments of Europe or even the Russian government for that matter.”

Game on?!

• Russia’s Biggest Bank Halts Foreign Currency Personal Loans (RT)

Sberbank has temporarily suspended giving foreign currency loans to individuals. Experts say other Russian banks are not likely to follow. Russian banks aren’t going to suspend foreign currency loans to individual Russians as they have just simplified credit product operations. Experts suggest Sberbank’s ruble-only loans have a more political character. The bank said its April 1 decision was intended “to optimize the structure of the current portfolio and its stable behavior in the future, in case of any foreign currencies exchange rate fluctuations “.

“The bank preliminarily analyzed the needs of the clients and revealed that the current demand for loans can be completely satisfied with rubles without losing any advantages for the Sberbank products, including stocks offers,” the Prime news quotes Sberbank officials. In 2013 Sberbank issued $50 million of foreign currency loans, which account for 0.07% of the $68 billion loaned. 90% of the foreign currency loans were consumer, 9% mortgage, and 1% was for vehicles.

Not sure we need the World Bank to tell us this, but it’s certainly true.

• Climate Change Will ‘Lead To Battles For Food’, Says Head Of World Bank (Guardian)

Battles over water and food will erupt within the next five to 10 years as a result of climate change, the president of the World Bank said as he urged those campaigning against global warming to learn the lessons of how protesters and scientists joined forces in the battle against HIV. Jim Yong Kim said it was possible to cap the rise in global temperatures at 2C but that so far there had been a failure to replicate the “unbelievable” success of the 15-year-long coalition of activists and scientists to develop a treatment for HIV.

The bank’s president – a doctor active in the campaign to develop drugs to treat HIV – said he had asked the climate change community: “Do we have a plan that’s as good as the plan we had for HIV?” The answer, unfortunately, was no. “Is there enough basic science research going into renewable energy? Not even close. Are there ways of taking discoveries made in universities and quickly moving them into industry? No. Are there ways of testing those innovations? Are there people thinking about scaling [up] those innovations?”

Interviewed ahead of next week’s biannual World Bank meeting, Kim added: “They [the climate change community] kept saying, ‘What do you mean a plan?’ I said a plan that’s equal to the challenge. A plan that will convince anyone who asks us that we’re really serious about climate change, and that we have a plan that can actually keep us at less than 2C warming. We still don’t have one. “We’re trying to help and we find ourselves being more involved then I think anyone at the bank had predicted even a couple of years ago. We’ve got to put the plan together.”

Home › Forums › Debt Rattle Apr 4 2014: The Fed Desecrates The Constitution