Timothy H. O’Sullivan Gettysburg Campaign Army of the Potomac at Fairfax Court House, Virginia June 1863

Ukraine has a new president, or at least someone, Petro Poroshenko, who claims to be. One of the first things to come out of his mouth was that he doesn’t recognize Crimea as being a part of Russia. Still, the good listener knows there were no Ukraine presidential elections in Crimea either on Sunday. So Crimea is supposedly still a part of Ukraine, despite a referendum in which 89% of Crimeans chose not to be, and they get no vote in who gets to be their president either? What does all that mean?

Poroshenko also vowed to bring peace to east Ukraine, something he aims to achieve through violence, as yesterday’s 100 deaths can bear silent witness to. Ukraine has a new president and the first thing he orders, even before being inaugurated, is the killing of more of his own citizens. Petro P. had lofty words about wanting a good working relationship with Russia, but those were only words; why, or even how, would Moscow want to talk to someone who has not even officially been elected yet but already wants to kill ethnic Russians who happen to live just across the border from Russia because of a map redrawn pretty much at random 60 years ago? What about that map permits Ukrainians in one part of the country to kill fellow Ukrainians who live in another part?

If Russia would withdraw its troops, chances are there would be a massacre, if not a genocide. That it cannot do. It cannot allow it either. So what is Poroshenko’s idea? That if he can kill enough eastern Ukrainians the rest will submit to anything he wants? And that Putin will let him? Neither seems even remotely likely, and the president-to-be knows it. What then is behind this? Is he even his own man?

If on teh other hand the US and EU would withdraw from the conflict, after first having told Poroshenko to stop killing his own people, and to, after that, set up a dialogue with all parties involved, at the very least fewer casualties would be the result. But US and EU don’t seem to have any such intentions. Which should tell us all something. For real. The peacemaking efforts from the side of the west have been so few and far between you’d need a search light. Add that to what we know about the west’s involvement in Maidan and the ouster of Yanukovych, the last elected Ukrainian President, add the presence of Blackwater ops on the ground in east Ukraine and CIA and FBI advisors in Kiev, and we get a picture that does not make “us” look very pretty.

Today, unelected – or elected by the west – PM Yatsenyuk spoke for the first time in a while. Yes, he’s still there. So no, Ukraine didn’t get a new government, since none was elected. The shots are still – quite literally – called by the handpicked crew that took over in February, with a heavy presence of Svoboda, the Right Sector and other squeaky clean fine folk. For those who hoped the first thing a new president, the first person in a while with actual legitimate credentials, would tell everyone was to quiet down amidst all the turmoil caused by the different claims to power, no such luck. Willy Wonka wants blood.

It’s up to Obama, and only Obama, now to tell Yatsenyuk and Poroshenko and Blackwater and the various symbol-wielding fractions on their side of the fence to stop doing what they’re doing. They are the agressors here, not the separatists or terrorists or whatever they’re being called, and not Vladimir Putin either. There was never a chance that Putin was going to let anyone threaten the Gazprom pipelines underneath Ukraine soil, and everyone involved knew that from the get-go.

And Putin knew that Yanukovych was an idiot, but he didn’t interfere in internal Ukraine politics. He worked with the guy, to make sure the pipelines were safe. Then Victoria Nuland et al began to fund, to the tune of at least $5 billion, the movement to overthrow the president that they knew all to well included some very questionable elements. Just like the US works with many dozens of regimes that are far worse than Yanukovych when it comes to issues such as human rights. Why then was it so important to topple Yanukovych? It can’t be explained without bringing into play ulterior motives. In this case, these motives are carbon resources. Russia has lots of those, they’re amongst the last few available in the world, and the west wants them. It’s not hard to understand.

What Yatsenyuk said today was that Russia owes Ukraine $1 billion for gas stolen when Crimea chose to join Russia. Reuters quoted a Gazprom spokesman as saying.”We have no idea what he means.” Now, there probably are gas fields below the Black Sea, but they haven’t been developed. And Yats may have had dreams of developing them, but he and all his wastern banker and Big Oil friends knew all along that Russia would never give up its Black Sea access, and without that the fields would not be exploitable. So in making his ‘stolen gas’ claim, Yats gives away at least some of his, and his backers’, reasons to do what they do.

But that doesn’t explain why they feel they have the liberty to go kill fellow Ukrainians. Unless they try to evoke an all out war with Russia and/or topple the elected Russian government. After all, kill enough ethnic Russians and Putin will have to act. And he will. And then we in the west will be treated to more Goebbels inspired stories comparing him to Hitler; there are dozens of examples of that already today, just wait till they make it impossible for him not to act. But it’s not Putin who has expanded his rein westward, it’s the NATO that’s moved east, and at an aggressive pace, after having pledged it wouldn’t. I’ve said it before, we may want to be careful with what we let people do in our name. The dozens of people murdered in Odessa a few weeks ago, and the 100 yesterday in Slovensk, plus all the others in this conflict, would have been alive today if only Obama had said stop. He didn’t, and that puts us on the hook, because he’s our guy.

But perhaps we can put all this on the backburner if the Chinese government attempts to hide its utterly failing economic policies, and the violent unrest that will be the consequence of them, behind more attacks on Vietnamese and Japanese vessels and the occasional island. That sort of development could make Ukraine an afterthought in the media. Not that it should for us though: there are still people being killed in our name there, and we should should shout out loud that we don’t want that to happen. If we don’t, isn’t it obvious we lose our right to speak, let alone shout?!

” … the risks will not only be in the real estate sector. The bigger risk will be in the financial sector. [..] “When housing prices fall 20% to 30%, these problems will be all exposed …”

• Real Estate Tycoon Sees Titanic Moment for Chinese Housing Market (WSJ)

China’s once buoyant property market is facing some rough sailing. In fact, according to one tycoon – Soho China chief Pan Shiyi – the real estate market is looking more like the Titanic headed in the direction of an iceberg. Mr. Pan, the co-founder and chairman of Soho China Ltd., is taking a very bearish view on the housing market, which has struggled this year. In the first four months of the year, home sales were down 9.9% from the same period a year ago in value terms, official data shows. New construction starts — as calculated by area — were down almost 25% year over year in the same period.

As if that’s not bad enough, demand is also weakening in an expanding number of cities as banks tighten mortgage lending and sales are dampened by widespread expectations of price cuts. “I think China’s property market is like the Titanic and it will soon hit an iceberg in front of it,” Mr. Pan told a financial forum on Friday, according to the China Business News. “After hitting the iceberg, the risks will not only be in the real estate sector. The bigger risk will be in the financial sector,” he added. He said serious problems lie with financial products like trust and wealth management products, as well as entrusted loans that charge higher interest rates than banks and are key financing vehicles for the property sector.

“When housing prices fall 20% to 30%, these problems will be all exposed,” he was quoted as saying. Soho China declined to comment about Mr. Pan’s remarks. But in a post on his verified Weibo account Monday, Mr. Pan said that during the forum’s question and answer session, he had first asked whether there were any journalists present before replying to a question about the housing market. Only upon being told there were no reporters present, he said, did he proceed to answer. “I didn’t expect there are countless reporters hiding [in the audience],” he said.

Shillling’s first in a series. Useful data.

• Dear Investors: China’s Problems Are Your Problems (A. Gary Shilling)

I have long argued that it will take a sizable shock to switch the current “risk on” investment climate to one of “risk off.” The robust U.S. stock market persists even though the housing recovery has stagnated, labor markets remain weak, consumer spending is subdued and the U.S. Federal Reserve continues to taper its securities purchases. Yet a financial crisis in China could well be the trigger that persuades investors to pull in their horns. China is the world’s second-largest economy, even if it remains an economic pygmy, with $6,091 in per-person gross domestic product in 2012, compared with the U.S.’s $51,749. Its global importance was magnified when North America and Europe shifted their manufacturing to the Middle Kingdom. That shift made China the primary importer of raw materials and exporter of manufactured goods.

China’s size and impact on the global economy mean that China’s problems – I will identify nine of them in this series – are now the world’s problems. No single issue is likely to cause a major crisis, yet in combination they certainly could. The first and biggest problem is slowing economic growth. Until 2008, China had accelerating double-digit real GDP growth. Then the recession and retrenchment of U.S. and European buyers knocked growth down to 6% – a recessionary rate for China. In 2009, China pumped huge amounts of stimulus into its economy, equal to 12% of GDP or twice the size of the U.S.’s stimulus package that year. China’s version largely took the form of bank lending, which pushed growth back up to double digits but also fueled inflation and a housing bubble. The Chinese government responded with various fiscal and regulatory restraints, and growth dropped back toward its 7.5% target (if you believe China’s vastly inflated numbers).

More important, manufacturing is declining. An index compiled by HSBC Holdings PLC shows manufacturing at 49.7 in May (a number below 50 indicates a contraction). Manufacturing, construction and utilities account for 45% of China’s economy, compared with only 17% in the U.S. It stands to reason that, if manufacturing is declining, the economy is barely growing. The comparable U.S. index is running above 50 – and the U.S. economy is growing at only about 2% annually. Rapid economic growth covers a multitude of sins, especially in a developing country like China where it’s needed to provide jobs and improve living conditions. In contrast, slow growth magnifies economic and social ills. Slow growth also favors those with political power instead of creating a bigger pie that benefits many.

In contrast to the long-term goals of promoting consumer spending, remaking state-owned enterprises and liberalizing interest rates, Chinese officials have recently resorted to the same-old, same-old: infrastructure spending and easy money. Rail and road investments jumped 22% in the third quarter of 2013 versus a year earlier. The government plans to spend $23 billion on five new rail lines and to boost spending on China’s electric grid by 22%. The government also plans to spend more on public housing – 7 million units compared with the five-year-plan’s 5 million to 6 million units. The fiscal deficit, meanwhile, will jump 12.5% to accommodate new spending for social services, the environment and the military.

The coming economic transition the government is planning is the second big challenge. After the recession, Chinese leaders realized their earlier growth model — with an emphasis on exports and the infrastructure that supported it — wasn’t working. Most of its exports were bought by Americans and Europeans. But as those economies continue to deleverage and grow slowly, the game has changed. Now, Chinese leaders want to shift from export-driven to domestic-led growth. But in promoting a consumer-led economy, China is way behind the goal post. The latest data from 2012 show that consumer spending only accounted for about 36% of GDP, far behind the developed countries. Even emerging economies are faring better: Russia’s consumers make up 48% of GDP; India’s are 60% and Brazil’s 62%.

How credible would more stimulus be in China?

• China Interest-Rate Swaps Drop to 11-Month Low on Stimulus Bets (Bloomberg)

China’s interest-rate swaps slid to an 11-month low on speculation monetary policy will be loosened to combat a slowdown in the world’s second-largest economy. Policies will be fine-tuned when needed to solve issues such as any shortage of funds for the real economy, Premier Li Keqiang was cited as saying in a statement on the central government’s website on May 23. New home prices rose in April in the fewest cities in a year and a manufacturing gauge stayed below 50, the dividing line between expansion and contraction, for a fifth month in May, data showed last week.

“The anticipation of easing and the ongoing risk of a larger deterioration in property market should continue to keep Chinese rates low,” Wee-Khoon Chong, Singapore-based head of rates strategy for Asia ex-Japan at Nomura Holdings Inc. “Expectations are rising on the back of Premier Li’s comments.” The cost of one-year swaps, the fixed payment needed to receive the floating seven-day repurchase rate, fell five basis points, or 0.05%age point, to 3.57%. People’s Bank of China Governor Zhou Xiaochuan said the central bank and its local branches must implement prudent monetary policy and create a good monetary and financial environment to support local economic development, according to a statement posted on its website. He made the comments during a May 25-26 visit to a central bank branch in Zhejiang province’s Jiaxing city.

China’s banking assets have grown to over 100% of its GDP in the last three years, according to Bass. If the U.S. had engaged in similar policies – which he said would translate to $17 trillion in lending over that time period – it, too, would have achieved more than 7% GDP growth.

• Kyle Bass: The Looming Crises In Asia And The Fed’s Worst Nightmare (Huebscher)

For the last several years, nobody has been more outspokenly bearish on Japan than Kyle Bass. In a recent talk, Bass reiterated his doubts about Japan’s chances of averting a debt crisis. What’s more, he also said China’s economy will fall below expectations. Bass changed one aspect of his outlook on Japan. Instead of predicting a collapse of the Japanese bond market, he focused on a severe weakening of the yen – without predicting when that might happen. His predictions for China were equally distressing. He said that its banks will be saddled with non-performing loans and that its economy is actually contracting. “I don’t think the markets are discounting what’s really happening in China,” he said.

Bass is the founder of Hayman Capital, a Dallas-based hedge fund. He was featured prominently in Michael Lewis’ recent book, The Big Short, for profiting from investments during the sub-prime crisis, which he accurately predicted. He spoke on May 19 at in San Diego at the Strategic Investment Conference, which was sponsored by Altegris and John Mauldin. I’ll look at Bass’ predictions for Asia’s two biggest economies – and how Bass believes investors can profit from their plights.

China

China’s economy isn’t just slowing down, according to Bass: It’s contracting. While China’s published rates for annual growth are still positive, Bass said the nation’s economic growth was negative from the fourth quarter of 2013 to the first quarter of 2014. That is a result of excessive government spending on unproductive sectors of the economy. Bass said the People’s Bank of China has been more aggressive in its quantitative easing (QE) that the Federal Reserve has, but much of that money has gone into unproductive credit expansion. China’s banking assets have grown to over 100% of its GDP in the last three years, according to Bass. If the U.S. had engaged in similar policies – which he said would translate to $17 trillion in lending over that time period – it, too, would have achieved more than 7% GDP growth.China’s banking assets now total approximately $25 trillion, or almost three times the size of its $9 trillion economy. Its low default rate on bank loans – about 1% – is about to rise, according to Bass. Much of that lending is construction-related. Bass said that 55% of China’s GDP growth has been in the construction sector. The marginal return on those loans must be very small, he argued “A rolling loan gathers no loss,” Bass said, “and that’s what’s been going on in China for the last few years.” He said it is impossible to believe China could “manipulate” the inputs of its financial system without losing control of the outcomes. Deflation is also threatening China. Bass said that its GDP deflator is now below zero. He expects the PBoC to engineer a devaluation of the renminbi as a way to stimulate exports and avert further deflation. [..]

Japan

Bass expects Japan’s reform program to fail. That program is based on “three arrows”: aggressive fiscal policy, which is causing Japan to run a deficit that is 10% of its GDP; aggressive monetary policy, which is the “Abenomic” pursuit of QE that has doubled the monetary base in pursuit of 2% inflation; and structural reform, which Bass said hasn’t happened and isn’t likely. None of those arrows, either individually or in combination, will be sufficient to normalize the Japanese economy, according to Bass. Japan recently instituted a consumption tax, which Bass expects to push inflation up to 3%. But that will cause real yields to be negative, since Japan’s 10-year bond now yields approximately 60 basis points.Bass said that would lead to selling of Japanese government bonds. The Bank of Japan (might step in to buy those bonds, he said, effectively monetizing the debt through QE. Japan’s QE is enormous relative to that of the U.S. Bass said Japan’s is 140% of tax receipts, 170% of its fiscal deficit and 14% of GDP, versus 13% of tax receipts, 62% of fiscal deficit and 2% of GDP in the U.S. But that QE, he contends, will cause the yen to depreciate. “It’s my supposition that at some point in time, once the currency depreciates enough and capital flows leave Japan’s current account that you can’t hold the bond,” he said. “When this happens I don’t know. But I can tell you this: The yen is going to do nothing but weaken from here.” [..]

Implications for the U.S.

With the Fed tapering and both China and Japan’s currencies likely to weaken, the net impact on the U.S. will be deflationary, Bass said. That trend will be accelerated by the improvement in the balance of trade for the U.S., which had its current account deficit shrink due to increased hydrocarbon production. The crucial moment will come when the U.S. reports a sub-6% unemployment rate, meeting the target it has set for normalizing its monetary policy by ending QE and raising rates. He predicted that will come in July. That will be the Fed’s “worst nightmare,” he said.

The stuff used as collateral is now itself losing value. Hence, margin calls must ensue.

• Fresh Lows For China Industrial Commodities (Kurtz)

In spite of what appeared to be an improvement in China’s manufacturing sector, China’s economic picture remains cloudy. A number of indicators point to rising uncertainty and slowing industrial demand. Investors are becoming increasingly uneasy with the nation’s property markets, which JPMorgan called “a major macro risk”. Volumes of unsold real estate are now at record levels and sales continue to slow. Nomura’s researchers are convinced “that the property sector has passed a turning point and that there is a rising risk of a sharp correction”. Of course since the authorities can easily intervene, the situation may not be as dire as Nomura predicts. Nevertheless, the nation’s property markets continue to pose significant risks.

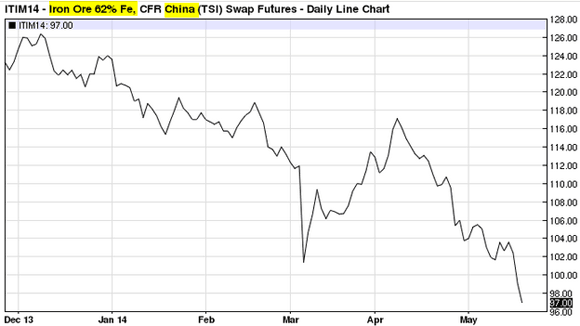

June China iron ore futures contract (source: barchart.com)Moreover, some high frequency indicators are once again flashing warning signals. According to the ISI Group research, exports to and sales in China by US corporations have turned materially lower after remaining stable since early 2013 – indicating weakening demand. Anecdotal evidence suggests that a similar slowdown has also occurred for Japanese and euro area firms selling to China. The most worrying indicators however are the key industrial commodity prices. Futures on iron ore sold at China’s ports fell below $100 for the first time in years.

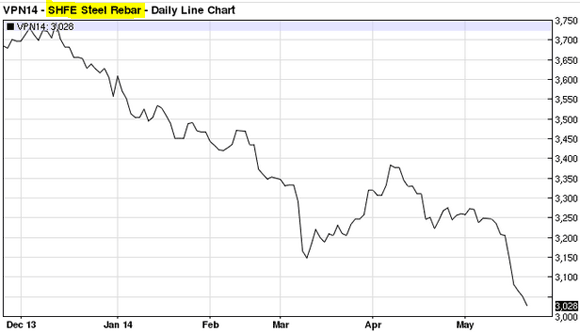

June China steel rebar futures contract (source: barchart.com)And steel rebar futures on the Shanghai exchange are also continuing to fall. Some of these declines are of course related to declining construction activity. Once again, most economists do not expect a “hard landing” for PRC because the government has enormous resources to “backstop” the nation’s economy. Nevertheless, a number of indicators from China still point to persistent risks to growth.

Somethign tells me we’re in for many headlines just like this one.

• China Middle-Class Protests Turn Violent After Petitions Ignored (Bloomberg)

The first time Yan heard authorities planned a waste incinerator near her home in eastern China was when a petitioner gave her a leaflet warning of the pollutants it might spew into the environment. Fearing that the burner might hurt her toddler’s health, the technology worker in Hangzhou petitioned the government to halt the project before joining hundreds of protesters near the proposed site on May 10. Violent clashes erupted as cars were overturned and police vehicles set on fire. “At the start, all people wanted was a way to reflect our concerns and grievances to the government,” said Yan, who is in her 30’s and asked not to be fully identified amid a government investigation.

The Hangzhou demonstrations, which prompted officials to suspend construction of the incinerator, were the third such violent protest in six weeks – a trend that challenges President Xi Jinping’s quest for social stability. The story of how poor government communication there sparked anger and then clashes with police is one being replayed across China as wealthier and better informed residents resist industrial projects more forcefully. “The failure of local governments to consult local communities is a big issue,” said Andrew Wedeman, a political science professor at Georgia State University in Atlanta. “As property owners, professionals, and possibly party members, they feel they should be consulted and it angers residents when they find out that decisions have been made without any prior notice.”

The number of middle class Chinese will almost double from as much as 180 million to about 300 million by 2022, according to a 2013 McKinsey & Co estimate. Rising incomes, growing impatience with pollution, and a worry about “nuisance facilities” affecting home values are empowering more Chinese to push back against projects. So too, Wedeman said, is their demand for transparency and accountability from the ruling Communist Party. In Hangzhou, an hour by train from Shanghai, word of the incinerator spread after a school principal, who has since been detained, spotted a notice on the local government website weeks before construction was scheduled to start. Mass campaigns have succeeded in stopping industrial projects elsewhere. A planned chemical plant in the southern city of Maoming was scrapped last month after protests led to street clashes. In Guangdong province, neighboring Hong Kong, hundreds took to the streets to voice opposition to a proposed crematorium.

Great headline. I’m jealous.

• EU Elections: Dinosaurs Duck First Meteorite (RT)

The latest European elections ought to mark a turning point in the increasingly unaccountable European project but outgoing President Van Rompuy has already made it clear the misgivings of the Euroskeptic minority will be ignored. Thus the two faces of the EU are apparent – democratic platitudes on one side while on the other: dictating an outmoded big government top down approach (which is clearly failing the people). The EU is now the preserve of the 21st century’s DINOsaurs: Brussels’ oligarchs who are ‘Democrats in Name Only’, with a distinctly archaic approach to growth, as demonstrated by their desire to expand the ‘empire’ east (into Ukraine and beyond), despite being unable to deliver coherent prosperity in their own back yard.

Thus the European People’s Party (EPP) alongside the Socialist and Democrat (S&D) parties will maintain their longstanding grand coalition agreement despite the upsurge in Euroskeptic votes. Their ‘grand coalition’ is a variant of electoral dictatorship: ramming through more regulations and above all, ‘more Europe’, at every turn. That the people of Europe are clearly losing their enthusiasm for the EU is irrelevant to the rather archaic structure of the European politburo, busy dictating daft centralized approaches to tractor production while competing economies are driven by high tech innovation.

(In a marvelously absurd outburst last week at a Brussels conference, President Barroso gave a speech on the topic of developing a more entrepreneurial Europe, wondering aloud why so many Europeans emigrants are developing new technology in silicon valley, without bothering to consider that his Jurassic Park of central planning cannot replicate the dynamic freedom from bottom up technological innovation dominant around Palo Alto.) Adding insult to injury in their contempt for European voters’ concerns, the DINOsaurs will soon further endorse their self-imposed democratic deficit. After lavish dinners’ at taxpayers’ expense, EU leaders’ summits will fudge candidates for the various presidencies and commissioner posts. Voters will, as always, be an afterthought in a process where only those pledging blind allegiance to the Europhile mania can be considered for high office.

“Does a viable euro-area ABS market in fact depend upon a hidden transfer union, or can it survive without a subsidy from a federal state?”

• Draghi’s Drive for Asset-Backed Action Rouses Academic Skeptics (Bloomberg)

Mario Draghi’s plans for credit easing may not turn out to be all that easy. In seeking to unblock the supply of loans to the economy by reviving the European market for asset-backed securities, the European Central Bank president risks an unprecedented reach into the functioning of the financial system that could backfire, according to academics including former Bank of England Deputy Governor Paul Tucker. Ten days before the ECB’s next policy meeting, where it is predicted to cut interest rates to stoke inflation, central-bank officials and researchers are meeting in Sintra, Portugal to discuss current monetary thinking. Draghi, who has shown support for measures from negative rates to liquidity injections and large-scale asset purchases, said today that buying packaged loans could reduce the “drag” on the economy.

“I would like to see an example, somewhere in the world, of someone who has successfully securitized small and medium enterprise bonds,” said Stephen Cecchetti, professor of international economics at Brandeis International Business School in Waltham, Massachusetts, and a former adviser to the Bank for International Settlements. “I don’t think this is an easy thing to do.” The ECB is seeking ways to help companies and households access credit to boost prices and sustain the euro area’s gradual economic recovery. While the central bank’s lending survey showed conditions for new loans stabilized in the first quarter, lending to companies and households has been contracting for almost two years. [..] Draghi today held out the possibility that the ECB could purchase such securities outright. As the euro area recovers, credit demand may rise faster than supply because banks are still repairing their balance sheets and capital markets are only slowly developing.

“We have to be mindful of mismatches between these various trends,” he said in his opening speech. “Term-funding of loans, be it on-balance sheet -– that is, through refinancing operations -– or off-balance sheet -– that is, through purchases of asset-backed securities -– could help reduce any drag on the recovery coming from temporary credit supply constraints.” Making packages of loans to companies into an attractive and tradeable investment may not be feasible without some kind of government backing that could distort the market, according to Tucker, who is now a senior fellow at Harvard Business School. “When you say that maybe the ECB should buy this paper, how can you convince the world that it isn’t going to be at subsidized prices?” he said. “Does a viable euro-area ABS market in fact depend upon a hidden transfer union, or can it survive without a subsidy from a federal state?”

Damage control all over the EU.

• EU Austerity Rethink Urged as Voters Back Protest Parties (Bloomberg)

European Union leaders north and south of the economic divide are channeling an anti-austerity electoral backlash as they seek to push the case for an easing of fiscal policy throughout the euro zone. Italian Prime Minister Matteo Renzi’s victory and French President Francois Hollande’s defeat in the European elections united them in seizing on the results to press for an overhaul of the EU’s German-backed budget-cutting model that has held sway since the debt crisis erupted more than four years ago. “Europe has overcome the euro crisis, but at what cost?” Hollande said in a televised address to the nation late yesterday after his Socialists were routed by the anti-euro, anti-immigration National Front. “Europe’s priorities must be growth, jobs, investment.”

As EU chiefs prepared to meet over dinner in Brussels today to discuss the way forward after the unprecedented surge of protest parties across the 28-nation bloc, the momentum for looser fiscal rules was building. With the euro-region’s fragile political stability at stake, political leaders stepped up their demands for more tolerance of public spending as more necessary than ever to head off the anti-austerity upsurge. “We’re asking to change the rules or make them tailored closer to our expectations,” Renzi told reporters in Rome yesterday. “We’re asking to change the approach that Europe has had in recent years.” In Greece, the success of Syriza, which placed first, may help Prime Minister Antonis Samaras by heralding easier debt-repayment terms for the first euro-area country to call for an international bailout in 2010.

Syriza leader Alexis Tsipras told reporters in Greece two days ago that the election results sent a message against austerity “from the country which was chosen to become the guinea pig” of the economic crisis. The yield on Greek 10-year bonds fell 25 basis points to 6.25% yesterday. After a six-year recession that wiped 25%, or €50 billion ($68 billion), off national gross domestic product, Greece recorded a primary budget surplus – which excludes interest and one-time payments – equivalent to 0.8% of GDP last year. “The election result puts Greece in a sweet spot for debt relief negotiations,” said Michael Michaelides, a rates strategist at Royal Bank of Scotland Group Plc in London. “If the debt relief is menial and Europe tries to force Greece to achieve an unrealistic 4.5% of GDP primary budget surplus target via new austerity, then a Syriza victory in national elections is on the cards.”

Marine Le Pen, the leader of France’s National Front, joined the stampede against the established parties’ adherence to austerity, capitalizing on Hollande’s status as the least-popular leader in France’s modern history. Faced with a sluggish growth rate — the economy grew just 0.2% last year – Hollande has been battling to cut his country’s budget deficit to within the EU ceiling of 3% of GDP. Last year, the European Commission gave France an extra two years, meaning that it would have to meet the goal by 2015. With the commission, the EU’s austerity controller, predicting that France will miss its relaxed target without changes in policy, a further extension may be on the cards. “Brussels is damned if it does and damned if it doesn’t,” Nicholas Spiro, managing director of Spiro Sovereign strategy in London, said by phone. “If it shows more leniency toward France, its credibility will suffer further and Germany will be up in arms. But if it keeps pressuring France to speed up reforms, this will play into the hands of Ms. Le Pen.”

France needs Brussels to take a few steps back. Brussels needs that like a hole in the head. As does Germany.

• Hollande Wants Reform Of ‘Incomprehensible’ EU (AFP)

French President François Hollande called on Monday for the European Union to scale back its role in the lives of its citizens after anti-EU parties made sweeping electoral gains across the bloc. In comments with far-reaching implications for the EU’s future, the Socialist leader said the spectacular success of parties like France’s own National Front (FN) reflected how the bloc had become “remote and incomprehensible” for many of its citizens. “This cannot continue. Europe has to be simple, clear, to be effective where it is needed and to withdraw from where it is not necessary,” Hollande said in a televised address to the nation. The comments will be greeted with delight by Eurosceptics who accuse Brussels of meddling in national affairs, and by the likes of British Prime Minister David Cameron, who also advocates a scaling back of the powers currently vested in the European institutions.

But their tone will cause concern among those, particularly in Germany, who believe European integration still has further to run. Hollande’s Socialist Party suffered a humiliating setback in Sunday’s elections for a new European Parliament, registering a record low vote of just under 14% while the FN topped the polls with nearly 25%. The French leader said France remained committed to playing a leading role in Europe, but also acknowledged that the economic austerity of recent years had alienated many ordinary people. “I am a European, my duty is to reform France and to change the direction of Europe,” Hollande added. “Europe, in the last two years, has overcome the euro crisis but at what price? An austerity that has ended up disheartening the people.”

The FN’s surge has left Hollande in dire straits. He is already the most unpopular French leader of modern times and a poll released on Monday revealed that only 11% of voters think he would be a good candidate for re-election in 2017. Le Nouvel Observateur, an influential left-leaning weekly, concluded that: “Hollande no longer has any chance for 2017,” and urged the French left to turn its attention to finding an alternative candidate with a better chance of combating the FN. Sunday’s vote marked the first time that the anti-immigration, anti-EU FN had topped a nationwide French poll.

“What pro-Europeans preached for so long has finally come to pass: European citizens actively engaging in an EU-wide democratic process. But, irony of ironies, they do so to vote against the EU.”

• Europe: The Continent For Every Type Of Unhappy (Guardian)

On the day the Bastille was stormed in 1789, King Louis XVI wrote in his diary, “rien”. Few European leaders will have typed “nothing” into their iPads today, but there is a real danger that, in response to the revolutionary cry across the continent, they will in effect do nothing. Today’s rien has a face and a name. The name’s Juncker. Jean-Claude Juncker. A disastrous “the same only more so” response from Europe’s leaders would be signalled by taking Juncker – Spitzenkandidat of the largest party grouping in the new European parliament, the centre-right European People’s party – and making him president of the European commission. The canny Luxembourgeois was the longest-serving head of an EU national government, and the chair of the Eurogroup through the worst of the eurozone crisis.

Although he has considerable skills as a politician and deal-maker, he personifies everything protest voters from left to right distrust about remote European elites. He is, so to speak, the Louis XVI of the EU. The danger also lies in what now seems likely to happen inside the European parliament. The most probable development is a kind of unspoken grand coalition of the current mainstream party groupings, centre-right, centre-left, liberal and (at least on some issues) greens, to keep all the anti-parties at bay. If another six of the more xenophobic, nationalist parties accept the lead of the Marine le Pen’s triumphant Front National, papering over their differences to form a recognised group within the parliament, that will give them funding (from European taxpayers’ pockets) and a stronger position in parliamentary procedure, but still not enough votes to overpower such a centrist grand coalition.

Surely that is a good thing? Yes, in the short term. But only if that grand coalition then supports decisive reform of the EU. It should start, symbolically, by refusing ever again to make its absurd regular commute from its spacious quarters in Brussels to its second luxurious seat in Strasbourg – the EU’s version of Versailles – at an estimated cost of €180m a year. If, however, the unspoken grand coalition does not deliver more of what so many Europeans want over the next five years, it will only strengthen the anti-EU vote next time round. Then all the mainstream parties will be held responsible for the failure.

The one silver lining to this continent-sized cloud is that, for the first time since direct elections to the parliament began in 1979, overall voter turnout has apparently not declined. Turnout varies greatly from country to country – in Slovakia it was estimated to be 13% – but in France, for example, significantly more voters showed up than last time. What pro-Europeans preached for so long has finally come to pass: European citizens actively engaging in an EU-wide democratic process. But, irony of ironies, they do so to vote against the EU.

Who’s my bitch?

• A Europe Hooked on Russian Gas Debates Imposing Sanctions (Bloomberg)

European leaders, while calling Ukraine’s May 25 presidential election a success, are still facing a deeper dilemma: how to free their countries from an addiction to Russian energy. Pro-European billionaire Petro Poroshenko’s victory has relieved the immediate pressure on the U.S. and the European Union to impose tougher sanctions against Russia. The European and American reluctance to escalate in the wake of an election that was at least a partial success, a U.S. official said yesterday, suggests that by finally tempering his actions and rhetoric, Russian President Vladimir Putin may have achieved much of what he sought in Ukraine.

Russia’s ever-changing mix of covert action, economic threats and the annexation of Crimea, followed by soothing words, the official said, has exposed the divergence of U.S. and European Union views on Russia and the EU members’ conflicting interests there, especially on energy. “The energy crisis is a test of what the EU really is,” Poland’s Prime Minister Donald Tusk said on May 21, calling it “a duel” over what’s more important: “bilateral relations with Russia or relations within the EU.” The only way to be “an equal partner to big suppliers” is to form a united front.

Europe’s energy dependence “ties the EU’s hands a great deal – you really have widely divergent views,” said Charles Ebinger, director of the energy security initiative at the Brookings Institution in Washington, in an interview. Fears about losing Russian natural gas have made sanctions “very weak and, in the end, fairly meaningless.” The European Commission will publish an energy security road map tomorrow that European Union leaders will consider at a June 26-27 summit. No decision on new sanctions is expected at today’s gathering of heads of state, said EU diplomats. Russia’s threat to cut off gas supplies to Ukraine if the country doesn’t pay its back bills and agree to prepay for future supplies at a higher price presents problems for the EU, which gets half its Russian gas – 15% of its total supply – through Ukraine’s Soviet-era pipelines.

What a joke Abenomics has been from day one. “if they only believe in it, it’ll work … “

• Japan Risks Low Growth Even as Easing Spurs Rising Prices (Bloomberg)

Japan’s risk of spurring inflation without boosting the nation’s growth potential is raising the stakes for Prime Minister Shinzo Abe’s next round of economic restructuring measures, due in June. An economy “with low real growth rates under mild inflation” is possible, should the government fail to deliver, Bank of Japan Deputy Governor Kikuo Iwata said in a speech in Tokyo yesterday. Investors are looking for lower corporate taxes, labor-market flexibility and progress on a U.S.-led trade pact as Abe prepares for the next phase of the roll-out of the so-called Third Arrow of Abenomics, economic restructuring to boost long-term growth prospects.

“The BOJ is stepping up its rhetoric to push the government to raise Japan’s potential,” said Junko Nishioka, chief Japan economist at Royal Bank of Scotland Group Plc in Tokyo and a former central bank official. “Iwata is basically saying that the BOJ is achieving results, so now it is time for the government to show its commitment to ending deflation.” Abe’s strategy for boosting long-term growth is under scrutiny as the initial jolt fades from monetary stimulus that weakened the yen and sent stocks surging. While the Topix index of stocks rose 0.7% in morning trading in Tokyo today, it remains down about 8% this year, after gaining more than 50% in 2013.

Japan’s economy grew at the fastest pace since 2011 in the first three months of this year, an annualized 5.9% gain, driven by spending that was front-loaded before an April 1 sales-tax increase. Economists project that gross domestic product will fall an annualized 3.4% this quarter as consumers pare back their purchasing. The government is aiming for an annual average 2% expansion over a decade.

That is one effing claim.

• Bank of Japan Claims More Confident About Recovery (Reuters)

The Bank of Japan has begun shifting its focus from supporting growth to ways of phasing out its massive stimulus, taking first tentative steps towards a potentially momentous move for the world economy. Current and former central bankers familiar with internal discussions say an informal debate is under way on how to prepare for an exit from the BOJ’s 13-month-old “quantitative and qualitative monetary easing.” The stimulus is a centrepiece of Prime Minister Shinzo Abe’s campaign to end two decades of deflation and fitful growth, and BOJ Governor Haruhiko Kuroda has vowed to keep cheap cash flowing until his 2% inflation target is in plain sight. But with inflation now past the half-way mark and signs that the economy has weathered last month’s sales tax increase, Japanese central bankers are already thinking about the next chapter.

First of all, Kuroda and his team are keen to avoid market confusion and volatility that the U.S. Federal Reserve triggered in May 2013 when it first signaled the possible “tapering” of its extraordinary stimulus. With the BOJ churning out 60-70 trillion yen per year($589-687 billion), withdrawal symptoms could be similarly acute and the lesson for the BOJ is that signaling a tapering too soon or being too specific could backfire. With that in mind, the BOJ has no plans to trim the stimulus or publicly suggest the eventual drawdown any time soon, say those familiar with the internal debate. But whereas weeks or months ago that debate would center on the potential need for more easing, now there is a strong sense within the BOJ board that the stimulus so far has worked well and the next step, albeit distant, could be policy tightening, not further easing.

HA! HA!

• China Pushes Banks to Remove IBM Servers in Spy Dispute (Bloomberg)

The Chinese government is pushing domestic banks to remove high-end servers made by IBM and replace them with a local brand, according to people familiar with the matter, in an escalation of the dispute with the U.S. over spying claims. Government agencies, including the People’s Bank of China and the Ministry of Finance, are reviewing whether Chinese commercial banks’ reliance on the IBM servers compromises the country’s financial security, said the four people, who asked not to be identified because the review hasn’t been made public.

The review fits a broader pattern of retaliation after American prosecutors indicted five Chinese military officers for allegedly hacking into the computers of U.S. companies and stealing secrets. Last week, China’s government said it will vet technology companies operating in the country, while the Financial Times reported May 25 that China ordered state-owned companies to cut ties with U.S. consulting firms. The results of the government review will be submitted to a working group on Internet security chaired by President Xi Jinping, two of the people said.

At low enough rates, every zombie can borrow enough to look like a living person. That’s the name of our economic game.

• Bad Credit No Problem as Balance-Sheet Bombs Rally 94% (Bloomberg)

In the U.S. equity market, the worse a company’s finances, the better it’s doing. Stocks with the weakest balance sheets have climbed more than 8% in 2014 and 94% since the end of 2011, generating almost twice the gain in the S&P 500 Index over that period, according to compiled by Bloomberg and Goldman Sachs. Shares in the category this year are beating those that most investors consider the bull market’s leaders, such as small caps and biotechnology, which tumbled in March. Gains are being sustained by speculation that the corporations whose finances put them most at risk will thrive as the economy improves. Helped by rising bond issuance and falling defaults, stocks from Tenet Healthcare to Frontier Communications are advancing even as Federal Reserve policy makers take steps to end unprecedented economic stimulus.

“Having a weaker balance sheet isn’t a liability or a drag on potential company performance at this point,” David Kostin, chief U.S. equity strategist at New York-based Goldman Sachs, said in a May 20 phone interview. “In an economy that’s getting better, you can operate perfectly fine with a little more leverage.” A basket of 50 companies that rank lowest in measures comparing equity to total liabilities and earnings to assets, compiled in a gauge known as the Altman Z-Score, has increased 8.3% in 2014 after climbing 50% last year. The highest-rated group is up 3% since December after rallying 28% in 2013, according to data compiled by Goldman Sachs.

Shares with weaker finances have benefited as the Federal Reserve held interest rates near zero for the past six years and bought $3.6 trillion of bonds to stimulate the economy, spurring an unprecedented wave of debt financing. Companies in the S&P 500 that issued junk bonds — securities deemed the riskiest by credit raters — in the past year have seen their stocks climb 26% over that period, according to data compiled by Bloomberg. That compares with a one-year increase of 15% for the full S&P 500, which closed at a record on May 23.

No effing kidding.

• Dutch Regulator Says Banks Benefit More Than They Pay For (Bloomberg)

Banks will draw benefits from the European Central Bank’s direct oversight that will outweigh the extra supervisory costs they face, according to the Dutch central bank’s chief supervisory official. “They said it’s a lot of money, but it’s worth it,” Jan Sijbrand, who is also a member of the board of the ECB’s banking supervisory arm, told reporters in Amsterdam today. “Banks benefit from cheaper funding.” The ECB is slated to take on oversight of about 130 of the euro-area’s biggest lenders in November as the bloc tries to prevent a repeat of taxpayer-funded bank bailouts. It is due to present a proposal for how to fund those tasks tomorrow.

Ahead of taking over the supervision, the ECB is in the process of examining more than €3.7 trillion ($5.1 trillion) in risk-weighted assets of the banks that will fall into its realm. The Dutch central bank plans to charge its banks including ING Groep NV (INGA) and Rabobank Groep for the test, which may cost as much as €62 million. On top of the one-time costs for the ECB’s test and the additional fees for the ECB regular supervision, the Dutch financial sector also faces additional costs for domestic oversight. Finance Minister Jeroen Dijsselbloem plans to pass on €40 million in supervision costs currently borne by the state to banks and insurers, he said last week. If the ECB’s exam and the supervision make it cheaper for Dutch banks to borrow in the markets, the reduced funding costs will quickly offset the higher costs, Sijbrand said.

This will blow up Europe, and maybe other places as well.

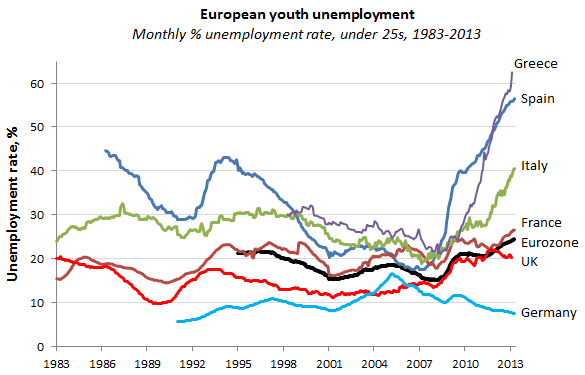

• The Global Crisis Of Young Adult Unemployment (MyBudget360)

\In the European Union, 12 countries now face an unemployment rate of 20% or higher for those 25 and younger. Little relief has come to this group. Many are with a college education but no employment market to practice what they have learned. The recipe of course is one where discontent grows and we saw this with the latest voting results. You also see a similar trend in the U.S. where a historically high number of young adults are living at home late into adulthood. This is partly due to the low wage employment market they are entering but also, the incredibly high levels of student debt many students exit college with. While global stock markets seem to have recovered, young adult unemployment is mired in problems.

People have a hard time understanding that work is more than a paycheck. For many people it gives them a sense of contributing to society and also a feeling of providing for their family. During the Great Depression, you had some that worked for reduced wages or promises of payment at a later date simply to avoid the crushing blow of being without work. Today, we face similar actions being taken by young adults working for reduced wages and benefits as they enter the low wage workforce. Many take on near illegal non-paid internships just to gain experience to build up their resumes. 12 countries in Europe have an unemployment rate of 20% or higher for those 25 years of age and younger. Some of the notable standouts:

• Spain: 53.6%

• Greece: 58.3% (last reading)

• Italy: 42.3%

• Portugal: 35%

• France: 23.6%

• Sweden: 23.6%This is extremely problematic. Many countries have layer upon layer of bureaucracy and cronyism and this has created a massive problem on a global scale for these countries. Unfortunately these countries cannot compete with the low wage employment trend that is overtaking the globe. While the stock market has been on a one way ticket up, young adult unemployment has followed a similar trajectory, for the worse:

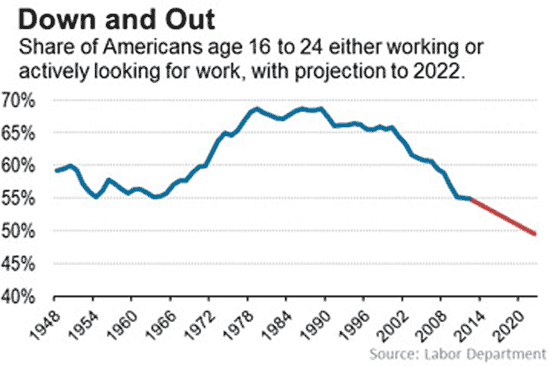

Having your youth facing a prospect of a gloomy future when it comes to work results in extreme voting as you recently saw. The U.S. is not immune to this. We have a shift with young adults and their working habits: This is an interesting trend. In the 1990s we had 65% of those 16 to 24 either working or actively looking for work. Today it is down to 55%, a multi-generation low. Now we can attribute this to people going to college but many are simply going to college to avoid looking for work. More troubling is the fact that many are being lured into back breaking levels of debt that are causing irreparable damage even before they have a diploma in hand.

Shale is a financial shell game, it’s not about energy. I wrote a whole series on just that. But it’s not done yet. Britain and other countries will fall for it too, and there the damage will be far greater even than in the Dakota’s.

• Shakeout Threatens Shale Patch as Frackers Go (For) Broke (Bloomberg)

The U.S. shale patch is facing a shakeout as drillers struggle to keep pace with the relentless spending needed to get oil and gas out of the ground. Shale debt has almost doubled over the last four years while revenue has gained just 5.6%, according to a Bloomberg News analysis of 61 shale drillers. A dozen of those wildcatters are spending at least 10% of their sales on interest compared with Exxon Mobil’s 0.1%. “The list of companies that are financially stressed is considerable,” said Benjamin Dell, managing partner of Kimmeridge Energy, a New York-based alternative asset manager focused on energy. “Not everyone is going to survive. We’ve seen it before.” Some investors are already bailing out.

On May 23, Loews Corp., the holding company run by New York’s Tisch family, said it is weighing the sale of HighMount Exploration & Production, its oil and natural gas subsidiary, at a loss. HighMount lost $20 million in the first three months of the year, after being unprofitable in 2013 and 2012, Loews said it its financial reports. As with much of the industry, HighMount has shifted its focus to oil after natural gas prices plunged and has struggled to find sites worth developing, company records show. In a measure of the shale industry’s financial burden, debt hit $163.6 billion in the first quarter, according to company records compiled by Bloomberg on 61 exploration and production companies that target oil and natural gas trapped in deep underground layers of rock. And companies including Forest Oil, Goodrich Petroleum and Quicksilver Resources racked up interest expense of more than 20%.

Quicksilver acknowledges the company is over-leveraged, said David Erdman, a spokesman for Quicksilver. The company’s interest expense equaled almost 45% of revenue in the first quarter. “We have taken concrete measures to reduce debt,” he said. Drillers are caught in a bind. They must keep borrowing to pay for exploration needed to offset the steep production declines typical of shale wells. At the same time, investors have been pushing companies to cut back. Spending tumbled at 26 of the 61 firms examined. For companies that can’t afford to keep drilling, less oil coming out means less money coming in, accelerating the financial tailspin.

This week, Greenwald is about to release a lot more files on Americans being spied on.

• Privacy Under Attack: NSA Files Reveal New Threats To Democracy (Guardian)

In the third chapter of his History of the Decline and Fall of the Roman Empire, Edward Gibbon gave two reasons why the slavery into which the Romans had tumbled under Augustus and his successors left them more wretched than any previous human slavery. In the first place, Gibbon said, the Romans had carried with them into slavery the culture of a free people: their language and their conception of themselves as human beings presupposed freedom. And thus, says Gibbon, for a long time the Romans preserved the sentiments – or at least the ideas – of a freeborn people. In the second place, the empire of the Romans filled all the world, and when that empire fell into the hands of a single person, the world was a safe and dreary prison for his enemies. As Gibbon wrote, to resist was fatal, and it was impossible to fly.

The power of that Roman empire rested in its leaders’ control of communications. The Mediterranean was their lake. Across their European empire, from Scotland to Syria, they pushed roads that 15 centuries later were still primary arteries of European transportation. Down those roads the emperor marched his armies. Up those roads he gathered his intelligence. The emperors invented the posts to move couriers and messages at the fastest possible speed. Using that infrastructure, with respect to everything that involved the administration of power, the emperor made himself the best-informed person in the history of the world. That power eradicated human freedom. “Remember,” said Cicero to Marcellus in exile, “wherever you are, you are equally within the power of the conqueror.”

The empire of the United States after the second world war also depended upon control of communications. This was more evident when, a mere 20 years later, the United States was locked in a confrontation of nuclear annihilation with the Soviet Union. In a war of submarines hidden in the dark below the continents, capable of eradicating human civilisation in less than an hour, the rule of engagement was “launch on warning”. Thus the United States valued control of communications as highly as the Emperor Augustus. Its listeners too aspired to know everything.

We all know that the United States has for decades spent as much on its military might as all other powers in the world combined. Americans are now realising what it means that we applied to the stealing of signals and the breaking of codes a similar proportion of our resources in relation to the rest of the world. The US system of listening comprises a military command controlling a large civilian workforce. That structure presupposes the foreign intelligence nature of listening activities. Military control was a symbol and guarantee of the nature of the activity being pursued. Wide-scale domestic surveillance under military command would have violated the fundamental principle of civilian control.

Home › Forums › Debt Rattle May 27 2014: Are You Sure You Want To Go To War?