Dorothea Lange Rear window tenement dwelling, 133 Avenue D, NYC June 1936

No emperor AND no clothes.

• Global Selloff Deepens as Stocks Sink With Oil (Bloomberg)

The global selloff in riskier assets deepened, spurring the biggest drop in Asian shares since 2011 and sending emerging-market currencies to the weakest levels on record. U.S. 10-year yields dropped below 2%. Commodity prices sank to a 16-year low, while credit risk in Asia increased to the highest since March 2014. The yen rallied and government bonds rose as investors sought haven assets. China’s Shanghai Composite Index tumbled 8.5%, while U.S. equity-index futures signaled a fifth straight day of losses. The rand dropped more than 3%. “Things are probably going to get worse before they get better,” Nader Naeimi at AMP Capital Investors said. “You really need rate cuts and more policy easing in China. In the meantime, things can get worse. We’ve got to see more clarity around the Fed.”

More than $5 trillion has been erased from the value of global stocks since China unexpectedly devalued the yuan, fueling speculation that the slowdown in the world’s second-largest economy may be deeper than previously thought. The rout is shaking confidence that the global economy will be strong enough to withstand higher U.S. interest rates. All major Asian markets were lower after U.S. stocks capped their biggest two-day retreat in almost four years Friday. Futures on the Standard & Poor’s 500 Index retreated as much as 3.1% after the U.S. benchmark plunged 5.2% through the final two days of last week. The MSCI Asia Pacific Index fell for a seventh straight day, sinking 4.3% by 12:57 p.m. Tokyo time, set for its lowest close since June 26, 2013. The gauge is on the cusp of a 20% slide from an April high.

View from Oz.

• Global Bloodbath Sparks Financial Crisis Fears (News.com.au)

Global markets are in meltdown with losses approaching those not seen since the global financial crisis. Should we be worried? Absolutely. Australia bet big on never-ending Chinese growth and, increasingly, it looks like we could walk out of the casino empty-handed. Global stock markets have been rocked over the past few weeks amid growing signs of a slowdown in China. It’s causing fears we could be seeing a re-run of the 1997-98 Asian financial crisis, and there are dire implications for the Australian economy. The Australian market has plunged by 3.5% today as of 12:45 AEST, with almost $60 billion stripped from the value of the nation’s companies.

It’s the biggest daily fall since September 2011, and is compounding an already dismal stretch which is on track to be the worst month since the GFC. The benchmark S&P ASX 200 has fallen more than 16% from its highs near the 6000 mark earlier this year. The local market looks to be heading for its first negative year since 2011. From their highs earlier this year, US shares are now down 7.5%, eurozone shares are down 14%, Asian shares have fallen 20%, Chinese shares are down 32% and emerging market shares are down by 17%. Meanwhile, the Shanghai Composite has crashed 8.4% this morning, putting even greater pressure on Australian stocks, particularly the big mining companies.

On top of everything else, there are fresh fears that Greece could exit the euro after Prime Minister Alexis Tsipras called for snap elections after growing division within his radical left-wing Syriza party over the stricken country’s bailout deal. So should we be worried? “The short answer is absolutely,” said ABC Bullion chief economist Jordan Eliseo. “The volatility over the last week has simply revealed the fact that the primary cause of the GFC — excessive debt and capital misallocation — has not been solved.”

Eruope off ‘only’ 2.5-3% as I write this. US futures look ugly.

• A Sell-Off Of Epic Proportions Spreads Further (FT)

Chinese equities fell more than 8% in the morning session, leading a sell-off across Asia that prompted fresh questions about what policymakers might do to staunch the losses. The benchmark Shanghai Composite fell 8.5%, erasing all of its 2015 gains, while the tech-heavy Shenzhen Composite tumbled 7.6%. Hong Kong’s Hang Seng Index lost 4.6%, extending its August decline to nearly 13%, writes Patrick McGee in Hong Kong. “Today has all the hallmarks of being one of the worst trading days of the past five years,” said Evan Lucas at IG, a spread-betting group. The MSCI Asia Pacific Index fell 4.3%, on pace for its lowest finish since late June 2013.

Before China markets opened the global equity rout of last week accelerated across Asia in a negative feedback loop. Once China joined in on the turmoil the sell-off accelerated and was joined by commodity prices. Tokyo’s Nikkei 225 slid 3.3%, falling below 19,000 for the first time since April, while the Topix sank 4.2%. In Sydney, the S&P/ASX 200 dropped 3.3%, while Taiwan’s Taiex was down as much as a 7.5% — at risk of its biggest daily sell-off since 1990 — before paring the loss to 4.3%. Turnover in Japan, Australia and Taiwan was 77%, 90% and 113% above the 30-day average. Bank and energy stocks led the declines as the slide in the price of commodities such as oil showed no signs of abating.

The Bloomberg Commodity Index, a 22 member gauge that looks at everything from egg futures to natural gas, fell 1.2% to $86.79, its lowest since 1999. Even the price of gold is down 0.4% today, as investors sell quality assets to raise much-needed cash for margin calls. The Chinese falls place further pressure on the country’s authorities to act. The Shanghai market fell nearly 12% last week as investors questioned whether Beijing was still propping up equities with an array of policies. A key manufacturing gauge hit a six-year low on Friday, spurring a wave of selling but drawing no real response from authorities. Many were expecting the People’s Bank of China to cut interest rates or inject liquidity over the weekend, however, no such steps were taken, heightening fears Beijing is no longer staking its credibility on bolstering the market.

Yes, that would be 1999.

• Commodities Slump to 16-Year Low as China Slowdown Roils Markets (Bloomberg)

Commodities sank to the lowest level in 16 years, joining a rout in global equities and emerging-market currencies on concern that China’s economic slowdown will exacerbate gluts of everything from oil to metals. The Bloomberg Commodity Index of 22 raw materials lost as much 1.7% to 86.3542 points, the lowest level since August 1999. Resources stocks from BHP Billiton to Cnooc tumbled while Brent crude fell below $45 a barrel for the first time since 2009. “Sentiment is extremely negative across the commodity complex,” Mark Keenan at Societe Generale in Singapore, said in an e-mail. “Markets are plagued by concerns of oversupply.” Raw materials are in retreat as supplies outstrip demand amid forecasts for the slowest Chinese growth since 1990.

The largest user of energy, grains and metals was much weaker than anyone expected in the first half of the year, according to Ivan Glasenberg, head of commodity trader Glencore Plc. Chinese shares plunged after U.S. stocks sank last week. “It’s being fueled by the large drop in the Chinese stock market today, which is making people nervous about the management of the Chinese economy, which has direct implications for commodities,” Ric Spooner, a chief market strategist at CMC Markets Asia Pty, said by phone from Sydney. “It’s now basically a risk-off move.”

Shares in BHP, the world’s largest mining company, fell as much as 5.3% in Sydney to the lowest level since 2008, while Fortescue Metals Group Ltd. plunged 15% after reporting full-year profit dropped 88%. Nanjing Iron & Steel Co. led losses on the Shanghai Composite Index, sliding 10% as the gauge erased its gains for the year. Cnooc slumped 7.1% in Hong Kong. Oil has sunk as producers maintain or boost supply even as a glut persists, prioritizing sales over price. Iran will raise output at any cost to defend its market share, Oil Minister Bijan Namdar Zanganeh told his ministry’s news website, Shana.

Brent for October settlement declined as much as 3.2% to $44 a barrel on the ICE Futures Europe exchange, the lowest price since March 2009. West Texas Intermediate in New York dropped 3.2%, taking its loss over the past year to 58%. Copper on the London Metal Exchange lost as much as 3% to $4,903 a metric ton, the lowest since 2009. The metal is regarded as an indicator of global economic activity. Output topped demand by 151,000 tons in the six months through June, according to the World Bureau of Metal Statistics.

Panic in Detroit: Reserve requirements down, pension funds forced to buy stocks. Remember when pensions could invest only in AAA rates assets?

• China Poised to Raise Banks’ Liquidity to Boost Lending (WSJ)

The People’s Bank of China is preparing to flood the banking system with liquidity to boost lending, according to officials and advisers to the central bank, as its recent currency moves are squeezing yuan funds out of the market and renewing concerns over capital leaving Chinese shores. The planned step—which involves cutting the deposits banks are required to hold in reserve—signals that the Chinese central bank’s exchange-rate maneuvering in the past two weeks is backfiring, forcing it to again resort to the reserve-requirement reduction, the same easing measure that so far has failed to help spur economic activity.

The move, which could come before the end of this month or early next month, would involve a half-percentage-point reduction in the reserve-requirement ratio, potentially releasing 678 billion yuan ($106.2 billion) in funds for banks to make loans. It would be the third comprehensive reduction in the reserve requirement this year. Another option being considered at the PBOC is to target the cut only at banks that lend large amounts to small and private businesses—the ones deemed key to China’s future growth—though such a strategy hasn’t proven effective in the past in channeling credit to those borrowers.

One concern the Chinese central bank has over further lowering the reserve-requirement ratio is that, in theory, releasing more liquidity could add to the depreciation pressure on the yuan. But right now, the PBOC’s bigger worry is over the liquidity squeeze as a result of its recent yuan intervention—actions that have resulted in yuan funds being drained from the financial system. That, on top of fresh signs of capital outflows, is threatening a shortage of funds at Chinese banks, causing greater market jitters. To ensure ample liquidity, the central bank is poised to cut the reserve-requirement again.

All under control anyone?

• China’s One-Year Bonds Decline in Sign of Tightening Liquidity (Bloomberg)

China’s one-year sovereign bonds fell for a second day amid speculation liquidity is tightening as the central bank buys yuan to support the exchange rate. The People’s Bank of China will likely cut lenders’ reserve requirements this week or next to replenish funds in the financial system and help arrest an economic slowdown, according to Standard Chartered. The currency has been kept at about 6.40 per dollar since Aug. 13, after a surprise devaluation led to a 3% drop over three days. Only the Hong Kong dollar, which is pegged, has been more stable over the past week among 31 major currencies.

The yield on notes due July 2016 rose three basis points to 2.35% as of 11:36 a.m. in Shanghai, according to National Interbank Funding Center prices. That for June 2018 debt increased two basis points to 2.90%. “It’s clear that the central bank wants to stabilize the exchange rate by selling dollars and buying the yuan via big banks, and the result is naturally a drop of local currency supply,” said Huang Wentao, an analyst at China Securities Co. in Beijing. “This is why some investors are refraining from putting money into the bond market. Reserve-ratio cuts could lead to further depreciation pressure, and that’s why the PBOC would prefer to use reverse repos in the short-term.”

To hold down borrowing costs, the PBOC is adding funds via loans to banks. It conducted 240 billion yuan ($37.5 billion) of reverse-repuchase agreements last week and extended 110 billion yuan using its Medium-term Lending Facility. The overnight repurchase rate, a gauge of funding availability in the banking system, was poised to increase for a record 38th day. It was at 1.83%, the highest level since April, according to a weighted average compiled by the National Interbank Funding Center. The seven-day repo rate fell two basis points to 2.53%, after rising to a six-week high of 2.58% on Aug. 20.

It was all only ever a sleight of hand.

• Is The Game Up For China’s Much Emulated Growth Model? (Ghosh)

[..] the “recovery package” in China essentially encouraged more investment, which was already nearly half of GDP. Provincial governments and public sector enterprises were encouraged to borrow heavily and invest in infrastructure, construction and more production capacity. To utilise the excess capacity, a real estate and construction boom was instigated, fed by lending from public sector banks as well as “shadow banking” activities winked at by regulators. Total debt in China increased fourfold between 2007 and 2014, and the debt-GDP ratio nearly doubled to more than over 280%. We now know that these debt-driven bubbles end in tears. The property boom began to subside in early 2014, and real estate prices have been stagnant or falling ever since.

Chinese investors then shifted to the stock market, which began to sizzle – once again actively encouraged by the Chinese government. The crash that followed has been contained only because the government pulled out all the stops to prevent further falls. All this comes in the midst of an overall slowdown in China’s economy. Exports fell by around 8% in the year to July. Manufacturing output is falling, and jobs are being shed. Construction activity has almost halted, especially in the proliferating “ghost towns” dotted around the country. Stimulus measures such as interest rate cuts don’t seem to be working. So the recent devaluation of the yuan– which has been dressed up as a “market-friendly” measure – is clearly intended to help revive the economy.

But it will not really help. Demand from the advanced countries – still the driver of Chinese exports and indirectly of exports of other developing countries – will stay sluggish. Meanwhile, China’s slowdown infects other emerging markets across the world as its imports fall even faster than its exports and its currency moves translate into capital outflows in other countries. The pain is felt by commodity producers and intermediate manufacturers from Brazil to Nigeria and Thailand, with the worst impacts in Asia, where China was the hub of an export-oriented production network. Many of these economies are experiencing collapses of their own property and financial asset bubbles, with negative effects on domestic demand. The febrile behaviour of global finance is making things worse. This is not the end of the emerging markets, but is – or should be – the end of this growth model.

Forced.

• Chinese Pension Fund ‘Allowed’ To Invest In Stock Market (BBC)

China plans to let its main state pension fund invest in the stock market for the first time, the country’s official news agency, Xinhua, has reported. Under the new rules, the fund will be allowed to invest up to 30% of its net assets in domestically-listed shares. China’s main pension fund holds 3.5tn yuan ($548bn; £349bn), Xinhua said. The move is the latest attempt by the Chinese government to arrest the slide in the country’s stock market. The fund will be allowed to invest not just in shares but in a range of market instruments, including derivatives. By increasing demand for them, the government hopes prices will rise. The Shanghai Composite Index closed down more than 4% on Friday after figures showed monthly factory activity contracting at its fastest pace in six years.

It capped a tough few days for Chinese investors, with the index down 12% on the week. Chinese shares are now down more than 30% since the middle of June. Earlier this month, the Chinese central bank devalued the yuan in an attempt to boost exports. These measures come against a backdrop of slowing economic growth in China. In the second quarter of this year, the country’s economy grew by 7% – its slowest pace for six years. Last year, the economy grew at its slowest pace since 1990. Fears of a prolonged slowdown have also hit global stock markets, with US and leading European indexes posting heavy losses last week.

We’re poised to see a lot of this.

• Angry Investors Capture Head Of China Metals Exchange (FT)

The head of a Chinese exchange that trades minor metals was captured by angry investors in a dawn raid and turned over to Shanghai police, as the investors attempted to force the authorities to investigate why their funds have been frozen. Investors have been protesting for weeks after the Fanya Metals Exchange in July ceased making payments on financial investment products. The exchange, based in the southwestern city of Kunming, bought and stockpiled minor metals such as indium and bismuth, while also offering high interest, highly-liquid investment products from its offices in Shanghai and its financing branch in Kunming. Troubles at the exchange are one of many factors contributing to turbulence in China’s financial markets, as a slowing economy exposes the weaknesses of the country’s debt-driven growth.

Some investors flew in from faraway cities to join hundreds more surrounding a luxury hotel in Shanghai before dawn on Saturday. When Fanya founder Shan Jiuliang attempted to check out, they manhandled him into a car before delivering him to the nearest police station. Shanghai police took Mr Shan into custody and promised to work with local authorities in Yunnan province to investigate what has happened to investors’ money. They later released him without charge. The demonstrations in Shanghai and Kunming and the exchange’s unusual accumulation of several years’ supply of some metals have so far failed to attract much public attention from regulators. A report by the local regulator identifying the exchange as one of the bigger investment risks in Yunnan was redacted to remove reference to Fanya late last year.

“The selloff [..] relegated Hong Kong to the same trading orbit as Pakistan..”

• Hong Kong Can’t Escape the Turmoil Next Door (Pesek)

Twelve months ago, it seemed Beijing’s retrograde politics would eventually sink Hong Kong’s exalted international reputation. Now China’s ailing economy seems likely to finish off the job sooner than anyone expected. Hong Kong is dealing with a long list of problems, including tumbling tourist arrivals, a dollar peg that makes it the priciest place in Asia, a precarious property bubble and a leader not up to even mundane challenges never mind an existential crisis. And that’s before you even get to Hong Kong’s biggest challenge: the fallout from China’s loss of economic credibility around the globe. How else to explain the 9% drop in the Hang Seng Index since Beijing’s Aug. 10 devaluation?

The selloff put the city’s valuations at their lowest, relative to global equities, since 2003, and relegated Hong Kong to the same trading orbit as Pakistan, a place grappling with chronic power shortages. Forbes magazine spoke for many last year when it asked: “Is Hong Kong Still China’s Golden Goose?” The concern then was that political turmoil would disrupt Hong Kong’s status as China’s financial green zone, where companies can enjoy the rule of law and politicians can invest ill-gotten millions in real estate and with Beijing-friendly billionaires. Hong Kong seemed to be the perfect Chinese special-enterprise zone – except for the mounting discontent among the city’s middle class, whose needs tended to be ignored in favor of the tycoons lording over the city.

When hundreds of thousands of residents began protesting in favor of democracy in September 2014, the city’s chief executive Leung Chun-ying, like the good Communist functionary he is, shut the demonstrations down. Political discord no longer seems an immediate existential threat to the city’s special status – but China’s sputtering economy does. Waning trust in the Chinese economy is driving investors away from Hong Kong, while China’s devaluation is making the city less attractive for mainland tourists enticed by cheaper destinations like Japan. Economy Secretary So Kam-leung blamed the 8.4% drop in visitors in July on the strong dollar. Retail sales in the city declined for a fourth straight month in June.

Hong Kong doesn’t have many good options. For years economists urged Hong Kong to diversify its growth engines – more tech and science startups, fewer hedge funds and property developers riding mainland growth. Rather than deliver the changes Hong Kong needed, Leung has squandered his three years as chief executive kowtowing to his Communist Party benefactors in Beijing.

All central banks that matter these days are Ponzi scams.

• Central Banks Have Become A Corrupting Force (Roberts and Kranzler)

Are we witnessing the corruption of central banks? Are we observing the money-creating powers of central banks being used to drive up prices in the stock market for the benefit of the mega-rich? These questions came to mind when we learned that the central bank of Switzerland, the Swiss National Bank, purchased 3,300,000 shares of Apple stock in the first quarter of this year, adding 500,000 shares in the second quarter. Smart money would have been selling, not buying. It turns out that the Swiss central bank, in addition to its Apple stock, holds very large equity positions, ranging from $250,000,000 to $637,000,000, in numerous US corporations — Exxon Mobil, Microsoft, Google, Johnson & Johnson, General Electric, Procter & Gamble, Verizon, AT&T, Pfizer, Chevron, Merck, Facebook, Pepsico, Coca Cola, Disney, Valeant, IBM, Gilead, Amazon.

Among this list of the Swiss central bank’s holdings are stocks which are responsible for more than 100% of the year-to-date rise in the S&P 500 prior to the latest sell-off. What is going on here? The purpose of central banks was to serve as a “lender of last resort” to commercial banks faced with a run on the bank by depositors demanding cash withdrawals of their deposits. Banks would call in loans in an effort to raise cash to pay off depositors. Businesses would fail, and the banks would fail from their inability to pay depositors their money on demand. As time passed, this rationale for a central bank was made redundant by government deposit insurance for bank depositors, and central banks found additional functions for their existence.

The Federal Reserve, for example, under the Humphrey-Hawkins Act, is responsible for maintaining full employment and low inflation. By the time this legislation was passed, the worsening “Phillips Curve tradeoffs” between inflation and employment had made the goals inconsistent. The result was the introduction by the Reagan administration of the supply-side economic policy that cured the simultaneously rising inflation and unemployment. Neither the Federal Reserve’s charter nor the Humphrey-Hawkins Act says that the Federal Reserve is supposed to stabilize the stock market by purchasing stocks. The Federal Reserve is supposed to buy and sell bonds in open market operations in order to encourage employment with lower interest rates or to restrict inflation with higher interest rates.

If central banks purchase stocks in order to support equity prices, what is the point of having a stock market? The central bank’s ability to create money to support stock prices negates the price discovery function of the stock market.

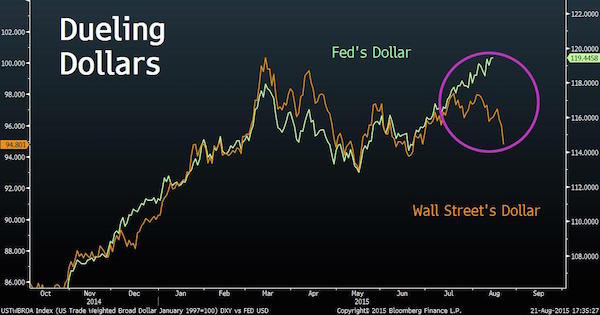

Why the rate hike may still happen.

• The Fed Is Looking at a Very Different Dollar Than Wall Street (Bloomberg)

By many popular measures, the dollar has traded sideways for the last six months. Then there’s the Federal Reserve’s measure. The greenback is surging, according to an index the Fed created to track the U.S. currency versus 26 of the country’s biggest trading partners. It’s risen 1.3% beyond a 12-year high reached in March, when the central bank fired the first of a series of warnings that a stronger dollar may hurt growth and lower inflation. At a time when the Fed’s tightening path has become one of the biggest drivers in the $5.3 trillion-a-day foreign-exchange market, the discrepancy between Wall Street’s view – largely based on the dollar’s performance against the euro and the yen – and that of policy makers may lead to a jolt for investors expecting recent ranges to persist.

The rapid trade-weighted appreciation this quarter has come mostly against big exporters such as China and Mexico, and it undercuts the Fed’s goal of quicker inflation. It may trigger further jawboning from officials looking to cool the dollar’s broad gains as the Fed begins raising interest rates for the first time in almost a decade. “The dollar still continues to strengthen on a trade-weighted basis and the Fed definitely takes that into the equation,” said Brad Bechtel, a managing director at Jefferies Group LLC in New York. “The risk is the Fed starts really emphasizing that, and the market would be caught offside.” The Fed’s trade-weighted broad dollar index measures the greenback against the currencies of 26 economies according to the size of bilateral trade. China, Mexico and Canada make up 46% of the gauge.

Meanwhile, most private-sector dollar gauges track a basket of the world’s most liquid, widely used currencies. Intercontinental Exchange Inc.’s U.S. Dollar Index, which serves as the benchmark for various futures and options instruments, has a 58% weight to the euro and 14% for the yen. It lacks representation from any emerging markets, which account for more than half of the U.S.’s total trade flow. The two indexes had moved alongside each other until a month ago. The Fed’s broad dollar index surged 3.4% this quarter to a 12-year high as China devalued the yuan to support a slowing economy, while a renewed commodities rout undermined Canada’s loonie and the Mexican peso. The ICE dollar gauge dropped 0.7% during the same period.

Amen.

• It’s Time To Lay Siege To The Robber Barons Of High Finance (Ben Chu)

Rent extraction, or “rent-seeking” as it is also often known, has evolved and broadened as an economic concept. It now covers a whole range of activities in a modern economy. A famous example used in economic textbooks is licensed taxis. Black cab drivers pressure city authorities to clamp down on the activities of unlicensed minicabs. More recently they’ve also tried to get new entrants to the taxi market, like those who work for the Uber web app service, banned. To the extent they are successful in these rent-seeking activities they boost the value of their own licences. It is their customers who end up paying in the form of higher fares. But cabbies are small fry in the rent-extraction ocean.

A more lucrative practice is found in the law firms that mildly tweak and re-file patents as a means of squeezing more money out of clients’ old intellectual property, or who aggressively sue other firms over minor and often spurious infringements. None of this incentivises more research or innovation. And it is the public who pay for this “patent trolling” in higher prices for products. But easily the biggest source of wealth extraction in modern economies is the wholesale financial sector. Much of the activity of Wall Street and City of London traders in investment bankers constitute a form of rent-extraction. Their phenomenally lucrative market-making activities in interest rates and foreign exchange don’t actually create new wealth – they merely shift money from the pockets of companies and pension funds into their own.

In a properly functioning market new players would enter and these outsize market-making profits would be competed away. But the sheer size of these financial dealers erects effective barriers to entry, curbing competition. And the “too big to fail” status of these mega financial institutions (which provides an implicit state guarantee) also secures them artificially cheap finance in the money markets, compounding their commercial advantage. But how do we distinguish rent extraction from high profits due to legitimate business success? A good indicator is the extent to which their profits seem to be dependent on political and official connections.

The American financial sector has spent $6.6bn (£4.2bn) since 1998 lobbying US politicians, according to researchers. It seems unlikely they would spend such sums for no reason. Our own ministers also seem to have an open door for the UK financial lobby. The power of the lobby can be seen in the fact that widespread calls to simply break up the too-big-to-fail banks in the wake of the global financial crisis were rejected on both sides of the Atlantic by politicians.

And who do you think pays for this?

• Bank Litigation Costs Hit $260 Billion With $65 Billion More To Come (FT)

The wave of fines and lawsuits that has swept through the financial industry since the 2007/8 crisis has cost big banks $260bn, new research from Morgan Stanley shows. The analysis, which covers the five largest banks in the US and the 20 biggest in Europe, predicts the group will incur another $60bn of litigation costs in the next two years. Bank of America, Morgan Stanley, JPMorgan, Citi and Goldman Sachs have borne the brunt of the fines so far, collectively paying out $137m. They have another $15bn to come in the next two years, Morgan Stanley said. The top 20 European banks have paid out about $125bn and have about $50bn to come “albeit with a wide range”, the analysis said.

In the States … there have been more precedents on settlements and so as more banks have settled, the market’s ability to make a guesstimate of the amount for other banks has improved, said Huw van Steenis, managing director at Morgan Stanley. Mr van Steenis said the fines, which cover everything from foreign exchange rate rigging to US mortgage-backed securities and mis-selling of payment protection insurance in the UK, are having a profound impact on the banks. Litigation not only takes a bite out of your equity but has a much longer lasting impact on the amount of capital you need to hold, he said. The figures include fines and penalties banks have already paid, plus any provisions taken by June 30 for issues the groups see coming down the tracks, such as US mortgage fines that European banks expect to pay.

The report also charts what banks have done to reduce the risk of future litigation, but concludes that lack of disclosure means it has been difficult for us to say definitively which firms have developed the best practices overall . Bank of America is spending $15bn a year on compliance, Morgan Stanley said, while JPMorgan is spending $8bn or $9bn. Mr van Steenis and his colleagues said they struggled to obtain consistent data on extra compliance costs in Europe. The impact goes beyond the financial. A lot of management time and IT budget has been focused on rectifying malfeasance rather than being able to position the bank for the future, said Mr van Steenis.

A crazed country.

• Brazil’s Scandal Takes Another Toxic Turn (Bloomberg)

On Thursday, Brazilian Attorney General Rodrigo Janot formally charged Eduardo Cunha, Brazil’s highest-ranking lawmaker with commanding a farrago of felonies, including shaking down suppliers of Petrobras, the scandal-ridden national oil company, for some $5 million, and then laundering the bribes through more than 100 financial operations from Montevideo to Monaco. Running 85 pages and garnished with an aphorism by Mahatma Gandhi, the indictment reads like the production notes to a noir movie script. My favorite scene: 250,000 reais (around $71,000) in booty decanted through Cunha’s preferred house of worship, the Assembly of God.

Not surprisingly, Janot’s indictment has enthralled Brasilia, where President Dilma Rousseff has seen the national economy and her approval ratings sink to record lows, and not even core allies can be trusted to back her emergency reforms. Ever since Cunha won the right to the top microphone in Congress, trouncing Rousseff’s own candidate for the job, the Rio de Janeiro lawmaker has dedicated his mandate to making her life miserable, delaying revenue raising initiatives and planting some “fiscal bombs” in Congress that would plump constituents’ earnings at the expense of the swelling public deficit. So how do you say schadenfreude in Portuguese? After weeks of escalating rhetoric and street protests clamoring for impeachment, suddenly it’s Rousseff’s archenemy who looks to be on the brink.

But hold those vuvuzelas. While Cunha may be hobbled by the scandal, he’s hardly out of play. Even if the Supreme Court accepts Janot’s indictment and sends Cunha to trial, he has no obligation to step aside. Removing him would take half plus one of the 513 members of Brazil’s lower house, an ecosystem where Cunha is at home.

This is getting beyond shameless.

• EU Border Agency Frontex To Boost Patrols In Aegean To Halt Migrants (Kath.)

A joint action plan drafted by the Greek Police, the Hellenic Coast Guard and Frontex aims to boost patrols in the eastern Aegean in a bid to curb a dramatic influx of refugees and immigrants, Fabrice Leggeri, the executive director of the EU’s border monitoring agency, has told Kathimerini. The key goal of the European border guards will be to spot smuggling vessels heading toward Greece from neighboring Turkey before they enter Greek waters and to inform Turkish Coast Guard officials so the vessels can be returned. The Frontex officials to be dispatched to Greece are to conduct sea patrols but also land patrols on islands such as Lesvos and Kos that have borne the brunt of an intensified influx of migrants.

In an interview with Kathimerini, Leggeri said European Union member-states have appeared reluctant to contribute equipment, particularly technical equipment, that Greek authorities need to effectively deal with the migration crisis. He said the organization’s budget for operations in Greece has been tripled, to €18 million, adding that he was pushing to secure as much aid as possible for the country. The EU “must show solidarity,” he said, noting that Greece, Italy and Hungary have been hit the hardest by the migration crisis, and to a lesser extent Spain.

A total of 340,000 refugees and immigrants have entered the European Union so far this year, he said, blaming the increase primarily on the war in Syria but also on a deteriorating security situation in Libya, which has discouraged migrants from taking that route. This week, Greek Police and Hellenic Coast Guard officials are to meet with Frontex officials at the agency’s office in Piraeus to hammer out a strategy.

Oh, right, and Merkel has shown herself to be a real leader, right?!

• Germany Shames EU for Failure to Shoulder Refugee Surge

The unwillingness of most European Union states to accommodate a surge in refugees amassing at the trade bloc’s southern fringes is a “huge disgrace,” German Vice Chancellor Sigmar Gabriel said. Speaking on the country’s ARD television Sunday, Gabriel said just three countries – Germany, Sweden and Austria – were taking on more refugees, with most states snubbing their plight. By closing the door to people fleeing wars, the EU puts its internal open-border policy at risk, Gabriel said. “I find it a huge disgrace when the majority of member states say, ’that’s got nothing to do with us’,” said the Social Democrat chairman, whose party co-rules with Chancellor Angela Merkel’s Christian Democrats. “Returning to a Europe without open borders will have catastrophic economic, political and cultural consequences.”

Germany and the EU Commission are failing to break the opposition of EU partners including the U.K., Spain, Denmark and Hungary to taking on a larger share of refugees thronging on the bloc’s borders. Germany can cope with a fourfold influx of refugees this year, to about 800,000, but “not indefinitely,” Gabriel said. Merkel and French President Francois Hollande will reopen the question of refugee quotas for individual EU members when they meet in Berlin tomorrow, French Foreign Minister Laurent Fabius said in Prague. An earlier effort to assign a firm number of refugees to each EU country failed after a majority of the bloc’s members refused to commit.

Hungary is building a wall along its border with Serbia to prevent refugees from crossing. Denmark in July said it would cut benefits for asylum seekers in a bid to stem their influx. Estonia said it could accept just 150-200 refugees over two years, while U.K. Prime Minister David Cameron this month characterized people trying to enter his country illegally from north Africa as a “swarm.” Underlining the urgency of countering the EU’s disunity over its refugee problem is a gross miscalculation of the number of people fleeing to the continent from such countries as Syria, Iraq, Eritrea and Afghanistan. As late as May, Germany predicted the number of refugees and asylum seekers entering the country this year at 450,000.

Home › Forums › Debt Rattle August 24 2015