Dorothea Lange Resettlement project, Bosque Farms, New Mexico Dec 1935

That sounds more like it.

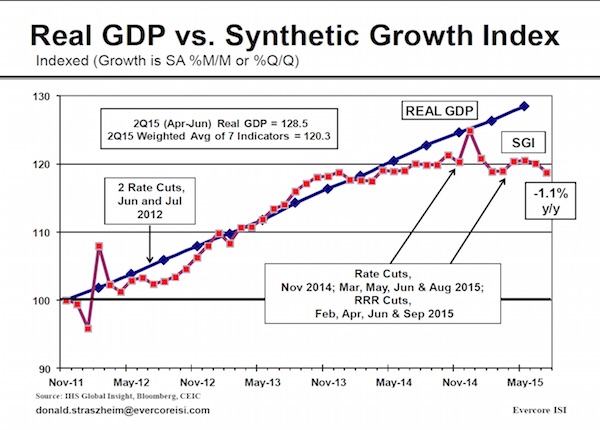

• Real Chinese GDP Growth Is -1.1%, According to Evercore ISI (Zero Hedge)

With Chinese data now an official farce even among Wall Street economists, tenured academics, and all others whose job obligation it is to accept and never question the lies they are fed, the biggest question over the past year has been just what is China’s real, and rapidly slowing, GDP – which alongside the Fed, is the primary catalyst of the global risk shakeout experienced in recent weeks. One thing that everyone knows and can agree on, is that it is not the official 7% number, or whatever goalseeked fabrication the communist party tries to push to a world that has realized China can’t even manipulate its stock market higher, let alone its economy.

But what is it? Over the past few months we have shown various unpleasant estimates, the lowest of which was 1.6% back in April. Today we got the worst one yet, courtesy of Evercore ISI, which using its own GDP equivalent index – the Synthetic Growth Index (SGI) – gets a vastly different result from the official one, namely Chinese growth of -1.1% annually. Or rather, contraction. To wit, from Evercore:

Our proprietary Synthetic Growth Index (SG!) fell 1.1% mim in July, and was also down 1.1% y/y. No wonder global commodities are so weak. The most recent 18 months have been much weaker than the 2011-13 period. Even if we adjust our SG I upward (for too-little representation of Services — lack of data), we believe actual economic growth in China is far below the official 7.0% yly. And, it is not improving, Most worrisome to us; the ‘equipment’ portion of Plant & Equipment spending is very weak, a bad sign for any company or country. Expect more monetary and fiscal steps to lift growth.

And here is why the world is in big trouble.

With confidence gone, is there another option left?

• BofA: China Stock Rout To Resume As Intervention Ends (Bloomberg)

The rebound in China’s stocks will be short-lived because state intervention is too costly to continue and valuations aren’t justified given the slowing economy, says Bank of America. “As soon as people sense the government is withdrawing from direct intervention, there will be lots of investors starting to dump stocks again,” said David Cui at Bank of America in Singapore. The Shanghai Composite Index needs to fall another 35% before shares become attractive, he said. The Shanghai gauge rallied for a second day on Friday amid speculation authorities were supporting equities before a World War II victory parade next week that will showcase China’s military might. The government resumed intervention in stocks on Thursday to halt the biggest selloff since 1996.

China Securities Finance, the state agency tasked with supporting share prices, will probably end direct market purchases within the next month or two, Cui said. While the benchmark gauge trades 47% above the levels of a year earlier, data from industrial output to exports and retail sales depict a deepening slowdown. China’s first major growth indicator for August showed the manufacturing sector is at the weakest since the global financial crisis. Profits at the nation’s industrial companies fell 2.9% in July, data Friday showed. Equities on mainland bourses are valued at a median 51 times reported earnings, according to data compiled by Bloomberg. That’s the most among the 10 largest markets and more than twice the 19 multiple for the Standard & Poor’s 500 Index. Even after tumbling 37% from its June 12 peak, the Shanghai gauge is the best-performing equity index worldwide over the past year.

This is going to be seminal.

• Money Pours Out of Emerging Markets at Rate Unseen Since Lehman (Bloomberg)

This week, investors relived a nightmare. As markets from China to South Africa tumbled, they pulled $2.7 billion out of developing economies on Aug. 24. That matches a Sept. 17, 2008 exodus during the week Lehman Brothers went under. The collapse of the U.S. investment bank was a seminal moment in the timeline of the global financial crisis. The retreat from risky assets, triggered by concern over a slowdown in China and higher interest rates in the U.S., has taken money outflows from emerging markets to an estimated $4.5 billion in August, compared with inflows of $6.7 billion in July, data compiled by Institute of International Finance show. It’s lower stock prices that people are most worried about.

Equity outflows from developing nations increased to $8.7 billion this month, the highest level since the taper tantrum of 2013 when the prospect of higher rates in the U.S., making riskier assets less attractive, first shook emerging markets. Debt inflows softened this month while remaining positive at $4.2 billion, the IIF says. “Emerging market investors have been spooked by rising uncertainty about China, and stress has been exacerbated by a combination of fundamental concerns about EM economic prospects and volatility in global financial markets,” Charles Collyns, chief economist at the IIF, said.

Interconnections.

• What China’s Treasury Liquidation Means: $1 Trillion QE In Reverse (ZH)

Earlier today, Bloomberg – citing the ubiquitous “people familiar with the matter” – confirmed what we’ve been pounding the table on for months; namely that China is liquidating its UST holdings. As we outlined in July, from the first of the year through June, China looked to have sold somewhere around $107 billion worth of US paper. While that might have seemed like a breakneck pace back then, it was nothing compared to what would transpire in the last two weeks of August. Following the devaluation of the yuan, the PBoC found itself in the awkward position of having to intervene openly in the FX market, despite the fact that the new currency regime was supposed to represent a shift towards a more market-determined exchange rate.

That intervention has come at a steep cost – around $106 billion according to SocGen. In other words, stabilizing the yuan in the wake of the devaluation has resulted in the sale of more than $100 billion in USTs from China’s FX reserves. That dramatic drawdown has an equal and opposite effect on liquidity. That is, it serves to tighten money markets, thus working at cross purposes with policy rate cuts. The result: each FX intervention (i.e. each round of UST liquidation) must be offset with either an RRR cut, or with emergency liquidity injections via hundreds of billions in reverse repos and short- and medium-term lending ops.

It appears that all of the above is now better understood than it was a month ago, but what’s still not well understand is the impact this will have on the US economy and, by extension, on US monetary policy, and furthermore, there seems to be some confusion as to just how dramatic the Treasury liquidation might end up being. Recall that China’s move to devalue the yuan and this week’s subsequent benchmark lending rate cut have served to blow up one of the world’s most popular carry trades. As one currency trader told Bloomberg on Tuesday, “it’s a terrible time to be long carry, increased volatility – which I think we’ll stay with – will continue to be terrible for carry. The period is over for carry trades.”

Negative records being set all over.

• Global Equity Funds Witness Biggest-Ever Exodus (CNBC)

Investors yanked $29.5 billion out of global equity funds in the week that ended August 26, the biggest single-week outflow on record as markets around the world over went into meltdown mode, according to data from Citi. On a regional basis, U.S. funds suffered the highest level of outflows at $12.3 billion, followed by Asia funds, which saw $4.9 million in redemptions. Citi’s records go back to 2000. European funds, which broke their chain of 14 weeks of inflows, witnessed $3.6 billion in outflows for the week.

Concerns around the outlook for the Chinese economy and jitters around the U.S. Federal Reserve’s impending rate hike have sent global markets into a tailspin over the past week. The MSCI World Index and MSCI Emerging Market Index both slid over 7% between August 19 and August 26. China, the market at the heart of the global selloff, saw losses of a far higher magnitude. The notoriously volatile benchmark Shanghai Composite tumbled 22% over this period, leading to outflows of $1.2 billion from China and Greater China funds during the week.

Yeah, sure, add more leverage…

• PBOC Uses Derivatives to Tame Yuan Fall Expectations (WSJ)

China’s central bank used an unusual and complex financial tool Thursday to tame growing expectations for the yuan to fall, three people familiar with the matter said. The People’s Bank of China intervened in the market for U.S. dollar-yuan foreign-exchange swaps, causing their price to fall sharply, a movement that implies a stronger Chinese currency and lower interest rates in the world’s No. 2 economy in the future, said the people. The move came after waves of sharp selloffs in the Chinese currency in offshore markets, such as Hong Kong’s, where the yuan trades freely, following Beijing’s surprise nearly 2% yuan devaluation on Aug. 11.

Thanks to what each of the three people described as “massive” orders from a few commercial banks acting on the PBOC’s behalf, the so-called one-year dollar-yuan swap spread—in rough terms, a measure of the implied future differential between Chinese and U.S. interest rates—plunged to 1200 points from 1730 points Wednesday. In the offshore market, the spread dropped to 1950 points from 2310 points Tuesday, following the onshore move. A drop in the spread for dollar-yuan swaps, which consist of a spot trade and an offsetting forward transaction, would also imply a weaker spot exchange rate at a predetermined future date.

The currency derivatives are typically used by investors seeking to hedge against exchange-rate and interest-rate fluctuations. “The central bank chose a rarely used tool this time—the FX swaps—to intervene and it did so via a couple of midsize banks, instead of the usual big state lenders that serve as its agent banks,” one of the people said.

Desperation. Again, remember when pensions were limited to AAA rated assets?

• China Local Govt Pension Funds To Start Investing $313 Billion ‘Soon’ (Reuters)

China’s local pension funds will start investing 2 trillion yuan ($313.05 billion) as soon as possible in stocks and other assets, senior government officials said on Friday, in a bid to boost the investment returns of such funds. China said last weekend that it would let pension funds under local government units to invest in the stock market for the first time, a move that might channel hundreds of billions of yuan into the country’s struggling equity market. Up to 30 percent can be invested in stocks, equity funds and balanced funds. The rest can be invested in convertible bonds, money-market instruments, asset-backed securities, index futures and bond futures in China, as well as major infrastructure projects.

“We will actively make early preparations… we will formally start investment operations as soon as possible,” Vice Finance Minister Yu Weiping told a briefing. But the timing of investment will depend on preparations as the National Social Security Fund (NSSF), the manager of local pension funds, will entrust professional investment firms to make actual investments, Yu told reporters after the briefing. “When they (investment firms) will enter the market, the government will not intervene,” Yu said. You Jun, vice minister of human resources and social security, told the same news conference that pension investment will benefit the economy and the country’s capital market, but he downplayed any attempt to support the ailing stock market. “Supporting the stock market or rescuing the stock market is not the function and responsibility of our funds,” You said.

The crucial point becomes how much of this can be kept hidden.

• Chinese Banking Giants: Zero Profit Growth as Bad Loans Pile Up (Bloomberg)

The first two Chinese banking giants to report earnings this week have two things in common: zero profit growth and bad loans piling up at more than twice the pace of a year earlier. Industrial & Commercial Bank of China posted a 31% increase in bad loans in the first half, while Agricultural Bank of China had a 28% jump, their stock-exchange statements showed on Thursday. At a press briefing in Beijing, ICBC President Yi Huiman indicated that the lender may have to abandon a target of keeping its nonperforming loan ratio at 1.45% this year, citing “severe” conditions. The level at the end of June was 1.4%.

The economic weakness and $5 trillion stock-market slump that prompted the central bank to cut interest rates and lenders’ reserve requirements this week may make it harder for China’s banks to revive earnings growth and attract investors. For now, the biggest banks are trading below book value. “We are nowhere near the end of this down cycle, not with the economy wobbling like now,” said Richard Cao at Guotai Junan Securities. ICBC’s profit was little changed at 74.7 billion yuan ($11.7 billion) in the quarter ended June 30, based on an exchange filing, almost matching 74.8 billion yuan a year earlier. That compared with the 75.7 billion yuan median estimate of 10 analysts surveyed by Bloomberg. Nonperforming loans jumped to 163.5 billion yuan, the company said.

Agricultural Bank reported a profit decline of 0.8% to 50.2 billion yuan and bad loans of 159.5 billion yuan, including debt in the construction and mining industries. For ICBC, the biggest increases in nonperforming credit in the first half were in China’s western region, where coal businesses are struggling, the Yangtze River Delta and the Bohai Rim. ICBC, Agricultural Bank and another of China’s large lenders to report on Thursday, Bank of Communications, all reported declines in net interest margins, a measure of lending profitability. The rural lender had the biggest fall, a slide of 15 basis points from a year earlier to 2.78%.

Bretton Woods.

• The Great Wall Of Money (Hindesight)

China is in severe trouble and that trouble has already been reverberating around EM exporters for a number of years. It is just one of many dollar currency peg countries that have experienced tightening conditions because of higher US interest rate guidance and dollar strength. An unwelcome addition to their own domestic issues, but always a circular outcome, as they are inextricably linked to the US by their Bretton Woods II relationship. By devaluing and thus de-stabilising the ‘nominal’ anchor for Asian exchange rates, they will crush the growth engine of the developed countries on whose consumption they so rely on.

Since 2009, we have forecast and documented the unwinding of the Bretton Woods II currency system. Financialisation of our economies and markets, which escalated post-2008 at the instigation of governments and central bankers, is going to go into full reverse for all asset classes. Economies and markets are so entwined that a drop in asset classes will lead the world back into recession. In 2013, we believed the odds had tilted firmly towards increasing debt deflation at the hands of China. Large current account deficits had led to unsustainable debt creation, and as a consequence the trade deficit countries were the first to experience a severe financial crisis. However, on the other side of the equation, the surplus countries were now experiencing their reaction to the crisis.

In November 2013, we wrote: “The deleveraging process which began in 2008 has been a slow burner but is likely now in full swing. The deflationary risks are very high. China is the driver. All eyes on China.” We conceive that this slow-burner of deleveraging, which has occurred since the 2008 crisis, is potentially about to engulf all asset prices. We are beginning to think the unthinkable – that just maybe asset prices will back up 20 to 30% and fast and that through the autumn we could experience even greater price depreciation. Almost 8 years on from the GFC, the Dow Jones Industrials are perched on the edge of a sharp drop.

Will the Ghost of 1937 revisit us eight years on from the Great Crash of 1929, when U.S. stocks and the world economy got roiled all over again? This is already unfolding as we speak. The Yuan movement may well send more Chinese capital floating across the globe into financial assets and real estate, but it will be short-lived. The debt deleveraging which has been engulfing Emerging Markets has just begun to turn into a ranging inferno, which will eventually burn down all, especially overpriced, global assets. Since the GFC, ‘The Great Wall of Money’ that Bretton Woods II has furnished via its vendor-financing relationship, has masked the deleveraging of our world economy. The Great Wall is about to collapse and fall.

Not too late, but too little. Because too little is all that is left.

• China Will Respond Too Late to Avoid -Global- Recession: Buiter (Bloomberg)

China is sliding into recession and the leadership will not act quickly enough to avoid a major slowdown by implementing large-scale fiscal policies to stimulate demand, Citigroup’s top economist Willem Buiter said. The only thing to stop a Chinese recession, which the former external member of the Bank of England defines as 4% growth on “the mendacious official data” for a year, is a consumption-oriented fiscal stimulus program funded by the central government and monetized by the People’s Bank of China, Buiter said. “Despite the economy crying out for it, the Chinese leadership is not ready for this,” Buiter said in a media call hosted Thursday by the Council on Foreign Relations in New York. “It’s an economy that’s sliding into recession.”

Premier Li Keqiang is seeking to defend a 7% economic growth goal at a time when concern over slowing demand in China is fueling volatility in global markets. The true rate of expansion “is probably something closer to 4.5% or less,” Buiter said. Li has repeatedly pledged to avoid stimulus similar to the one following the global financial crisis in 2008 that led to a surge in debt for local governments and corporations. Some economists and investors have long questioned the accuracy of China’s official growth data. When Li was party secretary of Liaoning province in 2007, he said that figures for gross domestic product were “man-made” and therefore unreliable, according to a diplomatic cable published by WikiLeaks in 2010.

“They will respond but they will respond too late to avoid a recession, which is likely to drag the global economy with it down to a global growth rate below 2% – which is in my definition a global recession,” said Buiter.

“..open capital account, independent monetary policy, and stable tightly managed exchange rate”

• China’s Ongoing FX Trilemma And Its Possible Consequences (FT)

From UBS’s Tao Wang on what, post China’s surprise revaluation, is now an oft used phrase, the impossible trinity — AKA the corner China finds itself in:

“The impossible trinity says that a country cannot simultaneously have an open capital account, independent monetary policy, and stable tightly managed exchange rate. Some academics argue that since capital controls are no longer as effective in the current day world, complete monetary policy independence is still not possible without some degree of exchange rate flexibility, even without a fully open capital account – or impossibly duality. Regardless of whether it is an impossible trinity or duality, the fact is that in recent years, as a result of substantial capital controls relaxation, China has found it increasingly difficult to manage independent monetary policy while simultaneously maintaining a fixed exchange rate.

Since last year, the PBOC has had to repeatedly inject liquidity and use the RRR to offset capital outflows – its efforts to ease monetary policy have been less effective because of FX leakages, while at the same time rate cuts are reducing arbitrage opportunities to add further downward pressures on the currency. As China’s government has announced and seems to be committed to fully opening the capital account soon, these challenges will only become greater. Therefore, it is the right thing to do to break the RMB’s dollar peg and move to materially increase its flexibility. At the moment, China’s weak domestic demand and deflationary pressures necessitate further interest rate cuts, which may further fan capital outflows and depreciation pressures.

Meanwhile, not only is the RMB’s recent effective appreciation still hurting China’s tradable goods sector, but the central bank’s defence of the exchange rate is also draining substantial domestic liquidity that necessitates constant replenishing, both of which is undermining the effectiveness of overall monetary policy easing. With a more flexible exchange rate, the RMB can be weakened by outflows and depreciation pressures without draining domestic liquidity, and domestic assets will become relatively cheaper and thus more attractive than foreign assets – which may ultimately alter market expectations to reduce capital outflows.

In addition, a weaker RMB should improve China’s current account balance to also alleviate depreciation pressures. Conversely, if China’s exchange rate is allowed to appreciate along with capital inflows and appreciation pressures, it will make domestic assets more expensive and less attractive, to ultimately worsen China’s current account balance.”

“The Chinese should have been warned, for they won accolades from Western economists for their “Goldilocks” economy.”

• China Has Exposed The Fatal Flaws In Our Liberal Economic Order (Pettifor)

How can we make sense of volatile global stock markets? Economists explained this week’s dramatic falls by pinning responsibility on China. They are at pains to assure us this is not 2008 all over again. I beg to disagree. Even though data is not reliable, it appears that China is slowing down. By 2009, the Chinese authorities were embracing the Western economic model that had just brought down much of Western capitalism. Undeterred, they launched a massive credit-fuelled investment programme. Growth soared at 10% per annum. Investment recently peaked at an extraordinary 49% of GDP. Total debt (private and public) rocketed to 250% of GDP – up 100 points since 2008, according to the IMF. Property and other asset markets boomed, as did consumption.

The Chinese should have been warned, for they won accolades from Western economists for their “Goldilocks” economy. China’s stimulus helped keep the global economy afloat in the years following. But there are economic, ecological, social and political limits to a developing country like China continuing to support richer economies. And there are limits to Beijing’s willingness to abandon control and adopt in full the Western neoliberal economic model; the Communist Party has begun intervening. It is this intervention, we are led to believe, that spooked global markets. Yet the real reason for global weakness lies elsewhere – in the Western neoliberal economic model itself, which lay behind the global financial crisis of 2007-9.

Financial and trade liberalisation, privatisation of taxpayer-financed assets, excessive private indebtedness and wage repression constituted an explosive economic formula and blew up the Western banking system. That model has not undergone even superficial change since 2009. On the contrary: economists and financiers used the “shock and awe” generated by the crisis to buttress the model. The crisis had its origins in banks suffering severe bouts of debt intoxication. Like alcohol addicts, they could not be treated effectively until admitting to the problem: the flawed liberal, financial and economic order. Yet neither the private finance sector nor central bankers and their political friends were willing to admit to the cause of the disease. Instead, central bankers rushed to offer life support in the form of QE to private banking systems in the UK, Japan and the US.

“Although I am a bear of very little brain one thing I have learned is that most investors only realise the economy is in a recession well after it has begun. ”

• Albert Edwards: “99.7% Chance We Are Now In A Bear Market” (Zero Hedge)

Over the years, SocGen’s Albert Edwards has repeatedly expressed his skepticism of both the economy and the market (the longest US equity “bull market” since 1945) both propped up by generous central banks injecting liquidity by the tens of trillions (at this point nobody really knows the number now that the ‘black box’ that is China has entered the global “plunge protection” game) and yet never did he have as “conclusive” a call as he does today. As the following note reveals, when looking at one particular indicator, Edwards is now convinced: ‘we are now in a bear market.” First, Edwards looks east, where he finds nothing short of China’s central bank succumbing to the “wealth effect” preservation pressures of its western peers:

After holding firm last weekend and resisting pressure to give the market what it wanted namely a cut in interest rates and the reserve requirement ratio – the PBoC caved in, unable to endure the riot in the equity markets. In giving the markets what they want China is indeed acting like a fully paid up member of the international financial community. I am not thinking here about freeing up their capital account and allowing the renminbi to be more market determined. I?m thinking instead of China?s replicating the failed US policies of ramping up the equity market to boost economic growth, only to then open the monetary flood gates as equity investors turn nasty.

We disagree modestly with this assessment because as we described first on Tuesday, the RRR-cut had much more to do with unlocking $100 billion in much needed funding so that China could continue to intervene in the FX market by dumping a comparable amount of US Treasurys since its August 11 devaluation, something which as we reported earlier today, China itself has also now admitted. But the reason why we do agree, is that while the RRR-cut may have had other “uses of funds”, today’s dramatic intervention by the PBOC in both the stock market, leading to a 5.5% surge in the last hour of trading, as well as a dramatic intervention in the FX market, it is quite clear that the PBOC will do everything in its power once again to prevent any market drops. Edwards, then goes on to observe something which is sure to anger the Keynesians and monetarists out there: no matter how many trillions central banks inject, they will never replace, or override, the most fundamental thing about the economy: the business cycle.

Despite deflation fears washing westward and US implied inflation expectations diving to levels not seen since the 2008 Great Recession, there remains a touching faith that the US is resilient enough to withstand further renminbi devaluation. And if it isn’t, why worry anyway, because QE4 will be around the corner. But let me be as clear as I can: the US authorities CANNOT eliminate the business cycle, however many QE helicopters they send up. The idea that developed economies will decouple from emerging market turmoil is as ridiculous as was the reverse in the first half of 2008. Remember EM and commodities had then de-coupled from the west’s woes until they too also crashed.

Which brings us to the key point – the state of the market, and why for Edwards the signal is already very clear – the bear market has arrived:

Although I am a bear of very little brain one thing I have learned is that most investors only realise the economy is in a recession well after it has begun. The same is true of an equity bear market. We need help before it is too late to react. Hence when Andrew Lapthorne shows that one of his key predictors of a bear market registers a 99.7% probability that we are already in a bear market, there might still be time to act!

Just about everyone will.

• Who Will Be the Bagholders This Time Around? (CH Smith)

Once global assets roll over for good, it’s important to recall that somebody owns these assets all the way down. These owners are called bagholders, as in “left holding the bag.” Those running the rigged casino have to select the bagholders in advance, lest some fat-cat cronies inadvertently get stuck with losses. In China, authorities picked who would be holding the bag when Chinese stocks cratered 40%: yup, the poor banana vendors, retirees, housewives and other newly minted punters who borrowed on margin to play the rigged casino. Corrupt Chinese officials, oil oligarchs and everyone else who overpaid for flats in London, Manhattan, Vancouver, Sydney, etc. will be left holding the bag when to-the-moon prices fall to Earth.

Anyone buying Neil Young’s 2-acre estate in Hawaii for $24 million will be a bagholder. (If nobody buys it at this inflated price, Neil may end up being the bagholder.) Bond funds that bought dicey emerging market debt (Mongolian bonds, anyone?) and didn’t sell at the top are bagholders. Everyone with bonds and stocks in the oil patch who didn’t sell last summer is a bagholder. Everyone holding yuan is a bagholder. Everyone who bought euro-denominated assets when the euro was 1.40 is a bagholder at euro 1.12. Everyone with 401K emerging market equities mutual funds who didn’t sell last summer is a bagholder. Everyone who reckons “buy and hold” will be the winning strategy going forward will be a bagholder.

Anyone buying anything with borrowed money is a bagholder. Leveraging up to buy risk-on assets like Mongolian bonds and homes in vancouver is brilliant in bubbles, but not so brilliant when risk-on turns to risk-off. As the asset’s value drops below the amount borrowed to buy it, the owner becomes a bagholder. Anyone betting China’s GDP is really expanding at 7% and the U.S. economy will grow by 3.7% next quarter is angling to be a bagholder.

One of many views. My own notion is that too many people believe the Fed is looking out for the US economy, whereas they really look out for banks.

• Now’s The Right Time For Yellen To Kill The ‘Greenspan Put’ (MarketWatch)

The Federal Reserve says the timing of its first interest rate hike in nine years depends on the data, but that doesn’t mean the Fed will be digging through the jobs, growth and inflation reports for the all-clear signal. Instead, the Fed will be doing what millions of people have been doing for the past couple of weeks: Watching the stock market. Many investors have assumed that the recent selloffs in markets from Shanghai to New York meant that the Fed definitely won’t pull the trigger on a rate hike at its Sept. 16-17 meeting. Many prominent talking heads – from Suze Orman to Jim Cramer – are explicitly begging the Fed to hold off on higher interest rates as a way to protect stock prices.

It seems they still fervently believe in the “Greenspan put.” They assume that the Fed will always come riding to the rescue of the markets, as Fed Chair Alan Greenspan did so many times. You can’t blame them for believing that, because from 1987 to today, the Fed has reacted to nearly every market hiccough and tantrum by flooding markets with liquidity and reassurances. They’ve given the markets rate cuts, quantitative easing and promises that easy-money policies will continue for a long time, if not forever. This “Greenspan put” means investing in the stock market is a one-way bet. On Wednesday, New York Fed President Bill Dudley seemed to close the door on a September rate hike when he said that, “at this moment,” a rate hike next month no longer seemed as “compelling” as it once did.

Traders in federal funds futures lowered the odds of an increase in September to about 24%, down from about 50% just before the global market selloff intensified last week. But Dudley didn’t take September off the table, as many people have assumed. Indeed, he explicitly said that a September rate hike “could become more compelling by the time of the meeting as we get additional information.” And what sort of additional information would make a rate hike more compelling? Dudley said the Fed is looking at more than the economic data, widening its scope to examine everything that might impact the economic outlook. They are looking at the value of the dollar, the price of commodities, the risk of contagion from Europe, from China, and from emerging markets. And, above all, the U.S. stock market.

I believe the market selloff has made a September rate hike even more compelling than it was before, because it gives Fed Chair Janet Yellen the opportunity she needs to kill the “Greenspan put” once and for all.

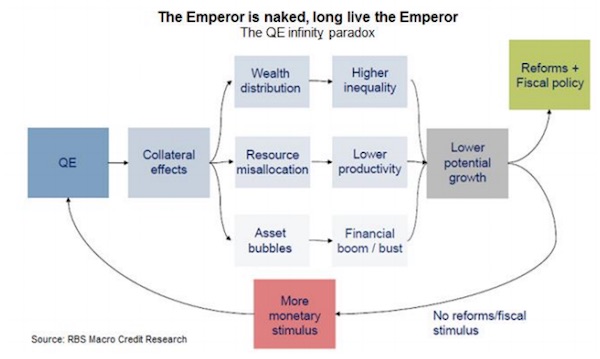

Great pic.

• The Emperor Is Naked; Long Live The Emperor (Fiscal Times)

Over at Barclays, economists Michael Gapen and Rob Martin pushed back their rate hike forecast to March 2016. They admit Fed policymakers are “market dependent” and won’t tighten policy in the maw of a stock correction, even as they see “economic activity in the U.S. as solid and justifying modest rate hikes.” Should the market turmoil continue, the rate hike could be pushed past March. Alberto Gallo, head of credit research at RBS, is more direct: “Policymakers responded to the financial crisis with easy monetary policy and low interest rates. The critics — including us — argued against ‘solving a debt crisis with more debt.’ Put differently, we said that QE was necessary, but not sufficient for a recovery. We are now coming to the moment of reckoning: central bankers look naked, and markets have nothing else to believe in.”

Gallo believes an overreliance on excess liquidity has actually hindered capital investment — as companies have focused on debt-funded share buybacks and dividend hikes instead — limiting the global economy’s potential growth rate. Now, contagion from China — lower commodity prices, lower demand, currency volatility — has revealed the structural vulnerabilities. More stimulus, in his words, “could be self-defeating without fiscal and reform support.” As for Fed hike timing, Gallo sees the odds of a September liftoff at just 30%, down from 36% last week, based on futures market pricing. December odds are at 60%. The open question is: Should the Fed delay its rate hike and the People’s Bank of China ease, will stocks actually rebound? Or has the Pavlovian reaction function been broken by a loss of confidence? We’re about to find out.

The IMF would have to do a 180 on its own sustainability assessment.

• IMF Could Contribute A Fifth To Greek Bailout, ESM’s Regling Says (Bloomberg)

The IMF will probably join Greece’s third bailout and might contribute almost a fifth to the €86 billion program, the head of Europe’s financial backstop said. Speaking to reporters in Berlin on Thursday, European Stability Mechanism Managing Director Klaus Regling said “it would make sense” for the fund to use the 16 billion euros it didn’t pay out to Greece during the second bailout, which expired at the end of June. “Up to 16 billion is something I could imagine,” Regling said. “I assume with a large probability that the IMF will contribute,” though less than the third it contributed to Greece’s bailout five years ago, he said.

Regling is expressing optimism on the IMF’s participation even after Managing Director Christine Lagarde said debt relief for cash-strapped Greece must go “well beyond what has been considered so far.” The IMF has accepted the euro-region view that Greece’s debt load as a percentage of its economy isn’t a proper debt sustainability gauge as long as bond redemptions and interest payments are largely suspended thanks to the financial support, Regling said. Greece’s gross financing need will be below 15% of GDP for a decade, he said. Maturities on outstanding Greek debt can be extended and interest rates lowered to a “certain” degree to achieve the debt easing demanded by the IMF, while a nominal haircut for public creditors is not on the agenda, Regling said. One “needn’t do a whole lot” to help Greece meet the revised debt sustainability requirement, he said.

Europe-wide will not get you anywhere.

• Yanis Varoufakis: ‘I’m Not Going To Take Part In Sad Elections’ (Reuters)

Yanis Varoufakis will not take part in “sad” elections expected next month in Greece and will instead focus on setting up a new movement to “restore democracy” across Europe, the former Greek finance minister told Reuters on Thursday. The combative, motorbike-riding academic was sacked as finance minister last month after alienating euro zone counterparts with his lecturing style and divisive words, hampering Greece’s efforts to secure a bailout from partners. The one-time political rock star has since steadily attacked the bailout programme that prime minister Alexis Tsipras subsequently signed up to and the austerity policies that go with it, rebelling against his former boss in parliament.

“I’m not going to take part in these sad elections,” Mr Varoufakis told Reuters by telephone when asked about the vote likely to be held on September 20th. Mr Tsipras’s Syriza party, which hopes to return to power with a strengthened mandate, says it will not allow Mr Varoufakis and others who voted against the bailout to run for parliament under the Syriza ticket anyway. “Not only him but other lawmakers who did not back the bailout will not be part of the ticket,” a party official said. Mr Tsipras has poured scorn on Mr Varoufakis, telling Alpha TV on Wednesday that he had realised in June that “Varoufakis was talking but nobody paid any attention to him” at the height of Greece’s negotiations with IMF and EU lenders.

“They had switched off, they didn’t listen to what he was saying,” Mr Tsipras said. “He didn’t say anything bad but he had lost his credibility among his interlocutors.” Mr Varoufakis, in turn, likened Mr Tsipras to the mythical Sisyphus condemned to push a rock uphill only to have it roll back down, telling Australia’s ABC Radio the prime minister had embarked on “pushing the same rock of austerity up the hill” against the laws of economics and ethical principles. The 54-year-old Mr Varoufakis has already dismissed speculation that he would join the far-left Popular Unity party that broke away from Syriza last week, telling ABC that he had “great sympathy” but fundamental differences with them and considered their stance “isolationist”.

Instead, he told Reuters he wanted to set up a European network aimed at restoring democracy that could eventually become a party, but at the moment was just an idea that he had seen a lot of support for. “Instead of having national parties that run on a national level it will be a European network which is active on a national level,” he said. “It’s not something immediate. It’s something slow-burning … something that gradually grows roots across Europe.”

Hunderds die every day now. Blame Brussels.

• For Those Trying to Reach Safety in Europe, Land can be as Deadly as Sea (HRW)

More gruesome details will undoubtedly emerge, but we already know enough to be horrified: Up to 50 people died in what were surely agonizing deaths, locked in a truck parked on an Austrian highway, leading to Vienna. That so many should die in a single episode, so close to a European capital where ministers are meeting to discuss migration in the Western Balkans, has made this international news. But the land route into the European Union trekked by migrants and asylum seekers has claimed thousands of victims over the years. In March, two Iraqi men died of hypothermia at the border between Bulgaria and Turkey. In April, 14 Somalis and Afghans were killed by a high-speed train in Macedonia as they walked along the tracks. Last November, a 45-day-old baby died with his father on those same tracks.

While deaths in the Mediterranean capture much of the attention, the list of those who have died of suffocation, dehydration, and exposure to the elements at land borders is unconscionably long. One count puts the overall death toll at EU borders at more than 30,000 since 2000. The smugglers directly responsible for deaths and abuse should be brought to justice. Ill-treatment by border guards and police in Macedonia and Serbia adds to the perils of the journey. But there’s lots of blame to spread around. Failed EU policies, which place an unfair burden on countries at its frontiers, and Greece’s inability to handle the numbers of migrants, have contributed to the crisis at EU borders.

Instead of erecting fences, as Hungary is, the EU should expand safe and legal alternatives for people seeking entry, especially those fleeing persecution and conflict. This means increasing refugee resettlement, facilitating access to family reunification, and developing programs for providing humanitarian visas. It also requires EU governments to meet their legal obligations to provide access to asylum and humane conditions for those already present. EU countries should step up to alleviate the humanitarian crisis in debt-stricken Greece, where 160,000 migrants have arrived since the start of the year. The umbrella group European Council on Refugees and Exiles (ECRE) has called for EU countries to relocate 70,000 asylum seekers from Greece within a year, double the insufficient relocation numbers agreed by governments for both Greece and Italy in July.

Many of those traveling along the Western Balkans route and into Austria are from Syria, Somalia, Iraq, and Afghanistan – countries experiencing war or generalized violence. Others are hoping to improve their economic prospects and the lives of their children. None of them deserve to be exploited, abused, or to die.

Home › Forums › Debt Rattle August 28 2015