DPC City Market, Kansas City, Missouri 1906

Europe and oil falling.

• Nikkei Climbs, But Shanghai Extends Fall (CNBC)

Asia markets were mostly higher on Wednesday after Wall Street surged overnight on a bounce in oil prices and positive earnings news, shrugging off the recent global rout, at least temporarily. China shares were volatile, erasing most early losses in late trade. “Swinging from depressive slumps to manic rallies, markets remain volatile,” Vishnu Varathan, an analyst at Mizuho Bank, said in a note Wednesday. China’s market is likely to remain the region’s sticky wicket for hopes the long global rout will end. The Shanghai Composite was down 0.46% after tumbling as much as 4.10% earlier. That followed the index’s worst day on Tuesday since the suspension of the circuit breaker rule in early January, closing down 6.4%, hitting its lowest level since December 2014. The Shenzhen Composite dropped 0.948% after trading down as much as 5.62% earlier in the session.

Amid concerns about slowing economic growth and depreciation of the yuan, shares on the mainland got an additional bit of bad news Wednesday: China’s industrial profits fell 4.7% on-year in December, declining for a seventh month. The Shanghai Composite is down more than 20% since its most recent high of 3,651.76 on December 22, leaving it in a “bear within a bear” market. The index is off more than 47% from its 52-week high of 5,166.35, set June 2015. “Chinese markets look like they will continue to sell off until their last day of trading before Chinese New Year on February 5,” Angus Nicholson at spreadbettor IG said in a note Wednesday. “There is a good chance that Chinese equities may find their cyclical bottom in the next week and half if the current pace of selloff continues.” He expects the Shanghai Composite might eventually bottom around the 2300-2400 level.

Self-fulfilling.

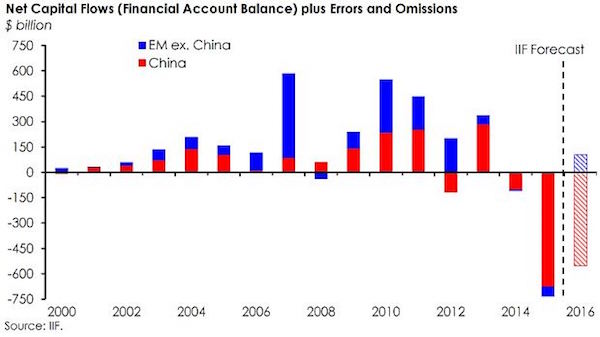

• Why China’s Capital Flight Carnage Will Continue (Telegraph)

Money has poured out of emerging market economies as fears that they will disappoint have continued to grow. This capital flight has put extreme pressure on emerging market currencies, driving speculation that more of these economies will have to capitulate, allowing marked devaluations of their currencies, or enforcing capital controls. $735bn was pulled out of emerging markets last year alone, according to the Institute of International Finance (IIF), up from $111bn in the preceding year. “The bulk of these outflows relate to China,” said the IIF, adding that money managers were taking out their money “in the face of concerns about a weakening currency”. Total capital outflows from the People’s Republic were thought to stand at $676bn last year.

The IIF said that it anticipated that capital would continue to leave emerging markets this year, but at a “more moderate pace”. Since Beijing’s botched readjustment of the yuan last August, investors have been anxious that a larger currency depreciation is on the way. As a result, they have taken their money out of the country in anticipation, increasing the demand for other currencies, at the expense of renminbi demand. The People’s Bank of China (PBoC) has had to intervene heavily, burning through reserves to keep the currency strong. “The recent flood of capital leaving China has been driven primarily by increased scepticism that the PBoC will hold to its pledge to keep the renminbi stable,” said Mark Williams at Capital Economics. Capital Economics estimated that outflows stood at $140bn in December alone, as firms may reassessing their expansion plans, and investors worry about the possibility of a further downturn.

“The PBoC has enough reserves to keep selling at December’s rate until mid-2018 but it would presumably throw in the towel before they were all exhausted,” said Mr Williams. “If investors think the PBoC may shift its stance in future, they have an incentive to sell renminbi assets now even if no policy change is currently being considered.” While the movements in Chinese stock markets are far removed from the real economy, and that economy does not seem to be melting down, high levels of capital flight could be toxic for the country. Helene Rey, an economics professor at the London Business School, told The Telegraph that there is a risk that investors overreact to recent moves, and negativity about China “becomes self-fulfilling”. “We know China has a lot of reserves, but when capital flows flow out at a quick rate this might have a lot of psychological consequences.” She suggested that a significant depreciation of China’s yuan would “probably not be good for the stability of a lot of emerging markets”.

Claudio Piron, a Bank of America Merrill Lynch strategist, said that China’s current problems were the result of its struggles with the impossible trinity, or “trilemma”. Policymakers cannot control capital flows, monetary policy and the currency all at the same time. Mr Piron said that the outflows have captured the “conflict between easing monetary conditions on one hand and contradictory attempts at foreign exchange intervention to target the yuan’s strength against the dollar on the other”. The policy uncertainty causing the outflows “may only be resolved once the market has regained confidence in China’s ability to restore a robust recovery and China’s monetary has come to an end”. Mr Piron suggested this would come in the final quarter of 2016 at the earliest.

In China, a bank default is a government default.

• A China Bank Contagion Could Blow Up Global Markets (CNBC)

If the dark predictions are going to come true — that the market turmoil out of China will lead to “another 2008” — it will have to be a very different kind of crisis than the original. Six months after sell-offs in Shanghai began to reverberate through markets worldwide, bond-rating agencies continue to rate Chinese banks’ credit as investment grade, suggesting that if China does lead the world into recession, it will be a different affair than the sudden, sharp downturn catalyzed by the collapse of Lehman Bros. A measure of default risk used by Moody’s Investors Service puts the risk of any of the Big Four Chinese banks — Bank of China, the Industrial and Commercial Bank of China, China Construction Bank and Agricultural Bank of China — defaulting in the next year at no more than 1.5%, and for some as little as 0.5%, said Samuel Malone at Moody’s Analytics.

Even with nearly $11 trillion of assets and loans that reach into all sectors of China’s $10.3 trillion economy, for now, experts see little likelihood the banks themselves will be a problem; China’s largest banks are all controlled by a government that has the determination and resources to prop them up if necessary. And their ties to U.S. institutions are narrow enough that bond-rating agencies don’t foresee anything like the financial contagion of 2008, when liquidity problems quickly spread from bank to bank and nation to nation as the extent of the mortgage crisis became clear.

“Declaring war on China’s currency? Ha ha”

• China Accuses George Soros Of ‘Declaring War’ On Yuan (AFP)

Chinese state media has stepped up a salvo of biting commentaries against George Soros and other currency traders as the yuan comes under pressure, with the billionaire investor accused of “declaring war” on the unit. At the annual World Economic Forum in Davos last week, Soros told Bloomberg TV that the world’s second-largest economy – where growth has already slowed to a 25-year low according to official figures – was heading for more troubles. “A hard landing is practically unavoidable,” he said. Soros – whose enormous trades are still blamed in some countries for contributing to the Asian financial crisis of 1997 – pointed to deflation and excessive debt as reasons for China’s slowdown.

The normally stable yuan, whose value is closely controlled by Beijing, has come under pressure in recent weeks and months in overseas markets and from capital outflows. Authorities have spent hundreds of billions of dollars to defend it. China’s official Xinhua news agency on Wednesday said that Soros had predicted economic troubles for China “several times in the past”. “Either the short-sellers haven’t done their homework or … they are intentionally trying to create panic to snap profits,” it said. An English-language op-ed in the nationalistic Global Times newspaper blamed “westerners” for not “accepting responsibility for the mess” in the world economy. The comments came after the overseas edition of the People’s Daily, the official mouthpiece of the Communist party, published a front-page article Tuesday titled “Declaring war on China’s currency? Ha ha” that was widely shared on Chinese social media.

Soros “publicly ‘declared war’ on China”, the paper said, citing the 85-year-old as saying that he had taken positions against Asian currencies. But some readers questioned whether the official rhetoric could fuel Chinese investors’ fears. “They say a lot of loud slogans, but do official media even know that Chinese investors are in hell?” said one poster on social media network Weibo. “I’m afraid that Chinese investors will die in a stampede before Soros even shows his hand.” In the 1990s Soros led speculators in bets against the Bank of England, which unsuccessfully sought to defend the pound’s exchange rate peg. “The Chinese left it too long” to change their growth model from dependence on exports to a consumer-led one, Soros said, even though Beijing had “greater latitude” than others to manage such a transition because of its currency reserves, which stand at over US$3tn.

Done just hours after he says all’s fine in the economy. Beijing must not want to restore confidence.

• Head Of China’s Statistics Bureau Investigated For Corruption (AFP)

The head of China’s statistics bureau is being investigated for corruption, the country’s watchdog said on Tuesday. “Wang Baoan is suspected of severe disciplinary violations, he is currently under investigation,” the Central Commission for Discipline Inspection said in a one-line statement on its website, using a phrase that is usually used to refer to corruption. The announcement came just hours after Wang appeared at a media briefing in Beijing on China’s economy in 2015. Last week the National Bureau of Statistics released data that showed China’s economy grew at the slowest pace in 25 years. Wang reiterated on Tuesday that the country’s GDP calculations were reliable, Chinese media reported, despite widespread criticism of the data.

Questions have repeatedly been raised about the accuracy of official Chinese economic statistics, which critics say can be subject to political manipulation. Wang was appointed head of the National Bureau of Statistics in April 2015. He previously spent about 17 years in various positions in the finance ministry. Official allegations of corruption against high-level politicians are generally followed by an internal investigation by China’s Communist party, and sometimes lead to criminal proceedings which often end in conviction. Internal investigations into high-level party officials operate without judicial oversight. Once announced, they are likely to lead to a sacking followed by criminal prosecution and a jail sentence.

They knew that in advance.

• Inquiry in China Adds to Doubt Over Reliability of Economic Data (NY Times)

The veracity of China’s economic data has been increasingly questioned as the slowing pace of the country’s growth has startled the world. And a new investigation into the official who oversees the numbers is unlikely to inspire confidence. The Communist Party’s anticorruption commission announced late Tuesday that it was looking into the head of the country’s statistics agency over what it called “serious violations.” It is unclear whether the investigation into the agency’s head, Wang Baoan, who became the director of the National Bureau of Statistics of China last April, is related to his current role or to his previous one as vice minister of finance. The commission did not release any further details about the inquiry.

China’s shrinking manufacturing sector and falling stock market have unnerved global investors. Any further doubt about its economic figures could paint an even darker picture of the health of the economy, adding to the pain in the markets. Stocks in Shanghai, which closed before the announcement, were off 6.4% on Tuesday. The statistics bureau has a variety of responsibilities that are hard to balance even in the best of times. The bureau is supposed to provide China’s leaders with an unvarnished assessment of the country’s economic strengths and weaknesses, even while reassuring the public about growth and maintaining consumer confidence. It is also supposed to release enough detailed and accurate information for investors and corporate leaders to make sound decisions about economic and financial prospects.

Few doubt that China has grown enormously over the past three decades. But economists, bankers and analysts who study the numbers believe that the bureau smooths data, underestimating growth during economic booms and overestimating it during downturns. Many economists are worried that China’s economy is not expanding anywhere close to the nearly 7% annual pace that bureau data still show. By some estimates, the pace is half of the official figures. Those skeptical about the data point, in part, to the underlying numbers. For example, electricity consumption, long a barometer of economic health and of the veracity of economic statistics, was nearly unchanged last year instead of rising in line with growth in China’s GDP. Some have cited the lack of correlation as a sign of possible fudging in the country’s economic statistics, while optimists have said that the figures may show how China is shifting away from energy-intensive manufacturing.

State news media reported last month that several officials in northeastern China had admitted to inflating investment figures and other data in previous years. Such moves, the reports indicated, helped explain steep drops in reported data from the region last year. Still, the bureau has consistently and repeatedly defended its statistics, contending that critics do not adequately understand the data or the Chinese economy. And the market impact of the investigation could be limited by the fact that many were already wondering about China’s data. “The international credibility of China’s GDP figures is anyway very low, so this probably is not a severe blow,” said Diana Choyleva at Lombard Street Research

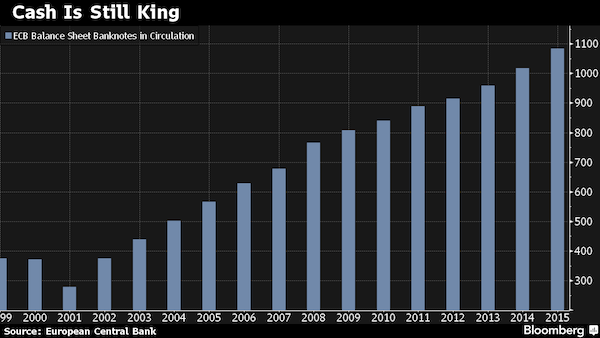

What happened to the war on cash?

• Cash Is King as Europe Adapts to Negative Interest Rates (BBG)

Europe’s ATMs worked overtime in 2015. A record €1.08 trillion ($1.17 trillion) of banknotes were in circulation, almost double the value 10 years ago, according to data compiled by the ECB. That’s a counterargument to some bankers who say that electronic forms of cash will replace paper money sooner rather than later. The value of banknotes in circulation rose 6.5% last year, the most since 2008. There are financial reasons – including negative rates on deposits – but part of the increase could be related to the influx of refugees, who don’t have bank accounts.

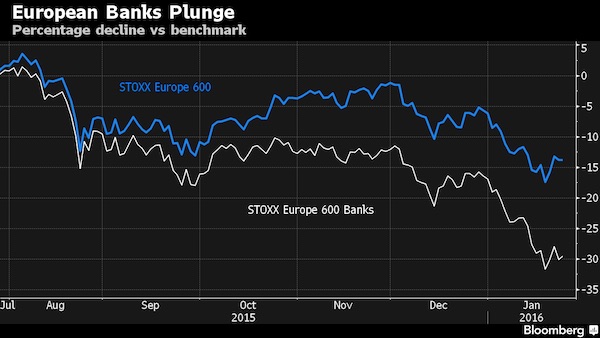

“Deutsche Bank and Standard Chartered are each down more than 40% since July.”

• Europe Bank Rout Erases $434 Billion In 6 Months (BBG)

The plunge in European bank stocks over the past six months has wiped out about €400 billion ($434 billion) in market value, an amount that’s more than twice the annual economic output of Greece at current prices. The STOXX Europe 600 Banks Index, grouping 46 lenders, dropped twice as much as the region’s benchmark share index since late July. Banking stocks have fallen 14% in January alone, heading for their worst monthly performance since the depths of Europe’s sovereign-debt crisis in 2011. Deutsche Bank and Standard Chartered are each down more than 40% since July.

“..after long absences, earthquakes come in quick succession. ”

• The Market’s Troubling Message (Ashoka Mody)

Amid one of the worst market routs on record, a chorus of reassuring economic commentators insists that global fundamentals are sound and investors are overreacting, behaving like a panicked herd. Don’t be so sure. Consider how wrong economists have been about the effects of the 2008 financial debacle. In April 2010, the IMF declared the crisis over and projected annualized global growth of 4.6% by 2015. By April 2015, the forecast had declined to 3.4%. When the weak last quarter’s results are released, the reality will probably be 3% or less. Economists are used to linear models, in which changes follow a relatively gradual and predictable path. But thanks in part to the political and economic shocks of recent years, we live in a highly non-linear world. The late Danish physicist Per Bak explained that after long absences, earthquakes come in quick succession.

A breached fault line sends shock waves that weaken other fault lines, spreading the vulnerabilities. The subprime crisis of 2007 breached the initial fault line. It damaged U.S. and European banks that had indulged in its excesses. The Americans responded and controlled the damage. Euro-area authorities did not, making them even more susceptible to the Greek earthquake that hit in late-2009. Europeans kept building temporary shelters as the banking and sovereign debt crisis gathered force, never constructing anything that would hold as new fault lines opened. Enter China, which briefly held the world economy together amidst the worst of the crisis. Just in 2009, the Chinese pumped in credit equal to 30% of gross domestic product, boosting demand for global commodities and equipment.

Germans benefited in particular from the demand for cars, machine tools, and high-speed rails. This activated supply chains throughout Europe. But China is becoming more a source of risk than resilience. The number to look at is not Chinese GDP, which is almost certainly a political statement. The country’s imports have collapsed. This is troubling because it is the epicenter of global trade. Shockwaves from China can test all the global fault lines, making it a potent source of financial turbulence. Only China can undo its excesses. Its vast industrial overcapacity and ghost real estate developments must be wound down. As that happens, large parts of the financial system will be knocked down. The resulting losses will need to be distributed through a fierce political process. Even if the country’s governance structure can adapt, the required deep-rooted change could cause China’s slowdown to persist for years.

The last gasps of the EU.

• EU Botched Billion Euro Bail-Outs During Financial Crisis (Telegraph)

The European Commission mishandled government bail-outs in the wake of the financial crisis, imposing harsher conditions on member states as contagion spread across the continent, the EU’s Court of Auditors has found. In the first major assessment of the Commission’s role in “Troika” of international creditors, the ECA said Brussels was unprepared for Europe’s spiralling debt crisis as it failed to spot dangerous deficit levels in member states. The spending watchdog looked at five bail-outs from 2009 to 2011. Auditors found the Commission escalated its austerity demands as the financial crisis spread to the single currency’s periphery. Portugal was required to comply with nearly 400 conditions as part of its €78bn rescue programme in 2011, while Hungary – which was bailed-out in 2008 – was only asked to adhere to a list of only 60 demands.

“Some countries’ deficit targets were relaxed more than the economic situation would appear to justify,” said the auditors. “Countries that needed more reforms in a given field were asked to comply with fewer conditions than better-performing countries.” Greece – the eurozone’s biggest recipient of rescue cash – was not part of the audit and will be subject to its own bail-out review. The findings seem to vindicate initial fears that the EU lacked the expertise to manage a crisis which bought Europe to its knees after 2009. German chancellor Angela Merkel pushed hard for the IMF to be involved in the financial rescues of Ireland, Portugal and Greece, in a bid to enhance the credibility of the rescue programmes. Auditors said the Commission failed to spot dangerous deficit levels building up in member states before the crisis, which meant “it was not prepared for the first requests for financial assistance” when the signs of financial stress emerged.

Other shortcomings included the use of basic and “cumbersome” spreadsheets to forecast economic performance and missing documentation, which have yet to be found by authorities. “It is imperative that we learn from the mistakes which were made” said Baudilio Tomé Muguruza of the European Court of Auditors. Criticism of the Commission comes after the former president of ECB was hauled before Ireland’s parliament to explain his institution’s actions during the country’s 2010 rescue. The ECB, which formed part of the Troika along with the Commission and IMF, has been accused of forcing Dublin to assume the vast liabilities of Ireland’s failing banks – protecting senior bonholders from taking losses.

Obvious.

• World’s Biggest Wealth Fund Speaks Out on Missing Liquidity at Banks (BBG)

As some of the world’s best-known investment banks blame tougher capital rules for contributing to the lack of liquidity in financial markets, the world’s biggest sovereign wealth fund has a different take. The argument is “an excuse for something else,” Oeyvind Schanke, chief investment officer of asset strategies at Norway’s $790 billion fund, said in an interview in Oslo on Tuesday. One week after bank executives met in Davos, Switzerland, where they spent some time discussing the fallout of stricter financial requirements, Norway’s wealth fund is questioning a tendency to blame regulators. “New regulations have reduced volume on a normal day because you don’t have that type of market-making activity from the investment banks and other large players,” Schanke said.

“But in times of big movements they wouldn’t be there anyway. 2008 is a perfect example. You didn’t have any tough regulation in 2008, but somehow the fixed-income market froze up – which you would have expected because this type of activity is to facilitate normal trading days.” “Obviously they are used to making money on this activity and now they can’t make money anymore,” he said. “They’re trying to find reasons for what’s going on.” Concerns that markets face a liquidity crunch are growing as the world’s biggest investment banks retreat from capital-intensive fixed income, currency and commodities trading to meet tougher regulatory demands. Liquidity has been affected by banks committing less capital. But the same regulations that are contributing to that have made the world of finance much safer, according to Schanke. “You can’t have it all.”

Now bubble to pop.

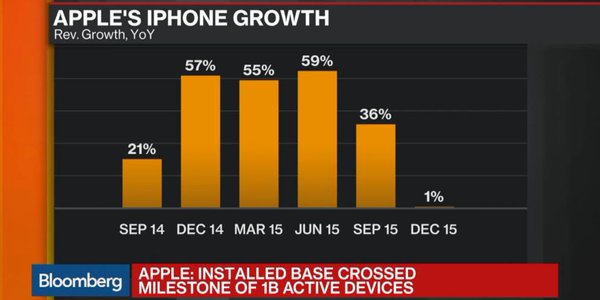

• Apple Reaches Peak iPhone, So What Now? (MW)

Apple confirmed the worst fears of many investors Tuesday: The company has hit peak iPhone. As many on Wall Street had predicted, Tuesday’s earnings report showed that Apple revenue growth has slowed, with sales increasing less than 2% year-over-year in the all-important holiday quarter. The iPhone grew by only 0.4% year-over year, and Chief Executive Tim Cook admitted smartphone sales are likely to decline for the first time in the current quarter. Apple depends on sales of the iPhone for the bulk of its revenue, including $51.6 billion of its $75.9 billion in holiday-quarter sales. As iPhone sales have continued to grow since its introduction in 2007, Apple has become the most valuable company in the world, but a slowdown likely signals Apple’s transition from a high-growth tech stock to a value stock.

Cook presented an outlook that shows total revenue will fall along with iPhone sales in the current quarter, citing economic ”malaise in virtually every country in the world” as well as currency headwinds. Apple’s outlook for its fiscal second quarter revenue — ranging from $50 billion to $53 billion — represents a potential revenue decline of 8.6% to 13.8% from $58 billion in the fiscal second quarter of 2015. Apple shares dropped more than 2.5% in late trading. Apple’s other businesses have not stepped up to augment the iPhone. In its fiscal first quarter, Apple saw a tiny uptick in iPhone revenue but declines in its other major hardware products, as iPad revenue fell 21% and Mac revenue fell 3%.

Apple introduced its first new hardware product since the iPad in 2015, the Apple Watch, but it still offers a small, unknown sales total for the company. Revenue for other products — which includes the Apple Watch along with the Apple TV, Beats headphones, the iPod and accessories — jumped 62% year-over-year, but still brought in less than $4.4 billion. Those numbers won’t move the needle when total revenues topped $75 billion.

Maybe what you experienced before was extreme, and this is normal?!

• Apple: ‘Extreme Conditions Unlike Anything We’ve Experienced Before'(BBG)

What’s keeping the CEO of a company that just reported the most profitable quarter in history up at night? For Apple’s Tim Cook, it’s the “economic challenges all over the world.” “This is a huge accomplishment for our company especially given the turbulent world around us,” said Cook, immediately after running through the company’s quarterly financial highlights on a conference call. Ever since the surprise devaluation of the Chinese yuan in August, the potential for a hard landing in the world’s second-largest economy has been front-of-mind for investors. Cook did nothing to assuage those concerns. While pointing out that Apple had been performing quite well in China last summer—unlike some other firms—he suggested that the forward outlook was not nearly as bright.

“Notwithstanding these record results, we began to see some signs of economic softness in Greater China earlier this month, most notably in Hong Kong,” he said. Meanwhile, other major markets for Apple, including Brazil, Russia, Japan, Canada, southeast Asia, Turkey, and the eurozone have been roiled by slow economic growth, the downturn in commodities prices, and weakening currencies. “Our results are particularly impressive given the challenging global macroeconomic environment,” said Cook. “We’re seeing extreme conditions unlike anything we’ve experienced before just about everywhere we look.”

For Apple, which generates roughly two-thirds of its revenues outside the U.S., this is no small matter. The lofty U.S. greenback crimped revenues received abroad, with Cook specifically citing the adverse effect of weakness in the British pound, euro, Canadian dollar, Aussie dollar, Mexican peso, Turkish lira, Brazilian real, and Russian ruble. According to Cook, these foreign exchange fluctuations shaved 15% off revenues the tech powerhouse earned abroad relative to its fiscal fourth quarter.

Yeah, sure, AIG is a going concern, yada yada. Thing is, what’s the bill, and who’s paying?

• AIG To Return $25 Billion After Activist Siege (FT)

American International Group’s chief executive has pledged to return $25bn to shareholders as he defies demands from activist investors Carl Icahn and John Paulson to break up the world’s fourth most valuable insurance company. Peter Hancock on Tuesday unveiled a streamlining plan including a listing of AIG’s mortgage insurance arm, accelerated cost cutting and a separation of legacy assets in an effort to rally support from other shareholders. He said that AIG, which has already scaled back dramatically since the financial crisis and its $185bn government bailout, would be willing to make further disposals if they made financial sense — but argued that there was no case at present to shed core divisions.

“We’re absolutely open to additional divestitures beyond what we’ve talked about — even of our largest units — but you don’t make a decision of that scale without thinking very hard about the impact,” he said. Management’s refusal to acquiesce to the activists’ break-up call sets the stage for a full-scale proxy war. Mr Icahn has already said that he hopes directors “will take matters into its own hands if management still resists drastic change”. The billionaire, who has received support from Mr Paulson, believes that AIG should split apart its life and general insurance arms, highlighting that Washington plans to subject the group to tougher regulations as a “systemically important” financial institution or Sifi. Mr Hancock rejected the Sifi argument as a “complete red herring”.

“It’s maybe issue number 15 on the list,” he said. “Now is not the time to be short-sighted and simply react to the demands of those who challenge us.” Shares in AIG, whose discount to book value has made it a target for activists, rose 1.3% to $56.08 after it made its long-awaited strategic update. The $25bn of capital to be distributed via dividends and stock buybacks over the next two years is equivalent to more than a third of AIG’s $68bn market capitalisation. The group returned $12bn last year. Mr Hancock’s initiatives include a stock market launch this year of AIG’s mortgage insurance arm, United Guaranty. The group plans to float a 20% stake as a “first step towards a full separation”. The division as a whole is estimated to be worth about $6bn.

As I said many times before.

• The Black Hole of Deflation Is Swallowing the Entire World (GWB)

Many high-powered people and institutions say that deflation is threatening much of the world’s economy … China may export deflation to the rest of the world. Japan is mired in deflation. Economists are afraid that deflation will hit Hong Kong. The Telegraph reported last week: RBS has advised clients to brace for a “cataclysmic year” and a global deflationary crisis, warning that major stock markets could fall by a fifth and oil may plummet to $16 a barrel. Andrew Roberts, the bank’s research chief for European economics and rates, said that global trade and loans are contracting, a nasty cocktail for corporate balance sheets and equity earnings.

The Independent notes:”Lower oil prices could push leading economies into deflation. Just look at the latest inflation rates – calculated before oil fell below $30 a barrel. In the UK and France, inflation is running at an almost invisible 0.2% per annum; Germany is at 0.3% and the US at 0.5%. Almost certainly these annual rates will soon fall below zero and so, at the very least, we shall be experiencing ‘technical’ deflation. Technical deflation is a short period of gently falling prices that does no harm. The real thing works like a doomsday machine and engenders a downward spiral that is difficult to stop and brings about a 1930s style slump. Referring to the risk of deflation, two American central bankers indicated their worries last week. James Bullard, the head of the St Louis Federal Reserve, said falling inflation expectations were “worrisome”, while Charles Evans of the Chicago Fed, said the situation was “troubling”.

Deflation will likely nail Europe: “Research Team at TDS suggests that the euro area looks set to endure five consecutive months of deflation, starting in February. “The further collapse in oil prices and what is likely spillover into core prices means the ECB’s 2016 inflation tracking is likely to be almost a full percentage point below their forecast of just six weeks ago.” (Indeed, many say that Europe is stuck in a depression.) The U.S. might seem better, but a top analyst said last year: “Core inflation in the US would be just as low as in the Eurozone if measured on the same basis”.

Funny tragedy.

• The Future is Blivets (Dmitry Orlov)

If you have been paying attention, you may have noticed that the global financial markets are currently in meltdown mode. Apparently, the world has hit diminishing returns on making stuff. There is simply too much of everything, be it oil wells, container ships, skyscrapers, cars or houses. Because of this, the world has also hit diminishing returns on borrowing money to build and sell more stuff, because the stuff we build doesn’t sell. And because it doesn’t sell, the price of stuff that’s already been made keeps going down, lowering its value as loan collateral and making the problem worse.

One solution that’s been proposed is to convert from a products economy to a services economy. For instance, instead of making widgets, everybody gives each other backrubs. This works great in theory. The backrub industry doesn’t generate an ever-expanding inventory of backrubs that then have to be unloaded. But there are some problems with this plan. The first problem is that too few people have enough money saved up to spend on backrubs, so they would have to get the backrubs on credit. Another problem is that, unlike a widget, a backrub is not a productive asset, and doesn’t help you pay off the money you had to borrow to pay for the backrub. Lastly, a backrub, once you have received it, isn’t worth very much. You can’t auction it off, and you can’t use it as collateral for a loan.

These are big problems, and one proposed solution is to create good, well-paying jobs that put money in people’s pockets—money that they can then spent on backrubs. This is best done by investing in productivity improvements: send people to school, invest in high tech and so on. It’s an intuitively obvious idea: productive workers are easier to employ than unproductive workers, because the stuff they make ends up cheaper, and people can afford to buy more of it. Whether they do buy more of it is debatable, especially if there is more than enough of it already and nobody has any extra money saved. Still, the theory makes sense.

But this theory doesn’t seem to be working all that well: no matter how much money we put into automation—robotic assembly lines, internet-based virtualization, what have you—the number of unemployed workers isn’t going down at all. And it’s even worse with driverless cars. In theory, they are great: if the driver doesn’t have to do the driving, then she can spend the time giving her passengers backrubs. But no matter how much money we throw at driverless cars, the number of unemplyed drivers, or unemployed massage therapists, isn’t going down.

The USA: “..a shameless land where anything goes and nothing matters.”

• The Agonies of Sensible People (Jim Kunstler)

I think it is fair to say that Michael Bloomberg’s success as the three-term mayor of New York City (2002 – 2013) was due almost completely to the financialization of the economy. A Niagara of money flowed into the city as banking ballooned from 5% to 40% of the US economy. As all the formerly skeezy neighborhoods of New York — the Bowery, the Meatpacking District, etc —got buffed up, the desolation in places like Utica, Dayton, Gary, and Memphis got worse. You might say New York City benefited hugely from all the assets stripped out of the flyover states. All of which is to say that that recent revival of New York City was not necessarily due to Michael Bloomberg’s genius. He presided over a very special moment in history when money was flowing in a particular way, and he went with flow.

For all that, it seems likely that he was also an able administrator as this occurred. A lot of out-front elements of city life improved visibly while he was around. Crime went down, the subways ran better, public spaces were improved. What would he be able to do in the compressive deflationary depression that I call the long emergency? Could he restore faith in authority? Could he comfort a battered public on the airwaves? Could he begin the awful task of politically deconstructing the matrix of rackets that has made it impossible for this country to move where history is taking us (smaller, finer, more local)?

Finally, on top of his Wall Street connection, Bloomberg is Jewish. (As I am.) Is the country now crazed enough to see the emergence of a Jewish Wall Streeter as the incarnation of all their hobgoblin-infested nightmares? Very possibly so, since the old left wing Progressives have adopted the Palestinians as their new pet oppressed minority du jour and have been inveighing against Israel incessantly. Well, that would be a darn shame. But that’s what you might get in a shameless land where anything goes and nothing matters. For now, anyway, the real disrupter is turning out to be Michael Bloomberg. Finally a serious man enters the stage.

There’s going to be a lot of empty offices in Brussels soon.

• Clock Ticks Down On EU Passport Free Travel Dream (AP)

Passport-free travel and hassle-free business in Europe has never been in more danger. With more than 1 million people streaming into the EU hoping for sanctuary or jobs, nations have erected fences, deployed troops and tightened border controls. “What we have worked for, for so many years, we are seeing it crumbling now in front of us,” Roberta Metsola, a leading EU lawmaker on migration, told AP on Tuesday. As draconian as they might seem, most attempts to stem the migrant flow have been within the letter, if not the spirit, of the rules governing the European travel haven known as the Schengen area, a jewel in the EUs integration crown But as of mid-May, the EU is in uncharted waters. The legal options for countries like Germany, Austria and Sweden to impose ID checks on everyone who enters, including Europeans, begin to run out.

“Our citizens have a right to feel safe,” Metsola said. “If that means that we will need to keep stock of who is crossing our borders for a specific amount of time, then we will have to do it.” The German government has signaled it’s unlikely to ease border controls on May 13, when its temporary border measures legally expire. If no other mechanism is in place by then, the Schengen rule book could effectively be suspended. Most EU nations blame Greece for this. [..] Aid groups estimate that Greece has shelter for barely 10,000 people; a little over one% of those who need it. The Greek coastguard is totally overwhelmed. Managing the country’s vast maritime border would challenge even an experienced government with a fully equipped public service. Greece, at the moment, is also consumed with a crippling economic crisis. But, Metsola said, “there is a lack of knowledge as to who is coming in and who is going out, and that automatically increases fear and increases the security concerns.

It will get much crazier than this yet.

• Danish Parliament Approves Plan To Seize Assets From Refugees (Guardian)

European states have reacted in some of the most drastic ways yet to the continent’s biggest migration crisis since the second world war, with Denmark enacting a law that allows police to seize refugees’ assets. The vote in the Danish parliament on Tuesday, which followed similar moves in Switzerland and southern Germany, came as central European leaders amplified calls to seal the borders of the Balkans, a move that would risk trapping thousands of asylum seekers in Greece. Under the new Danish law, police will be allowed to search asylum seekers on arrival in the country and confiscate any non-essential items worth more than 10,000 kroner (£1,000) that have no sentimental value to their owner.

The centre-right government said the procedure is intended to cover the cost of each asylum seeker’s treatment by the state, and mimics the handling of Danish citizens on welfare. Elsewhere in Europe, the Czech and Slovakian prime ministers condemned Greece’s inability to prevent hundreds of thousands of refugees from moving onwards to northern European countries. They jointly called for increased border protection to block the passage of refugees from Greece, a day after EU interior ministers said they were willing to consider the suspension of the Schengen agreement that allows free passage between most EU countries. Robert Fico, the Slovakian prime minister, said: “There must be a backup plan, regardless of whether Greece stays in Schengen. We must find an effective border protection.”

The idea outraged the Greek government, which must now consider the possibility of hundreds of thousands of refugees being unable to leave Greece, which is struggling with high unemployment and economic strife. Nikos Xydakis, Greece’s alternate foreign minister for EU affairs, called the idea “hysterical” and warned that it could lead to the fragmentation of Europe. “If every country raises a fence, we return to the cold war period and the iron curtain. This isn’t EU integration – this is EU fragmentation.” The Greek government faces calls to take tougher action to block the passage of the thousands of refugees arriving in Greece by boat every day, but Xydakis said the only way of stopping them would be to shoot them – an option that Greece was not willing to take, even if it meant being fenced in.

“If Europe is to put Greece in a deep humanitarian crisis, let’s see it [happen],” he said in an interview with the Guardian on Tuesday. “We are in the sixth year of a depression and [have] unemployment of 25% … But if our colleagues and partners in the EU think that we have to let people drown or sink their boats, we can’t do that. Maybe we will suffer, but we will manage.”

How about this for crazy?

• Belgium Wants Camp for 300,000 Refugees in Athens (DM)

Belgium has called for vast refugee camps holding up to 300,000 refugees to be built in Greece in a desperate attempt to stem the flow of migrants from Syria and other nations outside Europe. At an emergency summit of European leaders yesterday, Belgian migration minister Theo Francken raised the spectre of setting up ‘closed facilities’ in Greece to be operated by the EU. He said that the Greeks ‘now need to bear the consequences’ of being too weak to guard their own borders and called for Athens to face an EU ‘sanction mechanism’ under which the rising number of refugees entering the country would be forced to stay there.

Home › Forums › Debt Rattle January 27 2016