Arthur Rothstein Texas Panhandle dust bowl Summer 1936

The headlines speak of an earthquake. But just about absolutely everyone who’s been shaken manages to declare victory, including incumbents who have lost, which is the majority of them, in some cases painfully. And European stocks are rising too, in some cases to all time highs. It all adds up to a perfect illustration of the absurd bizarro Europe has become.

Despite the huge surge in anti-EU sentiments, Brussels claims that because pro-EU parties still have a majority in the European parliament, the people of Europe have voted for the EU. There are a few problems with that claim that they would rather not discuss. Almost two thirds of eligible voters did not vote, attendance was as low as 18% in Czech and 13%(!) in Slovakia. It’s safe to assume a larger number of non-voters are not pro-EU (there’s a difference between anti and not-pro) than the number who are. Not pro-EU voters often have the problem that there are no parties to vote for that they like in other issues than being euroskeptic. In a democratic system, that’s a dangerous gap and a big political deficit.

The picture painted by the establishment is that only “extreme” (i.e. nazi) elements oppose what the EU has become. This is what you might call ‘useful nonsense’. As is the claim that “you can’t be against Europe, because you are Europe”. As if Europeans have no right not to like what the EU has become. Still, many people would rather stay home than vote for a Farage or a Le Pen, even though they’re the only voice in their countries that share their opinion on Europe. When you add it all up, it’s safe to assume there are many more euroskeptics than the elections appear to show.

There are also big differences between the euroskeptics, who therefore don’t – and can’t – form a “block” in the parliament the way the established parties do (for some reason, you need parties from 7 different countries to cooperate to be recognized as a block). For instance, Farage refuses to discuss forming a block that Le Pen is part of. What all of this means is that the center-right EPP block is still the biggest, which is readily spun into a positive development, even though it lost 62 of its seats, plummeting from 274 to 212:

With partial results and exit polls suggesting that the centre-right EPP had claimed 212 seats in the European Parliament to 185 Socialists, Jean-CLaude Juncker, the former prime minister of Luxembourg, was presented as the next president of the EU executive by jubilant party supporters. “As lead candidate of the largest party, I have won the election,” he told reporters in the Parliament hemicycle. “The EPP has got a clear lead, a clear victory.”

You lose 22% of your seats and declare victory. It fits perfectly into the overall messages emanating from the parties, and it would be funny if it had no consequences. Both the French and Greek winners (right wing Le Pen and left wing Tsipras) have urged for early elections to be held in their respective countries. Don’t count on it. Le Pen called for the French parliament to be dissolved, and PM Manuel Valls described his country’s vote as very serious, before, about two seconds later, announcing tax breaks, presumably in an attempt to stem the bleeding.

French President Hollande’s Socialist party suffered a huge and bitter defeat, and there are crisis talks in Paris today, undoubtedly in a room so full of spin doctors cabinet ministers will have a hard time finding a seat. How legitimate and credible is a President with only 14% of the vote, with Le Pen getting 25%? Nevertheless, Valls said Hollande and the Socialist government were elected for a five-year term with a specific “road map”, and they’re not going to change that. Not even if 6 out of every 7 French(wo)men who did bother to vote are against them. You got to love democracy. It’s as if ‘democracy’ means everyone is free to make up their own definition of the term, and all definitions are equally valid.

In fact, most incumbent governments have lost, and, spinning aside, need to address the issue of their legitimacy in a serious fashion, but are for now mostly stuck in “well, we’re still sitting here and what are you gonna do about it?” mode. That is as curious as it is dangerous, but the how and why may not be apparent if and when an economic recovery is plucked out of the hat. It’s when that doesn’t happen that the dangerous part begins. With distortions such as Italian and Spanish bonds selling at about the prices as US Treasuries, things may seem to be picking up, but that won’t last.

And the autostrada may now seem free and open for Mario Draghi to come with stimulus measures, but not so fast. The big winners of these elections are, with perhaps one or two exceptions, not in favor of going about things the ECB way. Nigel Farage’s victory puts more pressure on Cameron’s Conservatives to finally get serious about renegotiating the terms under which the UK is part of the EU. Tsipras’ victory means that Greek eurozone membership is by no means assured, and may only be salvable through monetary policies which other EU nations cannot accept. Or another coup.

The best hope for Brussels’ bureaucrats may be to hope that everything will disappear from people’s minds and attention spans, but without substantial economic improvements that is not likely. Why would the people in Greece, Italy and Spain keep on believing that staying in the EU is a better option than leaving, if that leaves them with sky high unemployment numbers and crumbling health care systems? Moreover, what exactly do the Greeks have to say in Brussels? Not much. And that is a problem that many EU nations have: who defends their specific needs and wishes if and when these don’t sync with those of larger nations?

Because the appropriation of seats in the European parliament has been set up with a system of “degressive proportionality”, which means the larger the state, the more citizens are represented per MEP, It’s not even as bad for the Greeks as it could have been. Degressive proportionality means Malta with 400,000 people has 6 seats, or one seat per 67,000, while Germany with 82.5 million citizens has 99 seats, i.e. one seat per 859,000. That’s nice, but in the end Germany wins. the Greeks may look “proportionally advantaged”, but their 21 seats are less the 26 Marina le Pen picked up last night, and much less than Angela Merkel’s 30.

Germany has a total of 96 seats in the 766 total parliament, France has 74, and Greece their 21. And the “membership will make us rich” story Greece was fed has already lost most of its luster lately, while the Germans and French who outnumber the Greeks by more than 8 to 1 in the EU have done very little to lift the unemployment burden in Athens. Instead, the troika continues to force them to sell their assets, like for instance 110 of their best beaches, to the world’s elite in the name of “development”.

If Greece leaves the eurozone, returns to the drachma – and devaluates it – and negotiates, or simply declares, inevitable defaults on parts of its debt, does anyone believe it could possibly fare worse than it does now? Athens can’t get out of where it is today because it has no say in how that could be achieved. The ultimate insult added to the grave injury the EU has turned out to be for the Greeks is that they’re not even their own boss anymore. Instead, they’re mere servants to a bunch of autocrats and bureaucrats who are selling off their land and their treasures from under their feet. I don’t know about you, but I’d rather be poor and independent.

Perhaps Greece can adopt some elements of the election program of the German satire party simple named ‘Die Partei’, which even won a seat (yeah, that’s what it’s come to). They intend to rotate that one seat between members, a new one every month, who will then be eligible to be placed on a 6-month retainer. “We’ll ‘squeeze the EU the way a small Mediterranean nation does'”. Other points from Die Partei’s campaign: build a wall around Switzerland, abolish Daylight Savings Time, and maximize personal wealth at $1 million, the rest to be divided amongst the poor. They now have a seat in the European Parliament. How fitting is that?

• Eurosceptic ‘Earthquake’ Rocks EU Elections (BBC)

Eurosceptic and far-right parties have seized ground in elections to the European parliament, in what France’s PM called a “political earthquake”. The French National Front and UK Independence Party both performed strongly, while the three big centrist blocs in parliament all lost seats. The outcome means a greater say for those who want to cut back the EU’s powers, or abolish it completely. But EU supporters will be pleased that election turnout was slightly higher. It was 43.1%, according to provisional European Parliament figures. That would be the first time turnout had not fallen since the previous election – but would only be an improvement of 0.1%.

“The people have spoken loud and clear,” a triumphant Marine Le Pen told cheering supporters at National Front (FN) party headquarters in Paris. “They no longer want to be led by those outside our borders, by EU commissioners and technocrats who are unelected. They want to be protected from globalisation and take back the reins of their destiny.” Provisional results suggested the FN could win 25 European Parliament seats – a stunning increase on its three in 2009. The party also issued an extraordinary statement accusing the government of vote-rigging.

• EU Protest Parties’ Surge Posing Threat From U.K. to Greece (Bloomberg)

Protest parties racked up gains across the 28-nation European Union in elections to the bloc’s Parliament, turning the assembly designed to unite Europe into an echo chamber for politicians who want to tear it apart. The anti-establishment wave hit hardest in France, Greece and the U.K., undermining the leaders of those countries and making it more difficult to steer the EU as a whole. In all, anti-establishment parties won 30% of the Europe-wide vote, up from 20% in the current Parliament, according to official EU projections late yesterday. Political forces suspicious of the U.S. made inroads across the continent, threatening to snag trans-Atlantic trade talks the EU hopes will spur an economy struggling with the after-effects of the euro debt crisis.

The U.K. Independence Party, which wants to yank Britain out of the EU, won the election in Britain, beating Prime Minister David Cameron’s Conservatives into third place. The protest vote “will have a huge impact on the parties and policies back home,” said Pieter Cleppe, head of the Brussels office of U.K.-based think tank Open Europe. “They will make it harder to centralize powers in the EU, especially when it comes to managing the euro crisis.” National winners included Marine Le Pen, head of France’s anti-immigration National Front; Alexis Tsipras, head of Greece’s anti-austerity Syriza party; and Nigel Farage, UKIP leader. With most of the seats declared in Britain, UKIP had 27.5% of the vote, the main opposition Labour Party 25%, the Conservatives 24%, the Greens 8% and Deputy Prime Minister Nick Clegg’s Liberal Democrats 7%.

United mainly by opposition to European unity, the motley collection of protest movements shows no signs of agreeing on a policy program. Instead, their aim was to make life harder for people who weren’t on the ballot: leaders of national governments. European Central Bank President Mario Draghi said the election showed that voters were looking for answers to the “thorny questions” of economic growth and employment. “Sustainable growth and jobs are vital to continue European integration, which is, let’s never forget, the best guarantor of peace,” Draghi said at an event yesterday in Sintra, Portugal. In France, the National Front picked up 25%, estimates by TNS Sofres, Ipsos and Ifop showed. The breakthrough dealt a further blow to President Francois Hollande, the least popular leader in France’s modern history. Le Pen’s party has cashed in on discontent with an economy that has barely grown in two years.

Proclaiming “politics of the French, for the French, with the French,” Le Pen said the election was a “humiliation” for Hollande. She called on him to dissolve the French parliament and submit to new national elections — an appeal that was dismissed by Hollande’s camp. Jean-Luc Melenchon, leader of France’s Left Front, said the result was a “volcanic eruption” accompanied by “lots of acid rain.” “It’s a disaster,” he said on France 2 television. “I feel sorry for my country tonight.” Voters in Greece, the first debt-crisis victim, handed first place to Syriza, a party which chafed at the budget cuts demanded by German-led creditors in exchange for international financial aid. Preliminary results gave it 26.5%. Prime Minister Antonis Samaras’s New Democracy party trailed with 23.3%.

What can he do, even if we’d want to?

• Poroshenko Wins Ukraine Vote With Russia Ready for Talks (BW)

Billionaire Petro Poroshenko won Ukraine’s presidential election, handing him the task of stemming deadly separatist violence that’s threatened to rip the former Soviet republic apart. Poroshenko got 53.8% of yesterday’s vote with 63.6% of ballots counted, according to the Election Commission in Kiev. Ex-Prime Minister Yulia Tymoshenko was second of the 21 candidates with 13.1%. Russia said it’s ready for talks with Poroshenko, though warned him against renewing a push against rebels who curbed voting in the easternmost regions. Poroshenko is faced with a shrinking economy and a pro-Russian separatist movement that’s captured large swathes of the Donetsk and Luhansk regions. President Vladimir Putin, who doesn’t recognize the government in Kiev, has pledged to work with the winner. The U.S and its allies said they’d tighten sanctions against Russia if voting was disrupted.

Poroshenko’s victory “marks an important step forward in resolving the political crisis that’s gripped the country,” Neil Shearing, chief emerging-markets economist at London-based Capital Economics Ltd., said today in an e-mailed note. “However, the challenges remain daunting.” Poroshenko’s win is “strongly” positive for bond markets in Ukraine and Russia, Vladimir Miklashevsky, a strategist at Danske Bank, said by phone. The yield on Ukraine’s dollar debt due 2023 fell for a ninth session, dropping one basis point, or 0.01 percentage point, to a seven-week low of 9.02%. It’s returned 7.8% this month, the most among 56 nations Bloomberg tracks.

Scary.

• Ukraine: From Tragedy To Farce (RT)

Petro Poroshenko, the Ukrainian oligarch known as the Chocolate King, is the presidential candidate who is expected to save Ukraine from the abyss and deliver his country to Washington, Brussels, and the IMF. Judging by polling numbers, he is quite likely to be elected by those who plan to vote (and millions in the east and south say they won’t). Legally speaking, this election has no legitimacy. Ukraine’s constitutional order was destroyed on the night of the coup. Since then the country has been governed by a rump parliament, political parties not supporting the undemocratic government physically attacked, and presidential candidates intimidated. Poroshenko is set to be president, but this will hardly address Ukraine’s daunting problems.

Poroshenko’s biggest political problems will not be the protesters in the east and south, nor will it be Russia. Ukraine’s next president will have to immediately deal with what western governments and media are reluctant to talk about: the nature of the political forces currently running Ukraine. Poroshenko did back the protests on the Maidan, but not all protesters on the Maidan supported Poroshenko. It is doubtful groups like Right Sector and Svoboda will simply change or drop their ultranationalist and racist views to please an opportunist oligarch like Poroshenko. The most likely outcome is probably the following: either Poroshenko attempts to appease their leaders with the trappings of power and wealth (and dilute whatever power he will have as president), or he will have to guard against still another Maidan uprising backed by the likes of Right Sector and Svoboda. Neither outcome bodes well for Ukraine.

If Poroshenko continues the violent assault on the east and south he will demonstrate he is not president of all Ukrainians. But if he does reach out to the east and south, the radicals of the coup will be watching closely. Again, this is a lose-lose outcome for Ukraine. This is probably most tragic outcome of the forced collapse of the constitutional order – unelected radicals, racists, and ordinary thugs have been allowed to become important elements of the Ukrainian political landscape. Ukraine and the rest of the world have Washington to thank for this sad state of affairs. Let us now turn to Russia and the Kremlin’s view of Ukraine. Putin is not backing down or looking for a way out. Far from it. Ever since this artificial crisis began, Russia has been watching – and it continues to watch. Putin’s attitude regarding the May 25 presidential vote is one of indifference at best. Russia cannot stop the vote. But if Poroshenko can, somehow and in some way, prove himself as a leader of all the people, then Moscow has every interest in engaging the next Ukrainian president. But for reasons expressed above, this is hardly going to be the case.

But what can he do?

• Mario Draghi Warns of Euro Zone Deflation (NY Times)

The president of the European Central Bank acknowledged on Monday that there is a risk that the euro zone could become caught in a downward spiral of falling prices, a “classic deflationary cycle” that would require large-scale purchases of bonds or other assets to reverse. Mario Draghi, the central bank’s president, stopped short of specifying what action the bank might take in response to such a risk when it meets on June 5. Expectations that the bank will do something are high following a flurry of statements in recent weeks by Mr. Draghi and by other members of the E.C.B.’s governing council indicating that they are prepared to take further steps to stimulate the struggling euro zone economy.

Mr. Draghi said that members of the governing council, many of whom are gathered here for a conference, are still debating what would be the right response to a combination of falling prices, tight bank credit, and uneven growth. All agree that the central bank must try to push inflation, currently at an annual rate of 0.7%, back toward the official target of just below 2%. But Mr. Draghi also spoke in unusually direct language about the risk that the euro zone could sink into deflation, when expectations of falling prices cause people to delay purchases, which in turn undercuts corporate profits and makes businesses reluctant to hire. Deflation, which has afflicted Japan for years, is considered particularly pernicious because it is very difficult for policy makers to reverse.

“What we need to be particularly watchful for at the moment is the potential for a negative spiral to take hold between low inflation, falling inflation expectations and credit, in particular in stressed countries,” Mr. Draghi said, according to a text of his remarks. A “too prolonged” period of inflation below current expectations, Mr. Draghi said, “would call for a more expansionary stance, which would be the context for a broad-based asset purchase program.” Many economists have urged the central bank to emulate the United States Federal Reserve and buy large quantities of government bonds and other assets to pump money into the economy. But most analysts do not expect the European Central Bank to begin an asset program when it meets next week. More likely, analysts say, would be a cut of the benchmark interest rate to 0.15% from 0.25%, coupled with a so-called negative deposit rate which would charge lenders for parking money at the central bank.

Yay! Get a mortgage!

• UK Interest Rates Could Rise Sooner Than Spring 2015: BOE Deputy (Guardian)

UK interest rates could start rising sooner than next spring, but “in baby steps”, and are likely to settle at about 3% in a few years’ time, the Bank of England’s outgoing deputy governor predicted. It will take three to five years for borrowing costs to rise to about 3%, Charles Bean said, but below the average of 5% seen in the decade before the financial crisis. The main UK interest rate has been held at 0.5%, a historic low, since March 2009, and the central bank’s governor, Mark Carney, has indicated that rates will not rise until next year. Carney surprised the City when he played down calls for an early increase to rein in the booming housing market when the Bank released its quarterly inflation report in mid-May. “We should remember the economy has only just begun to head back to normal,” he cautioned then.

Financial markets have priced in a rate rise in March or April 2015, although a move seems more likely in an inflation report month – February or May – when the Bank can use its latest economic forecasts to explain the rationale for an increase. Bean, who is leaving the Bank at the end of June after 14 years, told BBC Radio 4’s The World This Weekend programme that raising borrowing costs “a bit earlier” than expected would enable the Bank to do it more gradually to minimise the economic pain. He said: “There’s a case for moving gradually because we won’t be quite certain about the impact of tightening the bank rate given everything that has happened to the economy. “It might not operate in quite the same way as it did before the crisis. So that’s an argument if you like for being a little bit cautious, moving in baby steps to avoid making mistakes. If you want to pursue that strategy you need to start taking those baby steps a bit earlier, otherwise you end up being behind the curve.”

Once more.

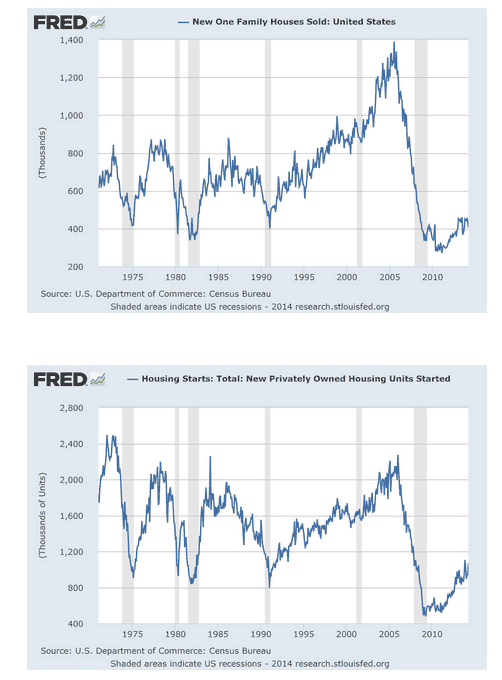

• US April New Home Sales Up 2K From March, But Down 5% Y/Y (Stockman)

Undoubtedly the Cool-Aid drinkers on Wall Street and at the Fed were encouraged that good weather has got everything back on track. The morning headline from Census was that new home sales were up 6.4% from March. Let’s see. There are about 130 million housing units in the USA and in good years we used to build about 1.5-2.0 million new units. But thanks to the long Greenspan housing boom from 1994-2007, the nation is now saddled with massive excess supply and has nearly 20 million vacant units. So home builders have been slow to translate the Fed’s cheap money into new starts because the demand just isn’t there to absorb the existing enormous surplus.

Compounding the slump is the fact that new household formation rates have dropped into the sub-basement of historical experience—coming in at about 500K annually in recent years compared to 1.5-2.0 million in pre-crisis times. The reason the data is in the sub-basement, of course, is that the kids are still in mom and dad’s basement, surviving on student loans and hamburger flipping gigs a few hours per week. So it is not surprising that new housing starts and new home sales have the trend profiles shown below. Needless, to say these graphs do depict a “new normal”, not the same old same old business cycle recovery that the Fed and its acolytes keep espying just around the corner.

So that gets us to the April new home sales numbers that got the algos all jiggy, including carbon-unit type algos like Joe LaVorgna, Deutschebank’s chief economist and stock tout, who mustered the following:

“Apr new home sales rebounded strongly (433k vs. 407k), providing further evidence that housing is recovering from Q1 weather-related weakness”.

Yes, Joe, actual monthly sales in April came in at 41,000 compared to 39,000 in March. That’s a gain of 2K that requires a Wall Street microscope to ascertain, but then it was also a 2K drop from the 43K new homes sold last year. Might the more relevant point here be that new homes sales are still bumping along a mighty historic bottom; that the beginning of interest rate normalization has already put the kibosh on the tepid recovery that had been underway; and that $3.5 trillion of Fed money printing since September 2008 has done far more for the Wall Street gamblers who speculate in homebuilder stocks than for the Main Street homebuilders and tradesman who actually build them. Never have the 19 unelected bureaucrats who inhabit the Eccles Building wreaked more havoc with what used to be a prosperous American economy. And then they have the audacity to proclaim progress in making everything better!

• Everything You Think About The Housing Market Is Wrong (Salon)

(Excerpted from “Other People’s Houses: How Decades of Bailouts, Captive Regulators, and Toxic Bankers Made Home Mortgages a Thrilling Business”)

The news cameras kept recording after the power failed. Complete darkness. Then a heavy red curtain was swept aside, allowing a bit of sunlight to stream into the woodpaneled hearing room. This natural illumination had a strange effect on Alan Greenspan, the day’s first witness. He was seated before the Financial Crisis Inquiry Commission (FCIC), a ten-member panel of private citizens appointed by Congress to examine the causes of the financial and economic crisis. By that day, in April 2010, the FCIC had already conducted several hearings and public meetings. Greenspan had spent much of the morning before the power outage in a defensive mode, denying that, as chairman of the Fed for nearly two decades, he had the tools to predict or prevent the subprime mortgage meltdown and the connected global financial crisis.

Yet he had admitted to the panel: “I was right 70% of the time, but I was wrong 30% of the time. And there are an awful lot of mistakes” over the years. Now, in the semidarkness, Greenspan retreated a bit. He responded to a question about whether he believed there still was excessive debt in the banking system with a nod, a gesture not captured on the official record. The commissioner who posed the question remarked that he saw Greenspan nod. An audience member said he had not nodded. Greenspan sat silently, not offering to clarify. Minutes later, the hearing adjourned and the witness departed.

That was classic Greenspan: bright moments of clarity followed by obfuscation and retreat. Eighteen months earlier in October 2008, in his most candid moment, he told a congressional subcommittee that he had found “a flaw” in his entire system of thought. He had adhered for decades to a particular view of how markets operated, only to discover several decades later he’d been very wrong. Yet the question for the panel that April morning was whether the crisis could have been avoided. At the hearing, Greenspan explained that the origination of subprime mortgages had posed no problems between 1990 and 2002. In that early era, he said, it was a contained market, but then things changed. It was the expansive sale of adjustable rate subprime mortgages, followed by the securitization of these mortgages, and the transformation of those securities into collateralized debt obligations (CDOs) that caused problems.

There was a huge demand from Europe for CDOs backed by such mortgages, thus fueling increasingly higher-risk originations. Greenspan also made it clear that without “adequate capital and liquidity,” the “system will fail to function.” He called for additional equity capital (less borrowing relative to assets held). He said he now realized that our banking system had been undercapitalized for forty to fifty years. But in 2011, when it came time to require banks to have greater equity capital, he publicly denounced “an excess of buffers” in an op-ed in the Financial Times. Seeming to forget the savings and loan (S&L) crisis of just twenty years earlier, he asked: “How much of its ongoing output should a society wish to devote to fending off once-in-50 or 100-year crises?” This was Greenspan, light and dark.

The less fear in the markets, the more there is to be afraid of.

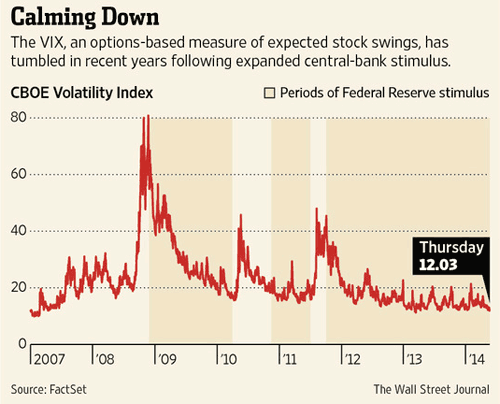

• Low VIX Sparks Volatile Debate (WSJ)

Many market watchers have been scratching their heads over low readings in the CBOE Volatility Index. The VIX, often called the market’s “fear index,” continued to slide ahead of the holiday weekend, briefly touching 11.46 in recent trading, its lowest intraday level since March 2013. Investors and market watchers are at odds over what factors are driving ultra-low volatility and what it might portend for the markets. Optimists point out that the VIX is rightly at a multi-year low given that the S&P 500 is repeatedly carving out fresh all-time highs. The VIX measures the prices investors pay for options as insurance on S&P 500 stock portfolios. Short term, some point to lighter stock-trading volumes and the predictable lull in risk-taking that occurs before holiday weekends. People have less risk, so there’s little need to hedge that risk, they say.

Pessimists contend that a low VIX reading demonstrates that investors have let their guard down, dropping demand for S&P 500 stock-portfolio insurance just when they may need it. “The low VIX says to me that people are kind of complacent,” says Brian Overby, options analyst at brokerage TradeKing. “I find that odd considering that over the last couple months we’ve been trading sideways.” Most ominously, some say that the VIX isn’t the best place to look for fear right now since its tie to the S&P means it doesn’t capture recent declines in faster-moving corners of the stock market, or the rush into Treasury bonds in 2014. Take the Russell 2000 Index of small-cap stocks: While the S&P 500 is sitting near its all-time high, the Russell 2000 has dropped 7.6% from its own record high in March. An options-based volatility reading on the iShares Russell 2000 IndexIWM shows considerably more alarm than for the S&P 500, according to data from LiveVol.

Jonathan Krinsky, MKM Parners’ chief market technician, noted on Thursday that cases when small-caps plunge while large caps remain unstressed are exceedingly rare. He found just two instances over the past 20 years when the VIX marked fresh 52-week lows at the same time that the Russell 2000 traded below its so-called 200-day moving average—a long-term pivot point watched by market technicians. On Thursday, the signals aligned for a third time, but the Russell 2000 broke back above that threshold on Friday. Both previous times it’s happened—in 2000 and 2004—the VIX shot sharply higher over the following three months.

Let’s hope this gets real.

• Explosive Claims On JP Morgan Conduct (SMH)

A technical support person who worked for JP Morgan in Australia claims the bank regularly misled its New York parent and the US Federal Reserve by failing to report losing trades. The explosive allegations are contained in a submission by the person to the Senate inquiry into the performance of the Australian Securities and Investments Commission. BusinessDay has met the person and agreed to allow him to remain anonymous. He appears to be credible. The person complained to ASIC and later went to work for the regulator, but he said the regulator failed to investigate his claims. A spokesman for JP Morgan denied the allegations. “The claims are false and misleading,” he said.

In his submission, published by the inquiry, the person said he was employed at the Sydney office of JP Morgan between 2004 and 2007. He worked for a team involved in the post-trade management of the bank’s OTC (over the counter) equity derivative business for the Asia-Pacific region. In 2007, before the global financial crisis, he became increasingly concerned by “certain practices that appeared to circumvent regulatory commitments and risk management expectations,” he said. These included:

• Misleading reports being provided to head office and the Federal Reserve Bank of New York on the number of outstanding trades.

• Trades not being booked into the system until they were ”in-the-money”.

• Trades not booked into systems and only being tracked by paper-based legal agreements, which would be ”torn up” if required, thereby leaving no trace.

• Bypassing or attempting to bypass the opinions of in-house lawyers to complete work faster, even if this resulted in incorrect legal agreements being signed by the traders and sent to other major banks as final confirmation of the terms of the trade.

The person said he sought to discuss his concerns with lower and middle management but was warned that “front office would get rid of me if I persisted”. JP Morgan’s ‘Worldwide Rules of Conduct’ state: ‘The most important rule is also the most general: never sacrifice integrity, or give the impression you have, even if you think that it would help JP Morgan Chase’s business’. “In support of this policy, I lodged a complaint with senior management fully expecting to be able to discuss all my concerns and receive guidance from the relevant departments, including legal and compliance. This did not occur and instead I immediately stopped being paid.”

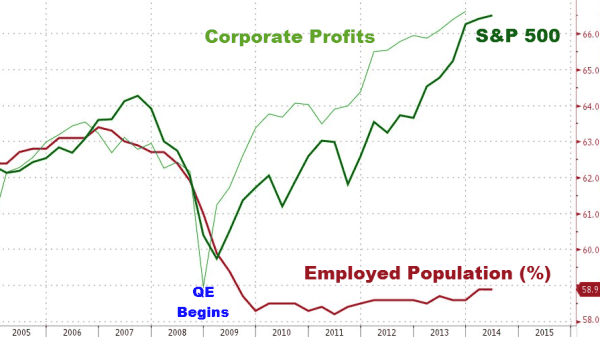

On a weekend so full of memories, we thought it appropriate to remember what was promised so many years ago from our central-planning overlords. All that printed money, all those bailouts, all those promises and Bernanke’s statement that “Fed actions did not favor Wall Street over Main Street…” and this is what we end up with… “not” all time highs in what really matters… Remember – Bernanke told us “The US economy is heading back to a full recovery” – then a few months later explained that interest rates would not normalize in his lifetime…

Just don’t tell Obama (or the Democrats who have been told not to mention the ‘recovery’), or the record number of middle-aged people living with their parents, or the almost imperceptible rise in the employed population since QE began…

Bill Black all the way!

• Bill Black: “The Bank Robbers’ Weapon Of Choice Is Accounting” (Zero Hedge)

William Black’s no-nonsense simplification of the fraud that we call a financial system is both addictive in its clarity and stunningly concerning in its scale. Having exposed Tim Geithner as perhaps the worst Treasury secretary ever, and that “banks have blood on their hands,” the following brief discussion of ‘how to rob a bank – from the inside’ is crucial to comprehend that nothing has changed and to make matters worse, after 2009’s ‘reforms’, “the weapon of choice remains accounting” as no one knows what it occurring behind the scenes of the banks…

In the US, our regulators have publicly embraced a “too big to prosecute” doctrine. We are restraining, underfunding and dismantling regulatory oversight in the interests of short-term stability for the status quo. Which as a criminologist, Black knows with certainty creates an environment where bad actors will act in their self-interest with assumed (and likely real, at this point) impunity.

If you can steal with impunity, as soon as you devastate regulation, you devastate the ability to prosecute. And as soon as that happens, in our jargon, in criminology, you make it a criminogenic environment. It just means an environment where the incentives are so perverse that they are going to produce widespread crime. In this context, it is going to be widespread accounting control fraud. And we see how few ethical restraints remain in the most elite banks. You are looking at an underlying economic dynamic where fraud is a sure thing that will make people fabulously wealthy and where you select by your hiring, by your promotion, and by your firing for the ethically worst people at these firms that are committing the frauds.

And so you have one of the largest banks in the world, HSBC, being the key ally to the most violent Mexican drug cartel, where they actually did so much business together that the drug cartel designed special boxes to put the cash in that they were laundering that fit exactly into the teller windows so that there would be no delay. This is the efficiency principle of drug laundering. So these banks figuratively have the blood of over a thousand people on their hands. They are willing to fund people that murder and torture and behead folks. And they are willing to do that year after year, despite warnings from the regulators that they are doing this. And the regulators are not willing to actually take serious action until there has been “true devastation.”

Fear! Fear!

• UK Finance Ministry Warns On Scottish Independence Costs (Reuters)

Britain’s finance ministry stepped up its attack on the Scottish government’s independence plans on Monday, saying it had not fully budgeted for setting up a new administration that could cost Scottish taxpayers over 1.5 billion pounds ($2.5 billion). People in Scotland vote on September 18 on whether to end a 307-year union with England and split from the rest of the United Kingdom. Britain’s finance ministry has repeatedly argued that Scots would be financially worse off after independence.

On Monday, it said setting up the new public bodies such as a Scottish tax authority, financial regulator and benefits system would cost each Scottish household a minimum of 600 pounds, and potentially much more. “The Scottish government is trying to leave the UK, but it won’t tell anyone how much the set-up surcharge is for an independent Scotland,” deputy finance minister Danny Alexander said. He is due to present a more detailed breakdown of the Westminster government’s estimates of the costs of Scottish independence and Scotland’s budget deficit on Wednesday. The Scottish government dismissed the report as “deeply flawed”.

The British finance ministry said new institutions would cost Scotland at least 1% of its annual economic output – or 1.5 billion pounds – based on estimates made when the Canadian province of Quebec voted on independence. The actual cost could be far higher. New Zealand, which has a similarly sized population and economy to Scotland, was currently spending 750 million pounds on a new tax system alone, while a new Scottish benefits system would cost 400 million pounds, the finance ministry said. A bill of 2.7 billion pounds was possible if the Scottish government pressed ahead with plans for 180 new public bodies, the finance ministry said, based on a cost of 15 million pounds for each new policy department. But the Scottish government said in a statement many of the public bodies which would be needed by an independent Scotland already existed and would be able to take on new functions.

• Piketty Rejects ‘Ridiculous’ Allegations of Data Flaws (Bloomberg)

Thomas Piketty rejected allegations that data behind his best-selling book on inequality are flawed as fellow economists spoke up in his defense. Piketty, the French economist whose book “Capital in the Twenty-First Century” has transformed the debate on the causes and consequences of disparities in income and wealth, called a Financial Times analysis of his statistics “just ridiculous.” He added in an e-mail to Bloomberg News that “there’s no mistake or error” in his work. The newspaper’s economics editor, Chris Giles, wrote last week that figures underpinning the 696-page book contain unexplained statistical modifications, “cherry picking” of sources and transcription errors. He said the mistakes undermine Piketty’s conclusion that wealth inequality in Europe and the U.S. is moving back toward levels last seen before World War I.

After correcting for the alleged errors, two of the book’s “central findings — that wealth inequality has begun to rise over the past 30 years and that the U.S. obviously has a more unequal distribution of wealth than Europe — no longer seem to hold,” according to Giles. Economists disputed that assertion. Scott Winship, a fellow at the New York-based Manhattan Institute for Policy Research, said the newspaper’s allegations aren’t “significant for the fundamental question of whether Piketty’s thesis is right or not.” James Hamilton, an economics professor at the University of California, San Diego, said there’s “abundant evidence” of widening inequality “from a good many sources besides Piketty.”

Piketty, a 43-year-old professor at the Paris School of Economics, examined centuries of data on countries including the U.S., Sweden, France and the U.K. to show that returns on capital in excess of economic growth lead to widening disparities in wealth. One “serious discrepancy” Giles said he found was in Piketty’s data on the U.K. While Piketty cited a figure showing the top 10% of its population held 71% of national wealth, a survey by the country’s Office for National Statistics put the figure at 44%.

The survey cited by Giles “is based upon self-reported data and is very low quality,” Piketty said in his e-mail. Other economists agreed. “The FT seems to take that survey as gospel, and I think that’s a mistake,” said Gabriel Zucman, an assistant professor at the London School of Economics whose research focuses on global wealth, inequalities and tax havens. “Anybody involved in this literature knows that survey data can massively underestimate wealth inequality. In this case, that is exactly what is happening.”

Home › Forums › Debt Rattle May 26 2014: The Absurd Bizarro That is Europe